Middle East And Africa Pulp And Paper Industry Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

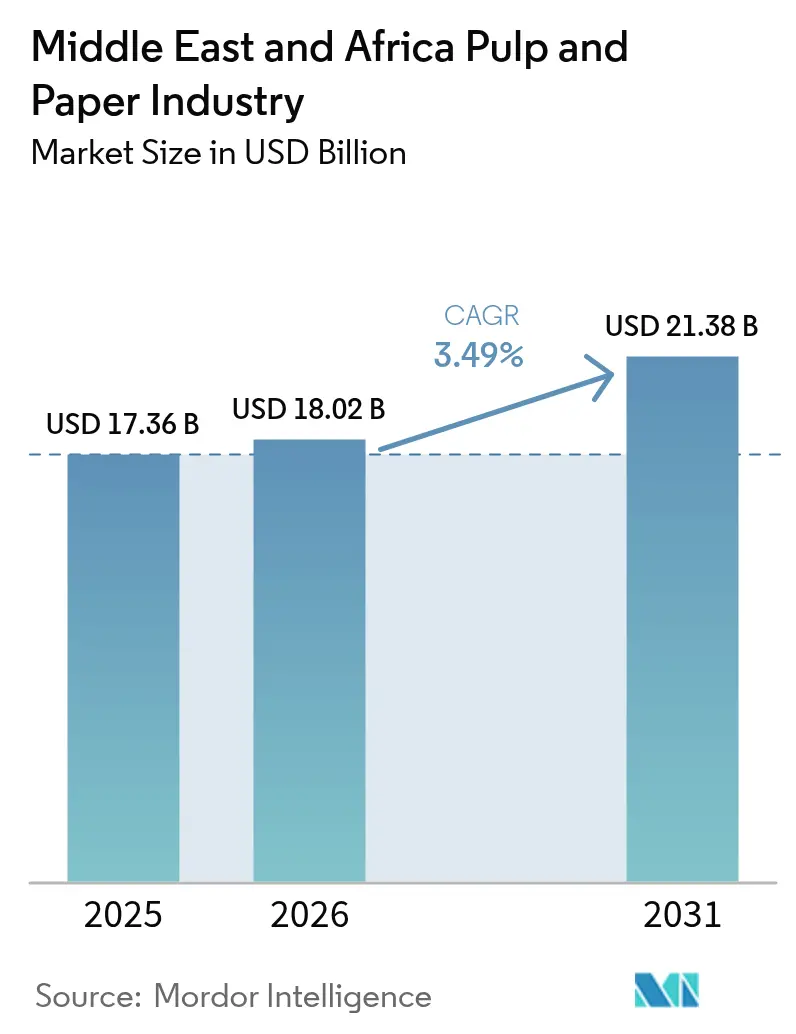

| Base Year Market Size (2025) | USD 17.36 Billion |

| Market Size (2026) | USD 18.02 Billion |

| Market Size (2031) | USD 21.38 Billion |

| Growth Rate (2026 - 2031) | 3.49% CAGR |

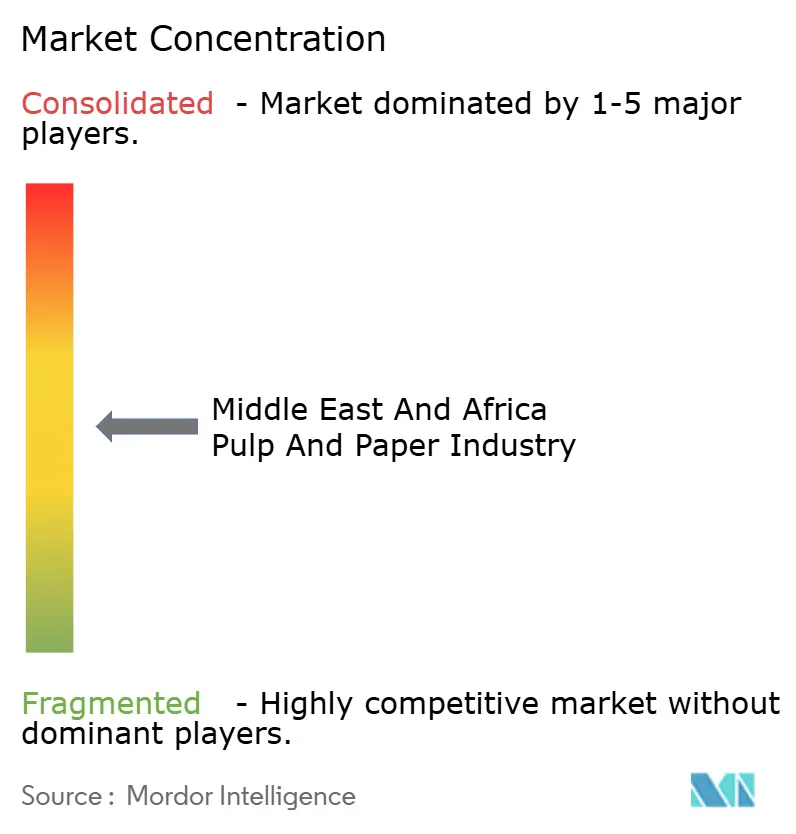

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Pulp And Paper Industry Analysis by Mordor Intelligence

The Middle East and Africa pulp and paper market size is projected to expand from USD 17.36 billion in 2025 and USD 18.02 billion in 2026 to USD 21.38 billion by 2031, registering a CAGR of 3.49% between 2026 and 2031. Structural fiber shortages keep recovered-paper imports elevated, while sovereign capital in the Gulf Cooperation Council (GCC) bankrolls integrated mills and alternative-fiber pilots that temper raw-material risk. Rising e-commerce parcel volumes in South Africa and Saudi Arabia, single-use plastic bans in Kenya and the United Arab Emirates (UAE), and steady population growth across North and East Africa underpin boxboard, cartonboard, and tissue consumption. Currency depreciation in several African markets compresses converter margins but also accelerates import-substitution investments as producers seek to localize feedstock, energy, and logistics. Freight disruption on Red Sea lanes has reinforced the strategic premium on regional self-sufficiency, prompting leading mills to diversify shipping routes and sign longer-tenor supply contracts with Gulf and Indian suppliers.

Key Report Takeaways

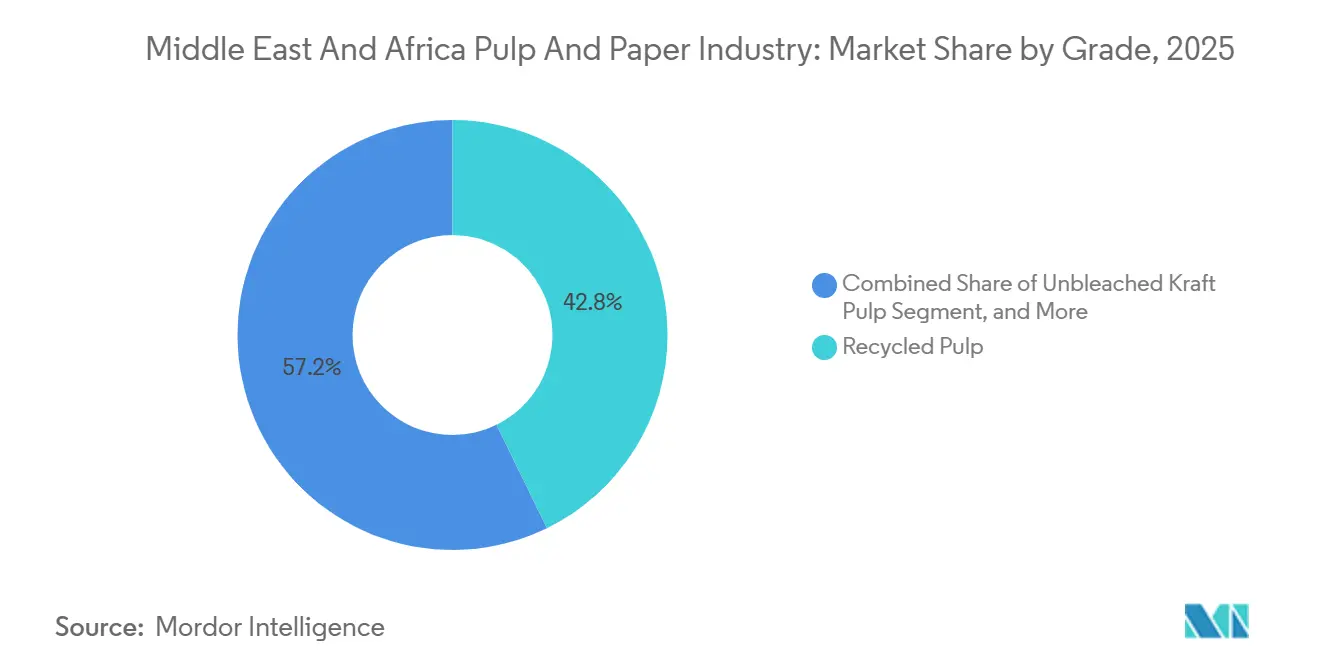

- By grade, recycled pulp led with 42.76% of the Middle East and Africa pulp and paper market share in 2025, while dissolving wood pulp is forecast to post the fastest CAGR at 4.43% through 2031.

- By application, containerboard accounted for 31.12% of revenue in 2025, whereas tissue is projected to expand at a 4.61% CAGR between 2026 and 2031.

- By end-user industry, consumer goods packaging accounted for 30.63% of 2025 demand, and hygiene products are set to advance at a 4.38% CAGR over the forecast period.

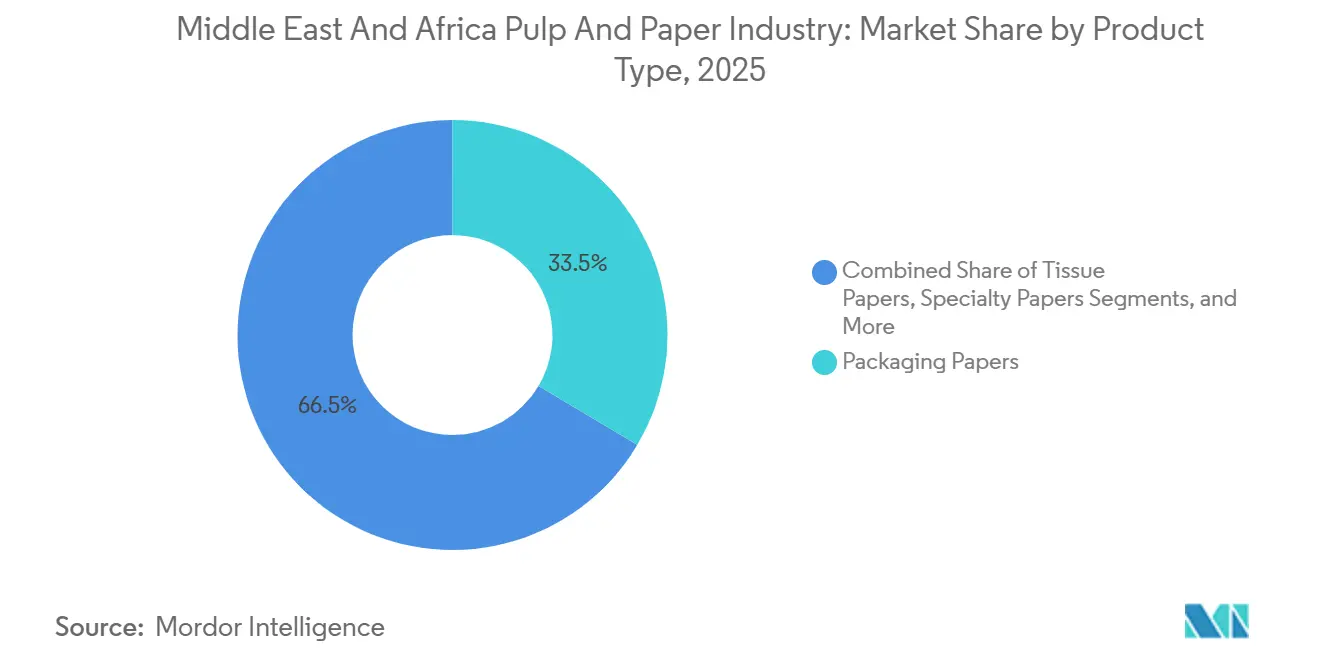

- By product type, packaging papers accounted for 33.53% of 2025 turnover, with tissue papers poised for 4.27% CAGR growth.

- By process technology, recycled-fiber lines accounted for 44.21% of 2025 revenue, while integrated pulp and paper mills are on track for a 4.27% CAGR of expansion as investors pursue vertical integration.

- By geography, Middle East dominated with 54.32% share in 2025, whereas the Africa is expanding at a 3.92% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Pulp And Paper Industry Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing E-Commerce Packaging Demand | +0.9% | South Africa, UAE, Saudi Arabia, Kenya | Medium Term (2–4 Years) |

| Rising Urban Middle-Class Consumption of Tissue Products | +0.8% | Kenya, Nigeria, Egypt, GCC Urban Centers | Long Term (≥ 4 Years) |

| Government Bans on Single-Use Plastics Shifting Demand to Paper-Based Substitutes | +1.1% | Kenya, UAE, Egypt, Nigeria, Ethiopia, Ghana | Short Term (≤ 2 Years) |

| Surge in GCC Investment Into Integrated Pulp and Paper Capacity | +0.7% | Saudi Arabia, UAE, Kuwait | Medium Term (2–4 Years) |

| Date-Palm Agri-Residue Trials Lowering Fiber Deficit | +0.3% | Saudi Arabia, UAE, Iraq | Long Term (≥ 4 Years) |

| Maritime Free-Zone Circular-Economy Incentives | +0.4% | UAE Free Zones, Saudi Arabia Economic Cities | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Growing E-Commerce Packaging Demand

Rapid digital-commerce adoption is rewriting corrugated-box demand curves. Domestic containerboard output in South Africa cannot keep pace with the 30% jump in online sales volume, prompting converters to source linerboard from Southeast Asia at elevated freight premiums. GCC logistics reforms that target faster customs clearance are expected to triple intra-regional parcel flows, encouraging mills to invest in light-weight, high-strength grades that trim shipping weight U.AE. The African Continental Free Trade Area (AfCFTA) digital-trade protocol further accelerates last-mile logistics into landlocked economies, reinforcing containerboard as the backbone of retail fulfillment packaging. Producers that couple post-consumer fiber procurement with automated fluting lines are best positioned to capture this incremental tonnage.

Rising Urban Middle-Class Consumption of Tissue Products

Urbanization in sub-Saharan Africa surpassed 43% in 2024, yet household tissue use still trails the global average by a wide margin. New tissue machines in Saudi Arabia and Kuwait deploy through-air-drying and structured-roll technologies that yield premium softness with lower fiber input, enabling mills to differentiate on quality while defending margins. Multinational hygiene brands report mid-single-digit regional sales growth, validating demand resilience even amid currency volatility. With hospitality pipelines expanding across GCC tourism hubs, away-from-home tissue demand is also rising, supporting diversified grade portfolios.[1]Crown Paper Mill, “Tissue Facility Commissioning 2026,” crownpapermill.com

Government Bans on Single-Use Plastics Shifting Demand to Paper-Based Substitutes

Regulatory momentum is tilting procurement toward recyclable and compostable substrates. Kenya’s 2024 extended producer responsibility (EPR) law imposes collection quotas that raise the cost of non-recyclable plastics, accelerating the adoption of molded-fiber trays, paper wraps, and paper straws. Dubai’s 2025 phase-two plastic ban eliminates polystyrene serviceware, pushing fast-food chains to switch to grease-resistant cartonboard.[2]Dubai Municipality, “Single-Use Plastic Ban Phase Two,” dm.gov.ae Egypt and Nigeria are drafting similar decrees with minimum recycled-content thresholds, spurring investment in de-inking and aqueous-coating lines. Short-cycle policy shifts amplify near-term tonnage upside for paper converters with certified food-contact grades.

Surge in GCC Investment into Integrated Pulp and Paper Capacity

Sovereign funds and family conglomerates are committing billions to backward integration to hedge freight and currency risks. A flagship Saudi project will double domestic containerboard output by late 2027, while a UAE corn-starch plant supplies bio-based binders that cut reliance on petrochemical inputs. Rebuilt tissue lines in Kuwait integrate energy-recovery systems, slicing gas consumption by one-quarter per tonne. These capital programs aim to displace imports, capture value-added margins, and secure strategic autonomy in essential packaging grades.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Wood-Chip Import Prices | -0.6% | UAE, Saudi Arabia, Egypt | Short Term (≤ 2 Years) |

| Chronic Water-Stress in MENA Limiting Mill Permitting | -0.8% | Saudi Arabia, UAE, Egypt, Jordan, Yemen | Long Term (≥ 4 Years) |

| Port Congestion and Red Sea Security Surcharges | -0.5% | Egypt, Saudi Arabia, Kenya | Short Term (≤ 2 Years) |

| Currency Depreciation in Key African Markets | -0.4% | South Africa, Kenya, Nigeria, Egypt | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Chronic Water-Stress in MENA Limiting Mill Permitting

Middle East and North Africa (MENA) freshwater availability is forecast to slip below the 500 m³ per-capita scarcity threshold by 2030, forcing regulators to tighten industrial effluent limits. Egypt has already delayed several high-capacity pulp projects until mills can prove desalination or wastewater-reuse solutions.[3]ITF-OECD, “Red Sea Maritime Disruptions Report 2024,” itf-oecd.org Because chemical pulping consumes roughly three times as much water as recycled-fiber lines, investors increasingly favor recovered-paper plants and non-wood feedstocks such as date-palm residues that require minimal bleaching. The cap-ex premium for water treatment, combined with rising desalinated-water tariffs, weighs on expansion economics and nudges project pipelines toward lower-intensity technologies.

Port Congestion and Red Sea Security Surcharges

Security incidents around the Bab el-Mandeb choke point diverted many Asia-Europe strings around the Cape of Good Hope, stretching voyages by up to two weeks and catapulting spot rates above USD 3,500 per forty-foot equivalent. For pulp and wastepaper cargoes valued at USD 13,000–23,000 per TEU, additional surcharges of USD 160–272 per box eroded converter spreads and ballooned working-capital needs. Mills in Egypt and western Saudi Arabia now carry higher safety stocks, inflating inventory costs, while some buyers have shifted sourcing to North American and Brazilian suppliers that route via the Atlantic despite longer lead times.[4]World Bank, “MENA Water Scarcity Projections 2024,” worldbank.org Persisting maritime risk continues to keep cost volatility elevated.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Recycled Pulp Dominates, Dissolving Wood Pulp Accelerates

Recycled pulp secured the largest slice of 2025 revenue, reflecting chronic fiber shortages and EPR rules that incentivize post-consumer collection networks U.AE. Multiple mills upgraded drum pulpers and screening lines to handle mixed-paper bales imported from Europe, tightening loop economics and improving furnish quality. On the premium end, dissolving wood pulp is on track for the quickest growth, buoyed by viscose-staple-fiber expansion in Turkish and Egyptian textile clusters that target European apparel brands seeking sustainable cellulose inputs. The Middle East and Africa pulp and paper market size for dissolving wood pulp is projected to expand at a 4.43% CAGR through 2031, supported by a 110,000-tonne capacity addition at Sappi’s Saiccor mill. Alternative fibers such as date-palm residues promise to displace up to 8% of imported wood chips once commercial trials reach scale, offering mills a hedge against volatile international chip prices.

The grade mix continues to favor closed-loop solutions. Integrated GCC projects pair Kraft lines with recycled furnish to flex grades in response to spot-pulp swings, while African converters rely on swing imports until local forestry programs mature. Government R&D grants in the UAE support solvent-based delignification of agricultural waste, with pilot runs demonstrating pulp yields above 50% and water savings of nearly 60% versus hardwood kraft U.AE.

By Application: Containerboard Leads, Tissue Surges

Containerboard commanded 31.12% of 2025 application turnover, anchored by food-export packaging and surging e-commerce volumes. The Middle East and Africa pulp and paper market share for this segment is forecast to remain dominant as GCC mills add nearly 900,000 tpa of testliner and fluting by 2028. Lightweight, high-burst grades below 125 gsm are gaining ground among parcel shippers seeking freight savings, nudging furnish recipes toward higher recycled-fiber ratios. Tissue, however, exhibits the fastest trajectory at a 4.61% CAGR. Retail shelves across Kenya, Nigeria, and Egypt are broadening SKU ranges from economy one-ply to premium three-ply rolls, lifting average value per tonne. Tourism-led demand in the UAE and Saudi Arabia is driving growth in away-from-home products such as napkins and towels, prompting mills to commission energy-efficient crescent-former machines.

Printing and writing papers see secular volume erosion but remain relevant in textbook contracts funded by African education ministries. Specialty papers, though low in tonnage, deliver margins two to three times those of containerboard, prompting converters in Egypt and South Africa to install silicone-coating and security-thread embedding lines that serve regional label and banknote markets.

By End-User Industry: Consumer Goods Packaging Anchors, Hygiene Products Climb

Consumer goods packaging absorbed 30.63% of 2025 demand as multinational fast-moving consumer goods (FMCG) firms insisted on primary and secondary packs that comply with plastic-reduction pledges. Cartonboard and sack kraft benefit from higher box-compression requirements in ambient logistics chains, while grease-resistant wraps replace polystyrene clam-shells in quick-service restaurants post-ban. The Middle East and Africa pulp and paper market size for hygiene products is forecast to register 4.38% CAGR, propelled by rising birth rates in sub-Saharan Africa and medical-tourism spillover in the Gulf that push demand for diapers, fem-care, and adult incontinence products. Brand owners co-locate converting assets near new tissue capacities to skirt tariff barriers and cut freight on bulky finished rolls.

Industrial users take niche volumes in abrasive backing and electrical insulation, but the regulatory burden of REACH and IEC standards shields this pocket from commoditization. Publishing and education sales remain stable where government textbook subsidies persist, though offset demand migrates to digital in higher-education segments.

By Product Type: Packaging Papers Lead, Tissue Papers Gain

Packaging papers topped the product taxonomy, accounting for 33.53% of 2025 sales, spanning linerboard, folding-boxboard, sack kraft, and wrap grades. Gulf mills optimize furnish blends to meet European recycled-content mandates, chasing export premiums tied to EU Packaging and Packaging Waste Regulation targets. Tissue papers are set for a 4.27% CAGR as capacity additions in Saudi Arabia and the UAE deploy structured-roll and through-air-drying technologies that cut fiber input by double-digits while delivering premium softness. In the Middle East and Africa pulp and paper market size context, tissue’s incremental tonnage equates to roughly two new 60,000 tpa machines per year across the forecast horizon. Graphic papers retreat as office-automation and digital media eat into demand, whereas specialty papers command price markups of 40-80% but require strict ISO 13485 and ISO 9001 compliance, narrowing the qualified supplier pool.

Innovation centers on barrier coatings that replace polyethylene extrusion with water-based or bio-polymer layers, enabling recyclability and compostability. Producers that master dispersion-barrier technology will unlock higher-margin food-service and liquid-packaging channels as plastic bans tighten.

By Process Technology: Recycled Fiber Processing Dominates, Integrated Mills Rise

Recycled-fiber systems held 44.21% market share in 2025, a testament to robust recovered-paper import channels and expanding domestic collection under new EPR schemes. Digital waste-trading platforms in the UAE and Kenya now match generators with recyclers in real time, improving bale quality and price transparency. The Middle East and Africa pulp and paper market size tied to integrated mills is forecast to grow 4.27% annually as investors couple pulping and papermaking to slash freight and drying costs. South African chemical-kraft lines enjoy captive plantation wood, but power outages push mills to co-fire biomass and install steam-condensate recovery systems that curb energy use by 10-15%.

Mechanical pulping remains a marginal niche because high electricity tariffs and shrinking newsprint volumes erode economics.Hybrid projects that co-locate dissolved pulp and cartonboard capitalize on shared utilities and sludge-to-energy loops, advancing circularity targets while diversifying product risk.

Geography Analysis

The Middle East contributed 54.32% of 2025 revenue, buoyed by Saudi Arabia’s Vision 2030 industrial push and the UAE’s circular-economy milestones. Saudi containerboard capacity is slated to reach 1.2 million tpa by 2028, positioning the kingdom as a net exporter to neighboring Gulf and East African markets. The UAE’s National Agenda for Integrated Waste Management mandates 80% solid-waste treatment by 2031, funneling sorted fiber to local mills and anchoring recycled-pulp economics. Turkey straddles supply chains into Europe and North Africa, but lira volatility and gas-price spikes have deferred two planned board-machine upgrades.

Africa is forecast to expand at a 3.92% CAGR over 2026-2031. South Africa hosts the region’s only full forest-to-board value chains; however, chronic load shedding increases power costs and forces mills to invest in on-site generation. Mondi’s Richards Bay and Sappi’s Ngodwana pulp lines feed both domestic and export channels despite currency swings. Kenya’s 2024 EPR regime is expected to double paper recovery rates to 30% by 2027, improving raw-material security for recyclers in the Nairobi area. Nigeria, Egypt, and Ghana advance single-use plastic bans, but patchy waste-collection infrastructure slows the ramp-up of fiber supply.

Freight and forex headwinds persist. Kenyan shilling depreciation raised landed chip and chemical costs by about 20%, compressing converter EBITDA margins. South African converters hedge rand exposure through forwards, adding up to 3% to working-capital outlays. Still, AfCFTA’s digital-trade rules lower parcel-shipping friction, underpinning containerboard demand growth across landlocked Central African economies.

Competitive Landscape

Market concentration is moderate. The recent Smurfit WestRock merger created a USD 34 billion global packaging heavyweight with Egyptian corrugating assets that supply North African and Levant customers. Mondi’s South African mills generated EUR 494 million (USD 527 million) EBITDA in Q3 2024, leveraging integrated forestry and kraft operations to weather power disruptions. Sappi’s Saiccor expansion positions the firm to serve rising viscose-fiber demand from Turkish and Egyptian spinners seeking traceable cellulose inputs.

Regional actors pursue vertical integration. Middle East Paper Company’s USD 474.6 million PM5 line will double Saudi testliner capacity, while Al Ghurair’s UAE starch facility delivers bio-based adhesives that cut carbon intensity in corrugated converting. Gulf Paper Manufacturing rebuilt its Kuwait tissue line with energy-recovery modules that slash gas usage by one-quarter. Emerging disruptors include UAE and Saudi recyclers piloting date-palm pulp blends, and the UAE’s Tahweel marketplace, which aims to divert 1 million tonnes of paper and cardboard from landfill by 2027, democratizing feedstock access for small mills.

Strategic themes center on alternative fibers, energy efficiency, and proximity to end-use markets to offset freight volatility. Mills that secure ISO 14001 certificates and align with EU due-diligence rules gain export preference. Technology bets favor aqueous-barrier coatings, structured-roll tissue formers, and AI-enabled optical sorters that lift recovered-fiber yield.

Middle East And Africa Pulp And Paper Market Leaders

Smurfit WestRock

International Paper Company

Lions Gate Paper & Pulp LLC

Sappi Limited

Billerud AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Crown Paper Mill commissioned a 60,000 tpa tissue facility in Saudi Arabia that deploys structured-roll technology to reduce fiber use by 12% while maintaining softness metrics.

- January 2026: Al Ghurair opened a 50,000 tpa corn-starch plant in the UAE to supply bio-based adhesives and coatings, with a 20,000 tpa expansion slated for 2028.

- September 2025: The UAE launched the Tahweel digital marketplace, targeting diversion of 1 million tonnes of paper and cardboard from landfill by 2027.

- March 2025: The UAE formed its Circular Economy Council to drive implementation of a waste-management agenda that mandates extended producer responsibility for paper packaging.

Middle East And Africa Pulp And Paper Industry Report Scope

The Middle East and Africa Pulp and Paper Industry Report is Segmented by Grade (Bleached Chemical Pulp, Dissolving Wood Pulp, Unbleached Kraft Pulp, Mechanical Pulp, Recycled Pulp), Application (Printing and Writing, Newsprint, Tissue, Cartonboard, Containerboard, Specialty Papers), End-user Industry (Food and Beverage Packaging, Consumer Goods Packaging, Hygiene Products, Publishing and Education, Industrial and Specialty Applications), Product Type (Graphic Papers, Packaging Papers, Tissue Papers, Specialty Papers), Process Technology (Chemical Pulping, Mechanical Pulping, Recycled Fibre Processing, Integrated Pulp and Paper Mills), and Geography (Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Bleached Chemical Pulp (BCP) |

| Dissolving Wood Pulp (DWP) |

| Unbleached Kraft Pulp |

| Mechanical Pulp |

| Recycled Pulp |

| Printing and Writing |

| Newsprint |

| Tissue |

| Cartonboard |

| Containerboard |

| Specialty Papers |

| Food and Beverage Packaging |

| Consumer Goods Packaging |

| Hygiene Products |

| Publishing and Education |

| Industrial and Specialty Applications |

| Graphic Papers |

| Packaging Papers |

| Tissue Papers |

| Specialty Papers |

| Chemical Pulping |

| Mechanical Pulping |

| Recycled Fibre Processing |

| Integrated Pulp and Paper Mills |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Rest of Africa |

| By Grade | Bleached Chemical Pulp (BCP) | |

| Dissolving Wood Pulp (DWP) | ||

| Unbleached Kraft Pulp | ||

| Mechanical Pulp | ||

| Recycled Pulp | ||

| By Application | Printing and Writing | |

| Newsprint | ||

| Tissue | ||

| Cartonboard | ||

| Containerboard | ||

| Specialty Papers | ||

| By End-user Industry | Food and Beverage Packaging | |

| Consumer Goods Packaging | ||

| Hygiene Products | ||

| Publishing and Education | ||

| Industrial and Specialty Applications | ||

| By Product Type | Graphic Papers | |

| Packaging Papers | ||

| Tissue Papers | ||

| Specialty Papers | ||

| By Process Technology | Chemical Pulping | |

| Mechanical Pulping | ||

| Recycled Fibre Processing | ||

| Integrated Pulp and Paper Mills | ||

| By Geography | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the Middle East and Africa pulp and paper market be by 2031?

It is forecast to reach USD 21.38 billion by 2031, rising at a CAGR of 3.49% from 2026.

Which grade is growing fastest in regional pulp output?

Dissolving wood pulp is set to grow at 4.43% CAGR as textile mills expand viscose and lyocell lines.

What is driving tissue demand across the region?

Urban middle-class expansion and tourism growth are lifting retail and away-from-home tissue volumes, especially in GCC economies.

How are plastic bans affecting packaging demand?

Kenya, the UAE, and others have enacted single-use plastic restrictions that shift procurement toward recyclable paper-based substitutes.

Why are integrated mills attracting new investment?

Vertical integration hedges volatile imported-pulp costs, trims logistics expenses, and positions producers for recycled-content mandates.

Which countries account for the bulk of regional revenue?

Saudi Arabia and the UAE together anchor more than half of regional sales, supported by sovereign-led industrial and circular-economy programs.

Page last updated on: