Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

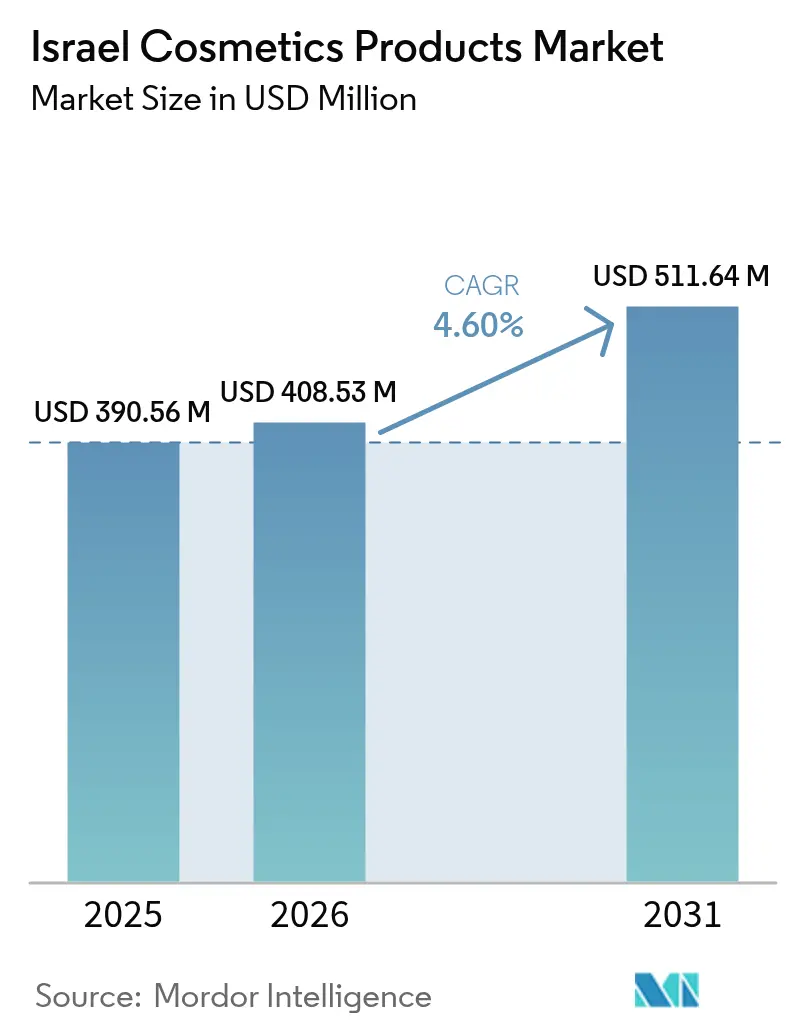

| Base Year Market Size (2025) | USD 390.56 Million |

| Market Size (2026) | USD 408.53 Million |

| Market Size (2031) | USD 511.64 Million |

| Growth Rate (2026 - 2031) | 4.60% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Israel Cosmetics Products Market Analysis by Mordor Intelligence

The Israel cosmetic products market size was valued at USD 390.56 million in 2025 and estimated to grow from USD 408.53 million in 2026 to reach USD 511.64 million by 2031, at a CAGR of 4.60% during the forecast period (2026-2031). Strong digital connectivity continues to drive consumer engagement, while resilient consumer spending supports consistent market growth. Companies are actively introducing innovative products to meet evolving consumer preferences. Urban consumers, who possess advanced knowledge of beauty trends, increasingly demand multifunctional facial products that offer convenience and efficiency. Retailers are integrating pharmacy consultations with seamless e-commerce platforms to create a robust omnichannel retail ecosystem. Additionally, in a moderately fragmented market, established multinational corporations and agile local brands engage in healthy competition. Trends like premiumization, a rising interest in ethical consumption, and tech-enabled personalization are driving significant market growth. Yet, companies face challenges from supply-chain disruptions and increasing compliance costs, which they must navigate to maintain their momentum.

Key Report Takeaways

- By product type, facial makeup led with 46.68% revenue share in 2025; lip and nail makeup is projected to rise at a 5.78% CAGR through 2031.

- By category, the mass segment held 70.12% of the Israel cosmetic products market share in 2025, while premium products are poised for a 6.02% CAGR to 2031.

- By nature, conventional items accounted for 86.12% of the Israel cosmetic products market size in 2025 and natural/organic formulations are advancing at a 5.66% CAGR through 2031.

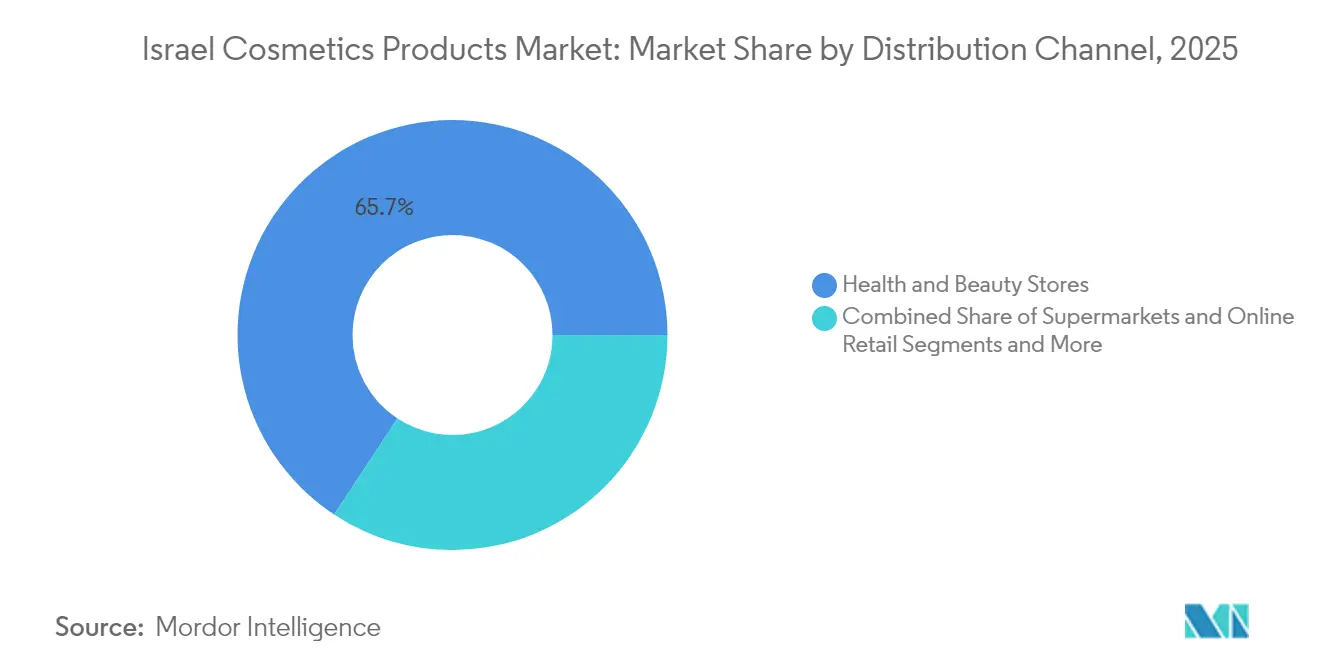

- By distribution channel, health and beauty stores captured 65.72% share in 2025; online retail is forecast to expand at a 6.12% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Israel Cosmetics Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing consumer awareness about personal grooming and beauty trends | +1.2% | National, with concentration in Tel Aviv, Jerusalem, Haifa metropolitan areas | Medium term (2-4 years) |

| Growing inclination toward vegan, cruelty-free, and natural cosmetic products | +0.8% | National, with premium segments in urban centers | Long term (≥ 4 years) |

| Technological advancements enabling innovative formulations and packaging | +1.0% | National, with Research and development clusters in Tel Aviv-Yafo, Rehovot | Medium term (2-4 years) |

| Influence of social media and beauty influencers shaping consumer preferences | +0.9% | National, with highest impact among 18-35 demographics | Short term (≤ 2 years) |

| Rising demand for personalized beauty and tailored cosmetic solutions | +0.7% | Urban centers, expanding to secondary cities | Long term (≥ 4 years) |

| Government initiatives simplifying cosmetic product importation and registration | +0.4% | National, affecting import-dependent segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing consumer awareness about personal grooming and beauty trends

Increasing consumer awareness about personal grooming and evolving beauty standards is a key driver of Israel’s cosmetics products market. With rising urbanization, greater disposable income, and widespread access to global lifestyle trends, consumers are increasingly focused on maintaining an attractive and well-groomed appearance. Social media platforms, beauty influencers, and digital advertising have amplified the desire for flawless skin, personalized makeup, and advanced haircare routines, shaping new beauty ideals among younger demographics. Additionally, the growing participation of men in the beauty and grooming segment is expanding the consumer base, particularly for skincare, perfumes, and beard care products. This heightened awareness, combined with the influence of health and wellness trends, continues to drive innovation and demand for high-quality, sustainable, and dermatologically tested cosmetic products in Israel.

Growing inclination toward vegan, cruelty-free, and natural cosmetic products

The growing inclination toward vegan, cruelty-free, and natural cosmetic products is a significant driver of the Israel cosmetics products market. Israeli consumers are increasingly prioritizing ethical and sustainable beauty choices, reflecting global trends that emphasize animal welfare and environmental responsibility. The demand for products free from animal testing (cruelty-free) and containing no animal-derived ingredients (vegan) is rising sharply, especially among millennials and Gen Z. These consumers are not only focused on product efficacy but also on ingredient transparency and the environmental impact of cosmetics. Technological advancements in plant-based alternatives and lab-grown ingredients are enabling manufacturers to offer high-performance, ethical products that appeal to this conscious segment. Additionally, government initiatives simplifying the import and registration of cosmetic products are facilitating easier access to vegan and natural products. This ethical shift is expanding the market in Israel, with consumers willing to pay a premium for cruelty-free, vegan, and natural cosmetics that align with their values.

Influence of social media and beauty influencers shaping consumer preferences

The influence of social media and beauty influencers is a powerful driver shaping consumer preferences in the Israel cosmetics products market, supported by the fact that about three-quarters of Israelis (74%) used social media in 2024 according to Pew Research [1]Source: Pew Research Center, "Many Israelis say social media content about the Israel-Hamas war should be censored", pewresearch.org. Social media platforms have heightened beauty standards and significantly impacted purchasing behaviors by promoting new products, trends, and beauty routines through influencers and online reviews. These digital channels enable rapid dissemination of information and peer recommendations, encouraging consumers—particularly younger demographics like millennials and Gen Z—to explore and adopt innovative cosmetics. Influencers not only introduce consumers to global beauty trends but also foster engagement through tutorials and authentic content, boosting brand visibility and trust. This dynamic online ecosystem accelerates market growth by driving demand for diverse, trendy, and personalized cosmetic products readily available across both digital and traditional retail channels in Israel.

Government initiatives simplifying cosmetic product importation and registration

The Israeli regulatory frameworks have actively evolved to enhance market access while upholding stringent safety standards. The Ministry of Health has implemented more efficient procedures for cosmetic product registration and import licensing, ensuring a smoother process for stakeholders. Simultaneously, the Ministry of Economy and Industry has taken proactive steps to administer comprehensive trade promotion initiatives. These initiatives aim to attract inbound investments and support the global expansion of Israeli beauty companies. Furthermore, the Ministry of Health has revised its tariff schedules, which will come into effect in July 2025, to address pricing structures and administrative procedures [2]Source: Ministry of Health, "Ministry of Health Tariff", gov.il. These updates demonstrate the government's ongoing efforts to reduce bureaucratic barriers and foster a more business-friendly environment. By simplifying market entry for international brands and facilitating export opportunities for domestic companies, these measures significantly contribute to the market's growth. The reduction in friction for product launches and market expansion initiatives further underscores the positive impact of these regulatory improvements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict regulatory compliance and registration requirements | -0.6% | National, affecting all market participants | Medium term (2-4 years) |

| High cost of natural and vegan cosmetics limiting affordability | -0.4% | National, with higher impact in price-sensitive segments | Long term (≥ 4 years) |

| Intense competition from counterfeit and substandard cosmetic products | -0.3% | National, concentrated in online and informal retail channels | Short term (≤ 2 years) |

| Supply chain disruptions impacting product availability and import timelines | -0.5% | National, with particular impact on import-dependent categories | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Strict regulatory compliance and registration requirements

Regulatory complexities in Israel actively create significant barriers to market entry and product innovation. These challenges are particularly pronounced for smaller companies that lack dedicated compliance teams to navigate the intricate requirements. The Ministry of Health enforces strict oversight on product safety, labeling standards, and import documentation [3]Source: Ministry of Health, "Cosmetics Department", gov.il. Recent studies have highlighted gaps in the regulatory framework for emerging categories, such as gel nail polish. In this category, the absence of professional certification requirements for manicurists has raised serious concerns about consumer safety. Companies face disproportionately high compliance costs when developing innovative formulations and natural products, as these require extensive documentation and rigorous testing to validate their safety and efficacy. Although the regulatory framework prioritizes consumer protection, it often delays product launches and significantly increases development costs. This is especially true for companies attempting to introduce novel ingredients or advanced delivery systems. International companies encounter additional hurdles, including the need to comply with Hebrew-language requirements and local testing protocols. These challenges provide established players with a competitive edge, as they already possess the regulatory expertise needed to navigate the system effectively.

High cost of natural and vegan cosmetics limiting affordability

The high cost of natural and vegan cosmetics is a significant restraint limiting affordability in the Israel cosmetics products market. While the demand for ethically-produced, cruelty-free, and natural beauty products is growing rapidly among conscious consumers, the premium pricing of these items poses a challenge for widespread adoption. The use of specialized ingredients like plant-based extracts, organic components, and advanced lab-grown alternatives, coupled with sustainable packaging, contributes to higher production costs. As a result, natural and vegan cosmetics often come with a price premium compared to conventional products, which restricts accessibility for price-sensitive consumers. Despite government initiatives to simplify import processes and the entry of major retailers boosting market availability, the cost factor continues to limit the reach of natural and vegan beauty products to a broader customer base in Israel.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Facial Makeup Drives Premium Innovation

Facial Makeup holds the largest share in the Israel Cosmetics Products Market, commanding 46.68% of the market in 2025. This dominance reflects Israeli consumers’ sophisticated and nuanced approach to complexion enhancement and color cosmetics. The segment benefits from high per-capita spending on foundation, concealer, and complexion products tailored to diverse skin tones and climate-related concerns prevalent in the Mediterranean environment. The growing influence of beauty trends on social media and increasing demand for products that offer long-lasting, natural-looking coverage further bolster this segment. Innovation in formulation, including products that combine skincare benefits with makeup, adds to the category's appeal. Additionally, the segment’s strength is supported by professional makeup artists and retailers who emphasize comprehensive color matching and personalized service.

Lip and Nail Makeup emerges as the fastest-growing segment, expected to expand at a CAGR of 5.78% through 2031. This growth is driven by trend-conscious consumers and the influential power of social media platforms that accelerate product trial and repurchase cycles. The segment benefits from frequent new product launches, limited-edition collections, and collaborations with influencers and celebrities that keep consumer interest high. Awareness about nail care and innovative formulations, such as long-lasting lipsticks and gel nail polishes, further stimulate demand. Meanwhile, Eye Makeup maintains steady demand due to its established usage patterns, with professional application techniques taught in beauty schools and retail environments. The combined effect of innovation, consumer engagement, and ongoing training keeps eye makeup relevant alongside the rapidly growing lip and nail segments.

By Category: Mass Market Dominance Faces Premium Challenge

Mass category products dominate the Israel Cosmetics Products Market, capturing a substantial 70.12% share in 2025. This dominance underscores the price-conscious nature of Israeli beauty consumers who favor accessible luxury options without the premium price tag. The mass category’s success is supported by effective distribution through pharmacy chains, supermarkets, and health and beauty stores, which offer convenience and professional guidance while keeping prices affordable. These channels help reach a broad consumer base that values product availability and trusted brands for their everyday beauty needs. The mass segment also benefits from innovations that align quality with affordability, maintaining consumer loyalty across different product categories. Its widespread presence across diverse market tiers ensures that mass category products remain the cornerstone of the Israeli cosmetics landscape.

In contrast, the premium category is the fastest-growing segment, exhibiting a robust CAGR of 6.02% through 2031. This growth trajectory reflects an increasing consumer willingness to invest in higher-value products that deliver superior performance, elegant packaging, and prestigious brand appeal. The premium segment is energized by rising consumer awareness around product efficacy, ingredient transparency, and the experiential nature of luxury beauty products. Social media and influencer marketing play pivotal roles in driving demand for exclusive and niche premium products among trend-conscious consumers. Additionally, the premium category’s focus on innovation and personalization elevates its appeal to discerning buyers looking for exceptional skincare and makeup solutions. This upward trend presents significant opportunities for brands targeting the luxury end of the market to expand their presence and profitability.

By Nature: Conventional Products Face Ethical Pressure

Conventional cosmetic products maintain a commanding 86.12% market share in Israel's cosmetics market in 2025, bolstered by their established formulations, competitive pricing, and consumer familiarity with traditional beauty routines. Israeli consumers prioritize efficacy and value in their daily beauty regimens, which reinforces the dominance of these time-tested products. The widespread use of conventional cosmetics also reflects practical considerations where consumers often prefer tested and trusted options over emerging ethical or natural alternatives. Major brands actively support this segment with a broad range of products that meet diverse beauty needs while maintaining affordability. Furthermore, conventional products benefit from strong distribution channels, including pharmacies, supermarkets, and health and beauty stores, which enhance accessibility for the mass market. This segment's stability anchors the overall cosmetics market by catering to a large and loyal customer base.

In contrast, the Natural/Organic segment is the fastest-growing category in the Israel cosmetics market, expanding at a robust CAGR of 5.66% through 2031. This growth is driven primarily by younger demographics who show greater awareness of ingredient safety, environmental sustainability, and ethical consumption. Increasing demand for products free from harmful chemicals, combined with the appeal of botanical, vegan, and cruelty-free formulations, significantly fuels this segment's expansion. As consumers become more conscious about the long-term effects of beauty products on skin and the environment, brands are innovating to develop clean-label offerings with transparent ingredient sourcing. The rise of social media and influencer endorsements further amplifies consumer interest and adoption of natural and organic cosmetics. This trend represents a shift toward wellness-oriented beauty that balances performance with sustainability, positioning the Natural/Organic segment as a key growth driver in Israel’s cosmetics market landscape.

By Distribution Channel: Health and Beauty Stores Lead Digital Transformation

Health and Beauty Stores command the largest share of the Israel Cosmetics Products Market, holding 65.72% of the market in 2025. This dominance is driven by Israel's pharmacy-centric retail model, where professional consultation and personalized product recommendations play a crucial role in guiding consumer purchase decisions. This channel’s strength is particularly evident in skincare and therapeutic cosmetics, where knowledge of ingredients and application techniques significantly influence product adoption and success. Consumers value expert advice, which enhances their confidence in product efficacy and safety, reinforcing the central role of health and beauty stores. Availability, in-store experience, and established trust build strong consumer loyalty, further supporting sustained market leadership. As a result, health and beauty stores remain a key distribution channel vital for premium and mass-market segments alike.

Meanwhile, Online Retail Stores represent the fastest-growing distribution segment, expanding at a CAGR of 6.12% through 2031. This rapid growth is fueled by the rising presence of digital-native consumers who prefer the convenience of shopping from home. The ability to access a wider range of products, benefit from competitive pricing, and enjoy seamless shopping experiences through omnichannel strategies bolster this segment's appeal. Online platforms also facilitate personalized marketing, targeted promotions, and access to reviews and ratings, influencing consumer choice effectively. The integration of physical and digital touchpoints creates enhanced customer engagement, building trust across both retail formats. As e-commerce infrastructure and logistics improve, the online retail channel is set to reshape the Israel cosmetics market landscape by increasing accessibility and augmenting growth opportunities.

Geography Analysis

The Israel Cosmetics Products Market shows significant concentration in urban centers, particularly major cities such as Tel Aviv and Jerusalem. These metropolitan areas contribute substantially to the market revenue, driven by higher disposable income levels, greater exposure to global beauty trends, and access to premium retail channels. Consumers in these urban hubs are generally more trend-conscious and willing to invest in diverse cosmetic offerings, including luxury, natural, and tech-enabled products.

The rural and peripheral regions of Israel exhibit relatively lower cosmetics product sales compared to urban centers, but this segment is gradually expanding. Increasing disposable income, improved distribution infrastructure, and changing lifestyle aspirations among rural populations are contributing to steady market growth outside major cities. The ongoing urbanization trend and increasing penetration of e-commerce platforms are also bridging the urban-rural consumption gap, facilitating wider product accessibility.

Israel’s cosmetics market benefits from its strategic geographical location as a gateway to the Middle East and Mediterranean regions, supporting vibrant export activities and regional market penetration. Additionally, Israel’s innovative beauty tech ecosystem—characterized by startups focused on sustainable ingredients, personalized skincare, and smart devices—enhances the country’s position as a growing beauty innovation hub. This geographic advantage fosters cross-border collaborations and attracts international investments, solidifying Israel’s role in the broader cosmetics landscape within the MEA (Middle East and Africa) region.

Competitive Landscape

The Israeli cosmetics market is moderately fragmented, with established multinational corporations with strong market presence, and innovative domestic companies also hold significant influence. The coexistence of global giants and agile local players fosters a dynamic market environment, encouraging continuous product innovation, diverse consumer offerings, and competitive pricing strategies. This balance ensures healthy rivalry, which benefits consumers through a wider range of choices and improved product quality.

The competitive landscape in Israel is characterized by key players such as L'Oréal S.A., Estée Lauder Companies Inc., Revlon, and emerging domestic brands like Olea Essence and FARAN Cosmetics. These companies differentiate themselves through unique product formulations, advanced ingredient technologies, and targeted marketing campaigns tailored to the distinctive preferences of Israeli consumers. The domestic players often focus on natural and organic product lines, tapping into growing consumer awareness around sustainability and ingredient safety. Meanwhile, multinational brands leverage their global expertise and extensive distribution networks to maintain leadership positions, creating a rich mix of competition. This diversity drives market growth by appealing to both mass and premium consumer segments, fostering innovation across all categories.

Furthermore, Israeli cosmetics companies actively invest in research and development, digital transformation, and e-commerce expansion to sustain their competitiveness. The market players emphasize omnichannel distribution strategies, balancing brick-and-mortar presence with growing online sales platforms. This approach allows them to reach a broader audience, cater to changing shopping behaviors, and enhance customer engagement. Additionally, partnerships between Israeli beauty tech startups and established brands facilitate the introduction of cutting-edge innovations, such as personalized skincare solutions and digital beauty tools. Overall, the moderate concentration level reflects a vibrant industry where collaboration and competition coexist, fueling robust growth and continued evolution in the Israel cosmetics market.

Israel Cosmetics Products Industry Leaders

-

L'Oréal S.A.

-

The Estée Lauder Companies Inc.

-

Revlon Inc.

-

Olea Essence Ltd

-

FARAN Cosmetics Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: NYX Professional Makeup, a brand under L'Oréal Israel, has made its debut in the Israeli market, making it officially accessible to local consumers for the first time. NYX, celebrated for its youthful branding, robust social media engagement, and budget-friendly pricing, had already carved a niche among Israeli consumers through international online sales prior to this local introduction. Now, around 300 NYX offerings, spanning primers, concealers, foundations, lipsticks, and brow products, are being rolled out across drugstore chains, select beauty retailers, and perfumeries throughout Israel.

- April 2025: Super Pharm has launched what is claimed to be Israel’s first dedicated K-beauty department, currently being trialed at its concept store, Super-Pharm Gallery, before a planned rollout to more branches. This department offers the largest selection of Korean beauty brands in Israel, including several making their debut in the country.

- November 2024: Dolce & Gabbana has officially relaunched its makeup and cosmetics brand, now available in Israel for the first time through Beauty & Co, part of the Schestowitz Group. The initial launch includes a capsule collection called Devotion, featuring nine shades of matte liquid lipstick (priced at 169 shekels), mascara (149 shekels), and a luminous powder highlighter (229 shekels), with pricing aligned to the brand's international levels.

Israel Cosmetics Products Market Report Scope

Any product used to clean, improve, or change the complexion, skin, or hair is referred to as "cosmetic." Israel's cosmetics product market is segmented by product type, category, and distribution channel. On the basis of product type, the market is segmented into color cosmetics and hair styling and coloring products. On the basis of the distribution channels, the market is segmented into hypermarkets and supermarkets, specialty stores, pharmacies and drugstores, online retail stores, and other distribution channels. For each segment, market sizing and forecasts have been done based on value (in USD million).

By Product Type

| Facial Makeup |

| Eye Makeup |

| Lip and Nail Makeup |

By Category

| Mass |

| Premium |

By Nature

| Natural / Organic |

| Conventional |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Health and Beauty Stores |

| Online Stores |

| Other Off-Trade Channels |

| By Product Type | Facial Makeup |

| Eye Makeup | |

| Lip and Nail Makeup | |

| By Category | Mass |

| Premium | |

| By Nature | Natural / Organic |

| Conventional | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Health and Beauty Stores | |

| Online Stores | |

| Other Off-Trade Channels |

Key Questions Answered in the Report

How large is the Israel cosmetic products market in 2026?

It totals USD 408.53 million and is projected to rise to USD 511.64 million by 2031.

Which segment grows fastest through 2031?

Lip and nail cosmetics post the highest 5.78% CAGR, driven by trend-led purchases and social-media buzz.

What drives premiumization in Israeli beauty?

Higher disposable incomes, travel exposure to global luxury lines, and influencer content encourage trading up.

Why do natural and vegan products remain niche?

Elevated ingredient and certification costs keep prices high, limiting mass adoption despite ethical appeal.

How are retailers blending online and offline sales?

Pharmacy chains add click-and-collect, virtual advisors, and same-day delivery to enhance convenience and consultation.

Page last updated on: