United Kingdom Digital Transformation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

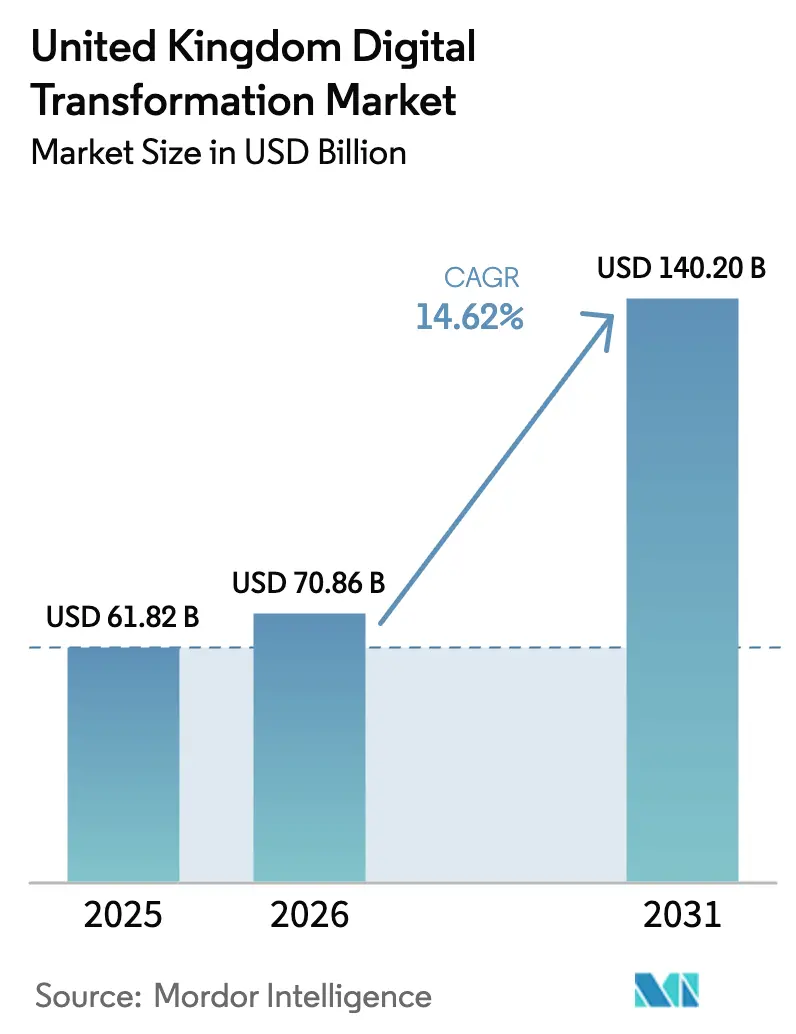

| Base Year Market Size (2025) | USD 61.82 Billion |

| Market Size (2026) | USD 70.86 Billion |

| Market Size (2031) | USD 140.2 Billion |

| Growth Rate (2026 - 2031) | 14.62% CAGR |

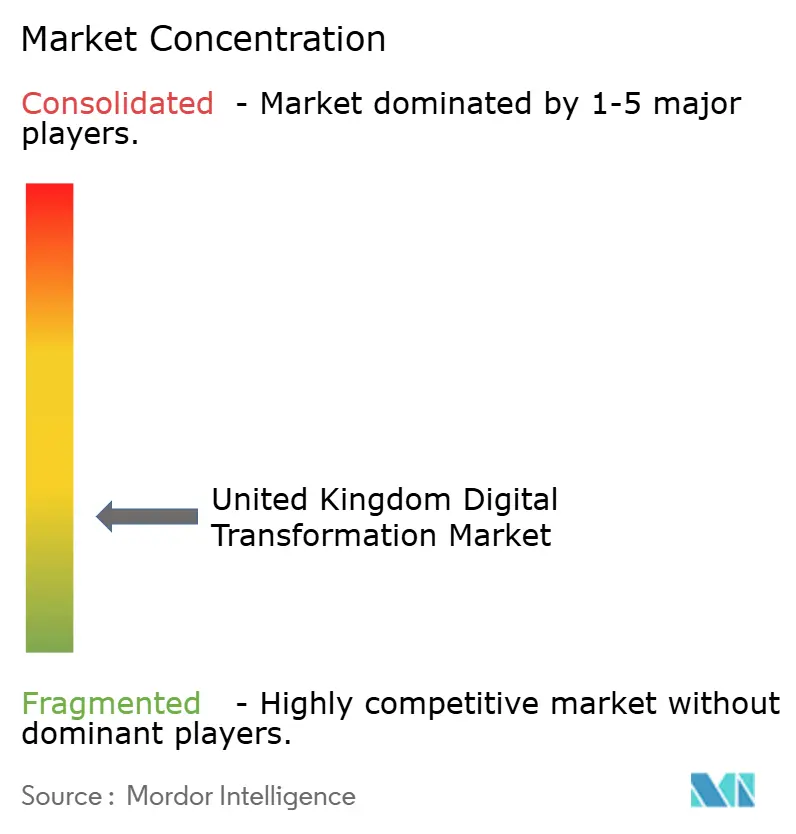

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Digital Transformation Market Analysis by Mordor Intelligence

The United Kingdom Digital Transformation Market size in 2026 is estimated at USD 70.86 billion, growing from 2025 value of USD 61.82 billion with 2031 projections showing USD 140.2 billion, growing at 14.62% CAGR over 2026-2031. The UK digital transformation market benefits from coordinated public-sector mandates, sustained venture funding and large-scale 5G and fibre deployments that lower connectivity barriers. Cloud-first strategies dominate enterprise roadmaps, creating a foundation for rapid AI adoption, while regulatory sandboxes de-risk experimentation. Banks accelerate platform modernisation in response to open-finance rules, healthcare providers digitise patient records under National Health Service targets and manufacturers deploy Industry 4.0 solutions to boost productivity. Market competition remains intense as global cloud hyperscalers, consulting majors and home-grown specialists vie for contracts emphasizing AI, data sovereignty and sustainability outcomes.

Key Report Takeaways

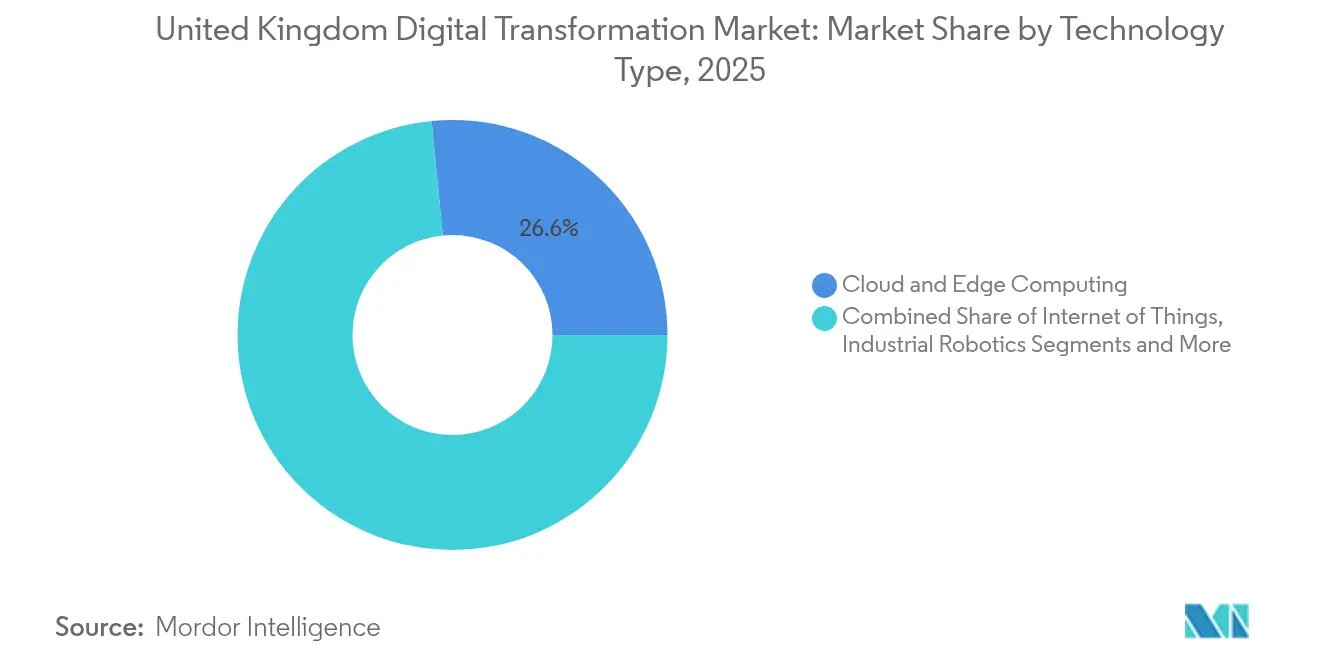

- By technology type, Cloud & Edge Computing commanded 26.55% of the UK digital transformation market share in 2025; Generative AI Platforms are forecast to grow at a 23.6% CAGR to 2031.

- By end-user industry, the Banking, Financial Services and Insurance sector led with 18.65% revenue share in 2025; Healthcare is advancing at an 18.25% CAGR through 2031.

- By component, Services accounted for 52.70% of the UK digital transformation market size in 2025, whereas Solutions are projected to expand at a 15.75% CAGR between 2026-2031.

- By deployment mode, Cloud deployments held 64.30% of the UK digital transformation market size in 2025 and are poised to grow at a 17.15% CAGR to 2031.

- By organisation size, Large enterprises controlled 67.20% of the UK digital transformation market size in 2025, while SMEs are tracking a 16.65% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Expected changes in United kingdom many a times form part of a broader pattern of global movement rather than an isolated trend. The report on worldwide digital transformation (dx) market outlook by Mordor Intelligence brings these expectations together.

United Kingdom Digital Transformation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| The move toward cloud-first operating models | +3.2% | Nationwide, strongest in London and Manchester | Medium term (2–4 years) |

| Government push for digital public services | +2.8% | Country-wide, early gains in England and Scotland | Short term (≤2 years) |

| Wider 5G and fibre coverage that unlocks edge computing | +2.1% | National, with notable value for rural areas | Long term (≥4 years) |

| Safe-testing zones for generative-AI projects | +1.9% | London and Cambridge tech corridors | Medium term (2–4 years) |

| Carbon-tracking rules for greener IT | +1.5% | Industrial regions across the UK | Long term (≥4 years) |

| Venture-capital pockets in regional tech hubs | +1.3% | Manchester, Edinburgh, Birmingham, Leeds | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

The move toward cloud-first operating models

Most organisations now treat cloud as the default home for new workloads, shifting focus from simple cost savings to rapid innovation. This approach lets businesses scale AI and analytics on demand, trim the time needed for new service roll-outs and avoid heavy capital spend. Large financial groups, for example, run customer-facing apps on hyperscale platforms so they can add new features weekly rather than quarterly.[1]Microsoft Corporation, “FY25 Q3 Earnings Release,” microsoft.com

Government push for digital public services

Central and devolved administrations continue to digitise everything from tax submissions to hospital records. Clear targets, pooled budgets and a single oversight body reduce procurement friction and open steady work for tech suppliers. Citizens benefit from faster transactions and round-the-clock access to services, driving expectations that ripple into the private sector.[2]Cabinet Office, “Generative AI Framework for HMG,” gov.uk

Wider 5G and fibre coverage that unlocks edge computing

The march toward near-universal gigabit broadband and 5G means businesses outside major cities can finally deploy latency-sensitive applications. Manufacturers stream machine data to local edge nodes for real-time quality checks, while rural tele-health pilots cut travel times for patients. As coverage approaches national saturation, the gap between urban and rural digital capability narrows.

Safe-testing zones for generative-AI projects

Regulatory sandboxes give firms a controlled space to trial large-language-model services without risking compliance breaches. Financial institutions test AI assistants for complaints handling, and healthcare providers explore draft clinical notes, all under clear guardrails. Early clarity lowers legal risk and speeds time-to-production for breakthrough use cases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Not enough qualified cyber-security staff | -2.1% | Acute gaps in London and Manchester | Short term (≤2 years) |

| Ageing government IT estates | -1.8% | Central departments nationwide | Medium term (2–4 years) |

| Limited power capacity for new data centres | -1.4% | London and South-East England | Long term (≥4 years) |

| Uncertain post-Brexit data-sharing rules | -1.2% | Country-wide, affects firms with EU links | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Not enough qualified cyber-security staff

Nearly half of UK businesses report shortages in basic security skills, and competition for seasoned professionals drives salary inflation. Smaller firms struggle most, sometimes delaying cloud migrations or new digital services because they cannot staff monitoring roles. Government grant schemes and school outreach aim to widen the talent pool, but relief is unlikely in the next two years.

Ageing government IT estates

Many core public-sector systems still sit on decades-old frameworks, making integration with modern cloud services costly and time-consuming. Technical debt absorbs budgets that could fund new capabilities and complicates data sharing across departments. Until legacy platforms are retired or refactored, overall transformation momentum remains slower than policy ambition.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology Type: Generative AI Platforms Intensify Competition

The technology landscape is led by Cloud & Edge Computing, which captured 26.55% of the UK digital transformation market share in 2025. Continual investment in hyperscale facilities and regional data-centre build-outs positions cloud as the backbone for advanced workloads. Generative AI Platforms are on a steep 23.6% CAGR trajectory to 2031 as enterprises move from proof-of-concept to production deployments that automate content generation, software code assistance and intelligent search. The UK digital transformation market size attributed to AI platforms is forecast to expand markedly as regulatory sandboxes speed up pilots across finance and healthcare.

Analytics, machine learning and IoT retain broad relevance, underpinning predictive maintenance and customer-insight use cases. Extended-reality investments accelerate in defence and life-sciences training environments, validated by multi-million pound virtual-reality roll-outs for navy personnel and pharmaceutical engineers. Blockchain remains niche but gains credibility in digital identity, buoyed by government recognition of decentralised credentials. Industrial robotics and additive manufacturing adoption is steadier, concentrated in automotive, aerospace and food-processing plants that leverage Made Smarter grants to modernise legacy production lines. Together these sub-segments ensure the UK digital transformation market remains technology-agnostic yet innovation-driven.

By End-User Industry: Healthcare Growth Outpaces BFSI Leadership

Financial services maintained their leadership with a 18.65% revenue contribution in 2025, driven by open-banking compliance, real-time payments infrastructure and omnichannel service upgrades. The UK digital transformation market benefits from banks migrating core systems to cloud platforms while integrating AI-powered fraud detection and personalised advisory chatbots. However, Healthcare is growing faster at an 18.25% CAGR under NHS frontline digitisation mandates. Hospitals invest in electronic patient records, AI-enabled diagnostic tools and teleconsultation portals, which together broaden care access and rationalise costs.

Manufacturing leverages edge-enabled analytics to improve quality control and reduce unplanned downtime, aligning with government productivity objectives. Retail and e-commerce players deploy personalisation engines and unified inventory platforms that blur online-offline boundaries. Transportation and logistics operators prepare for autonomous-vehicle regulations that take effect from 2026, encouraging integrated fleet-management and safety-assurance systems. Finally, the public sector digitises licensing, taxation and benefits administration, reinforcing pervasive demand across the UK digital transformation market.

By Component: Services Sustain Majority Position

Services accounted for 52.70% of 2025 revenue, underscoring how organisational change-management, system integration and skills transfer often outweigh pure software expenditure. Consulting majors and niche boutiques codify repeatable playbooks for cloud migration, ERP replacement and data-governance frameworks, reducing execution risk for clients. The shift toward outcome-based fees increases alignment between provider and customer, incentivising measurable returns.

Solutions revenue, although smaller, accelerates at 15.75% CAGR as vendors bundle low-code platforms, AI accelerators and cybersecurity modules into subscription suites that shorten deployment cycles. Productised accelerators address SME pain points around compliance and reporting, broadening addressable demand. Both components reinforce the UK digital transformation market’s service-centric character while signalling growing appetite for integrated tooling.

By Deployment Mode: Cloud Dominance Inspires Hybrid-Edge Architectures

The cloud model represented 64.30% of deployments in 2025, reflecting its economic advantages and fast access to AI innovations. The associated 17.15% CAGR to 2031 indicates mainstream confidence in multitenant security, sovereign-cloud controls and pay-as-you-grow billing flexibility. Critical infrastructure operators such as National Grid adopt hybrid designs that couple central cloud orchestration with local edge nodes to meet latency and compliance requirements.

On-premise environments persist in defence, life-sciences and highly regulated public-sector workloads. Yet these installations increasingly expose Kubernetes or API gateways to exchange data with external cloud services, illustrating how hybrid patterns blur deployment distinctions. As 5G coverage expands nationwide, edge processing shifts nearer to sensors and devices, unlocking computer-vision and autonomous-system use cases. This continuum cements cloud’s role as the default innovation substrate within the UK digital transformation market.

By Organisation Size: SMEs Accelerate Through Democratised Tooling

Large enterprises held 67.20% revenue share in 2025, supported by capital strength, multi-year programme portfolios, and mature vendor ecosystems. Their continued investment anchors baseline demand across the UK digital transformation market. SMEs, however, are scaling faster at 16.65% CAGR on the back of government funding instruments and SaaS affordability. The British Business Bank’s Enterprise Capital Funds programme channels capital into deep-tech start-ups, stimulating local solution options that suit smaller operating budgets.

Cloud marketplaces, modular ERP suites, and managed-security offerings reduce complexity barriers, enabling SMEs to digitise customer engagement, supply-chain visibility, and compliance reporting without specialist teams. As a result, the UK digital transformation market experiences a democratising effect where digital capabilities spread beyond blue-chip organisations to the wider business community.

Geography Analysis

London and the South East remain the largest regional contributors owing to dense financial services, consulting, and policymaking ecosystems. The UK digital transformation market benefits from London-based venture funds that systematically back AI, cybersecurity, and fintech start-ups, reinforcing a virtuous cycle of innovation, talent attraction, and client proximity. National government departments headquartered in Westminster procure cloud, identity, and data-platform projects that become reference accounts for suppliers entering other regions.

Scotland exhibits robust momentum led by Edinburgh’s banking cluster and Glasgow’s industrial base. Universities in both cities anchor research partnerships that funnel data-science graduates into local employers, supporting a steady pipeline of skills. Devolved-government programmes emphasise rural broadband, digital-health pilots, and manufacturing competitiveness, helping the UK digital transformation market broaden beyond the M25 corridor. Wales and Northern Ireland follow similar trajectories, leveraging public-funded skills academies and 5G corridors to entice inward investment.

Northern England and the Midlands demonstrate rising adoption as Freeports, advanced-manufacturing zones, and regional tech hubs attract cloud datacentres and specialist integrators. Manchester, Leeds, and Birmingham combine lower operating costs with university talent pools, making them attractive near-shore delivery centres for consultancies. Government “levelling-up” grants prioritise fibre backhaul and smart-city pilots, creating ample contract flow for regional service providers. Collectively, these dynamics distribute the benefits of the UK digital transformation market more evenly across the country.

Mordor Intelligence's coverage of the digital transformation (dx) market extends across other regions including Europe, Africa, and Middle East, while country-specific intelligence is also available for Poland, France, Nigeria, United Arab Emirates, India, and Netherlands, each offering a view on the jurisdiction-level dynamics as applicable.

Competitive Landscape

The competitive field is moderately fragmented. Global hyperscalers such as Microsoft, Google and IBM leverage infrastructure scale and integrated AI toolchains to secure transformational contracts with banks, retailers and ministries. Microsoft’s Copilot generative-AI features, integrated into productivity suites, deepen account penetration and raise switching costs. IBM augments platform depth with advisory capacity, illustrated by its planned acquisition of Applications Software Technology LLC to extend Oracle Cloud expertise.

Tier-one consultancies—Accenture, Capgemini, CGI, Wipro and Infosys—specialise in industry solutions and large-scale change management. Accenture and Siemens formed a 7,000-strong joint business group focused on digital-twin adoption that promises 20% cost savings for manufacturers. UK-based systems integrators and managed-service providers such as BJSS, Softcat and Kainos compete in regulated markets where local delivery credentials and security clearances are decisive. Start-ups innovating in low-code automation, cybersecurity analytics and edge orchestration add dynamism, often partnering with channel distributors to reach mid-market clients.

Sustainability and sovereign-cloud considerations reshape selection criteria as buyers evaluate carbon intensity and data-residency guarantees alongside price and functionality. Providers offering integrated decarbonisation dashboards and UK-hosted AI inference zones gain competitive advantage. Overall, collaboration outpaces substitution: alliances between cloud vendors, consultants and telecom operators create bundled propositions that accelerate decision making and implementation across the UK digital transformation market.

United Kingdom Digital Transformation Industry Leaders

Google LLC (Alphabet Inc.)

IBM Corporation

Microsoft Corporation

Siemens AG

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Accenture and Siemens created a dedicated business group to scale industrial automation and AI twins.

- March 2025: CGI finalised its acquisition of BJSS, increasing UK headcount to 8,500 and expanding consulting-led services.

- February 2025: NHS England unveiled a virtual-reality training programme to upgrade healthcare professional skills.

- January 2025: IBM announced intent to acquire Applications Software Technology LLC to expand Oracle Cloud capabilities in public-sector transformations.

United Kingdom Digital Transformation Market Report Scope

Digital transformation is referred to as the process of incorporating digital technologies such as analytics, artificial intelligence, machine learning, extended reality (XR), Iot, industrial robotics, blockchain, additive manufacturing/3D printing, cybersecurity, cloud, and edge computing, and others (digital Twin, mobility, and connectivity) in various end-user industries across the United Kingdom.

United Kingdom digital transformation market is segmented by type (analytics, artificial intelligence, and machine learning, extended reality (XR), IoT, industrial robotics, blockchain, additive manufacturing/3D printing, cybersecurity, cloud, and edge computing, and others [digital Twin, mobility, and connectivity]) and end-user industry [manufacturing, oil, gas, and utilities, retail and e-commerce, transportation and logistics, healthcare, BFSI, telecom and IT, government and public sector and others (education, media & entertainment, environment, etc.)]. Market sizes and forecasts are provided in terms of value (USD ) for the segments

| Analytics, AI and ML |

| Generative AI Platforms |

| IoT |

| Industrial Robotics |

| Blockchain |

| Additive Manufacturing / 3-D Printing |

| Cyber-security |

| Cloud and Edge Computing |

| Others |

| Manufacturing |

| Oil, Gas and Utilities |

| Retail and E-commerce |

| Transportation and Logistics |

| Healthcare |

| BFSI |

| Telecom and IT |

| Government and Public Sector |

| Others |

| Solutions |

| Services |

| Cloud |

| On-premise |

| Large Enterprises |

| SMEs |

| By Technology Type | Analytics, AI and ML |

| Generative AI Platforms | |

| IoT | |

| Industrial Robotics | |

| Blockchain | |

| Additive Manufacturing / 3-D Printing | |

| Cyber-security | |

| Cloud and Edge Computing | |

| Others | |

| By End-User Industry | Manufacturing |

| Oil, Gas and Utilities | |

| Retail and E-commerce | |

| Transportation and Logistics | |

| Healthcare | |

| BFSI | |

| Telecom and IT | |

| Government and Public Sector | |

| Others | |

| By Component | Solutions |

| Services | |

| By Deployment Mode | Cloud |

| On-premise | |

| By Organisation Size | Large Enterprises |

| SMEs |

Key Questions Answered in the Report

What is the current value of the UK digital transformation market?

The UK digital transformation market is valued at USD 70.86 billion in 2026 and is projected to reach USD 140.2 billion by 2031.

Which industry segment is expanding the fastest?

Healthcare shows the fastest expansion, set to grow at an 18.25% CAGR through 2031 due to NHS digitisation mandates.

How dominant is cloud deployment across UK organisations?

Cloud deployment accounts for 64.30% of implementations in 2025 and is expected to rise at a 17.15% CAGR as enterprises pursue cloud-first strategies.

What role do SMEs play in the UK digital transformation market?

While large enterprises hold 67.20% share, SMEs are growing at 16.65% CAGR, supported by government finance schemes and affordable SaaS offerings.

Which technology type currently leads market adoption?

Cloud & Edge Computing leads with a 26.55% market share, followed by rapid growth in Generative AI Platforms.

What are the main barriers to digital transformation in the UK?

A cyber-security talent shortage and legacy systems in government agencies present the most significant near-term constraints on transformation projects.

Page last updated on: