UAE Digital Transformation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

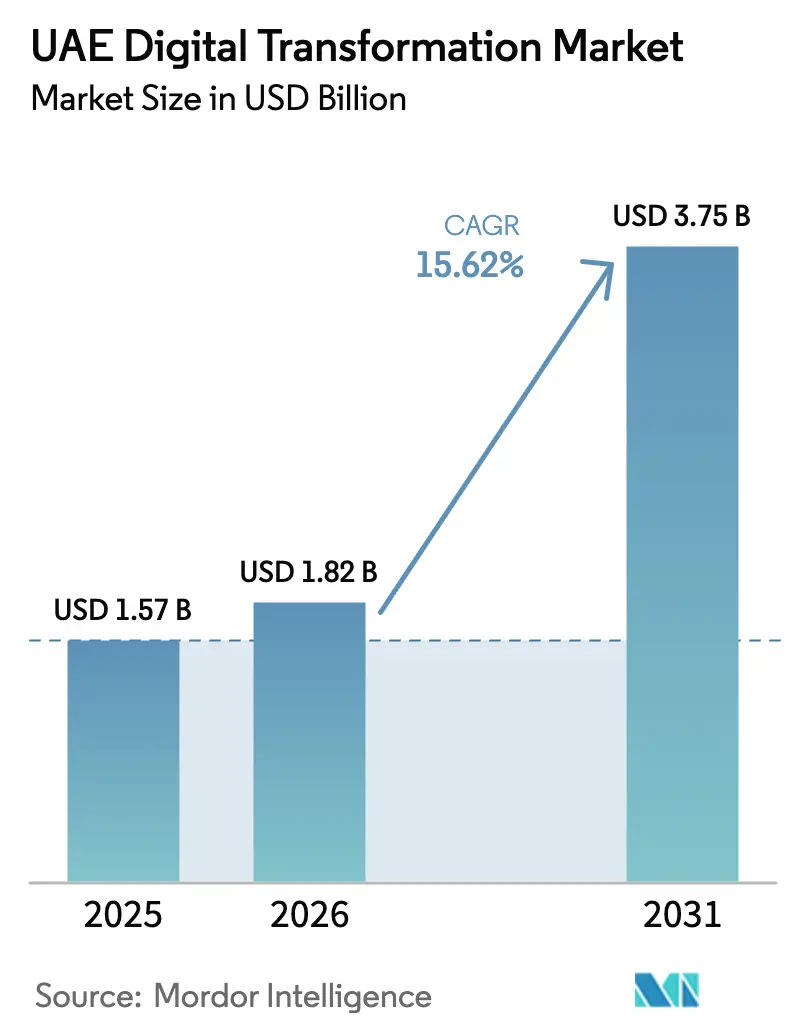

| Base Year Market Size (2025) | USD 1.57 Billion |

| Market Size (2026) | USD 1.82 Billion |

| Market Size (2031) | USD 3.75 Billion |

| Growth Rate (2026 - 2031) | 15.62% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Digital Transformation Market Analysis by Mordor Intelligence

The UAE Digital Transformation Market size was valued at USD 1.57 billion in 2025 and estimated to grow from USD 1.82 billion in 2026 to reach USD 3.75 billion by 2031, at a CAGR of 15.62% during the forecast period (2026-2031). Accelerated public-sector funding, hyperscale-cloud build-outs, 5G commercialisation and mandatory ESG reporting are converging to keep the UAE digital transformation market on a double-digit growth path despite global IT budget rationalisation. Sovereign wealth fund appetite—illustrated by the 136-times-oversubscribed Presight AI IPO—signals institutional confidence in the domestic AI stack, while Operation 300bn’s incentives sustain demand from industrial firms. Cloud remains the dominant delivery model, yet edge computing, analytics and AI workloads are expanding faster, confirming that enterprises now prioritise intelligent automation rather than basic lift-and-shift migration. Data sovereignty rules and a shortage of advanced digital talent present near-term hurdles, but domestic language-AI breakthroughs and aggressive skills programmes are mitigating the headwinds.

Key Report Takeaways

- By component, Solutions led with 58.45% revenue share in 2025, whereas Services are advancing at a 19.6% CAGR through 2031.

- By deployment mode, cloud captured 69.25% of the UAE digital transformation market share in 2025; hybrid architectures are projected to expand at a 23.7% CAGR to 2031.

- By organisation size, large enterprises controlled 67.95% of spending in 2025, while SMEs record the fastest growth at 24.3% through 2031.

- By technology type, cloud & edge computing commanded 29.65% of the UAE digital transformation market size in 2025, with analytics & AI posting a 27.2% CAGR to 2031.

- By end-user industry, manufacturing posted the largest contribution, and public sector digital projects are set to deliver the highest CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Figures recorded within United arab emirates feed into a worldwide estimate while studying the global industry. Mordor Intelligence's digital transformation (dx) market size captures this aggregation.

UAE Digital Transformation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government digital-economy strategy funding surge | +4.2% | National, concentrated in Abu Dhabi and Dubai | Medium term (2-4 years) |

| Rapid 5G and hyperscale-cloud roll-outs | +3.8% | National, with early deployment in Dubai and Abu Dhabi | Short term (≤ 2 years) |

| Explosive AI / analytics spending in finance and public sector | +3.1% | Dubai financial district; Abu Dhabi government sector | Short term (≤ 2 years) |

| COP28-driven mandatory ESG digital platforms | +2.4% | National, with industrial focus in Abu Dhabi | Medium term (2-4 years) |

| “Operation 300bn” Industry 4.0 upgrade incentives | +1.9% | Manufacturing hubs in Abu Dhabi, Sharjah and the Northern Emirates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Digital-Economy Strategy funding surge

Abu Dhabi has earmarked AED 13 billion to transform every public service into an AI-native process, triggering a wave of sovereign-cloud contracts, localisation mandates and compliance opportunities for vendors that can meet stringent data-residency rules.[1]e&, “e& UAE Sets New Record With World’s Fastest 5G Speed of 30.5 Gbps,” eand.com International hyperscalers are entering joint ventures with local telcos to satisfy the 100% sovereign-cloud requirement, while Dubai’s parallel investment programme is creating multiplier effects in private-sector adoption. The funding model shifts spending from isolated projects to platform-based ecosystems, locking in long-term demand for managed services. Early movers that align with nascent AI-governance frameworks gain preferred-supplier status, building durable revenue streams.

Rapid 5G & hyperscale-cloud roll-outs

Carrier-aggregation tests that achieved 30.5 Gbps showcase the network’s readiness for time-critical industrial AI workloads.[2]Akin Gump, “Abu Dhabi Aims to Be World’s First Fully AI-Native Government Across All Digital Services by 2027,” akingump.com Edge nodes embedded in private 5G campus networks allow oil, gas and manufacturing operators to run autonomous control loops, cutting latency-induced downtime. Hyperscale data-centre expansion—highlighted by the AED 2 billion du–Microsoft facility—adds the compute headroom required for model training and generative-AI inference rcrwireless. Taken together, connectivity and compute roll-outs set a foundation for the UAE digital transformation market to commercialise 6G use cases later in the decade.

Explosive AI/analytics spend in finance & public sector

Chief AI Officers installed in most banks and ministries are steering budgets toward governance, explainability and risk analytics platforms. e&’s launch of IBM watsonx.governance in the UAE reflects the pivot from proof-of-concept chatbots to enterprise-grade AI controls. Dubai Healthcare City demonstrates scale, processing claims data from 300+ providers via AI pipelines that flag anomalies in real time.[3]Dubai-Healthcare-Regulatory, “AI Initiative at Arab Health 2025,” dhcc.ae Spend is shifting from compliance to revenue generation as lenders deploy AI models for hyper-personalised services.

COP28-driven mandatory ESG digital platforms

Abu Dhabi Securities Exchange now obliges listed firms to file ESG metrics, spurring uptake of SaaS sustainability dashboards that ingest scope-3 emissions data from blockchain-verified supply chains.[4]SSE-Initiative, “Abu Dhabi Securities Exchange,” sseinitiative.org Utilities and construction firms deploy digital twins and solar-hybrid trackers to meet the Net Zero 2050 pledge, feeding fresh demand into the UAE digital transformation market for carbon-optimisation analytics .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-sovereignty and cross-border transfer limits | -2.1% | National, with particular impact on multinational enterprises | Medium term (2-4 years) |

| Advanced digital-skills shortage and rising labour cost | -1.8% | National, with acute shortages in Abu Dhabi and Dubai tech hubs | Short term (≤ 2 years) |

| Rising utility tariffs and carbon caps on data centres | -1.5% | National, highest impact in Dubai and Abu Dhabi data-centre clusters | Medium term (2-4 years) |

| Fragmented Arabic content degrading generative-AI accuracy | -0.8% | National, with stronger effects on government and education sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-sovereignty & cross-border transfer limits

Federal Decree-Law 45/2021 raises the bar for cross-border data flows, compelling multinationals to adopt costly localisation or enclave-based architectures. Fragmented rules between mainland and free-zone jurisdictions add compliance complexity that especially burdens SMEs. Restrictions on exporting large datasets also reduce access to diverse training corpora, hurting model accuracy for Arabic generative-AI. The upcoming Digital Dirham requires segregated ledgers, adding parallel infrastructure overhead.

Advanced digital-skills shortage & rising labour cost

AI job vacancies outstrip supply by a wide margin, lifting salaries and elongating project timelines. Emiratisation quotas, while crucial for strategic autonomy, temporarily shrink the available talent pool as local skilling programmes ramp up. Wage inflation squeezes SME budgets, dampening uptake even as low-code platforms lower technical barriers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Outpaces Solutions Despite Infrastructure Dominance

Solutions accounted for 58.45% spending in 2025, mirroring early-stage investment priorities in foundational platforms. Services now scale at 19.6% CAGR as enterprises seek integration, governance and optimisation expertise. Emirates Global Aluminium’s 80+ Industry 4.0 use cases prove the value of specialist partners for monetising deployed platforms. The UAE digital transformation market size for managed services covering AI lifecycle management is projected to reach double the 2025 base by 2031. Implementation complexity therefore shifts revenue pools toward consultants and MSPs able to certify to sovereign-cloud and AI-ethics standards.

Strong service momentum is also visible in public contracts that require outcome-based SLAs. The appointment of Chief AI Officers embeds continuous optimisation cycles, favouring long-term service engagements over one-off licences. As a result, the UAE digital transformation market is gradually tilting toward value-added recurring revenue streams.

By Deployment Mode: Cloud Supremacy Masks Hybrid Complexity

Cloud retained a 69.25% stake in 2025 spending, underwritten by policy mandates stipulating 100% sovereign-cloud usage for critical workloads. On-premise systems remain vital for oil-field telemetry and defence datasets, creating a hybrid topology that demands orchestration layers capable of consistent policy enforcement. The UAE digital transformation market size attached to hybrid-integration tooling is scaling with a 23.7% CAGR.

Inter-cloud networking, data-fabric technologies and zero-trust micro-segmentation are becoming standard requisites. Vendors that bundle multi-tenant orchestration with edge nodes gain favour because they reduce architectural sprawl. Over the forecast period, the UAE digital transformation market will therefore converge toward platforms that abstract location and provider specifics but still satisfy local-data regulations.

By Organisation Size: SME Acceleration Challenges Enterprise Dominance

Large organisations spent 67.95% of the 2025 total, leveraging deep capital reserves to finance large-scale AI pilots. Government programmes that target 20,000 SMEs for digitisation support are however compressing the dominance gap. SMEs expand at a 24.3% CAGR, adopting modular SaaS suites that bake in compliance and analytics by design.

E-commerce, e-invoicing and remote-HR platforms lower the entry barrier, allowing small firms to tap advanced capabilities without large CAPEX. Micro-vertical offerings for retail, F&B and micro-manufacturing quicken adoption, ensuring the UAE digital transformation market gains breadth as well as depth.

By Technology Type: Analytics & AI Surge Challenges Cloud & Edge Leadership

Cloud & edge computing preserved 29.65% share in 2025 yet faces competition from analytics & AI, which grow at 27.2% CAGR. Language-specific models such as Falcon-Arabic drive demand for fine-tuning and inference services optimised for regional dialects. The UAE digital transformation market now prizes contextually aware AI that can navigate bilingual transactional data.

Digital twin platforms, blockchain-secured ledgers and autonomous industrial robots add to the compute burden, reinforcing the need for distributed edge nodes that host inference closer to data sources. Cybersecurity tools using AI for real-time anomaly detection are scaling fastest as 52% of enterprises modernise threat-monitoring stacks.

By End-User Industry: Government Leadership Drives Cross-Sector Adoption

Government agencies continue to pilot AI-first workflows, setting reference architectures for private adopters. Manufacturing uptake accelerates through Operation 300bn grants, with proof of USD 100 million financial impact at EGA validating ROI cases. Oil, gas and utilities adopt private 5G plus edge AI to maximise uptime in harsh environments, as evidenced by ADNOC’s USD 920 million well-digitalisation contract.

BFSI’s Digital Dirham initiative adds a catalyst for blockchain and analytics spending. Healthcare follows, integrating AI to process claims and medical imaging, while transport embraces autonomous vehicle pilots slated to cover 25% of Dubai journeys by 2030.

Geography Analysis

Dubai claimed 55.10% of 2025 revenue, leveraging its status as a fintech and logistics hub with mature smart-city infrastructure. The emirate’s self-driving taxi law and D33 economic agenda foster real-world testbeds that give technology vendors fast feedback loops. Retail-banking digitisation and tourism recovery add further stimuli.

Abu Dhabi is the fastest-growing territory, delivering a 18.95% CAGR on the back of the AED 13 billion Digital Strategy and expansive sovereign-AI roadmap. Integration centres in Masdar City and mega-projects such as the 1 GW Stargate data-centre campus compound localisation effects that benefit domestic providers. Manufacturing corridors in the emirate tap Operation 300bn subsidies that require applicants to embed Industry 4.0 metrics.

Sharjah and the Northern Emirates harness spill-over talent and infra build-outs while offering lower real-estate costs. Federal ranking of 13th in the UN e-Government index guarantees that high-value digital public services reach these regions. Planned 6G trials will further democratise advanced connectivity, ensuring the UAE digital transformation market gains a truly national footprint.

Mordor Intelligence evaluates the digital transformation (dx) market across all key regional markets, including North America, Africa, and Middle East, with deeper country-level insights covering Israel, Germany, Canada, South Korea, United States, and United Kingdom.

Competitive Landscape

Competition is intensifying yet remains moderately fragmented. Global hyperscalers localise through equity partnerships—Microsoft’s billion-dollar stake in G42 and du’s data-centre JV are prime examples. Regional champions such as e& and G42 cross-sell telecom, cloud and cybersecurity stacks, lowering customer acquisition costs and reinforcing domestic ecosystems.

Pure-play integrators feel margin pressure but pivot to specialised offerings in AI ethics, Arabic NLP and ESG reporting. Consolidation is evident in G42’s acquisition of CPX, merging AI and security portfolios under one roof. Telcos convert network analytics into managed-service propositions, competing head-to-head with incumbents like Accenture and IBM.

Vendor success is increasingly tied to compliance credentials: data-residency stamps, Emirati workforce ratios and AI safety certifications. Those able to fulfil these check-boxes while offering competitive total-cost-of-ownership enjoy preferred-supplier status on government frameworks, shaping future share distribution within the UAE digital transformation market.

UAE Digital Transformation Industry Leaders

Microsoft Corporation

IBM Corporation

SquareOne Technologies

Oracle Corporation

G42 Holding AI Cloud Computing Company L.L.C.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Cisco joined the Stargate UAE Initiative to deliver networking and security solutions for a 1 GW AI data-centre campus in Abu Dhabi.

- April 2025: du entered a AED 2 billion hyperscale data-centre partnership with Microsoft to underpin Dubai’s AI ambitions.

- March 2025: ADNOC awarded a USD 920 million contract to Jereh Oil & Gas Engineering for AI-enabled well digitalisation across 2,000 wells.

- February 2025: G42 and Etisalat merged data-centre assets into Khazna, creating the UAE’s largest facility portfolio.

UAE Digital Transformation Market Report Scope

Digital transformation is the process of incorporating digital technologies such as analytics, artificial intelligence, and machine learning, extended reality (XR), Iot, industrial robotics, blockchain, additive manufacturing/3D printing, cybersecurity, cloud and edge computing, and others (digital Twin, mobility, and connectivity) in various end-user industries across UAE.

The UAE digital transformation market is segmented by type [analytics, artificial intelligence, and machine learning, extended reality (XR), IoT, industrial robotics, blockchain, additive manufacturing/3D printing, cybersecurity, cloud and edge computing, and others (digital twin, mobility, and connectivity)] and end-user industry [manufacturing, oil, gas and utilities, retail and e-commerce, transportation and logistics, healthcare, BFSI, telecom and IT, government and public sector and others (education, media & entertainment, environment etc)]. The market sizes and forecasts are provided in terms of value (USD ) for the segments.

| Solutions (Software / Platforms) |

| Services (Consulting, Integration, Managed) |

| Cloud |

| On-premise / Hybrid |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Analytics, AI and ML |

| Extended Reality (XR) |

| Internet of Things (IoT) |

| Industrial Robotics |

| Blockchain |

| Additive Manufacturing / 3-D Printing |

| Cybersecurity |

| Cloud and Edge Computing |

| Digital Twin, Mobility and Connectivity |

| Manufacturing |

| Oil, Gas and Utilities |

| Retail and E-commerce |

| Transportation and Logistics |

| Healthcare |

| BFSI |

| Telecom and IT |

| Government and Public Sector |

| Education, Media and Entertainment, Environment |

| By Component | Solutions (Software / Platforms) |

| Services (Consulting, Integration, Managed) | |

| By Deployment Mode | Cloud |

| On-premise / Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises (SMEs) | |

| By Type | Analytics, AI and ML |

| Extended Reality (XR) | |

| Internet of Things (IoT) | |

| Industrial Robotics | |

| Blockchain | |

| Additive Manufacturing / 3-D Printing | |

| Cybersecurity | |

| Cloud and Edge Computing | |

| Digital Twin, Mobility and Connectivity | |

| By End-User Industry | Manufacturing |

| Oil, Gas and Utilities | |

| Retail and E-commerce | |

| Transportation and Logistics | |

| Healthcare | |

| BFSI | |

| Telecom and IT | |

| Government and Public Sector | |

| Education, Media and Entertainment, Environment |

Key Questions Answered in the Report

What is the current value of the UAE digital transformation market?

The UAE digital transformation market is valued at USD 1.82 billion in 2026 and is projected to reach USD 3.75 billion by 2031.

Which segment is growing fastest within the UAE digital transformation market?

Services are expanding at a 19.6% CAGR as organisations seek integration, governance and optimisation expertise.

How significant is SME adoption of digital solutions in the UAE?

SMEs account for a 24.3% CAGR, supported by federal programmes that lower technical and financial barriers.

What role does 5G play in the UAE digital transformation market?

5G’s 30.5 Gbps record speed enables real-time AI inference at the edge, unlocking industrial automation and autonomous mobility use cases.

How are data-sovereignty rules affecting the UAE digital transformation market?

They compel local data-centre investment and sovereign-cloud adoption, increasing infrastructure costs but creating new domestic service opportunities.

Which emirate is experiencing the fastest growth in digital transformation spending?

Abu Dhabi leads with a 18.95% CAGR driven by its AED 13 billion Digital Strategy and sovereign-AI initiatives.

Page last updated on: