South Africa Artificial Intelligence (AI) Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

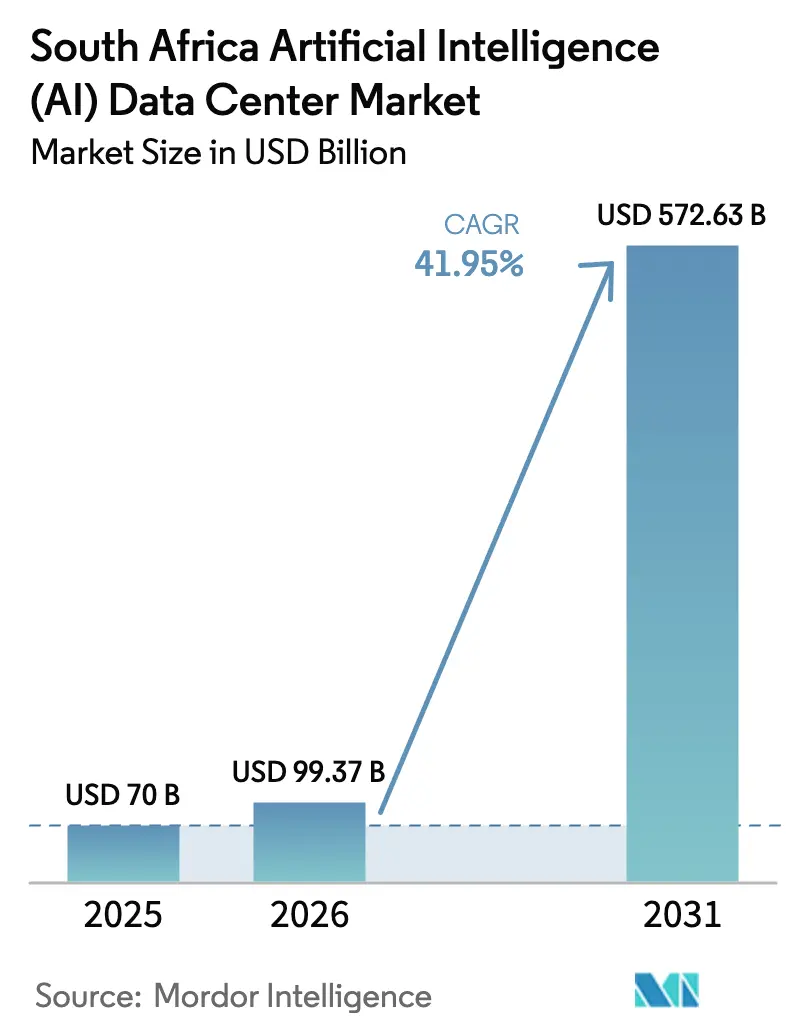

| Base Year Market Size (2025) | USD 70 Billion |

| Market Size (2026) | USD 99.37 Billion |

| Market Size (2031) | USD 572.63 Billion |

| Growth Rate (2026 - 2031) | 41.95% CAGR |

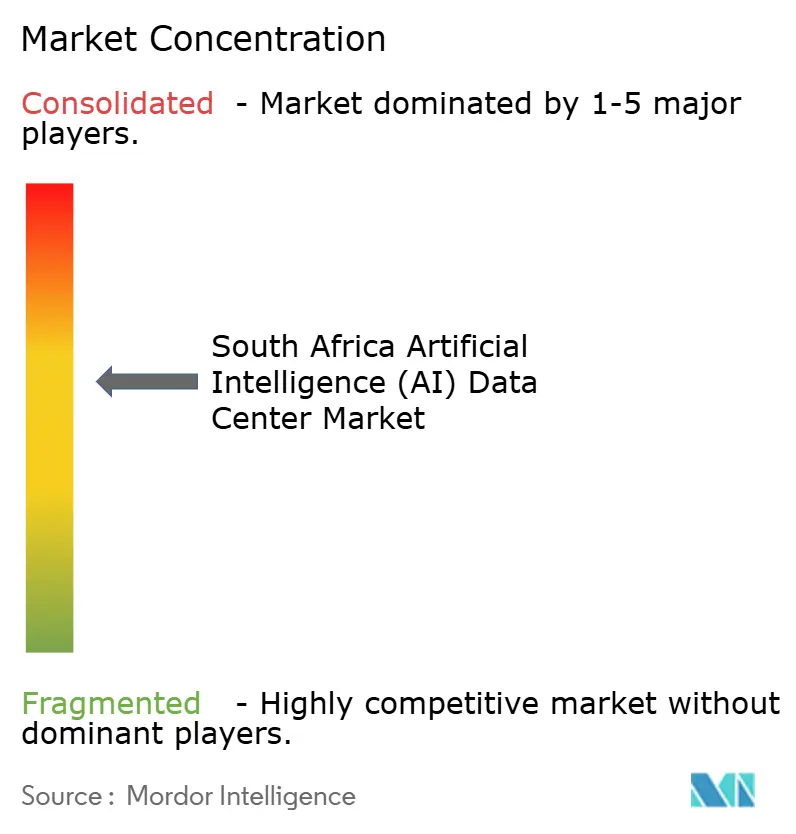

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Artificial Intelligence (AI) Data Center Market Analysis by Mordor Intelligence

The South Africa artificial intelligence data center market size is expected to grow from USD 70 million in 2025 to USD 99.37 million in 2026 and is forecast to reach USD 572.63 million by 2031 at 41.95% CAGR over 2026-2031. Rapid hyperscaler capital inflows, a well-articulated National AI Strategy, and grid modernization incentives position South Africa at the center of sub-Saharan AI infrastructure development. Enterprise and government demand for sovereign cloud regions, the acceleration of 5G-enabled edge workloads, and virtual-wheeling rules that unlock long-term renewable power purchase agreements further expand growth prospects. Competitive momentum is reinforced by hardware partnerships that secure GPU supply, while energy-efficient cooling innovations mitigate resource constraints. These elements collectively support the South Africa artificial intelligence data center market as a preferred landing point for African AI workload consolidation.

Key Report Takeaways

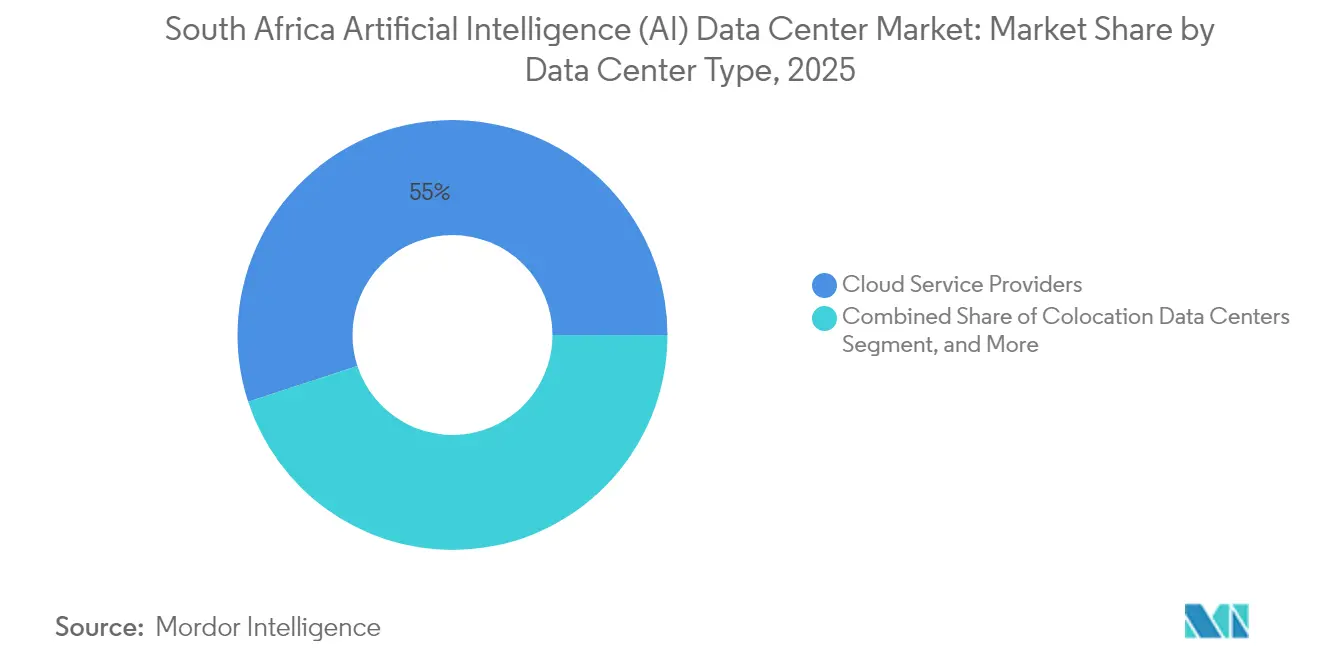

- By data center type, Cloud Service Providers led the South African artificial intelligence data center market with a 55.02% revenue share in 2025; Colocation Data Centers are projected to advance at a 45.14% CAGR through 2031.

- By component, Software accounted for 45.05% of the South Africa artificial intelligence data center market share in 2025, while Hardware is poised for the fastest growth at 45.2% CAGR to 2031.

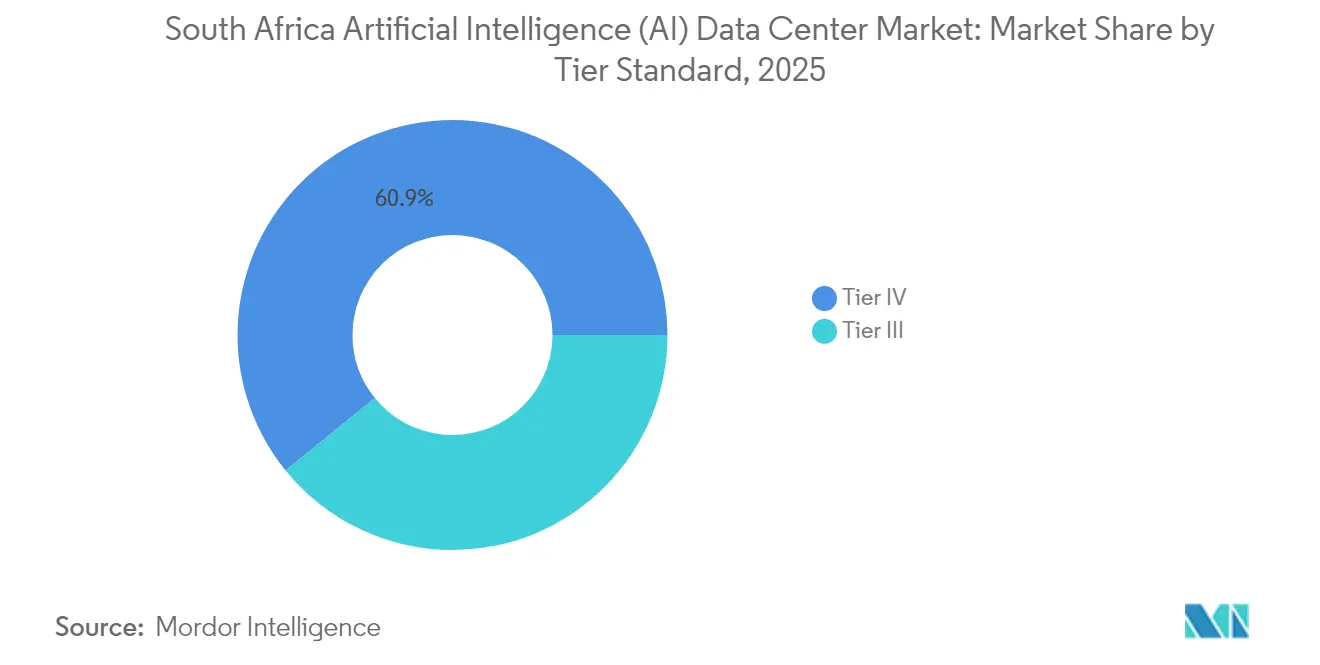

- By tier standard, Tier IV facilities captured a 60.85% share of the South African artificial intelligence data center market size in 2025; Tier III deployments are projected to climb at a 45.3% CAGR through 2031.

- By end-user industry, IT and ITES held a 33.21% share of the South Africa artificial intelligence data center market in 2025, whereas Internet and Digital Media workloads are expanding at a 42.8% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide industry scale is not derived from any single country or region but from the combination of national and regional inputs. The artificial intelligence (ai) data center market size of Mordor Intelligence integrates these into one global valuation.

South Africa Artificial Intelligence (AI) Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscaler capital inflows accelerating multi-MW campus build-outs | +12.5% | National, concentrated in Gauteng and Western Cape | Medium term (2-4 years) |

| Cloud-first enterprise and government digital transformation surge | +8.7% | National, with early gains in Johannesburg, Cape Town, Durban | Short term (≤ 2 years) |

| 5G rollout fuelling edge-AI and low-latency workload demand | +7.2% | National, urban centers prioritized | Medium term (2-4 years) |

| National AI Strategy targeting ZAR 70 billion investment by 2030 | +6.8% | National | Long term (≥ 4 years) |

| Virtual-wheeling rules unlocking long-term renewable PPAs for DCs | +4.9% | National, particularly beneficial for Western Cape and Northern Cape | Medium term (2-4 years) |

| NVIDIA DGX-Ready colocation partnerships lowering AI entry barriers | +3.1% | National, concentrated in major data center hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Hyperscaler Capital Inflows Accelerating Multi-MW Campus Build-outs

Hyperscaler commitments topping USD 3 billion are reshaping facility scale across Gauteng and Western Cape. Microsoft’s ZAR 5.4 billion expansion and AWS’s USD 1.7 billion investment in the Cape Town region raise the bar for single-site capacity, prompting local suppliers to upgrade their fiber backbones and on-site substations.[1]Microsoft South Africa, “Microsoft Announces ZAR 5.4 Billion Investment in South Africa to Accelerate Digital Transformation,” news.microsoft.com Google’s Johannesburg cloud region optimizes latency-sensitive AI workloads, and procurement volumes enable downstream providers to negotiate more favorable GPU pricing. The resulting economies of scale compress deployment timelines and enhance the competitiveness of the South African artificial intelligence data center market across the continent.

Cloud-First Enterprise and Government Digital Transformation Surge

Virtual-wheeling regulations enacted in 2024 allow data centers to source renewable power directly, giving enterprises confidence to migrate sensitive workloads. Financial institutions such as Standard Bank saved ZAR 1.1 billion through AI-driven fraud detection, showcasing tangible ROI. Parallel modernization programs at the State Information Technology Agency accelerate the migration of legacy applications into AI-ready facilities. Defense spending through the DAIRU program injects R51.8 billion into sovereign AI R&D, adding a secure government demand base. Collectively, these initiatives shorten sales cycles and deepen utilization rates for AI-optimized capacity.

5G Rollout Fueling Edge-AI and Low-Latency Workload Demand

MTN’s 44% population coverage, combined with 8.6 Gbps 5.5G trials, elevates South Africa into the global top tier for mobile broadband performance.[2]MTN Group, “Annual Reports and Financial Results 2024,” mtn.com Low-latency industrial cases, predictive maintenance in manufacturing, autonomous haulage in mining, and real-time video analytics require compute locations within 50 km of endpoints. Telecom operators such as Vodacom leverage Microsoft edge nodes to automate network optimization, simultaneously acting as infrastructure suppliers and anchor tenants. Demand for micro-data centers expands the total addressable footprint beyond Johannesburg and Cape Town, distributing revenue opportunities across second-tier cities.

National AI Strategy Targeting ZAR 70 Billion Investment by 2030

The National AI Strategy offers tax incentives on projects above R100 million, streamlines environmental approvals, and mandates AI readiness for public-sector ICT procurements.[3]Department of Science and Innovation, “Artificial Intelligence Strategy for South Africa,” dst.gov.za University research clusters require on-shore compute to comply with data-sovereignty clauses, further stimulating capacity additions. Concessional finance from multilateral development banks fills early-stage funding gaps, lowering the weighted cost of capital for greenfield builds. The policy clarity widens the investor pool and stabilizes the forecast for the South African artificial intelligence data center market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Eskom grid unreliability and recurring load-shedding risk | -8.3% | National, most severe in Gauteng and KwaZulu-Natal | Short term (≤ 2 years) |

| High capex/opex for extreme-density power and advanced liquid cooling | -6.1% | National, concentrated in major data center hubs | Medium term (2-4 years) |

| GPU supply-chain bottlenecks inflating hardware lead-times and costs | -4.7% | Global supply chain, affecting all regions | Short term (≤ 2 years) |

| Water-scarcity constraints on large-scale evaporative cooling in Gauteng and Western Cape | -3.4% | Gauteng and Western Cape provinces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Eskom Grid Unreliability and Recurring Load-Shedding Risk

Stage-4 outages persisted for 89 days in 2024, forcing data centers to divert up to 15% of opex to diesel generation. Operators now carry 48-hour fuel reserves and invest in dual-feed substations, raising capex hurdles versus peer markets. Teraco’s 120 MW solar-plus-storage program lowers exposure but requires upfront spending exceeding R2 billion. Transmission bottlenecks limit renewable integration to roughly 2 GW nationally, resulting in short-term reliance on carbon-intensive peaking plants. These factors compress margins and extend payback periods even as demand rises.

High Capex/Opex for Extreme-Density Power and Advanced Liquid Cooling

GPU racks exceeding 40 kW require liquid or immersion cooling, which adds 35–50% to the first-cost outlays. Schneider Electric’s hybrid units deliver 75% energy savings but require an investment of R5–8 million per 100 kW of cooling capacity. Scarcity of certified technicians elevates service contracts by 20–25%, and the limited domestic supply chain for dielectric fluids amplifies opex volatility. For smaller operators, these economics impede competitive positioning against hyperscaler self-builds.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Colocation Momentum Builds on Hyperscaler Footprint

The South African artificial intelligence data center market size for Cloud Service Providers was led by a 55.02% share in 2025, reflecting the USD 3 billion collective commitments of Microsoft, AWS, and Google. Colocation facilities are now projected to post a 45.14% CAGR through 2031, as enterprises pursue hybrid architectures that blend sovereign control with hyperscaler compatibility. Africa Data Centers’ Cape Town project raises installed capacity from 30 MW to 50 MW, illustrating sustained capex appetite among neutral hosts.

Colocation providers leverage carrier neutrality to aggregate traffic from 5G edge nodes, content delivery networks, and fintech ecosystems. Renewable energy-as-a-service options, enabled by virtual-wheeling rules, further differentiate offers. The proliferation of distributed inference workloads widens geographic coverage requirements, prompting the need for micro-colocation pods in Durban and Port Elizabeth. These trends position third-party capacity as a pivotal growth lever across the South Africa artificial intelligence data center market.

By Component: Hardware Upswing Follows GPU Supply Stabilization

Software retained 45.05% of the South Africa artificial intelligence data center market share in 2025, driven by rapid SaaS adoption for language models, fraud detection, and predictive analytics. Yet hardware is forecast to outpace all other components at 45.2% CAGR, underpinned by NVIDIA DGX SuperPOD deployments and custom accelerator orders from telecom operators. Power and cooling infrastructure upgrades track this momentum, with immersion tanks designed for 200 kW loads gaining acceptance.

The services layer captures value through design-build contracts, GPU cluster orchestration, and MLOps management, especially as enterprises confront skills gaps. Altron’s turnkey offerings exemplify how integrators mitigate adoption hurdles by bundling hardware, software, and managed operations. The combined pull of hardware acceleration and services optimization reinforces the capital cycle for the South Africa artificial intelligence data center industry.

By Tier Standard: Tier III Designs Address Distributed AI Needs

Tier IV builds commanded 60.85% of 2025 capacity, a reflection of hyperscaler requirements for fault tolerance. Nonetheless, Tier III is projected to log a 45.3% CAGR as operators balance uptime against capital intensity. Uptime Institute’s concurrently maintainable criteria meet 99.982% availability expectations while reducing redundancy overhead, making them appealing for edge and regional deployments.

Edge inference for mining and manufacturing tolerates brief maintenance windows, making Tier III the preferred topology outside metropolitan hubs. Certification scarcity provides early-mover advantage for any provider achieving formal Tier III or IV recognition, opening doors to regulated industries such as banking and healthcare. Diverse workload criticality levels thereby foster a layered tier mix across the South Africa artificial intelligence data center market.

By End-User Industry: Digital Media Surge Reorders Demand Patterns

IT and ITES sectors still represented 33.21% of end-user demand in 2025, anchored by cloud migration projects and fintech innovation. However, Internet and Digital Media workloads are advancing at 42.8% CAGR, buoyed by generative AI for content creation and real-time OTT streaming personalization. Standard Bank’s AI fraud savings validate ROI in financial services, while Discovery Health’s AI claims processing extends adoption into healthcare.

Manufacturing sees uptake in computer-vision quality control, and telecom players deploy AI for customer-experience automation. Government and defense allocations, typified by the DAIRU program, add sovereign workloads that must reside on-shore. These diverse verticals ensure balanced utilization profiles throughout the South Africa artificial intelligence data center market.

Geography Analysis

Hyperscaler investments exceeding USD 3 billion solidify Gauteng and Western Cape as the nucleus of the South Africa artificial intelligence data center market. Johannesburg hosts the majority of hyperscale campuses, which leverage dense fiber routes and meet the financial services demand. Cape Town benefits from subsea cable landings and renewable-rich grids, enabling operators to secure long-term green PPAs that lower levelized energy costs.

Secondary metros such as Durban and Port Elizabeth emerge as edge-AI staging grounds, serving manufacturing corridors and logistics hubs that require low-latency inference. Virtual-wheeling policies extend renewable access beyond Eskom’s centralized model, fostering competitive electricity pricing for distributed builds. Collectively, the geographic diversification strengthens national resilience while expanding total capacity across the South Africa artificial intelligence data center market.

South Africa’s operational expertise in balancing load-shedding, water scarcity, and grid decarbonization presents a transferable blueprint for neighboring states. Cross-border collaborations are already emerging through pan-African initiatives led by Cassava Technologies and Africa Data Centers. As a result, local operators position domestic facilities as staging nodes for the redistribution of continental AI workloads, thereby reinforcing South Africa’s role as a gateway to sub-Saharan Africa.

Mordor Intelligence tracks the artificial intelligence (ai) data center market across other major regions such as Europe, Asia, and Middle East and Africa, with additional country-level coverage spanning Netherlands, Indonesia, Saudi Arabia, Spain, Canada, and Germany, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

The market exhibits moderate concentration, with Teraco, Africa Data Centers, and NTT holding the largest market share. Teraco secured R8 billion for its JB7 expansion, adding 40 MW of AI-ready capacity and achieving a 1.47 PUE and 0.05 L/kWh water intensity benchmark. Africa Data Centers secured R2 billion in financing to double its Cape Town capacity, underscoring investor confidence despite macroeconomic and energy headwinds.

New entrants, such as Vantage Data Centers and Digital Parks Africa, pursue greenfield campuses, leveraging modular construction for rapid scaling. Cassava Technologies differentiates through vertical integration, coupling NVIDIA DGX SuperPOD hardware with sovereign AI services. Edge specialists, such as 4Sight Holdings, target the mining and oil-and-gas verticals with ruggedized micro-facilities, while telecom tower owners explore colocation extensions to monetize their existing locations. Cooling innovation and renewable procurement are emerging as key battlegrounds for competitive advantage, with operators racing to secure PPAs before transmission capacity is saturated.

Strategic moves solidify positioning: Teraco’s long-term solar-plus-storage contract shields opex against diesel volatility, Africa Data Centers’ modular edge design cuts build cycles by 30%, and NTT’s partnership with MTN accelerates hybrid-cloud onboarding for enterprise customers. These maneuvers collectively elevate performance benchmarks and raise barriers for late entrants into the South Africa artificial intelligence data center market.

South Africa Artificial Intelligence (AI) Data Center Industry Leaders

Teraco Data Environments (Pty) Ltd.

Africa Data Centres (Pty) Ltd.

NTT Global Data Centers EMEA Ltd. (South Africa)

Vantage Data Centers, LLC

Business Connexion (Pty) Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Altron Arrow secured rights to distribute ASUS AI GPU hardware, easing domestic supply constraints.

- June 2025: Cassava Technologies completed deployment of NVIDIA DGX SuperPOD, branding it Africa’s first “AI factory”.

- April 2025: Dell Technologies and NVIDIA expanded their collaboration to provide PC-to-data-center AI solutions locally.

- March 2025: Schneider Electric South Africa released hybrid cooling units, achieving 75% energy savings for GPU racks.

- February 2025: 4Sight Holdings partnered with Armada to deliver satellite-connected modular edge data centers for mining operations.

- January 2025: Open Access Data Centers announced comprehensive upgrades to accommodate high-density AI compute.

South Africa Artificial Intelligence (AI) Data Center Market Report Scope

The research encompasses the full spectrum of AI applications in data centers, covering hyperscale, colocation, enterprise, and edge facilities. The analysis is segmented by component, distinguishing between hardware and software. Hardware considerations include power, cooling, networking, IT equipment, and more. Software technologies under scrutiny encompass machine learning, deep learning, natural language processing, and computer vision. The study also evaluates the geographical distribution of these applications.

Additionally, it assesses AI's influence on sustainability and carbon neutrality objectives. A comprehensive competitive landscape is presented, detailing market players engaged in AI-supportive infrastructure, encompassing both hardware and software utilized across various AI data center types. Market size is calculated in terms of revenue generated by products and solutions providers in the market, and forecasts are presented in USD Billion for each segment.

| Cloud Service Providers |

| Colocation Data Centers |

| Enterprise / On-Premises / Edge |

| Hardware | Power Infrastructure |

| Cooling Infrastructure | |

| IT Equipment | |

| Racks and Other Hardware | |

| Software | Technology |

| Machine Learning | |

| Deep Learning | |

| Natural Language Processing | |

| Computer Vision | |

| Services | Managed Services |

| Professional Services |

| Tier III |

| Tier IV |

| IT and ITES |

| Internet and Digital Media |

| Telecom Operators |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Manufacturing and Industrial IoT |

| Government and Defense |

| By Data Center Type | Cloud Service Providers | |

| Colocation Data Centers | ||

| Enterprise / On-Premises / Edge | ||

| By Component | Hardware | Power Infrastructure |

| Cooling Infrastructure | ||

| IT Equipment | ||

| Racks and Other Hardware | ||

| Software | Technology | |

| Machine Learning | ||

| Deep Learning | ||

| Natural Language Processing | ||

| Computer Vision | ||

| Services | Managed Services | |

| Professional Services | ||

| By Tier Standard | Tier III | |

| Tier IV | ||

| By End-user Industry | IT and ITES | |

| Internet and Digital Media | ||

| Telecom Operators | ||

| Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial IoT | ||

| Government and Defense | ||

Key Questions Answered in the Report

How large is the South Africa artificial intelligence data center market in 2026?

The market stands at USD 99.37 million in 2026 and is forecast to reach USD 572.63 million by 2031.

What is the projected CAGR for AI data centers in South Africa?

The sector is forecast to register a 41.95% CAGR between 2026 and 2031.

Which data center type is expanding fastest?

Colocation Data Centers lead growth with a projected 45.14% CAGR, driven by enterprise hybrid-cloud adoption.

Why are hardware investments accelerating?

GPU cluster deployments and liquid-cooling upgrades are pushing Hardware to a 45.2% CAGR, outpacing Software growth.

How are power reliability challenges being addressed?

Operators deploy on-site solar-plus-storage, enter renewable PPAs via virtual-wheeling, and maintain diesel reserves for resilience.

What role does the National AI Strategy play?

It offers tax incentives, streamlined approvals, and a ZAR 70 billion investment target, creating a stable policy backdrop for new builds.

Page last updated on: