Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.53 Billion |

| Market Size (2026) | USD 2.64 Billion |

| Market Size (2031) | USD 3.28 Billion |

| Growth Rate (2026 - 2031) | 4.45% CAGR |

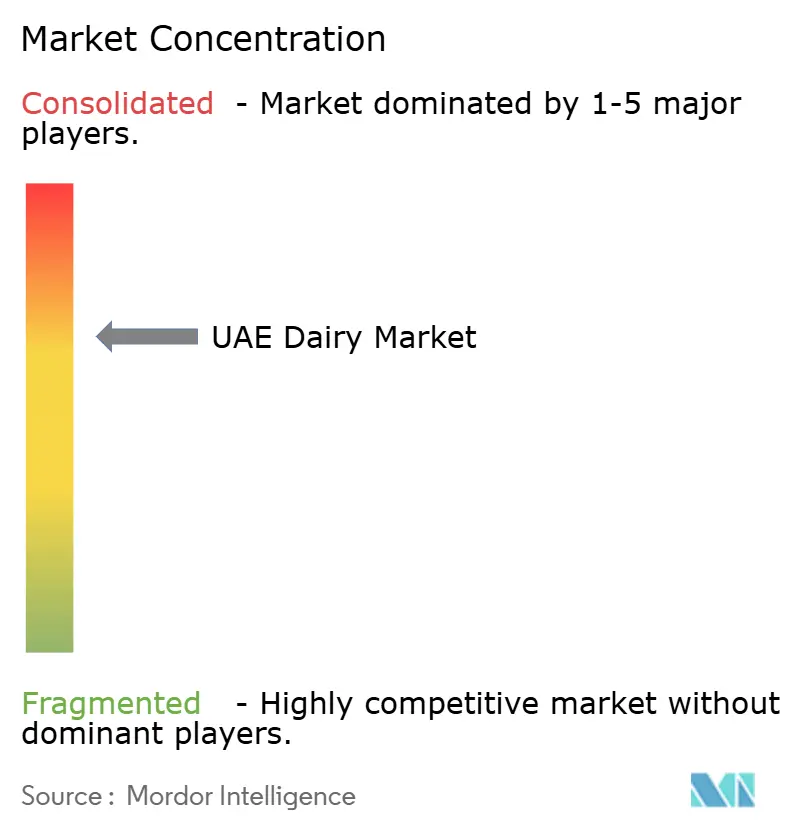

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

UAE Dairy Market Analysis by Mordor Intelligence

The United Arab Emirates (UAE) dairy market size is expected to grow from USD 2.53 billion in 2025 to USD 2.64 billion in 2026 and is forecast to reach USD 3.28 billion by 2031 at 4.45% CAGR over 2026-2031. This growth trajectory reflects the Emirates' strategic positioning as a regional food hub while addressing domestic consumption demands driven by a diverse expatriate population and robust tourism recovery. The market's expansion aligns with the National Food Security Strategy 2051, which aims to reduce food import dependency from 90% to 50% [1]Source: United Arab Emirates Government, "National Food Security Strategy 2051", u.ae. Growth springs from population gains, tourism momentum, and the National Food Security Strategy 2051 that encourages local production and technological investment. Dubai’s dominance, premiumization trends, and packaging advances reinforce steady value expansion. A moderate concentration of leading suppliers spurs innovation while sustaining competitive pricing. Resilient supply networks, diversified consumer bases, and government-backed industrial financing programs anchor confidence in the UAE dairy products market over the next five years.

Key Report Takeaways

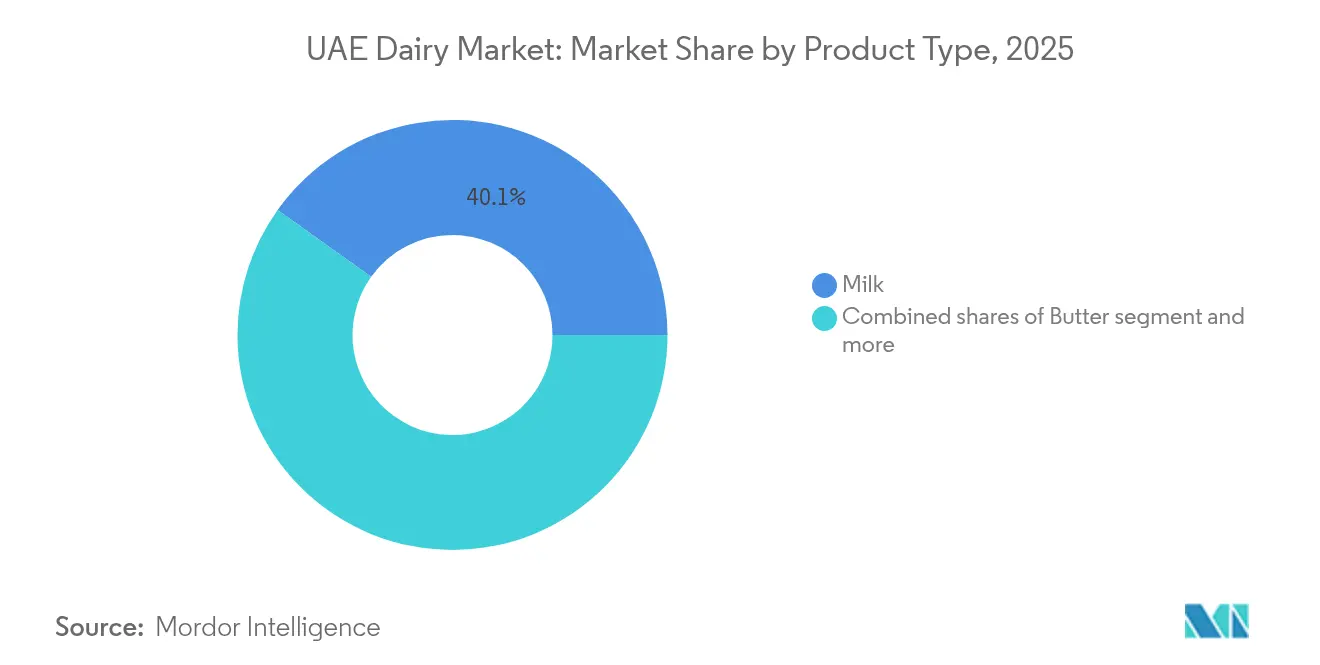

- By product type, milk captured 40.12% of the UAE dairy products market share in 2025; yogurt is forecast to expand at a 5.82% CAGR through 2031.

- By nature, conventional items held 97.41% of the UAE dairy products market share in 2025, while organic products are on track for a 5.39% CAGR to 2031.

- By packaging, cartons/Tetra Pak accounted for 50.08% of the UAE dairy products market size in 2025; pouches are projected to post the fastest 5.92% CAGR by 2031.

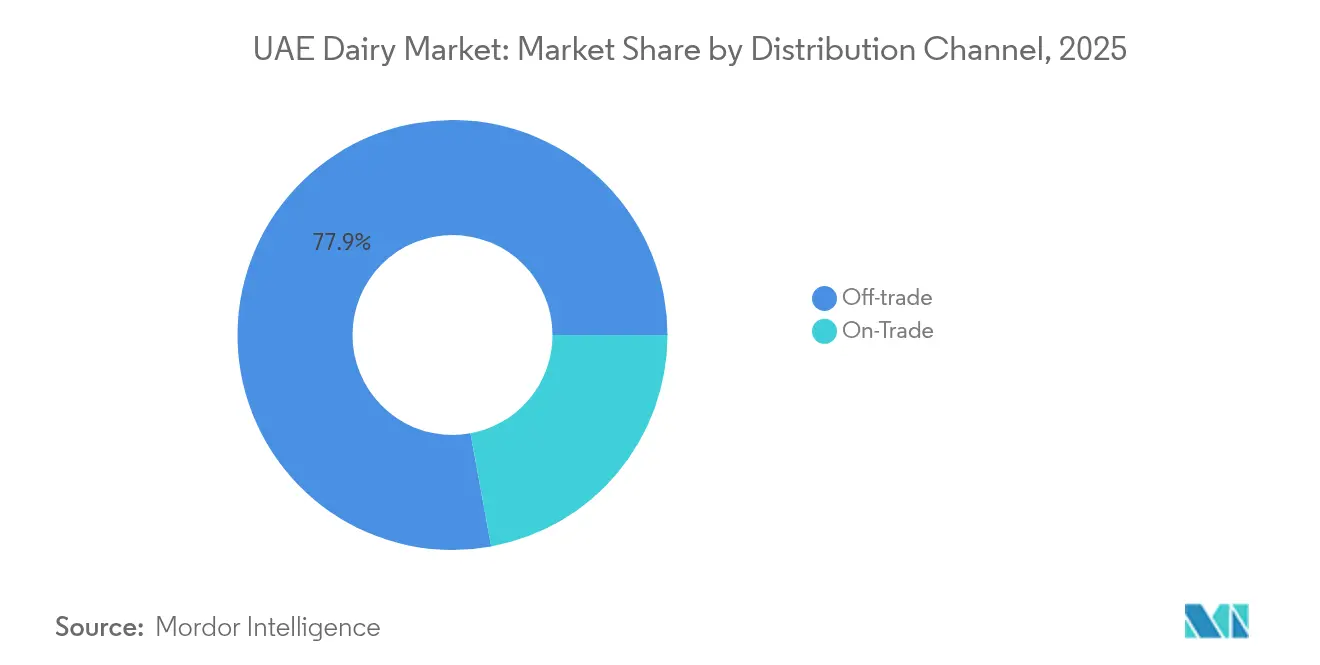

- By distribution channel, off-trade outlets represented 77.88% of the UAE dairy products market share in 2025, whereas on-trade sales are forecast at a 5.08% CAGR as hospitality rebounds.

- By geography, Dubai led with 40.21% of the UAE dairy products market share in 2025 and is advancing at a 5.04% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Dairy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health and Wellness Awareness | +1.2% | UAE-wide, strongest in Dubai and Abu Dhabi | Medium term (2-4 years) |

| Product Innovation | +0.9% | National, with early adoption in urban centers | Short term (≤ 2 years) |

| Cultural Diversity and Culinary Trends | +0.8% | Dubai, Abu Dhabi, with spillover to other emirates | Long term (≥ 4 years) |

| Branding and Marketing | +0.6% | UAE-wide, concentrated in major retail hubs | Short term (≤ 2 years) |

| Modern Retail Development | +0.7% | National, accelerated in Dubai and Abu Dhabi | Medium term (2-4 years) |

| Sustainable and Technological Advances | +0.5% | National, led by government initiatives | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health and Wellness Awareness

Rising health consciousness among UAE residents drives premium dairy segment expansion, particularly benefiting organic and functional dairy products. Consumer surveys indicate over 60% of Middle East consumers prioritize fresh produce and express concerns about ultra-processed foods, creating opportunities for locally produced, minimally processed dairy alternatives. This trend gains momentum through government health initiatives targeting childhood nutrition and obesity prevention. The emergence of A2A2 protein milk production at facilities like Mleiha Dairy Farm demonstrates industry response to digestive health concerns, addressing the 11% lactose-intolerant population while positioning premium products for health-conscious consumers. Regulatory influence from the Abu Dhabi Agriculture and Food Safety Authority ensures product quality standards that support consumer confidence in health-focused dairy innovations.

Sustainable and Technological Advances

Environmental sustainability initiatives reshape production practices and consumer preferences, driving the adoption of eco-friendly packaging and resource-efficient farming methods. Tetra Pak's recognition as "Sustainable Company of the Decade" at Gulfood Manufacturing 2024 highlights industry commitment to circular economy principles and waste reduction. Advanced farming technologies, including IoT sensors for livestock monitoring and automated feeding systems, improve operational efficiency while reducing environmental impact. Solar energy adoption in dairy farming operations aligns with the UAE's renewable energy goals while reducing operational costs. Water conservation technologies become essential given regional scarcity, with farms implementing recycling systems and drought-resistant feed crops. These advances support the UAE's broader sustainability commitments while creating competitive advantages for early adopters.

Cultural Diversity and Culinary Trends

The UAE's multicultural population creates diverse dairy consumption patterns that drive product variety and specialized offerings. Expatriate communities, comprising the majority of the population, maintain dietary preferences from their home countries while adapting to local availability and climate considerations. This cultural mosaic generates demand for region-specific dairy products, from European-style cheeses to South Asian yogurt varieties and Middle Eastern dairy desserts. Tourism recovery amplifies this effect, with hospitality sectors requiring diverse dairy ingredients to cater to international guests' culinary expectations. The interplay between traditional Emirati cuisine and international influences creates opportunities for fusion products that blend local ingredients with global dairy applications. Cultural celebrations and religious observances, particularly Ramadan, create seasonal demand spikes that influence production planning and inventory management across the sector.

Branding and Marketing

Strategic brand positioning becomes increasingly critical as market competition intensifies and consumer sophistication grows. Companies invest heavily in digital marketing channels, with Agthia Group reporting 64% of total sales through digital channels in H1 2024, demonstrating the effectiveness of omni-channel strategies. Brand differentiation focuses on origin stories, production methods, and health benefits, with local producers emphasizing freshness and regional authenticity while international brands leverage global reputation and innovation capabilities. Marketing campaigns increasingly target health-conscious consumers through educational content about nutritional benefits and sustainable production practices. The rise of social media influence and food blogging culture amplifies brand messaging, particularly for premium and artisanal dairy products that benefit from visual storytelling and lifestyle association.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short Shelf Life of Fresh Dairy | -0.8% | UAE-wide, particularly affecting rural distribution | Short term (≤ 2 years) |

| Consumer Shift to Plant-Based | -0.6% | Urban centers, strongest in Dubai and Abu Dhabi | Medium term (2-4 years) |

| Limited Local Production Capacity | -0.9% | National, with capacity constraints in all emirates | Long term (≥ 4 years) |

| Supply Chain Vulnerability | -0.7% | National, with particular impact on import-dependent segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Short Shelf Life of Fresh Dairy

Fresh dairy products' inherent perishability constrains market expansion and increases operational complexity across the value chain. The UAE's extreme climate conditions accelerate spoilage rates, requiring sophisticated cold chain infrastructure that increases distribution costs and limits geographic reach. Rural and remote areas face challenges accessing fresh dairy products, creating market segmentation between urban centers with robust cold storage facilities and peripheral regions relying on shelf-stable alternatives. This constraint drives investment in ultra-high temperature processing and extended shelf-life technologies, though these solutions often compromise taste and nutritional profiles that consumers increasingly value. The challenge intensifies during summer months when ambient temperatures exceed 45°C, straining refrigeration systems and increasing energy costs throughout the supply chain.

Limited Local Production Capacity

Domestic dairy production constraints force continued reliance on imports, exposing the market to currency fluctuations and international supply disruptions. The UAE imports approximately 80% of its agricultural products, including USD 1.92 billion in dairy products in 2023, highlighting the scale of import dependency [2]Source: U.S. Department of Agriculture, "Exporter Guide Annual", apps.fas.usda.gov. Climate limitations and water scarcity restrict large-scale dairy farming expansion, despite government initiatives like the AGRIX Accelerator program supporting agricultural innovation. Investment requirements for modern dairy facilities are substantial, with projects like Mleiha Dairy Farm requiring Dh600 million for 5,000-cow capacity, creating barriers for smaller operators. The constraint becomes more acute as population growth and tourism recovery increase demand faster than local production capacity can expand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Milk Dominance Drives Market Growth

Milk commands 40.12% market share in 2025 while simultaneously leading growth projections with 5.78% CAGR through 2031, reflecting both established consumption patterns and emerging premium product adoption. The segment benefits from diverse applications spanning direct consumption, food service, and industrial processing, with fresh milk maintaining preference despite shelf-life challenges. Cheese represents the second-largest category, driven by expanding food service sectors and growing consumer sophistication regarding artisanal varieties, while processed cheese gains traction in quick-service restaurants and convenience applications. Yogurt segments experience robust growth through health positioning and probiotic awareness, with spoonable varieties dominating traditional consumption while drinkable formats capture on-the-go occasions.

Dairy desserts emerge as a high-value segment, capitalizing on tourism recovery and celebration culture, with ice cream and frozen desserts performing particularly well during extended summer seasons. Cream products serve specialized culinary applications, with double cream and whipping varieties supporting the expanding bakery and confectionery sectors. The others category, encompassing spreads and fermented products, demonstrates innovation potential as manufacturers develop culturally-adapted products for diverse expatriate communities. Federal Law No. 10 of 2015 ensures quality standards across all product categories, supporting consumer confidence in both imported and locally-produced varieties .

By Nature: Organic Growth Accelerates Premium Positioning

Conventional dairy products maintain overwhelming market dominance at 97.41% share in 2025, reflecting established supply chains and price sensitivity among mainstream consumers. However, organic alternatives demonstrate the fastest growth trajectory at 5.39% CAGR through 2031, driven by health consciousness and premium positioning strategies. This growth differential suggests a gradual but persistent market evolution toward higher-value products, supported by increasing consumer education about production methods and nutritional benefits. The organic segment benefits from government initiatives promoting sustainable agriculture, including the Plant the Emirates program that encourages organic farming practices.

Local organic production receives support through projects like Mleiha Dairy Farm, which emphasizes chemical-free feeding and natural production methods to create A2A2 protein organic milk. The premium pricing of organic products creates attractive margins for producers while limiting market penetration among price-conscious consumers. Import regulations for organic certification add complexity but ensure quality standards that support consumer trust. The segment's growth trajectory indicates potential for market share expansion as organic supply chains mature and economies of scale reduce price premiums.

By Packaging: Innovation Drives Format Evolution

Cartons/Tetra Pak packaging dominates with 50.08% market share in 2025, benefiting from superior shelf stability and environmental positioning, while pouches emerge as the fastest-growing format at 5.92% CAGR through 2031. This growth pattern reflects consumer preferences for convenience and sustainability, with pouches offering portion control and reduced packaging waste. Bottles/Jars maintain a significant presence in premium segments, particularly for specialty products like organic milk and artisanal yogurts, where glass packaging conveys quality perception and product integrity. The "Others" category encompasses a diverse range of formats, including sachets for single-serve applications and plastic tubs for dairy desserts.

Packaging innovation focuses on sustainability and functionality, with Tetra Pak's recognition of sustainable practices highlighting the industry's commitment to environmental responsibility. Advanced packaging technologies extend shelf life while maintaining nutritional quality, addressing the UAE's climate challenges and distribution requirements. Regulatory compliance factors influence packaging choices, with food safety standards requiring specific barrier properties and labeling requirements. The shift toward e-commerce creates demand for packaging formats optimized for shipping and handling, driving innovation in protective and sustainable materials.

By Distribution Channel: Off-Trade Dominance with On-Trade Growth

Off-trade channels command 77.88% market share in 2025, reflecting consumer preference for grocery shopping and home consumption, while on-trade segments show promising 5.08% growth through 2031 as hospitality sectors recover. Supermarkets/Hypermarkets dominate off-trade distribution, benefiting from extensive product ranges and competitive pricing, while convenience stores capture impulse purchases and emergency needs. Online retail experiences rapid expansion, accelerated by pandemic-driven behavioral changes and improved delivery infrastructure, though current penetration remains modest compared to traditional formats.

The on-trade recovery reflects tourism sector rehabilitation and expanding food service operations, with hotels, restaurants, and cafes increasing dairy procurement as occupancy rates and dining frequency normalize. Convenience stores benefit from urbanization trends and busy lifestyles, offering extended hours and strategic locations that support impulse dairy purchases. E-commerce growth receives support from improved cold chain logistics and consumer comfort with online grocery shopping, though fresh dairy products face delivery challenges that favor shelf-stable alternatives. Distribution channel evolution reflects broader retail transformation trends while accommodating the unique requirements of perishable dairy products.

Geography Analysis

Dubai's market dominance stems from its unique position as a global city with over 85% expatriate population, creating diverse dairy consumption patterns that drive both volume and premium product adoption. The emirate's dominance reflects superior retail infrastructure, including extensive hypermarket networks and modern food service sectors that cater to international tastes and dietary requirements. Tourism recovery amplifies consumption through hotel and restaurant channels, while the emirate's role as a regional business hub generates consistent demand from corporate catering and events sectors. Dubai's growth trajectory at 5.04% CAGR through 2031 benefits from continued economic diversification, infrastructure development, and population growth that sustains dairy market expansion. The emirate serves as a testing ground for new products and formats, with consumer acceptance often predicting broader UAE market trends.

Abu Dhabi's market position reflects its role as the political and cultural capital, with government sector employment providing stable income levels that support premium dairy consumption. The emirate hosts major food production facilities and agricultural research initiatives, including the Abu Dhabi Agriculture and Food Safety Authority's innovation programs that advance local production capabilities. Strategic investments in food security infrastructure, including the AGRIX Accelerator program, position Abu Dhabi as a hub for agricultural technology development and sustainable farming practices. The emirate's cultural institutions and international events create demand for diverse dairy products, while its proximity to agricultural regions supports fresh product distribution.

Sharjah and the remaining emirates demonstrate growth potential through industrial development and targeted agricultural investments, with the Mleiha Dairy Farm project exemplifying local production enhancement strategies. These regions benefit from lower operational costs and available land for agricultural development, while maintaining access to Dubai's distribution networks and consumer markets. The northern emirates show promise in organic and specialty dairy production, leveraging climate advantages and government support for sustainable agriculture. Regional development initiatives ensure balanced growth while recognizing each emirate's unique strengths and market positioning within the broader UAE dairy ecosystem.

Competitive Landscape

The UAE dairy market exhibits moderate consolidation, reflecting established player dominance while maintaining space for innovation and market entry. Local champions like Al Rawabi Dairy and Al Ain Farms leverage regional expertise and fresh product positioning against international giants, including Almarai, Danone, and Nestlé, creating competitive dynamics that benefit consumers through product diversity and competitive pricing.

Strategic consolidation accelerates through acquisitions like Ghitha Holding's USD 65.3 million purchase of Arabian Farms, indicating industry maturation and scale-building initiatives. Technology adoption becomes a key differentiator, with companies investing in IoT-enabled livestock monitoring, automated processing systems, and sustainable packaging solutions to improve efficiency and meet evolving consumer expectations.

Opportunities emerge in premium segments, including organic dairy, camel milk products, and culturally adapted specialty items that serve the UAE's diverse population. Emerging disruptors focus on direct-to-consumer models, plant-based alternatives, and innovative packaging formats that address sustainability concerns and convenience preferences. The competitive landscape benefits from government initiatives like Operation 300bn, which provides AED 30 billion in financing support for priority sectors including food security, enabling both established players and new entrants to expand production capabilities. Regulatory compliance factors create barriers to entry while ensuring product quality, with Federal Law No. 10 of 2015 establishing comprehensive food safety standards that all market participants must meet.

UAE Dairy Industry Leaders

-

Emirates Rawabi

-

Arla Foods amba

-

Danone

-

Fonterra Co-operative Group Limited

-

FrieslandCampina

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Anchor Food Professionals, renowned for its premium dairy products, unveiled its latest innovation: 100 percent recyclable mini butter portions designed specifically for the hospitality and F&B industry in the Middle East. These single-serve portions were crafted from 100 percent grass-fed New Zealand.

- January 2025: Sharjah Agriculture and Livestock officially launched Meliha Laban at the second Al Dhaid Agricultural Exhibition ahead of the holy month of Ramadan. The launch followed the remarkable success of Meliha milk, which had seen long queues of customers eager to purchase the product across the UAE.

- October 2023: Nutridor, a food and beverage (F&B) company under TGI Group, launched its first dairy production facility in the UAE at Dubai Industrial City, part of TECOM Group PJSC. The facility, which represented an investment of AED 75 million, was established to serve demand for Nutridor's dairy products under the 'Abevia' brand.

UAE Dairy Market Report Scope

Dairy products or milk products are produced from or contain the milk of cattle, water buffaloes, goats, sheep, and camels, among other mammals. The United Arab Emirates (UAE) dairy market is segmented by product type, nature, packaging, distribution channel, and geography. By product type, the market is segmented into milk, cheese, butter, dairy desserts, yogurt, and other product types. By nature, the market is segmented into organic and conventional. By packaging, the market is segmented into cartons/tetra Pak, bottles/jars, pouches, and others. By distribution channel, the market is segmented into off-trade and on-trade. By geography, the market is segmented into Dubai and more. The market forecasts are provided in terms of value (USD) and volume (Tons).

By Product Type

| Butter | Cultured Butter |

| Uncultured Butter | |

| Cheese | Natural Cheese |

| Processed Cheese | |

| Cream | Double Cream |

| Single Cream | |

| Whipping Cream | |

| Others | |

| Dairy Desserts | Cheesecakes |

| Frozen Desserts | |

| Ice Cream | |

| Mousses | |

| Others | |

| Milk | Condensed milk |

| Flavored Milk | |

| Fresh Milk | |

| Powdered Milk | |

| UHT Milk | |

| Yogurt | Spoonable Yogurt |

| Drinkable yogurt | |

| Others |

By Nature

| Organic |

| Conventional |

By Packaging

| Cartons/Tetra Pak |

| Bottles/Jars |

| Pouches |

| Others |

By Distribution Channel

| Off-trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channel | |

| On-trade |

By Region

| Dubai |

| Abu Dhabi |

| Sharjah |

| Rest of the United Arab Emirates |

| By Product Type | Butter | Cultured Butter |

| Uncultured Butter | ||

| Cheese | Natural Cheese | |

| Processed Cheese | ||

| Cream | Double Cream | |

| Single Cream | ||

| Whipping Cream | ||

| Others | ||

| Dairy Desserts | Cheesecakes | |

| Frozen Desserts | ||

| Ice Cream | ||

| Mousses | ||

| Others | ||

| Milk | Condensed milk | |

| Flavored Milk | ||

| Fresh Milk | ||

| Powdered Milk | ||

| UHT Milk | ||

| Yogurt | Spoonable Yogurt | |

| Drinkable yogurt | ||

| Others | ||

| By Nature | Organic | |

| Conventional | ||

| By Packaging | Cartons/Tetra Pak | |

| Bottles/Jars | ||

| Pouches | ||

| Others | ||

| By Distribution Channel | Off-trade | Supermarkets/Hypermarkets |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channel | ||

| On-trade | ||

| By Region | Dubai | |

| Abu Dhabi | ||

| Sharjah | ||

| Rest of the United Arab Emirates | ||

Key Questions Answered in the Report

How significant is Dubai’s role within national dairy sales?

Dubai contributes 40.21% of value and is forecast at a 5.04% CAGR, cementing its role as the core consumption hub.

What is the current value of the UAE dairy products market?

The UAE dairy products market size is USD 2.64 billion in 2026.

How fast is the UAE dairy products market expected to grow?

Market value is projected to rise at a 4.45% CAGR, reaching USD 3.28 billion by 2031.

Which dairy segment holds the largest share in UAE retail value?

Milk leads with 40.12% of 2025 revenue, thanks to widespread household and food-service demand.

Page last updated on: