United Arab Emirates Color Cosmetics Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

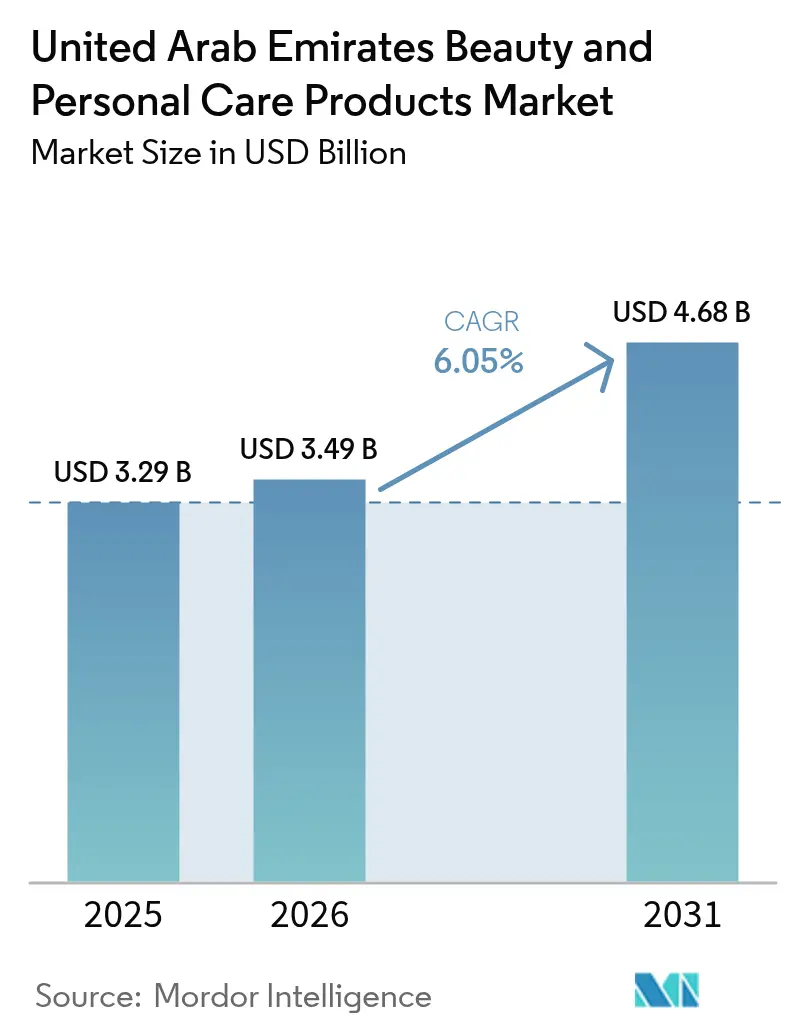

| Base Year Market Size (2025) | USD 428.5 Million |

| Market Size (2026) | USD 445.32 Million |

| Market Size (2031) | USD 525.38 Million |

| Growth Rate (2026 - 2031) | 4.84% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Color Cosmetics Market Analysis by Mordor Intelligence

The United Arab Emirates cosmetics market size was valued at USD 428.50 billion in 2025 and is estimated to grow from USD 445.32 billion in 2026 to reach USD 525.38 billion by 2031, at a CAGR of 4.84% during the forecast period 2026-2031. The United Arab Emirates cosmetics market continues to benefit from the country’s role as a major travel and shopping hub, which supports cosmetics demand beyond resident spending alone. Dubai Duty Free recorded annual sales of AED 8.68 billion in 2025, equal to USD 2.38 billion, and cosmetics remained among the top-performing categories, showing how travel flows continue to support beauty purchases in the country[1]Source: Dubai Government Media Office, “Dubai Duty Free Celebrates Record-Breaking 2025 With Milestone Annual Sales of Dhs8.680 Billion,” Dubai Government Media Office, mediaoffice.ae. The United Arab Emirates cosmetics market is also supported by a large expatriate base, strong digital retail access, and rising interest in halal, clean-label, and long-wear formulations that suit local climate conditions. Buyers are moving across both accessible and premium price points, which keeps volume demand broad while also creating room for trade-up purchases in prestige channels. Competition remains moderately fragmented, with global beauty groups and regional names competing across specialty retail, duty free, and online platforms, while counterfeit products and import dependence remain clear operating risks for the market.

Key Report Takeaways

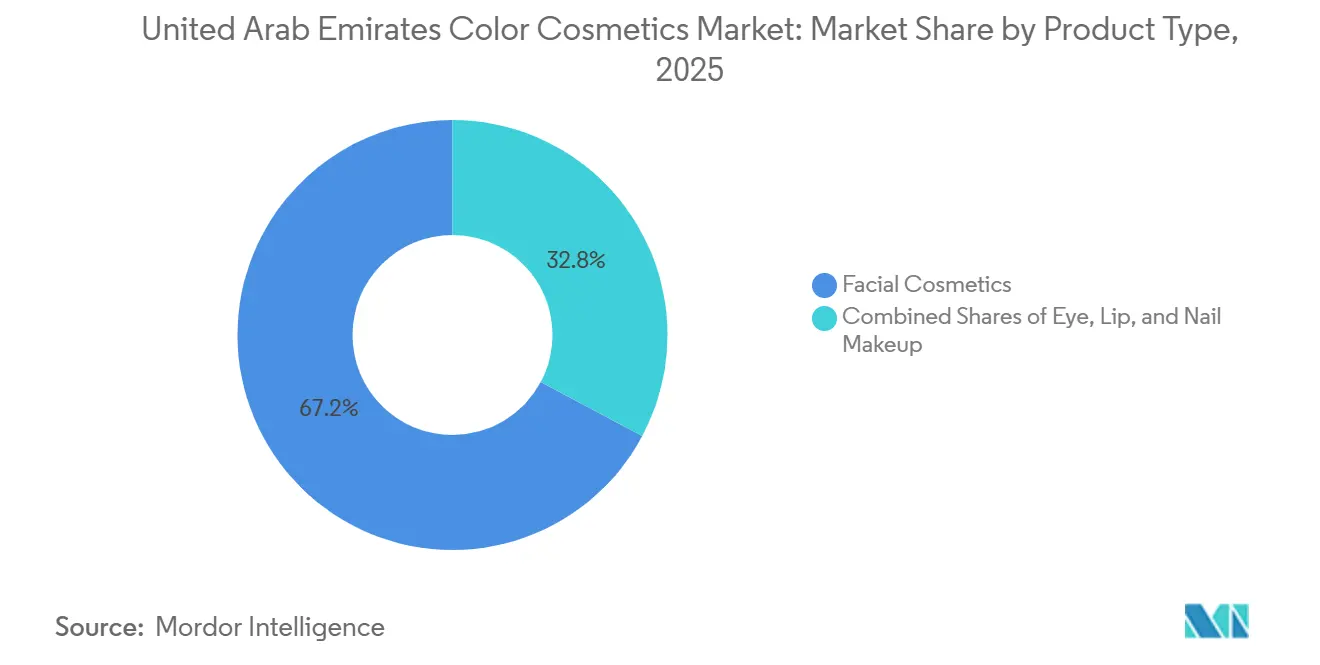

- By product type, facial cosmetics held a 67.21% share in 2025, while eye cosmetics are forecast to expand at a 6.78% CAGR through 2031.

- By category, mass products accounted for an 85.38% share in 2025, while premium products recorded the highest projected CAGR at 6.25% through 2031.

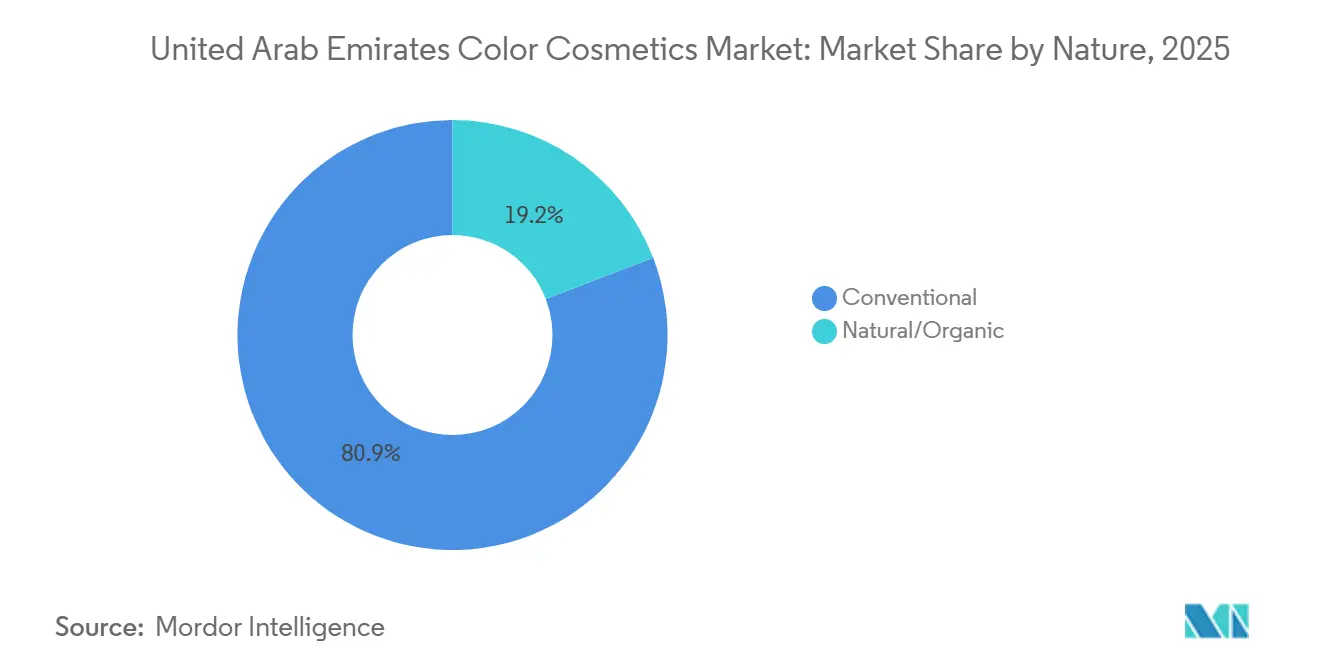

- By ingredient type, conventional and synthetic formulations held a 75.88% share in 2025, while organic and natural formulations are projected to grow at a 6.11% CAGR through 2031.

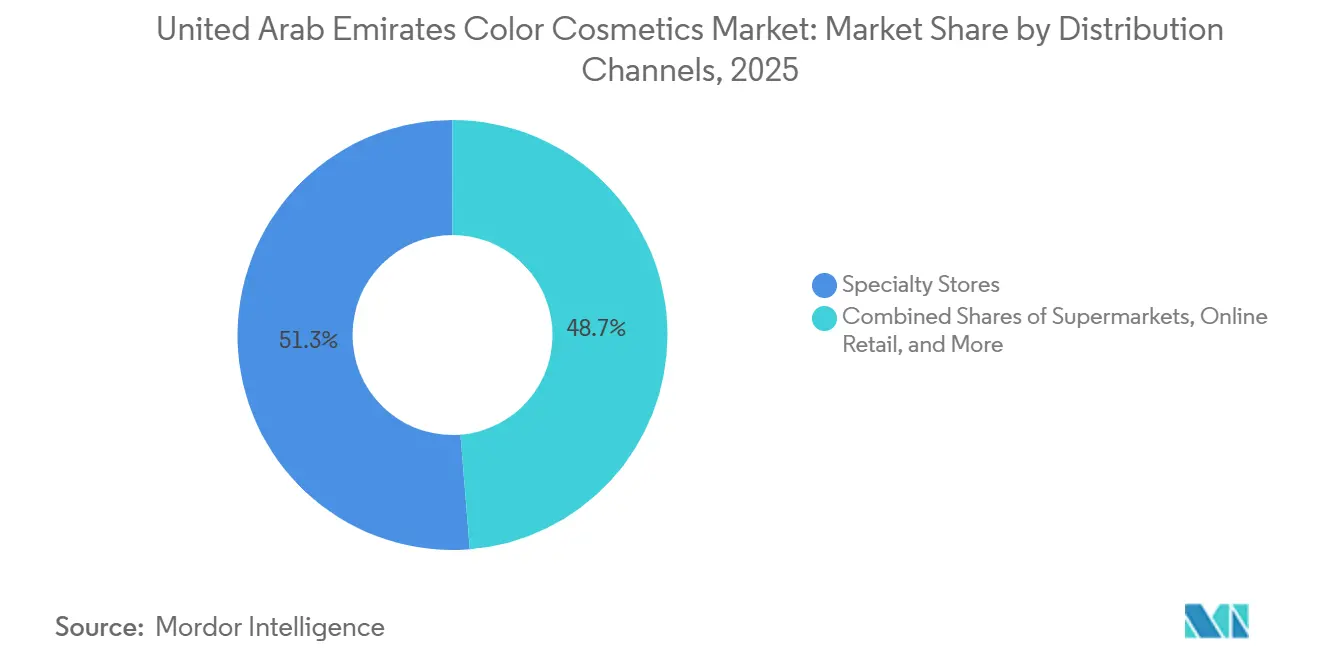

- By distribution channel, specialty stores captured a 51.28% share in 2025, while online retail is expected to advance at a 5.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Color Cosmetics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong Demand from Inbound Tourists Driving Cosmetics Sales | +1.10% | Dubai airport corridor, spill-over to Abu Dhabi and RAK free zones | Short term (≤ 2 years) |

| Rising Demand for Premium and Luxury Cosmetic Brands | +0.90% | Dubai luxury retail corridor, Abu Dhabi high-net-worth nationals | Medium term (2-4 years) |

| Growing Preference for Halal-Certified Cosmetic Products | +0.80% | Global, with primary gains in UAE and wider GCC, early uptake in Northern Emirates | Long term (≥ 4 years) |

| Increasing Consumer Demand for Natural, Organic, and Clean-Label Cosmetics | +0.70% | UAE-wide, strongest in Dubai premium beauty specialty stores | Medium term (2-4 years) |

| Strong Influence of Social Media, Beauty Influencers, and Digital Marketing | +0.60% | UAE-wide, digital demand concentrates in Dubai and Abu Dhabi | Short term (≤ 2 years) |

| Growing Demand for Long-Lasting, Climate-Resistant Cosmetic Formulations | +0.40% | UAE-wide, amplified across Northern Emirates and Abu Dhabi interior zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strong Demand from Inbound Tourists Driving Cosmetics Sales

The United Arab Emirates cosmetics market has a demand layer that is tied directly to tourism, and that makes the country different from many domestic-only beauty markets. Dubai remained one of the world’s most visited cities in 2025, and this kept airport retail, destination malls, and prestige beauty counters highly active through the year. Travel shoppers use the UAE as a premium sourcing point for global brands, gift purchases, and limited retail formats that are not always available in their home countries. Dubai Duty Free reported record first-half and full-year sales in 2025, with perfumes and cosmetics among the leading categories, confirming that beauty demand is closely linked to passenger traffic and airport dwell time. This gives the United Arab Emirates cosmetics market a resilience advantage when local spending is mixed, although brands that depend too heavily on travel corridors still face risk if aviation flows weaken for external reasons.

Rising Demand for Premium and Luxury Cosmetic Brands

The United Arab Emirates cosmetics market continues to attract premium and luxury beauty investment because the country combines high-spending residents, affluent visitors, and strong retail visibility. Prestige demand is no longer limited to traditional department store counters, as brands are now investing in dedicated boutiques, airport counters, and service-led formats that turn beauty buying into an experience. Charlotte Tilbury opened two counters at Dubai Duty Free in November 2025, using fast consultations and premium traffic exposure to reach both travelers and residents in transit. Dior also expanded its beauty presence in Dubai during 2025 through a spa-led format at The Lana hotel, which shows that premium beauty is extending into hospitality-linked environments as well. This pattern supports higher-value sales in the United Arab Emirates cosmetics market and gives established prestige players a stronger platform than smaller entrants that rely only on shelf presence.

Growing Preference for Halal-Certified Cosmetic Products

Halal-certified cosmetics are becoming increasingly important in the United Arab Emirates cosmetics market as compliance and consumer trust converge. The UAE Ministry of Industry and Advanced Technology continues to oversee the national halal program, and qualifying products are subject to certification requirements under the existing framework[2]Source: UAE Ministry of Industry and Advanced Technology, “Halal Programme,” UAE Ministry of Industry and Advanced Technology, moiat.gov.ae. This has pushed brands to review solvents, pigments, and ingredient sourcing more closely before products reach shelves. Reformulation for halal suitability also aligns with the broader demand for gentler, more transparent products, meaning halal and clean-label positioning often reinforce each other rather than operating as separate trends. Brands that build certification capability early are likely to hold a stronger position in the United Arab Emirates cosmetics market because late entrants will face a harder path on compliance, registration, and reputation at the same time.

Increasing Consumer Demand for Natural, Organic, and Clean-Label Cosmetics

The United Arab Emirates cosmetics market is also seeing stronger demand for natural, organic, and clean-label products, especially in premium and digitally visible retail spaces. Buyers are paying closer attention to ingredient lists, packaging claims, and brand credibility, and that is pushing more beauty companies toward simpler and more transparent formulation stories. L’Oréal Middle East signed the UAE Climate-Responsible Companies Pledge in June 2026 and expanded work on refillable packaging formats, with reported material reductions of up to 67% in plastic and 61% in cardboard in selected formats. The same market is also giving greater visibility to products that use traditional regional ingredients in a modern format, which helps local relevance without moving away from premium positioning. This gives the United Arab Emirates cosmetics market another layer of growth, as sustainability, ingredient transparency, and cultural fit now shape purchase decisions alongside color payoff and wear performance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Dependence on Imported Cosmetic Products and Ingredients | -0.50% | UAE-wide, most acute for SME importers reliant on single-origin supply chains | Medium term (2-4 years) |

| Counterfeit and Grey-Market Cosmetic Products Affecting Brand Trust | -0.40% | Dubai and Northern Emirates, secondary spill into online channels | Short term (≤ 2 years) |

| High Retail Prices of Premium and Luxury Cosmetics | -0.30% | UAE-wide, disproportionate impact on lower-income expatriate segments | Medium term (2-4 years) |

| Rising Logistics, Warehousing, and Distribution Costs | -0.20% | UAE-wide, amplified in last-mile delivery for e-commerce orders | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Dependence on Imported Cosmetic Products and Ingredients

The United Arab Emirates cosmetics market remains exposed to imported inputs because the country has only a limited domestic base for cosmetic ingredients and large-scale formulation materials. That means freight costs, shipment timing, and registration requirements can move quickly into retail pricing and margin pressure. Products entering the market must comply with ingredient disclosure and labeling rules, and this adds time and cost for importers that need approvals across multiple stock keeping units. Free-zone activity and local blending help reduce part of that burden, but they do not remove the basic dependence on global supply routes for raw materials and finished beauty products. This remains a real restraint for the United Arab Emirates cosmetics market because any disruption in sourcing or freight can affect availability, launch timing, and price stability across both premium and mass channels.

Counterfeit and Grey-Market Cosmetic Products Affecting Brand Trust

Counterfeit and grey-market goods remain a visible challenge for the United Arab Emirates cosmetics market because beauty purchases depend heavily on product trust and ingredient safety. Dubai authorities reported the seizure of 37,110 non-compliant cosmetic products during a 2025 enforcement sweep, showing that non-authentic goods are still reaching the market in meaningful volume. In another major action, Ras Al Khaimah police seized 650,468 counterfeit items worth AED 23.00 million, equal to USD 6.26 million, in August 2024, including fake cosmetics from well-known brands[3]Source: Ras Al Khaimah Police, “Ras Al Khaimah Police Seize 650,000 Counterfeit Items Worth Dh23 Million in Raid,” The National, thenationalnews.com. Counterfeit products do more than divert sales, because they can damage confidence in the wider category when consumers encounter poor quality or unsafe ingredients. This problem matters even more in the United Arab Emirates cosmetics market because halal, clean-label, and premium claims carry more value only when buyers trust the product’s origin and integrity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Eye Cosmetics Gaining on a Broad Facial Foundation

Facial cosmetics held 67.21% of the United Arab Emirates cosmetics market share in 2025, which confirms that base makeup remains the core of category demand across age groups and shopping formats. Foundations, concealers, blush products, and contouring items remain central because they match both daily use and occasion-driven beauty routines in the country. The need for long-wear performance in high heat also keeps facial products closely tied to function rather than only appearance. Shade matching remains a major selling point, and brands are widening tone ranges to suit Middle Eastern undertones and mixed expatriate demographics. This part of the United Arab Emirates cosmetics market also benefits from the role of Dubai as a testing ground for broader regional product launches.

Lip and nail makeup products add breadth to the category, but eye cosmetics stands out as the fastest-growing product type. The United Arab Emirates cosmetics market size for eye cosmetics is projected to expand at a 6.78% CAGR through 2031, which places it well above the overall market growth rate. Demand is being shaped by a local beauty context where eye definition carries strong visual importance across both modest and non-modest styling choices. Mascara, eyeliner, brow products, and long-wear eyeshadow are therefore gaining share through routine use as well as social and event-led purchases. Product development is also adapting to humidity, heat, and long wear hours, which supports sealed formats, transfer-resistant textures, and stronger repeat buying in the United Arab Emirates cosmetics market.

By Category: Premium Ascent Within a Mass-Anchored Market

Mass products accounted for 85.38% of the market in 2025, which shows that the broad base of demand still sits in affordable and frequently purchased items. This reflects the large expatriate mid-market consumer base and the steady need for everyday cosmetics across a wide income range. It also shows that scale in the United Arab Emirates cosmetics market still depends on accessible pricing, broad distribution, and repeat-use categories such as foundation, lip color, and nail products. Brands that sit in the mass-to-masstige band have done well because they combine strong brand identity with price points that remain reachable for regular use. KIKO Milano’s network of more than 26 stores across Dubai, Abu Dhabi, and Sharjah shows how widely this approach can travel inside the country.

Premium products are growing faster than the category average even though they start from a smaller base. The premium segment is forecast to grow at a 6.25% CAGR through 2031, giving it the fastest pace within this segmentation type. This growth is being supported by high-spending visitors, long-stay residents with stronger purchasing power, and a retail environment that gives prestige brands strong visibility. Dubai remained a clear target for investment in 2025 and 2026, with prestige names using offices, counters, partnerships, and selective store environments to deepen local relevance. The United Arab Emirates cosmetics market therefore combines a mass-led volume base with a premium layer that is expanding faster and pulling more brand investment into the country.

By Ingredient Type: Formulation Shift Accelerating Beneath a Synthetic Base

Conventional and synthetic formulations held a 75.88% share in 2025, which shows that proven performance still matters most when consumers choose color cosmetics. These formulations remain strong because they offer dependable color payoff, wear time, and heat resistance, all of which are highly relevant in the local climate. The United Arab Emirates cosmetics market has practical performance demands that can slow any rapid shift away from established synthetic systems. Products that fail on wear stability or finish consistency are unlikely to hold repeat demand even if they carry cleaner positioning. That helps explain why synthetic formulations still form the larger base of the category in the United Arab Emirates cosmetics market.

Organic and natural formulations are still the faster-moving part of this segment despite that large synthetic base. The United Arab Emirates cosmetics market size for organic and natural formulations is projected to grow at a 6.11% CAGR through 2031. This growth is linked to stronger consumer attention to ingredient transparency, plant-based inputs, halal suitability, and reduced use of alcohol or animal-derived components. Regional buyers are also showing greater interest in beauty products that combine performance with clear product stories around sourcing and safety. As more brands improve formula performance in this area, the United Arab Emirates cosmetics market is likely to see faster movement from stated preference to actual purchase behavior.

By Distribution Channel: Digital Commerce Reshaping a Specialty-Anchor Market

Specialty stores led distribution with a 51.28% share in 2025, which shows that beauty shoppers still value in-person consultation, product trial, and curated brand environments. The United Arab Emirates cosmetics market has a strong specialty base because malls, travel retail, and branded counters remain central to discovery and conversion. Beauty advisors, live demonstrations, and premium merchandising continue to matter, especially for facial products where shade matching and finish assessment are harder to finalize without physical trial. Major retail destinations such as Dubai Mall and Mall of the Emirates continue to act as both sales channels and brand theaters for local and international launches. This keeps specialty retail firmly anchored in the United Arab Emirates cosmetics market even as digital demand rises.

Online retail is growing faster than all other channel types. The United Arab Emirates cosmetics market size for online retail is forecast to expand at a 5.89% CAGR through 2031, supported by strong e-commerce infrastructure and heavy digital engagement. Social commerce, mobile-led browsing, and AI-enabled shade tools are reducing the main barriers that once limited online sales of color cosmetics. Ahead of its Gulf launch, e.l.f. Beauty said the GCC had become its most organically requested unserved market, and UAE social mentions helped show how digital pull can turn quickly into channel expansion. This gives the United Arab Emirates cosmetics market a channel pattern where online growth is not replacing physical retail, but instead reshaping the way interest turns into purchase.

Geography Analysis

Dubai remains the main commercial center of the United Arab Emirates cosmetics market because it combines airport traffic, destination malls, affluent residents, and heavy tourist spending in one place. The emirate acts as both a sales engine and a market-entry platform for international beauty brands that want visibility across the wider Gulf region. In November 2025, Charlotte Tilbury opened two counters at Dubai Duty Free, adding a prestige beauty presence in one of the world’s highest-traffic travel retail settings. In January 2026, Dubai Duty Free reported AED 858.21 million in total monthly sales, equal to USD 233.57 million, with cosmetics sales of AED 40.00 million, equal to USD 10.89 million, up 7.67% year over year. These numbers show that Dubai continues to give the United Arab Emirates cosmetics market a level of traffic exposure that few regional markets can match.

The city also works as a launch venue where brands test counters, pop-ups, and creator-led activations before wider GCC expansion. Charlotte Tilbury’s Pillow Talk in Bloom activation at Dubai Mall in April 2026 and L’Oréal Middle East’s regional creator program rollout in June 2026 both support that role. Success in Dubai often helps brands build credibility with retail partners across the rest of the Gulf, which gives the local market influence beyond its national sales value. This makes Dubai the most visible geography inside the United Arab Emirates cosmetics market and the place where competition is easiest to observe in real time. It also means that shifts in tourism, retail leasing, or premium footfall can affect brand performance quickly.

Abu Dhabi holds a different but still important place in the United Arab Emirates cosmetics market because its buyer mix includes more UAE nationals and GCC visitors, which raises the importance of culturally aligned products and premium service quality. Demand in Abu Dhabi is therefore well suited to halal-certified offerings, premium formulations, and deeper shade assortments that match regional undertones. Sharjah and the Northern Emirates are smaller in scale, but they matter as expansion zones for modern retail and digital fulfillment while also carrying higher exposure to counterfeit trade in some areas. Sharjah also adds a technology and logistics angle through new digital commerce activity linked to beauty distribution, which gives the United Arab Emirates cosmetics market another growth path beyond Dubai’s store-led dominance. This broader geographic pattern shows a national market where Dubai leads visibility, Abu Dhabi supports premium depth, and the Northern Emirates widen reach while bringing a different risk profile.

Competitive Landscape

The United Arab Emirates cosmetics market is moderately fragmented, and no single beauty company is described in the source material as holding a dominant position across all channels and product types. Global groups such as L’Oréal, Estée Lauder Companies, Coty, LVMH, and Shiseido remain strong in prestige and upper mid-tier segments because they have brand recognition, established partners, and broad product portfolios. Regional names such as Huda Beauty and Mikyajy hold an advantage in local relevance because they understand shade needs, product preferences, and Gulf-facing beauty communication more closely. The competitive mix is therefore broad, with multinational scale and regional cultural fit both carrying weight inside the United Arab Emirates cosmetics market. This structure keeps pricing, shelf space, and launch timing highly competitive across specialty stores, duty-free counters, and online channels.

Several strategic moves in 2025 and 2026 show how brands are trying to strengthen their position. L’Oréal completed its acquisition of Kering Beauté in March 2026, which deepened its prestige portfolio and may influence how luxury beauty is distributed and marketed in the country going forward. Huda Kattan repurchased TSG Consumer Partners’ minority stake in 2025, returning Huda Beauty to full founder ownership while the brand also moved into fragrance in 2026. e.l.f. Beauty entered the GCC through Sephora in November 2025, which gave a value-led but branded player broad regional visibility across 70 stores and e-commerce from the start. These examples show that the United Arab Emirates cosmetics market attracts both portfolio expansion by established leaders and entry moves from brands that see unmet demand in accessible price tiers.

Competition is also shifting because digital influence is now part of commercial strength, not only a marketing support tool. L’Oréal Middle East’s creator-focused loyalty platform launch in 2026 shows how large companies are trying to formalize influencer ecosystems instead of depending only on one-off campaigns. At the same time, sustainability visibility is becoming another marker of competitive readiness, especially for large groups that can invest in refill systems, packaging changes, and disclosure standards. Smaller and mid-tier brands can still win space in the United Arab Emirates cosmetics market, but they need sharper positioning because they usually do not match global players on compliance resources, creator networks, or premium retail access. The result is a market that remains open to new brands, yet increasingly rewards those that combine local fit, digital agility, and operational discipline.

United Arab Emirates Color Cosmetics Industry Leaders

L’Oréal SA

Procter & Gamble Company

Unilever PLC

Beiersdorf AG

Huda Beauty

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: SK. Cosmetics expanded into the United Arab Emirates with the official launch of its operations and a dedicated UAE e-commerce platform. The company introduced a portfolio of Korean beauty, skincare, haircare, cosmetics, and wellness brands, including Cataleya, Pestlo, Hair It, Blend Smart, and secured the exclusive Middle East distribution rights for Cathy Doll.

- November 2025: e.l.f. Beauty enters GCC via Sephora across 70 stores. e.l.f. Beauty made its first-ever GCC market entry through an exclusive Sephora partnership, bringing its vegan, clean-beauty lineup to all 70 Sephora GCC stores and regional e-commerce. The GCC was the brand's most-requested unserved market, with UAE social media mentions up 38% organically ahead of launch.

- November 2025: Charlotte Tilbury debuts at Dubai Duty Free. Charlotte Tilbury opened two prestige counters in Concourses C and D at Dubai International Airport, offering skincare, makeup, and fragrance to one of the world's highest-volume travel retail audiences. The launch includes rapid makeup consultations tailored to airport dwell times.

United Arab Emirates Color Cosmetics Market Report Scope

Color cosmetics are pigments that add color to make-up, skincare, hair care, personal hygiene, scents, and other personal care products. These cosmetics help give off a fresh and attractive look while improving the appearance, defining facial features, and covering blemishes and marks.

The United Arab Emirates color cosmetics market is segmented by Type into facial makeup, eye makeup, nail makeup, lip makeup, and hair color products. The market is segmented by distribution channel into supermarkets/hypermarkets, specialty stores, online retail stores, and other distribution channels.

The report offers market size and forecasts in value (USD million) for the above segments.

| Facial Cosmetics |

| Eye Cosmetics |

| Lip and Nail Make-up Products |

| Premium Products |

| Mass Products |

| Natural and Organic |

| Conventional/Synthetic |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Online Retail Stores |

| Other Channels |

| Product Type | Facial Cosmetics |

| Eye Cosmetics | |

| Lip and Nail Make-up Products | |

| By Category | Premium Products |

| Mass Products | |

| By Ingredient Type | Natural and Organic |

| Conventional/Synthetic | |

| By Distribution Channel | Specialty Stores |

| Supermarkets/Hypermarkets | |

| Online Retail Stores | |

| Other Channels |

Key Questions Answered in the Report

What is the 2026 to 2031 growth outlook for cosmetics in the United Arab Emirates?

The market is projected to grow at a 4.84% CAGR from 2026 to 2031, reaching USD 525.38 billion by 2031 from USD 445.32 billion in 2026.

Which product segment leads sales in the country?

Facial cosmetics led with a 67.21% share in 2025, supported by strong demand for foundation, concealer, blush, and contour products.

Which product type is growing the fastest?

Eye cosmetics is the fastest-growing product type, with a projected 6.78% CAGR through 2031.

Why does Dubai matter so much for beauty sales?

Dubai combines tourism, airport retail, luxury malls, and premium brand visibility, which makes it the main launch and demand center for the country.

Page last updated on: