Middle East And Africa Indoor Farming Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

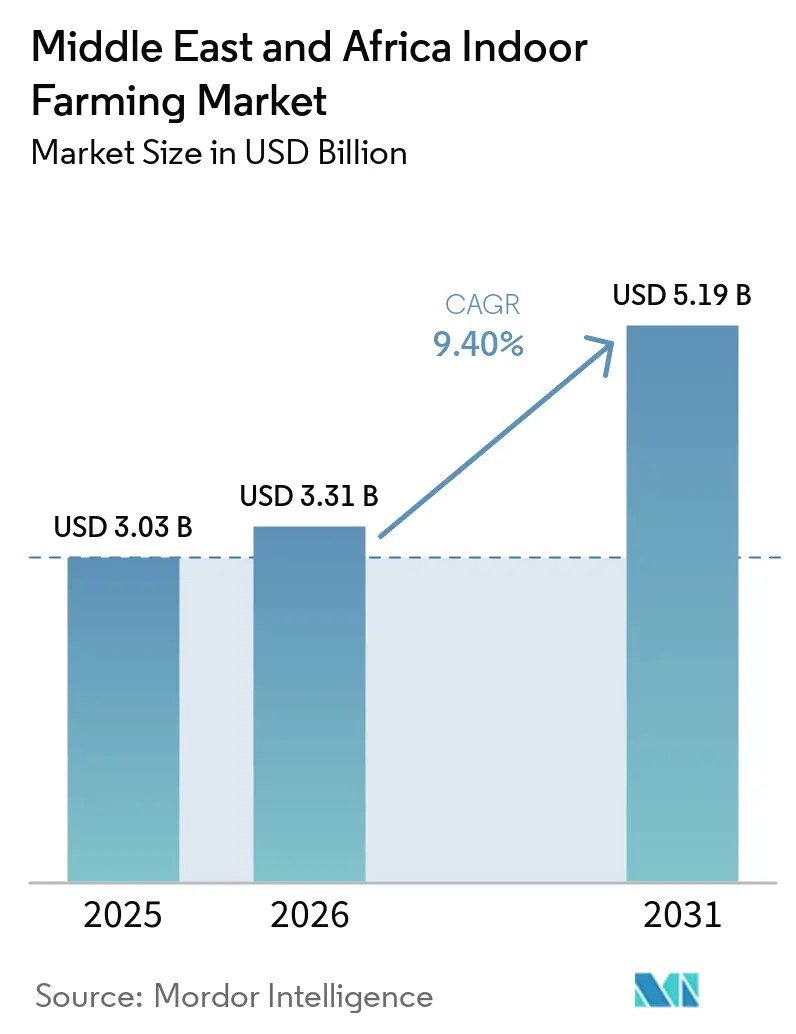

| Base Year Market Size (2025) | USD 3.03 Billion |

| Market Size (2026) | USD 3.31 Billion |

| Market Size (2031) | USD 5.19 Billion |

| Growth Rate (2026 - 2031) | 9.40% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Indoor Farming Market Analysis by Mordor Intelligence

The Middle East and Africa Indoor Farming Market size is projected to expand from USD 3.03 billion in 2025 and USD 3.31 billion in 2026 to USD 5.19 billion by 2031, registering a CAGR of 9.40% between 2026 and 2031. The market's growth is primarily driven by long-term food security initiatives rather than small-scale pilot projects, as challenges such as water scarcity, limited arable land, and supply chain vulnerabilities exert pressure on traditional agriculture in the region. Governments are actively promoting controlled-environment agriculture through policies aimed at sustainable local food production and the adoption of advanced farming technologies. Additionally, consumer demand for locally grown produce and the need for robust domestic food supply chains are contributing to market growth. However, high operational costs associated with cooling systems, electricity use, and imported equipment remain significant barriers to entry, favoring larger, financially stronger operators in the market.

Key Report Takeaways

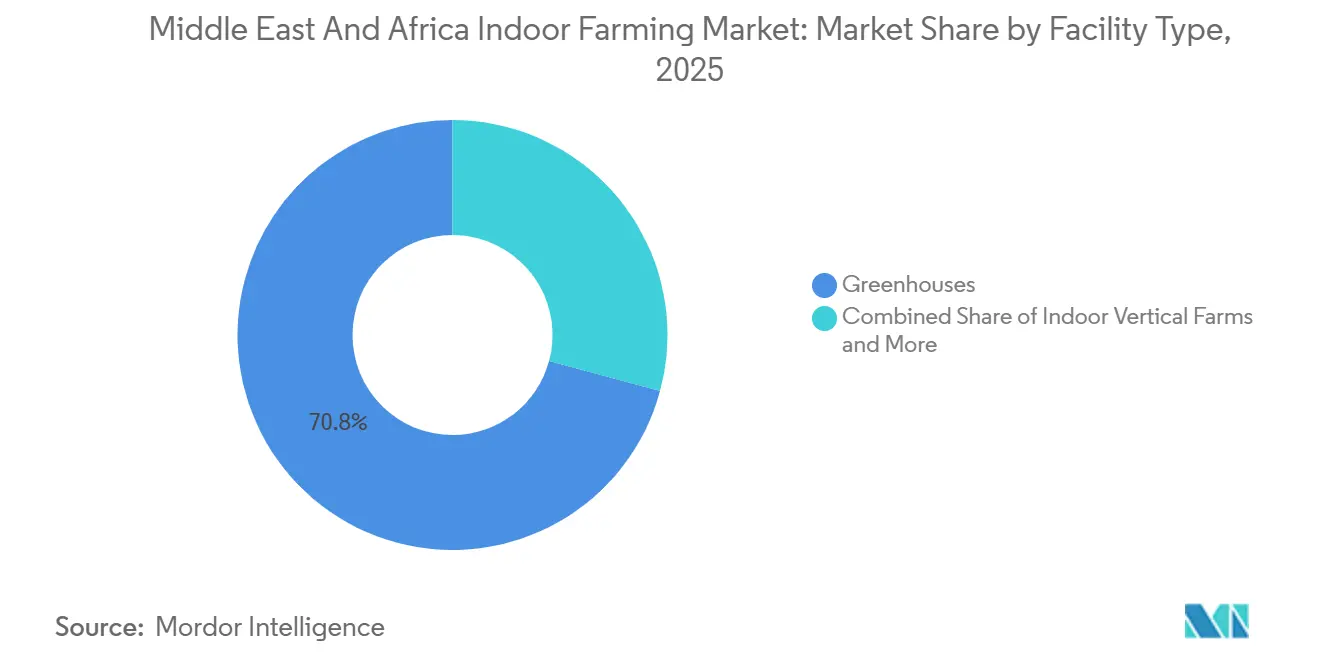

- By facility type, the Middle East and Africa indoor farming market for the greenhouse segment held the largest 70.8% in 2025, while the Middle East and Africa indoor farming market size for the container farms segment is forecast to grow at the fastest CAGR of 12.8% from 2026 to 2031.

- By growing system, hydroponics led with the largest 59.8% in 2025, while aeroponics is projected to grow at the fastest CAGR of 15.6% from 2026 to 2031.

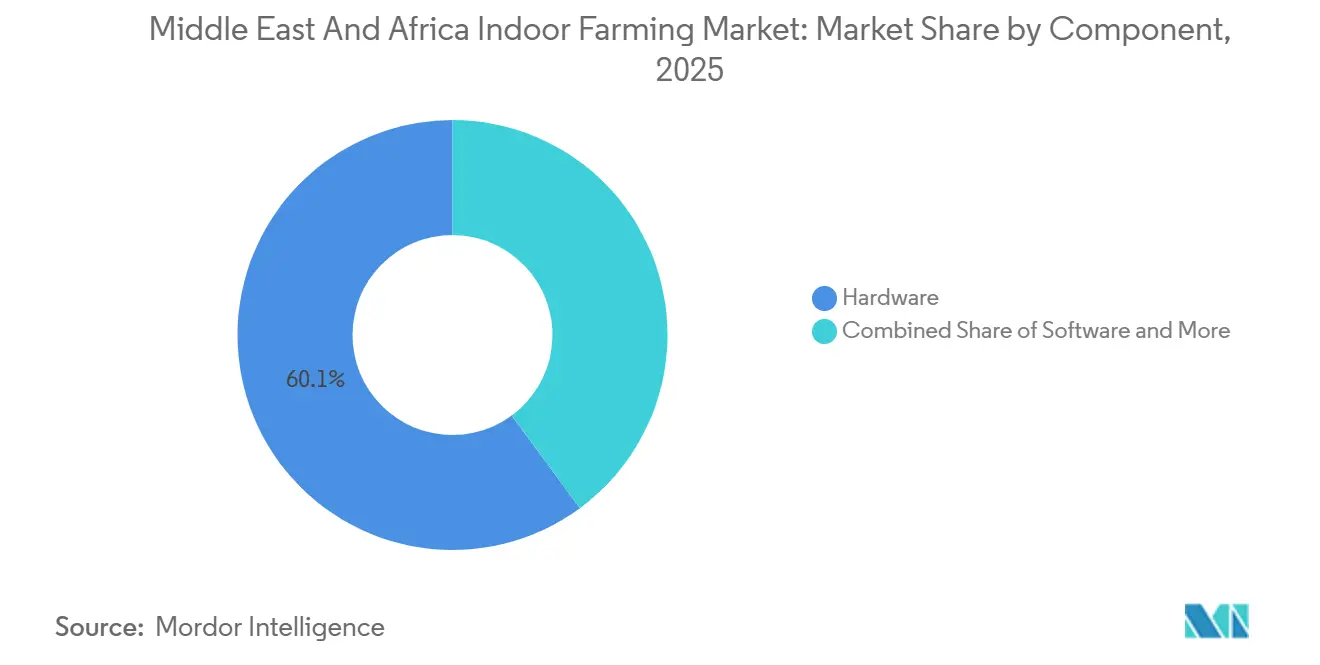

- By component, hardware accounted for the largest 60.1% in 2025, while software is forecast to grow at the fastest 12.0% CAGR from 2026 to 2031.

- By crop type, fruits, vegetables, and herbs accounted for the largest 47.4% share in 2025, while flowers and ornamentals are forecast to grow at the fastest CAGR of 10.2% from 2026 to 2031.

- The United Arab Emirates held the largest 32.6% of the regional market revenue in 2025, while South Africa is projected to grow at the fastest CAGR of 9.0% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East And Africa Indoor Farming Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Water scarcity and arable-land constraints | +2.0% | Global, most acute across Gulf Cooperation Council (GCC) core and North Africa | Long term (≥ 4 years) |

| Food-security and import-substitution programs | +2.3% | UAE and Saudi Arabia primary, with spillover to Egypt and Kenya | Short term (≤ 2 years) |

| Demand for local fresh pesticide-residue-free produce | +1.5% | UAE, Saudi Arabia, and South Africa | Medium term (2-4 years) |

| AI, IoT, LED, and automation gains | +1.8% | UAE primary, scaling across GCC and South Africa | Medium term (2-4 years) |

| Sovereign-wealth-backed agritech expansion | +2.0% | UAE and Saudi Arabia, concentrated in Abu Dhabi and Riyadh | Short term (≤ 2 years) |

| Utility-tariff support and arid-climate research localization | +0.7% | UAE and Saudi Arabia, early stage in East Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Water Scarcity and Arable-Land Constraints

Water scarcity significantly drives the indoor farming market in the Middle East and Africa. With limited arable land and minimal freshwater resources, the region increasingly turns to resource-efficient food production systems. This shift has spurred investments in hydroponics and controlled-environment agriculture, particularly in Gulf economies. A 2025 study highlighted in "Solar-Powered RO–Hydroponic Net House" showcased the economic benefits: a solar-powered reverse osmosis system for hydroponic tomato farming generated irrigation-grade water at USD 1.05/m³. In contrast, conventional utility supplies ranged from USD 2.52 to 3.20/m³, marking a 58–68% reduction in water costs. Such economic and resource efficiencies are propelling the adoption of indoor farming, bolstering food security and agricultural sustainability in the region.

Food-Security and Import-Substitution Programs

Food security and import substitution programs are emerging as significant growth drivers for the indoor farming market in the Middle East and Africa. Governments are increasingly focusing on domestic agricultural production to reduce dependence on food imports. Policies promoting controlled-environment agriculture, greenhouse expansion, and localized supply chains are fostering investments in advanced farming technologies across the region. This trend is particularly evident in the United Arab Emirates (UAE), where the National Food Security Strategy 2051 emphasizes sustainable domestic food production and modern agricultural technologies as critical priorities for enhancing long-term food resilience[1]Source: US-UAE Business Council, “Food and Agriculture Sector Update,” usuaebusiness.org. Such policy initiatives are improving access to financing, infrastructure development, and commercial confidence in indoor farming projects throughout the region.

Demand for Local Fresh Pesticide-Residue-Free Produce

In the Middle East and Africa, a burgeoning indoor farming market is responding to an escalating demand for fresh, locally sourced, and pesticide-free produce. This demand surge is particularly evident in the upscale urban retail and hospitality sectors. Modern consumers prioritize produce with traceability, consistent quality, and shorter supply chains. This evolving preference is driving investments in controlled-environment agriculture. A prime illustration of this trend is seen in the United Arab Emirates. The National Food Security Strategy has ambitiously targeted a 30% reduction in food imports by 2030[2]Source: AgriNext Conference, “UAE Agriculture Policy 2025: Innovation, Sustainability and Food Security,” agrinextcon.com.. Realizing this ambition relies heavily on amplifying investments in advanced agricultural technologies, including hydroponics, vertical farming, and other controlled-environment systems. Such progressive moves are not only strengthening local fresh-food supply chains but also accelerating the region's embrace of indoor farming technologies.

AI, IoT, LED, and Automation Gains

Technology integration is a significant growth driver for the Middle East and Africa indoor farming market, as growers increasingly implement AI, IoT, LED lighting, and automation systems to enhance productivity and lower operational costs. Smart farming technologies enable operators to optimize irrigation, climate control, and energy consumption within controlled-environment facilities. A 2025 study published in the Journal of the Saudi Society of Agricultural Sciences demonstrated that IoT-enabled greenhouse monitoring, combined with precision subsurface drip irrigation, achieved an irrigation water-use efficiency of 7.66 to 15.73 kilograms per cubic meter under optimal treatment conditions[3]Source: Journal of the Saudi Society of Agricultural Sciences, “Optimizing Water Management in Greenhouse Farming Through an IoT-Enabled Monitoring System,” link.springer.com. This underscores the efficiency advantages of advanced indoor farming technologies in arid regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital intensity and payback risk | -1.5% | Pan-MEA, most acute across sub-Saharan Africa | Long term (≥ 4 years) |

| Controlled-environment agronomy talent gaps | -1.0% | GCC and sub-Saharan Africa | Medium term (2-4 years) |

| Cooling-energy intensity and grid-cost exposure | -1.2% | UAE, Saudi Arabia, and Egypt | Short term (≤ 2 years) |

| Imported inputs and non-harmonized CEA regulations | -0.8% | GCC, with fragmented rules across member states, and North Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Intensity and Payback Risk

High initial investment continues to be a significant challenge for the indoor farming market in the Middle East and Africa, particularly outside the Gulf region, where securing project financing is more difficult. Indoor farming requires substantial upfront expenditures for greenhouse structures, enclosed growing systems, lighting, cooling, irrigation, automation, and post-harvest handling before generating consistent revenue. This financial burden is more manageable in Gulf countries with sovereign-backed projects compared to many African markets, where access to credit is limited, and long-term supply contracts are less prevalent. The challenge is not only the scale of the initial investment but also the risk that current equipment may become outdated within a few years due to advancements in lighting efficiency and control software. Operators who construct rigid facilities without modular upgrade options risk falling behind newer farms equipped with more advanced systems and lower operating costs. As a result, many developers prioritize phased rollouts, smaller-scale entry models, or hybrid formats over large-scale enclosed farm designs.

Cooling-Energy Intensity and Grid-Cost Exposure

Cooling and electricity expenses are significant constraints for the indoor farming market in the Middle East and Africa due to the high outdoor temperatures in Gulf countries, which substantially increase the energy required for climate control and indoor crop production. Indoor farms in the region must operate cooling systems, ventilation equipment, and LED lighting continuously, leading to higher operational costs compared to facilities in regions with milder climates. According to Agrifarming, commercial greenhouse operations in the UAE allocate over 30% of their total operating costs to cooling and climate-control systems. This high energy dependence reduces profitability, increases payback risks, and creates cost uncertainties for indoor farming operators in the region.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Facility Type: Greenhouses Anchor Regional Scale While Container Farms Accelerate

The Middle East and Africa indoor farming market share for the greenhouse segment accounted for the largest 70.8% in 2025, reflecting the region’s preference for scalable protected cultivation systems that balance production control with lower operating complexity than fully enclosed vertical farms. Greenhouse adoption is particularly strong in Gulf countries, where high temperatures and water scarcity drive investments in climate-controlled cultivation. In the United Arab Emirates and Saudi Arabia, commercial hydroponic greenhouse operators are expanding production capacity to support food security strategies and ensure a year-round vegetable supply. Additionally, large greenhouse systems are more commercially viable for staple crop production due to their ability to support larger cultivation areas and lower per-unit infrastructure costs.

The Middle East and Africa indoor farming market size for container farms is projected to grow at the fastest CAGR of 12.8% from 2026 to 2031, supported by rising demand for modular indoor farming systems that can operate close to urban consumption centers. The flexibility of container farms makes them appealing in markets with limited land availability, smaller capital budgets, or pilot-scale expansion plans. These systems also enable faster deployment compared to large greenhouse or vertical farming facilities. While indoor vertical farms are gaining attention in Gulf countries, their expansion is primarily concentrated among well-funded operators with strong retail or institutional partnerships. Specialty facility formats, such as Deep Water Culture (DWC) systems, continue to serve premium produce markets, research cultivation, and controlled pilot applications.

By Growing System: Hydroponics Leads as Aeroponics Scales Fastest

Hydroponics accounted for the largest share of 59.8% in 2025, maintaining its position as the leading growing system in controlled-environment agriculture operations within the region. This system remains widely adopted due to its ability to ensure predictable nutrient delivery, consistent crop quality, and reduced water consumption compared to traditional soil-based cultivation. Hydroponic systems are particularly significant in Gulf countries, where water scarcity and extreme climate conditions necessitate precision irrigation for commercial food production. Growers continue to rely on hydroponics for crops such as tomatoes, cucumbers, peppers, herbs, and leafy greens, as the technology has demonstrated a strong operational track record in desert climates and commercial greenhouse environments.

Aeroponics is projected to grow at the highest CAGR of 15.6% from 2026 to 2031, driven by increasing interest in high-efficiency cultivation systems for premium crops and urban food supply applications. Aeroponic systems utilize fine nutrient mist delivery methods, which significantly reduce water usage while enabling rapid crop cycles and high-density production. This technology is gaining relevance for leafy greens, herbs, microgreens, and specialty produce, particularly for supply to retail, hospitality, and foodservice sectors. Additionally, aquaponics and hybrid growing systems are attracting attention in specific projects focused on sustainable food production, although their commercial adoption remains lower than hydroponic systems across most regional markets.

By Component: Hardware Dominates a Build-Phase Market

Hardware led with the largest 60.1% share in 2025 because indoor farming investments across the region remain heavily focused on greenhouse construction, climate-control systems, irrigation equipment, LED lighting, sensors, automation platforms, and crop racks. Gulf countries continue allocating substantial capital toward building controlled-environment agriculture facilities designed to manage high temperatures and water efficiency requirements. Climate-control and cooling systems remain particularly important because desert operating conditions increase dependence on ventilation, humidity management, and temperature stabilization technologies. The market, therefore, continues reflecting a build-phase environment where infrastructure spending remains higher than operational software and long-term service revenue.

Software is projected to grow at the fastest CAGR of 12.0% from 2026 to 2031 as indoor farm operators increasingly adopt digital monitoring platforms, remote-control systems, predictive analytics, and automated crop management technologies. Farm operators are prioritizing software integration because precision management improves energy efficiency, crop consistency, and irrigation performance across large facilities. Demand for technical services is also increasing as more projects move from development into full-scale commercial operation. Installation support, maintenance, staff training, and crop optimization services are becoming more important as operators seek year-round production stability. Despite this shift, hardware spending remains dominant because regional expansion still depends heavily on new facility construction.

By Crop Type: Staple Produce Leads While Ornamentals Post Stronger Growth

Fruits, vegetables, and herbs accounted for the largest market share of 47.4% in 2025, reflecting strong regional demand for staple produce categories that support food security goals and reduce import dependence. Tomatoes, cucumbers, peppers, lettuce, spinach, and herbs remain the primary crops cultivated in greenhouse and hydroponic systems due to their alignment with retail demand and year-round consumption trends. Indoor farming operators in Gulf countries continue to focus on staple produce, as controlled cultivation systems ensure stable yields despite harsh climatic conditions. Additionally, premium hospitality, retail, and foodservice sectors contribute to the demand for microgreens and specialty herbs, although these represent smaller volume categories compared to mainstream vegetable production.

Flowers and ornamentals are projected to grow at the fastest CAGR of 10.2% from 2026 to 2031 as greenhouse operators diversify into higher-value crop segments. This growth is supported by export-oriented floriculture activities in East Africa and increasing demand for premium ornamentals and decorative indoor plants in Gulf countries' hospitality sectors. Greenhouse cultivation plays a critical role in ensuring quality consistency, extending seasonal availability, and enhancing supply reliability for export-focused flower producers. Indoor cultivation systems are also facilitating the production of edible flowers and specialty ornamentals for hotels, restaurants, and premium retail channels. This expansion not only broadens revenue streams beyond staple vegetable cultivation but also promotes greater crop diversification within controlled-environment agriculture projects.

Geography Analysis

In 2025, the Middle East dominated the indoor farming market, accounting for 69.0% of revenue. This dominance was bolstered by robust sovereign investments, government-led food security initiatives, and the establishment of the region's largest commercial controlled environment agriculture (CEA) facilities. The United Arab Emirates' growth is supported by strong food security policies, infrastructure investment, and commercial adoption of controlled-environment agriculture technologies. The United Arab Emirates (UAE) continues to lead regional indoor farming initiatives through greenhouse expansion, hydroponic cultivation, and vertical farming development, all aligned with its long-term domestic food supply objectives. Saudi Arabia is also advancing greenhouse and hydroponic vegetable production through localized food supply initiatives.

However, projections indicate that Africa's market will expand faster, with a CAGR of 10.3% from 2026 to 2031, outpacing the Middle East's growth. This accelerated growth in Africa can be attributed to the increasing adoption of CEA in countries such as South Africa, Kenya, and Egypt, driven by multilateral financing and a rising urban appetite for locally sourced food. The disparity between Africa's current market share and its projected growth trajectory indicates a shift. Africa is transitioning from mere pilot projects to the establishment of a commercially viable CEA foundation. This growth is supported by increasing commercial greenhouse investments, rising premium retail demand for locally produced vegetables, and the expanding adoption of protected cultivation technologies. Kenya and Ethiopia remain significant horticultural production hubs, as greenhouse systems facilitate export-oriented floriculture and high-value vegetable supply chains. While the Middle East continues to outpace Africa in terms of project scale and funding, this very disparity presents Africa as a more accessible and pragmatic entry point for mid-sized tech suppliers and smaller commercial operators through 2026-2031.

The rest of the Middle East continues to adopt greenhouse and indoor farming systems gradually, with Oman, Qatar, and Kuwait increasing investment in hydroponic cultivation and climate-controlled food production. In Africa, commercial indoor farming adoption remains focused on greenhouse vegetables, community hydroponic systems, and floriculture projects, rather than fully enclosed vertical farming operations. This creates a regional dynamic where Gulf countries lead in technology deployment and capital investment, while African countries offer longer-term growth opportunities tied to food supply modernization and export horticulture.

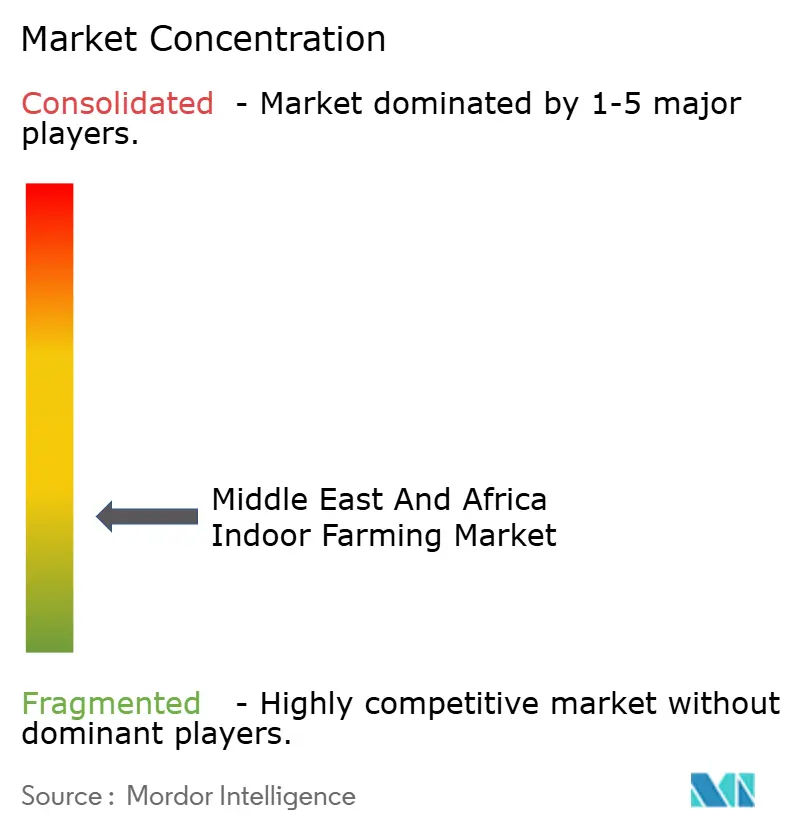

Competitive Landscape

The market remains fragmented across Gulf countries and even more so across African economies, where greenhouse projects and hydroponic operations are generally smaller in scale. Major players such as Pure Harvest Smart Farms Ltd., Emirates Bustanica LLC (Emirates Flight Catering Co. LLC), VeggiTech Hydroponic Technologies Private Limited, Mowreq Specialized Agriculture Company, and Badia Al Sahra Agricultural L.L.C. are strengthening their positions through significant investments in controlled-environment agriculture and retail supply agreements. Competition is increasingly driven by factors such as operational scale, climate adaptation capabilities, crop consistency, and access to food retail channels. Larger operators benefit from better access to financing and government-supported food security programs that facilitate infrastructure expansion and long-term production planning.

Technology suppliers are active across segments such as lighting, irrigation, automation, software, and turnkey greenhouse construction within the regionally controlled-environment agriculture ecosystem. Companies like Signify Holding B.V., Netafim Ltd., Priva Holding B.V., Argus Control Systems Limited, and Certhon Build B.V. continue to support commercial greenhouse and indoor farming expansion projects in Gulf countries. In 2024, Intelligent Growth Solutions Limited participated in the Dubai Food Tech Valley GigaFarm development by deploying multi-level vertical farming technology designed for large-scale urban food production. Technology reliability remains a critical factor, as climate-control failures pose significant operational risks under desert conditions.

Regional competition increasingly favors operators capable of managing high energy costs, climate-control expenses, and advanced automation requirements while ensuring year-round crop consistency. Many indoor farms focus on crops such as leafy greens, herbs, tomatoes, and cucumbers due to their stable commercial demand and operational familiarity. While premium produce, ornamentals, and specialty crops remain less developed, they offer future diversification opportunities for experienced operators. Consequently, the competitive landscape is characterized by a limited number of large Gulf-based operators with robust infrastructure and financing capabilities, alongside a broader group of smaller greenhouse developers and emerging hydroponic growers operating across African markets.

Middle East And Africa Indoor Farming Industry Leaders

Pure Harvest Smart Farms Ltd.

Emirates Bustanica LLC (Emirates Flight Catering Co. LLC)

VeggiTech Hydroponic Technologies Private Limited

Mowreq Specialized Agriculture Company

Badia Al Sahra Agricultural L.L.C.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Emirates Bustanica LLC (Emirates Flight Catering Co. LLC) has expanded its indoor farming operations beyond airline catering by launching retail-ready salads, soups, juices, and foodservice products as part of Emirates Flight Catering’s broader commercial food strategy. This development underscores the growing commercialization of vertical farming and the rising regional demand for locally produced fresh food products.

- February 2025: Pure Harvest Smart Farms and PlanTFarm have inaugurated an integrated smart farm in Al Ain, United Arab Emirates. The facility incorporates AI-powered controlled-environment agriculture technologies to produce premium crops and cultivate water-efficient animal fodder. This initiative aims to enhance regional food security and promote sustainable indoor farming in arid climates.

- February 2024: Emirates Flight Catering Co. LLC has fully acquired Emirates Bustanica LLC, making the operator of the world’s largest indoor vertical farm entirely owned by the United Arab Emirates. This acquisition enhances regional investment in controlled-environment agriculture and supports long-term food and water security initiatives in the Middle East.

Middle East And Africa Indoor Farming Market Report Scope

Indoor farming involves cultivating crops in controlled environments, including greenhouses, vertical farms, container farms, and indoor facilities. This method utilizes technologies such as hydroponics, aeroponics, LED lighting, and climate-control systems. It facilitates year-round crop production while optimizing water, nutrient, and space usage, and minimizes reliance on external weather conditions and traditional farmland. The Middle East and Africa indoor farming market is segmented by Facility Type (greenhouses, indoor vertical farms, container farms, indoor Deep Water Culture (DWC) systems, and other facility types), by Growing System (hydroponics, aeroponics, aquaponics, soil-based, and hybrid), by Component (hardware, software, and services), by Crop Type (fruits, vegetables, and herbs, flowers and ornamentals, and microgreens and specialty crops), and by Geography (Middle East and Africa). The market forecasts are provided in terms of value (USD).

| Greenhouses |

| Indoor Vertical Farms |

| Container Farms |

| Indoor Deep Water Culture Systems |

| Other Facility Types |

| Hydroponics |

| Aeroponics |

| Aquaponics |

| Soil-based |

| Hybrid |

| Hardware |

| Software |

| Services |

| Fruits, Vegetables, and Herbs |

| Flowers and Ornamentals |

| Microgreens and Specialty Crops |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Kenya | |

| Rest of Africa |

| By Facility Type | Greenhouses | |

| Indoor Vertical Farms | ||

| Container Farms | ||

| Indoor Deep Water Culture Systems | ||

| Other Facility Types | ||

| By Growing System | Hydroponics | |

| Aeroponics | ||

| Aquaponics | ||

| Soil-based | ||

| Hybrid | ||

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Crop Type | Fruits, Vegetables, and Herbs | |

| Flowers and Ornamentals | ||

| Microgreens and Specialty Crops | ||

| By Geography | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the Middle East and Africa indoor farming market by 2031?

The market is forecast to reach USD 5.19 billion by 2031.

Which facility type leads regional revenue?

Greenhouses lead the regional mix, with the largest 70.8% share in 2025.

Which growing system is expanding the fastest in the region?

Aeroponics is projected to grow the fastest, with a 15.6% CAGR from 2026 to 2031.

Which crop category is showing the strongest momentum beyond staple produce?

Flowers and ornamentals are growing the fastest, with a 10.2% CAGR from 2026 to 2031.

Page last updated on: