Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

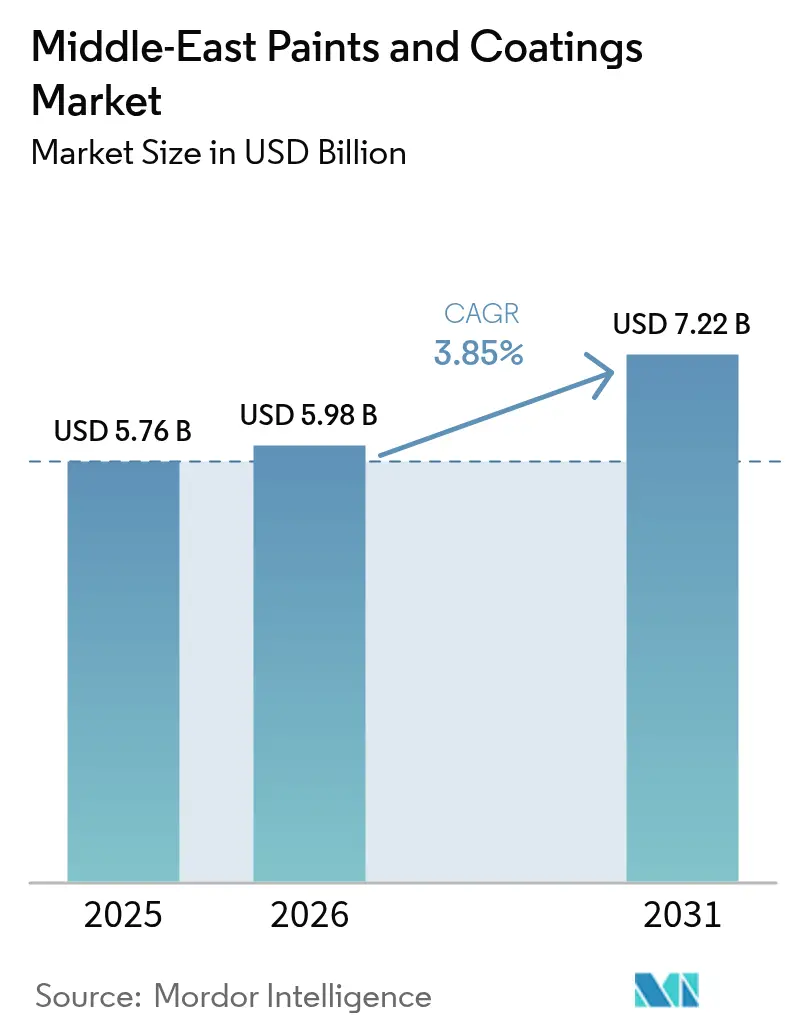

| Base Year Market Size (2025) | USD 5.76 Billion |

| Market Size (2026) | USD 5.98 Billion |

| Market Size (2031) | USD 7.22 Billion |

| Growth Rate (2026 - 2031) | 3.85% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle-East Paints And Coatings Market Analysis by Mordor Intelligence

The Middle East Paints and Coatings Market size in 2026 is estimated at USD 5.98 billion, growing from 2025 value of USD 5.76 billion with 2031 projections showing USD 7.22 billion, growing at 3.85% CAGR over 2026-2031. Solid demand visibility comes from tourism-led giga-projects, strict low-VOC rules, and localization incentives that enlarge both volume and value pools. Firms able to supply water-borne, self-cleaning, or highly durable polyurethane systems secure pricing leverage, while those tied to solvent-borne chemistries face the costs of reformulation. Local manufacturing expansion in Saudi Arabia and the UAE shortens lead times and limits currency risk. Price volatility in titanium dioxide and logistics disruptions in the Red Sea compress short-term margins, yet they also accelerate forward-buying and vertical-integration strategies. Intensifying competition raises the bar on technical service, with certified applicators now pivotal in winning large façade or pipeline jobs.

Key Report Takeaways

- By resin type, acrylics held a 34.00% share of the Middle East paints and coatings market size in 2025, and polyurethane grades are projected to grow at a 4.18% CAGR between 2026 and 2031.

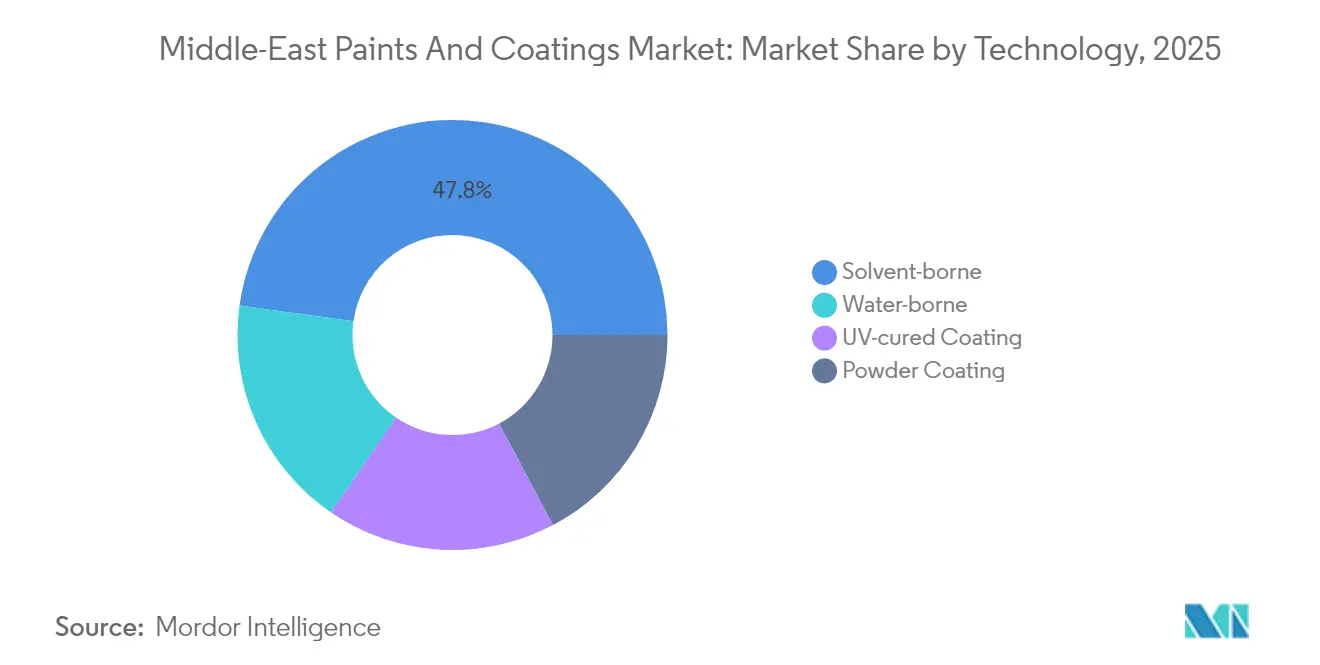

- By 2025, solvent-borne systems accounted for 47.80% of the Middle East paints and coatings market share, while water-based chemistries registered the fastest growth rate of 4.26% through 2031.

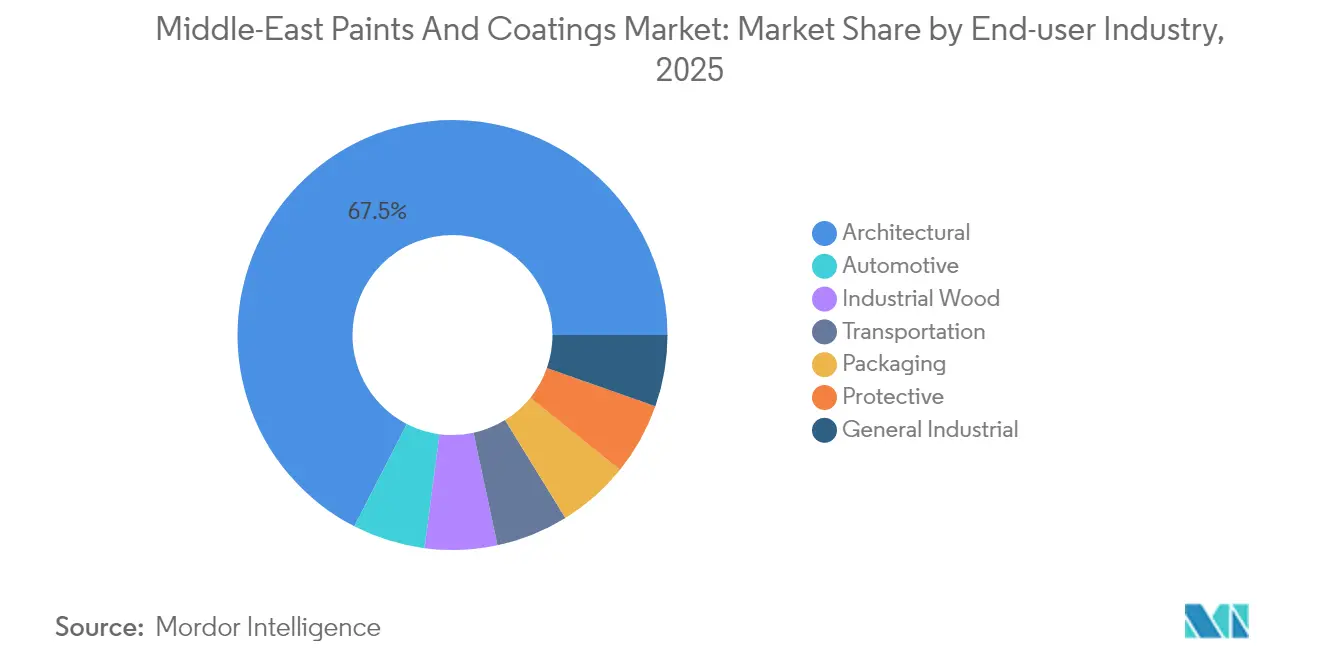

- By end-user industry, architectural coatings led with a 67.45% revenue share in 2025; the segment is expected to advance at a 4.10% CAGR through 2031.

- By geography, Saudi Arabia captured 31.05% of the Middle East paints and coatings market size in 2025 and is set to expand at a 4.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle-East Paints And Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Focus on tourism-led giga-projects (Saudi NEOM, Expo City Dubai) | +1.2% | Saudi Arabia, UAE core with spillover to Qatar, Oman | Long term (≥ 4 years) |

| Booming commercial and residential construction pipeline | +1.0% | Global Middle East, concentrated in GCC | Medium term (2-4 years) |

| Regulatory shift to low-VOC water-borne systems | +0.8% | GCC countries with Dubai Municipality leading | Medium term (2-4 years) |

| Localization incentives for regional paint production | +0.6% | Saudi Arabia, UAE primary with Oman emerging | Long term (≥ 4 years) |

| Rapid uptake of self-cleaning facade coatings for high-rise maintenance | +0.4% | UAE, Qatar, Kuwait urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Focus on tourism-led giga-projects (Saudi NEOM, Expo City Dubai)

Saudi Arabia’s USD 500 billion NEOM development and Dubai’s USD 2.7 billion Expo City extension project shift spending from cyclical construction toward permanent infrastructure that demands premium, climate-adapted coatings. NEOM’s 200,000-strong workforce creates secondary residential and commercial builds that multiply coating volumes, while the focus on architectural icons shifts preferences toward polyurethane and self-cleaning products. These projects, therefore, convert temporary exhibition or hospitality structures into long-term asset classes that require higher-value maintenance cycles[1]Source: NEOM Communications Team, “NEOM Project Progress Update 2025,” neom.com.

Booming commercial and residential construction pipeline

A USD 3.9 trillion MENA project pipeline ensures a predictable pull for the Middle East paints and coatings market across the decade. The UAE’s USD 590 billion commitments and Saudi Arabia’s USD 1.5 trillion backlog include high-value mixed-use towers, downstream energy plants, and logistics hubs that require both corrosion-resistant and decorative systems. Energy–linked contracts, such as ADNOC’s AED 720 million local procurement award, increase protective-coating volume in harsh, salt-laden environments.

Regulatory transformation toward low-VOC systems

More than 27,000 unified Gulf standards now govern coating chemistry, while Dubai Municipality VOC thresholds, bilingual safety data sheets, and SABER certification in Saudi Arabia move compliance close to European norms. The rulebook rewards firms that already conduct water-borne R&D, thereby accelerating the 4.41% CAGR for compliant systems. Initial formulation spending tightens margins, yet the medium-term prize is preferred-supplier status in public contracts.

Localization incentives for regional paint production

Saudi Vision 2030 and the UAE’s “Make it in the Emirates” program anchor tariff breaks, grant funding, and domestic-content rules. SIPCO’s January 2025 purchase of Premium Paints and Oman’s USD 300 million polymer plant demonstrate how regional value chains are transitioning from import models to integrated hubs, reducing freight exposure and driving scale benefits for early movers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in petro-derived raw-material prices | -0.7% | GCC, especially UAE and Saudi Arabia | Short term (≤ 2 years) |

| Stricter VOC and indoor-air-quality compliance costs | -0.4% | GCC early adopters | Medium term (2-4 years) |

| Shortage of certified spray-application labour | -0.3% | UAE, Qatar, Kuwait | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Raw-material price volatility pressures margins

Titanium dioxide hovering near USD 1,974 per metric ton and Red Sea shipping delays force producers to boost safety stocks, stretch working capital, and hedge feedstocks. While GCC petrochemical expansion is expected to ease long-term resin supply, short-term price swings still closely mirror global energy markets. Smaller regional firms, lacking integration or procurement scale, feel the squeeze hardest, hastening them as takeover targets for well-capitalized rivals.

Compliance costs challenge solvent-based incumbents

Water-borne conversions demand new dispersion equipment, employee training, and parallel inventory during the transition. Dubai Municipality’s label-traceability rules and SABER digital audits mean non-compliant batches risk border rejections. Large multinationals spread their R&D outlays across global portfolios, while niche regional players either partner for technology or exit low-margin lines[2]Dubai Municipality, “VOC Limits for Building Materials,” dm.gov.ae.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Polyurethane narrows the gap with acrylic

Acrylics controlled 34.00% of the market in 2025, thanks to their affordability; however, polyurethanes posted the fastest 4.18% CAGR through 2031, as specifiers seek UV resistance and a long lifecycle in desert sun. Epoxy and alkyd grades hold niche roles in oil-and-gas and heritage restoration work. Investment in hybrid chemistries, led by research from the Technology Innovation Institute on soft-material composites, hints at next-generation blends that merge the cost efficiency of acrylic with the robustness of polyurethane. Manufacturing footprints expand accordingly, with National Paints' lifting capacity to 264 million liters to serve premium growth pockets.

Deadline-driven giga-projects reward suppliers able to scale polyurethanes without sacrificing color consistency or cure time. As plant numbers increase, regional buyers negotiate shorter lead times and in-country technical service support, embedding local labs within Saudi and Emirati industrial zones. This dynamic raises the floor for quality across the Middle East paints and coatings market and deepens barriers to low-spec imports.

By Technology: Water-borne chemistries outpace yet do not displace solvent-borne

Solvent-borne systems still represent 47.80% in 2025, but water-borne grades advance at 4.26% CAGR on the back of VOC limits and welfare concerns for applicators laboring in enclosed, climate-controlled spaces. Powder and UV-cure segments accelerate in specialty equipment casings, fixtures, and high-speed furniture lines, aided by Qemtex’s 10,000-tonne UAE plant. DELTA Coatings’ new Dubai site, which runs partly on solar power, increases polyurea output for fast-return pipeline and tank linings.

During the next five years, regulators and end-users will converge on a performance-plus-compliance mindset, transforming water-borne from a cost-premium option into the baseline for public tenders. Vendors wielding on-site tinting hubs and digital color-matching win contracts by guaranteeing exact shade replication despite quick-dry constraints. The mix shift therefore builds volume for dispersant, neutralizing amine, and rheology-modifier suppliers inside the Middle East paints and coatings market.

By End-User Industry: Architectural segment remains the growth engine

Architectural projects commanded a 67.45% share in 2025 and are expected to continue growing at a 4.10% CAGR through 2031. Towers, resorts, and smart-city districts pivot away from basic whitewash toward textured, fade-resistant, and dirt-shedding solutions. Automotive coatings are expected to follow as Saudi and Emirati vehicle-assembly corridors mature, while pipeline corrosion programs increase protective-coating demand in Abu Dhabi and the Eastern Province.

Interior designers and real estate investors now issue tender documents stipulating solar-reflective index values and antimicrobial ratings. These add-ons boost average selling prices and reward firms that bundle paint, warranty, and applicator training. As product SKUs proliferate, distributors are adopting e-catalogs, stock-optimization software, and same-day tint delivery to builders, thereby strengthening their ties to leading brands in the Middle East paints and coatings market.

Geography Analysis

Saudi Arabia’s robust 4.55% CAGR springs from public-sector capital flows into diversified industry parks, leisure islands, and green energy platforms. Contract models emphasize domestic labor and on-shore suppliers, prompting multinationals to co-invest in Jubail or Yanbu facilities. The shift accelerates innovation centers focused on testing and training for arid-climate products.

The UAE remains a leading market for product launches, thanks to Dubai’s design-centric real estate landscape and Abu Dhabi’s energy megaprojects. Government purchasing rules that grant preference to VOC-compliant portfolios accelerate waterborne penetration. Logistics services improve as the Khalifa Port Free Zone offers bonded warehousing and re-export incentives to the wider GCC.

Qatar, Kuwait, and Oman form the next tier. Qatar targets façade makeovers in economic zone expansions around Hamad Port. Kuwait revitalizes petrochemical assets, demanding high-build epoxy novolacs. Oman’s Sohar and Duqm corridors position the sultanate as both a raw-material and finished-goods node, cushioning freight risk for the wider Middle East paints and coatings market.

Competitive Landscape

The Middle East Paints and Coatings Market is moderately fragmented. Capital outlays are shifting toward plant automation, energy-efficient reactors, and on-site solar arrays, helping to keep unit costs in check even as electricity subsidies decline. Technology collaborations emerge, with Axalta partnering with Gulf universities on thermal-reflective topcoats and Hempel forming a partnership with ADNOC for in-service hull performance tracking. Training centers in Dubai and Dammam fill certified applicator gaps and create lock-in for preferred spray equipment and consumables. White space lies in smart or functional coatings—anti-carbonation concretes, anti-viral interiors, and roof membranes that reduce HVAC load. Smaller innovators team up with Emirates-based venture funds to scale niche chemistries, eyeing exit routes via trade sale to the large formulators once pilot adoption hits breakeven. As MEPCA harmonizes testing protocols, product approvals accelerate, reducing market entry lead times.

Middle-East Paints And Coatings Industry Leaders

Akzo Nobel N.V.

Jotun

Jazeera Paints

Hempel A/S

NATIONAL PAINTS FACTORIES CO. LTD.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Jazeera Paints officially launched its products in select SACO company showrooms. This move is a strategic part of Jazeera's broader expansion plans, aiming to craft an environment where innovative paints and construction solutions seamlessly blend with essential home items and furniture, catering to both indoor and outdoor needs.

- April 2025: ONYX COATING officially launched its franchise in Saudi Arabia, marking a significant milestone for both the company and the Kingdom's automotive sector. This move introduces cutting-edge vehicle protection technologies to one of the Middle East's automotive markets.

Middle-East Paints And Coatings Market Report Scope

Paints and coatings can be classified as water-based and solvent-based based on the drying technique employed. Water-based coatings contain water as a volatile compound, and solvent-based coatings contain volatile compounds like benzene. Paints and coatings are used to decorate and protect buildings, appliances, automobiles, equipment, and others. The market is segmented by resin type, technology, end-user industry, and geography. By resin type, the market is segmented into acrylic, alkyd, polyurethane, epoxy, polyester, and other resin types. By technology, the market is segmented into water-borne, solvent-borne, radiation cure, and other technologies. By end-user industry, the market is segmented into architectural, automotive, wood, general industrial coatings, transportation, and other end-user industries. The report also covers the market size and forecast for the Middle-East paints and coatings market in eight countries across the region. For each segment, the market sizing and forecasts have been done on the basis of value (USD million).

By Resin Type

| Acrylic |

| Alkyd |

| Polyurethane |

| Epoxy |

| Polyester |

| Others (Silicone, Vinly, Fluoropolymer) |

By Technology

| Water-borne |

| Solvent-borne |

| Powder Coating |

| UV-cured Coating |

By End-user Industry

| Architectural |

| Automotive |

| Industrial Wood |

| Protective |

| Transportation |

| General Industrial |

| Packaging |

By Geography

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| Iran |

| Iraq |

| Rest of Middle East |

| By Resin Type | Acrylic |

| Alkyd | |

| Polyurethane | |

| Epoxy | |

| Polyester | |

| Others (Silicone, Vinly, Fluoropolymer) | |

| By Technology | Water-borne |

| Solvent-borne | |

| Powder Coating | |

| UV-cured Coating | |

| By End-user Industry | Architectural |

| Automotive | |

| Industrial Wood | |

| Protective | |

| Transportation | |

| General Industrial | |

| Packaging | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain | |

| Iran | |

| Iraq | |

| Rest of Middle East |

Key Questions Answered in the Report

What is the current value of the Middle East paints and coatings market?

It is valued at USD 5.98 billion in 2026, with a forecast to hit USD 7.22 billion by 2031.

Which segment contributes most to coating demand in the region?

Architectural applications lead with 67.45% share in 2025 and retain the fastest growth at 4.10% CAGR.

How fast are water-borne coatings growing in the Gulf?

Water-borne chemistries register a 4.26% CAGR from 2026 to 2031, outpacing the overall market.

Why is Saudi Arabia so important for suppliers?

The kingdom holds 31.05% of regional demand and posts a 4.55% CAGR, supported by Vision 2030 mega-projects.

What risks affect producers’ margins?

Feedstock price swings, shipping delays in the Red Sea, and compliance expenses tied to low-VOC rules squeeze profitability.

Page last updated on: