France Artificial Intelligence (AI) Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

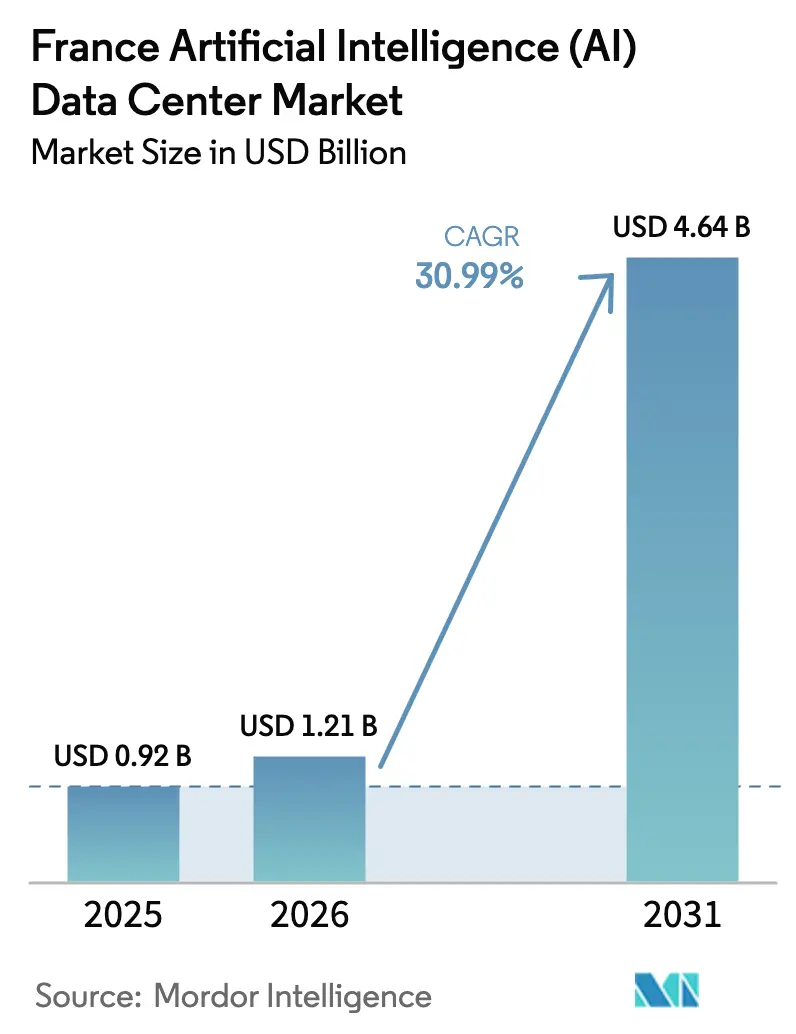

| Base Year Market Size (2025) | USD 0.92 Billion |

| Market Size (2026) | USD 1.21 Billion |

| Market Size (2031) | USD 4.64 Billion |

| Growth Rate (2026 - 2031) | 30.99% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

France Artificial Intelligence (AI) Data Center Market Analysis by Mordor Intelligence

The France artificial intelligence data center market size was valued at USD 0.92 billion in 2025 and estimated to grow from USD 1.21 billion in 2026 to reach USD 4.64 billion by 2031, at a CAGR of 30.99% during the forecast period (2026-2031). Rising generative-AI workloads, the country’s low-carbon nuclear and renewable energy mix, and targeted public incentives under the France 2030 program anchor this growth trend. Investors have announced more than EUR 109 billion (USD 117 billion) in new or expanded French facilities through 2030, signaling confidence that regulatory safeguards on data residency will continue to favor in-country processing. Operators are also prioritizing liquid-cooling retrofits and high-density power designs to host GPU clusters that consume 5-10 times more electricity than CPU-only racks. At the same time, grid-connection delays in Île-de-France and Marseille corridors are compelling providers to secure capacity early or pivot toward secondary metros where lead times are shorter.

Key Report Takeaways

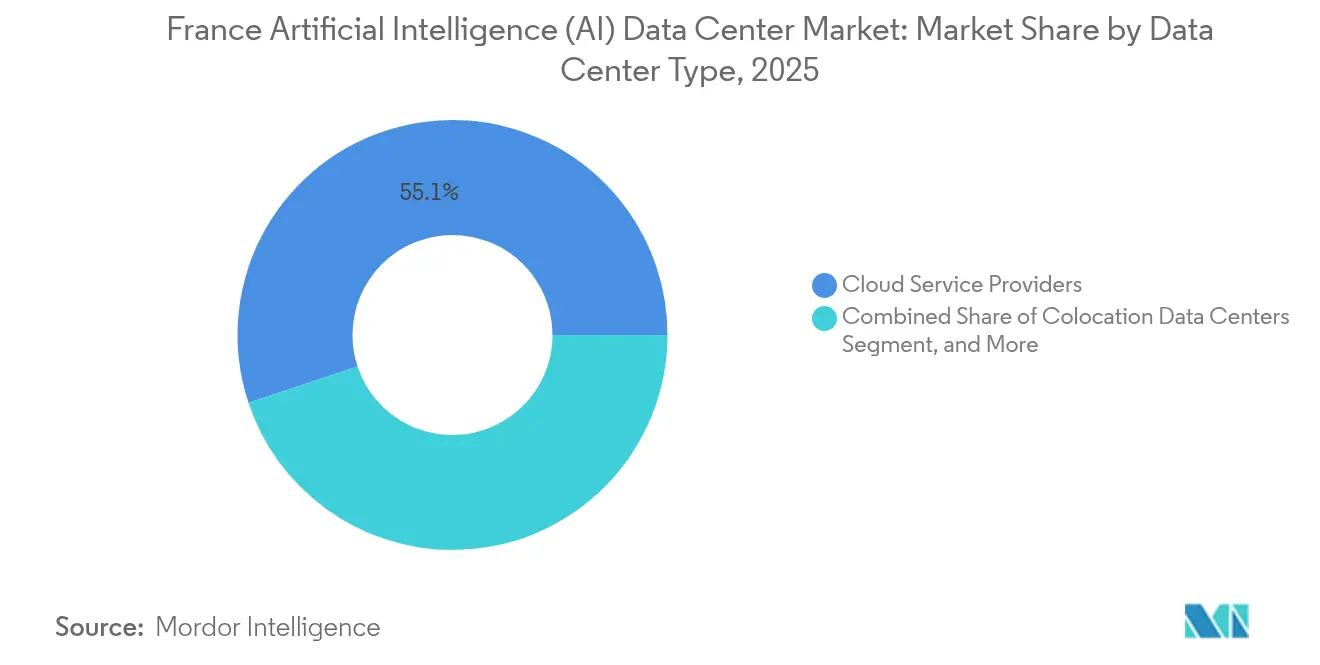

- By data center type, cloud service providers led with a 55.10% revenue share in 2025 in the France AI data center market, while colocation facilities are forecast to advance at a 33.6% CAGR through 2031.

- By component, software retained 45.20% share in 2025 in the France AI data center market, whereas hardware spending is projected to expand at a 32.92% CAGR over the same period.

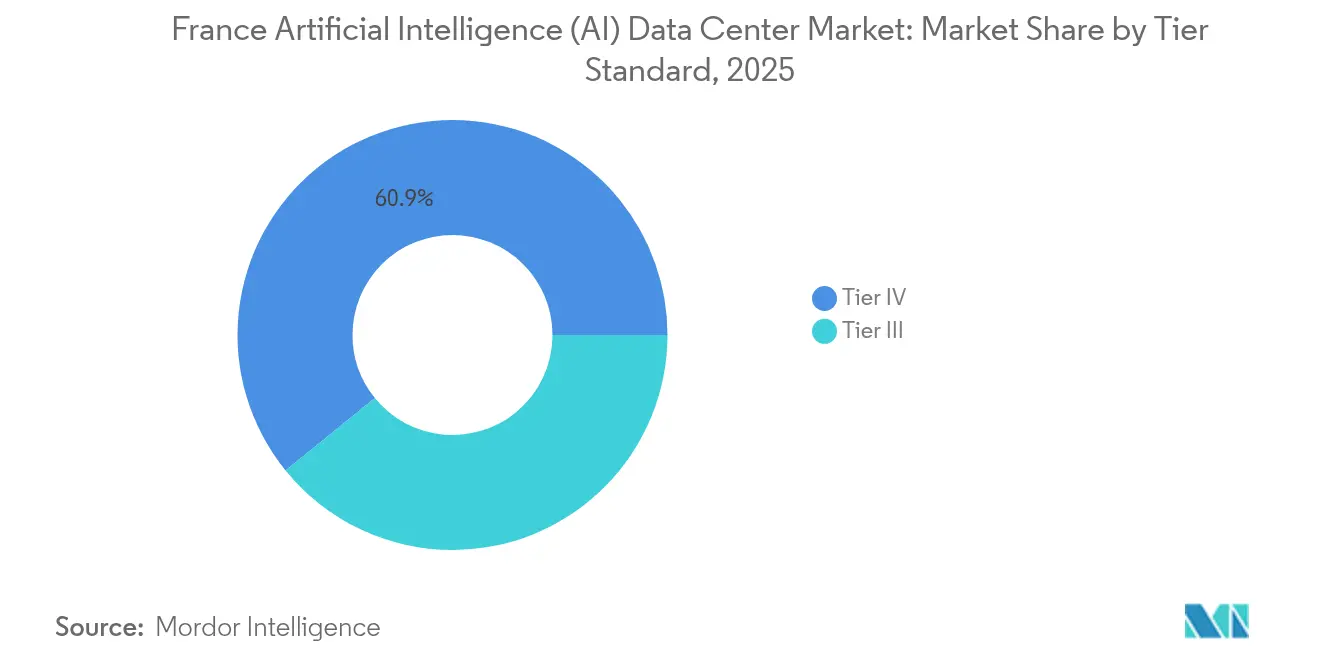

- By tier standard, Tier IV campuses accounted for 60.85% of capacity in 2025in the France AI data center market, yet Tier III sites are poised to grow at a 33.9% CAGR as edge deployments accelerate.

- By end-user, IT and ITES firms captured 33.10% of spending in 2025 in the France AI data center market, internet and digital-media platforms show the fastest trajectory at a 33.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

The pace and direction of global change depend on shifts occurring across countries and regions simultaneously, not within any one of them alone. The global artificial intelligence (ai) data center market outlook research of Mordor Intelligence reflects this combined progression.

France Artificial Intelligence (AI) Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acceleration of GPU-Hungry Gen-AI Workloads Toward Sovereign French Clouds | +8.5% | Global, with early gains in Paris, Lyon, Marseille | Medium term (2-4 years) |

| Abundant Nuclear and Renewable Energy Mix Enabling Low-Carbon AI Compute | +6.2% | National, with concentration in nuclear regions | Long term (≥ 4 years) |

| Government AI Investments via France 2030, Bpifrance and SIF Subsidies | +5.8% | National, with priority zones receiving enhanced support | Medium term (2-4 years) |

| Cool Northern and Western France Climate Supporting Economiser-Driven Free Cooling | +3.1% | Northern and Western regions, spill-over to temperate zones | Long term (≥ 4 years) |

| Rapid Uptake of AI-Optimised DC-Energy Management Platforms by French Operators | +4.2% | National, with early adoption in Tier III+ facilities | Short term (≤ 2 years) |

| Paris Region's Dense Dark-Fiber Backbone Fostering High-Density AI Clusters | +4.6% | Île-de-France core, extending to adjacent departments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Acceleration of GPU-Hungry Gen-AI Workloads Toward Sovereign French Clouds

Sovereign-cloud mandates are redirecting large language-model training and inference tasks back to domestic facilities that can guarantee data residency under EU-AI and CNIL rules. Microsoft’s EUR 4 billion (USD 4.4 billion) pledge to build two additional French regions underscores the scale of demand migration from Ireland and the Netherlands to France.[1]Microsoft News Center, “Microsoft investit 4 milliards d’euros dans l’IA et le cloud en France,” news.microsoft.com Under the PINM fast-track scheme, 35 pre-zoned greenfield sites now cut construction timelines from 36 to 18 months, giving domestic operators a first-mover edge. A further EUR 30–50 billion (USD 32–54 billion) from Middle-Eastern sovereign investors amplifies capital inflows.[2]Les Echos, “IA générative : la France veut accélérer sur les centres de données,” lesechos.fr In parallel, stricter localization clauses for AI in healthcare, finance, and public services ensure sustained workload stickiness.

Abundant Nuclear and Renewable Energy Mix Enabling Low-Carbon AI Compute

Nuclear and renewable power shares help French data centers publish among Europe’s lowest carbon intensity scores, a draw for ESG-driven hyperscalers. EDF’s 15-year agreements lock wholesale electricity prices through 2040, offering 15-25% operating-expense savings compared with gas-reliant peers in Germany or the United Kingdom.[3]EDF Group, “EDF signe des contrats long terme avec des opérateurs de centres de données,” edf.fr The government’s 2030 net-zero target further aligns with corporate mandates, pushing operators to invest in closed-loop liquid cooling and heat-recovery schemes that reduce water withdrawal by up to one-third. These energy advantages have become a decisive site-selection criterion for global AI tenants under pressure to publish scope-2 emissions cuts.

Government AI Investments via France 2030, Bpifrance and SIF Subsidies

The France 2030 roadmap allocates EUR 7.5 billion to AI, including EUR 2 billion in direct compute grants, while Bpifrance can fund up to 40% of capex for strategic infrastructure, terms that de-risk large-scale builds for both local and foreign investors. Regions such as Normandy and Hauts-de-France add incremental tax credits for energy-efficient campuses, whereas Provence-Alpes-Côte d’Azur accelerates permitting on projects above EUR 100 million. The 2024 AI-Action Summit secured 15 corporate letters of intent, locking in future demand for sovereign workloads hosted within French borders. Compliance oversight by CNIL and EU state-aid rules ensures transparency and prevents subsidy overreach.

Cool Northern and Western France Climate Supporting Economizer-Driven Free Cooling

Average annual temperatures below 12 °C in Brittany, Normandy and Hauts-de-France allow operators to run economizer modes for 2,500–3,000 hours per year, cutting chiller energy use by 20-30%. This climatic edge, combined with low land costs, has begun shifting site announcements away from Paris and Marseille toward northern ports such as Dunkirk and Le Havre. Operators also exploit seawater-based systems that circulate cool brine through heat exchangers, enhancing sustainability metrics. Economic development agencies in these regions advertise over 400 MW of immediately securable power, shortening time-to-market for AI clusters that need 20–50 MW per site.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-Connection Bottlenecks in Île-de-France and Marseille Corridors | -2.8% | Île-de-France and Marseille metropolitan areas | Short term (≤ 2 years) |

| Shortage of AI-Ready DC-Operations Talent Outside Major Hubs | -1.9% | Regional markets excluding Paris, Lyon, Toulouse | Medium term (2-4 years) |

| Lengthy ICPE and Environmental Permitting for Greenfield Campuses | -2.1% | National, with extended timelines in environmentally sensitive areas | Medium term (2-4 years) |

| High CAPEX for Liquid / Immersion-Cooling Retrofits in Legacy Sites | -1.6% | National, affecting older facilities built before 2020 | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Grid-Connection Bottlenecks in Île-de-France and Marseille Corridors

RTE is juggling more than 140 data-center interconnection requests totaling 21 GW, saturating substations that already serve 60% of national capacity within Île-de-France. AI-optimized halls need 4-5 times the power envelope of legacy rooms, driving wait times of 18–24 months for 20+ MW feeds. Marseille faces similar pressure as Europe’s sixth-largest landing station attracts new cables and edge nodes, yet the local grid remains sized for conventional commercial demand. Until EUR 3.2 billion in transmission upgrades land in 2028, operators must bank on redundant feeds or prioritize pre-approved brownfield plots with unused capacity.

Shortage of AI-Ready DC-Operations Talent Outside Major Hubs

INSEE counts 83,000 open ICT roles nationally, and data-center posts carry a 49% higher vacancy rate than the tech average. Skills in liquid cooling, high-amp busway deployment and GPU-cluster orchestration are scarce beyond Paris, Lyon and Toulouse, forcing secondary-city operators to import staff on rotational schedules. Although new university tracks with Schneider Electric and Vertiv will graduate cohorts from 2026, near-term staffing shortfalls threaten SLAs for Tier III and IV sites. Labor-law mandates on hazardous-material training further lengthen onboarding, driving wage inflation in provincial markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Sovereign Clouds Drive Colocation Growth

Cloud service providers held 55.10% of the France artificial intelligence data center market share in 2025 as AWS, Microsoft and Google expanded Paris-area regions to host regulated workloads. Colocation demand, however, is projected to outpace all other formats at a 33.6% CAGR to 2031. This surge means the France artificial intelligence data center market size attributed to colocation is on track to quadruple, buoyed by enterprises mixing public cloud agility with privately owned GPU clusters in shared halls.

Many French banks and healthcare groups lease suites inside Digital Realty and Equinix campuses to comply with CNIL guidelines yet preserve latencies under 5 ms for high-frequency AI inference. Secondary metros such as Lille and Bordeaux are seeing an influx of <10 MW facilities that serve manufacturing 4.0 and logistics clients requiring local autonomy during fiber disruptions. Providers differentiate through sovereign-cloud labels and dedicated dark-fiber cross-connects to Paris and Marseille exchanges.

By Component: Hardware Retrofits Accelerate Infrastructure Upgrades

Software frameworks still command 45.20% of spending as firms license machine-learning operations platforms and NLP pipelines, but hardware allocations will expand at a 32.92% CAGR, the fastest among all components. The France artificial intelligence data center market size devoted to power-delivery gear, chillers and liquid-cooling loops will therefore multiply, given that a single hall outfitted with NVIDIA H100 racks can draw 70–100 kW per cabinet.

Operators report 6–12-month lead times for switchgear and busways, prompting multi-year framework deals with Schneider Electric and ABB. Liquid-cooling retrofits often cost EUR 1,500–2,000 per kW, squeezing budgets in legacy Tier II rooms built before 2020. Yet improved PUE ratios below 1.25 offset capital outlays in under five years, especially with EDF fixed-price nuclear contracts that magnify kilowatt-hour savings.

By Tier Standard: Edge Applications Drive Tier III Expansion

Tier IV campuses owned by hyperscalers and French stock-exchange operators captured 60.85% of capacity in 2025, reflecting mission-critical payment and trading workloads. Nonetheless, Tier III footprints will rise at a 33.9% CAGR to accommodate edge cases where latency and cost trump five-nines redundancy. For these use cases, the France artificial intelligence data center market share commanded by Tier III institutions could exceed one-third by 2031 as manufacturers embed predictive-maintenance clusters on-site.

Retailers deploy Tier III micro-hubs within 10 km of urban stores to run computer-vision models for self-checkout, shrinkage analytics and last-mile route optimization. Regulatory nuances also matter: ICPE rules set lower staffing thresholds for Tier III, reducing operating expense. Meanwhile, campus operators deploy modular battery storage to soften grid-integration challenges and preserve uptime commitments.

By End-User Industry: Digital Media Fuels Content Generation Demand

IT and ITES firms accounted for 33.10% of 2025 spend, leveraging private AI sandboxes for software-development acceleration and round-the-clock help-desk chatbots. Internet and digital-media services, however, are forecast to expand at a 33.2% CAGR, the fastest among verticals. As a result, the France artificial intelligence data center industry is witnessing a wave of content-platform tenants reserving hundreds of petaflops for video upsizing, real-time dubbing and personalized recommendations.

Telecom carriers follow closely, pushing traffic-management models to the edge for sub-20 ms packet routing, while financial institutions ramp up anti-fraud engines that parse large streaming datasets without crossing borders. Healthcare uptake accelerates in imaging-heavy specialties, where AI inference cut CT scan read times by 40% in pilot studies at Paris hospitals. Compliance burdens such as HIPAA-equivalent laws require encrypted, in-country processing, which in turn keeps demand anchored to domestic halls.

Geography Analysis

Île-de-France houses roughly 60% of current capacity thanks to a dense dark-fiber backbone, global cloud headquarters and proximity to the country’s largest enterprise clients. The region’s growth, however, is moderating to a 26.9% CAGR as grid queues lengthen and land scarcity lifts per-acre costs above EUR 6 million. Operators with existing substations enjoy a lock-in advantage, but new entrants increasingly pivot to land parcels in inner-ring departments such as Seine-et-Marne and Essonne that still qualify for Île-de-France latency budgets.

Marseille ranks as the nation’s second hub, favored for its 15 subsea cables that terminate within 10 km of carrier-neutral sites. These links attract AI inference workloads needing real-time access to datasets in Africa, the Middle East and Asia. Yet water-consumption concerns and coastal-view preservation rules have sparked localized opposition, nudging newcomers toward inland communes like Gardanne where reclaimed industrial land eases permitting.

Northern and western regions, Normandy, Brittany and Hauts-de-France, are now labeled “ready-to-use” under the PINM framework. Average outdoor temperatures of 9–11 °C support free-cooling for up to two-thirds of the year, and nuclear plants at Flamanville and Gravelines guarantee low-carbon power contracts. These factors explain why the combined France artificial intelligence data center market size across secondary metros is forecast to grow at 34.2% CAGR through 2031, outpacing traditional hotspots.

Mordor Intelligence examines the artificial intelligence (ai) data center market across diverse other regional markets as well, including Europe, South America, and Asia, while also offering granular country-level perspectives for Spain, Netherlands, Brazil, Singapore, Thailand, and Australia and more.

Competitive Landscape

AWS leads with a 46% share by installed AI compute and continues to pre-lease brownfield halls near Paris for 2026-onward availability. Microsoft holds 17% and is adding Lyon and Toulouse regions that target government workloads requiring sovereign isolation. Google’s 8% slice belies strong influence through partnerships with French research institutes that shape industry standards.

Domestic champion OVHcloud leverages GDPR heritage to secure defense and public-sector contracts; it recently unveiled a Paris GPU cluster service priced 20% below U.S. peers. Scaleway differentiates with minute-based billing for NVIDIA H100 nodes, attracting startups focused on text-to-video generation. Data4, now under Digital Realty, supplies colocation shells fitted for 2,000 W/ft² densities, enabling financial clients to bring their own immersion tanks.

Emerging challengers are flush with non-EU capital: Sesterce, backed by ADQ, plans 12 AI-optimized campuses by 2028, while Nebius targets Russian-language model training that U.S. clouds increasingly restrict. Technology leadership favors operators that deploy AI-driven DCIM suites to trim PUEs below 1.25; Schneider Electric’s EcoStruxure AI has already yielded 15-20% energy savings in French pilots. Competitive tension is likely to intensify as grid constraints allocate scarce megawatts to players able to demonstrate superior energy and community footprints.

France Artificial Intelligence (AI) Data Center Industry Leaders

-

NVIDIA Corporation

-

Schneider Electric SE

-

Intel Corporation

-

Advanced Micro Devices, Inc.

-

Vertiv Group Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: French cloud provider Sesterce will invest USD 471.85 million in a new AI data center in Valence, France. The center, located in the Rovaltain business park, will house 40,000 GPUs for AI operations. Its water-cooling system will reuse waste heat. The center will open by 2026. Sesterce aims to build 1.5GW of compute power in France and install 1.2 million GPUs by 2030.

- February 2025: France and the United Arab Emirates plan to invest USD 31-52 billion in a 1GW data center and additional artificial intelligence infrastructure. The project is expected to enhance France's data center industry by increasing storage capacity, improving data processing capabilities, and establishing new facilities across the country. This development will likely attract more international technology companies to host their operations in France, leading to increased demand for data center services and supporting infrastructure. The investment is also anticipated to drive technological advancements in data center design, energy efficiency, and sustainable operations within the French market.

- December 2024: Digital Realty acquired Data4’s Paris campus for EUR 800 million to scale colocation for regulated sectors.

- November 2024: EDF signed 15-year nuclear power purchase agreements with five large operators, fixing energy prices through 2040.

France Artificial Intelligence (AI) Data Center Market Report Scope

The research encompasses the full spectrum of AI applications in data centers, covering hyperscale, colocation, enterprise, and edge facilities. The analysis is segmented by component, distinguishing between hardware and software. Hardware considerations include power, cooling, networking, IT equipment, and more. Software technologies under scrutiny encompass machine learning, deep learning, natural language processing, and computer vision. The study also evaluates the geographical distribution of these applications. Additionally, it assesses AI's influence on sustainability and carbon neutrality objectives. A comprehensive competitive landscape is presented, detailing market players engaged in AI-supportive infrastructure, encompassing both hardware and software utilized across various AI data center types. Market size is calculated in terms of revenue generated by products and solutions providers in the market and forecasts are presented in USD Billion for each segment.

| Cloud Service Providers |

| Colocation Data Centers |

| Enterprise / On-Premises / Edge |

| Hardware | Power Infrastructure |

| Cooling Infrastructure | |

| IT Equipment | |

| Racks and Other Hardware | |

| Software Technology | Machine Learning |

| Deep Learning | |

| Natural Language Processing | |

| Computer Vision | |

| Services | Managed Services |

| Professional Services |

| Tier III |

| Tier IV |

| IT and ITES |

| Internet and Digital Media |

| Telecom Operators |

| BFSI |

| Healthcare and Life Sciences |

| Manufacturing and Industrial IoT |

| Government and Defense |

| By Data Center Type | Cloud Service Providers | |

| Colocation Data Centers | ||

| Enterprise / On-Premises / Edge | ||

| By Component | Hardware | Power Infrastructure |

| Cooling Infrastructure | ||

| IT Equipment | ||

| Racks and Other Hardware | ||

| Software Technology | Machine Learning | |

| Deep Learning | ||

| Natural Language Processing | ||

| Computer Vision | ||

| Services | Managed Services | |

| Professional Services | ||

| By Tier Standard | Tier III | |

| Tier IV | ||

| By End-user Industry | IT and ITES | |

| Internet and Digital Media | ||

| Telecom Operators | ||

| BFSI | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial IoT | ||

| Government and Defense | ||

Key Questions Answered in the Report

How large is the France artificial intelligence data center market in 2026?

It generated USD 1.21 billion of revenue in 2026 and is forecast to hit USD 4.64 billion by 2031, reflecting a 30.99% CAGR.

Which data center type is growing fastest for AI workloads in France?

Colocation sites are projected to expand at a 33.6% CAGR through 2031 as enterprises pursue hybrid deployment models.

Why is France attractive for low-carbon AI compute?

A power mix of 41% nuclear and 30% renewables provides 24/7 low-emission electricity, reinforced by long-term fixed-price contracts from EDF.

What are the main growth restraints for new French AI facilities?

Grid-connection delays in Paris and Marseille corridors and a nationwide shortage of advanced data-center talent pose near-term hurdles.

Which region outside Paris is emerging as a secondary AI hub?

Marseille is gaining share due to its 15 subsea cable landings that connect European AI clusters with Africa, the Middle East and Asia.

Page last updated on: