Qatar Digital Transformation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

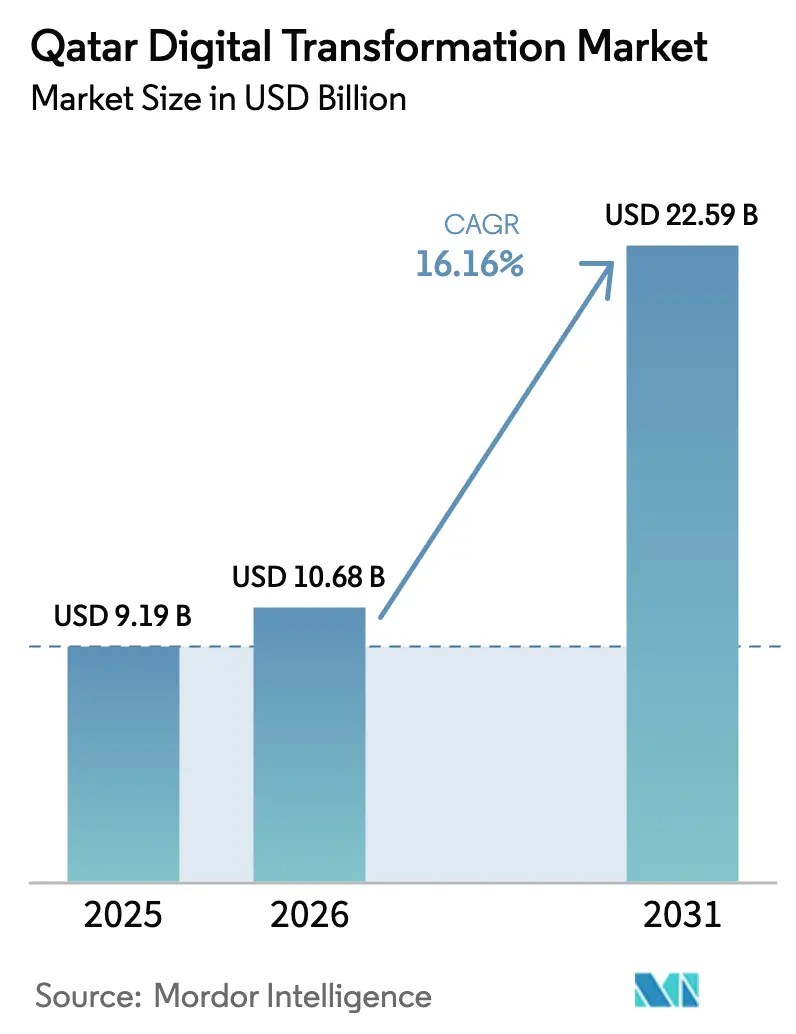

| Base Year Market Size (2025) | USD 9.19 Billion |

| Market Size (2026) | USD 10.68 Billion |

| Market Size (2031) | USD 22.59 Billion |

| Growth Rate (2026 - 2031) | 16.16% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Qatar Digital Transformation Market Analysis by Mordor Intelligence

The Qatar digital transformation market size was valued at USD 9.19 billion in 2025 and estimated to grow from USD 10.68 billion in 2026 to reach USD 22.59 billion by 2031, at a CAGR of 16.16% during the forecast period (2026-2031). Steady execution of national digital-agenda programs, rising cloud-first mandates, and sustained 5G rollout put the Qatar digital transformation market on a clear expansion path. Hyperscale datacenter launches slash latency and satisfy data-sovereignty rules, stimulating workload migration from on-premises environments and unlocking new platform revenues. Pervasive mobile broadband enables smart-city services, industrial IoT, and telehealth solutions that drive incremental demand across verticals. Large enterprises consolidate spending power through multi-year vendor accords, while government funding and accelerator schemes channel emerging-technology adoption into fast-scaling start-ups. In parallel, robust investment in artificial intelligence and analytics cultivates a specialized partner ecosystem able to capture high-value services opportunities.[1]Ministry of Communications and Information Technology, “Digital Agenda 2030,” MCIT.GOV.QA

Key Report Takeaways

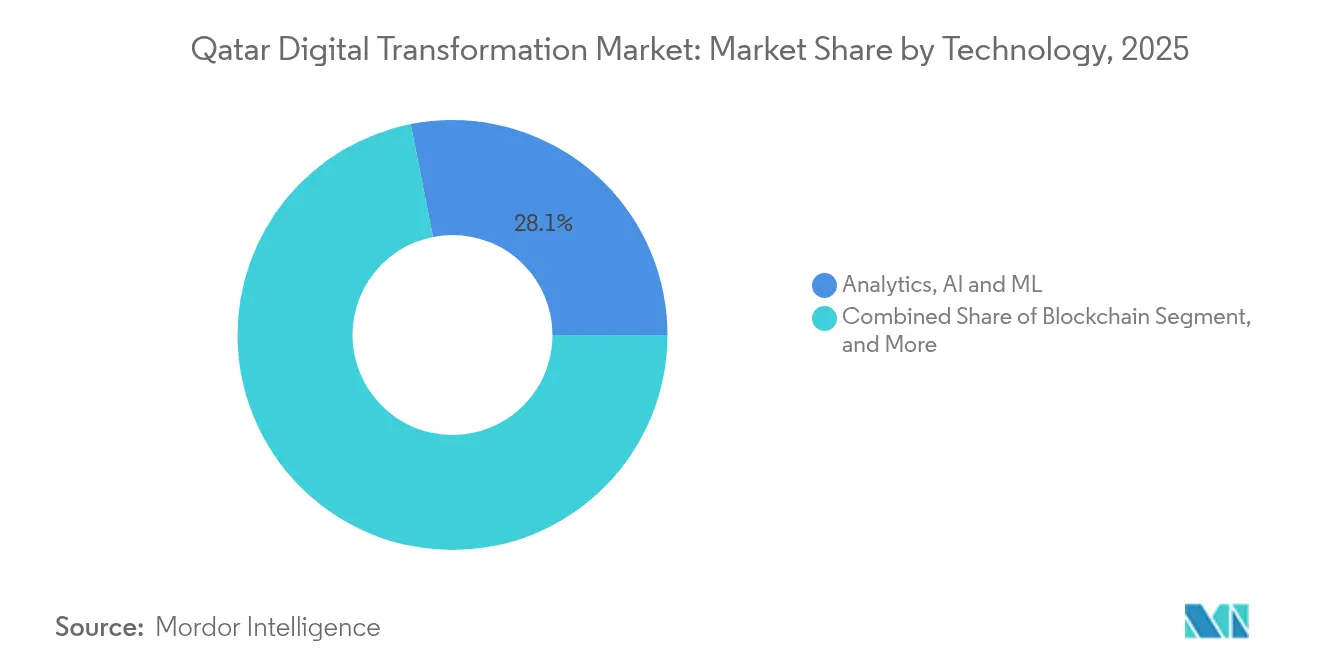

- By technology, analytics, artificial intelligence and machine learning held a 28.12% share of the Qatar digital transformation market in 2025, whereas blockchain is forecast to advance at an 18.02% CAGR through 2031.

- By end-user industry, government and public sector accounted for 24.55% of the Qatar digital transformation market in 2025, while retail and e-commerce are expected to expand at a 19.12% CAGR to 2031.

- By deployment mode, cloud deployment captured 56.62% of the Qatar digital transformation market share in 2025 and is also the fastest-growing option with a 17.35% CAGR through 2031.

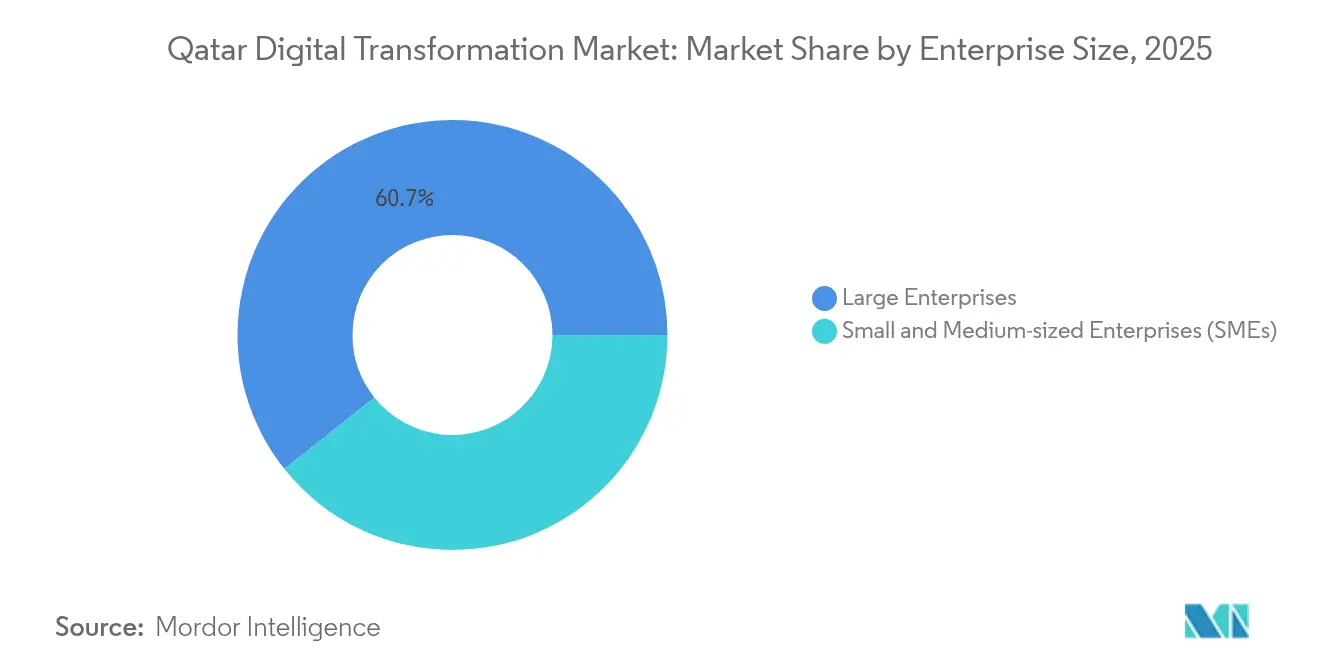

- By enterprise size, large enterprises represented 60.72% of adoption in 2025, whereas small and medium-sized enterprises are poised for an 18.27% CAGR through 2031.

- By service type, consulting services led at 32.14% of 2025 value; managed services are projected to post a 18.74% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Qatar forms part of a network that extends across countries and regions, each contributing to a shared international environment. The global digital transformation (dx) market outlook by Mordor Intelligence consolidates those connections.

Qatar Digital Transformation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government's Qatar National Vision 2030 digital pillars | +4.20% | National, with concentrated effects in Doha, Lusail, Msheireb | Long term (≥ 4 years) |

| Surge in cloud adoption across Qatari enterprises | +3.80% | National, with spillover to regional operations | Medium term (2-4 years) |

| Rapid proliferation of 5G-enabled mobile devices and apps | +2.90% | National, with early gains in Doha, West Bay, Lusail | Short term (≤ 2 years) |

| Growing investments in big-data analytics and AI | +3.10% | National, with research concentration in QSTP, HBKU | Medium term (2-4 years) |

| Mandatory e-invoicing roll-out by Qatar Tax Authority | +1.80% | National, affecting all registered businesses | Short term (≤ 2 years) |

| Under-the-radar – Post-World-Cup smart-stadium technology spill-over | +1.40% | National, with technology transfer to smart cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government’s Qatar National Vision 2030 Digital Pillars Drive Comprehensive Transformation

High-level oversight by the Steering Committee for Smart Government and Digital Leadership has accelerated 29 integrated projects targeting world-class e-government delivery.[2] Centralized platforms such as the Tawtheeq National Authentication Service streamline citizen engagement, while Qatar Cloud Services supplies sovereign infrastructure for agencies transitioning from legacy stacks. Continuous advancement in the UN E-Government Development Index underscores tangible progress and positions the Qatar digital transformation market for sustained long-term growth.

Surge in Cloud Adoption Accelerated by Strategic Partnerships

Cloud maintains the largest deployment footprint in the Qatar digital transformation market, reinforced by the Azure OpenAI region and Google Cloud’s Center of Excellence. Native availability of hyperscale services encourages full-stack migrations, evidenced by SAP RISE deals in cement, banking, and aviation sectors. In-country data residency both complies with regulation and reassures risk-averse enterprises, lifting the appeal of consumption-based pricing models.

Rapid 5G Infrastructure Expansion Enables Advanced Applications

Nationwide 5G coverage positions Qatar first globally in mobile internet speed, enabling low-latency use cases such as autonomous vehicles and critical-infrastructure monitoring.[3]The Peninsula, “MCIT Signs Partnership with Microsoft,” THEPENINSULAQATAR.COM Vendor collaborations are piloting private 5G networks in manufacturing plants, airports, and energy facilities, translating network capability into sector-specific solutions that deepen the Qatar digital transformation market footprint.

Growing AI and Analytics Investments Create Innovation Ecosystem

A USD 2.5 billion commitment to AI infrastructure, complemented by a five-year partnership with Scale AI, embeds predictive analytics across more than 50 public-service applications. Research centers at Hamad Bin Khalifa University and Qatar Computing Research Institute commercialize algorithms for medical imaging and traffic optimization, seeding intellectual property that domestic integrators can scale into regional export offerings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened concerns over data privacy and cyber-security | -2.10% | National, with regulatory compliance affecting all sectors | Medium term (2-4 years) |

| Shortage of advanced digital skills in local workforce | -2.80% | National, with acute impact in Doha tech sector | Long term (≥ 4 years) |

| Heavy reliance on expatriate IT talent causing churn | -1.90% | National, affecting private sector competitiveness | Medium term (2-4 years) |

| Fragmented legacy systems in state-owned enterprises | -1.60% | National, concentrated in government and utilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cybersecurity Skills Gap Constrains Transformation Velocity

The National Cybersecurity Strategy 2024-2030 highlights acute workforce deficits that could cap adoption speed. Salary premiums for senior roles underscore scarcity, and although new academies and scholarship programs are underway, internal capabilities remain uneven across sectors.

Legacy-System Integration Complexity in State Enterprises

State-owned entities face heavy technical debt, with multiyear migrations such as Qatar Petroleum’s shift to ABB 800xA required to modernize control centers without operational disruption. Extended timelines and specialized vendor expertise inflate project costs and can delay benefits realization for the Qatar digital transformation market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Analytics and AI Anchor Spending

Analytics, artificial intelligence and machine learning captured 28.12% of the Qatar digital transformation market size in 2025, illustrating the centrality of data-driven decision-making across sectors. Public-sector use cases from tax-fraud detection to predictive maintenance set benchmarks rapidly mirrored by financial services and transport operators. Blockchain, underpinned by a USD 50 million digital-assets studio, is projected to record an 18.02% CAGR, the swiftest growth rate among emerging technologies.

Edge-to-cloud architectures, industrial robotics, and digital-twin deployments round out adoption priorities as enterprises seek operational resilience and supply-chain visibility. Continuous AI model retraining strengthens competitive defensibility, and local research institutions expand patent portfolios that elevate the Qatar digital transformation market on a regional stage.

By End-User Industry: Government Leadership Spurs Private Uptake

Government and public sector accounted for 24.55% of the Qatar digital transformation market in 2025 thanks to integrated platforms such as Dhareeba and the TASMU Smart Qatar program. Successful delivery of citizen-facing services validates large-scale cloud and AI initiatives and encourages regulatory clarity.

Retail and e-commerce, propelled by mobile-first consumer behaviour and supportive policy workshops, is forecast to grow at a 19.12% CAGR through 2031, outpacing other industries. Banking, healthcare, and utilities continue to scale digital interfaces and automation, broadening the user base and deepening overall spend in the Qatar digital transformation market.

By Deployment Mode: Cloud Dominance Continues

Cloud captured 56.62% of the Qatar digital transformation market share in 2025, while hybrid models satisfy workloads with strict latency or compliance thresholds. Enterprise reliance on locally hosted hyperscale regions accelerates SaaS uptake and simplifies disaster-recovery design.

On-premises footprints persist in oil and gas, where real-time control systems mandate air-gapped security. Nevertheless, the 17.35% CAGR projected for cloud confirms its role as the default for new workloads, reinforcing Qatar digital transformation market momentum across sectors.

By Enterprise Size: SME Digitization Accelerates

Large enterprises commanded 60.72% of 2025 spending as they standardized platforms across multi-business portfolios. Scale grants bargaining power with global vendors and allows rapid trial-to-production cycles for AI services.

Small and medium-sized enterprises, projected to grow at an 18.27% CAGR, benefit from subsidized accelerator programs and low-entry cloud pricing. Widespread availability of fintech and logistics APIs lowers operational hurdles, inserting thousands of SMEs into the Qatar digital transformation market value chain.

By Service Type: Consulting Leads, Managed Services Gains Momentum

Consulting services represented 32.14% of 2025 value, reflecting demand for roadmap design, regulatory compliance, and change-management support. Multi-disciplinary teams integrate cybersecurity with process-re-engineering to safeguard project ROI.

Managed services are expected to log a 18.74% CAGR through 2031 as organizations outsource monitoring, automation, and AI-ops functions to focus on core competencies. This trend widens recurring-revenue pools for vendors and increases service depth across the Qatar digital transformation market.

Geography Analysis

Doha holds the lion’s share of the Qatar digital transformation market owing to dense government bodies, financial headquarters, and newly established data centers. Smart-city deployments in Msheireb Downtown mesh more than 650,000 sensors, creating a live showcase that attracts solution providers and investors. Continuous 5G and fiber upgrades further entrench the capital’s leadership.

Lusail City ranks as the fastest-growing geography after locking in a USD 60 million smart-infrastructure contract through 2027. Its integrated command-and-control platform, AI-governed utilities, and autonomous-transit pilots generate fertile demand for analytics, cybersecurity, and mobility applications.

Industrial corridors in Mesaieed and Ras Laffan extend influence beyond hydrocarbons. Advanced process-control retrofits, industrial IoT, and digital-twin modelling lift operational efficiency and safety benchmarks, channelling specialized vendors into the broader Qatar digital transformation market. Research hubs within Qatar Science and Technology Park and Free Zones add a pipeline of start-ups and foreign entrants, balancing geographic concentration with nationwide capability diffusion.

Mordor Intelligence delivers a comprehensive view of the digital transformation (dx) market across all major regions such as Europe, North America, and Africa, alongside country-level analysis for Nigeria, Poland, United States, Malaysia, Indonesia, and Brazil, each offering a view of the local market realities.

Competitive Landscape

Competition in the Qatar digital transformation market remains moderate, with global vendors embedding operations to comply with data-residency and talent-development mandates. Microsoft, Google Cloud, Oracle, and SAP anchor large contracts, often in consortium with local integrators. Five-year frameworks such as the Scale AI public-sector engagement signal a shift from transactional deals to strategic partnerships that de-risk multiyear transformations.

Local systems integrators like Qatar Computer Services carve niches in government and energy verticals, while telecom operators leverage 5G assets to offer edge and private-network services. Consulting majors reinforce capabilities through joint innovation centers, upskilling programs, and sovereign-cloud offerings that dovetail with national policy. Vendor differentiation increasingly hinges on cybersecurity assurances, carbon-neutral operations, and contribution to the domestic skills pipeline, shaping a landscape characterized by solution breadth rather than price discounting.

Qatar Digital Transformation Industry Leaders

IBM Corporation

Microsoft Corporation

Wipro Limited

Qatar Computer Services

Ooredoo Qatari Public Shareholding Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Ministry of Communications and Information Technology partnered with Microsoft to launch Azure OpenAI services across government and private sectors, hosted in the local datacentre region

- February 2025: Qatar and Scale AI entered a five-year pact to inject AI into more than 50 public-service applications

- February 2025: Media City Qatar and Huawei agreed to develop a smart media campus featuring AI-powered access control and multi-cloud storage

- February 2025: MCIT introduced the Scale Now program to mentor digital entrepreneurs and ready them for regional expansion

Qatar Digital Transformation Market Report Scope

Digital transformation leverages digital technologies such as artificial intelligence and machine learning, extended reality (XR) for industrial applications, and IoT to create new business processes or modify existing ones, reshape organizational culture, and enhance customer experiences.

Qatari digital transformation market is segmented by type (analytics, artificial intelligence, and machine learning, extended reality (XR), IoT, industrial robotics, blockchain, additive manufacturing/3D printing, cybersecurity, cloud, and edge computing, and others (digital twin, mobility, and connectivity)) end-user industry (manufacturing, oil, gas and utilities, retail & e-commerce, transportation and logistics, healthcare, BFSI, telecom and IT, government and public sector, and others (education, media & entertainment, environment etc)). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| Analytics, Artificial Intelligence and Machine Learning |

| Extended Reality (XR) |

| Internet of Things (IoT) |

| Industrial Robotics |

| Blockchain |

| Additive Manufacturing / 3D Printing |

| Cybersecurity |

| Cloud Edge Computing |

| Digital Twin |

| Mobility and Connectivity |

| Manufacturing |

| Oil, Gas and Utilities |

| Retail and e-commerce |

| Transportation and Logistics |

| Healthcare |

| Banking, Financial Services and Insurance (BFSI) |

| Telecom and IT |

| Government and Public Sector |

| Education |

| Media and Entertainment |

| Environment and Sustainability |

| On-Premise |

| Cloud |

| Hybrid |

| Small and Medium-sized Enterprises (SMEs) |

| Large Enterprises |

| Consulting |

| Integration and Implementation |

| Managed Services |

| Support and Maintenance |

| Training and Education |

| By Technology | Analytics, Artificial Intelligence and Machine Learning |

| Extended Reality (XR) | |

| Internet of Things (IoT) | |

| Industrial Robotics | |

| Blockchain | |

| Additive Manufacturing / 3D Printing | |

| Cybersecurity | |

| Cloud Edge Computing | |

| Digital Twin | |

| Mobility and Connectivity | |

| By End-User Industry | Manufacturing |

| Oil, Gas and Utilities | |

| Retail and e-commerce | |

| Transportation and Logistics | |

| Healthcare | |

| Banking, Financial Services and Insurance (BFSI) | |

| Telecom and IT | |

| Government and Public Sector | |

| Education | |

| Media and Entertainment | |

| Environment and Sustainability | |

| By Deployment Mode | On-Premise |

| Cloud | |

| Hybrid | |

| By Enterprise Size | Small and Medium-sized Enterprises (SMEs) |

| Large Enterprises | |

| By Service Type | Consulting |

| Integration and Implementation | |

| Managed Services | |

| Support and Maintenance | |

| Training and Education |

Key Questions Answered in the Report

How large is the Qatar digital transformation market in 2026?

The Qatar digital transformation market size is USD 10.68 billion in 2026.

What is the expected growth rate through 2031?

The market is forecast to grow at a 16.16% CAGR through 2031.

Which deployment mode dominates spending?

Cloud deployment leads with 56.62% share in 2025 and remains the fastest-growing option.

Which end-user segment is expanding the quickest?

Retail and e-commerce is projected to register a 19.12% CAGR between 2026 and 2031.

What technology segment commands the largest share?

Analytics, artificial intelligence and machine learning held a 28.12% share in 2025.

Why are managed services gaining traction?

Organizations outsource monitoring and automation to focus on core operations, driving a 18.74% CAGR for managed services.

Page last updated on: