Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

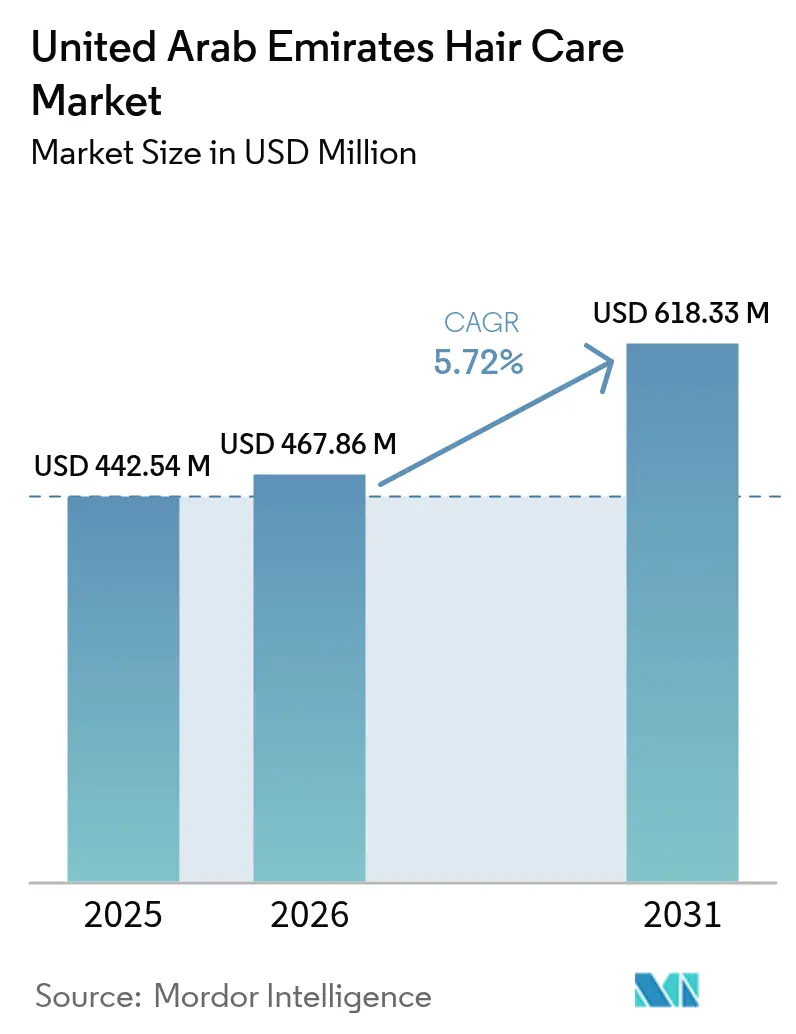

| Base Year Market Size (2025) | USD 442.54 Million |

| Market Size (2026) | USD 467.86 Million |

| Market Size (2031) | USD 618.33 Million |

| Growth Rate (2026 - 2031) | 5.72% CAGR |

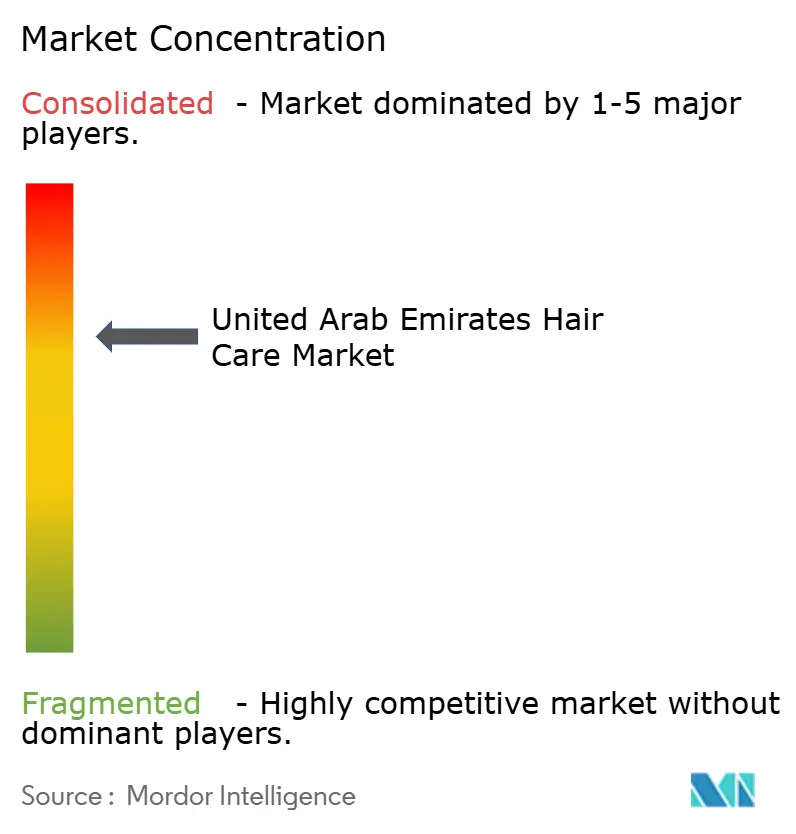

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Hair Care Market Analysis by Mordor Intelligence

The United Arab Emirates hair care market size was valued at USD 442.54 million in 2025 and estimated to grow from USD 467.86 million in 2026 to reach USD 618.33 million by 2031, at a CAGR of 5.72% during the forecast period (2026-2031). The United Arab Emirates stands out as the Middle East's premier beauty hub, bolstered by a youthful populace that values personal grooming and government policies championing retail growth. Climate-induced hair damage, a surge in male grooming, and a booming e-commerce landscape are spurring the development of new products. Furthermore, rising disposable incomes and a wave of expatriates with varied hair care needs are fueling both innovation and demand. Global and regional brands, through assertive marketing, are swaying consumer preferences and propelling category growth. Influencers and beauty bloggers, especially on social media, are pivotal in molding grooming trends and enhancing brand visibility, particularly among the youth. The growing number of upscale salons and specialized beauty outlets is further amplifying the demand for premium and professional-grade hair care products. In 2024, while shampoos dominate the market, hair styling products are witnessing the swiftest growth. Although synthetic ingredients remain prevalent, there's a notable shift towards natural and organic products as health consciousness rises. Supermarkets and hypermarkets lead in distribution, yet online retail is rapidly gaining ground, owing to the UAE's flourishing e-commerce scene. The competitive arena is moderately concentrated, with established brands firmly entrenched, yet there's ample room for newcomers.

Key Report Takeaways

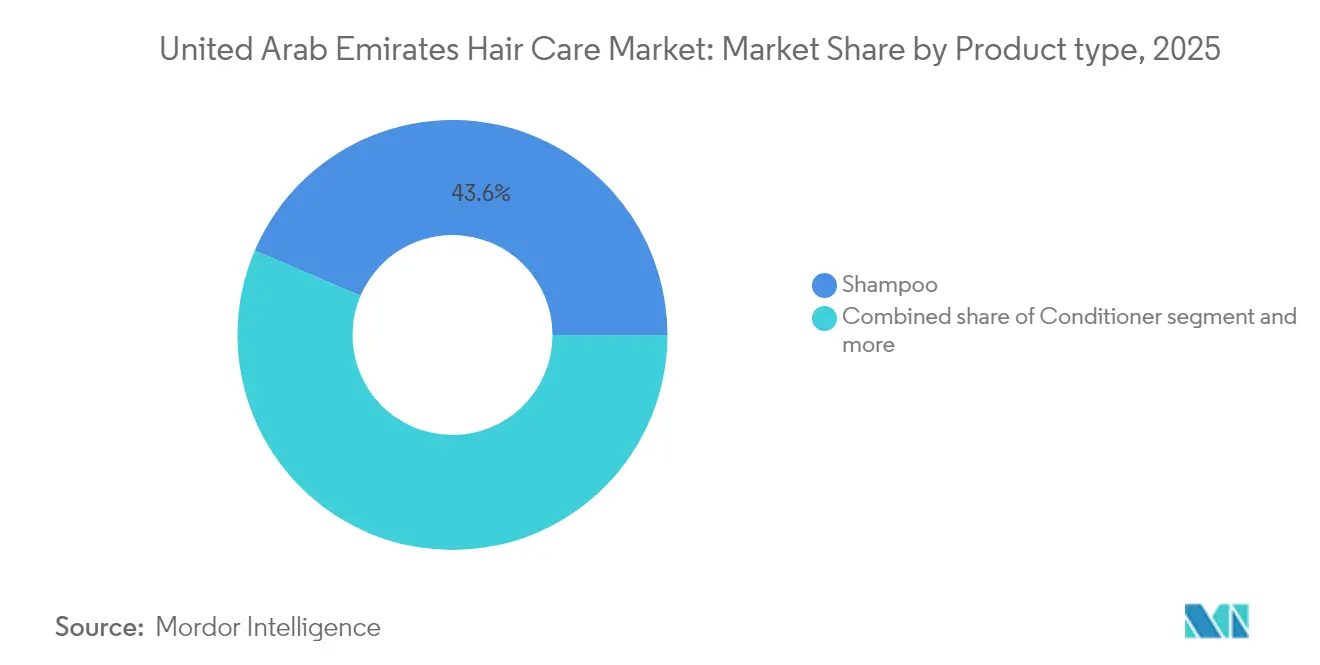

- By product type, shampoo led with 43.58% of the United Arab Emirates hair care market share in 2025; hair styling products are advancing at a 6.08% CAGR through 2031.

- By category, mass products accounted for 69.85% of the United Arab Emirates hair care market size in 2025; premium products are projected to expand at a 6.6% CAGR to 2031.

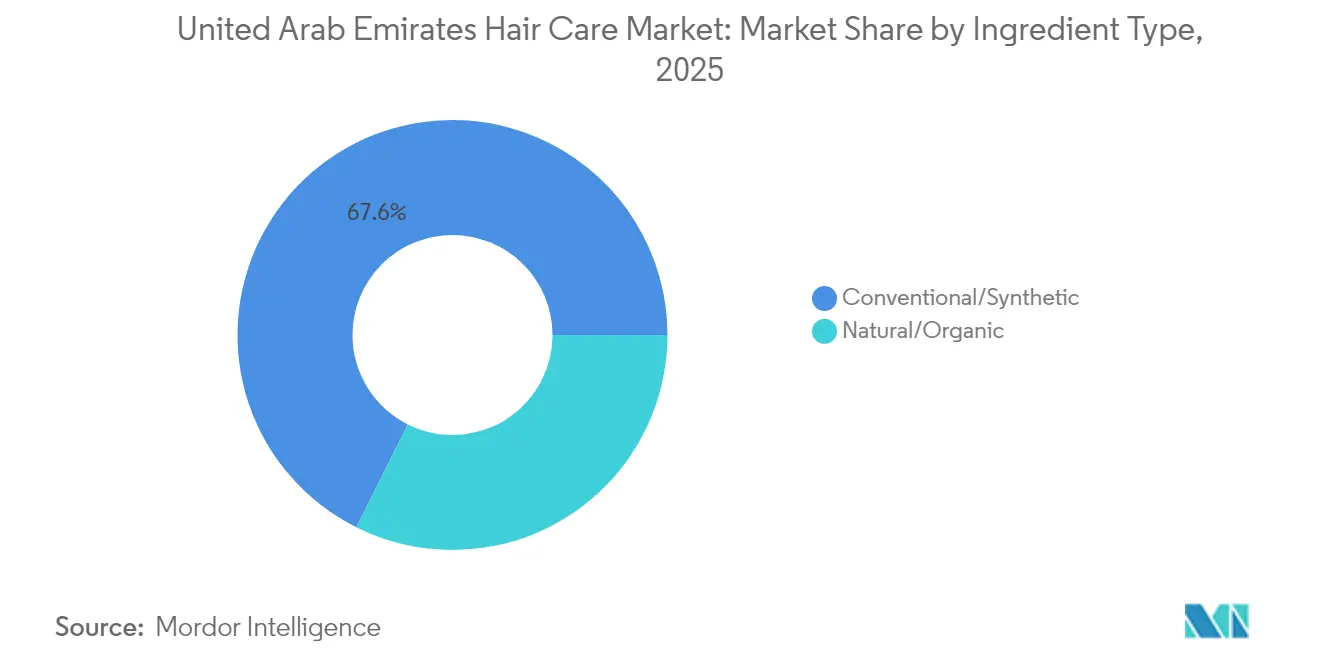

- By ingredient type, conventional/synthetic formulations retained 67.62% share of the United Arab Emirates hair care market size in 2025; natural/organic products are outpacing at a 6.89% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets held 78.73% revenue share in 2025, while online retail is growing at 7.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Hair Care Market Trends and Insights

Drivers Impact Table*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High incidence of hair loss due to desalinated water and heat | +1.2% | United Arab Emirates nationwide, particularly Dubai and Abu Dhabi | Medium term (2-4 years) |

| Demand for multi-functional and damage control products | +0.9% | United Arab Emirates nationwide with spillover to GCC | Short term (≤ 2 years) |

| Technological innovations in product formulations | +0.8% | United Arab Emirates early adoption | Long term (≥ 4 years) |

| Growing male grooming consciousness | +1.1% | United Arab Emirates urban centers, expanding to suburban areas | Medium term (2-4 years) |

| Influence of social media and beauty influencers | +0.7% | United Arab Emirates nationwide, strongest in Dubai | Short term (≤ 2 years) |

| Increasing focus on scalp health | +0.6% | United Arab Emirates premium segment adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High incidence of hair loss due to desalinated water and heat

In the United Arab Emirates, many people believe that desalinated tap water, which contains high mineral content, is a major cause of hair loss. This water is thought to lead to dryness and breakage. However, dermatologists highlight that the primary reasons for hair loss are nutritional deficiencies, such as low levels of iron, vitamin D, and zinc, along with hormonal imbalances. According to Dr Batra's Homeopathy, as of June 2025, studies show that around 66% of men in the United Arab Emirates experience hair loss, and 67% of residents overall report similar issues, often blaming the water quality. In cities like Dubai, factors such as extreme heat, high humidity, a stressful lifestyle, and the use of desalinated water worsen the problem. According to EPI YALE EDU, the United Arab Emirates's rankings for unsafe sanitation and drinking water in 2024 were 37 and 61, respectively [1]Source: Yale Center for Environmental Law & Policy, “Unsafe Drinking Water,” Environmental Performance Index, epi.yale.edu. Consumer perceptions of water quality are shaping their purchasing decisions, notably boosting the demand for products such as anti-hair-loss shampoos. Brands like Himalaya and OGX have seized this opportunity, offering detox and anti-hair fall shampoos specifically designed for areas with mineral-heavy water. This strategic move not only caters to immediate consumer needs but also aligns these brands with the larger narratives of wellness and environmental consciousness.

Demand for multi-functional and damage control products

Professionals in the UAE, who often have busy schedules, are increasingly looking for hair care products that can serve multiple purposes and help repair damage while saving time. This demand has led to the rise of multi-functional products inspired by the "skinification" trend, where hair care adopts ingredients and techniques from skincare. These products combine treatment and protection in one formula, such as serums with niacinamide, conditioners with hyaluronic acid, and sprays that include UV filters along with nourishing oils like argan. For example, in February 2024, L’Oréal Paris launched its Elvive Hydra Hyaluronic Shampoo and Conditioner. These products are designed to deeply hydrate hair using hyaluronic acid, mimicking the moisturizing benefits commonly found in skincare. The market is increasingly favoring such innovations that simplify hair care routines by combining cleansing, repairing, and protecting functions into a single product. This approach caters to the fast-paced lifestyles of consumers, offering salon-quality results with less effort and reducing the need for multiple products, ultimately minimizing bathroom clutter.

Technological innovations in product formulations

In the UAE, advanced technology is revolutionizing the hair care market, with consumers increasingly gravitating towards high-performance, science-backed solutions. Treatments infused with peptides, shampoos that neutralize odors, and scalp care products drawing inspiration from stem cell research are witnessing a surge in popularity. For instance, Kerastase's Genesis Anti Hair Fall Serum and Grow Gorgeous's Hair Density Serum leverage peptides to fortify hair strands and enhance density. Meanwhile, L’Oréal's Elvive Bond Repair Shampoo, making its debut in 2024, utilizes a citric acid complex to mend broken hair bonds and restore strength, echoing trends seen in professional treatments. These premium offerings strike a chord with the affluent consumers of the UAE, who are keen to invest in targeted, results-oriented care. This inclination dovetails with the nation's strong purchasing power, projected at a GDP per capita of USD 49,500 in 2025 by the International Monetary Fund [2] Source: International Monetary Fund, “United Arab Emirates: Country Profile,” IMF DataMapper, imf.org. The UAE stands out as a pivotal launchpad for avant-garde hair care innovations, frequently acting as a testing ground prior to their global introduction. Retail giants like Sephora UAE and Boots are championing these advanced product lines, facilitating their swift acceptance in the market.

Growing male grooming consciousness

In the UAE, heightened awareness of scalp health and premium hair care products is transforming the retail landscape for men's grooming. Responding to this trend, major retailers such as Sephora Middle East and Boots UAE are broadening their men's hair care selections, bringing in global brands for shampoos, conditioners, and styling products. For instance, Head & Shoulders Men Ultra Series, with its cleansing charcoal and zinc formulation, addresses common male concerns like scalp buildup and hair fall, especially in the UAE's hot and humid climate. Likewise, American Crew's Fiber Cream offers a strong hold with a natural finish, appealing to men desiring top-tier styling without the residue. The push for salon-quality results at home is amplified by regional social media influencers and changing grooming norms in sectors like hospitality, aviation, and corporate services, where a polished look signifies professionalism. Products once considered niche, such as volumizing shampoos, age-defying conditioners, and lightweight styling creams, are now mainstream. Moreover, the surge of e-commerce and focused digital marketing has made these products more accessible, prompting men to delve deeper into advanced grooming.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Proliferation of counterfeit products | -0.8% | United Arab Emirates nationwide, particularly free zones | Short term (≤ 2 years) |

| Adoption of traditional at-home hair care solutions | -0.5% | United Arab Emirates with cultural community concentrations | Medium term (2-4 years) |

| Regulatory challenges for imported products | -0.4% | United Arab Emirates import-dependent market | Long term (≥ 4 years) |

| Price sensitivity among mass market consumers | -0.9% | United Arab Emirates nationwide, strongest in price-conscious segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Proliferation of counterfeit products

The increasing presence of counterfeit hair and beauty products is a major challenge for the United Arab Emirates's hair care market. In 2024, authorities confiscated large quantities of fake products, including 650,468 counterfeit cosmetics worth AED 23 million in Ras Al Khaimah and 1 million fake cosmetics and drugs valued at AED 17 million in Dubai. Additionally, Dubai Customs seized 10.8 million counterfeit items across 54 operations during the year. These fake products, which include shampoos, conditioners, serums, and styling sprays, harm consumer trust and reduce revenue for genuine brands. This issue also discourages customers from purchasing premium products due to concerns about authenticity. To combat this, leading manufacturers are introducing advanced packaging solutions like QR codes and tamper-evident seals to help customers verify product authenticity. On the government side, the UAE is using AI and advanced customs technologies to monitor supply chains more effectively. While these measures, including product seizures, act as strong deterrents, raising consumer awareness remains essential to protect the market’s integrity and ensure buyers invest in authentic, high-quality products.

Regulatory challenges for imported products

In the UAE, strict regulations pose significant hurdles for imported hair care products. The Emirates Authority for Standardization and Metrology (ESMA) and Dubai Municipality require all cosmetics, including shampoos, conditioners, and serums, to be registered and pass safety assessments prior to market entry. Imported products frequently encounter delays due to stringent mandates, including detailed ingredient disclosures, halal certification, shelf life testing, and compulsory Arabic labeling. Recent bans on certain chemicals, such as the preservative methylisothiazolinone, have forced international brands to reformulate specifically for the UAE and Gulf markets. These regulatory hurdles not only inflate costs but also postpone product launches, a challenge especially pronounced for smaller or niche brands. In light of these challenges, many companies are forging partnerships with local distributors and channeling investments into region-specific research and development. Furthermore, they're increasingly gravitating towards online sales platforms, which typically promise swifter approval processes than conventional retail avenues.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Styling surge narrows shampoo lead

In 2025, shampoo dominated the United Arab Emirates's hair care market, capturing 43.58% of the total market share. This stronghold is largely attributed to the daily hair-washing routines of consumers, a necessity in the UAE's hot, humid, and dusty climate. Given these conditions, regular cleansing becomes vital for maintaining scalp hygiene, solidifying shampoo's status as a universal staple. The category's appeal is further enhanced by its diverse product range, from anti-hair fall to moisturizing and dandruff-control variants. These offerings address specific concerns, such as hair damage from desalinated water and environmental stressors. Meanwhile, conditioners, often used in tandem with shampoos, maintain a consistent market share as consumers increasingly rely on them to enhance their cleansing routines and hair texture.

While hair styling products currently occupy a smaller segment of the market, they are the fastest-growing category, boasting a projected CAGR of 6.08% from 2025 to 2031. This surge is largely driven by evolving consumer behaviors, particularly among younger audiences and men. These groups, swayed by social media, fashion trends, and professional grooming standards, are gravitating towards styling products. Multi-functional offerings, like pomades that blend hold with conditioning, are witnessing a rise in popularity. Furthermore, there's a growing demand for travel-friendly aerosols and heat-resistant sprays, especially among frequent travelers. Hair colorants are also experiencing steady demand, fueled by both functional needs (like grey coverage) and fashion trends. Together, these factors underscore a market shift towards high-performance, premium products tailored for individual care, leading to elevated average selling prices and sustained revenue growth.

By Category: Premium outpaces but does not overtake mass

In 2025, mass-market hair care products dominated the UAE hair care scene, clinching a 69.85% share in terms of sales volume. Budget-conscious consumers gravitate towards these products, drawn by their affordability, easy accessibility, and aggressive promotions in supermarkets and hypermarkets. Frequent discounts and enticing bundle offers further heighten the allure. With widespread availability and brand recognition, mass-market brands have become the go-to choice for daily use. Yet, to stay in the competitive race, many of these brands are now refining their formulations, bolstering them with scientifically backed claims and enhanced ingredient profiles, thereby narrowing the quality divide with their premium counterparts.

On the other hand, premium hair care products are on an upward trajectory, forecasting a robust CAGR of 6.6% leading up to 2031. This surge is fueled by the affluent Emiratis, high-income expatriates, and a steady stream of tourists, highlighted by the 1.94 million who flocked to Dubai in January 2025, as reported by the Dubai Department of Economy and Tourism . Premium offerings are coveted for their potent efficacy, luxurious ingredients, and the status they confer. These products are available in luxury malls, boutique outlets, and select pharmacies, often accompanied by in-store advisors who elucidate their benefits. Despite a notable price disparity between mass and premium products, the latter significantly bolsters profit margins and steers innovation trends in the United Arab Emirates's hair care landscape.

By Ingredient Type: Natural claims chip at synthetic stronghold

In 2025, conventional/synthetic formulations dominate the United Arab Emirates hair care market, holding a 67.62% share. Their affordability and consistent results keep them in high demand. Mass-market staples like Head & Shoulders Classic Clean Shampoo and Pantene Pro-V Daily Moisture Renewal Conditioner exemplify these conventional products. Utilizing traditional cleansing and conditioning agents, they cater to everyday needs. Bolstered by strong brand recognition, frequent promotions, and widespread availability in hypermarkets, these products are the top choice for budget-conscious consumers. Yet, this stronghold faces challenges from a rising demand for cleaner beauty options.

Natural and organic hair care products are on the rise, boasting an anticipated annual growth rate of 6.89%. Health-conscious consumers fuel this surge in search of gentler, sustainable alternatives. Brands like Faith in Nature Argan Oil Shampoo highlight naturally derived ingredients, free from sulfates and parabens. These offerings not only align with the eco-conscious trend but also withstand the UAE’s sweltering heat, often surpassing 40°C. Retailers are amplifying this movement, introducing dedicated sections for natural products, refill stations, and recyclable packaging. Such initiatives resonate especially with the younger, environmentally-conscious demographic. Consequently, the United Arab Emirates's hair care landscape is witnessing a transformation, with natural and organic products leading the charge, spurring innovation and broadening premium segments.

By Distribution Channel: E-commerce momentum redefines convenience

In 2025, supermarkets and hypermarkets dominated the United Arab Emirates hair care market, capturing 78.73% of its revenue. Their success stems from widespread accessibility, a robust presence, and deep-rooted consumer trust. With a vast network of stores in urban and suburban locales, these retailers have become the go-to choice for a diverse clientele. Strategies like promotions, product bundling, and enhanced shelf visibility further fuel impulse purchases. Yet, the online retail sector is rapidly gaining ground, boasting a projected CAGR of 7.55%. This boom is largely attributed to widespread smartphone adoption, a tech-savvy younger demographic, and national initiatives aimed at bolstering the digital economy. E-commerce giants like Amazon UAE are luring shoppers with a penchant for value and convenience, offering enticing flash sales, subscription discounts, and AI-tailored product suggestions. A case in point: during the 2024 White Friday event, Amazon slashed prices by up to 40% on popular hair care brands like L’Oréal Elvive, Head & Shoulders, and OGX, spurring urgency and multi-unit buys.

In response to the digital wave, traditional retail formats are undergoing significant transformations. Many outlets now feature QR code-enabled shelves, granting shoppers instant access to detailed ingredient breakdowns and usage instructions. The rising trend of 'click and collect' services allows consumers to shop online and conveniently pick up their items at nearby locations, often on the same day. Beauty giants like Sephora UAE are revolutionizing in-store experiences by weaving in digital innovations, from virtual try-ons to interactive kiosks. A standout example is Sephora’s Dubai Mall outlet, which boasts an AI-driven hair diagnostics tool, guiding patrons to the ideal shampoos and treatments tailored to their scalp conditions and hair aspirations.

Geography Analysis

Dubai and Abu Dhabi, with their affluent residents, professional populations, and a steady stream of tourists, dominate the United Arab Emirates's hair care market. The high foot traffic in luxury malls, beauty boutiques, and department stores in these cities makes them prime locations for launching new product lines and gauging global trends. Many international brands have set up flagship outlets here, bolstering their market visibility and influence. For instance, L'Oréal Professionnel and Kerastase frequently debut styling products at Sephora in Dubai Mall and Paris Gallery in Abu Dhabi, capitalizing on heightened customer engagement. Meanwhile, cities like Sharjah and Ras Al Khaimah, spurred by urbanization and rising disposable incomes, are witnessing a surge in demand, leading to the expansion of modern beauty retail outlets beyond the major metros.

The UAE's strategic position as a regional trade hub bolsters the retail hair care sector's resilience. Logistics centers and free zones, notably Jebel Ali, act as distribution hubs for international brands, streamlining supply to both domestic and GCC markets. This robust infrastructure guarantees consistent product availability nationwide, enabling retailers to swiftly restock and offer a diverse product range. For example, Unilever and Procter & Gamble leverage UAE-based hubs to distribute widely sought products, like Head & Shoulders and Dove's hair therapy range, ensuring they're readily available across the region's outlets, catering to both premium and mass-market segments.

The UAE's climate plays a pivotal role in shaping hair care consumer behavior. As summer peaks, there's a surge in demand for hydrating shampoos, anti-frizz products, and color-protecting treatments, with consumers seeking relief from dryness and sun exposure. In Al Ain, where sandstorms are frequent, products like Neutrogena's T/Gel Therapeutic Shampoo and other scalp clarifying items enjoy heightened sales due to their deep-cleansing advantages. Manufacturers, recognizing these seasonal demands, adjust their product assortments and promotional tactics. This strategic alignment not only sustains consistent sales year-round but also cultivates brand loyalty by addressing customers' unique environmental and lifestyle challenges..

Competitive Landscape

The United Arab Emirates hair care market is moderately consolidated. Major companies, including Unilever, Procter & Gamble, and L’Oréal, leverage robust retail and distribution partnerships, aggressive marketing strategies, and a diverse product portfolio to cater to both mass-market and premium consumers. Their vast scale and established brand equity ensure a prominent shelf presence across leading retail channels. Yet, the market remains receptive to competition, especially as shifting consumer preferences and localized challenges pave the way for new entrants.

Responding to localized concerns, especially those related to water quality and its effects on hair, an increasing number of international and regional brands are tailoring their offerings. Concurrently, homegrown and regional companies are capitalizing on their cultural insights are rolling out natural and halal-certified products. These offerings, often competitively priced and marketed with regionally relevant narratives, resonate well with consumers. A case in point is Herbal Essentials Arabia, which is gaining popularity by incorporating Himalayan spring water and locally sourced botanicals, targeting health-conscious and eco-aware buyers.

Brands that swiftly navigate the registration maze with the Emirates Authority for Standardization and Metrology (ESMA) gain a crucial first-mover advantage, expediting their product launches. Conversely, brands that falter in meeting standards, be it ingredient disclosures, Arabic labeling, or halal certifications, face costly repercussions, from relabeling expenses to potential shelf removals. In this evolving landscape, a dependable supply chain and nimble regulatory navigation are as vital as branding and innovation, especially when dealing with retailers who emphasize operational efficiency and compliance. Consequently, the United Arab Emirates hair care market is witnessing heightened dynamism and competition, with innovation, localization, and regulatory preparedness emerging as the cornerstones of growth.

United Arab Emirates Hair Care Industry Leaders

Unilever PLC

Loreal S.A

Procter & Gamble Company

The Estée Lauder Companies Inc.

Beiersdorf AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Unilever is escalating its investment in the UAE, launching a major push into premium and hybrid beauty products tailored to evolving consumer preferences. It plans to enhance its digital commerce capabilities and roll out a regional talent development program to build a next-generation beauty leadership pipeline.

- May 2025: The French luxury haircare brand Christophe Robin officially entered the UAE market, catering to a growing appetite for high-end, ingredient-focused products among affluent consumers.

- October 2024: Zaphira Nature launched its premium vegan and sustainable curly‑hair line “Souffle Méditerranéen”. The brand dedicated to textured hair offers eight clean‑beauty products infused with Ylang Ylang and formulated to hydrate, strengthen, and protect curls in harsh regional climates.

- February 2024: Tata Elxsi has developed an innovative and eco-friendly packaging design for Vatika Shampoo, delivering significant sustainability and performance improvements. The new design achieves a 15% reduction in plastic usage per 400ml pack compared to the previous version.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United Arab Emirates hair care market as retail value generated by shampoos, conditioners, styling aides, colorants, and specialized treatment formulas sold to end-consumers through offline and digital channels, whether imported or locally filled.

Scope Exclusion: Professional salon service revenue and sales of appliances such as dryers or irons are excluded to keep the focus on packaged products.

Segmentation Overview

- By Product Type

- Shampoo

- Conditioner

- Hair Colorants

- Hair Styling Products

- Other Product Types

- By Category

- Premium Products

- Mass Products

- By Ingredient Type

- Natural/Organic

- Conventional/Synthetic

- By Distribution Channel

- Specialty Stores

- Supermarkets/Hypermarkets

- Online Retail Stores

- Other Channels

Detailed Research Methodology and Data Validation

Primary Research

We held structured calls with brand managers, dermatologists, e-commerce category heads, and salon buyers across Dubai, Abu Dhabi, and Sharjah. These conversations validated unit pricing, premium-segment share, natural-ingredient uptake, and channel mix assumptions that secondary material could not fully detail.

Desk Research

We begin with releases from the UAE Federal Competitiveness & Statistics Center, Dubai Customs HS-33 import codes, and Gulf Beauty Federation outlooks, which place a hard floor under national consumption. Our team then layers in company 10-Ks, retailer annual reports, trade-press price trackers, and peer-reviewed dermatology journals that quantify usage shifts toward sulfate-free and scalp-health lines. Paid databases, D&B Hoovers for brand financials, Dow Jones Factiva for deal flow, and Questel for active patent counts, let Mordor analysts benchmark manufacturer revenue curves against shelf sales. The sources cited are illustrative; many additional publications informed collection, cross-checks, and clarification.

Market-Sizing & Forecasting

A top-down construct starts with import landings plus reported local output, adjusted for tourist purchases, re-exports, and leakage. Results are stress-tested through selective bottom-up checks; for example, sampled average selling price multiplied by units sold in leading hypermarkets and online platforms. Five fingerprints drive projections: expatriate population growth, shampoo bottles per capita, premium penetration, online channel share, and salon visitation frequency. A multivariate regression extends these variables to 2030, with scenario bands refined in expert panels; any sub-segment gaps are bridged by weighted channel splits derived from buyer interviews.

Data Validation & Update Cycle

Mordor analysts run variance scans against Nielsen retail indices and customs signals, escalate anomalies to a senior reviewer, and adjust when corroborated. Models refresh annually, with mid-cycle updates triggered by tariff shifts, VAT revisions, or abrupt ASP changes, followed by a last-mile check before every client delivery.

Why Our United Arab Emirates Hair Care Baseline Commands Reliability

Published estimates often diverge because firms pick different scopes, price bases, or refresh rhythms, and because some lean on legacy averages when scanners already show premiumization. By anchoring value to verifiable trade flows and living demographics, we believe our baseline remains the most dependable decision support.

Key gap drivers include omission of men's premium colorants in some studies, constant ASP usage despite inflation, and under-counting of fast-growing e-commerce units.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 442.54 mn (2025) | Mordor Intelligence | - |

| USD 436.68 mn (2024) | Global Consultancy A | Scope omits men's premium colorants; updates every two years |

| USD 401.29 mn (2022) | Industry Association B | Holds ASP constant; excludes online retail surge |

Figures for Global Consultancy A and Industry Association B come from their 2024 and 2022 publications respectively.

These contrasts show how Mordor's disciplined scope selection, annual refresh, and transparent variable set deliver a balanced, repeatable baseline for decision-makers.

Key Questions Answered in the Report

What is the UAE hair care market size in 2026?

The UAE Hair Care market is valued at USD 467.86 million in 2026 and is projected to reach USD 618.33 million by 2031.

What is the fastest-growing hair care segment in the UAE?

Online Retail Stores at 7.55% CAGR is the fastest growing hair care segment, followed by Natural and Organic ingredients at 6.89% CAGR.

Which product type dominates the UAE hair care market?

Shampoo commands the product type with 43.58% market share in 2025.

Which distribution channel holds the largest market share?

Supermarkets/Hypermarkets holds the largest market share with 78.73% market share in 2025.

Page last updated on: