Bahrain Indoor Farming Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

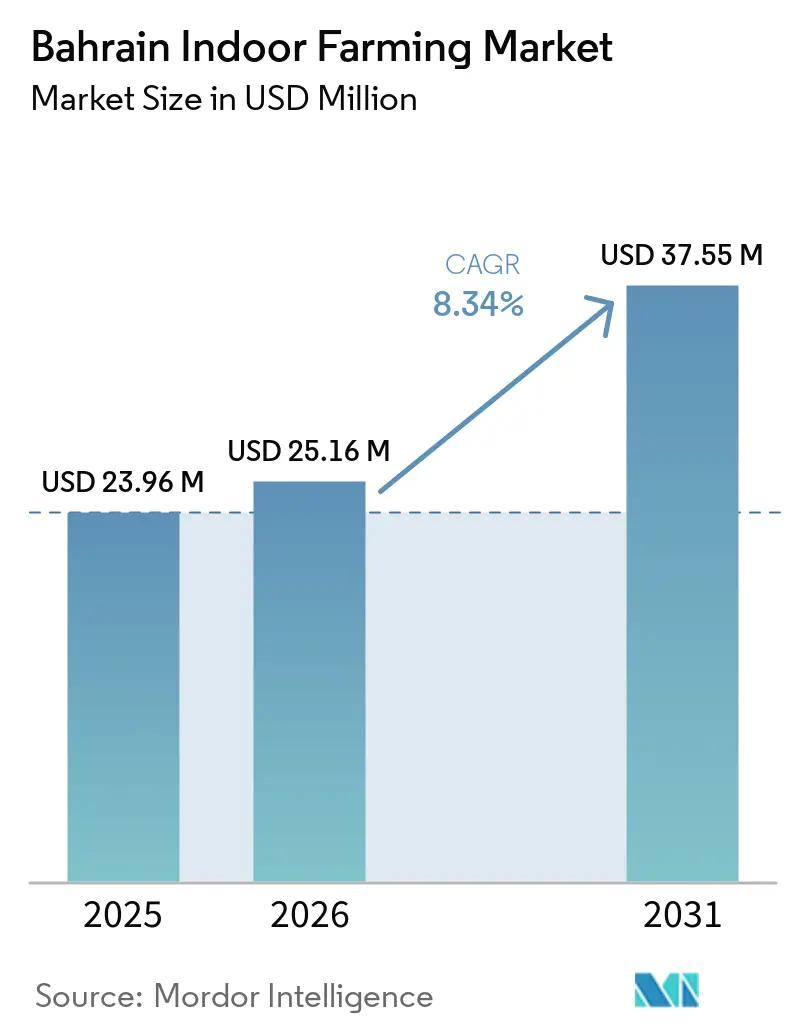

| Base Year Market Size (2025) | USD 23.96 Million |

| Market Size (2026) | USD 25.16 Million |

| Market Size (2031) | USD 37.55 Million |

| Growth Rate (2026 - 2031) | 8.34% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bahrain Indoor Farming Market Analysis by Mordor Intelligence

The Bahrain indoor farming market size is anticipated to grow from USD 23.96 million in 2025 to USD 25.16 million in 2026 and is forecast to reach USD 37.55 million by 2031 at 8.34% CAGR over 2026-2031. The Bahrain indoor farming market is expanding because domestic food production has become a structural priority in a country that imports more than 90% of its food and has only 2.1% arable land [1]Source: Bahrain Supreme Council for Environment, “Bahrain National Adaptation Investment Plan,” United Nations Framework Convention on Climate Change, unfccc.int. Water stress is also pushing commercial farms toward controlled growing systems, since Bahrain was ranked among the 5 most water-stressed countries globally, and freshwater withdrawal reaching 133.71% of available renewable resources in 2022 [2]Source: World Resources Institute, “Aqueduct Water Risk Atlas,” World Resources Institute, wri.org. Government support for indoor farming agriculture aligns with Bahrain's long-term objectives for food security and climate resilience. In November 2025, Bahrain released its National Adaptation Investment Plan, outlining investments to increase domestic food production, optimize water use, and enhance agricultural resilience to address climate-related challenges. Competitive positioning in the Bahrain indoor farming market is increasingly shaped by access to sovereign-linked food platforms, proven cooling technology, and certification-led sales models that strengthen supply credibility with retailers and food service buyers.

Key Report Takeaways

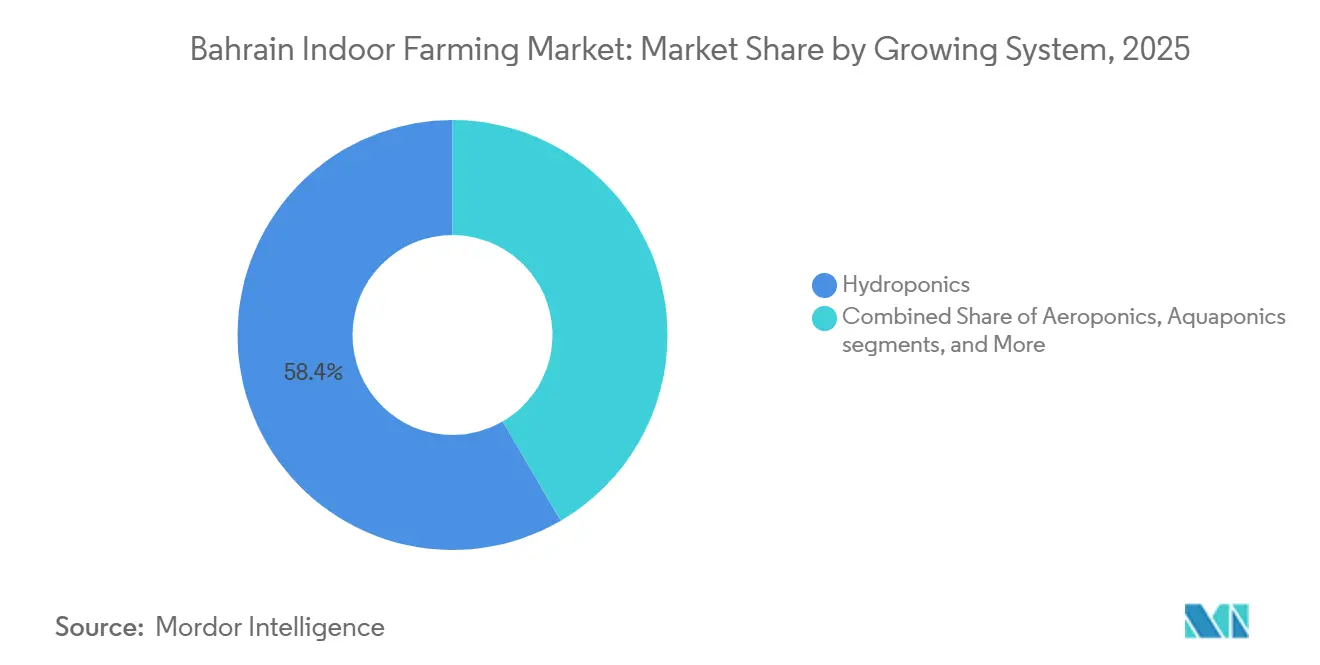

- By growing system, hydroponics was the largest segment, and accounted for 58.4% of the Bahrain indoor farming market share in 2025, while aeroponics will be the fastest-growing segment and is projected to expand at a 16.3% CAGR during 2026-2031.

- By facility type, greenhouses were the largest segment, and accounted for 62.1% of the Bahrain indoor farming market size in 2025, while vertical farms are the fastest-growing segment at a 15.8% CAGR during 2026-2031.

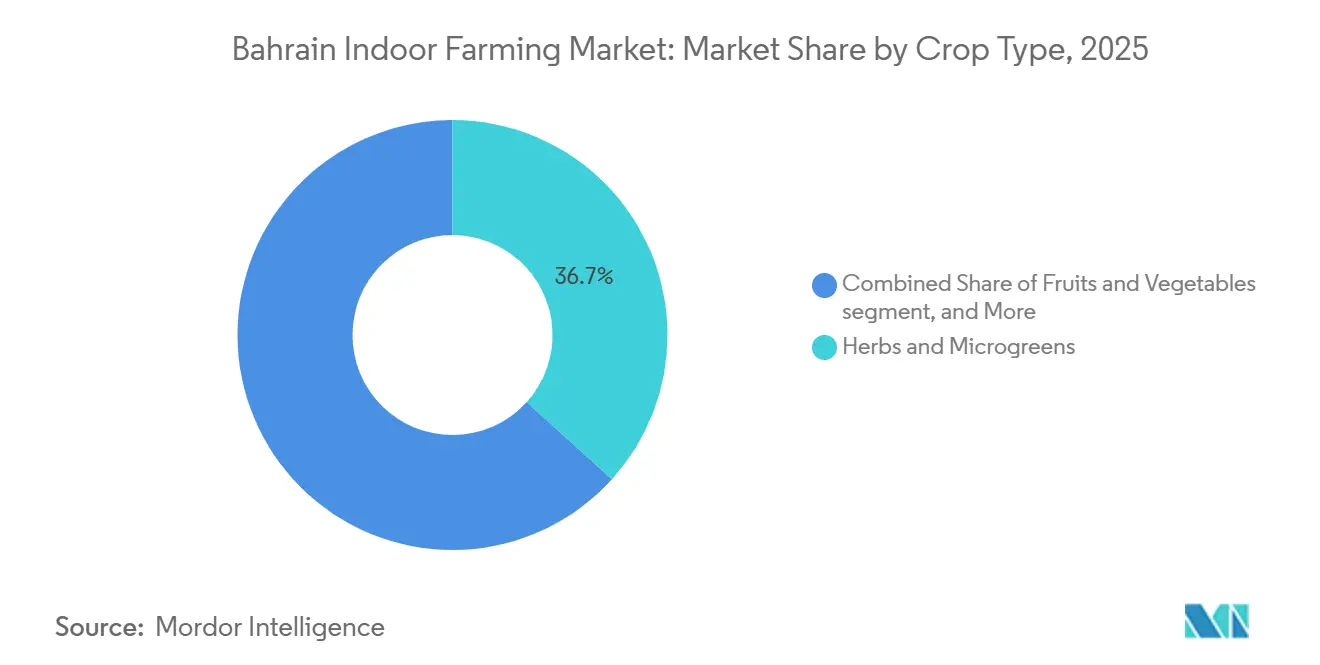

- By crop type, herbs and microgreens were the largest segment, and represented 36.7% of the Bahrain indoor farming market in 2025, while fruits and vegetables will be the fastest-growing segment at a 15.2% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Bahrain Indoor Farming Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |

|---|---|---|---|---|

| Government-Backed Food Security Hydroponics Rollout | +2.10% | National in scope, with stronger early adoption in established commercial farming zones and public-backed production sites | Short term (≤ 2 years) | |

| Land and Climate Constraints Favor Controlled Environments | +1.70% | National, because low arable land availability and extreme heat affect all governorates | Long term (≥ 4 years) | |

| Water-Efficiency Gains Versus Field Cultivation | +1.30% | National, with the strongest commercial relevance in high-intensity vegetable production systems | Medium term (2-4 years) | |

| Premium Retail and HORECA Demand for Reliable Local Produce | +1.20% | Strongest in Northern and Capital Governorates where premium retail and hospitality demand is concentrated | Medium term (2-4 years) | |

| Treated-Wastewater Connectivity for New Farm Sites | +0.60% | More relevant to new expansion zones, especially where municipal infrastructure can support new farm clusters | Medium term (2-4 years) | |

| Government Land-Platform and Incubator-Led Project Acceleration | +0.50% | National, with visible early gains at public incubation sites and government-linked farm platforms | Short term (≤ 2 years) | |

| Source: Mordor Intelligence | ||||

Government-Backed Food Security Hydroponics Rollout

Bahrain’s food security agenda is no longer limited to policy language, because it now includes direct public backing for controlled agriculture. The National Adaptation Investment Plan submitted in August 2025 identified hydroponics, aeroponics, and aquaponics as priority technologies within a USD 55.8 million (BHD 21.0 million) climate-resilient agriculture program in 2023. That support matters for the Bahrain indoor farming market because it reduces project uncertainty and provides investors with clearer direction on which systems are likely to receive policy attention. The November 2024 transfer of Bahrain Agriculture Development Company (Gheras) to Bahrain Food Holding Company under Mumtalakat also created a stronger public platform for scaling local production and distribution. In practical terms, state-backed rollout helps the Bahrain indoor farming market move from pilot activity toward more repeatable commercial deployment.

Land and Climate Constraints Favor Controlled Environments

The indoor farming industry in Bahrain faces challenges due to inherent agricultural limitations that are not anticipated to change significantly during the forecast period. As outlined in Bahrain's National Adaptation Investment Plan, arable land accounts for only 2.1% of the country's total land area, limiting opportunities for traditional field cultivation. These land limitations, along with Bahrain's reliance on imported food products, underscore the strategic importance of controlled-environment agriculture systems. Such systems enable domestic crop production with improved land and water-use efficiency. Peninsula Farms W.L.L. shows why controlled systems fit the local climate, with its closed-loop cooling and hydroponic setup designed to maintain high yields year-round, and the company reports 98% crop yields year-round. Because these land and temperature conditions are structural, the Bahrain indoor farming market remains relevant even when short-term input costs fluctuate.

Water-Efficiency Gains Versus Field Cultivation

Water efficiency remains one of the clearest growth supports for the market. Bahrain ranked among the 5 most water-stressed countries globally, which means agricultural water use is under permanent pressure to become more productive. Freshwater withdrawal reached 133.7% of available renewable resources, underscoring the limited natural water base for open-field farming [3]Source: Food and Agriculture Organization of the United Nations, “AQUASTAT Bahrain Country Profile,” fao.org. Water resource efficiency is a significant driver of indoor farming adoption in Bahrain. A 2025 study titled "Evaluating Future Alternatives for a Sustainable Water Sector in Bahrain Using WEAP" revealed that only approximately 40% of Bahrain's treated wastewater is reused, despite the country's critical water scarcity. The study also highlighted a national target to increase irrigation efficiency to at least 60% by 2035. These insights underscore the appeal of hydroponic and controlled-environment farming systems, which optimize production while minimizing freshwater usage.

Premium Retail and HORECA Demand for Reliable Local Produce

Demand from premium retail and food service buyers is helping the indoor farming industry build a more stable commercial base. Operators serving hotels, restaurants, and catering buyers benefit from the ability to offer year-round supply and consistent crop quality, which matters in channels where availability and freshness shape procurement decisions. Al Ghalia Farms reflects this positioning through its Terra Aqua hydroponic platform, which supplies produce to in-house brands, business clients, and local retail outlets. The company’s emphasis on locally and sustainably grown produce shows that commercial value in Bahrain is not based on volume alone, but also on traceability and quality assurance. This demand profile supports the market by enabling commercial farms to target higher-value sales channels rather than competing solely on low-margin bulk output.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex for Cooled Greenhouses and Vertical Farms | -2.50% | National, because all large commercial projects must invest in climate control and protected structures | Long term (≥ 4 years) |

| Commercial Electricity and Water Tariffs Pressure Margins | -1.80% | National, with stronger impact on high-cooling and high-recirculation operations | Short term (≤ 2 years) |

| Imported Inputs and Technical-Service Dependency | -1.10% | National, especially for farms using specialized automation, climate software, and advanced growing systems | Medium term (2-4 years) |

| Small Domestic Offtake Base Limits Scale Efficiency | -0.70% | National, with the strongest effect on large projects that need steady volume absorption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capex for Cooled Greenhouses and Vertical Farms

High initial investment remains a major restraint for the Bahrain indoor farming market. Climate-controlled farms in Bahrain need insulated structures, cooling systems, irrigation controls, and specialized growing equipment to operate reliably in extreme heat. Peninsula Farms W.L.L. illustrates the technical intensity of this model because its system uses custom cooling, hygiene management, and hydroponic production architecture rather than low-cost basic infrastructure. That capital burden narrows the field of operators that can scale quickly and makes phased expansion more common than rapid national rollout. As a result, the indoor farming industry in Bahrain can grow steadily, but capex intensity continues to slow the pace of new commercial capacity additions.

Commercial Electricity and Water Tariffs Pressure Margins

Operating cost pressure is another restraint for the market, as controlled cultivation in Bahrain depends heavily on cooling, pumping, lighting in some formats, and water management, so any increase in utility costs directly affects farm margins. Public and private operators are responding by testing energy-saving and solar-linked approaches, which shows that cost pressure is already shaping operating decisions. Even with efficiency upgrades, cost exposure remains higher in Bahrain than in milder climates because temperature control is a basic requirement rather than an optional performance upgrade. This means margin management will remain a central issue for the Bahrain indoor farming market during 2026-2031.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Growing System: Hydroponics Is the Largest Segment, Aeroponics Accelerates

Hydroponics was the largest segment in the Bahrain indoor farming market, and accounted for 58.4% of revenue by growing system in 2025. This lead reflects the commercial maturity of hydroponic production across Bahrain, where growers already use nutrient film and flatbed-based systems at an operating scale. Peninsula Farms W.L.L. built its output model on hydroponic architecture designed for Bahrain’s climate, and the company reports 98% crop yields year-round through closed-loop cooling and controlled hygiene practices. Al Ghalia Farms also uses advanced hydroponic methods and positions locally grown produce across restaurants, business customers, and retail channels. The hydroponics base provides the Bahrain indoor farming industry with a practical technology path that has already proven itself in commercial use.

Aeroponics is the fastest segment in the Bahrain indoor farming market and is projected to expand at a 16.3% CAGR during 2026-2031. The National Adaptation Investment Plan directly supports that outlook by naming aeroponics as one of the priority technologies for climate-resilient agriculture. Haya Gardens shows that aeroponics has already moved beyond the concept stage in Bahrain, with the company operating aeroponic, hydroponic, and soil agriculture across 2 sites, including Hamala and Manama. Aquaponics remains smaller by revenue, but its credibility is strengthened by Dar Aqua & Agriculture W.L.L., which presents itself as Bahrain’s first and largest aquaponic farm and reports more than 1000 metric tons of organic vegetables produced. Soil-based and hybrid systems still have a presence, but the market's investment bias is clearly moving toward highly water-efficient soilless systems.

By Facility Type: Greenhouses Are the Largest Segment, Vertical Farms Set the Pace

Greenhouses were the largest segment, and represented 62.1% of the Bahrain indoor farming market size by facility type in 2025. This position reflects their role as the standard commercial format for crop programs that need scale, manageable cooling economics, and operating familiarity. The strongest evidence comes from active farm models in Bahrain, where hydroponic greenhouse systems remain central to the production practices of Peninsula Farms W.L.L. and Al Ghalia Farms. Greenhouses also align well with public initiatives focused on practical food security gains rather than highly specialized showcase facilities. This keeps greenhouses at the center of current revenue even as more advanced formats gain attention.

Vertical farms are the fastest segment in the Bahrain indoor farming market and are forecast to grow at a 15.8% CAGR during 2026-2031. Their appeal lies in their ability to intensify output in a country where land is limited, and climate control is essential. The technology pathway is also improving through public trials and imported automation, as shown by the 2025 work of the UK Agri-Tech Center and its partner companies at ministry-backed sites. Container farms and deep-water culture systems serve narrower roles, mainly for rapid deployment, pilot crop programs, or high-turnover leafy greens. Even so, the market is likely to keep favoring greenhouses for revenue scale while vertical farms expand faster from a smaller base.

By Crop Type: Herbs and Microgreens Are the Largest Segment, Fruits and Vegetables Surge

Herbs and microgreens were the largest segment, and accounted for 36.7% of the Bahrain indoor farming market share in 2025. This reflects the commercial value of short growing cycles, premium pricing, and steady demand from restaurants, hotels, and specialty retail buyers. Operators that can deliver freshness and consistent visual quality are well placed in this category because these crops are purchased as much for reliability as for volume. The Bahrain indoor farming market for herbs and microgreens remains strong because these crops enable faster asset rotation within controlled growing spaces. That makes them especially attractive in a market where capital recovery and operating efficiency matter at every production cycle.

Fruits and vegetables are the fastest segment in the Bahrain indoor farming market and are forecast to grow at a 15.2% CAGR during 2026-2031. The shift is tied to the broader national food security agenda, which places greater emphasis on staple fresh produce rather than on premium niche crops. Bahrain Agriculture Development Company (Gheras) opened Phase 1 of its hydroponics production project in Hoorat Aali in 2024 with 7 greenhouses targeting an annual output of 520 metric tons of vegetables. Flowers and ornamentals still hold a viable niche, and Prasada (Xiamen) Agricultural Engineering Co., Ltd. confirms that it operates both hydroponic vegetable production and a flower greenhouse project in Bahrain. The crop mix in the Bahrain indoor farming market is therefore moving toward a dual structure, with staple vegetables growing faster while herbs and microgreens remain the largest current revenue pool.

Geography Analysis

The Northern Governorate was the largest geographic segment in the Bahrain indoor farming market in 2025. Its position is supported by the concentration of established commercial activity and by its link to the country’s main retail and hospitality demand centers. Dar Aqua & Agriculture W.L.L. operates from Hawrat A’ali and describes itself as Bahrain’s first and largest aquaponic farm, with supply relationships with more than 20 supermarkets and over 310 restaurants and coffee shops. Public-backed farming activity also supports this geography, as Bahrain Agriculture Development Company (Gheras) has advanced hydroponic prarea production in Hoorat Aali, which was officially inaugurated in 2024. Together, these assets make the Northern Governorate the clearest production anchor in Bahrain.

The Southern Governorate is the fastest-growing geographic area in Bahrain. Its growth story is tied to new site development, available land, and the ability to deploy modern, controlled systems in less-constrained expansion zones. Haya Gardens illustrates this shift, as the company’s growth began in Hamala and now spans 2 official sites in Bahrain with aeroponic, hydroponic, and soil-based farming methods. The policy push toward climate-resilient agriculture further supports southern expansion, as new projects can be aligned with priority technologies identified in the national plan. In the Bahrain indoor farming market, the Southern Governorate is emerging as the main area for future capacity additions, without relying solely on older farm clusters.

The Capital and Muharraq Governorates play different roles in the Bahrain indoor farming market. These areas function more as demand, service, and distribution hubs than as large-volume production bases, because urban land use limits the scale of agricultural installations. MHB Agricultural Supplies Hydroponics, based in Muharraq, plays this support role by distributing hydroponic inputs and system components to growers in Bahrain. Manama also remains commercially important because Haya Gardens operates one of its official sites there, linking the supply of fresh produce to dense urban demand. This geographic pattern means the market will continue to depend on Northern and Southern production, while the Capital and Muharraq Governorates remain essential for sales channels, services, and end-market access.

Competitive Landscape

The Bahrain indoor farming market is moderately concentrated and the competitive structure is led by a small group of operators with meaningful production scale or system reach. Dar Aqua & Agriculture W.L.L., Peninsula Farms W.L.L., Bahrain Agriculture Development Company (Gheras), Al Ghalia Farms, and MHB Agricultural Supplies Hydroponics are among the leading companies operating in the market. Dar Aqua & Agriculture W.L.L. stands out for scale and channel access, reporting annual production of more than 1,000 metric tons of organic vegetables, supplied to supermarkets, restaurants, and coffee shops in Bahrain through relationships. Peninsula Farms W.L.L. competes through production discipline, with a technology stack built around closed-loop cooling, hydroponics, and hygiene control that supports 98% crop yields year-round. This leaves the Bahrain indoor farming market led by players differentiated by scale, climate technology, distribution access, or input control.

Competitive strategy is also being shaped by state-linked consolidation and public platform building. In 2024, Mumtalakat transferred Bahrain Agriculture Development Company (Gheras) to Bahrain Food Holding Company, placing hydroponic production inside a broader national food portfolio that also includes Bahrain Flour Mills, General Poultry Company, and Delmon Poultry Company. That move gives Bahrain Agriculture Development Company (Gheras) stronger institutional backing and a clearer route into established food distribution channels. In 2025, the UK Agri-Tech Center project with the Ministry of Municipalities Affairs and Agriculture brought Polysolar, Ostara, and Zayndu into local trial settings, demonstrating how technology partnerships are entering the Bahrain indoor farming market through public collaboration rather than solely through private procurement. In 2024, Priva B.V. also introduced new greenhouse automation products at GreenTech Amsterdam, reinforcing the wider supplier push toward precision climate management for controlled agriculture.

Certification and market positioning add another layer of competition in the Bahrain indoor farming market. Al Ghalia Farms uses its Terra Aqua platform to supply locally and sustainably grown produce to restaurants, business clients, and retail channels, supporting a quality-led commercial model. MHB Agricultural Supplies Hydroponics occupies an upstream position that matters because access to nutrients, growing media, and equipment relationships can influence farm expansion timing and technology choices. Haya Gardens adds competitive pressure from the local growth side, as it combines aeroponic, hydroponic, and soil agriculture across sites in Hamala and Manama and targets a broad local produce proposition. Overall, the Bahrain indoor farming market remains open to new entrants, but the strongest competitive advantage still lies with operators that already control proven systems, trusted channels, or public-backed growth platforms.

Bahrain Indoor Farming Industry Leaders

Dar Aqua & Agriculture W.L.L.

Peninsula Farms W.L.L.

Bahrain Agriculture Development Company (Gheras)

Al Ghalia Farms

MHB Agricultural Supplies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Priva B.V. integrated its crop management platform with IUNU's artificial intelligence-based plant monitoring system, enabling real-time predictive yield adjustments for controlled environment operators and materially lowering the technical expertise threshold for advanced crop management across small- to mid-sized farms.

- November 2025: Bahrain submitted its National Adaptation Investment Plan (NAIP) to the United Nations Framework Convention on Climate Change (UNFCCC), allocating USD 55.8 million (BHD 21 million) for climate-resilient agriculture. The plan specifically identifies hydroponics, aeroponics, and aquaponics as priority investment areas. This represents the highest level of state endorsement for the indoor farming sector in Bahrain and establishes a clear policy framework to guide future project approvals and financing decisions.

- July 2025: The Capital Trustees Board of Bahrain proposed promoting hydroponic farming systems in residential and commercial buildings. This initiative aims to enhance urban agriculture by utilizing space-efficient cultivation methods to address challenges related to land and water availability. The proposal highlights the need to increase institutional support for hydroponic production and indoor farming technologies in urban areas.

Bahrain Indoor Farming Market Report Scope

The Bahrain Indoor Farming Market is Segmented by Growing System (Aeroponics, Hydroponics, Aquaponics, Soil-based, and Hybrid), by Facility Type (Greenhouses, Vertical Farms, Container Farms, Deep-Water Culture, and Other), and by Crop Type (Fruits and Vegetables, Herbs and Microgreens, Flowers and Ornamentals, and Other). The Market Forecasts are Provided in Terms of Value (USD).

| Aeroponics |

| Hydroponics |

| Aquaponics |

| Soil-based |

| Hybrid |

| Glass or Poly Greenhouses |

| Indoor Vertical Farms |

| Container Farms |

| Indoor Deep-Water Culture Systems |

| Other Facility Types |

| Fruits and Vegetables |

| Herbs and Microgreens |

| Flowers and Ornamentals |

| Other Crop Types |

| By Growing System | Aeroponics |

| Hydroponics | |

| Aquaponics | |

| Soil-based | |

| Hybrid | |

| By Facility Type | Glass or Poly Greenhouses |

| Indoor Vertical Farms | |

| Container Farms | |

| Indoor Deep-Water Culture Systems | |

| Other Facility Types | |

| By Crop Type | Fruits and Vegetables |

| Herbs and Microgreens | |

| Flowers and Ornamentals | |

| Other Crop Types |

Key Questions Answered in the Report

What is the outlook for the Bahrain indoor farming market, including growth, from 2026 to 2031?

The Bahrain indoor farming market is projected to rise from USD 25.16 million in 2026 to USD 37.55 million by 2031, at 8.34% CAGR during 2026-2031.

Which growing system leads revenue in Bahrain?

Hydroponics is the largest growing system segment, with 58.4% share in 2025, because it already has proven commercial deployment across established local farms.

Which facility type is expanding the fastest in Bahrain?

Vertical farms are the fastest facility type, with a forecast CAGR of 15.8% during 2026-2031, supported by land constraints and rising interest in intensive controlled production.

Which crop group currently generates the most revenue?

Herbs and microgreens are the largest crop segment, with 36.7% share in 2025, supported by premium retail and food service demand.

Why is controlled farming becoming important in Bahrain?

Bahrain imports more than 90% of its food, has only 2.1% arable land, and faces severe water stress, which makes protected and water-efficient production systems increasingly important.

Which areas are most important for commercial activity?

The Northern Governorate is the largest current production hub, while the Southern Governorate is the fastest-growing geography during 2026-2031.

Page last updated on: