UAE Indoor Farming Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

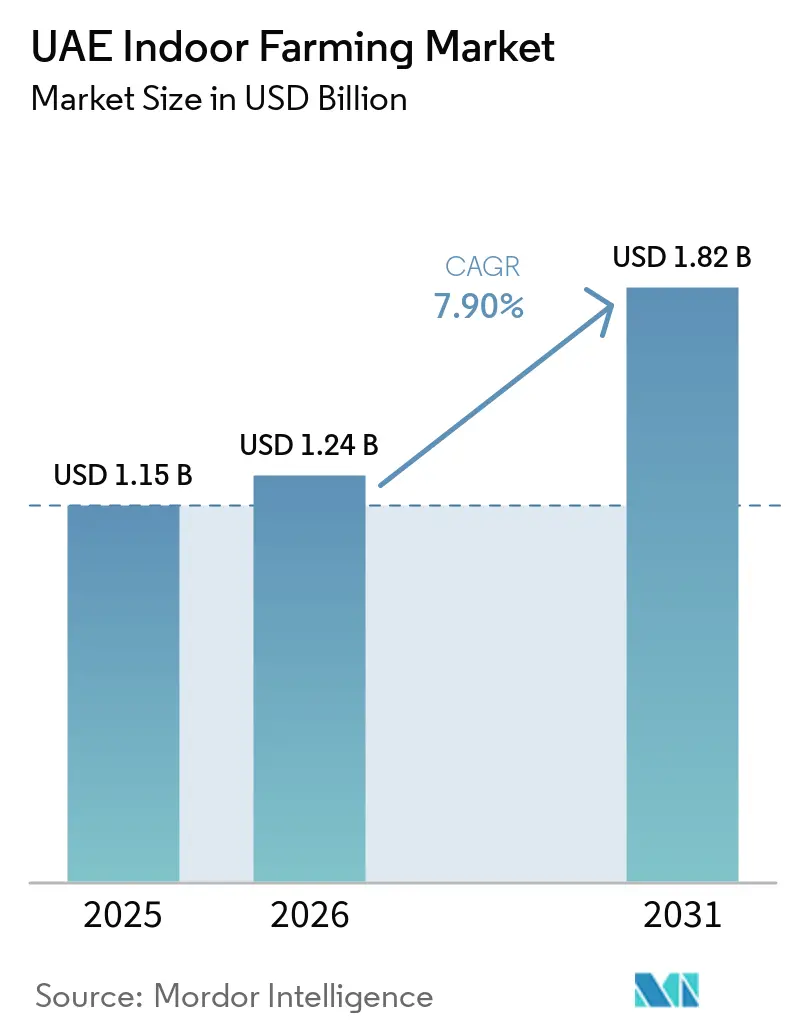

| Base Year Market Size (2025) | USD 1.15 Billion |

| Market Size (2026) | USD 1.24 Billion |

| Market Size (2031) | USD 1.82 Billion |

| Growth Rate (2026 - 2031) | 7.90% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Indoor Farming Market Analysis by Mordor Intelligence

The UAE indoor farming market size was valued at USD 1.15 billion in 2025 and is estimated to grow from USD 1.24 billion in 2026 to reach USD 1.82 billion by 2031, at a CAGR of 7.90% during the forecast period (2026-2031). The UAE indoor farming market continues to expand because the national food security policy now treats controlled-environment agriculture as a core domestic production tool rather than a niche farming format. The October 2024 Plant the Emirates campaign strengthened that direction by creating a national center for domestic farming and setting a 20% growth target for agricultural output over five years, which provides indoor farming operators with a more stable, long-term demand base[1] Source: Daniel Bardsley, “How Plant the Emirates Is Part of a Wider Strategy to Strengthen Food Security,” The National, thenationalnews.com . The UAE indoor farming market also benefits from public and quasi-public project platforms in Dubai and Abu Dhabi, where new research hubs, smart greenhouse assets, and food production clusters are lowering commercialization risk for larger operators.

Key Report Takeaways

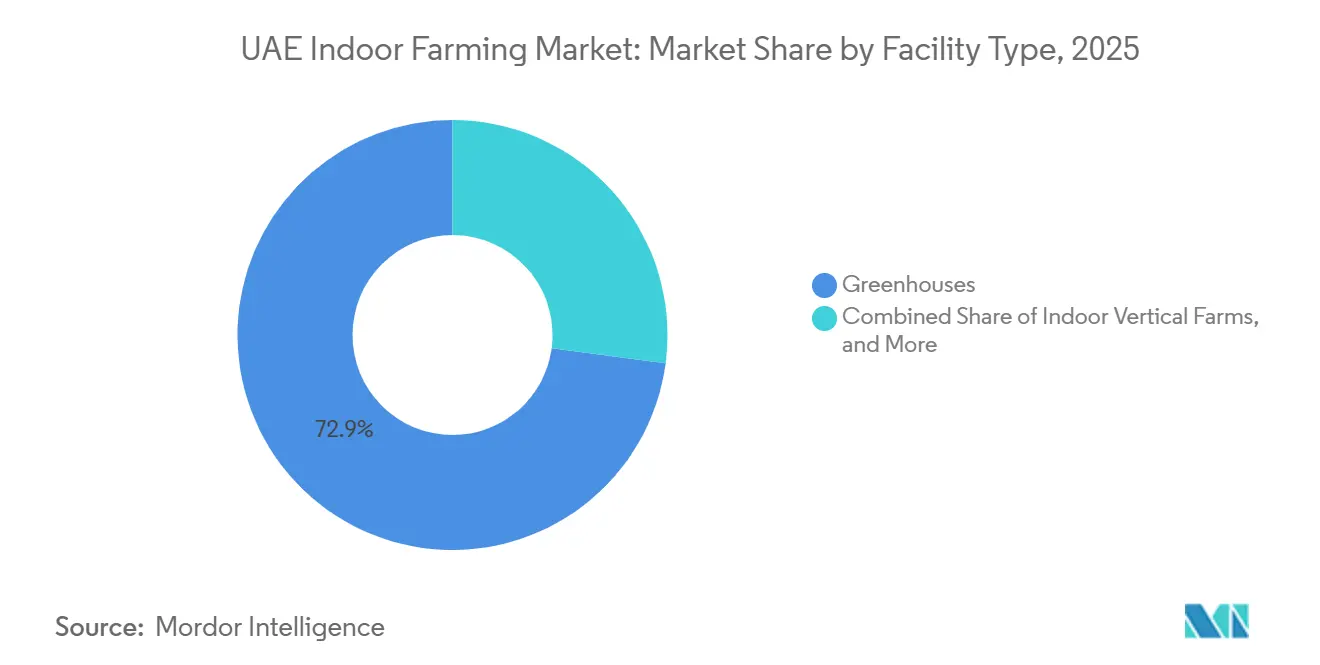

- By facility type, greenhouses accounted for the largest share of the UAE indoor farming market in 2025, at 72.9%, while indoor vertical farms were the fastest-growing facility type and are forecast to expand at a 14.0% CAGR through 2026 to 2031.

- By growing mechanism, hydroponics accounted for the largest segment, 61% of the UAE indoor farming market size in 2025, while aeroponics is the fastest-growing segment, projected to grow at an 11.0% CAGR through 2026 to 2031.

- By crop category, fruits and vegetables accounted for the largest share of the UAE indoor farming market in 2025, at 84%, while flowers and ornamentals are the fastest-growing crop, forecast to expand at a 13.5% CAGR through 2026 to 2031.

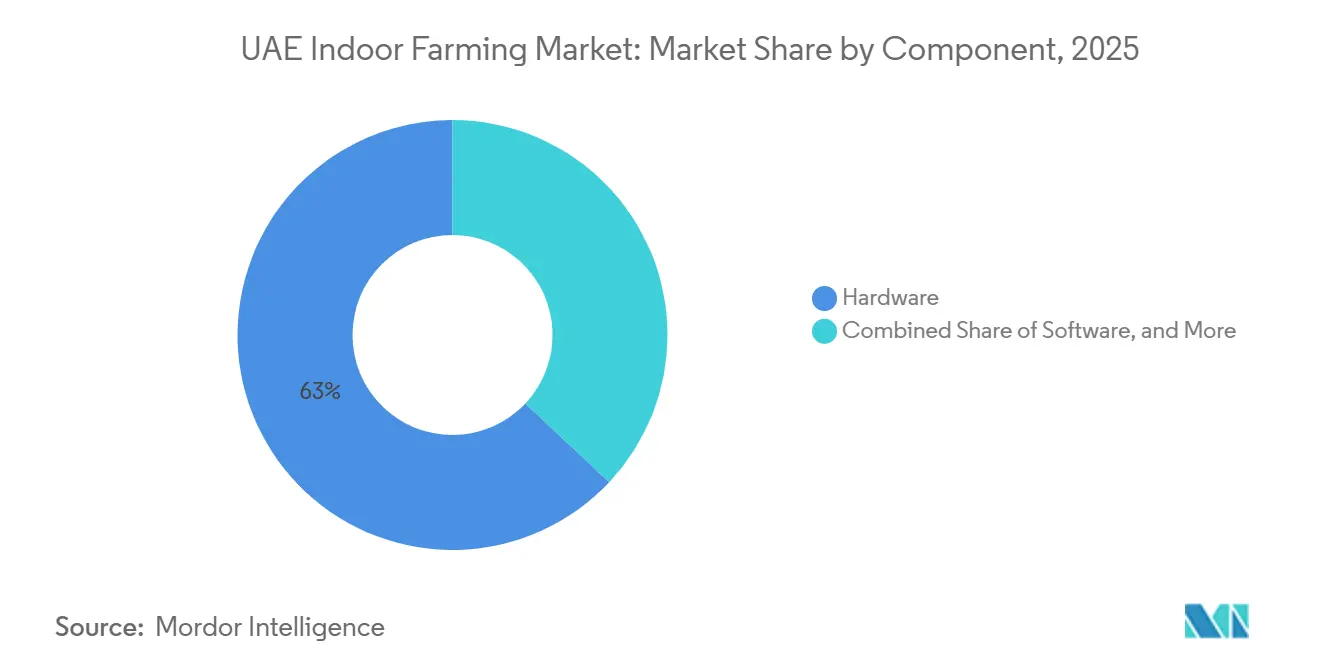

- By component, hardware accounted for the largest component, 63% of the UAE indoor farming market in 2025, while software is the fastest-growing component, projected to grow at an 11.2% CAGR through 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

UAE Indoor Farming Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Food import substitution and food security mandate | +1.8% | UAE-wide, with highest urgency in Abu Dhabi and Dubai institutional supply chains | Medium term (2-4 years) |

| Water-efficient local production in extreme climate | +1.5% | UAE-wide, highest intensity in Al Ain, Al Dhafra, and inland production zones | Long term (≥ 4 years) |

| Premium demand for fresh local pesticide-free produce | +1.2% | Dubai and Abu Dhabi City retail and hospitality corridors | Short term (≤ 2 years) |

| Large-scale public and quasi-public agritech incentives | +1.4% | Abu Dhabi and Dubai | Medium term (2-4 years) |

| Public procurement targets for local fresh produce | +1.0% | UAE-wide, with strongest leverage in Dubai and Abu Dhabi institutional buyer networks | Long term (≥ 4 years) |

| Clustered infrastructure in Food Tech Valley and Al Ain agritech hubs | +0.8% | Dubai, Al Ain, and Al Dhafra corridor | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Food Import Substitution and Food Security Mandate

The UAE indoor farming market is supported by a food security framework that places domestic fresh produce capacity inside a national resilience agenda rather than a purely commercial one. The National Food Security Strategy 2051 identifies controlled-environment agriculture as a core production instrument and links it to the country’s long-term food access goals[2]Source: Abu Dhabi Agriculture and Food Safety Authority, “Innovation and Development,” ADAFSA, adafsa.gov.ae. Agriculture and Food Safety Authority (ADAFSA) also expanded the supply-side foundation in 2024, with 1,530 farms certified under Abu Dhabi Good Agricultural Practices, strengthening the pool of traceable suppliers available to institutional buyers. This policy setting provides indoor farms with closer access to public procurement and strategic sourcing channels, reducing revenue uncertainty for operators that meet compliance standards.

Water-Efficient Local Production in Extreme Climate

The UAE indoor farming market is also driven by the value of water efficiency in a desert climate where freshwater supply remains structurally constrained. Bustanica states that controlled hydroponic production can use 95% less water than conventional agriculture, which gives indoor systems a clear operating advantage in the local resource setting. Agriculture and Food Safety Authority (ADAFSA) innovation work at Kuwiatat Research Station in Al Ain has focused on closed hydroponic water reuse with Korea’s Rural Development Administration, showing that water recycling is now part of practical technology adaptation for UAE conditions. The value of this efficiency extends beyond crop output, as lower water demand also reduces pressure on desalination-related infrastructure. That makes water-smart indoor farming more relevant over time in inland production zones where long-term agricultural planning must account for both climate and utility constraints.

Premium Demand for Fresh Local Pesticide-Free Produce

The UAE indoor farming market benefits from rising demand for local produce that offers freshness, consistency, and a pesticide-free positioning in premium retail and food service channels. Bustanica’s production model is built around pesticide-free leafy greens, and the company has steadily widened its commercial reach beyond airline meals into retail and quick-commerce channels. In February 2025, Bustanica partnered with Careem to expand delivery access across Dubai and Abu Dhabi, which shows that local indoor produce is moving closer to everyday household demand. This creates a favorable environment for operators to pair reliable year-round output with product quality that aligns with premium urban consumption habits.

Large-Scale Public and Quasi-Public Agritech Incentives

The UAE indoor farming market is being shaped by public and quasi-public support platforms that reduce the risk of scaling new facilities. In November 2024, Food Tech Valley formalized strategic partnerships and procurement arrangements with private operators, including Badia Farms, Spinneys, and Golden Leaf Farm, while Emirates Development Bank aligned technology adoption support with the National Food Security Strategy 2051. These platforms matter because they shorten the path from pilot projects to commercial deployment for operators that need land access, technical support, and buyer connectivity simultaneously.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital intensity for climate-controlled assets | -1.5% | UAE-wide, most acute for new entrants in Sharjah, Ras Al Khaimah, and outer emirates | Long term (≥ 4 years) |

| Cooling and lighting costs pressure unit economics | -1.2% | UAE-wide, structurally higher in inland zones versus coastal locations | Medium term (2-4 years) |

| Tight traceability and packing compliance raise scale-up costs | -0.7% | Abu Dhabi, with partial spillover to Dubai through unified food safety standards | Short term (≤ 2 years) |

| Crop economics remain narrow outside leafy greens, selected berries, and tomatoes | -0.9% | UAE-wide, the most constraining for operators attempting diversified crop portfolios | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Intensity for Climate-Controlled Assets

Large indoor farming assets in the UAE still require heavy upfront investment, which limits the field of operators that can scale quickly. In 2024, the Plenty Unlimited and Mawarid joint venture’s first Abu Dhabi strawberry facility alone carries an investment of more than AED 500 million (USD 136 million), underscoring the capital required before revenue begins[3]Source: “Plenty and Mawarid Launch Regional Partnership to Grow Fresh Produce in GCC,” PR Newswire, prnewswire.com . This creates a clear divide between projects backed by sovereign, institutional, or corporate capital and smaller operators that must stay within narrow formats. High capital intensity also increases the risk of slower expansion if funding conditions become less favorable or public priorities shift to adjacent agricultural programs. That constraint is most visible outside the main Abu Dhabi and Dubai corridors, where ecosystem support is still thinner.

Cooling and Lighting Costs Pressure Unit Economics

Cooling and lighting remain a structural cost burden for the UAE indoor farming market because production must run through very high ambient temperatures for much of the year. A 2024 engineering study on controlled-environment lettuce production in the GCC estimated energy demand at 22.68 kWh per 150 grams of produce, with HVAC cooling accounting for 30% of the load, in addition to LED energy use. This puts fully enclosed vertical systems under more pressure than climate-assisted greenhouses when operators try to widen crop portfolios. Until energy-saving design becomes standard across more projects, unit economics will remain tighter for farms with the heaviest reliance on artificial lighting and cooling.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Facility Type: Greenhouse Dominance Anchors Revenue While New Formats Emerge

Greenhouses were to hold the largest share, accounting for 72.9% of the UAE indoor farming market in 2025. This dominance is attributed to their suitability for year-round production and lower energy requirements compared to fully enclosed vertical farms. Glass and poly greenhouse systems enable scalable production of crops such as tomatoes, cucumbers, berries, and leafy greens, offering a more balanced cost structure. An example of this model is Pure Harvest Smart Farms, which operates multi-hectare climate-controlled campuses to supply fruits and vegetables at volumes that compete effectively with imports.

Indoor vertical farms are the fastest-growing facility type, projected to grow at a compound annual growth rate (CAGR) of 14.0% from 2026 to 2031. These farms currently constitute the second-largest facility base, driven by prominent projects such as Bustanica in Dubai. Container farms and indoor deep-water culture systems cater to smaller deployment needs, particularly in scenarios where land availability, rapid setup, or project flexibility take precedence over large-scale operations. The UAE indoor farming market is experiencing accelerated growth in non-greenhouse facility types, notably warehouse vertical farms and hybrid systems under development. In November 2024, construction commenced on the GigaFarm project at Dubai Food Tech Valley, a 900,000-square-foot closed-loop facility poised to become one of the largest vertical farming projects in the country upon completion.

By Growing Mechanism: Hydroponics Leads Revenue While Aeroponics Gains Speed

Hydroponics holds the largest share, accounting for 61% of the UAE indoor farming market in 2025, making it the leading growth mechanism. Its position reflects long commercial use in leafy greens, tomatoes, and cucumbers, along with deeper supplier familiarity in Abu Dhabi and Dubai. Recirculating nutrient delivery remains well-suited to arid conditions, where reliability and water control are central to farm performance. The hydroponic base is also reinforced by major operating references such as Bustanica and Armela Farms. Aquaponics remained a niche but closely watched option because it links fish and produce in a closed-loop system.

Aeroponics is the fastest-growing segment, with the UAE indoor farming market for this segment projected to expand at a 11.0% CAGR from 2026 to 2031. The appeal comes from stronger water efficiency and better alignment with premium crops such as strawberries and selected herbs. Institutional interest in berry cultivation and indoor specialty crops is helping move aeroponics from trial work toward broader commercial use. At the same time, solar-integrated protected agriculture projects in Al Ain are showing that mechanism choice is increasingly tied to energy design and crop science. This keeps hydroponics dominant today, while giving aeroponics the stronger growth runway through the forecast period.

By Crop Category: Core Produce Holds Volume While Berries Lift Growth

Fruits and vegetables accounted for the largest share of the UAE indoor farming market in 2025, at 84%, underscoring the sector's concentration in high-turnover perishables. Tomatoes also gained ground as indoor production moved into larger commercial formats. In April 2026, UNS Vertical Farms commissioned a 10,000-square-meter facility in Al Ain, targeting 150,000 kilograms of cherry and bunch tomatoes annually, which confirms tomatoes as a more established expansion category. Herbs and microgreens continued to serve premium retail and hospitality channels where freshness and delivery speed support stronger pricing.

Flowers and ornamentals represent the fastest-growing crop category, projected to grow at a compound annual growth rate (CAGR) of 13.5% from 2026 to 2031. Flowers and ornamentals held a small but stable position, mainly tied to hospitality and events demand in Dubai and Abu Dhabi. Other high-value categories, including mushrooms and seedling propagation, remain early-stage opportunities rather than core revenue drivers. This leaves the UAE indoor farming industry focused on a practical balance between proven volume crops and selective premium diversification.

By Component: Hardware Still Leads While Software Moves Up the Value Stack

Hardware captured the largest segment, 63% of the UAE indoor farming market size in 2025, giving it the largest component position across the UAE indoor farming market. This reflects the capital-heavy buildout of greenhouses, vertical farms, cooling systems, lighting rigs, and sensor networks. Climate control equipment remained one of the largest spending lines because UAE facilities must manage heat loads year-round. LED lighting also remained a major investment area as operators upgraded systems to improve power efficiency and crop control. Sensors and monitoring devices grew in importance as precision management became standard on newer sites.

Software is the fastest-growing component segment, with an 11.2% CAGR projected from 2026 to 2031. As the installed base expands, operators are shifting more attention toward yield optimization, workflow control, and AI-assisted decision tools rather than only adding physical equipment. Bustanica’s use of machine learning and proprietary growing algorithms shows how software is becoming a practical operating differentiator in the UAE indoor farming market. Services remain the smallest segment, but they are rising steadily as smaller farms outsource integration, agronomy, and system support. That pattern suggests the UAE indoor farming industry is moving from a pure asset buildout phase into a more data-led efficiency phase.

Geography Analysis

Dubai leads the UAE indoor farming market, driven by strong demand from retail, hospitality, and airline catering sectors. The presence of Bustanica, which produces over 1 million kilograms of leafy greens annually at its 330,000-square-foot facility near Al Maktoum International Airport, further solidifies its position. By 2026, Bustanica plans to expand into ready-to-eat salads, soups, juices, and strawberries, broadening Dubai’s role beyond leafy greens production. Additionally, Al Ain is emerging as a significant agricultural innovation hub in the UAE indoor farming market, supported by its traditional farming base, its relatively moderate climate compared to coastal emirates, and increasing institutional support.

Abu Dhabi is positioning itself as the most policy-driven growth center in the UAE indoor farming market. In May 2025, Silal and China’s SVG launched a 100,000-square-meter smart agritech hub in Al Ain, backed by an AED 120 million (USD 32.7 million) investment. The Plenty and Mawarid strawberry facility, anticipated to be completed by late 2026, will introduce a premium crop anchor, potentially reducing the emirate gap over time. Abu Dhabi is increasingly focusing on high-tech greenhouse cultivation, hydroponics, and research-driven agritech initiatives aimed at enhancing water efficiency and crop resilience. Investments in smart farming zones and food security initiatives are attracting both local and international operators to Al Ain, offering scalable production environments outside major urban centers.

Sharjah, Ajman, Ras Al Khaimah, Fujairah, and Umm Al Quwain represent the emerging tier of the UAE indoor farming market. Among these, Sharjah is the most commercially active, with specialty crops and controlled-environment farming concepts gaining traction in smaller-scale applications. Ras Al Khaimah is drawing early-stage operators due to its lower land costs and expanding industrial base. Fujairah and Umm Al Quwain remain in the early stages of development, with infrastructure limitations and distance from major demand centers hindering immediate growth. Improved cold-chain logistics and national support measures are anticipated to gradually increase operator presence across these emirates over time.

Competitive Landscape

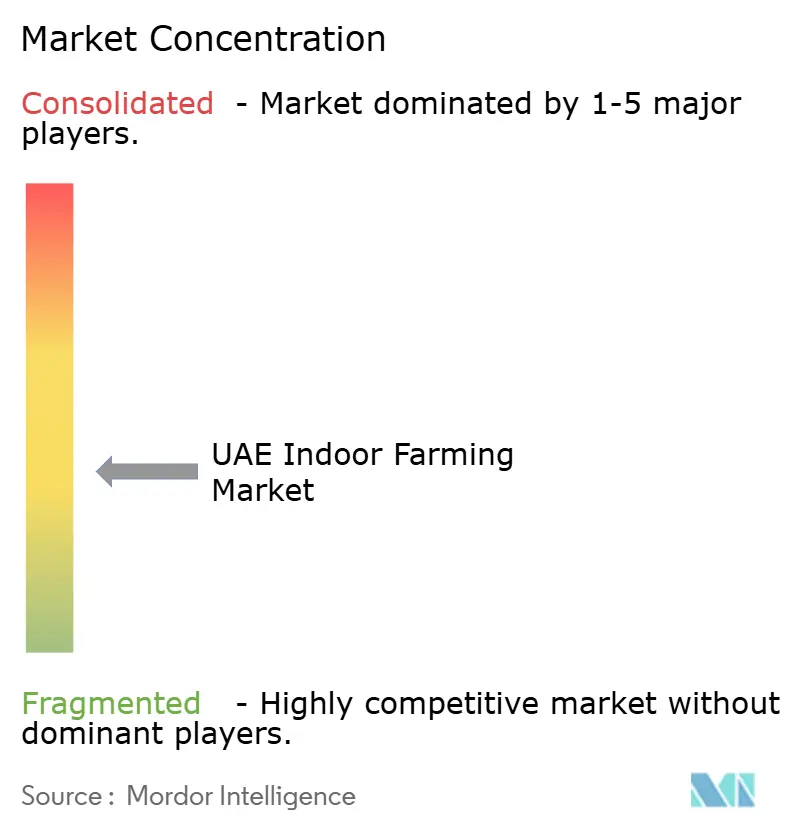

The UAE indoor farming market is moderately fragmented, with the top five players, including Pure Harvest Smart Farms, Armela Farms, Emirates Flight Catering Company L.L.C., UNS Farms, and Madar Farms, accounting for a significant combined market share. This structure reflects the breadth of facility models, crop priorities, and emirate-level operating environments rather than weak commercial traction. In practice, many operators compete in adjacent niches instead of directly chasing the same customer base.

Recent strategic moves show how competition is evolving inside the UAE indoor farming market. Emirates Flight Catering fully acquired Bustanica in February 2024, which gave the group full control of one of the country’s best-known large-scale vertical farming assets. Pure Harvest and PlanTFarm opened an AI-powered integrated facility in Al Ain in February 2025, signaling a hybrid model that blends greenhouse economics with vertical production capabilities. These moves show a market where scale, crop specialization, and technology design are becoming increasingly important.

Opportunities remain strongest in mushrooms, seedling propagation, aquaponic systems, and managed software services for growers that need technical support without building full in-house teams. The GigaFarm project’s planned seedling supply role for the UAE’s operational farms also points to downstream service opportunities beyond direct produce sales. Smaller players such as Smart Acres, Greener Crop, and Iyris continue to occupy narrower crop or geography positions that the largest operators have not fully targeted. This keeps the UAE indoor farming market open to specialized entrants even as better-funded platforms capture the largest project announcements.

UAE Indoor Farming Industry Leaders

Pure Harvest Smart Farms

Armela Farms

Emirates Flight Catering Company L.L.C.

UNS Farms

Madar Farms

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: UNS Vertical Farms (part of Speedex Group) launched a 10,000-square-meter controlled-environment tomato facility in Al Ain targeting approximately 150,000 kilograms of cherry and bunch tomatoes annually, marking the company's entry into large-format fruiting crop production and expanding its UAE footprint beyond its core Dubai microgreens and leafy greens operation

- May 2025: Silal and China's Shouguang Vegetable Industry Group (SVG) signed a strategic agreement witnessed by UAE Ministers to establish a 100,000-square-meter smart agritech hub in Al Ain with an SVG investment of over AED 120 million (USD 32.7 million), incorporating AI and robotics, intelligent photovoltaic glass greenhouses, and solar-powered operations designed to reduce water and fertilizer use by up to 30%

- February 2024: Emirates Flight Catering fully acquired Emirates Bustanica, making the world's largest indoor vertical farm a 100% UAE-owned entity, consolidating control over the 330,000-square-foot Dubai facility that produces over 1 million kilograms of leafy greens annually using 95% less water than conventional agriculture.

UAE Indoor Farming Market Report Scope

Indoor farming involves cultivating crops in controlled environments, such as greenhouses, warehouses, shipping containers, or purpose-built indoor facilities. The UAE Indoor Farming Market Report is Segmented by Facility Type (Greenhouses, Indoor Vertical Farms, Plant Factories, Indoor Aquaponics Farms, and More), by Growing System (Hydroponics, Aquaponics, Aeroponics, Soil-Based Controlled Environment Systems, and Hybrid Systems), by Crop Type (Fruits and Vegetables, and More), and by Component (Hardware, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Greenhouses | Low-tech Greenhouses |

| Mid-tech Evaporatively Cooled Greenhouses | |

| High-tech Climate-controlled Greenhouses | |

| Indoor Vertical Farms | Building-based Vertical Farms |

| Container-based Vertical Farms | |

| Plant Factories | |

| Indoor Aquaponics Farms | |

| Mushroom Growing Chambers |

| Hydroponics | Nutrient Film Technique |

| Deep Water Culture | |

| Dutch Bucket and Drip Systems | |

| Ebb and Flow Systems | |

| Aquaponics | |

| Aeroponics | |

| Soil-based Controlled Environment Systems | |

| Hybrid Systems |

| Leafy Greens |

| Herbs and Microgreens |

| Fruits and Vegetables |

| Seedlings and Nursery Crops |

| Flowers and Ornamentals |

| Hardware |

| Software |

| Services |

| By Facility Type | Greenhouses | Low-tech Greenhouses |

| Mid-tech Evaporatively Cooled Greenhouses | ||

| High-tech Climate-controlled Greenhouses | ||

| Indoor Vertical Farms | Building-based Vertical Farms | |

| Container-based Vertical Farms | ||

| Plant Factories | ||

| Indoor Aquaponics Farms | ||

| Mushroom Growing Chambers | ||

| By Growing System | Hydroponics | Nutrient Film Technique |

| Deep Water Culture | ||

| Dutch Bucket and Drip Systems | ||

| Ebb and Flow Systems | ||

| Aquaponics | ||

| Aeroponics | ||

| Soil-based Controlled Environment Systems | ||

| Hybrid Systems | ||

| By Crop Type | Leafy Greens | |

| Herbs and Microgreens | ||

| Fruits and Vegetables | ||

| Seedlings and Nursery Crops | ||

| Flowers and Ornamentals | ||

| By Component | Hardware | |

| Software | ||

| Services | ||

Key Questions Answered in the Report

What is the current size of the UAE indoor farming market?

The UAE indoor farming market size was USD 1.15 billion in 2025 and is estimated to grow from USD 1.24 million in 2026 to reach USD 1.82 million by 2031, at a CAGR of 7.9% during the forecast period (2026-2031).

Which facility type generates the most revenue in the UAE indoor farming space?

Greenhouses led with 72.9% of revenue in 2025 because they offer a better balance between scale and energy use in the local climate.

Which growing mechanism is expanding the fastest in the UAE?

Aeroponics is the fastest-growing mechanism, with an 11.0% CAGR projected from 2026 to 2031, while hydroponics remains the largest segment.

Which crop category has the strongest growth outlook?

Flowers and ornamentals are forecast to grow at a 13.5% CAGR through 2031, while fruits, vegetables, and herbs still account for the bulk of revenue.

Page last updated on: