Niger Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

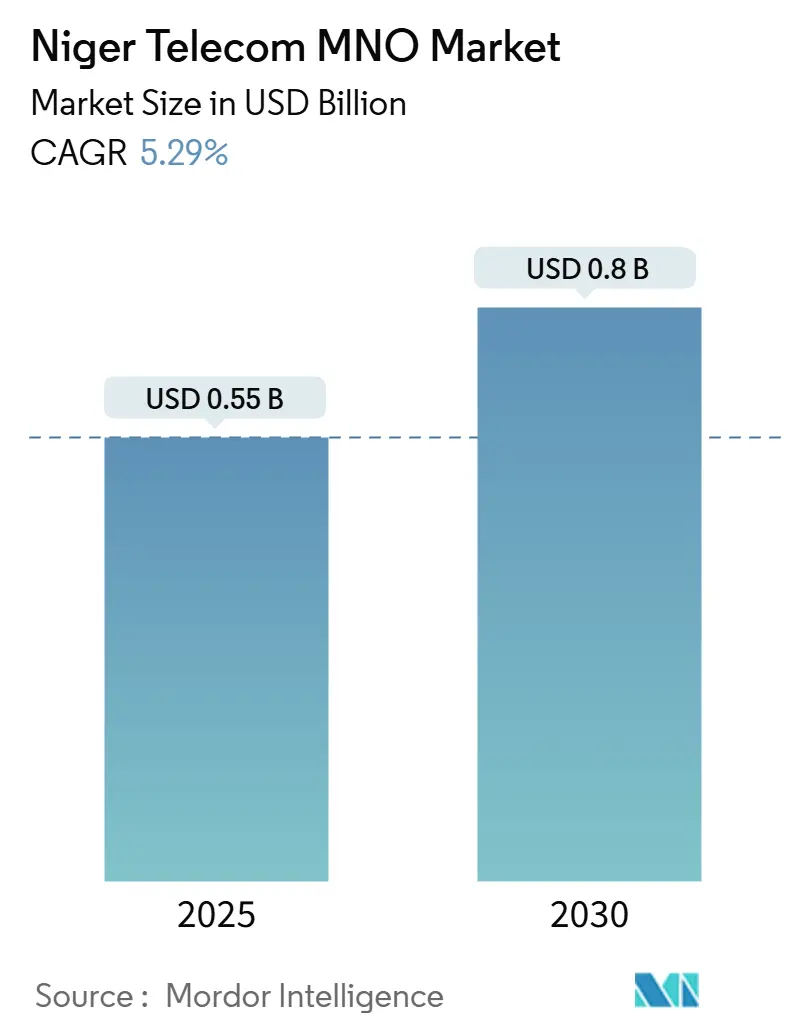

| Market Size (2025) | USD 0.55 Billion |

| Market Size (2030) | USD 0.8 Billion |

| Growth Rate (2025 - 2030) | 5.29% CAGR |

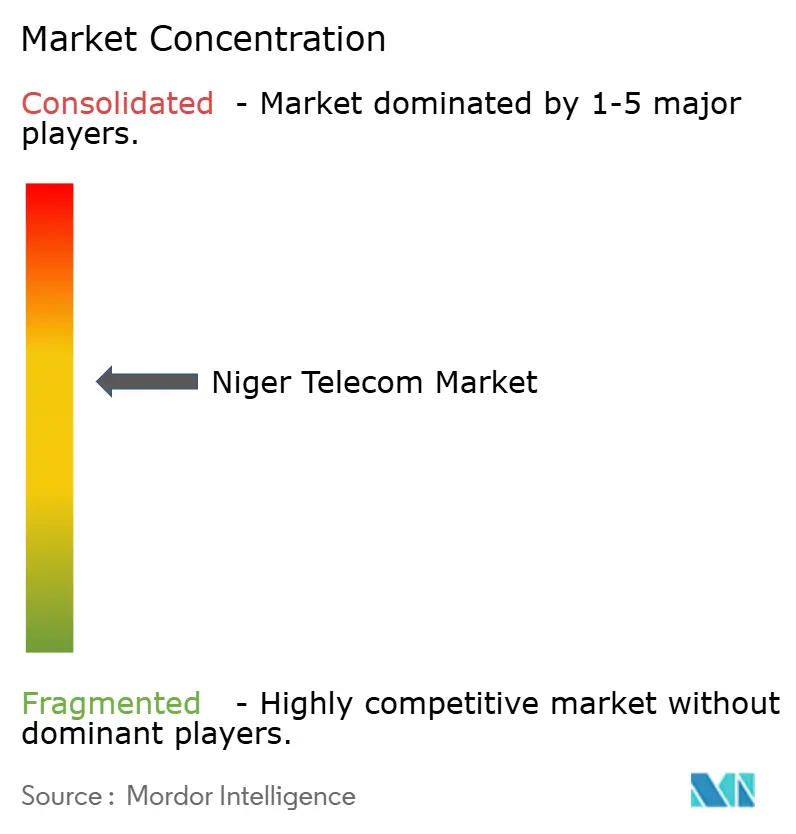

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Niger Telecom MNO Market Analysis by Mordor Intelligence

The Niger Telecom MNO Market size is estimated at USD 0.55 billion in 2025, and is expected to reach USD 0.8 billion by 2030, at a CAGR of 5.29% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 15.05 million subscribers in 2025 to 18.74 million subscribers by 2030, at a CAGR of 4.49% during the forecast period (2025-2030).

Niger’s upward trajectory springs from overlapping public and private investment programs that reinforce national fiber links, extend fourth-generation mobile sites, and seed new satellite gateways that fill the rural connectivity gap. Steady macro-economic support through the CFA Franc, combined with a young demographic that embraces data-centric services, keeps subscriber growth resilient even during broader West African volatility. Competitive pressures remain visible: Airtel, Orange, Moov, and the state-owned SahelCom are locked in a race to upgrade radio access networks and introduce richer mobile financial services. At the same time, the arrival of low-Earth-orbit capacity strengthens national backhaul, helping operators satisfy rising demand for streaming, e-commerce, and digital payments.

Key Report Takeaways

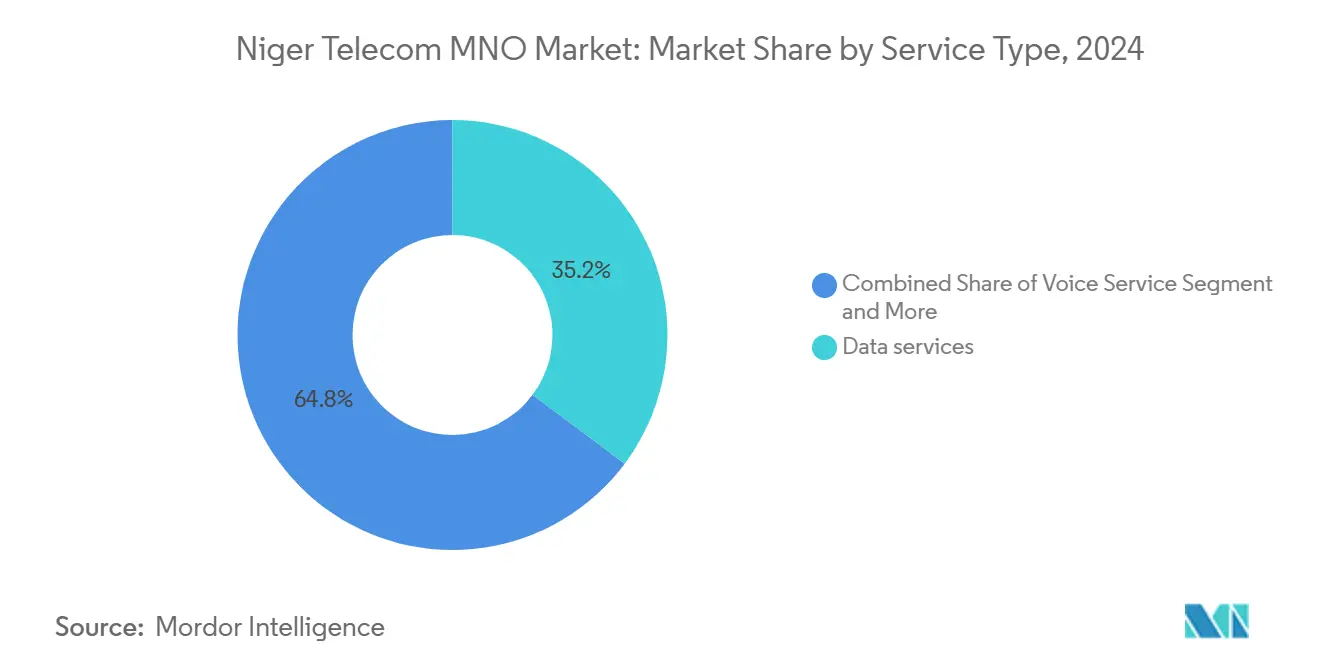

- By service type, data services captured 45.64% of the Niger telecom market share in 2024, while IoT services are advancing at a 4.73% CAGR through 2030.

- By service type, voice services retained 36.99% revenue share of the Niger telecom market size in 2024 and are projected to expand at a 5.24% CAGR through 2030.

- By end user, consumer services held 69.29% of the Niger telecom market share in 2024, whereas the enterprise segment is forecast to grow at a 5.62% CAGR to 2030.

Niger Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated 4G roll-outs following 1800 MHz refarming | +1.2% | National, with early gains in Niamey, Maradi, Zinder | Medium term (2-4 years) |

| Government-backed National Fiber Backbone expansion | +0.9% | National, prioritizing rural and underserved areas | Long term (≥ 4 years) |

| Soaring demand for mobile money & digital payments | +1.1% | National, with higher adoption in urban centers | Short term (≤ 2 years) |

| Starlink LEO licence unlocking high-speed rural backhaul | +0.8% | Rural and remote areas nationwide | Medium term (2-4 years) |

| Energy-as-a-Service tower upgrades lowering OPEX | +0.6% | National, focusing on off-grid locations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated 4G roll-outs following 1800 MHz refarming

Reconfiguration of the 1800 MHz band lets operators unlock contiguous 4G blocks that carry data traffic farther than legacy 3G channels. Niger Telecoms recently activated 16 new sites in Maradi and has earmarked additional base stations for Zinder, Tahoua, and rural communes where voice coverage once stalled at edge-only speeds. Field reports show that every refarmed site lifts average downlink throughput above 25 Mbps, slashing page-load latency and enlarging the feasible market for low-cost smartphones. These metrics explain why user migration toward data-rich applications gained pace in 2024 and why regulators consider the spectrum policy a foundational pillar of the 6.64% market CAGR. Independent audits confirm that refarming also trims capex per gigabit delivered because carriers reuse existing tower inventory instead of purchasing fresh frequencies. [1]ARCEP Niger, “Spectrum Refarming Progress Report 2024,” arcep.ne

Government-backed national fiber backbone expansion

The Trans-Saharan optical backbone, funded with EUR 43.9 million by the African Development Bank, is progressing in parallel with Phase3 Telecom’s aerial link that runs north from Kano in Nigeria to Niamey. When lit, the combined routes will carry multi-terabit capacity, cutting wholesale IP transit costs and allowing mobile operators to shift base-station backhaul from microwave to fiber. In turn, fiber reach improves network resiliency and encourages cloud-based enterprise workloads that underpin the fastest-growing 7.89% CAGR enterprise segment. Rural councils also benefit because the Smart Villages project reserves last-mile grants for 2,000 schools and clinics, ensuring that critical public services access dedicated bandwidth.

Soaring demand for mobile money and digital payments

Mobile money wallets such as Zamani Cash and Airtel Money doubled active clients between 2019 and 2024, a pattern reinforced by an UNCDF grant that financed 70 new kiosks and training for women-led agents. Transaction ceilings hit 2,000,000 CFA per day for full-KYC accounts, letting migrant workers remit wages securely from cities to remote farms. Every payment ride increases data-session frequency because users must verify balances, approve PINs, or download receipts, which raises blended ARPU and supports the Niger telecom market growth path. Orange’s pay-to-merchant QR pilot in Niamey’s Soudouré market shows that small traders adopt the service within three months of exposure, reinforcing the short-term +1.1% uplift in forecast CAGR.[2]UNCDF, “Zamani Cash Agent Network Expansion,” uncdf.org

Starlink LEO licence unlocking high-speed rural backhaul

ARCEP cleared Starlink to sell consumer terminals that average 200 Mbps downstream, a leap over the sub-5 Mbps speeds that characterize legacy Ku-band satellite services. Early field tests in Tillabéri showed video conference latency under 40 ms, enabling distance-learning sessions that were impossible over 2G data. Mobile operators can also book Starlink capacity under wholesale agreements to close terrestrial backhaul gaps that previously forced them to postpone site roll-outs. This hybrid topology keeps opex predictable and makes coverage in 30% of the territory economically viable for the first time.[3]Ecofin Agency, “Starlink Secures Licence in Niger,” ecofinagency.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency depreciation inflating capex & spectrum fees | -0.7% | National, with varying impact on international transactions | Short term (≤ 2 years) |

| High poverty rates constraining service affordability | -0.9% | National, with higher impact in rural areas | Long term (≥ 4 years) |

| Chronic electricity shortages limiting site uptime | -0.8% | National, particularly affecting rural and off-grid sites | Medium term (2-4 years) |

| Rising militant activity hindering rural roll-outs | -0.5% | Border regions and remote areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Currency Depreciation Inflating Capex & Spectrum Fees

Although the CFA Franc’s euro peg reduces abrupt swings, telecom vendors invoice radio equipment, core switches, and submarine‐capacity leases in USD. When a global chip shortage inflates hardware costs, local operators face a double hit that erodes operating margins. The effect is most acute for mid-tier licensees that lack multiregional treasury hedges and that must commit upfront cash to maintain build-out obligations. Operators therefore stage investments in tranches, stretching network plans and slowing coverage in sparsely populated arrondissements. If the Franc weakens by 5% against the USD basket, spectrum renewals scheduled for 2026 could rise beyond internal forecasts, delaying commitments to 5G trials.

High poverty rates constraining service affordability

More than 40% of Nigeriens live below the international poverty line, which caps discretionary spending on gigabyte bundles and handset upgrades. Even where 4G arrives, customers ration data to essential uses such as peer-to-peer transfers or exam results. Carriers respond with sachet-sized tariffs that slice validity into hourly or overnight windows, but ultra-low ARPU limits returns that fund network expansion. The affordability gap widens in harvest-lean months when rural income dips, forcing prepaid churn spikes that compress lifetime value metrics. Bridging this hurdle will rely on device financing alliances and targeted subsidies under the World Bank Smart Villages envelope that earmarks connectivity vouchers for low-income households.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Drive Digital Transformation

Data services captured 45.64% of 2024 sector revenue, making broadband the single largest line on operator income statements and the most dependable growth lever inside the Niger telecom market. Voice still matters because wireless calls account for 66.24% of the voice vertical, but user behaviour pivots toward data-heavy messaging and streaming that ride 4G upgrades. IoT stands out as the quickest climber with a 4.73% CAGR, buoyed by crop-monitoring sensors that alert farmers about soil moisture and by smart-meter pilots in Niamey’s industrial parks. Mobile data holds 68.95% slice of the data sub-total; here, operators reap economies of scale through bandwidth-saver codecs and carrier-grade caching. Fixed data is smaller yet clocks a brisk 7.45% expansion as fibre trenches pass public offices, mining camps, and high-income compounds. The Niger telecom market size for fixed broadband is therefore on track to layer fresh revenue atop the established mobile base. OTT music, local language video, and time-shifted education portals hover at an early phase but will accelerate once average access speeds cross the 10 Mbps threshold that Starlink already meets.

Continued data leadership depends on synchronized capacity creation across the radio, core, and international gateways. Operators now procure IP transit from cables that land in Lagos, then ride Phase3 aerial fibres into Niger, slashing wholesale per-megabit pricing by more than one-half compared with pre-2024 satellite backhaul. This blend reduces cost-of-service and sustains a competitive retail price ladder, a precondition for maintaining the Niger telecom market CAGR. High order modulation and massive MIMO trials in Niamey push spectral efficiency beyond 5 bps/Hz, freeing headroom for future 5G use cases without heavy incremental opex. Meanwhile, the government mandates open-access dark fibre along trunk roads, a move that multiplies ISP entrants and seeds fresh cloud solutions for enterprises that require guaranteed latency. The transition from voice-centric to digital-first is therefore not abstract; it reflects tangible capex, spectrum, and regulatory milestones already baked into operator budgets.

By End-User: Enterprise Segment Accelerates Digital Adoption

Consumers still generate 74.02% of aggregate 2024 revenue, mirroring a demographic structure in which two-thirds of the population is under 25. Young users fuel social media, short-form video, and cross-border remittance flows that anchor day-to-day traffic patterns. Value-added services such as airtime advances and bundles that pair data with discounted cab rides create micro-upsell moments that lift prepaid spend. Mobile money remains the quintessential sticky product, weaving itself into school-fee payments, market stall purchases, and salary disbursement for civil servants. Each of these actions lengthens session time and keeps the Niger telecom market on a firm expansion path.

Enterprises, in contrast, book a smaller yet faster slice, growing at 7.89% CAGR as banks digitize branch operations and mining majors install LTE-Advanced private networks to monitor fleet logistics. The Niger telecom market share of corporate VPNs rises with every kilometre of new backbone, allowing provincial branches secure links to HQ systems in Niamey. Government e-services also expand; electronic customs clearance, e-procurement, and national ID programs all demand carrier-grade links that operate round-the-clock. Cloud-hosted accounting for agribusinesses and IoT telemetry for storage silos widen the solution set and demonstrate why enterprise revenue will keep outpacing the consumer line. Operators tailor service-level agreements that guarantee uptime despite grid outages by bundling solar-storage backup at customer premises, deepening penetration in high-value verticals and reinforcing the long-term resilience of the Niger telecom market.

Geography Analysis

Urban Niamey remains the epicentre of the Niger telecom market, accounting for the lion’s share of high-ARPU subscribers and attracting the earliest upgrades to refarmed 1800 MHz 4G. Maradi, Zinder, and Tahoua follow, each exhibiting densification that supports carrier aggregation and high-capacity microwave rings. In these hubs, smartphone adoption already tops 55%, opening space for app-based ride-hailing, food-delivery, and video-on-demand. Fibre digs ride existing power trenches, lowering civil-works costs and accelerating build schedules that enable new fixed offerings. These urban pockets therefore underpin the baseline from which national averages climb year on year.

Beyond cities, population clusters thin rapidly, yet they still matter because 80% of Nigeriens live in rural communities and generate seasonal income that converts into airtime. The Niger telecom market strategy balances solar-powered micro-cells, satellite backhaul, and subsidised fibre spurs to extend both voice and data across remote prefectures. The Smart Villages program channels World Bank funds into communal access points that anchor healthcare, schooling, and market price information. As each village hub activates, nearby households adopt entry-level smartphones, swelling first-year data usage by double-digit percentages. This layered approach ensures that rural contributions to overall market growth, while starting from a low base, remain significant to long-run projections.

Niger’s landlocked status adds a regional dependency dimension. International capacity rides terrestrial fibre through Nigeria and Benin, making cross-border regulatory harmonisation crucial. Disruptions, such as ECOWAS sanctions in 2024, expose single-route vulnerabilities, yet they also galvanise authorities to fast-track redundant links to Algeria and Burkina Faso. These geographic interdependencies reinforce the importance of diversified gateways for safeguarding the Niger telecom market against geopolitical shocks. At the same time, border districts emerge as testbeds for roaming-friendly tariffs and regional e-commerce, suggesting that location will increasingly dictate service design choices as the market matures.

Competitive Landscape

The Niger telecom market hosts four network operators whose combined footprints blanket 77% of the population. Airtel Niger leads with 47% Niger telecom market share in 2024, leveraging scale efficiencies from its Pan-African backbone and a deep mobile money ecosystem that processes millions of micro-transactions daily. Orange Niger holds 29%, capitalising on brand equity and a franchise of 10,000 retail points that place SIM cards within walking distance for most urban dwellers. Moov Niger, the third entrant, focuses on bundled voice-data packs that target value seekers, while SahelCom, the state-backed carrier, emphasises universal-service obligations and builds coverage in frontier districts where private players hesitate.

Price competition stays disciplined due to the regulatory requirement that any bundle introduced by the market leader must be replicated within 24 hours by rivals, a rule designed to prevent predatory discounting while encouraging service innovation. Infrastructure-sharing accords let Moov and SahelCom collocate on Airtel masts, a decision that cuts their rural roll-out costs by up to 30% and frees capital to invest in core network virtualisation. The resulting parity in urban data speeds narrows perceived gaps in quality, forcing differentiation to migrate toward content partnerships and loyalty programs.

The competitive script entered a new act when Starlink secured its Type-A licence in 2024, opening an over-the-top challenge that bypasses terrestrial spectrum altogether. Mobile operators responded by exploring hybrid modems that switch between LTE and LEO paths, protecting enterprise accounts from potential churn. Parallel moves include pilot tests of open RAN to slash equipment vendor lock-in and cost optimisation through Energy-as-a-Service deals that swap diesel gensets for solar-battery hybrids. These strategic pivots underscore a moderate concentration market where innovation cycles run faster every year yet leave sufficient profit to sustain capital intensity and defend long-term service quality commitments.

Niger Telecom MNO Industry Leaders

Airtel Niger

Zamani Telecom (Orange Niger)

Moov Africa Niger

Niger Telecoms / SahelCom

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Niger’s Ministry of Communication granted Starlink a licence to operate satellite internet services that promise average 200 Mbps speeds, directly addressing coverage and latency concerns in under-served regions.

- July 2024: Niger Telecoms installed 16 new sites in Maradi to close gaps in rural voice and data coverage and strengthen its competitive stance.

- April 2024: China’s ambassador signalled willingness to deepen digital cooperation, paving the way for future infrastructure investment and technology transfer.

- December 2024: UNCDF expanded support for Zamani Cash, targeting 100,000 fresh clients in peri-urban and rural communities and adding 5,000 jobs

Niger Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming & International Services, Enterprise & Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming & International Services, Enterprise & Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

1. What is the current size of the Niger telecom market?

• The Niger telecom market size is USD 391.52 million in 2025.

2. How fast is the Niger telecom market expected to grow?

• Growth is projected at a 6.64% CAGR, taking sector revenue to USD 563.79 million by 2030.

3. Which service segment is expanding quickest?

• IoT connectivity leads with a 7.01% CAGR driven by agriculture and smart-meter applications.

4. Who holds the largest Niger telecom market share?

• Airtel Niger leads with 47% Niger telecom market share for 2024.

5. Why are satellite solutions important for Niger?

• Low-Earth-orbit licences such as Starlink supply 200 Mbps backhaul to rural zones where fiber is uneconomic, boosting national coverage and service quality.

Page last updated on: