UAE Artificial Intelligence (AI) Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

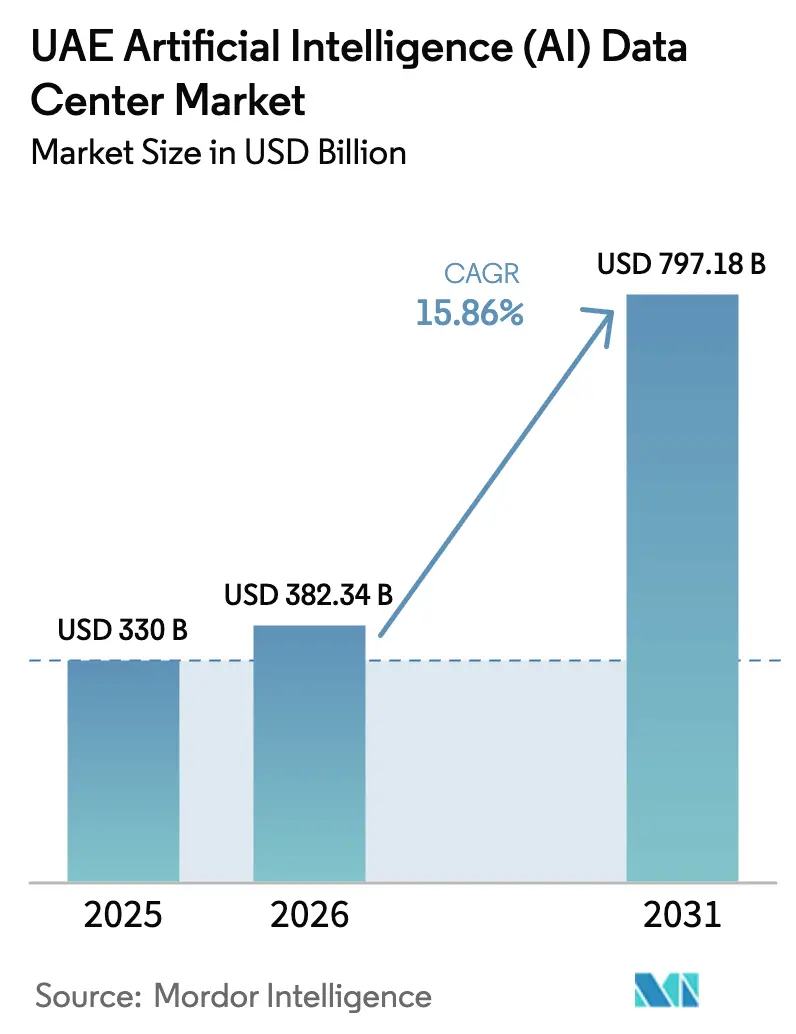

| Base Year Market Size (2025) | USD 330 Billion |

| Market Size (2026) | USD 382.34 Billion |

| Market Size (2031) | USD 797.18 Billion |

| Growth Rate (2026 - 2031) | 15.86% CAGR |

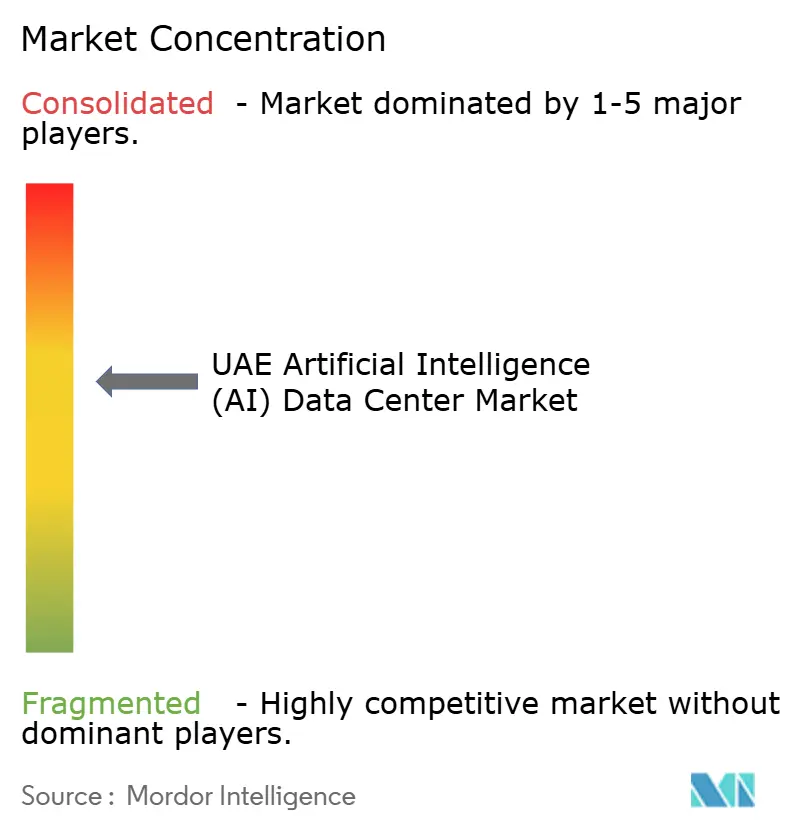

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Artificial Intelligence (AI) Data Center Market Analysis by Mordor Intelligence

The UAE artificial intelligence data center market size in 2026 is estimated at USD 382.34 million, growing from 2025 value of USD 330 million with 2031 projections showing USD 797.18 million, growing at 15.86% CAGR over 2026-2031. Sovereign AI-cloud mandates, hyperscale region launches, and clean-energy power purchase agreements together sustain a sharp uptick in capacity build-outs. Investment momentum from Microsoft, Oracle, and other global providers underpins significant capital inflows, while national strategies are tilting demand toward locally hosted, GPU-rich architectures. Hardware densification, liquid cooling, and renewable power integration reshape facility design, and Tier III expansions offer cost-optimized complements to the country’s dominant Tier IV footprint. Heightened land prices and specialized labor shortages temper near-term supply, yet rising digital-media, BFSI, and healthcare workloads expand the opportunity set for both hyperscale and colocation operators.

Key Report Takeaways

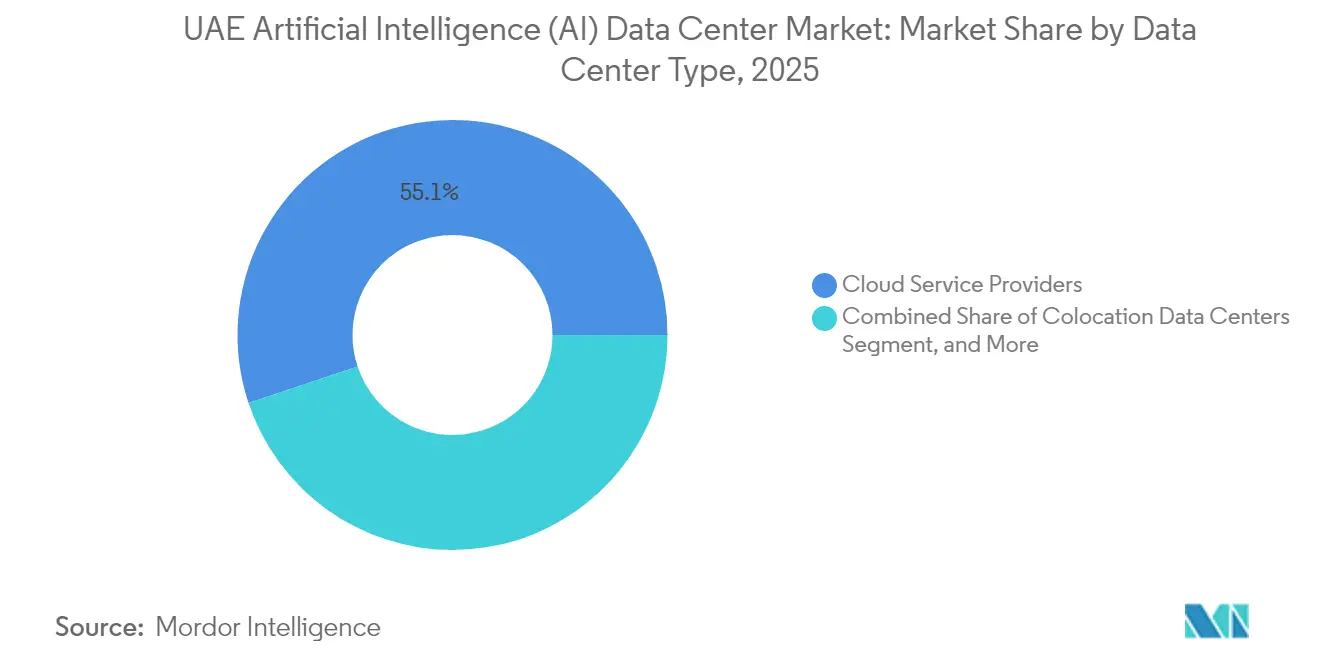

- By data center type, Cloud Service Providers led the UAE artificial intelligence data center market with 55.12% of the market share in 2025; Colocation Data Centers are projected to expand at a 17.61% CAGR through 2031.

- By component, Software captured 45.25% of the UAE artificial intelligence data center market size in 2025; however, hardware is forecast to grow at a 16.98% CAGR between 2026 and 2031.

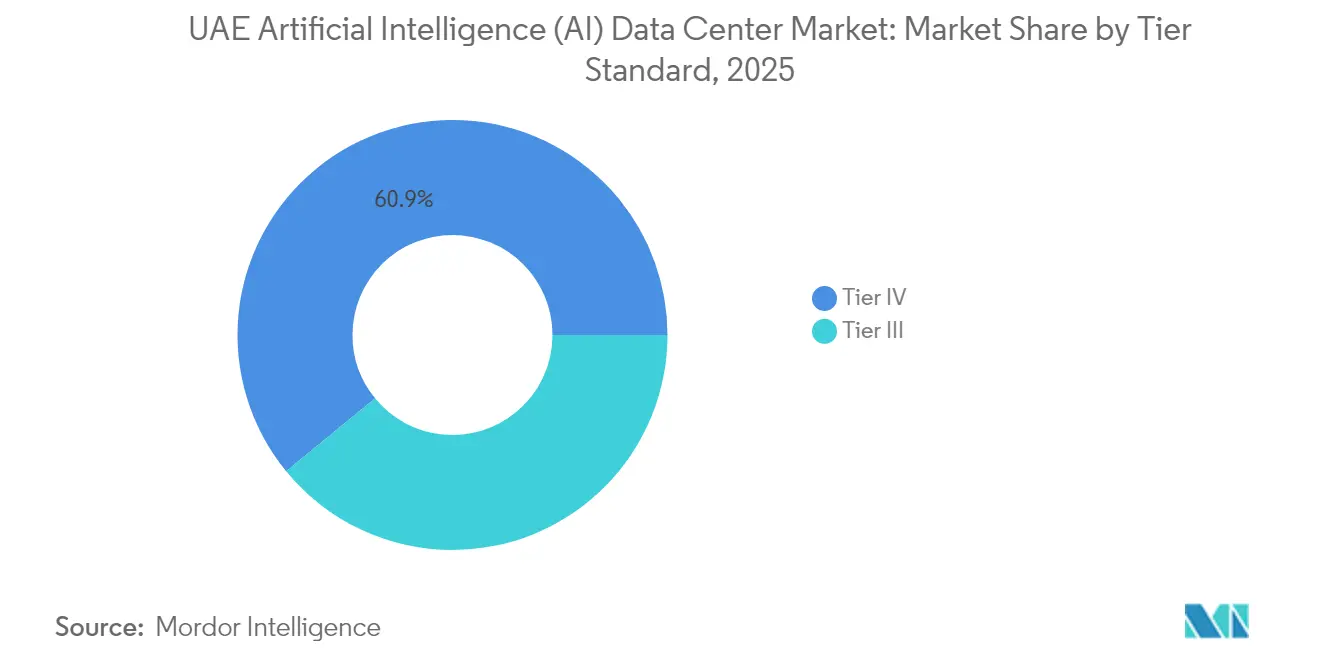

- By tier standard, Tier IV facilities accounted for 60.92% of the UAE's artificial intelligence data center market size in 2025, while Tier III deployments are expected to advance at a 17.74% CAGR to 2031.

- By end-user industry, IT and ITES held a 33.15% revenue share of the UAE artificial intelligence data center market in 2025; the Internet and Digital Media segment is expected to grow at a 16.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Expected changes in United arab emirates many a times form part of a broader pattern of global movement rather than an isolated trend. The report on worldwide artificial intelligence (ai) data center market outlook by Mordor Intelligence brings these expectations together.

UAE Artificial Intelligence (AI) Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale cloud region launches | +3.2% | Dubai, Abu Dhabi | Medium term (2-4 years) |

| Sovereign AI-cloud demand | +4.1% | National, centered in Abu Dhabi | Long term (≥ 4 years) |

| Generative AI uptake in BFSI and healthcare | +2.8% | Dubai financial district, Abu Dhabi | Short term (≤ 2 years) |

| Low-carbon nuclear and solar PPAs | +1.9% | Abu Dhabi (nuclear), Dubai (solar) | Long term (≥ 4 years) |

| Free-zone tax incentives | +2.3% | ADGM, DIFC | Medium term (2-4 years) |

| Liquid-cooling adoption | +1.5% | Dubai, Abu Dhabi clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Hyperscale Cloud Region Launches

Microsoft’s USD 1.5 billion commitment for new AI-optimized availability zones catalyzes a virtuous cycle of regional capacity expansion, latency reduction, and enterprise cloud migration. Oracle’s tie-up with du achieves sub-10 ms latency for mission-critical applications, reinforcing Dubai’s status as a primary node for cross-border traffic.[1]Oracle, “Oracle opens cloud region in UAE,” oracle.com The evaluation of similar footprints by AWS and Google Cloud intensifies competition for land, power, and talent, pushing operators toward multi-story designs. Spillover demand boosts colocation uptake as enterprises colocate adjacent to hyperscale clouds to meet their hybrid architectural needs. The cumulative effect elevates the UAE artificial intelligence data center market to a strategic hub in the Middle East, driving ancillary investment across edge and content-delivery nodes.

Sovereign AI-Cloud Demand from UAE Federal Initiatives

The National AI Strategy 2031 earmarks USD 20 billion for domestic AI capabilities, mandating local hosting for sensitive workloads. G42’s Core42 platform processes classified government data onshore, while the Dubai Universal Blueprint for AI directs all public-sector AI applications to domestically domiciled clouds.[2]Dubai Government, “Dubai Universal Blueprint for Artificial Intelligence 2031,” dubai.ae Preferential procurement amplifies captive demand, accelerating contract wins for Khazna and similar providers. Private firms follow suit to align with data-residency rules and benefit from reduced compliance overhead. Over the long term, sovereign mandates underpin consistent baseline demand regardless of macro cycles, anchoring investor confidence.

Rapid Adoption of Generative AI Workloads by BFSI and Healthcare

Emirates NBD’s deployment of large language models lifts compute intensity by 40% relative to conventional banking applications. Abu Dhabi Commercial Bank’s conversational AI spans 200 branches, requiring sub-second latency and fault-resilient architectures. Healthcare leaders, such as the Cleveland Clinic Abu Dhabi, process more than 50,000 medical images daily through cloud-based inference engines, driving the growth of GPU clusters. The convergence of stringent uptime requirements and data-privacy mandates is steering BFSI and healthcare toward Tier IV or compliant Tier III facilities. Consequently, operators expand managed-service portfolios to include AI model tuning and data-protection services, differentiating on value-added capabilities.

Low-Carbon Nuclear and Solar PPAs for Data Centers

Moro Hub’s solar-powered facility achieves a 1.2 PUE benchmark, setting a precedent for green AI hosting. Barakah Nuclear Power Plant supplies 24/7 carbon-free baseload electricity at rates competitive with those of natural gas, thereby lowering lifecycle operating costs. Microsoft secures a 20-year solar PPA, illustrating hyperscalers’ commitment to net-zero targets and ESG compliance. Clean-energy availability also enables flexible AI workload scheduling, maximizing renewable energy utilization during solar peaks. These initiatives elevate the UAE’s appeal to sustainability-conscious customers and institutional investors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Land scarcity in Dubai and Abu Dhabi | -2.1% | Dubai, Abu Dhabi | Short term (≤ 2 years) |

| Cross-emirate fiber-link permitting delays | -1.3% | Inter-emirate corridors | Medium term (2-4 years) |

| Skilled workforce shortage | -1.8% | National, acute in major hubs | Long term (≥ 4 years) |

| Volatile diesel backup fuel costs | -0.9% | National, higher at edge sites | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Scarcity of Tier 1 Utility-Grade Land in Dubai and Abu Dhabi

Prime parcels in the DIFC and ADGM fetch annual rentals topping USD 150 per square meter, pricing out newer entrants and compressing build timelines.[3]Dubai Land Department, “Dubai Land Market Reports,” dubailand.gov.ae High-rise conversions and brownfield retrofits gain traction but raise cooling-design complexity and capex. Existing incumbents with land banks, such as e& and ST Telemedia, capitalize on their first-mover advantage, thereby widening their competitive moats. Operators explore secondary emirates, though these sites may suffer higher latency to core demand centers. Consequently, the land crunch could delay near-term capacity additions, curbing market expansion.

Skilled Workforce Shortage in AI-Optimized Facility Operations

GPU cluster administrators, liquid cooling engineers, and AI infrastructure architects command 40% salary premiums over standard IT roles. Training programs often lag behind the evolving hardware and software stacks, resulting in operational bottlenecks during expansion ramps. Visa processing for foreign experts introduces further latency, while retention risk rises amid aggressive talent poaching by hyperscalers. Some operators respond by automating routine tasks and partnering with universities for specialized curricula, yet the talent gap remains a structural restraint on growth velocity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Cloud Dominance Drives Colocation Growth

Cloud Service Providers held 55.12% of the UAE artificial intelligence data center market share in 2025, reflecting sustained hyperscale capex and sovereign workload mandates. The segment benefits from multi-year investment roadmaps, ensuring predictable capacity rollouts through 2031. Meanwhile, Colocation Data Centers are forecast to grow at 17.61% CAGR, underpinned by hybrid-cloud adoption and data-residency compliance. Enterprises pursue cost-efficient paths by shifting AI training to hyperscale clouds while retaining inference workloads in proximate colocation sites.

In parallel, Enterprise and Edge deployments register steady, mid-teens growth as BFSI, healthcare, and industrial firms push latency-sensitive applications closer to users. Government regulations favor local hosting, giving colocation facilities a competitive edge in the sovereign-cloud market. Ultimately, the competitive dynamic pushes operators toward portfolio diversification, balancing hyperscale build-to-suits with retail-colocation suites to capture incremental demand.

By Component: Hardware Acceleration Outpaces Software Growth

Software retained a 45.25% share of the UAE artificial intelligence data center market in 2025, driven by machine-learning frameworks, NLP engines, and computer vision toolsets. Yet the Hardware segment will expand at a faster 16.98% CAGR as GPU-rich servers, high-density racks, and liquid-cooling systems become standard for generative AI. Power and Cooling subsegments draw heightened investment because AI clusters exceed 50 kW per rack, which is five times the traditional enterprise load.

Services revenue grows in tandem, encompassing migration, integration, and performance-tuning activities. Managed-service providers bundle model-ops platforms with infrastructure hosting, creating recurring revenue streams. Hardware vendors collaborate with data-center operators on reference designs optimized for local climatic conditions, promoting energy efficiency and reducing time-to-market.

By Tier Standard: Tier IV Reliability Enables Tier III Expansion

Tier IV facilities controlled 60.92% of the UAE's artificial intelligence data center market size in 2025, reflecting mission-critical AI training demands from government and BFSI customers. These sites provide the redundancy necessary for multi-week model training runs that cannot tolerate interruptions. However, Tier III facilities will chalk up 17.74% CAGR as cost-sensitive enterprises migrate stabilized workloads to more economical footprints.

Edge-node rollouts primarily rely on Tier III specifications to minimize latency for public-sector smart-city applications and e-commerce personalization engines. The resulting two-tier market structure enables operators to target distinct customer cohorts: Tier IV for high-risk, high-value applications, and Tier III for scalable inference and edge workloads.

By End-User Industry: Digital Media Disrupts IT Dominance

IT and ITES organizations accounted for 33.15% of 2025 revenue as software developers, system integrators, and fintechs required agile AI sandboxes. Yet, Internet and Digital Media workloads will grow fastest at a 16.94% CAGR, led by user-generated content moderation, generative video creation, and targeted advertising engines. BFSI and Telecom Operators deepen AI adoption for fraud detection and network optimization, respectively, demanding continuous uptime and strict compliance.

Healthcare and life sciences are accelerating due to initiatives in imaging, genomics, and drug discovery. The government and Defense Sectors sustain demand through smart-city and border-security projects, further diversifying the workload mix. The shifting end-user stack compels operators to develop vertical-specific compliance and service layers, widening addressable revenue pools.

Geography Analysis

Dubai and Abu Dhabi collectively host nearly 84% of the installed capacity in 2025, underpinned by robust fiber links, resilient power grids, and proximity to submarine cable landing points. Dubai edges ahead at 44% share thanks to an established commercial ecosystem anchored by Dubai Internet City and DIFC. Abu Dhabi, however, posts the quickest expansion path at 18.14% CAGR to 2031, propelled by sovereign-cloud mandates and generous utility incentives.

The Northern Emirates, including Sharjah, Ajman, and Ras Al Khaimah, emerge as alternative sites for operators facing land crunches in primary hubs. Although current infrastructure lags, TDRA-led backbone projects promise to narrow the latency gap, creating future hotspots for cost-effective edge nodes. Fujairah’s oceanfront location attracts cable-landing ventures, positioning it as a potential springboard for routing South Asian and East African traffic.

Free-zone benefits tilt many developers toward DIFC and ADGM despite higher real-estate costs because zero-tax regimes and streamlined licensing offset capex premiums. Cross-border fiber corridors into Saudi Arabia, Qatar, and Oman buttress the UAE’s role as a regional exchange, supporting resilience and market spillovers. Consequently, geographic strategies now weigh land cost, tax treatment, latency, and cross-border regulatory alignment in multi-variable site-selection models.

Mordor Intelligence's coverage of the artificial intelligence (ai) data center market extends across other regions including North America, South America, and Europe, while country-specific intelligence is also available for Netherlands, Germany, United States, Brazil, France, and United Kingdom, each offering a view on the jurisdiction-level dynamics as applicable.

Competitive Landscape

The market remains moderately fragmented, with the top five operators capturing a combined share of around 45%. Local champions Khazna and G42 leverage sovereign-cloud contracts and GPU partnerships to cement leadership, while global hyperscalers provide scale economics and cloud-native service portfolios. e& Data Centers, ST Telemedia, and Moro Hub differentiate via telecom heritage, renewable-energy PPAs, and district-cooling integrations.

Strategic initiatives are increasingly centered on AI-specific capabilities. Khazna’s tie-up with NVIDIA integrates turnkey GPU clusters, while Microsoft expands its zero-carbon regions to attract ESG-conscious clients. du and Oracle emphasize low-latency peering for enterprise SaaS workloads.[4]Khazna, “NVIDIA partnership announcement,” khazna.ae M&A momentum intensifies as Digital Realty, Equinix, and EdgeConneX seek quick-entry footprints, frequently via joint ventures with domestic developers. Operators with land reserves and in-house engineering talent gain a durable advantage, given the rising barriers associated with power, cooling, and skilled labor.

Edge-computing niches and industry-specific compliance layers (e.g., HIPAA equivalent for healthcare, PCI-DSS for BFSI) present white-space opportunities. Players that bundle infrastructure with managed AI-ops and data-governance services stand to capture premium margins. Competitive intensity, however, pressures pricing for vanilla colocation, pushing providers to pursue differentiation through service depth and sustainability credentials.

UAE Artificial Intelligence (AI) Data Center Industry Leaders

Khazna Data Centers LLC

G42 Cloud LLC (Injazat)

e& Data Centers (Emirates Telecommunications Group Company PJSC)

du Data Centers (Emirates Integrated Telecommunications Company PJSC)

Amazon Web Services Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: G42 and Core42 inaugurate the Middle East’s first sovereign large-language-model training facility in Abu Dhabi, powered by 10,000 NVIDIA H100 GPUs.

- March 2025: ST Telemedia gains TDRA Tier IV certification for a new Abu Dhabi facility.

- February 2025: du and Oracle commission a Dubai cloud region delivering sub-5 ms latency to major business districts.

- February 2025: Moro Hub opens a district-cooled data center, achieving 1.15 PUE.

- January 2025: Microsoft increases its UAE AI infrastructure commitment to USD 2.1 billion, adding new Dubai and Abu Dhabi availability zones designed for generative AI clusters.

- January 2025: Khazna secures USD 800 million financing for 200 MW of additional AI-ready capacity in both Dubai and Abu Dhabi.

- January 2025: Digital Realty partners with DAMAC for a Dubai Business Bay project.

UAE Artificial Intelligence (AI) Data Center Market Report Scope

The research encompasses the full spectrum of AI applications in data centers, covering hyperscale, colocation, enterprise, and edge facilities. The analysis is segmented by component, distinguishing between hardware and software. Hardware considerations include power, cooling, networking, IT equipment, and more. Software technologies under scrutiny encompass machine learning, deep learning, natural language processing, and computer vision. The study also evaluates the geographical distribution of these applications.

Additionally, it assesses AI's influence on sustainability and carbon neutrality objectives. A comprehensive competitive landscape is presented, detailing market players engaged in AI-supportive infrastructure, encompassing both hardware and software utilized across various AI data center types. Market size is calculated in terms of revenue generated by products and solutions providers in the market, and forecasts are presented in USD Billion for each segment.

| Cloud Service Providers |

| Colocation Data Centers |

| Enterprise / On-Premises / Edge |

| Hardware | Power Infrastructure |

| Cooling Infrastructure | |

| IT Equipment | |

| Racks and Other Hardware | |

| Software | Technology |

| Machine Learning | |

| Deep Learning | |

| Natural Language Processing | |

| Computer Vision | |

| Services | Managed Services |

| Professional Services |

| Tier III |

| Tier IV |

| IT and ITES |

| Internet and Digital Media |

| Telecom Operators |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Manufacturing and Industrial IoT |

| Government and Defense |

| By Data Center Type | Cloud Service Providers | |

| Colocation Data Centers | ||

| Enterprise / On-Premises / Edge | ||

| By Component | Hardware | Power Infrastructure |

| Cooling Infrastructure | ||

| IT Equipment | ||

| Racks and Other Hardware | ||

| Software | Technology | |

| Machine Learning | ||

| Deep Learning | ||

| Natural Language Processing | ||

| Computer Vision | ||

| Services | Managed Services | |

| Professional Services | ||

| By Tier Standard | Tier III | |

| Tier IV | ||

| By End-user Industry | IT and ITES | |

| Internet and Digital Media | ||

| Telecom Operators | ||

| Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial IoT | ||

| Government and Defense | ||

Key Questions Answered in the Report

What revenue does the UAE artificial intelligence data center market generate in 2026?

The market records USD 382.34 million in 2026 and is projected to reach USD 797.18 million by 2031.

Which segment grows fastest through 2031?

Colocation Data Centers lead with an 17.61% CAGR as enterprises embrace hybrid-cloud architectures.

Why are Tier III facilities gaining momentum?

Tier III sites balance reliability with lower capex, making them attractive for AI inference and edge workloads expanding across the emirates.

How do sovereign AI policies influence demand?

Federal mandates require sensitive data to remain onshore, creating captive demand that underpins long-term capacity growth for local operators.

What power-sourcing trends shape future build-outs?

Operators increasingly sign solar and nuclear PPAs to satisfy ESG mandates and secure long-term, cost-stable power for GPU-dense facilities.

Which industries are fueling near-term compute demand?

BFSI, healthcare, and digital-media companies deploy generative AI at scale, driving spikes in GPU utilization and low-latency hosting needs.

Page last updated on: