Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.03 Billion |

| Market Size (2031) | USD 1.71 Billion |

| Growth Rate (2026 - 2031) | 10.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Stevia Market Analysis by Mordor Intelligence

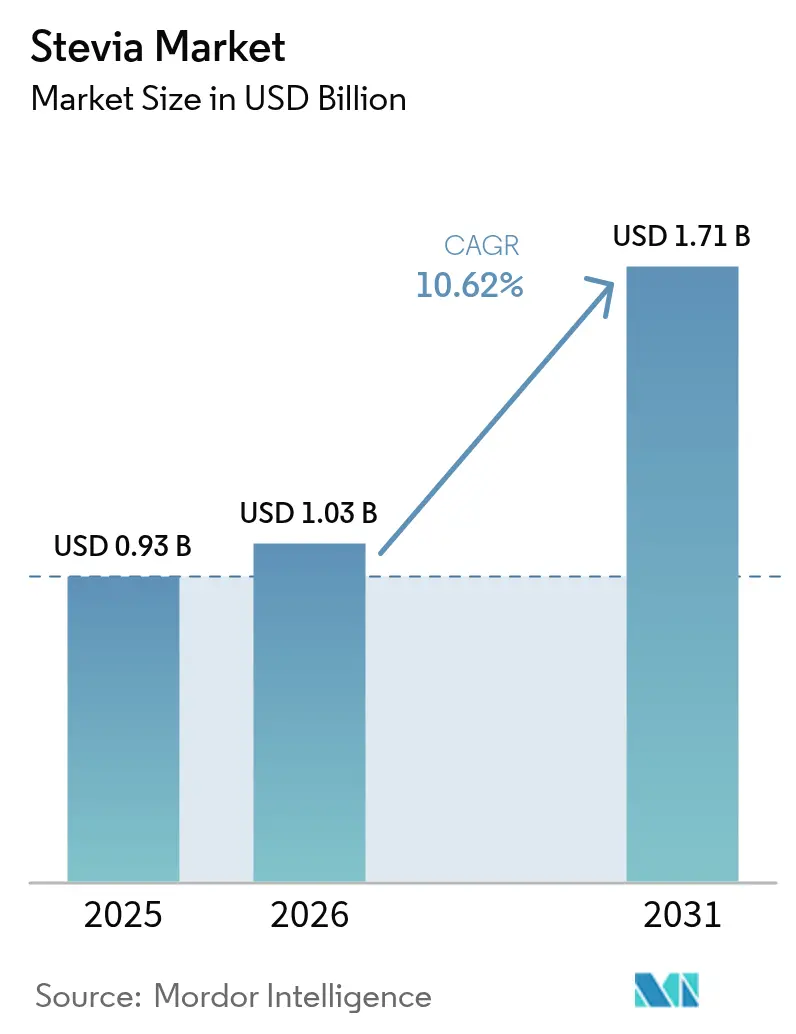

The stevia market size is expected to grow from USD 0.93 billion in 2025 to USD 1.03 billion in 2026 and is forecast to reach USD 1.71 billion by 2031 at 10.62% CAGR over 2026-2031. The global stevia market is shifting rapidly as biotech fermentation delivers high‑purity Reb M at lower costs, driving strong growth in beverages and clean‑label products. Asia‑Pacific, led by China’s production and rising imports, anchors expansion, while powder formats dominate, but liquid solutions gain traction with new solubility technologies. Conventional stevia remains cost‑driven, yet organic variants grow on sustainability demand. Moderate consolidation in the stevia market by major players coexists with agile biotech entrants, while regulatory fragmentation and climate volatility push the industry toward fermentation to secure a stable, scalable supply.

Key Report Takeaways

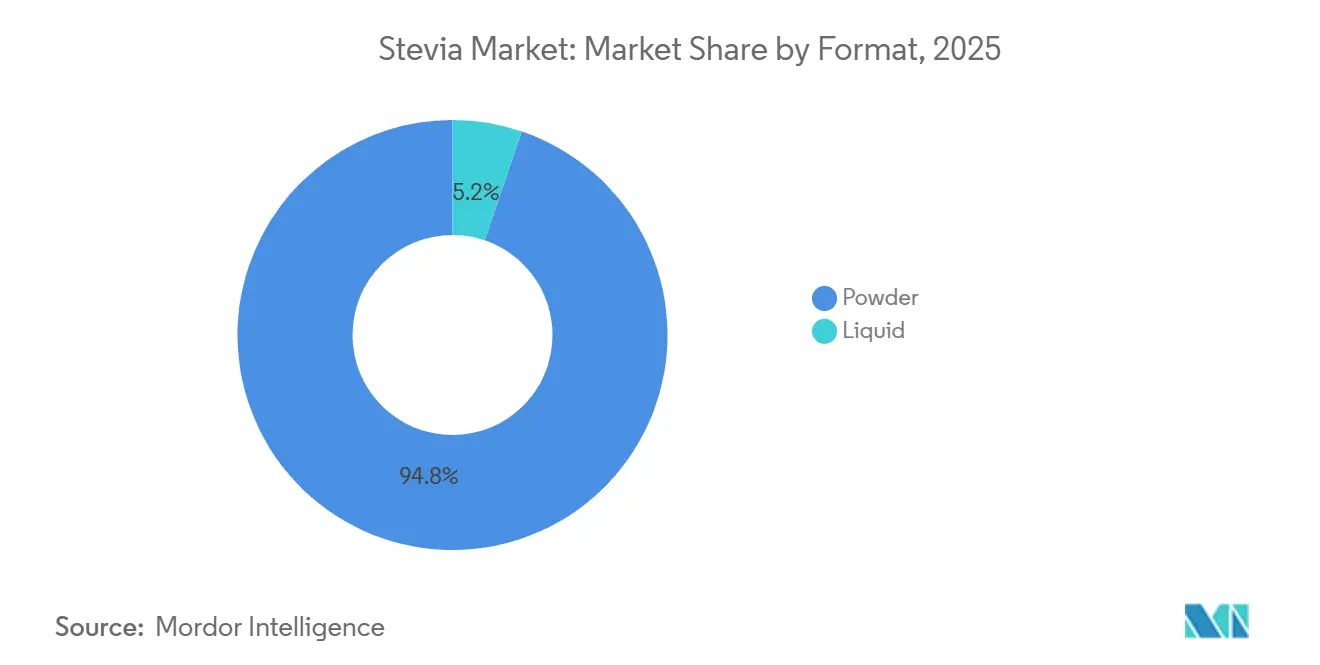

- By format, powder accounted for 94.78% of the stevia market share in 2025, while liquid formats are forecast to grow at 12.31% CAGR through 2031.

- By ingredient type, conventional variants led with an 79.41% share in 2025, whereas organic Stevia is positioned to grow at 11.22% CAGR through 2031.

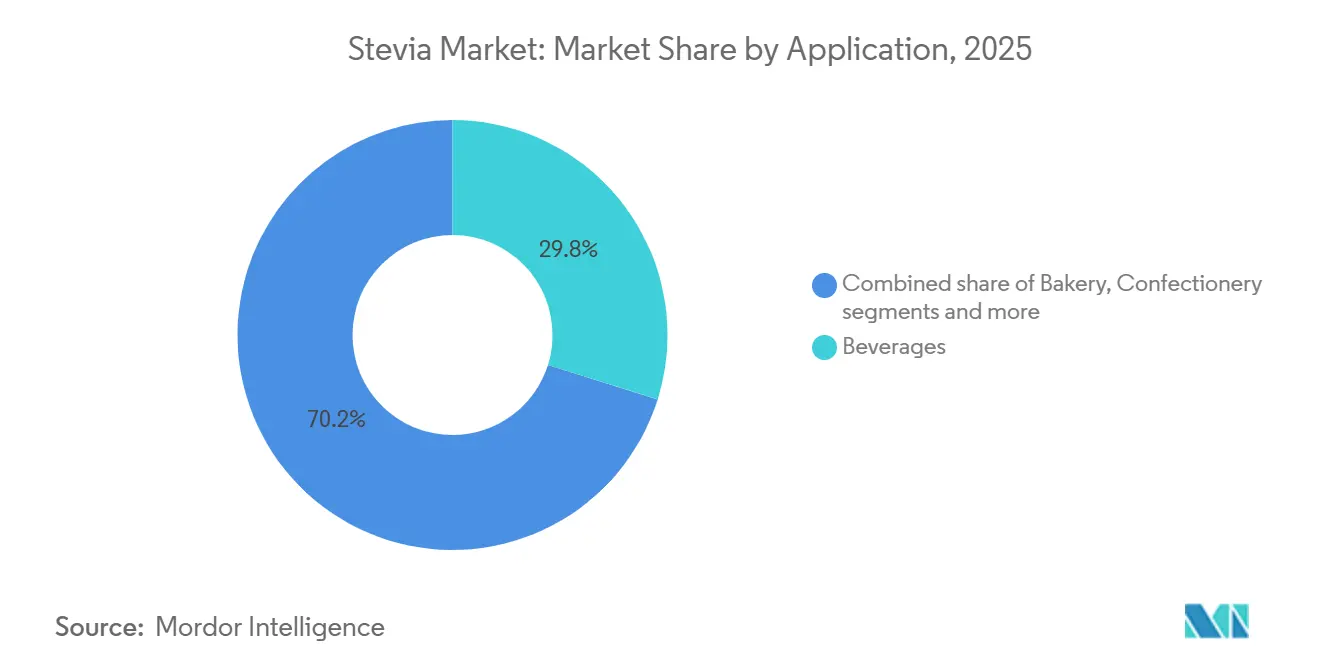

- By application, beverages captured 29.84% share of the Stevia market size in 2025 and are projected to expand at 12.97% CAGR to 2031.

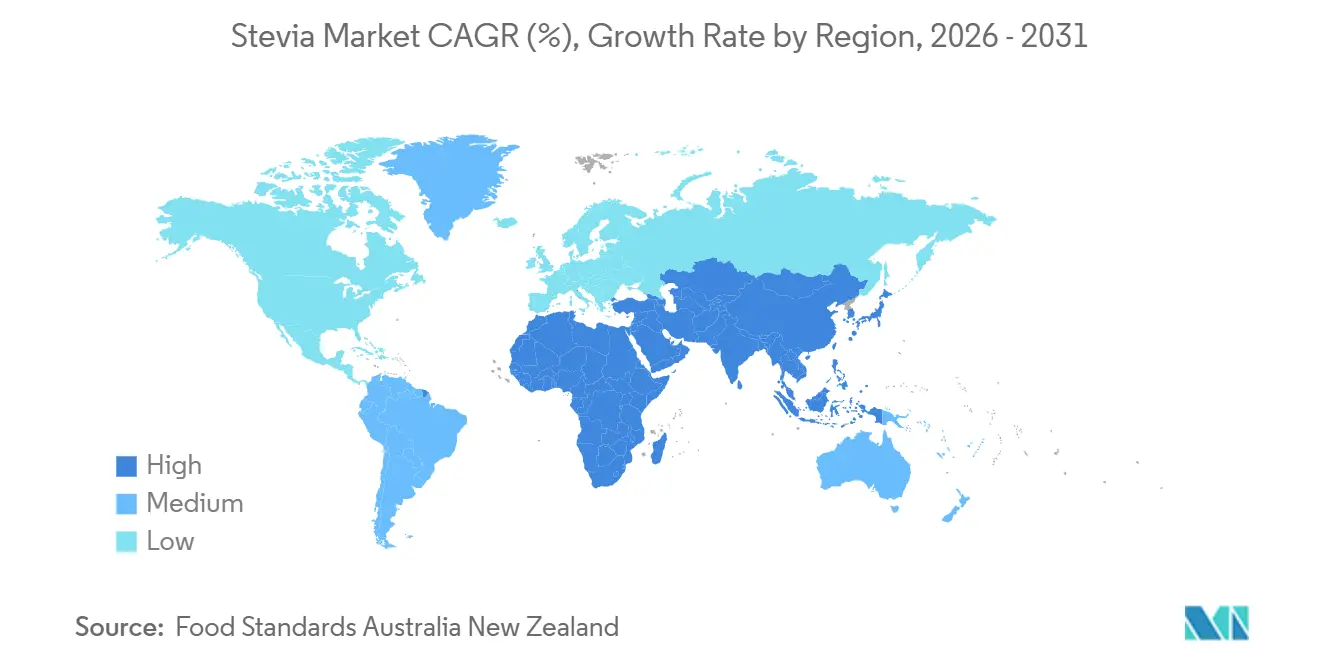

- By geography, Asia-Pacific commanded a 31.05% share of the global stevia market in 2025 and is advancing at 11.94% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Stevia Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift in consumer preference toward natural and plant-based sweeteners | 2.1% | Global, with strongest uptake in North America and Europe | Medium term (2-4 years) |

| Increasing prevalence of diabetes and obesity | 1.8% | Global, concentrated in Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Expanding use of stevia in low- and zero-sugar beverages | 2.5% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Advancements in extraction/processing technologies | 1.4% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Biotech fermentation and bioconversion pathways lowering cost and footprint | 1.9% | Global, led by North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Growing popularity of natural sweeteners in sports nutrition and protein products | 0.9% | North America, Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shift in consumer preference toward natural and plant-based sweeteners

Global consumer preference is clearly shifting toward natural and plant‑based sweeteners, creating strong momentum for stevia adoption. Clean‑label mandates from major retailers are pushing suppliers to eliminate artificial sweeteners, while widespread sugar‑sweetened beverage taxes are accelerating reformulation toward zero‑calorie options. Stevia’s botanical origin gives brands a unique edge in maintaining “natural” claims under evolving EU and FDA standards, unlike synthetic alternatives. Regulatory advancements, like the FDA's GRAS approvals for steviol glycosides in May 2025, enhance trust by confirming safety and versatility [1]Source: U.S. Food and Drug Administration, "Recently Published GRAS Notices and FDA Letters", fda.gov. Leading companies such as Coca‑Cola have already reformulated flagship products with stevia to hedge against regulatory risk, and the trend is evident in the surge of new beverage launches featuring stevia compared to synthetics. This convergence of regulatory pressure, retailer mandates, and consumer demand positions stevia as a central driver in the global stevia market and broader sweetener landscape.

Increasing prevalence of diabetes and obesity

As the global prevalence of diabetes and obesity rises, stevia is emerging as a favored zero-calorie sweetener, bolstered by supportive policies. The International Diabetes Federation (IDF) Diabetes Atlas highlighted that in 2025, 11.1% of adults aged 20-79, equating to 1 in 9, were living with diabetes, with over 40% unaware of their condition[2]Source: International Diabetes Federation, "Diabetes facts and figures", idf.org. With diabetes rates set to surge, especially in the Asia-Pacific and other developing regions, governments are tightening nutritional regulations. They've introduced front-of-pack warning labels that penalize products high in added sugars. These initiatives are reshaping purchasing habits, particularly among health-conscious millennials and Gen Z, by diminishing the shelf visibility and appeal of sugary foods. Stevia, with its zero glycemic index and non-insulin-stimulating properties, is becoming the go-to choice for reformulating diabetic-friendly and reduced-sugar products. Major food players like Nestlé and Danone are broadening their portfolios within the stevia market through stevia-sweetened dairy and dessert lines, highlighting the direct link between rising metabolic health concerns and the growing mainstream adoption of stevia.

Expanding use of stevia in low- and zero-sugar beverages

The global stevia market is gaining strong momentum from its rapid penetration into low- and zero-sugar beverages, the fastest-growing application segment, as beverage manufacturers demand sweeteners that deliver high solubility, thermal stability, and consistent taste over extended shelf life. Recent advances, such as Ingredion’s high-dispersion Reb M solutions, have overcome earlier technical limitations like cloudiness and sedimentation, enabling stevia’s use in clear RTD formats. Leading brands such as PepsiCo and Unilever are reformulating flagship products with stevia blends to cut calories while maintaining sugar‑like sweetness, demonstrating how fermentation‑derived Reb M provides consistent performance compared to variable leaf extracts. This shift underscores stevia’s strategic role in beverage reformulation across the stevia market, where consumer acceptance hinges on taste parity with sugar and regulatory pressure continues to favor zero‑calorie alternatives.

Advancements in extraction/processing technologies

Advancements in extraction and processing technologies are transforming the global stevia market by making premium glycosides more cost‑effective and scalable. Techniques such as ultrasound‑assisted extraction and supercritical fluid extraction have significantly reduced processing times and energy use while improving purity levels, and membrane filtration now enables continuous purification with less waste. These innovations, combined with fermentation‑based production, have lowered the price of high‑quality Reb M, allowing mid‑tier brands to incorporate stevia into mainstream confectionery and bakery products. Ingredion's expansion of its bioconversion facility in Malaysia highlights the industry's focus on scaling advanced technologies. Patent filings for improved rebaudioside M solubility, including PureCircle's contributions, reflect efforts to enhance product quality. These innovations are strengthening competitiveness across the stevia market by increasing access to high-quality steviol glycosides, particularly Reb M and Reb D, while integrating biotechnology with traditional methods to strengthen the supply chain and meet growing global demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility of stevia-leaf prices linked to climate and agriculture | -1.2% | Global, acute in South America and East Africa | Short term (≤ 2 years) |

| Stringent regulatory requirements and lengthy approval processes sweeteners | -0.8% | Global, most pronounced in Europe and Asia-Pacific | Medium term (2-4 years) |

| Sensory challenges of rare-glycoside blends in high-acid RTD beverages | -0.6% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Geographic concentration of cultivation heightening ESG-related supply risk | -0.5% | Global, concentrated in China, Paraguay, Kenya | Long term (≥ 4 years |

| Source: Mordor Intelligence | |||

Volatility of stevia-leaf prices linked to climate and agriculture

Volatility in stevia-leaf pricing, driven by climate variability and agricultural concentration, remains a structural restraint for the global stevia market. Recurrent droughts and erratic weather in key producing regions such as Paraguay, Kenya, and China have reduced yields and degraded glycoside quality, triggering sharp increases in leaf prices and disrupting contract-based supply chains. China’s outsized role in global production further magnifies risk, as localized weather shocks can quickly translate into worldwide price spikes. Limited access to crop insurance among smallholder farmers weakens the effectiveness of long-term sourcing contracts, exposing ingredient buyers to unexpected cost escalation. As a result, multinational sweetener producers in the stevia market are increasingly pivoting toward fermentation-based production to stabilize supply economics and insulate margins from agricultural uncertainty.

Stringent regulatory requirements and lengthy approval processes sweeteners

Stringent and asynchronous global regulatory approval cycles remain a major restraint for the stevia market, as fragmented standards across regions slow innovation and inflate costs. European Food Safety Authority (EFSA’s) lengthy dossier requirements, Japan’s insistence on domestic toxicology studies, India’s restrictive usage caps, and Brazil’s complex traceability rules all force companies to adapt formulations market by market. This lack of harmonization prevents economies of scale, compels multinational brands to maintain multiple SKUs, and raises supply‑chain costs compared to synthetic sweeteners that benefit from unified Codex approvals. As a result, smaller biotech firms face disproportionate compliance burdens, while larger players struggle to accelerate global rollouts of next‑generation stevia blends.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Format: Powder Maintains Market Leadership

In 2025, powder stevia holds a 94.78% share of the stevia market, establishing itself as the preferred choice in food and beverage manufacturing. Powder stevia dominates due to its versatility and performance in solid and semi-solid applications. Bakery, confectionery, tabletop sweeteners, and dairy formulations rely on powdered formats for their superior shelf stability, dosing precision, and ability to replicate sugar’s bulk and texture. In applications such as frozen dairy, powders withstand mechanical stress and temperature fluctuations better than liquids. This clear functional divide underscores a format-driven structure within the stevia market, where liquid stevia is optimized for beverages, while powder remains indispensable across food and tabletop applications.

Liquid stevia is emerging as the fastest-growing format segment, with a projected CAGR of 12.31% from 2026 to 2031. Beverage manufacturers intensify reformulation efforts in low- and zero-sugar drinks. Advances in solubility technology, most notably high-dispersion Reb M liquid systems, have overcome long-standing challenges such as cloudiness and sedimentation, enabling use in clear RTD beverages. These liquid concentrates integrate seamlessly into high-speed bottling lines, reducing processing time, minimizing equipment fouling, and improving flavor consistency, which has driven adoption by leading beverage players in RTD tea and functional drink portfolios. As a result, liquid stevia is expanding rapidly despite its smaller current revenue base.

By Ingredient Type: Conventional Stevia Maintains Dominance

In 2025, conventional stevia commands a dominant 79.41% market share, due to its cost advantages and well-established supply chains that cater to the price-sensitive food and beverage sectors. This dominance stems from economies of scale and processing efficiencies, allowing for competitive pricing in high-volume applications. While China and India bolster conventional supply chains, disruptions such as United States tariffs and concerns over forced labor are prompting shifts in sourcing strategies. Moreover, advanced cultivation practices and technologies are optimizing yields and slashing production costs in these key regions.

Between 2026 and 2031, organic stevia is projected to witness an 11.22% CAGR. This growth is largely fueled by sustainability mandates from retailers and stringent pesticide-free sourcing demands in Europe and North America. Brands are increasingly gravitating towards organic variants, often absorbing higher farm-gate costs to achieve a clean-label and organic market stance. The expansion of certified cultivation is bolstering supply for private-label and health-centric SKUs, propelling the segment's robust growth. Yet, it's worth noting that structural supply constraints pose challenges to the scalability of organic stevia.

By Application: Beverages Dominate Market Position

In 2025, the beverages segment accounted for the largest market share at 29.84%, with a projected CAGR of 12.97% from 2026 to 2031. The segment's growth within the stevia market is primarily driven by regulatory initiatives, such as sugar-sweetened beverage taxes and mandatory front-of-pack labeling requirements. Leading companies, including Coca-Cola and Unilever, are reformulating flagship products with stevia blends to reduce calorie content while maintaining a sugar-like taste. These efforts demonstrate the efficient integration of liquid stevia concentrates into existing production processes with minimal capital investment. High-growth categories, such as RTD teas, sports drinks, and flavored waters, are particularly responsive, enabling beverage applications to surpass the overall market growth rate.

Manufacturers are adopting advanced processing technologies to improve taste profiles, enhancing the appeal of stevia-based products to consumers. Additionally, sugar taxation policies in key markets, such as Saudi Arabia and the UAE, are accelerating this trend[3]Source: The World Health Organization, "A review of sugar-sweetened beverages taxation in Saudi Arabia and United Arab Emirates", emro.who.int. In these regions, a 50% excise tax on sugar-sweetened beverages has significantly reduced consumption and contributed to lower obesity rates, creating a favorable environment for stevia adoption.

Geography Analysis

In 2025, the Asia-Pacific region holds a 31.05% share of the global stevia market and is projected to grow at a 11.94% CAGR from 2026 to 2031. Growth is fueled by China’s dual role as the largest producer and a rising importer of premium Reb M concentrates. Multinational brands are localizing zero‑sugar portfolios to target China’s vast diabetic population, while India’s regulatory approval of steviol glycosides has opened new opportunities despite restrictive usage caps. Japan remains a mature market with long‑standing consumer acceptance, and emerging economies such as Indonesia, Thailand, and South Korea are accelerating adoption through government‑led sugar‑reduction campaigns.

North America and Europe together account for a significant share of global stevia market demand, with growth centered on clean-label and regulatory-compliant reformulation. Accelerated approvals for next-generation steviol glycosides in the United States are enabling wider use in carbonated beverages, while European markets continue to expand despite fragmented labeling rules that complicate fermentation-derived stevia positioning.

South America and the Middle East and Africa play strategically distinct roles in the global stevia ecosystem. South America functions mainly as a supply hub within the global stevia market ecosystem, led by Paraguay’s export-oriented cultivation and Brazil’s evolving regulatory framework, while domestic consumption remains comparatively limited.

Regulatory Landscape

The regulatory framework for steviol glycosides continues to be shaped by safety benchmarks and method-specific specifications across major markets. In the European Union, EFSA reaffirmed the Acceptable Daily Intake (ADI) for steviol glycosides at 4 mg/kg body weight per day (as steviol equivalents) in 2024 for E 960 variants, setting the ceiling that formulators work within when establishing use levels across beverages and other food categories. The EU has also moved to codify additional production routes for steviol glycosides, including fermentation-derived pathways, with Regulation (EU) 2023/447 applying from April 2025 for steviol glycosides produced via Yarrowia lipolytica (E 960b), supporting commercialization of fermentation-origin ingredients alongside leaf-extracted options.

Regulatory fragmentation persists because approvals and permitted conditions differ by jurisdiction and sometimes by production method. In the United States, the FDA GRAS process remains a primary route for new steviol-glycoside ingredients and processing methods, including enzymatic modification. FDA "no questions" letters were issued in 2026 for enzymatically modified steviol glycosides, including CJ CheilJedang (GRN 1288) and Arzeda (GRN 1294). The United Kingdom also updated its food-additives framework via the Food Additives and Novel Foods (Authorisations and Miscellaneous Amendments) (England) Regulations 2024, while international reference points continue to be anchored by FAO/WHO JECFA specifications and the 0 to 4 mg/kg bw ADI range (as steviol equivalents) reflected in JECFA evaluations and monographs.

Competitive Landscape

Numerous regional and international players vie for dominance in the global stevia market, which remains moderately fragmented. Major players, including Cargill, Ingredion, and Tate & Lyle, leverage their vast distribution networks and cutting-edge research and development capabilities to maintain a stronghold. Meanwhile, a host of small and medium enterprises carve out niches by offering products tailored to local preferences and specialized applications. This dynamic competition spurs continuous innovation in product formulations, purity levels, and blends with other sweeteners, granting food and beverage manufacturers a diverse array of choices.

Health-conscious consumers' growing appetite for natural, zero-calorie sweeteners is propelling the market's expansion. The market's moderate fragmentation not only ensures competitive pricing and a diverse product lineup but also opens doors for global market expansion. Companies are turning to advanced technologies, like bioconversion, precision fermentation, and enhanced extraction methods, to boost product quality and trim production costs.

Emerging in the stevia industry, players harnessing precision fermentation and sweet protein technologies are challenging the status quo, disrupting the age-old extraction-based business models. This evolution compels established firms in the stevia industry to innovate and pivot, lest they cede market share. The competitive arena is bifurcating: on one side, technology-centric leaders who can set premium prices, and on the other, producers prioritizing scale and cost-effectiveness.

Stevia Industry Leaders

-

Ingredion Incorporated

-

Tate & Lyle PLC

-

Archer Daniels Midland Company

-

Cargill Incorporated

-

GLG Life Tech Corp.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Commercial whitespace is opening around next-generation stevia solutions that improve taste and reduce reliance on leaf supply, which matters for consistent performance in beverages, where stevia is already the largest application share (29.84% in 2025). Producers are scaling fermentation, bioconversion, and enzymatic-treatment routes to improve access to high-purity Reb M and related glycosides naturally present at very low levels in the leaf, supporting beverage manufacturers that need solubility and stable taste in clear RTD formats. Tate and Lyle and Manus launched the Yume M stevia brand in February 2026 for food and beverage applications, while Arzeda increased ProSweet Reb M capacity, reported at 500 metric tons in North America in 2025, indicating continued investment in biomanufactured stevia supply.

Validation work is also improving pathways for broader adoption of new formats and origins, especially for enzymatically produced and fermentation-derived steviol glycosides. EFSA issued a 2026 safety opinion related to updates to enzymatically produced steviol glycosides (E 960c), and the EU authorization framework for fermentation-derived steviol glycosides (E 960b) has been in application since April 2025, which reduces uncertainty for EU-compliant reformulations. Suppliers are also using approvals and certifications as customer-qualification signals, including Layn Natural Ingredients receiving FEMA GRAS approval (No. 5106) for its SteviUp M2 sweetener in June 2026. These developments support opportunities across zero-sugar beverages, dairy, and tabletop sweeteners, where clean-label positioning, supply stability, and method-specific compliance (leaf extract vs bioconversion vs fermentation) increasingly shape supplier selection and SKU rollout decisions.

Recent Industry Developments

- June 2026: Tate & Lyle launched Yume, a branded portfolio of stevia-derived sweeteners, formalizing its platform approach to sugar-reduction ingredients for food and beverage customers. The launch clarifies its go-to-market positioning for next-generation stevia solutions and supports broader customer adoption through standardized specifications and application support.

- April 2025: Ingredion achieved Farm Sustainability Assessment (FSA) Silver performance level for 100% of its PureCircle stevia supply chain, verified under the Sustainable Agriculture Initiative framework. This positions sustainability verification as a procurement differentiator for large CPG customers that require auditable agricultural sourcing alongside taste and cost performance.

- June 2024: United Kingdom food safety authorities approved the use of PureCircle steviol glycosides produced from bioconversion, supporting commercialization of non-traditional production routes in a major European market. The approval improves supplier flexibility for UK-compliant reformulation programs, especially for beverage and other reduced-sugar applications needing consistent glycoside profiles.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated from stevia-based sweetening ingredients sold into food, beverage, and other end-use applications, counted at the ingredient level across major producing and consuming regions.

Scope exclusions: We exclude finished consumer products where stevia is only one of many ingredients, and we also exclude other non-stevia sweeteners even when they are blended in the final formulation.

Segmentation Overview

-

By Format

- Powder

- Liquid

-

By Ingredient Type

- Organic

- Conventional

-

By Application

- Bakery

- Confectionery

- Beverages

- Dairy

- Table-top Sweeteners

- Other Applications

-

Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean view of demand and supply signals that are visible in public data, and then mapping them to how stevia is used and priced. We referred to sources such as USDA and other agriculture statistics, FAO crop and trade series, UN Comtrade customs data for relevant HS codes, and Codex or regional food additive regulations to understand what can be sold and labeled.

To convert those signals into a usable market model, we also reviewed company annual reports, investor presentations, and credible press coverage to confirm capacity additions, product launches, and application mix changes over time. Where needed, a paid subscription focused on company financials and a patent database were used to cross-check key players activity and technology shifts (like newer glycoside mixes). These desk research sources are illustrative, and many other public references were used for data collection, clarification, and validation.

Primary Interviews and Surveys

Primary work was used to pressure-test the desk assumptions, especially around average selling price movement, blending ratios in formulations, and the split between powder and liquid formats across regions. We spoke with a mix of ingredient suppliers, distributors, and high-usage end customers in food and beverage, with coverage across APAC, EMEA, and the Americas so local pricing and regulation realities were reflected.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 15% | APAC: 52% |

| Mid tier: 52% | Functional/Unit leaders: 34% | EMEA: 29% |

| Smaller Players: 15% | Managers: 51% | Americas: 19% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where food and beverage production and trade signals are reconstructed by region, and then filtered through stevia adoption rates in key applications, which are then multiplied by realistic dosage ranges and price bands. Once that total is formed, it is checked with selective bottom-up approximations using sampled supplier revenues, channel checks, and ASP times volume sanity tests, and gaps are adjusted when the two views cannot be reconciled.

Inputs used in the model include stevia extract pricing by form (powder versus liquid), the mix of use across beverages, bakery and dairy reformulations, regulatory approvals that influence addressable demand, and regional import dependence that can swing supply availability. For forecasting, scenario analysis was applied so adoption growth, pricing softening or tightening, and application expansion could be flexed, and then aligned with what interviewees considered practical for the next few years.

Data Validation & Update Cycle

Outputs are cross-checked against independent signals like trade directionality, reported capacity changes, and application-level demand cues, and then reviewed for outliers that do not match known market events. When large variances appear, assumptions are revisited and respondents are re-contacted to confirm whether the change is a one-off or a structural shift.

Before sign-off, the model and assumptions go through a multi-step analyst review so unit logic, currency conversions, and year alignment are consistent. Reports are refreshed annually, with interim updates when material events occur, and a final freshness check is done close to delivery so clients receive an updated view.

Mordor Intelligence's Stevia Market Size Measured Against Other Published Estimates

Published stevia market numbers often differ, even when they look like they are talking about the same product, because each publisher draws the line at a different point in the value chain. Differences also come from how pricing is averaged across forms and regions, and from whether the number reflects ingredient demand in applications or a narrower sweeteners-only definition.

In this study, the main gap drivers were scope and price logic, since some estimates count only stevia sweeteners while others include a broader ingredient market, and a few use aggressive adoption curves without checking typical dosage ranges and reformulation timelines. The table points to a narrower sweeteners-only scope as the largest reason for the spread, with the ingredient-level view anchored through application mix and powder versus liquid price bands, a scope choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.93 B (2025) | |

| Global Data Publisher A | USD 0.64 B (2025) | Uses a stevia sweeteners-only definition inside a wider high-intensity sweeteners frame, which can exclude some ingredient sales and non-sweetener end uses counted in the broader market view. |

| Industry Publisher B | USD 0.87 B (2025) | Leans more on historic revenue reporting with a different application mapping, and the price averaging appears less sensitive to regional mix shifts between powder and liquid formats. |

Overall, the differences are explainable once scope and pricing steps are made explicit. By keeping the demand pool tied to application usage and then validating it with supplier-side checks, the estimate stays traceable to clear inputs that can be repeated year to year.

Key Questions Answered in the Report

What is the current valuation of the Stevia market in 2026?

Regulatory confidence and a steady demand for natural sweeteners bolster the Stevia market, projected to reach USD 1.03 billion by 2026.

How fast is the Stevia market expected to grow through 2031?

By 2031, the market is set to grow to USD 1.71 billion, with a projected CAGR of 10.62%.

Which application segment leads Stevia consumption?

In 2025, beverages are set to command a 29.84% market share, with a projected CAGR of 12.97%, fueled by initiatives aimed at reducing sugar content.

Why is Asia-Pacific considered crucial for Stevia supply?

China and India, with their extensive cultivation and processing infrastructure, bolster the Asia-Pacific's contribution of 31.05% to global revenue.

Page last updated on: