Croatia MVNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

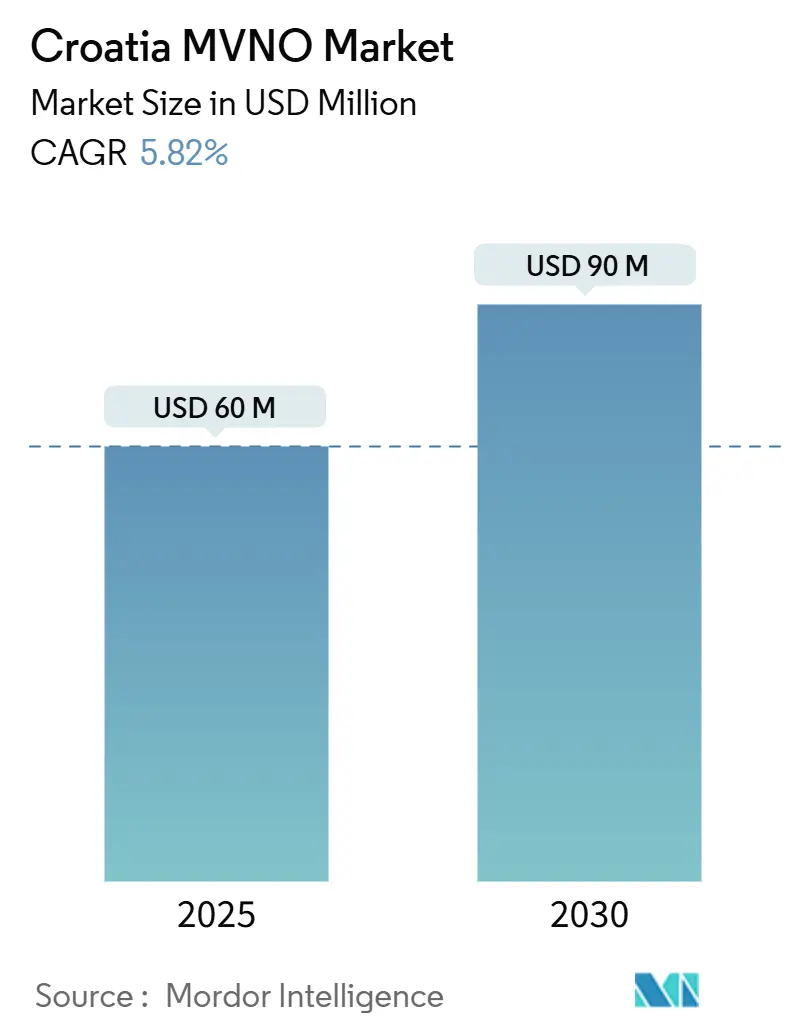

| Market Size (2025) | USD 60 Million |

| Market Size (2030) | USD 90 Million |

| Growth Rate (2025 - 2030) | 5.82% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Croatia MVNO Market Analysis by Mordor Intelligence

The Croatia MVNO Market size is estimated at USD 60 million in 2025, and is expected to reach USD 90 million by 2030, at a CAGR of 5.82% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 288.45 thousand subscribers in 2025 to 366.98 thousand subscribers by 2030, at a CAGR of 4.93% during the forecast period (2025-2030).

This performance reflects the country’s supportive wholesale‐access regulation, the pull of seasonal tourism, and a consumer shift toward digital, value-oriented mobile propositions. Strong cloud adoption, asset‐light operating models, and eSIM-based onboarding lower entry barriers for nimble brands, while spectrum refarming and satellite-terrestrial integration open new capacity corridors. Incumbent MNO bundling continues to raise the competitive bar, yet MVNOs leverage agile pricing, instant activation, and niche service design to defend margins. Growth headwinds include high regulated wholesale charges, limited mobile number prefixes, and EU “roam-like-home” revenue leakage, but the structural forces of digital tourism, IoT rollout, and regulatory parity keep the near-term outlook positive for both new entrants and incumbent sub-brands.

Key Report Takeaways

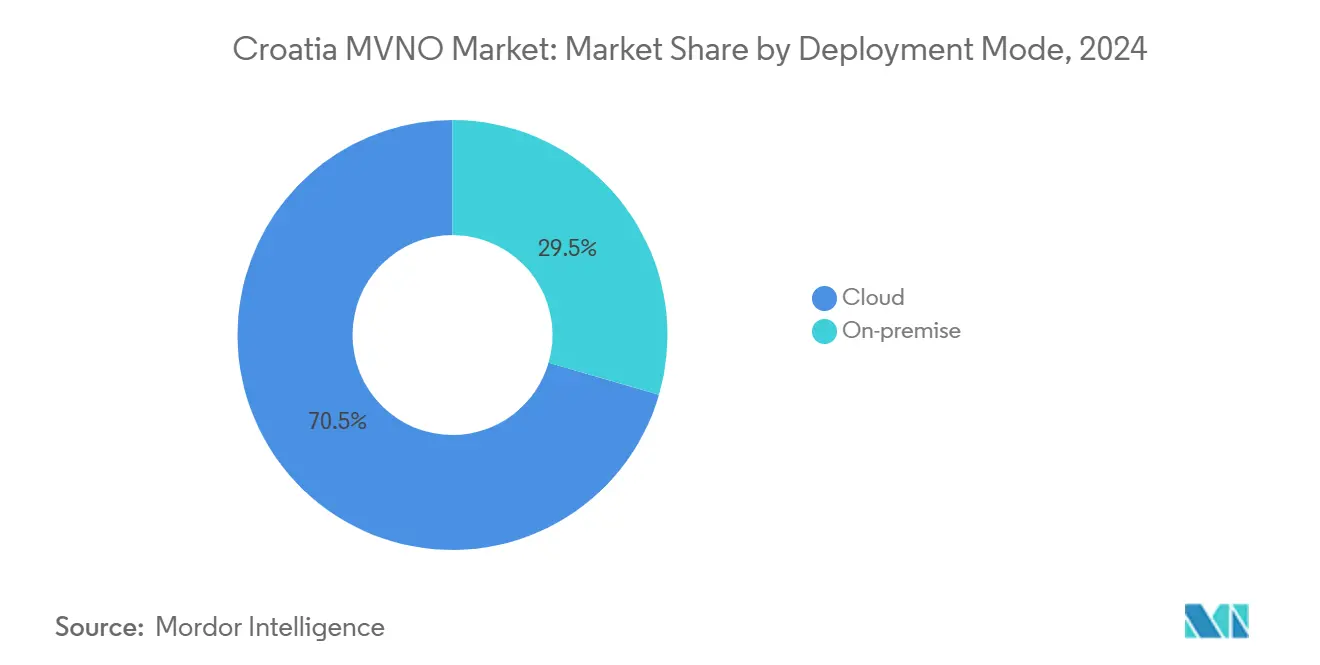

- By deployment model, cloud infrastructure held 70.51% revenue share in 2024, while cloud also recorded the fastest 10.21% CAGR through 2030.

- By operational mode, reseller and light MVNO formats captured 59.62% share in 2024, whereas full MVNO operations are projected to grow at 16.88% CAGR by 2030.

- By subscriber type, consumer connections accounted for 84.08% of the Croatia MVNO market share in 2024; IoT lines are forecast to accelerate at 25.84% CAGR to 2030.

- By application, discount services led with 41.52% of the Croatia MVNO market size in 2024, while cellular M2M posts the highest 24.20% CAGR through 2030.

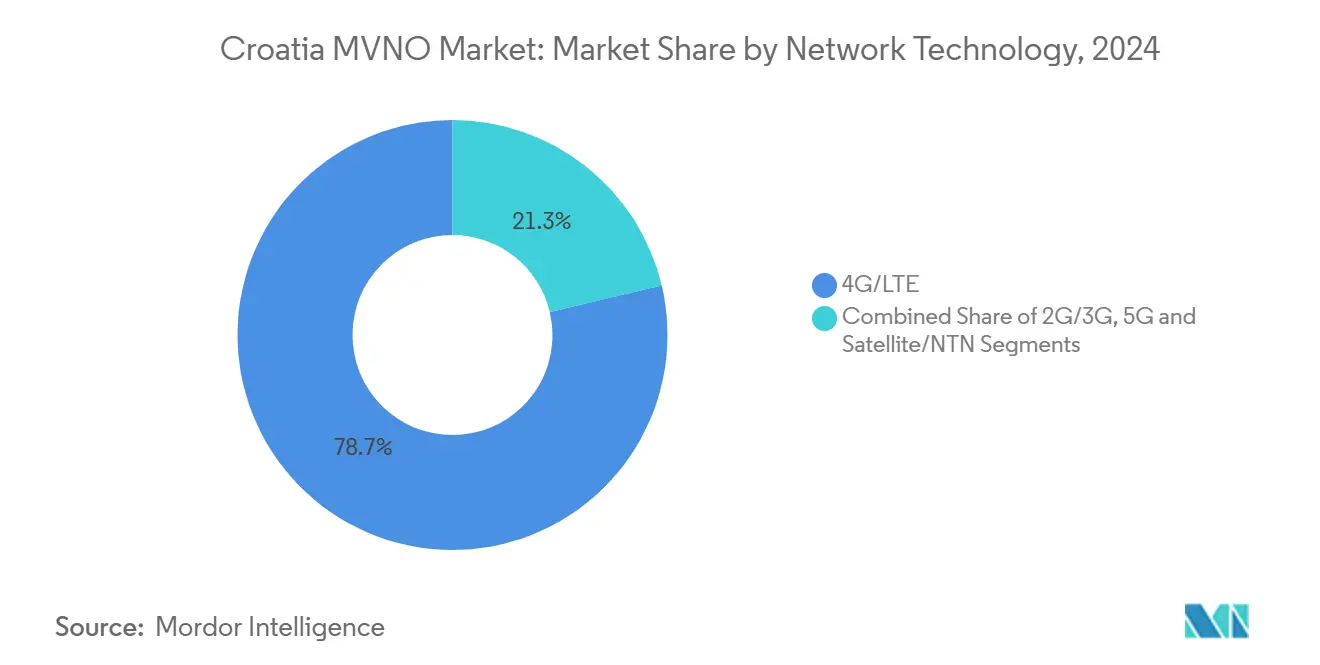

- By network technology, 4G/LTE dominated with 78.69% revenue share in 2024; satellite/NTN solutions show the fastest 46.00% CAGR to 2030.

- By distribution channel, digital-only platforms contributed 58.04% of 2024 revenue and are growing at an 8.63% CAGR to 2030.

Croatia MVNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulator-mandated wholesale access & non-discrimination | +1.2% | National; intensive in Zagreb, Split, Rijeka | Medium term (2-4 years) |

| Surge in tourist inflows demanding short-term SIM/eSIM offers | +0.9% | Coastal regions, Zagreb, islands | Short term (≤ 2 years) |

| Rapid consumer adoption of eSIM and digital onboarding | +0.8% | Urban centers, expanding to secondary cities | Medium term (2-4 years) |

| Price-sensitive migration from MNO bundles to discount brands | +0.7% | National, higher in rural and suburban areas | Short term (≤ 2 years) |

| Port & logistics IoT deployments needing private-label MVNOs | +0.5% | Port cities and logistics corridors | Long term (≥ 4 years) |

| 3G spectrum refarming unlocking QoS capacity | +0.4% | National, prioritizing urban areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulator-mandated wholesale access and non-discrimination

HAKOM’s Equivalence of Input (EoI) framework obliges Hrvatski Telekom to expose the same APIs, ordering systems, and provisioning timelines to MVNOs that its retail arm enjoys. Compliance deadlines beginning in April 2025 remove a historic bottleneck that inflated time-to-launch and service adjustments for virtual operators. Equalized back-office integration allows brands to focus on product design instead of operational firefighting, which is particularly material for niche segments such as IoT, hospitality, and on-demand tourist packages. Real-time wholesale performance monitoring further deters discriminatory practices and generates data that MVNOs can reference in negotiations. Over the medium term, access parity is forecast to add 1.2 percentage points to overall CAGR, underpinning a healthier competitive canvas for the Croatia MVNO market.

Surge in tourist inflows demanding short-term SIM/eSIM offers

Scheduled airline seats for summer 2025 stand at 14.34 million, a 7.7% jump over the prior season. Tourists combine roaming-fee avoidance with an appetite for local data bundles tuned to coastal coverage, stabilizing a high-volume prepaid base that MVNOs can serve efficiently via eSIM QR codes and app-based activation. Visa programs for digital nomads, which require monthly earnings of EUR 2,300, add a premium user stratum willing to pay for dual-country or regional packages. Seasonal demand spikes align well with MVNO wholesale contracting cycles, allowing operators to lock in capacity months ahead and monetize the influx without long-term spectrum costs. Tourism intensity consequently boosts the Croatia MVNO market by 0.9 percentage points in the near term.

Rapid consumer adoption of eSIM and digital onboarding

More than 100,000 users have downloaded the Moj Tomato self-care app, rating it 4.1 out of 5, which confirms Croatian consumers’ comfort with app-based number management A1.HR. eSIM removes the logistical hurdles of plastic SIM distribution and enables international entrants to launch Croatian offers without a domestic storefront. For existing brands, digital-only onboarding reduces acquisition cost per subscriber and accelerates upsell cycles through real-time push notifications. The trend also dovetails with EU sustainability goals, which encourage paperless, contactless services. These combined effects inject an estimated 0.8 percentage-point lift into CAGR projections for the Croatia MVNO market.

Price-sensitive migration from MNO bundles to discount brands

Inflation-indexed price escalators in legacy contracts are testing Croatian household budgets, nudging users toward stripped-down prepaid offers. MVNOs capitalize by positioning flat-rate data and voice packs devoid of entertainment tie-ins or handset subsidies. Rural zones see the highest take-up, where fiber penetration is limited and bundled entertainment holds less appeal. However, the resulting average-revenue-per-user erosion pressures operating margins, forcing MVNOs to automate customer support and rely on cloud billing stacks for scale. Still, the volume upside contributes a 0.7 percentage-point boost to the Croatia MVNO market CAGR.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High regulated wholesale charges | -0.8% | National, all MVNOs | Medium term (2-4 years) |

| Aggressive convergence bundling by MNOs | -0.6% | Urban areas, expanding to secondary cities | Short term (≤ 2 years) |

| Scarcity of mobile number prefixes | -0.4% | National | Long term (≥ 4 years) |

| EU “roam-like-home” rules reducing roaming revenue | -0.3% | Border regions, tourist corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High regulated wholesale charges

While the EoI model equalizes access, it does not cap wholesale tariffs, leaving Croatian MVNOs paying above-EU-average per-gigabyte fees. Smaller brands lack the volume to negotiate discounts, squeezing gross margins below 15% in many prepaid packages. Investment capacity for differentiated service layers—such as embedded fintech or video-streaming—therefore remains constrained. IoT-centric MVNOs find the economics even tighter, as low-ARPU sensors cannot absorb high bearer costs. Unless fee schedules ease, the drag on market growth is forecast at -0.8 percentage points over the next three years.

Aggressive convergence bundling by MNOs

Hrvatski Telekom achieved 6% top-line growth in 2024 by pushing integrated mobile, fiber, and TV bundles, raising switching costs for households. Pure-play MVNOs rarely hold fixed-line or IPTV assets, forcing them to partner or remain excluded from multiproduct tenders. In urban centers where convergence uptake is highest, discount positioning alone cannot offset the perceived value of single-bill quad-play. The tactic is expected to shave 0.6 percentage points off the Croatia MVNO market CAGR in the short term, prompting niche operators to double down on underserved verticals rather than mainstream consumer segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Adoption Reshapes Cost Curves

The cloud segment accounted for 70.51% of 2024 revenue, underscoring its pivotal role in the Croatia MVNO market. Enhanced scalability, pay-as-you-grow licensing, and rapid feature rollout drove a leading 10.21% CAGR outlook, allowing brands to align opex with volatile tourist-season usage. The Croatia MVNO market size attached to on-premise deployments remains relevant for banking, public-sector, and critical-infrastructure clients requiring controlled data residency.

Cloud-native stacks democratize advanced analytics and AI-powered care bots, once exclusive to tier-1 carriers. Implementation cycles as short as six weeks permit foreign MVNOs to test-bed Croatian offerings with minimal sunk cost. The elasticity also supports burstable capacity for summer peaks, avoiding year-round commitments. Consequently, cloud vendors such as Microsoft Azure and AWS forge turnkey MVNE alliances, intensifying competition for legacy bare-metal suppliers.

By Operational Mode: Light Infrastructure Spurs Quick Entry

Reseller and light MVNO frameworks delivered 59.62% of 2024 revenue, confirming their dominance in the Croatia MVNO market. Capital-light compliance regimes and shorter time-to-launch make these formats attractive to digital upstarts, yet full MVNOs are projected to grow at 16.88% CAGR to 2030 as maturing brands seek deeper customer control.

Service operators moving toward full core ownership gain latitude in IMS-based VoLTE, 5G slicing, and private APN provisioning. This progression elevates switching barriers and opens enterprise contract opportunities. Nevertheless, regulator-mandated interconnection tests and lawful interception requirements impose higher fixed costs, so hybrid models emerge—outsourcing network functions yet retaining policy control. The diversity of modes underscores a healthy innovation funnel within the Croatia MVNO market.

By Subscriber Type: Consumer Base Dominates; IoT Surges

Consumer lines held 84.08% revenue share in 2024 as prepaid bundles remain the default tourist connectivity choice. Conversely, IoT lines exhibit a turbocharged 25.84% CAGR forecast, positioning them as the next growth pillar for the Croatia MVNO market size. EU-funded smart-port projects and industrial automation pilots in Rijeka, Split, and Ploče ports are already requesting private APNs and network slicing.

Enterprise demand, while smaller in absolute numbers, prizes fully customizable SLAs. Cross-border trucking fleets, for instance, need flat-rated Balkan roaming, which MVNOs can deliver via multi-IMSI steering agreements. Higher penetration of industry-specific connections diversifies revenue away from price-sensitive consumer tiers and bolsters ARPU stability.

By Application: Discount Offers Lead; M2M Accelerates

Discount propositions retained 41.52% share in 2024, benefiting from transparent pricing and simplified onboarding. Yet cellular M2M is on a 24.20% CAGR course, supported by EU logistics corridors and domestic Industry 4.0 initiatives. As connectivity becomes a line item in corporate OT budgets, bundles that combine SIM management portals, predictive maintenance dashboards, and security over-the-air updates gain traction.

Business application lines target SMEs needing dependable voice and data without corporate-grade complexity. MVNOs exploit cloud CRM hooks to upsell fixed IP addresses, mobile VPNs, and device financing. Combined, these vectors hint at a gradual pivot toward value-add and away from pure-price competition in the Croatia MVNO market.

By Network Technology: 4G Maturity; Satellite Breakout

4G/LTE accounted for 78.69% of 2024 revenue as nationwide coverage and affordable terminals aligned. The Croatia MVNO market share for satellite/NTN links remains modest but its 46.00% CAGR illustrates geographic pragmatism—Croatia’s 1,200-plus islands require non-terrestrial back-haul. A1’s integration of Starlink back-haul feeds low-latency 350 Mbps bursts to shoreline villages, enabling summer pop-up kiosks.

As A1 decommissions 3G in February 2025, spectrum refarming will feed extra carriers to 4G and 5G. MVNOs gain from richer QoS profiles and may package tiered data classes for gaming or UHD streaming. While 5G SA is still metro-centric, wholesale exposure will widen in 2026, letting virtual brands experiment with network slicing for industrial IoT.

By Distribution Channel: Digital Pathways Prevail

Digital-only stores contributed 58.04% of 2024 revenue and remain the fastest-growing outlet at 8.63% CAGR. eSIM QR delivery, in-app KYC via electronic ID, and chat-bot care reduce both acquisition and support friction. Traditional retail retains utility for SIM swaps and handset financing, yet domestic postal kiosks now stock generic eSIM vouchers, blurring offline and online.

Third-party e-commerce platforms partner with MVNOs to bundle tourist insurance and data packs at booking checkout, inserting connectivity into the travel purchase path. Carrier sub-brand boutiques serve as hybrid models, where brand equity of parent MNOs attracts risk-averse shoppers while maintaining MVNO-level pricing. Digital supremacy thus anchors the future footprint of the Croatia MVNO market.

Geography Analysis

Zagreb, Split, and Rijeka jointly account for more than 55% of Croatia MVNO market transactions, leveraging dense population, university clusters, and enterprise headquarters. Coastal districts, however, command the lion’s share of prepaid data-only traffic during June–September, when airline seat capacity peaks. Consequently, MVNOs preload regional network profiles to optimize hand-over along motorway A1 and island ferries, ensuring the tourist experience matches urban benchmarks.

Islands such as Hvar and Korčula pose coverage economics that favor satellite or small-cell neutral-host deployments. MVNOs use multi-IMSI orchestration to switch traffic among host operators, reducing dead-zone complaint rates. Inland counties like Slavonia continue to emphasize voice and SMS, so discount bundles remain popular, whereas Istria, with high German and Italian visitor mix, values EU-wide flat-rate data.

EU smart-city funds channel grants into Rijeka’s port, Osijek barracks, and Dubrovnik parking sensors, driving localized IoT demand. MVNOs cooperate with municipal IT agencies to deliver secure SIM provisioning over NB-IoT, complying with GDPR data-sovereignty rules. Outside dense metros, renewable-energy farms in Lika are adopting satellite-back-hauled private APNs to monitor turbine performance, creating incremental lines for virtual operators.

Competitive Landscape

The Croatia MVNO market hosts a moderate concentration: Bonbon, Tomato, Simpa, and Lycamobile dominate prepaid tourist and migrant niches, while enterprise-oriented newcomers tackle logistics and IoT. Parent-company synergies grant Bonbon and Tomato efficient retail shelf presence and wholesale‐rate latitude, yet asset-light challengers rely on cloud MVNE partners to iterate offers in weeks instead of quarters. Regulatory oversight levels access equality, so differentiation increasingly shifts to UX, loyalty perks, and bundled fintech plug-ins.

A1’s Starlink partnership signals a defensive play against terrestrial saturation by extending reliable coverage to island campsites and marinas. Hrvatski Telekom’s CPaaS integration with Infobip automates dunning and tech-support flows, slashing opex and raising the digital-service bar competitors must meet. Tele2’s exit and rebrand under United Group (Telemach) recalibrated network-sharing agreements, creating room for specialized, region-focused MVNOs to negotiate fresh wholesale terms.

Strategic directions emphasize prepaid tourist eSIMs, dual-country packages for Balkan commuters, and private-label 5G slices for industrial clients. Successful operators focus marketing spend on digital channels, leverage referral programs with hostels and travel agencies, and use AI-driven upsell engines to cross-sell add-ons like travel insurance. Those lacking balance-sheet depth mitigate churn risk through joint promotions with ride-sharing and food-delivery apps that resonate with younger demographics.

Croatia MVNO Industry Leaders

Bonbon

Tomato

Lycamobile Croatia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: A1 Croatia shut down its 3G network, unlocking refarmed spectrum for 4G/5G wholesale access.

- January 2025: New Universal Service Regulation set minimum 14 Mbps download and EUR 29.21 price caps.

- December 2024: Hrvatski Telekom deployed Infobip CPaaS, achieving 50% automated resolution of technical inquiries.

- October 2024: HAKOM released final EoI regulations mandating equal APIs and processes for wholesale customers.

Croatia MVNO Market Report Scope

| Cloud |

| On-premise |

| Reseller |

| Service Operator |

| Full MVNO |

| Light / Brand MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online/Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party/Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller |

| Service Operator | |

| Full MVNO | |

| Light / Brand MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online/Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party/Wholesale |

Key Questions Answered in the Report

What is the current value of the Croatia MVNO market and its forecast growth?

The market is valued at USD 60 million in 2025 and is projected to reach USD 90 million by 2030, reflecting a 5.82% CAGR.

Which deployment model leads Croatian virtual networks?

Cloud-based infrastructure dominates with 70.51% 2024 share and shows the strongest 10.21% CAGR outlook.

How important is tourism to MVNO demand in Croatia?

Seasonal tourism adds 14.34 million airline seats in summer 2025, driving high prepaid eSIM demand along the coast and islands.

Which application segment is expanding fastest?

Cellular M2M lines, linked to logistics and smart-city projects, are growing at 24.20% CAGR through 2030.

What technology trend will most disrupt coverage gaps?

Satellite/NTN integration, led by A1’s Starlink partnership, is forecast at a 46% CAGR as operators extend service to island territories.

How does regulation influence MVNO competition?

HAKOM’s Equivalence of Input rules enforce identical wholesale APIs and processes, leveling the field for new entrants.

Page last updated on: