Canada AI Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

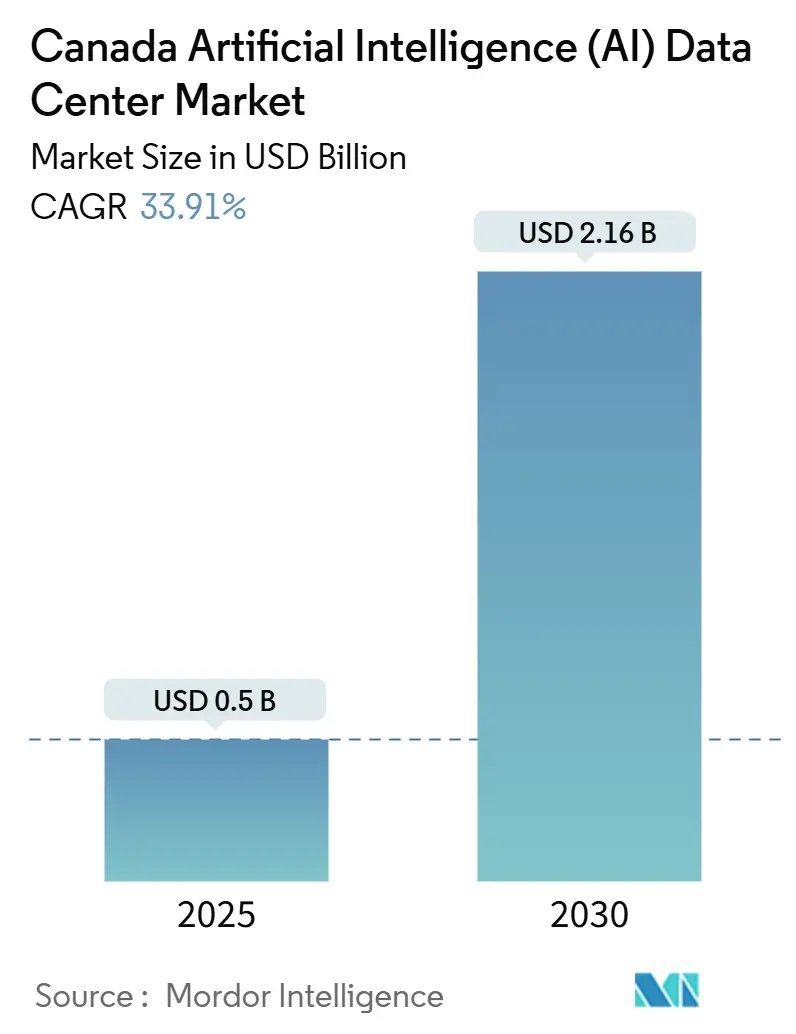

| Market Size (2025) | USD 0.5 Billion |

| Market Size (2030) | USD 2.16 Billion |

| Growth Rate (2025 - 2030) | 33.91% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada AI Data Center Market Analysis by Mordor Intelligence

The Canada AI Data Center Market size stands at USD 0.50 billion in 2025 and is forecast to climb to USD 2.16 billion by 2030, advancing at a 33.91% CAGR over 2025-2030. Inexpensive hydroelectric energy, a cool climate that supports free-air economizer cooling, and CAD 2.4 billion (USD 1.75 billion) of federal incentives are positioning Canada as the preferred overflow location for U.S. hyperscalers looking for carbon-free capacity at scale. The Canada AI Data Center Market is also benefiting from accelerated GPU cluster investments, with Tier IV facilities commanding the bulk of large-training workloads while Tier III sites proliferate to support edge inference demand. Colocation operators are capturing new enterprise workloads through Data-Center-as-a-Service (DCaaS) offerings, even as cloud providers continue to dominate hyperscale builds. Transmission bottlenecks, lengthy environmental assessments, and a shortage of AI-infrastructure talent outside major metros temper growth but have not derailed capacity additions. These dynamics indicate that the Canada AI Data Center Market will remain in hyper-growth mode through the end of the decade.

Key Report Takeaways

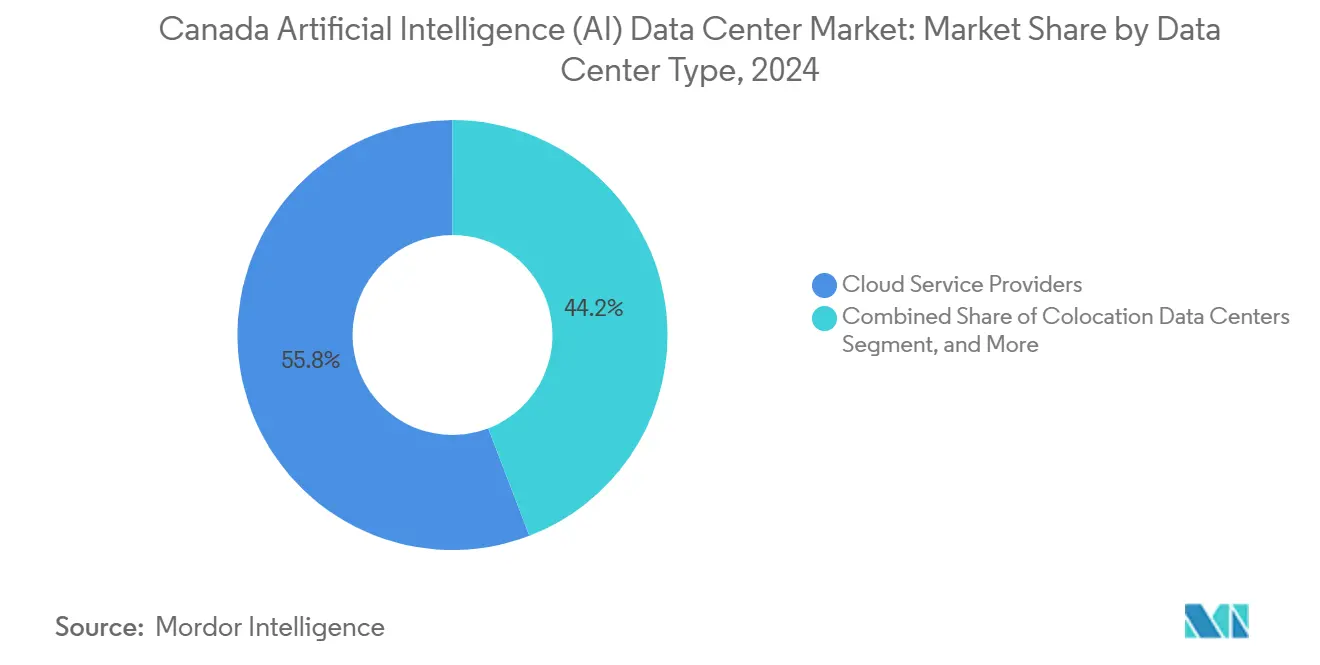

- By data center type, cloud service providers controlled 55.82% of the Canada AI Data Center Market share in 2024, while colocation data centers are expanding the fastest at a 35.23% CAGR through 2030.

- By component, software retained 45.83% share in 2024 in the Canada AI Data Center Market, but hardware is projected to widen at a 34.66% CAGR as GPU and liquid-cooling investments intensify.

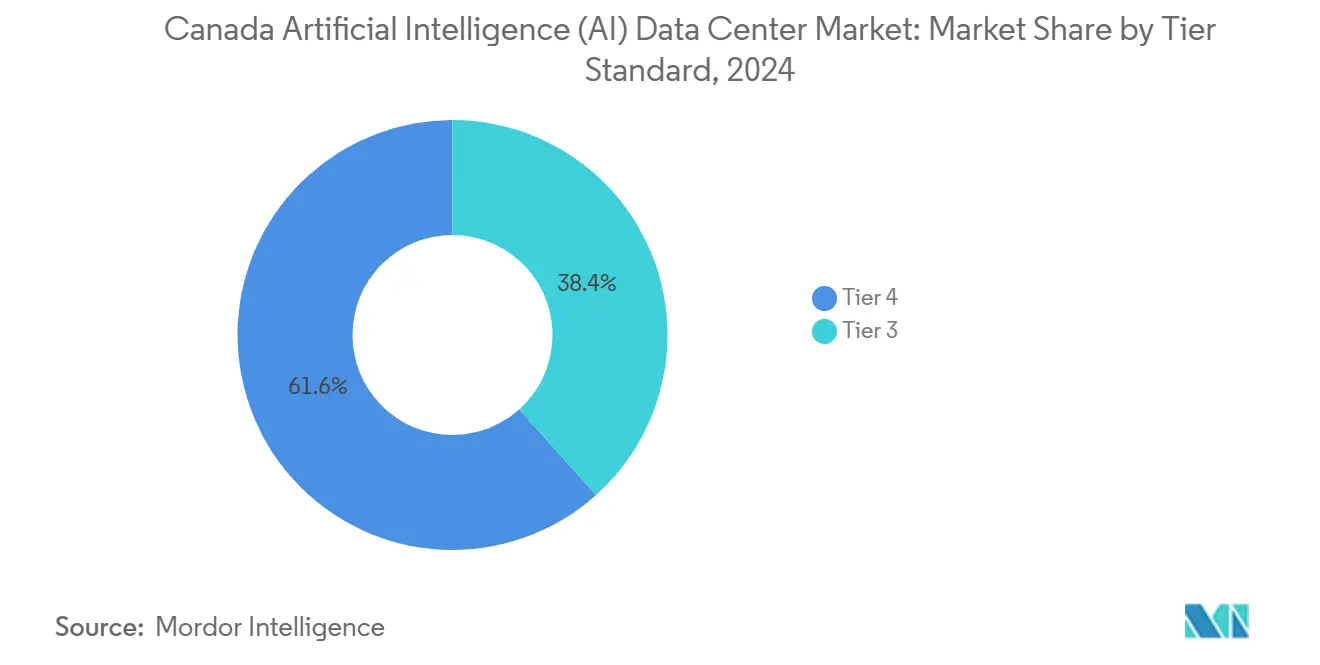

- By tier standard, Tier IV sites held 61.63% of the Canada AI Data Center Market size in 2024; Tier III facilities are set to grow at 35.76% CAGR on rising edge demand.

- By end-user industry, IT and ITES captured 33.82% revenue share in 2024 in the Canada AI Data Center Market, while internet and digital media will accelerate the most at 34.49% CAGR through 2030

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

The contribution of Canada is incorporated into a multi-country and multi-region total that reflects the full breadth of industry. The artificial intelligence (ai) data center market size by Mordor Intelligence expresses that combined magnitude.

Canada AI Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing AI Workload Spill-Over From U.S. Hyperscalers Into Quebec and Ontario | +8.2% | Quebec and Ontario, with expansion to Alberta | Medium term (2-4 years) |

| Abundant Low-Cost Hydro Power Enabling Carbon-Free AI Compute at Scale | +7.8% | Quebec, Ontario, British Columbia | Long term (≥ 4 years) |

| Cold Climate Allowing Economiser-Based Free Cooling for GPU Clusters | +5.4% | National, with highest impact in Northern regions | Medium term (2-4 years) |

| Federal and Provincial AI Grants (SIF, Investissement Québec) for DC Expansion | +6.1% | National, concentrated in Quebec and Ontario | Short term (≤ 2 years) |

| Emergence of Inter-Provincial Edge AI Clusters Along 5G Corridors | +4.7% | Toronto-Montreal-Ottawa corridor, Calgary-Edmonton | Medium term (2-4 years) |

| AI-Optimised DCaaS Models Boosting Adoption by Canadian SMEs | +3.9% | National, with early adoption in major metros | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing AI Workload Spill-Over From U.S. Hyperscalers Into Quebec and Ontario

Grid saturation and rising power prices across traditional U.S. data-center hubs are prompting hyperscalers to shift AI training loads northward. Microsoft’s CAD 1.3 billion (USD 949 million) Quebec City campus, announced in September 2024, is purpose-built for large-language-model training and leverages the province’s 99% renewable electricity mix.[1]Microsoft Canada, “Microsoft Breaks Ground on Quebec City Data Center,” microsoft.com Similar spillover is evident in Meta’s Toronto GPU edge nodes and Amazon’s 80-MW lease in suburban Montreal. The influx tightens local land and power availability but injects long-term anchor demand that benefits utility-scale projects. Provincial authorities continue to streamline permitting for strategic hyperscale investments, further cementing the Canada AI Data Center Market as North America’s overflow valve.

Abundant Low-Cost Hydro Power Enabling Carbon-Free AI Compute at Scale

Industrial electricity rates in Quebec start near CAD 0.029 per kWh (USD 0.021 per kWh), a fraction of the U.S. average and entirely sourced from hydropower.[2]Hydro-Québec, “Industrial Electricity Rates,” hydroquebec.com Multiyear AI training projects consuming 10-50 MW continuously can cut operating costs by USD 10 million annually versus many U.S. states, a decisive factor in site selection. Operators also gain credible renewable-energy claims critical for ESG reporting and financing. The financial and sustainability benefits jointly accelerate greenfield builds in Saguenay, Beauharnois, and the Outaouais region.

Cold Climate Allowing Economizer-Based Free Cooling for GPU Clusters

Ambient temperatures below 15 °C across large parts of Canada yield roughly 6,000 free-cooling hours each year. Advanced economizer systems can therefore slash cooling energy draw by up to 60% compared with compressor-based systems. Vertiv deployments show PUE falling from 1.6 to below 1.2 in optimized Canadian facilities. As next-generation GPUs exceed 80 kW per rack, these climatic advantages translate into lower opex and defer costly mechanical-chiller upgrades.

Federal and Provincial AI Grants for Data-Center Expansion

Since 2024 the Strategic Innovation Fund (SIF) has earmarked CAD 400 million (USD 292 million) for AI-infrastructure projects, while Investissement Québec offers accelerated depreciation and tax credits that can offset 15-25% of capital costs. The Sovereign AI Compute Strategy commits CAD 2.4 billion over five years to spark domestic capacity, blending grants with low-interest loans. These incentives compress payback periods, unlock low-cost financing, and attract first-time foreign investors into the Canada AI Data Center Market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Transmission Capacity in Hydro-Rich Regions for New DC Loads | -4.8% | Northern Quebec, Northern Ontario, Remote BC | Medium term (2-4 years) |

| Skilled AI Infrastructure Talent Shortage Outside Major Metro Hubs | -3.2% | National, acute in secondary markets | Long term (≥ 4 years) |

| Lengthy Environmental Assessment Process for Greenfield Campuses | -2.9% | National, varying by province | Short term (≤ 2 years) |

| Rising Insurance Premiums for High-Density GPU Colocation Suites | -1.7% | National, concentrated in urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Transmission Capacity in Hydro-Rich Regions for New Data-Center Loads

Remote hydro-generation centers in Quebec and Ontario lack high-voltage lines sized for 50+ MW AI campuses. Developers often face CAD 200-500 million grid-upgrade bills and multiyear build cycles. Consequently, some operators pivot to urban sites with higher tariffs but ready capacity, slowing migration toward the lowest-cost power zones.

Skilled AI-Infrastructure Talent Shortage Outside Major Metro Hubs

GPU-centric data-center engineering requires niche expertise in liquid cooling, high-density rack design, and AI workload orchestration. Positions can remain vacant for 6-12 months in cities such as Halifax or Winnipeg, inflating salaries 40-60% above conventional data-center roles. Persistent talent deficits elevate opex and delay commissioning schedules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Cloud Providers Anchor Capacity While Colocation Scales Fast

Cloud providers amassed 55.82% of the Canada AI Data Center Market size in 2024 on the strength of multibillion-dollar hyperscale campuses serving internal and third-party AI workloads. Microsoft’s Quebec build and AWS’s Montreal leases typify this concentration. Meanwhile, the colocation segment is projected to surge at 35.23% CAGR as enterprises favor capital-light migration paths and as GPU-as-a-Service bundles proliferate.

The shift toward colocation reflects rising comfort with outsourced AI infrastructure that still permits workload-level controls. Cologix’s 2024-launched AI Suites pre-install direct-to-chip liquid cooling, enabling tenants to reach 80 kW per rack without mechanical retrofits.[3]Cologix, “AI-Optimized Data Center Solutions,” cologix.com Edge and enterprise deployments remain comparatively small today but are strategically vital for latency-sensitive inference tied to 5G corridors. Collectively, these sub-segments diversify supply and embed resiliency into the Canada AI Data Center Market.

By Component: Software Commands Today’s Wallet Share, Hardware Drives Incremental Growth

Software captured 45.83% revenue in 2024, reflecting the critical role of orchestration frameworks, MLOps platforms, and data-fabric solutions in maximizing GPU utilization. Yet hardware will grow faster at 34.66% CAGR through 2030 as operators invest in H100 clusters, 800 G fiber networks, and liquid-immersion cooling to support transformer models.

Deployment of NVIDIA DGX SuperPods at QScale’s Q01 site shows how capital intensity tilts toward silicon and thermal infrastructure as density climbs. On the software side, Kubernetes-native AI schedulers and federated-learning stacks continue to evolve, securing recurring revenue streams even as hardware refresh cycles stabilize. Together, balanced spending ensures that the Canada AI Data Center Market retains holistic growth momentum.

By Tier Standard: Tier IV Safeguards Large-Training Runs, Tier III Powers the Edge

Tier IV facilities accounted for 61.63% of the Canada AI Data Center Market share in 2024 owing to concurrent-maintenance designs prized for multimillion-dollar AI training jobs. N+N power paths and 2N cooling redundancy mitigate the financial risk of interrupted epochs.

Tier III builds, forecast to post a 35.76% CAGR, target inference workloads where 99.982% availability suffices and capital discipline matters. Digital Realty’s new Toronto suite uses 1+1 UPS with on-floor CDU loops to balance reliability and cost. This tier stratification enables operators to align SLAs with application criticality, supporting a layered capacity model across the Canada AI Data Center Market.

By End-User Industry: IT Services Lead, Media and Streaming Accelerate

IT and ITES firms held 33.82% revenue in 2024 on early-mover adoption of generative-AI development environments and consulting workloads. Internet and digital-media providers display the loftiest 34.49% CAGR, scaling recommendation engines and live-transcoding farms that demand continuous low-latency inference.

BFSI usage is rising on real-time fraud analytics, while healthcare pilots center on AI-aided diagnostic imaging. Manufacturing embraces predictive maintenance running near-plant edge nodes. Government agencies pursue sovereign AI compute aligned with domestic custody laws. These diverse workflows collectively reinforce the broadening customer base of the Canada artificial intelligence (AI) data center industry.

Geography Analysis

Quebec and Ontario collectively generated roughly 75% of 2024 revenue, anchoring the Canada AI Data Center Market in provinces with plentiful hydro power, dense fiber routes, and direct proximity to enterprise demand hubs. Quebec’s sub-CAD 0.03 per kWh tariffs and 6,000 free-cooling hours attract mega-campuses such as Microsoft’s Quebec City and QScale’s Lévis sites.

Ontario commands the largest provincial revenue thanks to Toronto’s finance and tech ecosystem. Higher CAD 0.13 per kWh tariffs are offset by customer colocation preferences and reduced latency to end-users. Tier III and Tier IV footprints in Markham, Brampton, and downtown Toronto continue to swell as digital-media and fintech workloads scale.

British Columbia is emerging as the growth hotspot; Bell Canada’s six-site AI Fabric adds 500 MW of hydro-powered capacity, leveraging the province’s vast generation surplus. Alberta, Manitoba, and Atlantic provinces capture smaller but fast-growing edge deployments serving resource, agriculture, and port-logistics verticals. Cross-province 5G fiber corridors knit these nodes into a cohesive national fabric, reinforcing dispersion of the Canada AI Data Center Market.

Mordor Intelligence provides coverage of the artificial intelligence (ai) data center market across other key regional markets, including Asia, Middle East and Africa, and North America, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to Mexico, Brazil, Japan, United Arab Emirates, Malaysia, and Indonesia incorporating local coverage and market participation, as required.

Competitive Landscape

Global hyperscalers, multinational colocation giants, and homegrown specialists share a moderately concentrated field. Microsoft, AWS, and Google anchor utility-scale builds, stacking proprietary GPUs and ASICs for internal AI services while leasing excess to enterprises under sovereign-cloud frameworks. Cologix, Digital Realty, and Equinix target multi-tenant AI suites with pay-as-you-go GPU models, responding to enterprise demand for flexibility.

Emergent Canadian specialists such as QScale design greenfield campuses tuned for liquid-immersion cooling and near-substation siting, carving high-performance niches. Telecom operators Bell and Telus leverage network peering and edge real estate to insert themselves into the AI supply chain, creating hybrid carrier-compute propositions.

Competitive differentiation centers on power efficiency, sustainability credentials, and speed-to-GPU provisioning rather than rack count alone. Operators also cultivate regional talent pipelines with universities to mitigate skilled-labor shortages. M&A activity is expected to intensify as international investors seek entry into the Canada AI Data Center Market through local platforms.

Canada AI Data Center Industry Leaders

Advanced Micor Devices, Inc

NVIDIA Corporation

Green Revolution Cooling, Inc.

Vertiv Group Corp.

Schneider Electric SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Schneider Electric launched new liquid cooling solutions specifically designed for the Canadian market, addressing the thermal challenges of high-density AI workloads while optimizing performance for the country's cold climate, enabling more efficient operations and reduced energy consumption

- March 2025: Vertiv has introduced its latest product, the CoolLoop Trim Cooler. This unit is designed for both air and liquid cooling applications, specifically targeting AI and HPC deployments. The CoolLoop Trim Cooler works efficiently in various climate conditions, making it suitable for hybrid-cooled or liquid-cooled data centers, including those in Canada, as well as 'AI factories.' Vertiv claims this solution can reduce annual cooling energy consumption by up to 70% through free-cooling and mechanical operation. It also saves 40% more space compared to traditional systems.

- September 2024: Microsoft broke ground on a CAD 1.3 billion Quebec City facility engineered for AI-training clusters, tapping 100% renewable hydro power.

- August 2024: Cologix partnered with Consensus Core to launch GPU-as-a-Service across Canadian sites, offering on-demand H100 and A100 capacity.

Canada AI Data Center Market Report Scope

The research encompasses the full spectrum of AI applications in data centers, covering hyperscale, colocation, enterprise, and edge facilities. The analysis is segmented by component, distinguishing between hardware and software. Hardware considerations include power, cooling, networking, IT equipment, and more. Software technologies under scrutiny encompass machine learning, deep learning, natural language processing, and computer vision.

The study also evaluates the geographical distribution of these applications. Additionally, it assesses AI's influence on sustainability and carbon neutrality objectives. A comprehensive competitive landscape is presented, detailing market players engaged in AI-supportive infrastructure, encompassing both hardware and software utilized across various AI data center types. Market size is calculated in terms of revenue generated by products and solutions providers in the market ,and forecasts are presented in USD Billion for each segment.

| Cloud Service Providers |

| Colocation Data Centers |

| Enterprise / On-Premises / Edge |

| Hardware | Power Infrastructure |

| Cooling Infrastructure | |

| IT Equipment | |

| Racks and Other Hardware | |

| Software Technology | Machine Learning |

| Deep Learning | |

| Natural Language Processing | |

| Computer Vision | |

| Services | Managed Services |

| Professional Services |

| Tier III |

| Tier IV |

| IT and ITES |

| Internet and Digital Media |

| Telecom Operators |

| BFSI |

| Healthcare and Life Sciences |

| Manufacturing and Industrial IoT |

| Government and Defense |

| By Data Center Type | Cloud Service Providers | |

| Colocation Data Centers | ||

| Enterprise / On-Premises / Edge | ||

| By Component | Hardware | Power Infrastructure |

| Cooling Infrastructure | ||

| IT Equipment | ||

| Racks and Other Hardware | ||

| Software Technology | Machine Learning | |

| Deep Learning | ||

| Natural Language Processing | ||

| Computer Vision | ||

| Services | Managed Services | |

| Professional Services | ||

| By Tier Standard | Tier III | |

| Tier IV | ||

| By End-user Industry | IT and ITES | |

| Internet and Digital Media | ||

| Telecom Operators | ||

| BFSI | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial IoT | ||

| Government and Defense | ||

Key Questions Answered in the Report

How big is the Canada AI Data Center Market in 2025?

The market is valued at USD 0.50 billion in 2025, on track to reach USD 2.16 billion by 2030.

What is driving hyperscalers to build AI data centers in Canada?

Ultra-low hydroelectric power prices, abundant renewable energy, and supportive federal incentives lower total cost of ownership versus many U.S. regions.

Which Canadian province offers the most attractive power tariffs for AI workloads?

Quebec leads with industrial rates near CAD 0.029 per kWh, materially below the national average.

Why are Tier IV facilities dominant in Canadian AI deployments?

Weeks-long training runs worth millions of dollars cannot tolerate downtime, making Tier IV’s concurrent-maintenance design essential.

How are SMEs accessing GPU capacity without large capex?

Colocation providers now bundle GPU-as-a-Service and DCaaS models, letting businesses rent H100 clusters on a consumption basis.

Page last updated on: