Malawi Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

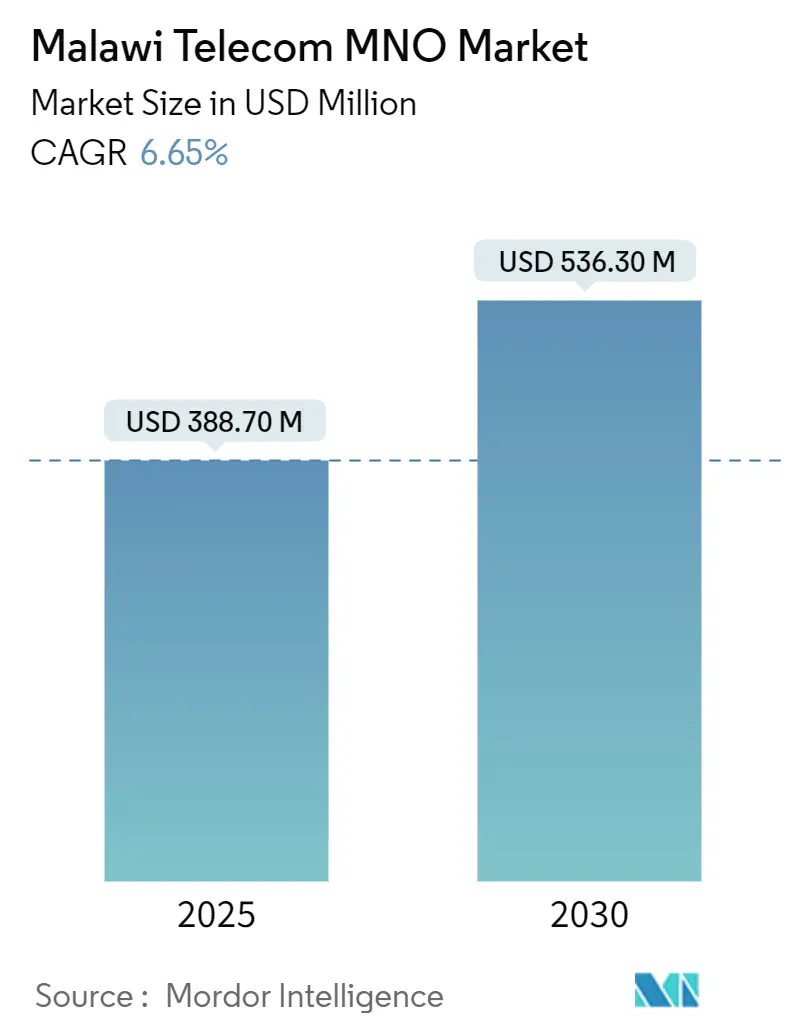

| Market Size (2025) | USD 388.70 Million |

| Market Size (2030) | USD 536.30 Million |

| Growth Rate (2025 - 2030) | 6.65% CAGR |

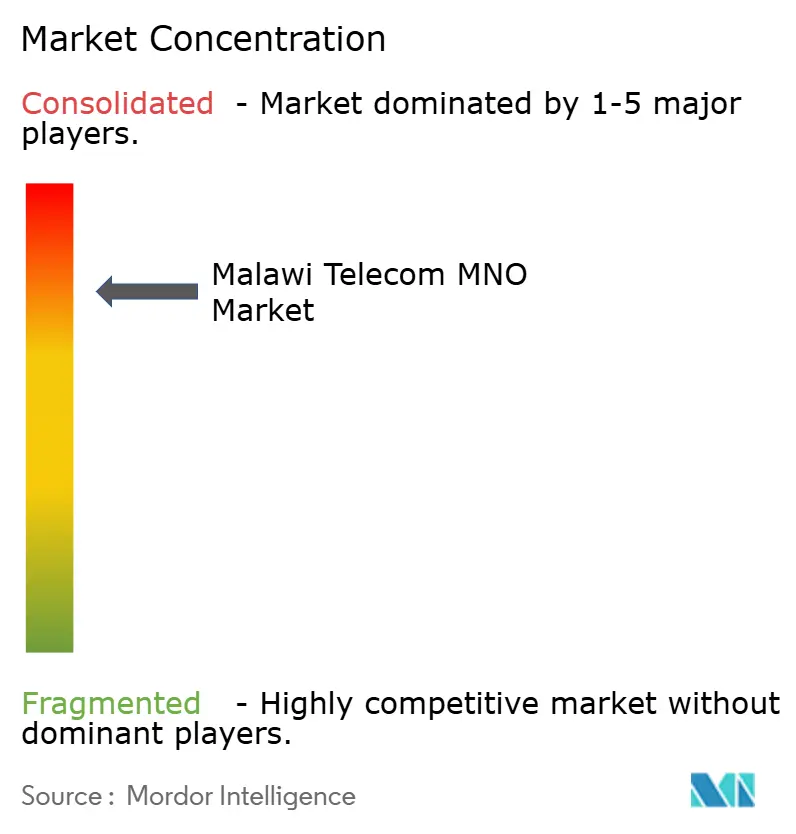

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malawi Telecom MNO Market Analysis by Mordor Intelligence

The Malawi Telecom MNO Market size is estimated at USD 388.70 million in 2025, and is expected to reach USD 536.30 million by 2030, at a CAGR of 6.65% during the forecast period (2025-2030).

Low mobile-penetration levels, accelerating mobile-money usage, and continued 4G roll-outs set the tone for steady-not spectacular-growth. Data services now account for more than one-third of sector revenue, while the number of registered mobile-money wallets has crossed 10 million, lifting average revenue per user (ARPU) even in price-sensitive rural districts. Competitive pressure is intensifying as Starlink and other entrants raise performance benchmarks, and cross-border fiber projects promise additional wholesale capacity . Against this opportunity, operators face persistent power deficits, a volatile Kwacha, and sector-specific taxes that cap household device uptake . Regulatory modernization-especially the June 2024 Data Protection Act-offers clearer guardrails for privacy, device approval, and universal-service funding that should help operators monetize new services over the medium term.

Key Report Takeaways

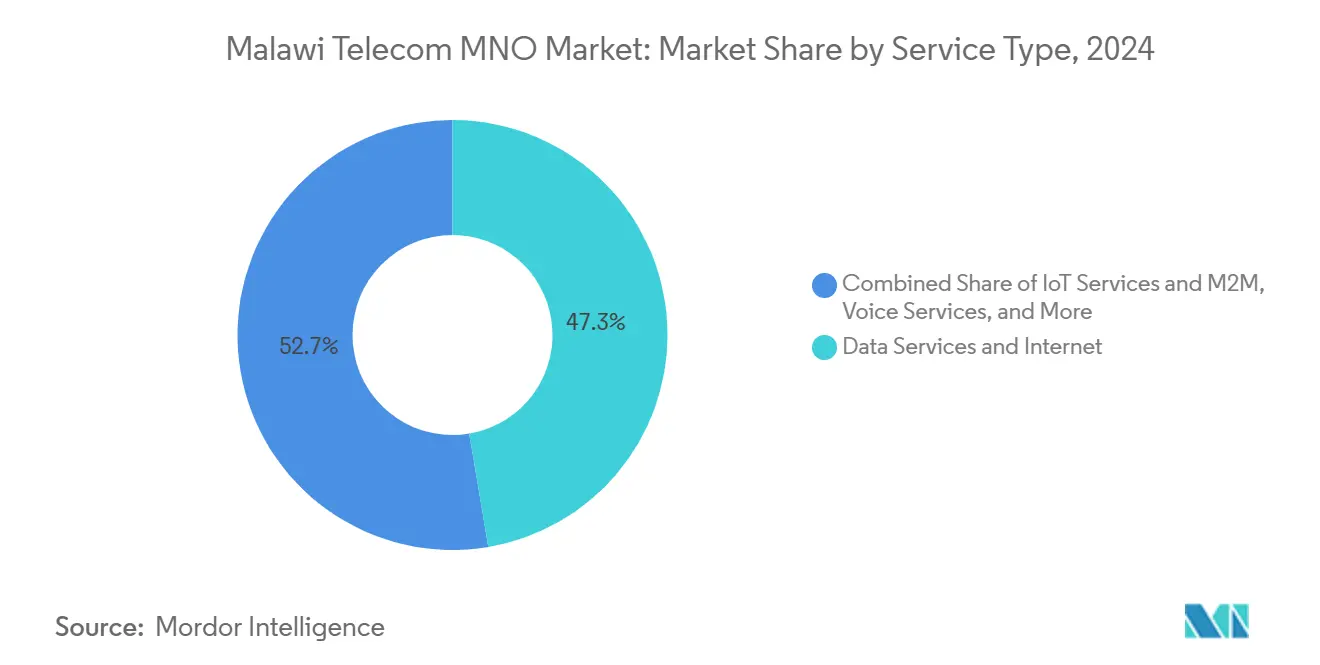

- By service type, data and internet services captured 47.33% of 2024 revenue, while IoT and M2M services posted 6.78% CAGR through 2030.

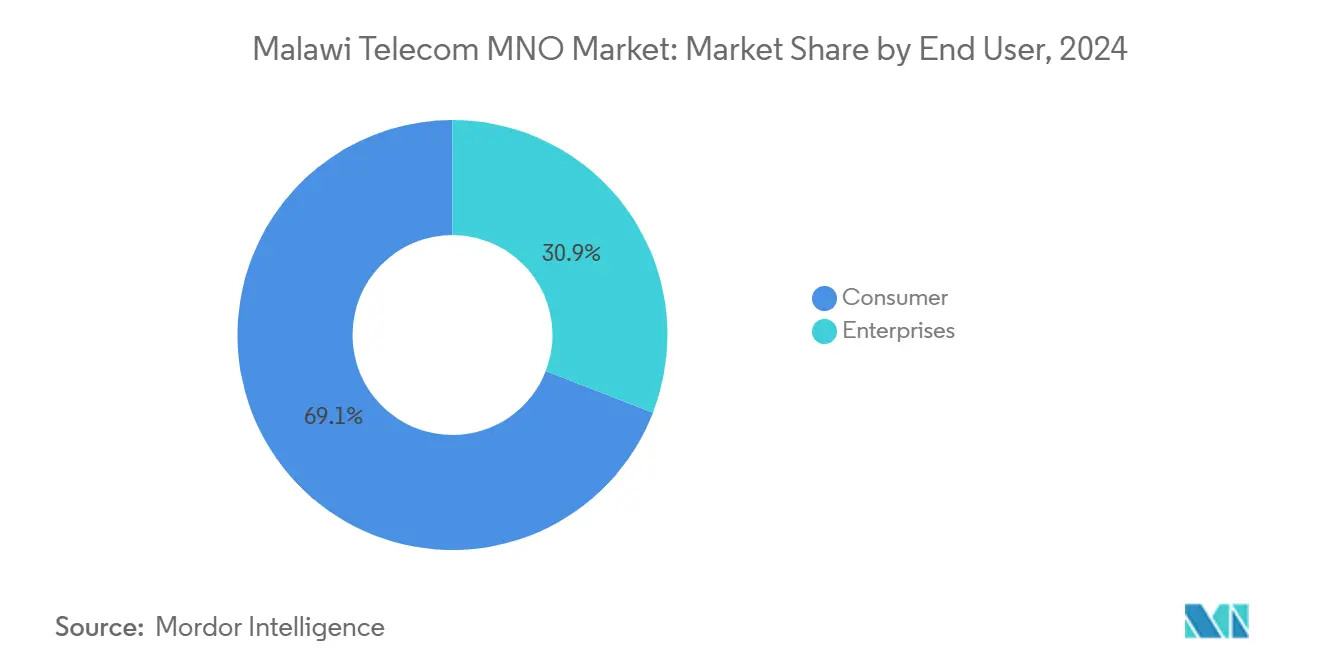

- By end user, the consumer segment led with 78.19% of the Malawi telecom MNO market share in 2024; enterprise usage is expanding at 7.12% CAGR.

Malawi Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 4G expansion and planned 5G trials | +1.2% | National; Lilongwe, Blantyre, Mzuzu | Medium term (2-4 years) |

| Spectrum-fee reductions driving capex | +0.8% | National | Short term (≤ 2 years) |

| Mobile-money transaction surge elevating ARPU | +1.5% | National; stronger in rural areas | Long term (≥ 4 years) |

| Government digitalization programs | +0.9% | National; early gains in urban centers | Medium term (2-4 years) |

| Enterprise-centric IoT in agriculture and utilities | +0.6% | Agricultural regions nationwide | Long term (≥ 4 years) |

| New cross-border fibre routes lowering IP transit costs | +0.7% | National with regional spillover | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid 4G expansion and planned 5G trials

4G now covers the largest cities, and both Airtel Malawi and TNM are moving into secondary towns to capture first-time smartphone users who still rely on older 3G networks. Infrastructure sharing models piloted elsewhere in Africa could be replicated to reduce Malawi capex if regulators approve passive-tower deals. Once MACRA finalises a 5G spectrum roadmap, operators plan limited trials focused on enterprise use cases, especially smart agriculture. Momentum is therefore building toward a data-first market in which video streaming, e-learning, and fintech applications dominate usage patterns.

Mobile-money transaction surge elevating ARPU

Registered wallets leapt from under 1,000 in 2012 to 10.1 million by 2024, with rural adoption outpacing urban on a percentage basis. TNM’s Mpamba and Airtel Money now bundle international remittances, cross-border virtual cards, and bill pay, lifting transaction frequency and fee income. World Bank research confirms that adults in mobile-money-enabled countries are far more likely to make digital payments within a 90-day window than those with access only to traditional banks. For Malawi operators, higher wallet stickiness offsets sliding voice rates and subsidises network investments that underpin broader data adoption.

Government digitalization programs

The Digital Malawi Project connected more than 600 public sites and pushed wholesale IP transit prices down from USD 460 to below USD 10 per Mbit/s, a 98% reduction that sharply improved operator economics. Over 100 free public Wi-Fi hotspots now serve schools and clinics, although critics question cybersecurity readiness. Membership in the Digital Public Goods Alliance gives ministries access to open-source health and social-service platforms, reducing total cost of ownership for e-government solutions. Complementary regulations-including December 2024 device-approval rules-raise compliance hurdles but aim to protect consumers and ensure network reliability.

Enterprise-centric IoT in agriculture and utilities

Pilot projects using Bluetooth LE, LoRa, and NB-IoT demonstrate how real-time soil and weather sensors enhance crop yields in districts hit hard by climate volatility. Utility firms are likewise testing smart grid and water meters, though initial deployments remain small because of capex constraints and unstable power supplies. Nonetheless, multisector IoT demand is growing as companies seek efficiency gains and prepare for carbon-reduction mandates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent power outages raising network OPEX | -0.9% | National; acute in rural areas | Long term (≥ 4 years) |

| Kwacha depreciation inflating imported capex | -1.1% | National | Short term (≤ 2 years) |

| Limited consumer purchasing power for smartphones | -0.7% | National; rural districts | Medium term (2-4 years) |

| High sector-specific taxes on SIMs and devices | -0.5% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent power outages raising network OPEX

A 27 MW electricity deficit forces base stations onto diesel generation, lifting operating spend and hindering green-network targets. Rural coverage is most affected, as only 14.2% of the population is on-grid and fuel logistics add cost and security risks. The forthcoming Malawi–Mozambique interconnector offers partial relief, but a resilient domestic grid remains years away, prolonging high OPEX.

Kwacha depreciation inflating imported capex

The Kwacha’s repeated devaluations push up prices for radios, solar panels, and towers that operators must import in hard currency, while inflation above 28% cuts consumer spending power. Airtel Africa’s latest filings singled out Malawi currency effects as a drag on reported revenue despite underlying subscriber growth. Central-bank foreign-exchange controls further lengthen procurement cycles, delaying network upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data and Internet Services Drive Revenue Transformation

Data and internet services generated 47.33% of operator turnover in 2024, cementing their role as the primary growth driver of the Malawi telecom MNO market. IoT and M2M services posted 6.78% CAGR, underpinned by agricultural and utility pilots. Project finance from the World Bank’s Digital Malawi Project slashed wholesale transit to below USD 10 per Mbit/s, enabling aggressive retail price reductions that unlocked latent demand . Together, these factors reinforce the structural shift from legacy voice to converged data, payments, and content services that characterize an emerging digital ecosystem.

Second-order effects include heightened competition over video and gaming partnerships, as operators bundle content to build brand stickiness. OTT providers have improved cache performance since the August 2024 launch of LIONEX, Malawi’s first neutral internet exchange point, further accelerating data use. To protect margins, operators increasingly upsell larger bundles and micro-loans for handset upgrades.

By End User: Consumer Dominance with Enterprise Acceleration

Consumers accounted for 78.19% revenue in 2024, an outcome shaped by a median age under 18 years and nearly universal reliance on prepaid mobile bundles. Mobile money, social media, and video streaming are core daily use cases, particularly since ARPU uplift from transfers helps subsidies data promotions. Enterprises represent a smaller, faster-growing base at 7.12% CAGR as manufacturers, agro-processors, and government agencies digitize operations. Regulatory demands for data protection and e-invoicing, alongside macro-pressures to improve productivity, increase the value of dedicated links, cloud access, and IoT solutions.

Despite momentum, enterprise uptake faces affordability hurdles: a 4 GB monthly bundle costs USD 3.54 against a USD 29 minimum wage, limiting small-business usage. The Universal Service Fund prioritized consumer sites in its first 16 projects, so dedicated enterprise subsidies remain limited. Still, satellite back-haul partnerships and cross-border mobile-money rails underscore new ways operators can serve businesses facing volatile supply chains and regional payment needs.

Geography Analysis

Urban–rural asymmetry defines network economics. Lilongwe, Blantyre, and Mzuzu host the bulk of LTE cells, achieving service availability that rivals regional peers. Rural districts, home to 81.5% of the population, contend with low electrification and sparse fiber backhaul, resulting in higher costs per user and slower data speeds. MACRA’s Universal Service interventions have added coverage in 80 additional sites but do not close the affordability gap where devices remain out of reach for many low-income households.

Cross-border connectivity is slowly improving. Angola Cables’ planned Malawi link will connect to under-sea systems at Luanda, relieving dependency on one wholesale route through Tanzania . Complementary partnerships with Zambia and Tanzania aim to diversify terrestrial routes and increase redundancy. LIONEX allows local ISPs to keep domestic traffic within the country, trimming latency and saving hard-currency transit fees.

Regional think tanks classify Malawi as an “Initial Market” for broadband, citing sparse private investment and limited infrastructure sharing. Yet the post-2024 regulatory environment now offers streamlined tower approvals and clearer fee structures that could shorten payback periods for rural roll-outs. Pilot 5G fixed-wireless tests in peri-urban zones will provide a litmus test for high-bandwidth services beyond city limits, while World Bank-funded power mini-grids could improve uptime for rural base stations.

Competitive Landscape

Airtel Malawi and TNM together hold virtually the entire Malawi telecom MNO market, forming a tight duopoly with limited room for price-based competition. Airtel enjoys a valuation of MK 1.4 trillion and a 156.4% one-year return, far outrunning TNM’s MK 265.1 billion valuation and 64.8% return as investors reward scale advantages. Mobile-money ecosystems add another layer of stickiness; Airtel Money’s virtual Mastercard and TNM Mpamba’s Israel remittance link are both deepening platform moats.

Disruptive forces, however, are mounting. Satellite broadband from Starlink delivers median download rates above 40 Mbps-double many urban mobile speeds-raising user expectations and pressuring terrestrial operators to accelerate 4G densification. Malcel’s anticipated entry could fragment the prepaid voice base, though spectrum assignment and tower deployment timelines remain uncertain.

Strategic partnerships typify responses. Airtel is teaming with SpaceX to integrate satellite back-haul, mitigating rural coverage gaps. Infrastructure-sharing frameworks piloted in Nigeria and Uganda suggest future cost-reduction alliances could emerge if regulators approve passive-tower pooling. Meanwhile, December 2024 equipment-approval rules standardize certification, potentially encouraging new vendor entrants and stimulating price competition in network hardware.

Malawi Telecom MNO Industry Leaders

Airtel Malawi Plc

Telekom Network Malawi Plc

Malawi Telecommunication Limited

Malcel Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: MTN Group and Airtel Africa signed a network-sharing pact for Uganda and Nigeria, establishing a model that could migrate to Malawi if regulators allow.

- February 2025: Bharti Airtel confirmed plans to acquire an additional 5% stake in Airtel Africa, consolidating its African footprint.

- November 2024: Angola Cables unveiled expansion into Malawi, Zambia, and Zimbabwe to lower wholesale bandwidth costs.

- August 2024: Malawi launched LIONEX, its first neutral internet exchange point, improving domestic traffic routing.

Malawi Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-User | Enterprises |

| Consumer |

Key Questions Answered in the Report

What is the current size of the Malawi telecom MNO market?

The market generated USD 388.7 million in 2025 and is projected to reach USD 536.3 million by 2030.

Which segment is growing fastest in the Malawi telecom MNO market?

Data and internet services show the highest 6.92% CAGR

How dominant are data and internet services compared with voice?

Data and internet services already contribute 47.33% of total revenue and continue to outpace voice as smartphone adoption rises.

Who are the main players in the Malawi telecom industry?

Airtel Malawi and TNM are the two main competitors

What are the biggest hurdles to telecom expansion in Malawi?

Unreliable electricity, Kwacha depreciation, and device-affordability constraints slow network investment and consumer uptake.

How will cross-border fiber projects affect Malawi’s connectivity?

New routes from Angola Cables and regional partners should cut IP transit costs, improve redundancy, and support faster fixed-broadband growth.

Page last updated on: