Middle East And Africa Artificial Intelligence (AI) Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

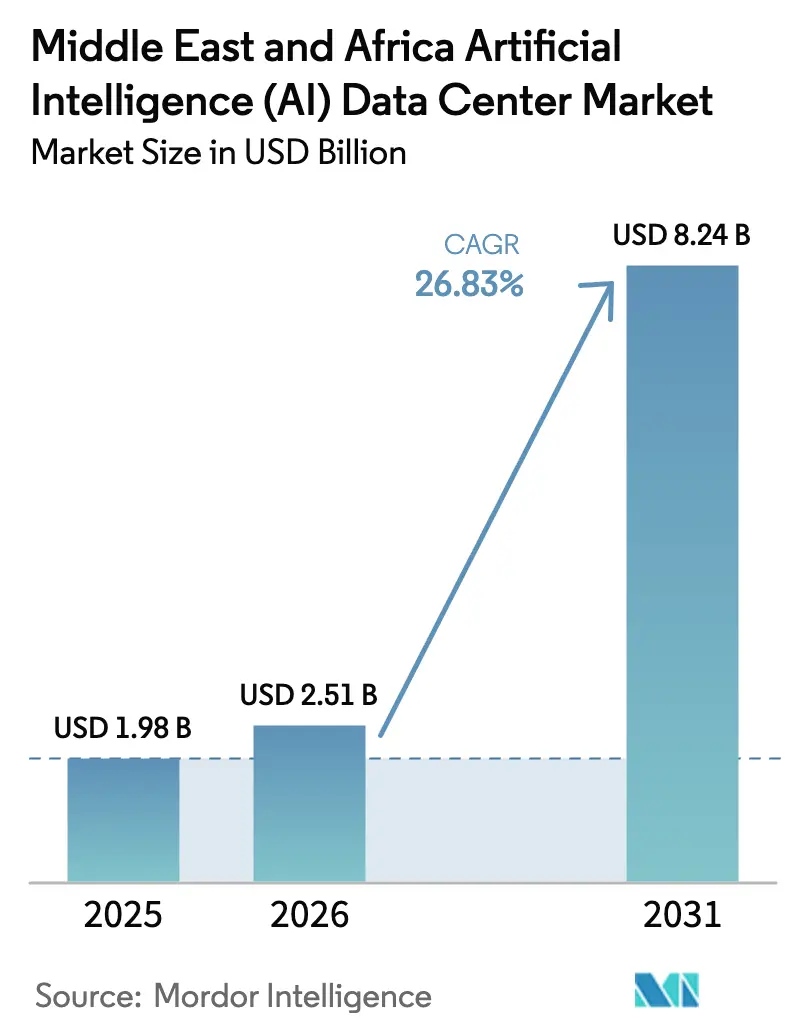

| Base Year Market Size (2025) | USD 1.98 Billion |

| Market Size (2026) | USD 2.51 Billion |

| Market Size (2031) | USD 8.24 Billion |

| Growth Rate (2026 - 2031) | 26.83% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Artificial Intelligence (AI) Data Center Market Analysis by Mordor Intelligence

The Middle East and Africa artificial intelligence data center market size in 2026 is estimated at USD 2.51 billion, growing from 2025 value of USD 1.98 billion with 2031 projections showing USD 8.24 billion, growing at 26.83% CAGR over 2026-2031. This rapid climb reflects rising demand for sovereign Arabic-language model training, large-scale GPU clusters, and low-latency inference capacity. Hyperscaler capital deployments, government digital-transformation mandates, 5G-enabled edge computing, and favorable free-zone incentives converge to accelerate new builds and facility upgrades. Tier IV redundancy remains the preferred reliability standard for multi-week model-training runs, yet Tier III innovation at the edge is widening adoption by cost-sensitive enterprises. Operators that combine renewable-energy sourcing with advanced liquid cooling gain a competitive edge by mitigating Gulf-state water scarcity and sub-Saharan grid instability.

Key Report Takeaways

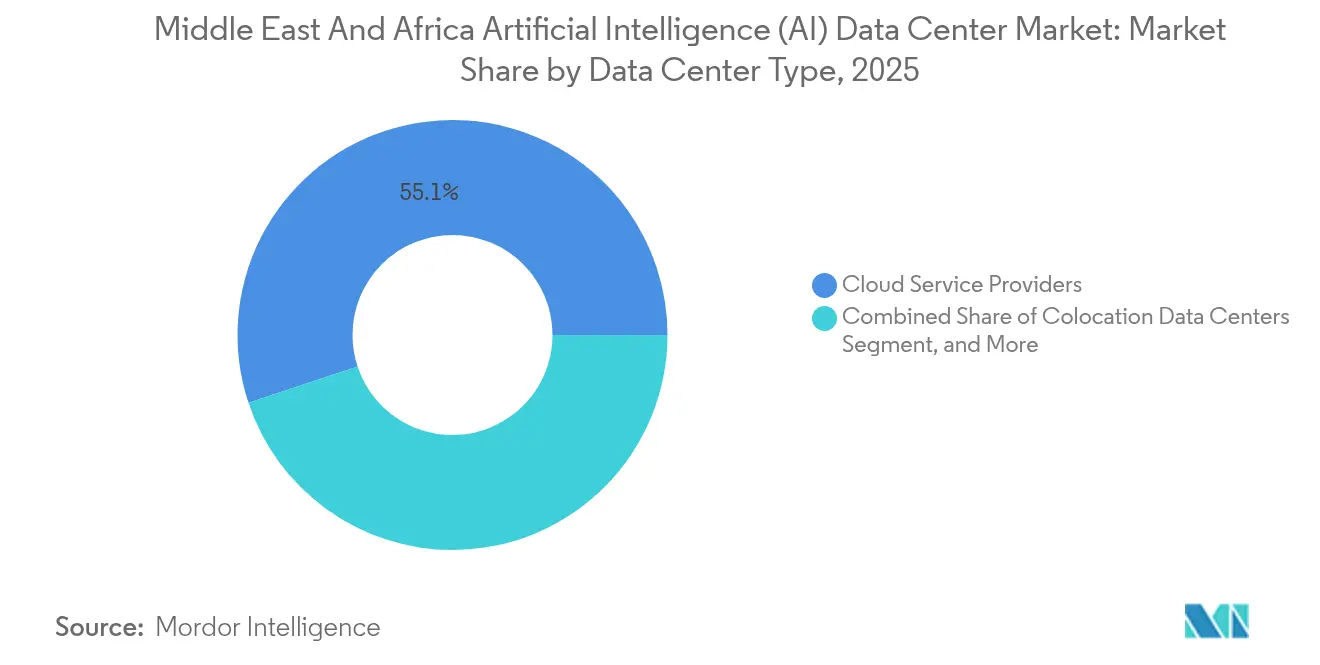

- By data-center type, cloud service providers led with 55.10% revenue share in 2025; colocation is advancing at a 28.45% CAGR to 2031.

- By component, software held 45.20% of the Middle East and Africa artificial intelligence data center market share in 2025, while hardware is set to expand at 27.95% CAGR through 2031.

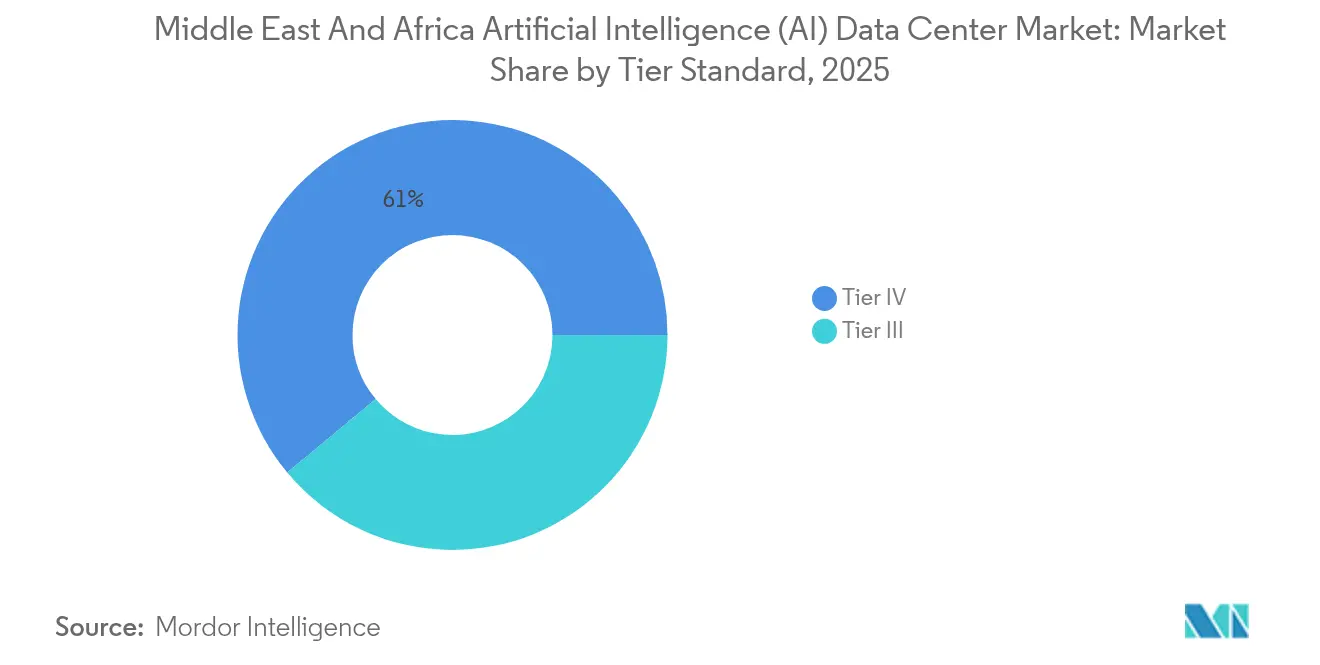

- By tier standard, Tier IV facilities captured 61.05% of the Middle East and Africa artificial intelligence data center market size in 2025 and Tier III is growing at 28.20% CAGR to 2031.

- By end-user industry, IT and ITES accounted for 33.25% of demand in 2025; Internet and Digital Media records the highest projected CAGR at 28.05% to 2031.

- By geography, Saudi Arabia commanded 31.10% revenue share in 2025, whereas South Africa is forecast to grow at 27.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle east and africa holds a defined position within a broader international distribution. The artificial intelligence (ai) data center market share data by Mordor Intelligence maps that allocation across all contributing regions, globally.

Middle East And Africa Artificial Intelligence (AI) Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in hyperscale cloud investments across GCC for AI workloads | +8.2% | GCC core, spill-over to Egypt and South Africa | Medium term (2-4 years) |

| Government digital transformation initiatives and Smart City programs | 6.8% | Saudi Arabia, UAE, Egypt with expansion to Morocco | Long term (≥ 4 years) |

| Growing adoption of 5G networks requiring edge AI data centers | 5.4% | UAE, Saudi Arabia, South Africa with regional expansion | Medium term (2-4 years) |

| Favorable free-zone tax incentives for data-center construction | 3.1% | UAE, Saudi Arabia, Bahrain with selective African markets | Short term (≤ 2 years) |

| Rising demand for Arabic-language foundation models needing local GPU clusters | 2.8% | GCC, North Africa with cultural relevance across MENA | Long term (≥ 4 years) |

| Planned East-African submarine-cable landings creating inference hubs | 1.9% | East Africa, South Africa with connectivity to global networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Hyperscale Cloud Investments Across GCC for AI Workloads

AWS allocated USD 5.3 billion for Saudi regions, Oracle earmarked USD 1.5 billion, and Microsoft placed USD 1.5 billion in G42 to accelerate sovereign AI capacity. Capital flows target GPU-dense clusters that host 70-billion-parameter models such as JAIS, enabling latency-sensitive services while meeting data-residency mandates. Multiplier effects include G42’s Condor Galaxy scale-out and local operators retrofitting halls for liquid cooling. Cooperative build-operate models shorten delivery schedules and deepen regional supply chains.[1]Oracle Corporation, “Oracle to Open Cloud Region in Saudi Arabia,” oracle.com

Government Digital Transformation Initiatives and Smart-City Programs

Saudi Vision 2030, the UAE’s AI-native government roadmap, and Egypt’s Atlas Project allocate multi-billion-dollar budgets for AI-enabled governance. Projects such as NEOM embed predictive analytics and autonomous systems that require near-real-time inference close to citizens. Guaranteed demand from public services underwrites long-term colocation contracts, eases financing for Tier IV builds, and shapes compliance frameworks favoring local hosting.

Growing Adoption of 5G Networks Requiring Edge AI Data Centers

UAE 5G coverage reached 95% by 2024 and Saudi rollouts underpin smart-mobility pilots. Low latency thresholds below 20 milliseconds push compute toward metro-edge sites that ingest video, sensor, and vehicle telemetry. Telecom operators Etisalat and STC co-locate micro-data centers inside base-station shelters, driving orders for compact immersion-cooled GPU servers and battery-backed power modules.[2]Telecom Regulatory Authority, “5G Network Coverage UAE,” tra.gov.ae

Favorable Free-Zone Tax Incentives for Data-Center Construction

Dubai International Financial Centre and Abu Dhabi Global Market permit 100% foreign ownership, zero corporate tax for qualifying digital-infrastructure activities, and single-window licensing. Investors attain faster break-even through reduced duty outlays and pre-built power corridors. Similar mechanisms in Bahrain and NEOM’s special economic zone catalyze regional spill-overs as African states emulate the model to court capital.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Power-grid reliability issues in several African countries | -4.3% | Sub-Saharan Africa with selective North African markets | Long term (≥ 4 years) |

| High capital expenditure and extended ROI for Tier IV AI data centers | -3.7% | Regional with concentration in GCC and South Africa | Medium term (2-4 years) |

| Shortage of advanced-semiconductor talent for on-site accelerator maintenance | -2.1% | Global with acute impact in emerging African markets | Long term (≥ 4 years) |

| Water-scarcity regulations limiting evaporative cooling in arid zones | -1.8% | GCC, North Africa with expansion to arid sub-Saharan regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Power-Grid Reliability Issues in Several African Countries

Grid outages in Kenya, Nigeria, and Ghana disrupt training cycles, forcing operators to oversize diesel backup and invest in solar-plus-battery microgrids. Redundancy raises operating costs, elongates rack deployment timelines, and diverts capital toward energy resiliency rather than compute innovation. Providers with independent power-producer alliances secure long-term supply contracts that offset volatility.[3]Kenya Power and Lighting Company, “Power Supply Updates,” kplc.co.ke

High Capital Expenditure and Extended ROI for Tier IV AI Data Centers

Redundant feeds, dual UPS lines, and concurrently maintainable liquid-cooling loops raise build costs by up to 60% relative to Tier III halls. Payback stretches as ramp-ups depend on hyperscaler pre-leases and sovereign-cloud accreditation. Smaller African entrants face financing hurdles without anchor tenants, widening the gap between global cloud majors and regional newcomers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Cloud Dominance Drives Colocation

Cloud operators captured the largest slice of the Middle East and Africa artificial intelligence data center market share at 55.10% in 2025, leveraging integrated AI-platform portfolios and multi-availability-zone footprints. Colocation, however, is forecast to outpace all other formats at 28.45% CAGR, buoyed by hybrid-cloud workloads that split sensitive data into on-premises cages while bursting training jobs to public regions. The Middle East and Africa artificial intelligence data center market size for colocation is projected to climb sharply as enterprises adopt sovereign AI postures aligned with regional data-protection statutes.

Enterprises now pre-book high-density suites exceeding 30 kW per rack, enabling colocation providers to command premium rates for purpose-built liquid-cooled white space. Edge and enterprise micro-sites supplement metro coverage by hosting latency-critical inference pipelines near smart-factory floors and financial-trade hubs. Partnerships such as G42-Khazna facilitate cross-connects that compress data-ingest times, further attracting AI-native software vendors.

By Component: Software Leadership Masks Hardware Acceleration

Software platforms controlled 45.20% revenue in 2025, reflecting regional prioritization of orchestration stacks, model-life-cycle automation, and Arabic NLP toolkits. Within the segment, specialized inference optimizers integrating parameter-efficient fine-tuning are becoming differentiators for colocation tenants. Meanwhile, the hardware subset is on track for a 27.95% CAGR through 2031 as demand surges for H100-powered clusters, 400 Gbps network fabrics, and rear-door heat-exchanger cooling. The Middle East and Africa artificial intelligence data center market size allocated to hardware will therefore narrow the revenue gap with software by 2031.

Service integrators monetize skills shortages by managing full-stack deployments, from GPU burn-in to model retraining, generating steady annuity streams. Operators bundle hardware leasing with software licenses and managed-service SLAs, enabling capital-light adoption for banks and media firms that cannot budget large capex outlays in a single fiscal year.

By Tier Standard: Tier IV Reliability Enables Tier III Innovation

Tier IV halls accounted for 61.05% of 2025 spend, anchored by hyperscaler SLAs that tolerate zero downtime during multi-week reinforcement-learning cycles. This slice equates to the largest portion of the Middle East and Africa artificial intelligence data center market size at facility-grade level. Yet Tier III is accelerating most quickly at 28.20% CAGR, driven by inference-only clusters and regional metro-edge deployments supporting streaming and smart-mobility analytics. Checkpoint-based training and distributed model-parallel architectures reduce single-site failure impact, legitimizing Tier III adoption where real estate or capex is constrained.

Operators strip Tier IV redundancy on water loops or transformers in edge builds while offsetting risk through software resilience and active-active regional clustering. This hybrid reliability strategy shrinks time-to-market and aligns op-ex budgets with workload criticality profiles.

By End-User Industry: IT Leadership Yields to Media Innovation

IT and ITES remained top contributors at 33.25% in 2025, consuming bulk GPU hours for software-development pipelines and system-integration proofs. However, Internet and Digital Media exhibits the fastest 28.05% CAGR, fueled by Arabic content generation, generative-audio translation, and personalized streaming requiring on-the-fly inference. Segment investors procure co-located H100 pods to tune transformer models for dialectal subtleties, elevating user engagement across MENA platforms.

BFSI workloads add risk-modeling sandboxes and GenAI chat agents, while healthcare pilots radiology-image classifiers under strict data-localization rules. Manufacturing and industrial IoT introduce digital-twin simulators needing millisecond feedback loops unavailable from distant cloud regions, accelerating demand for near-plant micro-data centers.

Geography Analysis

Saudi Arabia’s 31.10% market hold in 2025 stems from parallel public and private capital injections, streamlined permitting, and abundant low-cost hydrocarbons that temper electricity prices. AWS, Oracle, and Google Cloud accelerated ground-breaks after securing data-residency compliance, while NEOM’s special-economic-zone statutes shorten license approvals and entrench Tier IV design standards. Emerging Arabic foundation models, including JAIS, further anchor GPU clusters within kingdom borders to minimize cross-border data transfer latency.

The UAE follows closely, merging Dubai’s free-zone foreign-ownership incentives with Abu Dhabi’s research focus through MBZUAI and G42’s Condor Galaxy. Ninety-five percent 5G coverage enables edge-AI co-location at telecom points-of-presence, supporting smart-transportation pilots and computer-vision public-safety systems. Power-purchase agreements for solar overbuilds stabilize electricity input costs and align national net-zero-by-2050 ambitions.

South Africa emerges as fastest-expanding at 27.90% CAGR, underpinned by 2Africa cable landings, plentiful wind-solar resources, and a maturing carrier-neutral ecosystem around Johannesburg. Teraco and Africa Data Centres commission hyperscale pods that interconnect with Kenya, Nigeria, and Egypt via WACS and EASSy systems, furnishing distributed inference reach while maintaining strict data-protection observance. Government data-center tax allowances offset local-currency volatility, attracting foreign direct investment into Gauteng and Western Cape provinces.

Mordor Intelligence delivers a comprehensive view of the artificial intelligence (ai) data center market across all major regions such as North America, South America, and Europe, alongside country-level analysis for Saudi Arabia, South Africa, United Arab Emirates, Brazil, United States, and Spain, each offering a view of the local market realities.

Competitive Landscape

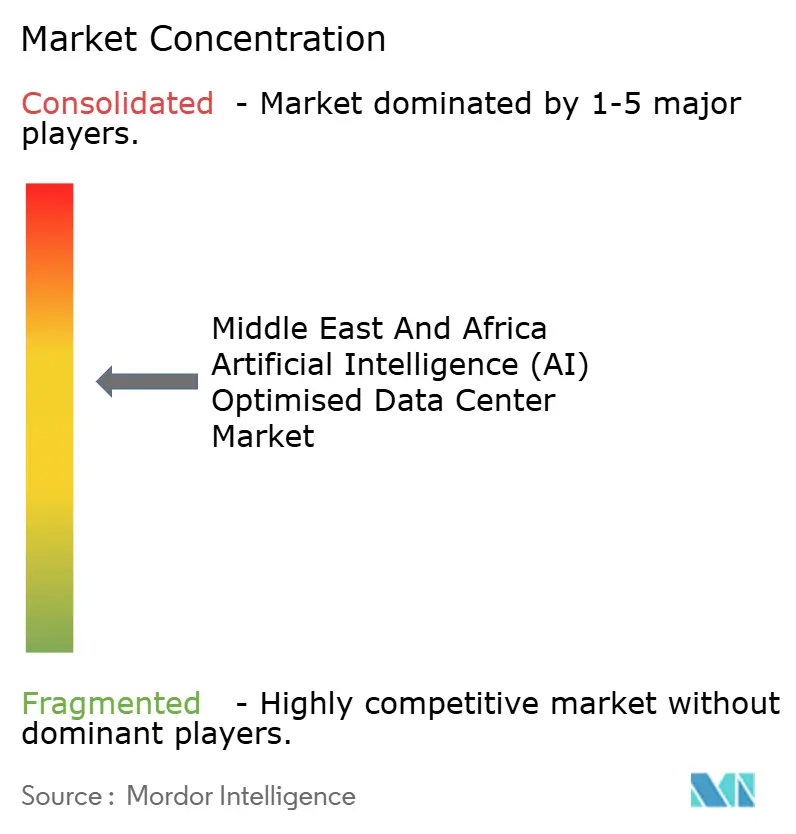

The market exhibits moderate concentration: hyperscalers dominate core AI workloads yet partner with regional specialists to meet sovereignty mandates. Amazon Web Services, Microsoft Azure, and Google Cloud scale Tier IV builds across Riyadh, Jeddah, Dubai, and Johannesburg, leveraging global procurement power to lock-in GPU supply. Regional champion G42 augments competitiveness through Condor Galaxy supercomputers and Arabic-first model catalogues that attract public-sector tenants seeking cultural relevance.

Colocation stalwarts Khazna, Teraco, and Africa Data Centres finance expansions via sale-and-leaseback vehicles and green bonds that tie interest rates to Power Usage Effectiveness metrics. Their neutral positioning garners multi-cloud interconnection and opens cross-border replication channels, enhancing resilience.

Edge-focused newcomers deploy modular immersion-cooled containers adjacent to 5G towers, winning contracts from telecom operators monetizing ultra-low-latency video analytics. Cooling-technology vendors pilot thermosyphon and heat-reuse systems in Gulf sites to navigate water-withdrawal caps, embedding sustainability as a competitive differentiator. Consequently, the blend of global scale and local specialization defines rivalry intensity, while regulatory heterogeneity preserves room for niche providers.

Middle East And Africa Artificial Intelligence (AI) Data Center Industry Leaders

Amazon Web Services, Inc.

Microsoft Corporation

Google LLC

Alibaba Cloud Computing Co., Ltd.

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Humain, a newly launched initiative backed by Saudi Arabia's sovereign wealth fund, has partnered with Cisco to develop large-scale AI data centers in Saudi Arabia. This collaboration is part of a broader effort that includes partnerships with major tech companies such as Nvidia, AMD, AWS, Qualcomm, and Groq. While Cisco's specific role in the data center projects has not been fully disclosed, the partnership underscores the Kingdom's commitment to advancing AI infrastructure as part of its Vision 2030 goals.

- March 2025: Cassava plans to implement Nvidia accelerated computing and AI software at its data centers in South Africa by June 2025, utilizing Nvidia Cloud Partner (NCP) reference architectures. Additionally, the company aims to expand these developments to its other data center facilities in Egypt, Kenya, Morocco, and Nigeria.

- December 2024: Africa50 injected USD 15 million into Raya Data Center for greenfield complexes powering Egypt’s Atlas Project.

- November 2024: Batelco and Qareeb Data Centers signed an MoU to build Bahrain’s first white-space campus within the Beyon Data Oasis hub.

Middle East And Africa Artificial Intelligence (AI) Data Center Market Report Scope

The research encompasses the full spectrum of AI applications in data centers, covering hyperscale, colocation, enterprise, and edge facilities. The analysis is segmented by component, distinguishing between hardware and software. Hardware considerations include power, cooling, networking, IT equipment, and more. Software technologies under scrutiny encompass machine learning, deep learning, natural language processing, and computer vision. The study also evaluates the geographical distribution of these applications.

Additionally, it assesses AI's influence on sustainability and carbon neutrality objectives. A comprehensive competitive landscape is presented, detailing market players engaged in AI-supportive infrastructure, encompassing both hardware and software utilized across various AI data center types. Market size is calculated in terms of revenue generated by products and solutions providers in the market, and forecasts are presented in USD Billion for each segment.

| Cloud Service Providers |

| Colocation Data Centers |

| Enterprise / On-Premises / Edge |

| Hardware | Power Infrastructure |

| Cooling Infrastructure | |

| IT Equipment | |

| Racks and Other Hardware | |

| Software | Technology |

| Machine Learning | |

| Deep Learning | |

| Natural Language Processing | |

| Computer Vision | |

| Services | Managed Services |

| Professional Services |

| Tier III |

| Tier IV |

| IT and ITES |

| Internet and Digital Media |

| Telecom Operators |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Manufacturing and Industrial IoT |

| Government and Defense |

| United Arab Emirates |

| Saudi Arabia |

| South Africa |

| Egypt |

| Rest of Middle East and Africa |

| By Data Center Type | Cloud Service Providers | |

| Colocation Data Centers | ||

| Enterprise / On-Premises / Edge | ||

| By Component | Hardware | Power Infrastructure |

| Cooling Infrastructure | ||

| IT Equipment | ||

| Racks and Other Hardware | ||

| Software | Technology | |

| Machine Learning | ||

| Deep Learning | ||

| Natural Language Processing | ||

| Computer Vision | ||

| Services | Managed Services | |

| Professional Services | ||

| By Tier Standard | Tier III | |

| Tier IV | ||

| By End-user Industry | IT and ITES | |

| Internet and Digital Media | ||

| Telecom Operators | ||

| Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial IoT | ||

| Government and Defense | ||

| By Region | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the Middle East and Africa artificial intelligence data center market by 2031?

The market is forecast to reach USD 8.24 billion by 2031.

Which country currently leads spending on AI-optimized data centers in the region?

Saudi Arabia held 31.10% of 2025 spending, the highest share.

Which data-center tier standard is expected to grow fastest?

Tier III facilities are forecast to post a 28.20% CAGR through 2031.

Why are colocation facilities expanding so rapidly?

Enterprises favor hybrid architectures that combine sovereign control with cloud connectivity, driving colocation to a 28.45% CAGR.

How is 5G deployment influencing AI data-center demand?

5G enables ultra-low-latency applications that require edge AI data centers positioned within metropolitan areas.

Page last updated on: