Middle East Digital Transformation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

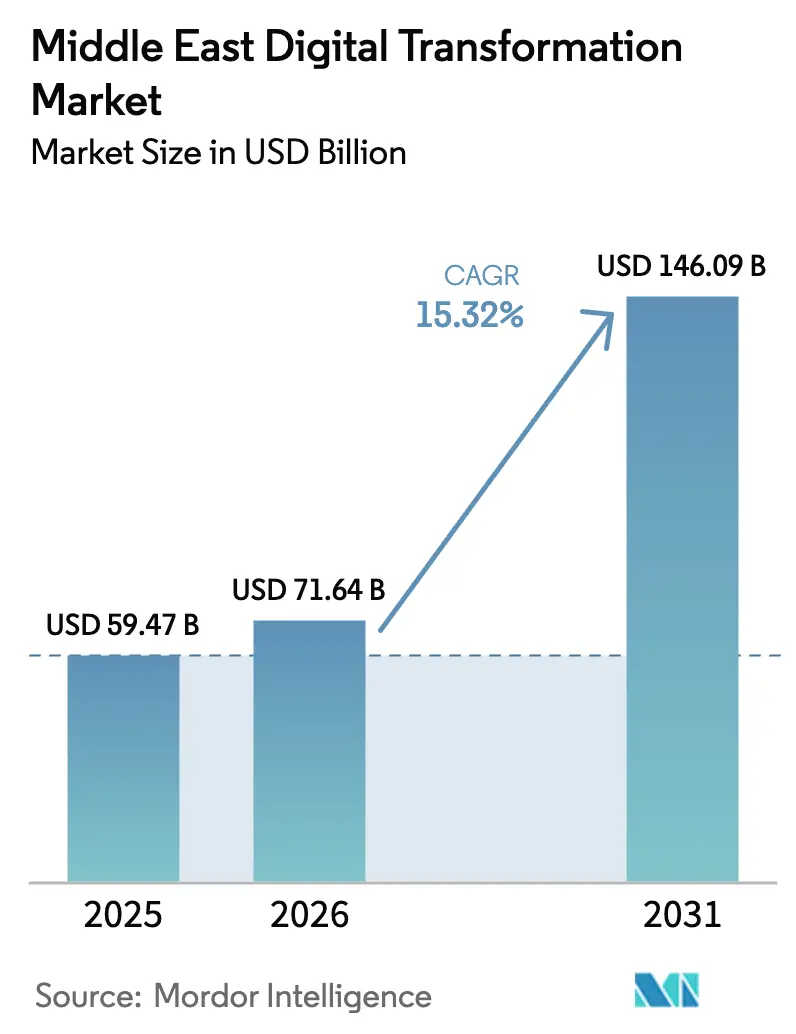

| Base Year Market Size (2025) | USD 59.47 Billion |

| Market Size (2026) | USD 71.64 Billion |

| Market Size (2031) | USD 146.09 Billion |

| Growth Rate (2026 - 2031) | 15.32% CAGR |

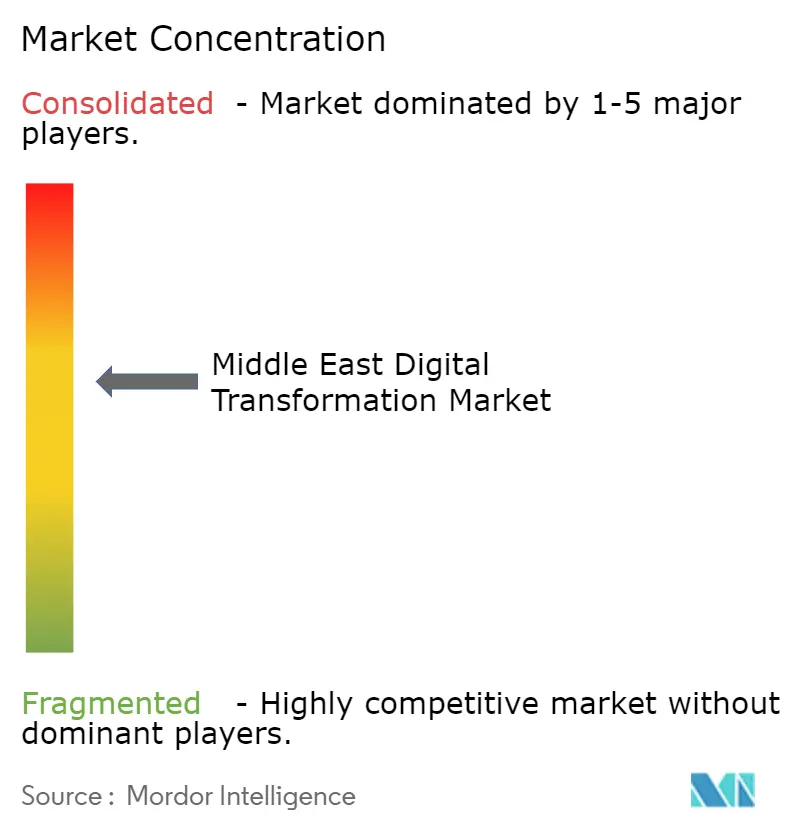

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Digital Transformation Market Analysis by Mordor Intelligence

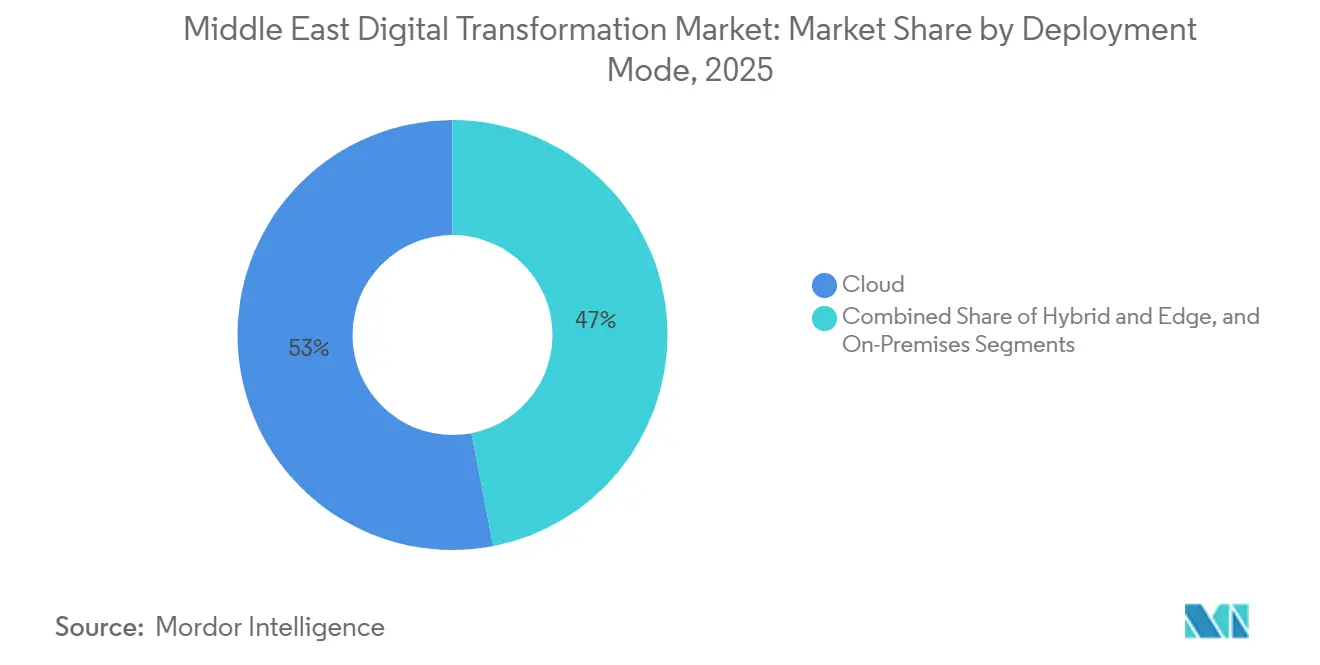

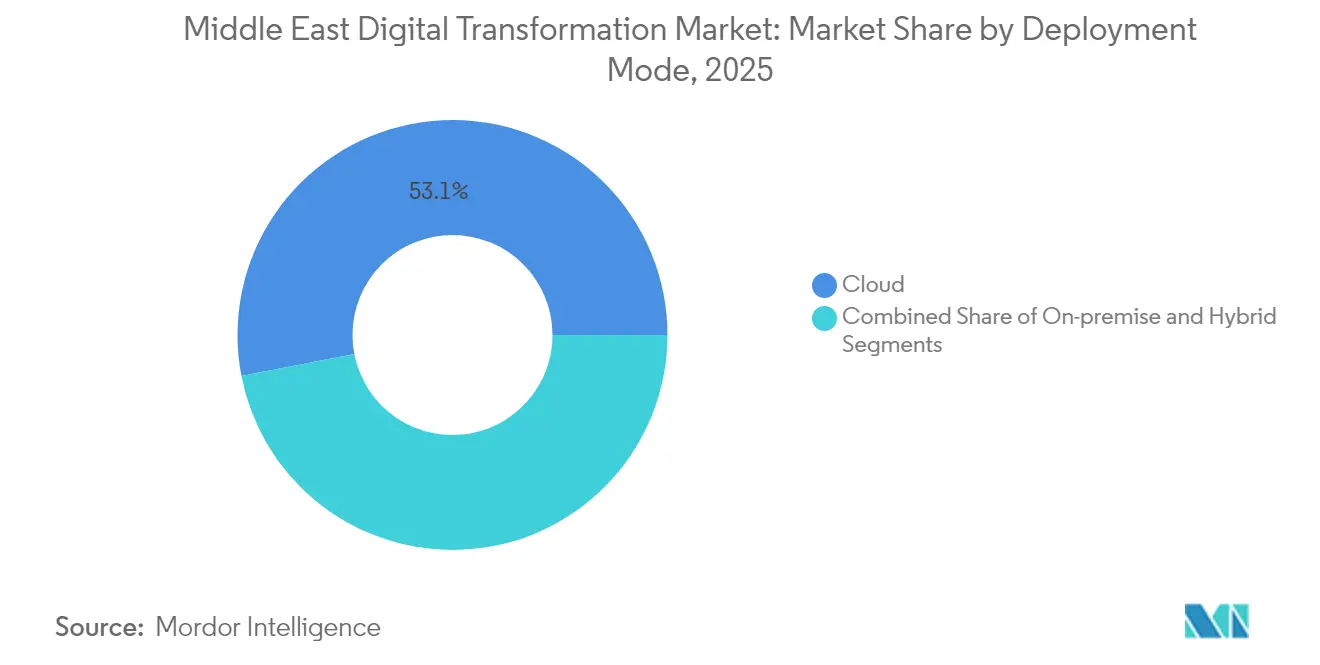

The Middle East digital transformation market size is expected to increase from USD 59.47 billion in 2025 to USD 71.64 billion in 2026 and reach USD 146.09 billion by 2031, growing at a CAGR of 15.32% over 2026-2031. Structural policy pivots across the Gulf Cooperation Council are redirecting sovereign wealth into large-scale artificial intelligence infrastructure, hyperscale cloud regions and national large language model programs that pull the region away from technology import dependence and toward home-grown capability. Mega-projects such as Saudi Arabia’s USD 5 billion NEOM DataVolt AI data center scheduled for 2028 and the United Arab Emirates’ Falcon and Jais 2 Arabic models illustrate how governments are compressing innovation cycles and attracting complementary private capital. Cloud deployment accounted for 53.04% of spending in 2025, reflecting enterprises’ preference for pay-as-you-go platforms that bypass on-premises capital outlays, while hybrid and edge architectures are projected to advance 17.19% through 2031 as latency-sensitive use cases in energy, manufacturing and logistics demand on-site compute. Banking, financial services and insurance led end-user spending at 18.56% in 2025, and healthcare is forecast to grow 17.31% as telemedicine and electronic health records scale. Saudi Arabia captured 34.11% of regional outlays in 2025, underpinned by its USD 40 billion AI commitment, while the UAE is set to expand 16.89% on the back of a USD 10 billion semiconductor and AI allocation. Competition is intensifying as global systems integrators and hyperscalers invest in in-country infrastructure, but local champions leverage Arabic-language AI and government ties to defend share. Talent shortages, GPU supply constraints and tightening cybersecurity mandates remain material headwinds to deployment velocity.

Key Report Takeaways

- By deployment mode, cloud commanded 53.04% revenue share of the Middle East digital transformation market in 2025. Hybrid and edge architectures are forecast to register a 17.19% CAGR through 2031.

- By technology type, Cloud and Edge Computing accounted for 22.47% of 2025 spending, while Artificial Intelligence and Machine Learning are slated to expand at a 18.07% CAGR between 2026-2031.

- By end-user industry, banking, financial services and insurance held 18.56% of the Middle East digital transformation market share in 2025. Healthcare is projected to record the fastest growth with a 17.31% CAGR to 2031.

- By enterprize size, Large enterprises accounted for 66.69% of 2025 spending, while small and medium enterprises are slated to expand at a 16.97% CAGR between 2026-2031.

- By region, Saudi Arabia led with 34.11% of regional spending in 2025 and remains the anchor market through the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide industry scale is not derived from any single region but from the combination of national and regional inputs. The digital transformation (dx) market size of Mordor Intelligence integrates these into one global valuation.

Middle East Digital Transformation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Mega-Initiatives Accelerating ICT and AI Spend | +3.8% | Saudi Arabia, UAE, spillover to Qatar and Kuwait | Medium term (2-4 years) |

| Hyperscale Cloud Region Rollouts Cutting Transformation Costs | +3.2% | GCC-wide, led by UAE and Saudi Arabia | Short term (≤ 2 years) |

| 5G and Fiber Network Densification Enabling IoT Scale-Up | +2.7% | UAE, Saudi Arabia, Qatar | Medium term (2-4 years) |

| Sovereign Wealth and Private-Capital Surge into AI Infrastructure | +2.4% | Saudi Arabia, UAE | Long term (≥ 4 years) |

| Emergence of Sovereign AI and National LLM Projects | +1.9% | Saudi Arabia, UAE, nascent in Qatar | Long term (≥ 4 years) |

| Telecom-Infrastructure Monetization Unlocking Digital CAPEX | +1.4% | Saudi Arabia, UAE, Kuwait | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Mega-Initiatives Accelerating ICT and AI Spend

Saudi Arabia earmarked more than SAR 113 billion (USD 30.1 billion) for ICT over a three-year horizon, and its 2026 budget prioritizes digital administration and artificial intelligence, signaling intent to cut hydrocarbon dependency. NEOM DataVolt’s planned 1.5 GW capacity exemplifies commitment to build supply ahead of private demand. The UAE mirrors this push through its national AI strategy and the Falcon and Jais 2 Arabic models, which widen access to Arabic-language applications.[1]“Falcon and Jais 2 Arabic LLMs,” AI.GOV.AE Procurement cycles for cloud, cybersecurity and enterprise software are shortening as agencies face digitization mandates, and spillover is nudging Qatar’s smart-city pilots and Kuwait’s fintech sandbox.

Hyperscale Cloud Region Rollouts Cutting Transformation Costs

Microsoft’s Saudi Azure region will reach general availability in Q4 2026, complementing Oracle’s UAE Central and UAE East zones and demonstrating that local availability zones unlock regulated-industry demand.[2]“Saudi Azure Region,” AZURE.MICROSOFT.COM Khazna Data Centers, jointly owned by G42 Holding and Etisalat, targets 1 GW over five years, underscoring the scale required for AI workloads. Data center capacity is projected to triple by 2030, led by Saudi Arabia, shrinking on-premises total cost of ownership. Aramco’s industrial distributed cloud places compute at oil sites to deliver sub-10 ms analytics. Edge-ready architectures are thus emerging as the default for energy and manufacturing operators navigating data-residency rules.

5G and Fiber Network Densification Enabling IoT Scale-Up

The UAE posted a median 5G download speed of 1.24 Gbps in Q4 2025, the fastest worldwide. Twenty-three operators across nine Middle East and North Africa markets have commercial 5G, and GCC adoption is on track for 95% by 2030. Qualcomm and Etisalat inaugurated a 5G and edge AI engineering center in Abu Dhabi, reinforcing telecoms’ priority to monetize next-generation connectivity.[3]Qualcomm-Etisalat Engineering Center,” QUALCOMM.COM Fiber-to-the-home penetration exceeds 80% in core metros, yet rural gaps curb uniform IoT rollout. Industrial robotics, autonomous logistics and smart-grid projects rely on these high-bandwidth, low-latency links to flourish.

Sovereign Wealth and Private-Capital Surge into AI Infrastructure

Saudi Arabia’s Public Investment Fund set aside USD 40 billion for AI by 2030 and unveiled a USD 100 billion AI-focused vehicle in 2024, anchoring compute capacity and talent at home. Mubadala allocated USD 10 billion to chips and AI in 2024, and Microsoft bought a USD 1.5 billion stake in G42 Holding, bundling technology transfer with capital. Venture funding rose to USD 1.5 billion in the UAE and USD 1.1 billion in Saudi Arabia in 2024, compressing the scale-up timeline for startups. However, execution risk persists as talent pipelines and regulation chase the speed of investment, risking under-utilized assets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic Shortage of Senior Digital Talent and AI Specialists | -2.1% | Saudi Arabia, UAE, broader GCC | Short term (≤ 2 years) |

| Heightened Cybersecurity and Data-Sovereignty Compliance Risks | -1.6% | GCC-wide, stronger in Saudi Arabia and UAE | Medium term (2-4 years) |

| GPU and Advanced-Server Supply Bottlenecks | -1.3% | Global, delays in Saudi Arabia, UAE, Qatar | Short term (≤ 2 years) |

| Energy-Water Constraints for Hyperscale Data Center Cooling | -0.9% | Saudi Arabia, UAE | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chronic Shortage of Senior Digital Talent and AI Specialists

Saudi Arabia needs 230,000 ICT professionals by 2030 yet graduates only 20,000 a year.[4]“ICT Talent Gap Analysis,” MCIT.GOV.SA The UAE reports that 30% of firms cannot recruit qualified AI talent, driving wage inflation and project delays. Systems integrators rely on expatriate consultants, but visa quotas and cultural assimilation hurdles raise costs. Universities are expanding computer-science programs, but updated curricula and practical cloud training lag employer demand. Fast-track certifications will help, though a mid-career talent pool will not materialize before 2028, constraining sovereign LLM deployments.

Heightened Cybersecurity and Data-Sovereignty Compliance Risks

Cyberattacks rose 28% in 2024, with ransomware hitting 60% of surveyed firms. Saudi Arabia’s Personal Data Protection Law, fully enforced since September 2024, levies fines up to SAR 3 million (USD 800,000) and mandates in-kingdom storage for sensitive data. UAE rules impose adequacy checks on cross-border transfers for finance and healthcare, adding legal overhead. Enterprises now fund security operations centers and compliance audits in parallel, a burden that smaller businesses struggle to shoulder, widening the digital divide.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Dominance Amid Hybrid Momentum

Cloud deployment held 53.04% of the Middle East digital transformation market share in 2025, while hybrid and edge architectures are forecast to post a 17.19% CAGR through 2031. Widespread in-country availability zones lower compliance hurdles and shrink time-to-launch for regulated enterprises that once relied on on-premises estates. Organizations now value externally certified uptime and pay-as-you-go pricing over the capital drag of self-managed servers. Hybrid traction accelerates as ministries and oil majors demand on-site compute for latency-sensitive tasks, yet still want centralized orchestration for non-critical workloads. Saudi and UAE residency statutes amplify this pivot by compelling foreign vendors to keep certain data categories inside national borders.

Latency-sensitive oil, gas and utilities projects already embed micro-data centers next to rigs and substations to keep response times below 10 ms. Aramco’s industrial distributed cloud, which pushes analytics to field assets, illustrates how hybrid cuts bandwidth backhaul and security exposure. Private 5G networks in industrial zones further expand edge potential by giving factories deterministic connectivity that public networks struggle to guarantee. As residency laws tighten across the Gulf, hybrid adoption shifts from an optional architecture to a strategic safeguard, ensuring continuous operations even when cross-border links falter.

By Technology Type: AI Outpaces the Legacy Stack

Cloud and edge platforms represented 22.47% of the Middle East digital transformation market share in 2025, yet artificial intelligence and machine learning are projected to deliver an 18.07% CAGR over 2026-2031. Sovereign AI programs, such as the Falcon and Jais 2 Arabic language models, accelerate compute demand as agencies insist that mission-critical inference stays inside national borders. These large models expand Arabic natural-language coverage, unlocking public-sector chatbots, education tools and media localization that imported platforms overlook.

Extended-reality pilots remain niche but gain traction in surgical training and immersive retail, while low-cost headsets improve accessibility. Internet of Things sensors proliferate across upstream oil and gas facilities where predictive maintenance slashes unplanned shutdowns. Digital twins model refinery behavior and city utilities, feeding operational data back into AI algorithms that refine simulations in near real time. Security spending climbs alongside broader attack surfaces, embedding zero-trust frameworks as default rather than discretionary. Together, these layers shift budget toward AI-first, data-centric architectures that rest on mature cloud foundations.

By End-User Industry: BFSI Leads and Healthcare Accelerates

Banking, financial services and insurance accounted for 18.56% of the Middle East digital transformation market share in 2025. Saudi and UAE open-banking frameworks catalyzed API ecosystems that let fintechs deliver mobile payments, micro-lending and robo-advisory at scale. High smartphone penetration, above 85% in both countries, redirected customer traffic from physical branches to digital channels, freeing capital to underwrite AI fraud-detection and credit-scoring engines. Banks now deploy conversational bots that operate natively in Arabic dialects, increasing cross-sell rates and shortening complaint resolution cycles.

Healthcare is set to expand at a 17.31% CAGR to 2031 as telemedicine revenue hit USD 500 million in the UAE in 2024 and electronic health records reached 70% penetration among Saudi providers that same year. The pandemic normalized remote consultations, and regulators subsequently codified licensing and reimbursement, locking in demand. Hospitals now trial AI triage that routes non-critical cases to virtual care, releasing scarce specialist hours for complex procedures. Cloud-based picture archiving and analytics compress diagnostic turnaround from days to minutes, while IoT wearables stream post-surgery vitals directly into clinician dashboards. These dynamics elevate healthcare to the second-fastest spending vertical behind BFSI.

By Enterprise Size: SMEs Narrow the Digital Gap

Large enterprises controlled 66.69% of the Middle East digital transformation market size in 2025. Deep balance sheets let conglomerates modernize ERP, CRM and supply-chain platforms in lockstep with Vision 2030 mandates. Centralized digital roadmaps align cybersecurity, data governance and sustainability objectives, while captive innovation hubs test emerging technologies before group-wide rollouts.

Small and medium enterprises are projected to grow at a 16.97% CAGR through 2031 as subsidized cloud vouchers in the UAE and grant programs under Saudi Arabia’s Monsha’at initiative lower entry costs. Low-code SaaS suites enable non-technical staff to automate workflows that once required specialist developers. Digital bookkeeping and e-invoicing feed alternative credit-scoring, widening financing access for smaller sellers. Compliance templates published by regulators reduce legal overhead, although SMEs still struggle to match enterprise salary bands for experienced talent. As platforms abstract complexity, the spending gap shrinks, but skill shortages and cyber-risk awareness remain persistent hurdles.

Geography Analysis

Saudi Arabia commanded 34.11% of the Middle East digital transformation market in 2025, propelled by a USD 40 billion AI pledge and a USD 100 billion dedicated fund that anchor compute supply. NEOM DataVolt’s 1.5 GW target positions the kingdom to host sovereign LLMs and serve regulated workloads locally. The Personal Data Protection Law forces multinationals to deploy hybrid patterns, bolstering domestic service providers. Execution risk persists because talent graduation rates lag demand and supply-chain delays for GPUs slow data-center commissioning.

The UAE is forecast to expand 16.89% between 2026-2031, buoyed by Mubadala’s USD 10 billion AI and semiconductor allocation and the operational Oracle cloud regions. Khazna plans 1 GW new capacity, and the nation leads global 5G speeds at 1.24 Gbps. High connectivity and sovereign-wealth capital create a reinforcing ecosystem for fintech, healthcare AI and advanced manufacturing. Nonetheless, desalinated-water-intensive cooling raises sustainability and cost concerns as data-center footprints swell.

Qatar, Kuwait and a cohort of smaller markets, Israel, Bahrain, Oman, Jordan and Iran, present mixed outlooks. Qatar leverages smart-city pilots but is constrained by a smaller population. Kuwait fosters fintech sandboxes yet lacks the fiscal firepower of its neighbors. Israel excels in cybersecurity and AI start-ups but remains demographically limited. Bahrain’s finance cluster explores blockchain for trade facilitation, while Oman and Jordan channel resources into fiber and digital literacy. Sanction-bound Iran turns to domestic providers, curbing access to advanced chips. Divergent policy support and capital depth imply that the Middle East digital transformation market will bifurcate, with Saudi Arabia and the UAE extending their lead over peripheral economies.

Mordor Intelligence tracks the digital transformation (dx) market across other major regions such as Latin America, Asia, and Europe, with additional country-level coverage spanning Oman, United Arab Emirates, Israel, Qatar, Brazil, and Colombia, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

Global systems integrators such as Accenture, Deloitte, PwC, Ernst and Young and Capgemini compete with hyperscalers Amazon Web Services, Microsoft Azure, Google Cloud and Oracle as each builds in-country regions to satisfy data-residency laws. Local champions G42 Holding, Etisalat by e and, stc Group and Ooredoo Group deploy Arabic-language AI and leverage government relationships to win contracts that multinationals struggle to penetrate. Microsoft’s USD 1.5 billion stake in G42 Holding illustrates hyperscalers’ willingness to exchange equity and intellectual property for market entry advantages.

Huawei and Ericsson vie for 5G network deals, yet security reviews skew procurement toward suppliers aligned with geopolitical preferences. Cisco, SAP and Siemens embed industry-specific modules to differentiate beyond generic cloud. Cognizant and Wipro scale Saudi and UAE delivery hubs to offset talent shortages and reduce project costs. The Middle East digital transformation market therefore balances global technology breadth with local domain expertise.

White-space opportunities emerge in Arabic natural language processing, compliance-as-a-service and edge inference for heavy industry. Smaller firms such as Baarez Technology Solutions and Techcarrot specialize in vertical software but lack scale. Telecom tower monetization, exemplified by stc Group’s SAR 3.75 billion (USD 1 billion) sale of 30% of TAWAL to Mubadala, frees capital for 5G and edge expansion. Consolidation is likely as hyperscalers acquire niche partners and talent shortages squeeze smaller vendors, yet sovereign capital and regulatory nuance will preserve moderate fragmentation.

Middle East Digital Transformation Industry Leaders

Cisco Systems Inc.

IBM Corporation

Microsoft Corporation

Alareeb ICT

Techcarrot FZ LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Microsoft confirmed that its Saudi Azure region will enter general availability in Q4 2026, enabling regulated customers to meet residency mandates while accessing the full Azure portfolio.

- December 2025: The UAE unveiled Jais 2, a 70-billion-parameter Arabic model developed by G42 Holding and local institutes, surpassing global peers on Arabic benchmarks.

- May 2025: The UAE released Falcon, an Arabic large language model that outperformed models ten times larger on regional tasks.

Middle East Digital Transformation Market Report Scope

Digital transformation is the process of incorporating digital technologies such as artificial intelligence and machine learning, extended reality (VR and AR) for industrial applications, IoT, industrial robotics, blockchain, digital twin, 3D printing/ additive manufacturing, industrial cyber security, wireless connectivity, edge computing, smart mobility, and others across various end-user industries.

The Middle East Digital Transformation Market Report is Segmented by Deployment Mode (On-Premises, Cloud, Hybrid and Edge), Technology Type (Artificial Intelligence and Machine Learning, Extended Reality, Internet of Things, Industrial Robotics, Blockchain, Digital Twin, Additive Manufacturing, Cybersecurity, Cloud and Edge Computing, Other Technology Types), End-User Industry (Manufacturing, Oil and Gas Utilities, Retail and E-Commerce, Transportation and Logistics, Healthcare, Banking Financial Services and Insurance, Telecom and IT, Government and Public Sector, Other End-User Industries), Enterprise Size (Large Enterprises, Small and Medium Enterprises), and Geography (Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Rest of Middle East Countries). The Market Forecasts are Provided in Terms of Value in USD.

| On-Premises |

| Cloud |

| Hybrid and Edge |

| Artificial Intelligence and Machine Learning |

| Extended Reality (VR and AR) |

| Internet of Things (IoT) |

| Industrial Robotics |

| Blockchain |

| Digital Twin |

| Additive Manufacturing |

| Cybersecurity |

| Cloud and Edge Computing |

| Other Technology Types |

| Manufacturing |

| Oil and Gas Utilities |

| Retail and E-Commerce |

| Transportation and Logistics |

| Healthcare |

| Banking, Financial Services, and Insurance (BFSI) |

| Telecom and IT |

| Government and Public Sector |

| Other End-User Industries |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Rest of Middle East |

| By Deployment Mode | On-Premises |

| Cloud | |

| Hybrid and Edge | |

| By Technology Type | Artificial Intelligence and Machine Learning |

| Extended Reality (VR and AR) | |

| Internet of Things (IoT) | |

| Industrial Robotics | |

| Blockchain | |

| Digital Twin | |

| Additive Manufacturing | |

| Cybersecurity | |

| Cloud and Edge Computing | |

| Other Technology Types | |

| By End-User Industry | Manufacturing |

| Oil and Gas Utilities | |

| Retail and E-Commerce | |

| Transportation and Logistics | |

| Healthcare | |

| Banking, Financial Services, and Insurance (BFSI) | |

| Telecom and IT | |

| Government and Public Sector | |

| Other End-User Industries | |

| By Enterprise Size | Large Enterprises |

| Small and Medium Enterprises (SMEs) | |

| By Region | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Rest of Middle East |

Key Questions Answered in the Report

What is the projected value of the Middle East digital transformation market by 2031?

The market is forecast to reach USD 146.09 billion by 2031.

Which deployment mode currently holds the largest share in Middle East digital transformation?

Cloud deployment led with 53.04% of regional spending in 2025.

Which industry vertical is expected to grow fastest through 2031?

Healthcare is projected to advance at a 17.31% CAGR, driven by telemedicine and electronic health records.

Why are Saudi Arabia and the UAE considered lead markets?

Both countries commit substantial sovereign wealth to AI infrastructure, enforce data-residency laws and host multiple hyperscale cloud regions.

What is the main challenge to scaling AI projects in the region?

A chronic shortage of senior digital talent and AI specialists delays project delivery and inflates costs.

How will small and medium enterprises participate in regional digital transformation?

Subsidized cloud programs and low-code SaaS platforms lower entry barriers, fueling a 16.97% CAGR for SME spending through 2031.

Page last updated on: