Ethiopia Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

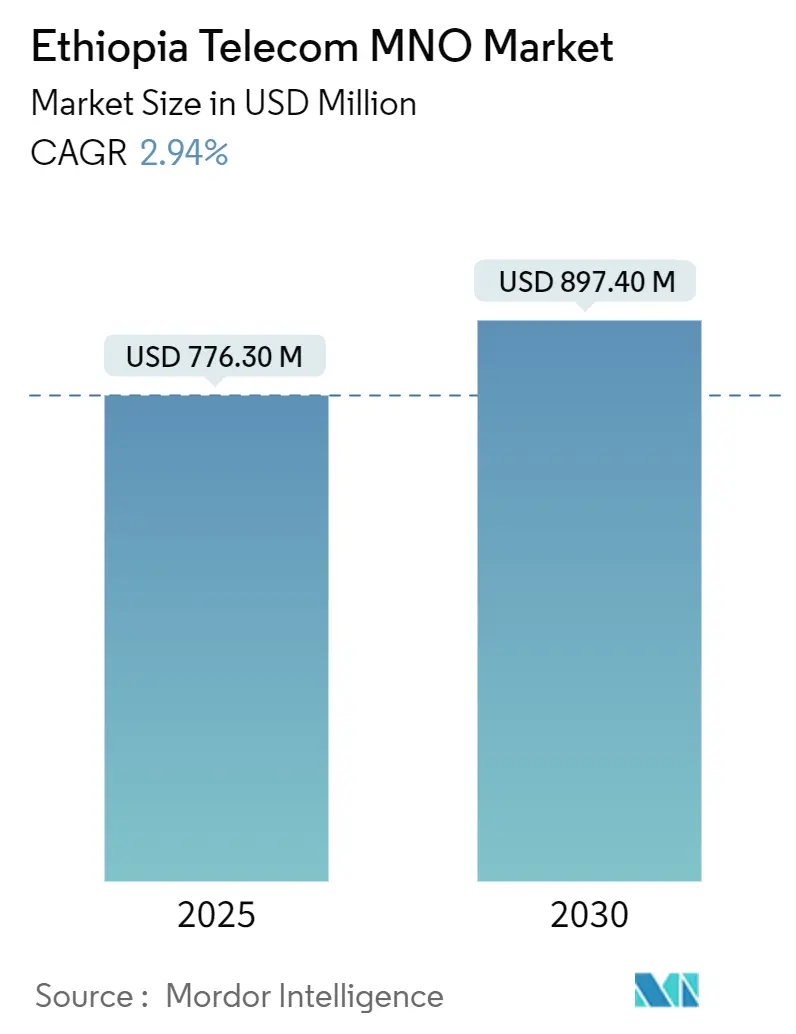

| Market Size (2025) | USD 776.30 Million |

| Market Size (2030) | USD 897.40 Million |

| Growth Rate (2025 - 2030) | 2.94% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ethiopia Telecom MNO Market Analysis by Mordor Intelligence

The Ethiopia Telecom MNO Market size is estimated at USD 776.30 million in 2025, and is expected to reach USD 897.40 million by 2030, at a CAGR of 2.94% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 86.20 million subscribers in 2025 to 100.90 million subscribers by 2030, at a CAGR of 3.20% during the forecast period (2025-2030).

Transition from a long-standing monopoly toward a regulated duopoly underpins this measured expansion, with liberalization, youth-led data demand, and an ambitious national digitization agenda balancing structural headwinds such as foreign-exchange scarcity and power-grid instability. Competitive price cuts of up to 70% in mobile data tariffs since 2017, accelerated 4G roll-outs, and early 5G pilots have widened access, while mobile-money platforms are raising average revenue per user (ARPU). Foreign-direct-investment inflows linked to Safaricom Ethiopia’s USD 1.6 billion license commitment and the government’s Digital Ethiopia 2025 targets continue to stimulate infrastructure build-outs even as operators navigate capital-intensive rural coverage obligations.

Key Report Takeaways

- By service type, data and internet services led with 46.89% revenue share in 2024; IoT and M2M services is expected to grow at 2.40% CAGR through 2030.

- By end-user, consumer lines held 68.19% of the Ethiopia telecom MNO market share in 2024, while enterprise connections expand at a 3.26% CAGR to 2030.

Ethiopia Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Liberalization and Entry of Safaricom Ethiopia | +0.8% | National, with early gains in Addis Ababa, Dire Dawa, Hawassa | Short term (≤ 2 years) |

| Government "Digital Ethiopia 2025" Broadband Push | +0.6% | National, prioritizing rural and underserved areas | Medium term (2-4 years) |

| Rising Smartphone Adoption among Youth | +0.4% | Urban centers expanding to secondary cities | Medium term (2-4 years) |

| Mobile-Money–Led ARPU Uplift | +0.3% | National, with higher adoption in urban areas | Short term (≤ 2 years) |

| LEO-Satellite Backhaul Enabling Rural Coverage | +0.2% | Rural and remote regions | Long term (≥ 4 years) |

| Solar-Powered Tower Incentives Reducing Opex | +0.1% | Rural areas with unreliable grid connectivity | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Liberalization and Entry of Safaricom Ethiopia

Safaricom Ethiopia’s market entry in 2022 broke eight decades of monopoly, forcing Ethio Telecom to slash mobile data tariffs by 70% and to quicken 4G and pilot 5G deployments.[1]British International Investment, “Safaricom Consortium Invests in Ethiopia,” bii.co.uk The consortium has built more than 3,000 towers, doubling the national 4G footprint and onboarding 8.31 million M-Pesa users whose early activity centers on airtime and data purchase rather than remittance. Competitive pressure has raised network quality benchmarks, though asymmetric spectrum allocations still favor the incumbent. The USD 1.6 billion license pledge represents Ethiopia’s largest private telecom investment and has signaled long-run confidence despite near-term operating losses. Heightened capex also stimulates local supply-chain jobs, amplifying the positive spill-over into construction and logistics.

Government “Digital Ethiopia 2025” Broadband Push

Digital Ethiopia 2025 aims to add ETB 1.3 trillion (USD 10 billion) to GDP by 2028, positioning broadband as the backbone of wider e-government and financial-inclusion goals. Mandatory digital IDs for public-service access, a World Bank-backed USD 350 million ID roll-out, and the launch of the Ethiopian Securities Exchange in 2025 collectively generate fresh data traffic and financing channels. Public-sector demand for connectivity in schools, hospitals, and administrative hubs anchors medium-term revenue certainty for operators. Success, however, hinges on inter-agency coordination led by the Ethiopian Communications Authority, which must harmonize spectrum road maps with fiscal incentives for rural build-out. Effective implementation is expected to shift the traffic mix further toward high-capacity fixed and mobile broadband products.

Rising Smartphone Adoption among Youth

Ethiopia’s median age of 19.1 positions a digitally native cohort at the center of mobile-first engagement. Mobile connections and overall penetration are rising, and growing average monthly data consumption supported by social-media utilization. Handset affordability remains an obstacle because import duties and forex scarcity inflate device prices. Consequently, financing schemes and low-cost Chinese brands have become critical levers for sustaining adoption momentum.

Mobile-Money-Led ARPU Uplif

Telebirr processed over ETB 1 trillion in transactions within two years and enrolled 36 million users by 2025, creating recurring payment touchpoints that lift customer stickiness. M-Pesa’s 8.31 million Ethiopian users mainly purchase airtime and bundles, producing modest KES 24.4 million revenue yet illustrating headroom for peer-to-peer and merchant use cases. The National Bank’s decision to allow foreign operators in payment services mirrors Kenya’s early-2000s policy trajectory and is expected to elevate mobile-money-driven ARPU. Bank-account ownership improved to 46% of adults in 2022 from 22% in 2014, but mobile-money ownership lags the Sub-Saharan average, signaling continued growth capacity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Forex Shortage for Network Capex | -0.7% | National, affecting all operators | Short term (≤ 2 years) |

| Unreliable National Power Grid | -0.3% | Rural and semi-urban areas | Medium term (2-4 years) |

| Region-level Right-of-Way Approval Delays | -0.2% | Regional variations, particularly conflict-affected areas | Medium term (2-4 years) |

| High Device and Service Tax Burden | -0.2% | National, with disproportionate impact on low-income segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Forex Shortage for Network Capex

The banking system prioritizes government import bills over private-sector letters of credit, leaving operators waiting months for equipment funding. Ethiopian-Birr depreciation of 4.8% in 2023, plus 28.7% inflation, raises dollar-denominated procurement costs. Satellite broadcasters’ protest over USD 6,000–8,000 monthly transponder fees underscores the wider cost inflation that accompanies dollar scarcity. While IMF Extended Credit Facility talks and BRICS membership promise incremental relief, Ethiopia’s USD 28.2 billion external debt stock limits near-term liquidity. Consequently, network expansion schedules are frequently revised, slowing rural coverage and constraining 5G momentum.[2]International Rescue Committee, “Ethiopia Economic Update 2024,” rescue.org

Unreliable National Power Grid

Grid outages, especially outside major cities, elevate site opex and threaten service continuity. Operators respond with solar-powered towers that ensure uptime and cut diesel dependence, though initial capex remains high. The Grand Ethiopian Renaissance Dam should strengthen long-term power availability, but distribution bottlenecks persist. Renewable-energy back-up forms part of Digital Ethiopia 2025 priorities, yet forex limitations again slow panel imports. Rural broadband economics, therefore, rely on a careful mix of solar, battery, and low-earth-orbit satellite backhaul to sustain viable operating margins.[3]Frontier Africa Reports, “Power Infrastructure Outlook Ethiopia,” frontierafricareports.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data and Internet Services Drive Revenue Growth

Data and Internet services commanded 46.89% of 2024 revenue, securing the top position within the service portfolio of the Ethiopia telecom MNO market. The segment benefits from soaring mobile-data usage, illustrated by Safaricom Ethiopia’s 144.3% jump in data revenue to KES 3.2 billion, equal to 52% of its service turnover. Average per-capita use now stands at 6.5 GB per month, spurred by youth-centric social-media habits and the mandatory digital ID ecosystem that pushes citizens online. Fixed broadband lines span speeds from 3 Mbps up to 2,048 Mbps and cater to enterprises and machine-to-machine health and logistics use cases, while Pay-TV and messaging add niche but steady contributions. The Ethiopia telecom MNO market size for data and internet services stands at USD 362.5 million in 2024 and is projected to climb at a 3.2% CAGR through 2030, reflecting rising smartphone penetration and digital-government programs.

IoT and M2M is expanding at 2.40% CAGR off a low base, helped by smart-city pilots in Bahir Dar and Addis Ababa that integrate cloud, surveillance, and traffic-management layers. Ethiopian agriculture, logistics, and health verticals are evaluating low-cost sensor networks that improve supply-chain transparency, while operators package dedicated NB-IoT and LTE-M connectivity. Regulatory moves toward data-localization under the 2024 Personal Data Protection Proclamation create compliance-driven demand for domestic hosting, which supports bundle sales of cloud and connectivity. As forex and spectrum challenges ease, the service mix is expected to skew further toward high-throughput data products, consolidating the dominance of data-centric revenue streams in the Ethiopia telecom MNO market.

By End User: Consumer Dominance with Enterprise Acceleration

Consumer lines held 74.01% share in 2024, underlining the mass-market orientation of the Ethiopia telecom MNO market. The demographic heft of 134 million citizens, together with a median age of 19.1, fuels sustained demand for affordable bundles and social-media access. Telebirr’s 36 million users and M-Pesa’s swift onboarding illustrate the consumer appetite for integrated connectivity-and-payment ecosystems. However, smartphone affordability remains a barrier for 51% of unbanked adults, prompting operators to trial instalment financing and feature-phone payment apps. The Ethiopia telecom MNO market size for the consumer segment reached USD 0.95 billion in 2024 and is advancing at 2.4% CAGR, driven mainly by data-add-ons and mobile-money ARPU uplift.

Enterprise accounts are the fastest-rising end-user category, expanding at 4.88% CAGR through 2030 as firms align with digital-trade, e-tax, and supply-chain modernization. Ethio Telecom’s dedicated broadband tiers of 100 Mbps to 2,048 Mbps, alongside smart-office and cloud-back-up solutions, anchor this momentum. The Raxio data-center opening brings carrier-neutral colocation that enables redundancy for banks and fintech’s, while the impending liberalization allowing 40% foreign bank ownership should catalyze further ICT spend. Smart-city contracts and public-cloud adoption by ministries add steady pipeline visibility. Thus, while consumers drive scale, enterprises will contribute disproportionate marginal revenue growth and diversify operator earnings within the Ethiopia telecom MNO market.

Geography Analysis

Urban nodes, particularly Addis Ababa, Dire Dawa, Hawassa, and regional capitals, record the highest penetration levels, with 4G availability exceeding 80% and pilot 5G cells active in core business districts. These cities host higher disposable incomes, concentrated government services, and the bulk of data-center and fiber infrastructure. Mobile-money take-up is correspondingly deeper, as citizens use Telebirr to pay taxes and utilities and access digital IDs. Rural and remote zones lag, constrained by unreliable grid supply, right-of-way delays, and the extended procurement cycles that forex shortages impose on tower hardware. Operators are eyeing low-earth-orbit satellite backhaul plus solar-powered towers to close the cost gap, yet commercial returns remain thin without mandatory infrastructure-sharing enforcement.

Conflict-affected northern and western regions face intermittent outages and security-related network suspensions, slowing site deployment despite regulatory obligations for geographic parity. Nonetheless, the Digital Ethiopia 2025 roadmap mandates universal broadband, causing regulators to weigh phased rollout milestones against realistic funding capabilities. The Ethiopian Communications Authority is revising penalties and incentives around underserved-area coverage, while the new stock exchange offers alternative capital sources for rural-network ventures. Satellite-internet aspirants such as Eutelsat have formally applied for landing rights, and their entry could leapfrog terrestrial constraints for schools and clinics in sparsely populated areas.

Topographical variation further complicates network economics; the Ethiopian Highlands create microwave-link planning challenges, whereas lowland pasture regions require extended backhaul runs with limited power available. Operators hence deploy hybrid fibre-microwave rings and trial battery-plus-solar arrays to ensure uptime. Population density disparities translate into tiered pricing strategies as well as technology mix decisions; urban areas support premium unlimited 5G offers, while rural bundles cap speeds and data volumes to retain affordability. Overall, the geography-driven digital divide remains pronounced, but sustained policy support, alternative backhaul, and evolving tower-share regulation collectively aim to narrow the gap in the Ethiopia telecom MNO market.

Competitive Landscape

The market is a regulated duopoly with Ethio Telecom and Safaricom Ethiopia accounting for roughly 90% of mobile connections, while small ISPs such as Websprix and Winet focus on fibre broadband niches. Ethio Telecom leverages its 21,000-kilometre national backbone, nationwide retail presence, and Telebirr integration with government services to consolidate incumbency. Safaricom differentiates through superior 4G and early 5G capability, bundled with the proven M-Pesa platform familiar to Kenyan diaspora and regional investors. Price wars have knocked prepaid data tariffs down by as much as 70% since 2017, compressing margins yet expanding user bases and data traffic volumes.

Investment rivalry has intensified. Ethio Telecom accelerated 5G rollouts in Addis Ababa and Bahir Dar and partnered with Visa to embed digital payments into its channels. Safaricom crossed 3,141 live sites by early 2025, tapped Chinese vendors for network gear, and confirmed ten-year tower leasing lines to support rural push. Infrastructure-sharing talks remain stalled over asset-valuation disagreements, resulting in parallel builds that raise capex and slow rural economics. Regulatory files mandate cost-based sharing, but the absence of a binding code of practice delays execution.

White-space opportunities persist in enterprise IoT, cloud, and sector-specific solutions. Raxio’s carrier-neutral data center is attracting both operators for offload and fintechs for secure colocation. Satellite-internet entrants hold potential for a disruptive layer that can bypass terrestrial bottlenecks. Looking ahead, spectrum auctions for 700 MHz and millimeter bands, plus a possible third mobile license, may recalibrate the balance of power. Overall, while Ethio Telecom retains scale leadership, Safaricom’s funding depth and innovation track record ensure sustained competitive intensity across the Ethiopia telecom MNO market.

Ethiopia Telecom MNO Industry Leaders

Safaricom Ethiopia

Ethio Telecom

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Safaricom reported record revenue of USD 3 billion for FY 2025, with Ethiopia contributing nearly 10% despite startup losses of KES 25.7 billion.

- April 2025: Ethio Telecom and Visa deepened cooperation to scale digital-payment acceptance across government portals.

- January 2025: Ethiopia inaugurated the Ethiopian Securities Exchange, opening new fundraising paths for telecom infrastructure.

- October 2024: Ethio Telecom launched the Smart Bahir Dar project featuring 5G-backed cloud and IoT services.

Ethiopia Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-User | Enterprises |

| Consumer |

Key Questions Answered in the Report

How large is the Ethiopia telecom MNO market in 2025?

The Ethiopia telecom MNO market is worth USD 776.3 million in 2025 and is projected to grow at 2.94% CAGR to USD 897.4 billion by 2030.

Which service category generates the most revenue today?

Data and internet services lead with 46.89% revenue share, reflecting rapid mobile-data adoption and rising broadband demand.

Who are the main competitors?

Ethio Telecom and Safaricom Ethiopia dominate

What is the fastest-growing segment within the Ethiopia telecom MNO market?

Data and internet services show the quickest expansion, recording a 3.34% CAGR through 2030

What are the main challenges to network expansion?

Persistent foreign-exchange shortages and an unreliable power grid delay equipment imports and rising operating costs, especially in rural deployments.

Page last updated on: