Oman Indoor Farming Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

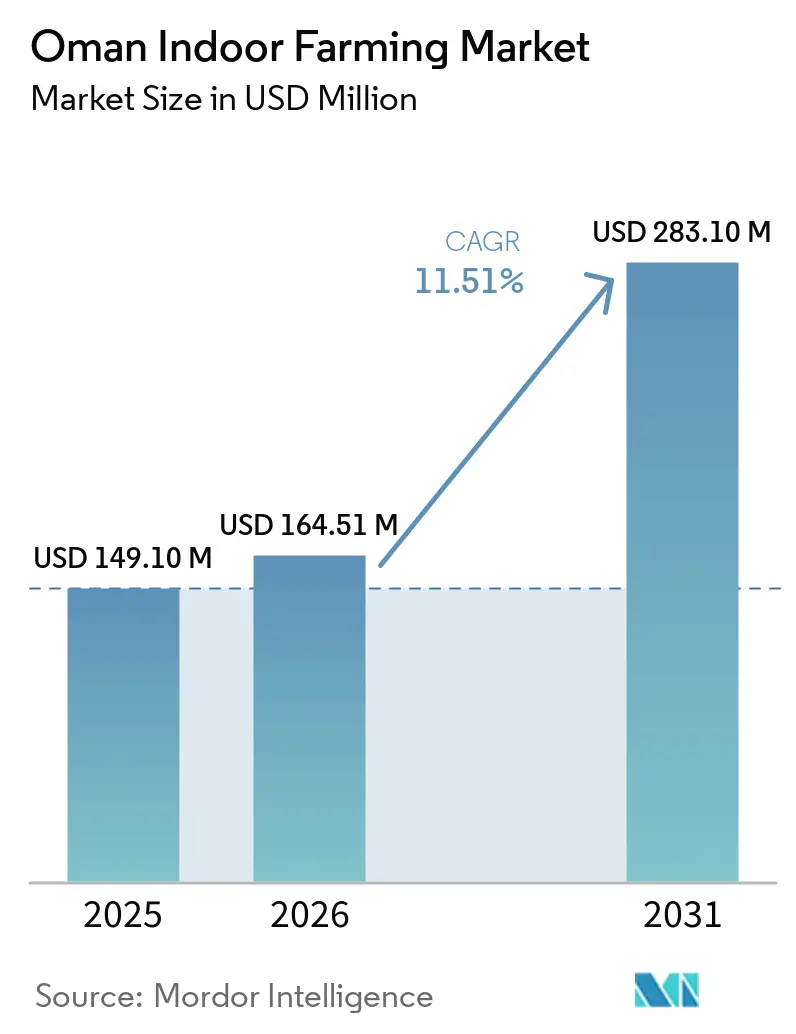

| Base Year Market Size (2025) | USD 149.10 Million |

| Market Size (2026) | USD 164.51 Million |

| Market Size (2031) | USD 283.10 Million |

| Growth Rate (2026 - 2031) | 11.51% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oman Indoor Farming Market Analysis by Mordor Intelligence

The Oman indoor farming market size was estimated to expand from USD 149.10 million in 2025 and USD 164.51 million in 2026 to USD 283.10 million by 2031, registering a CAGR of 11.51% between 2026 to 2031. According to the National Center for Statistics and Information (NCSI), Oman reached an overall food self-sufficiency rate of 65.8% in 2024, while agricultural product self-sufficiency stood at 49.4%[1]Source: Zawya Staff, “Oman Achieves 65.8% Food Self-Sufficiency in 2024,” Zawya, zawya.com, and that supply gap continues to support investment in controlled-environment agriculture. The Second Billion Import Substitution policy and the Food Security Lab 2025 roadmap give the Oman indoor farming market a funded policy base that is more operationally defined than in many neighboring Gulf markets. The Oman indoor farming market is also benefiting from a shift in the operator base, with domestic growers and solution providers moving from pilots into scaled production and commercial service models. Growth still faces limits from high summer cooling loads and uneven premium produce demand outside Greater Muscat, which keeps nationwide expansion more gradual than headline demand in the capital may suggest.

Key Report Takeaways

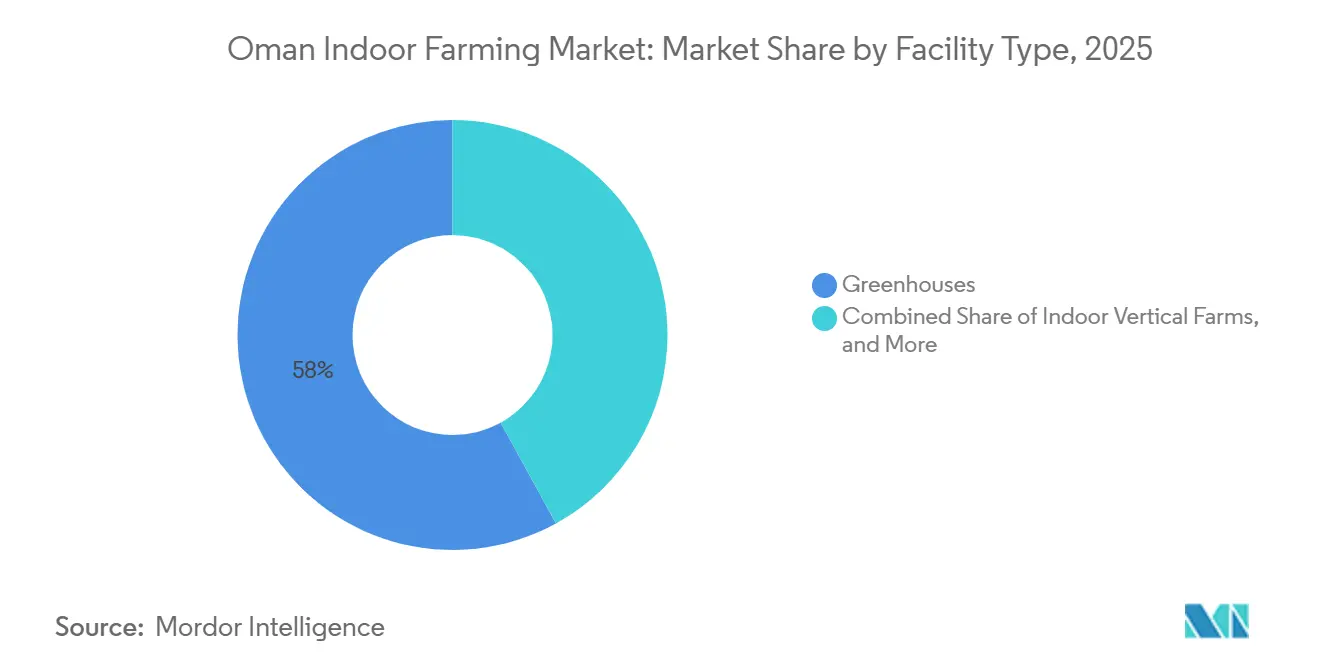

- By facility type, greenhouses hold the largest share of the Oman indoor farming market, accounting for 58.0% in 2025, while indoor vertical farms are the fastest-growing, projected to expand at a 16.2% CAGR through 2026 to 2031.

- By growing system, hydroponics was the largest segment, accounting for 61.0% of the Oman indoor farming market size in 2025, while aeroponics will be the fastest-growing, forecast to grow at a 14.8% CAGR through 2026 to 2031.

- By crop type, fruits and vegetables were the largest crop type, accounting for 37.0% of the Oman indoor farming market share in 2025, while leafy greens will be the fastest-growing crop type, projected to advance at a 15.4% CAGR through 2026 to 2031.

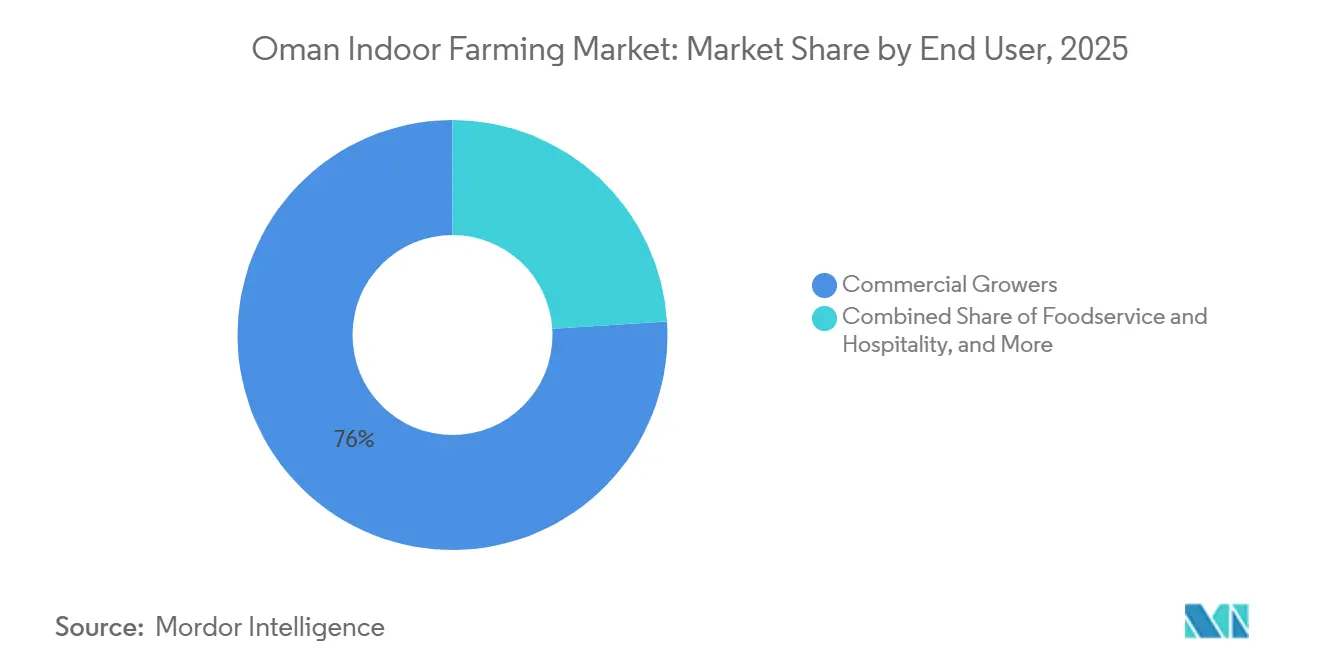

- By end user, commercial growers were the largest, holding 76.0% of the Oman indoor farming market in 2025, while foodservice and hospitality are projected to be the fastest-growing, recording the highest CAGR at 14.1% through 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Oman Indoor Farming Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-Backed Food Security and Import Substitution Programs | +2.5% | Oman-wide, with early gains in Muscat, North Batinah, and Dhofar | Medium term (2-4 years) |

| Water-Stress Economics Favor Closed-Loop Cultivation | +2.2% | Oman-wide, strongest in the arid interior, the Al Batinah plains, and North Sharqiyah | Long term (≥ 4 years) |

| Expansion of Smart Greenhouse and Agri-City Infrastructure | +1.8% | Saham, Al Najd, Dhahirah, and the Muscat metropolitan fringe | Long term (≥ 4 years) |

| Premium Retail and Hospitality Demand for Pesticide-Free Local Produce | +1.5% | Greater Muscat, Salalah, and the Jabal Akhdar tourism corridor | Medium term (2-4 years) |

| Smart Farm Pilots and Public-Private Demonstrations Reduce Adoption Risk | +1.2% | Sultan Qaboos University, North Batinah, and Dhofar Governorate | Short term (≤ 2 years) |

| Decentralized Hotel, Retail, And Home Hydroponic Systems Broaden Demand | +0.8% | Muscat, the Jabal Akhdar corridor, Muttrah, and Ruwi | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government-Backed Food Security and Import Substitution Programs

State-backed food security policy remains the clearest near-term support for the Oman indoor farming market. The Food Security Lab 2025 roadmap, unveiled in October 2025, linked import-substitution goals to value-chain mapping, investment facilitation, and cluster development under the 11th Five-Year Plan. Strong fiscal incentives and streamlined land-allocation processes are accelerating private investment into controlled-environment agriculture projects, while targeted grants and low-interest financing are lowering entry barriers for vertical farms and hydroponic operators. Simultaneously, rising consumer demand for year-round, high-quality produce and water‑efficiency mandates are making indoor farming economically attractive.

Water-Stress Economics Favor Closed-Loop Cultivation

Water economics are turning into a direct commercial reason to adopt indoor farming in Oman. Agriculture accounts for more than 80% of total national water withdrawals, and groundwater pressure remains severe across Al Batinah and interior aquifers. Hydroponics and aquaponics can use up to 90% less water per kilogram of produce than traditional field cultivation, which gives the Oman indoor farming market a clear cost argument in addition to a sustainability one. A 2024 trial at the Rumais Agricultural Research Center showed that root zone cooling, solar-powered ultra-low-energy drip systems, and insect-proof net houses reduced water use by 85% and energy use by 90%, while cucumber net income reached nearly 4 times that reported in comparable United Arab Emirates trials.

Expansion of Smart Greenhouse and Agri-City Infrastructure

Physical infrastructure investment is lowering the entry barrier for indoor farming operators in Oman. The plan for 3 agricultural cities in Saham, Dhahirah, and Al Najd was confirmed in February 2025, with a combined investment of OMR 3 billion (USD 7.8 billion), and construction already underway at Saham and Al Najd from 2024. The Jinan Tech project at Sultan Qaboos University added conventional, IoT-smart, and hybrid greenhouse structures on one site, providing growers with a live test bed for training and performance comparisons before they commit capital. These facilities are concentrated in agri-cities and integrated agri-industrial zones near urban centers such as Muscat and Sohar.

Premium Retail and Hospitality Demand for Pesticide-Free Local Produce

Premium food channels are providing indoor growers in Oman with more stable off-take conditions. In July 2024, Alila Jabal Akhdar launched the country’s first luxury hotel hydroponic farm on a 646-square-meter site, and the property later received EarthCheck Gold Certification in February 2025[2]Source: Oman Observer Staff, “Alila Jabal Akhdar Launches Oman’s First Luxury Hotel Hydroponic Farm,” Oman Observer, omanobserver.om. Trufud’s produce is now sold through Al Fair, Sultan Center, Spinneys, and Talabat, which shows that indoor-grown leafy greens have moved beyond a niche shelf position in Muscat’s premium grocery channel. Hotel buyers also behave differently from supermarket shoppers because menu consistency and provenance matter more than unit price, which strengthens year-round contract farming models. That pattern is visible in Al Maskaan Village’s May 2024 supply agreement with Trufud and in the 2025 use of hydroponic ingredients at Amouage Cafe within Alila Jabal Akhdar’s hospitality offer.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cooling and Electricity Intensity in Oman’s Summer Climate | -1.8% | Oman-wide, worst in the interior governorates and the Al Batinah coastal plain | Long term (≥ 4 years) |

| Skilled Agronomy, Automation, And Maintenance Talent Gap | -1.5% | Oman-wide, most acute outside Muscat and Sohar | Long term (≥ 4 years) |

| Nutrient, Substrate, And Spare-Parts Import Dependence | -1.2% | Oman-wide, especially acute for high-tech plant factory operators | Medium term (2-4 years) |

| Demand Volatility for Premium-Priced Indoor-Grown Produce Outside Muscat | -0.8% | Secondary cities, including Nizwa, Sur, Ibri, and Rustaq | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cooling and Electricity Intensity in Oman’s Summer Climate

Energy remains the most persistent operating challenge for indoor farms in Oman. Summer temperatures regularly exceed 40°C across the interior and coastal zones, forcing climate-controlled facilities to keep cooling systems near peak load for extended periods. Research covering Oman found that evaporative cooling alone accounted for around 35% of total controlled-environment agriculture energy use, and performance weakened further as coastal humidity rose. Oman's Authority for Public Services Regulation (APSR) Decision 44/2024 introduced an agricultural electricity tariff of 12-24 baisas per kWh from January 2025[3]Source: Oman Observer Staff, “New Agricultural Electricity Tariff Structure, APSR Decision 44/2024,” Oman Observer, omanobserver.om, which means larger plant factories can drift toward commercial-rate cost exposure as consumption increases. Solar integration helps at the margin, but even the Mustadeem program’s rollout of 55 independent 10 kW solar systems in North Batinah does not remove the capital burden of retrofitting larger facilities.

Skilled Agronomy, Automation, and Maintenance Talent Gap

Indoor farming depends on a skills base that is still narrow in Oman. Vision 2040 aims to raise cultivated land from 544 km2 to 1,044 km2 and lift food self-sufficiency to 70%, yet the labor pipeline for crop science, automation, and equipment maintenance is still developing more slowly than the project pipeline. Innovation Center in Sohar has expanded digital agronomy training, but current capacity remains small relative to the scale of planned agri-city and smart greenhouse rollouts. Companies such as Rakeeza are trying to reduce labor intensity through automation, but these systems add upfront cost that smaller farms and prosumer users may struggle to absorb. The result is a two-sided weakness where low-skill operating labor remains common, while the supply of Omani agronomists, technicians, and systems integrators is still limited.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Facility Type: Greenhouses Anchor Revenue While Vertical Farms Accelerate

Greenhouses accounted for the largest facility type, 58.0% of the Oman indoor farming market share in 2025. That lead reflects the country’s existing base of semi-intensive evaporatively cooled and net-house structures, especially along Barka and the wider Al Batinah coastal plain. The segment also benefits from lower capital costs per square meter than plant factories, making it attractive for high-volume fruiting vegetables and seedling production. Aquaponics remains a smaller but differentiated facility model, supported by Al Arfan Farms’ annual production potential of more than 120 metric tons of vegetables and 30 metric tons of tilapia, as well as WaterFarmers’ new Oman project targeting 300 metric tons of barramundi alongside 5 acres of greenhouse crops.

Indoor vertical farms are the fastest-growing facility segment, with a projected 16.2% CAGR from 2026 to 2031. Their momentum strengthened after the December 2025 launch of Smart Vegetable Farms in Oman, which introduced industrial-scale, closed-systems focused on leafy vegetable production. Containerized vertical farms are also gaining traction in hotels and remote institutional settings where modular deployment matters more than scale. The Jinan Tech project at Sultan Qaboos University has set a practical benchmark for operators considering an upgrade path from evaporative greenhouse systems to more comprehensive climate control.

By Growing System: Hydroponics Dominates As Precision Systems Gain Ground

Hydroponics accounted for the largest share of the Oman indoor farming market in 2025, at 61.0% of the market size, making it the core production method in the Oman indoor farming market. That position comes from the country’s established base of nutrient film technique and Dutch bucket systems, especially across the Batinah greenhouse corridor. Rakeeza’s work on locally formulated MBK hydroponic fertilizers is one early move toward input localization for this segment. Soil-based protected systems and hybrid formats still serve growers who want climate protection without taking on the full cost of a fully soilless facility.

Aeroponics is the fastest-growing system category and is projected to rise at a 14.8% CAGR through 2026 to 2031. Their growth is tied to plant factory deployments that require tighter root-zone control and lower water retention in the growing medium. Aquaponics plays a distinct role by combining fish and vegetable production within a single recirculating system, aligning with Oman’s food security focus and its reliance on protein imports.

By Crop Type: Fruiting Vegetables Lead Volume While Short-Cycle Crops Accelerate

Fruits and vegetables accounted for the largest crop type, 37.0% of Oman indoor farming market size in 2025, and remain the largest crop group in Oman’s indoor sector. Tomatoes and cucumbers dominate this segment because Dutch bucket and drip systems are already well established in Barka and North Batinah. Those crops also fit greenhouse economics, where a protected growing environment can extend the season without requiring a full plant factory build.

Leafy greens are the fastest-growing crop set, with a projected CAGR of 15.4% from 2026 to 2031. That pattern aligns closely with the Smart Vegetable Farms program and with premium retail demand in Muscat for short-cycle fresh produce. Trufud’s range of more than 15 products, including baby romaine, curly kale, Boston lettuce, basil, thyme, rosemary, microgreens, and edible flowers, shows how broad the short-cycle category has become in premium channels. Seedlings, nursery crops, and ornamentals complete the crop base, with GDS claiming more than 5 million square feet of automated greenhouse production capacity for nursery output

By End User: Commercial Growers Dominate As Hospitality Offtake Formalizes

Commercial growers are the largest end user, accounting for 76.0% of the market share in Oman. This structure reflects the capital intensity of indoor farming and the technical demands of managing yields, nutrient regimes, and food-safety consistency at scale. A smaller number of experienced operators, therefore, continue to account for most output. Setting up and managing indoor farms generally involves significant initial investment in climate control systems, LED lighting, irrigation infrastructure, automation technologies, and monitoring equipment.

Foodservice and hospitality are the fastest-growing end-user segments, with a projected CAGR of 14.1% through 2026 to 2031. That growth is tied to formal hotel supply programs, the expansion of luxury tourism corridors, and stronger demand for traceable local produce in branded hospitality settings. Modern retail and e-grocery represent the next major demand layer, and Trufud’s presence across Muscat’s main supermarket chains and on Talabat shows that indoor-grown produce can scale when shelf-life and logistics are well managed. Institutional demand from schools, hospitals, government cafeterias, and the military supply sector remains underdeveloped, but future procurement frameworks could expand this channel.

Geography Analysis

The Oman indoor farming market is a single-country study, as geographic differences within Oman are mainly shaped by climate, logistics, and the location of premium demand. Greater Muscat remains the main consumption anchor for indoor-grown leafy greens, herbs, and premium fruiting vegetables supplied from nearby production clusters. Modern retail penetration is deepest in the capital, and Muscat’s hotel network is moving more steadily toward contracted local supply through premium chains and delivery platforms.

Dhofar and the Salalah area form the second major geography for the Oman indoor farming market. The Khareef season creates a different production rhythm there, with cooler and wetter months that support open-field temperate crops but still leave room for indoor systems focused on non-seasonal and premium categories. Al Najd Agricultural City, near Thumrait, has already entered construction and includes controlled-environment facilities for onion and garlic projects. Salalah Gardens adds a separate agritourism model that blends controlled cultivation with retail and hospitality activity, while interior governorates such as Dakhiliyah, Al Sharqiyah, and Dhahirah are still earlier in the transition from traditional smallholder farming to protected systems.

Al Batinah, across both the North and South governorates, is the main production base for the Oman indoor farming market. The Barka cluster hosts Trufud’s 13,600 square meter complex, Thamra Foods’ 3 hydroponic farms totaling 8,000 square meters, Gulf Mushroom Products’ campus, and several smaller operator. Its flat terrain, land access, and proximity to Muscat make it the natural site for scaled greenhouse growth. The February 2025 MAFWR and OMIFCO hydroponics project also targeted saline-affected Batinah land, while the Saham Agricultural City and the Agriculture Innovation Centre in Sohar are reinforcing the region’s role as Oman’s leading indoor farming corridor

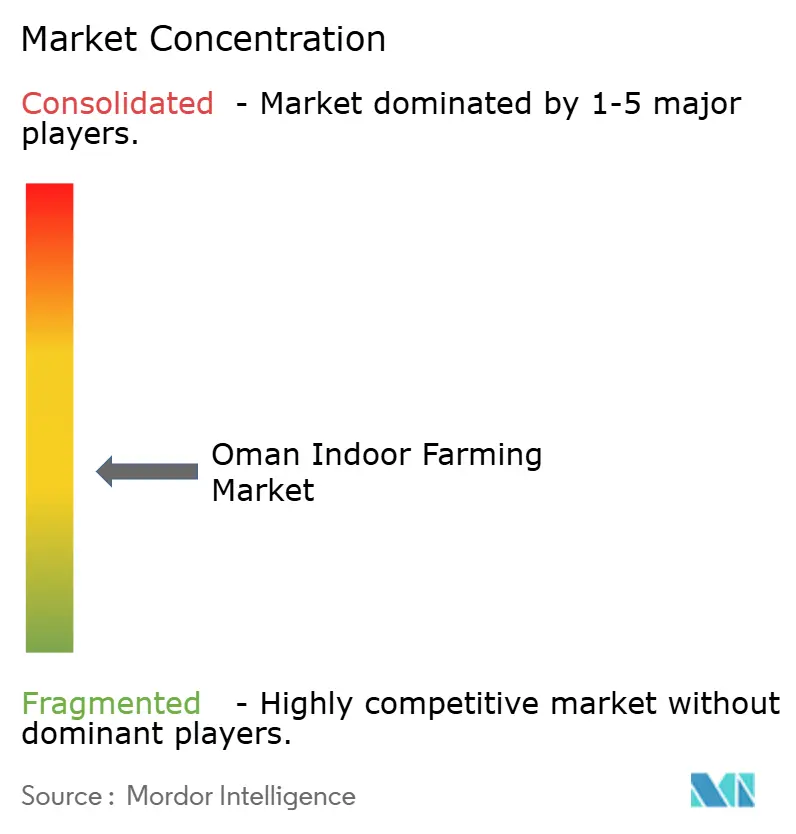

Competitive Landscape

In 2025, the Oman indoor farming market was moderately fragmented. The top five players, including Gulf Mushroom Products Company SAOG, Trufud Trading SPC, Thamra Foods LLC, GDS General Development Services LLC, and Al Arfan Farms, accounted for a significant combined market share. Trufud has built its position around pesticide-free branding and modern retail access, while GDS remains strongest in nursery and greenhouse-linked production services. Thamra Foods and Al Arfan Farms serve different operating niches through hydroponic farming services and aquaponics-based production of fish and vegetables.

MJ iFarm targets smaller modular installations, which broadens the field beyond large farm operators. Competitive white space remains open in premium aquaponics-linked seafood and specialty mushroom categories beyond button varieties, as well as in national institutional supply contracts that current growers have not yet built at scale. The Oman indoor farming market is also separating into technology-led and conventional operator groups as localized nutrients, IoT management, and benchmarking systems become more important to margins and reliability.

This structure should remain open through the forecast period because first movers are not guaranteed to lock in long-term dominance. State-backed agri-city projects are creating subsidized new entry points where smaller firms can access utilities and shared infrastructure without funding full greenfield builds on their own. That lowers some of the scale advantage held by existing operators, even if execution still favors companies with stronger agronomy and logistics capabilities. The result is a market where scale matters, but strategic partnerships, technical know-how, and channel access will matter just as much as acreage or installed equipment.

Oman Indoor Farming Industry Leaders

Gulf Mushroom Products Company SAOG

Trufud Trading SPC

Thamra Foods LLC

GDS General Development Services LLC

Al Arfan Farms

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: The Ministry of Agriculture, Fisheries, and Water Resources (MAFWR) plans to present 400 agricultural investment opportunities valued at RO400 million (USD 1.04 billion). This initiative highlights the government's ongoing efforts to provide commercially structured indoor farming opportunities for private sector operators.

- October 2025: WaterFarmers Inc. detailed the construction of a new coupled aquaponic RAS farm in Oman targeting 300 metric tons per year of barramundi integrated with 5 acres of deep-water-culture greenhouse crops, including baby-leaf greens, vine tomatoes, and herbs. The facility uses 80 dual-drain circular grow-out tanks and Linde SOLVOX Venturi oxygenation systems to maintain biosecurity and production stability across its independent RAS modules .

- May 2024: Trufud Trading SPC signed a strategic supply agreement with Al Maskaan Village to provide a consistent stream of fresh organic leafy vegetables for residents and Al Maskaan Catering, supporting Oman Vision 2040 food-security objectives and demonstrating the formalization of institutional off-take relationships for indoor-grown produce.

Oman Indoor Farming Market Report Scope

Indoor farming involves cultivating crops in controlled environments, such as greenhouses, warehouses, shipping containers, or purpose-built indoor facilities. The Oman indoor farming market report is segmented by facility type (greenhouses, indoor vertical farms, plant factories, indoor aquaponics farms, and mushroom growing chambers), by growing system (hydroponics, aquaponics, aeroponics, soil-based controlled environment systems, hybrid systems), and by crop type (fruits and vegetables, herbs and microgreens, seedlings and nursery crops, leafy greens, and ornamentals). The market forecasts are provided in terms of value (USD).

| Greenhouses | Low-tech greenhouses |

| Mid-tech evaporatively cooled greenhouses | |

| High-tech climate-controlled greenhouses | |

| Indoor Vertical Farms | Building-based vertical farms |

| Container-based vertical farms | |

| Plant Factories | |

| Indoor Aquaponics Farms | |

| Mushroom Growing Chambers |

| Hydroponics | Nutrient Film Technique |

| Deep Water Culture | |

| Dutch Bucket and Drip Systems | |

| Ebb and Flow Systems | |

| Aquaponics | |

| Aeroponics | |

| Soil-based Controlled Environment Systems | |

| Hybrid Systems |

| Leafy Greens |

| Herbs and Microgreens |

| Fruits and Vegetables |

| Seedlings and Nursery Crops |

| Ornamentals |

| Commercial Growers |

| Foodservice and Hospitality |

| Modern Retail and E-grocery |

| Institutional Buyers |

| Home and Prosumer Systems |

| By Facility Type | Greenhouses | Low-tech greenhouses |

| Mid-tech evaporatively cooled greenhouses | ||

| High-tech climate-controlled greenhouses | ||

| Indoor Vertical Farms | Building-based vertical farms | |

| Container-based vertical farms | ||

| Plant Factories | ||

| Indoor Aquaponics Farms | ||

| Mushroom Growing Chambers | ||

| By Growing System | Hydroponics | Nutrient Film Technique |

| Deep Water Culture | ||

| Dutch Bucket and Drip Systems | ||

| Ebb and Flow Systems | ||

| Aquaponics | ||

| Aeroponics | ||

| Soil-based Controlled Environment Systems | ||

| Hybrid Systems | ||

| By Crop Type | Leafy Greens | |

| Herbs and Microgreens | ||

| Fruits and Vegetables | ||

| Seedlings and Nursery Crops | ||

| Ornamentals | ||

| By End User | Commercial Growers | |

| Foodservice and Hospitality | ||

| Modern Retail and E-grocery | ||

| Institutional Buyers | ||

| Home and Prosumer Systems | ||

Key Questions Answered in the Report

What is the projected value of the Oman indoor farming sector by 2031?

The Oman indoor farming market was USD 149.10 million in 2025 and USD 164.51 million in 2026 to reach USD 283.10 million by 2031, registering a CAGR of 11.51% between 2026 to 2031.

Which facility type generates the most revenue in indoor farming in Oman?

Greenhouses led revenue in 2025 with a 58.0% share because they offer a lower capital cost per square meter than plant factories for high-volume crops.

Which crop group is growing fastest in Oman controlled-environment agriculture space?

Leafy greens, herbs, and microgreens are the fastest-growing crop category, with a projected 15.4% CAGR through 2031.

Why is hydroponics so dominant in Oman?

Hydroponics accounted for 61.0% of revenue in 2025 because it aligns with Oman's water constraints, an established greenhouse base, and existing operator experience with NFT and Dutch bucket systems.

Page last updated on: