Australia Artificial Intelligence (AI) Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

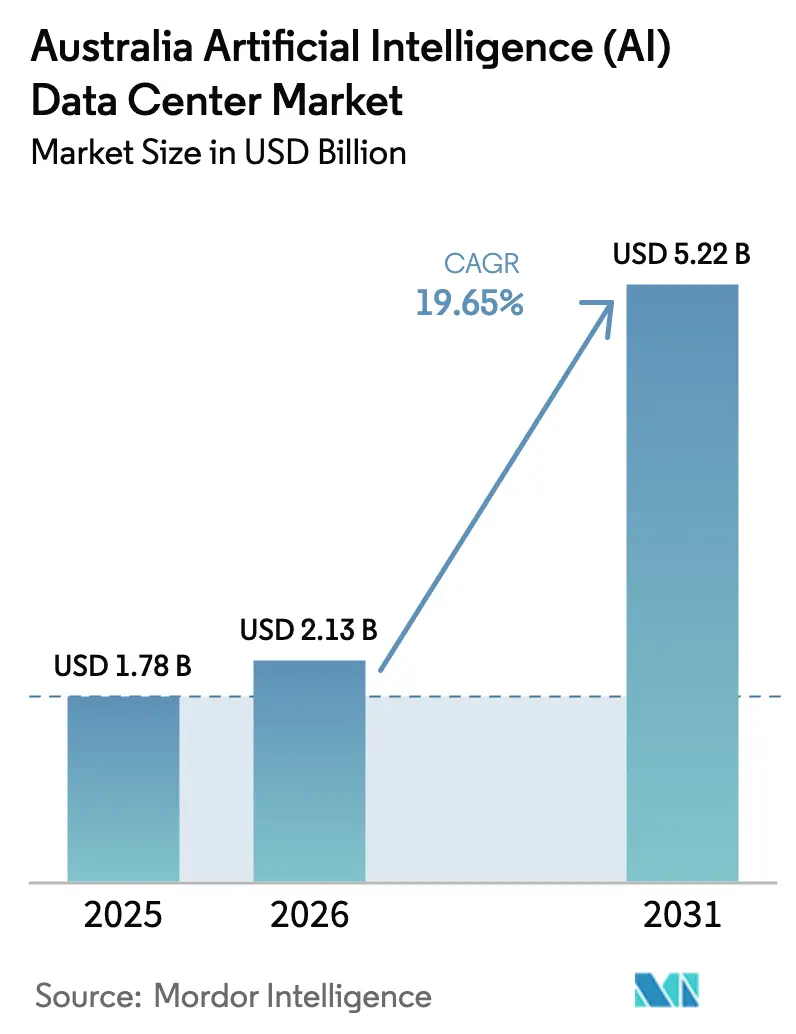

| Base Year Market Size (2025) | USD 1.78 Billion |

| Market Size (2026) | USD 2.13 Billion |

| Market Size (2031) | USD 5.22 Billion |

| Growth Rate (2026 - 2031) | 19.65% CAGR |

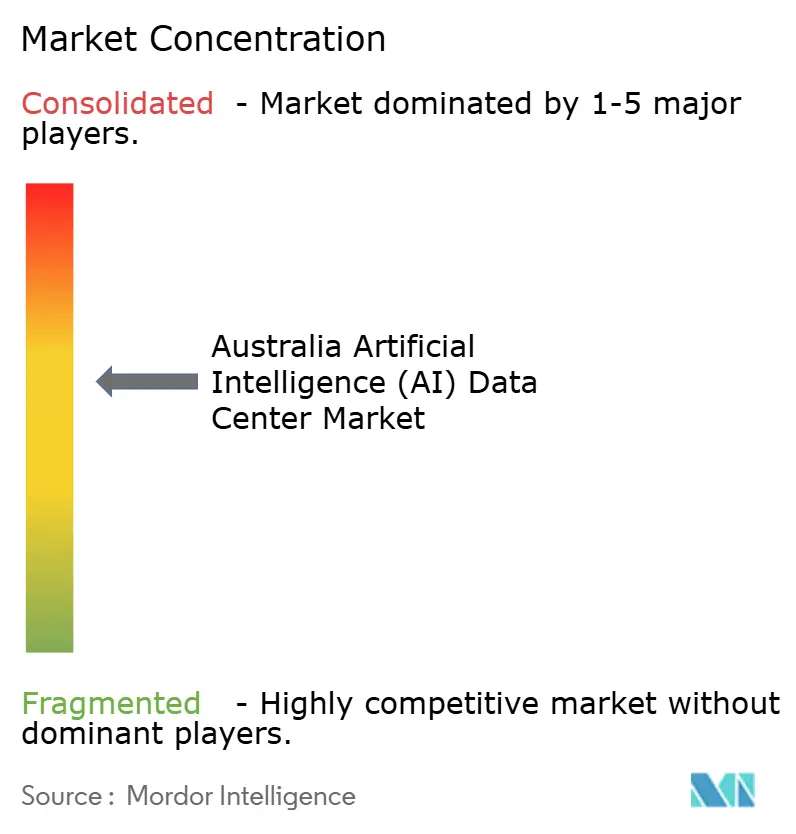

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Artificial Intelligence (AI) Data Center Market Analysis by Mordor Intelligence

The Australian artificial intelligence data center market size was valued at USD 1.78 billion in 2025 and estimated to grow from USD 2.13 billion in 2026 to reach USD 5.22 billion by 2031, at a CAGR of 19.65% during the forecast period (2026-2031). A trio of structural forces, unrestricted GPU imports, government data-sovereignty mandates, and accelerating hyperscale capital outlays, anchors this expansion. Cloud service providers already dominate capacity; however, colocation facilities are scaling faster as enterprises adopt hybrid deployment models. Hardware-related spending is rising even quicker than software outlays because liquid cooling, high-density racks, and redundant power upgrades have become prerequisites for training large language models. Finally, utilities in Sydney and Melbourne face mounting grid congestion, prompting operators to secure renewable power purchase agreements and evaluate secondary metropolitan areas for green-field builds.

Key Report Takeaways

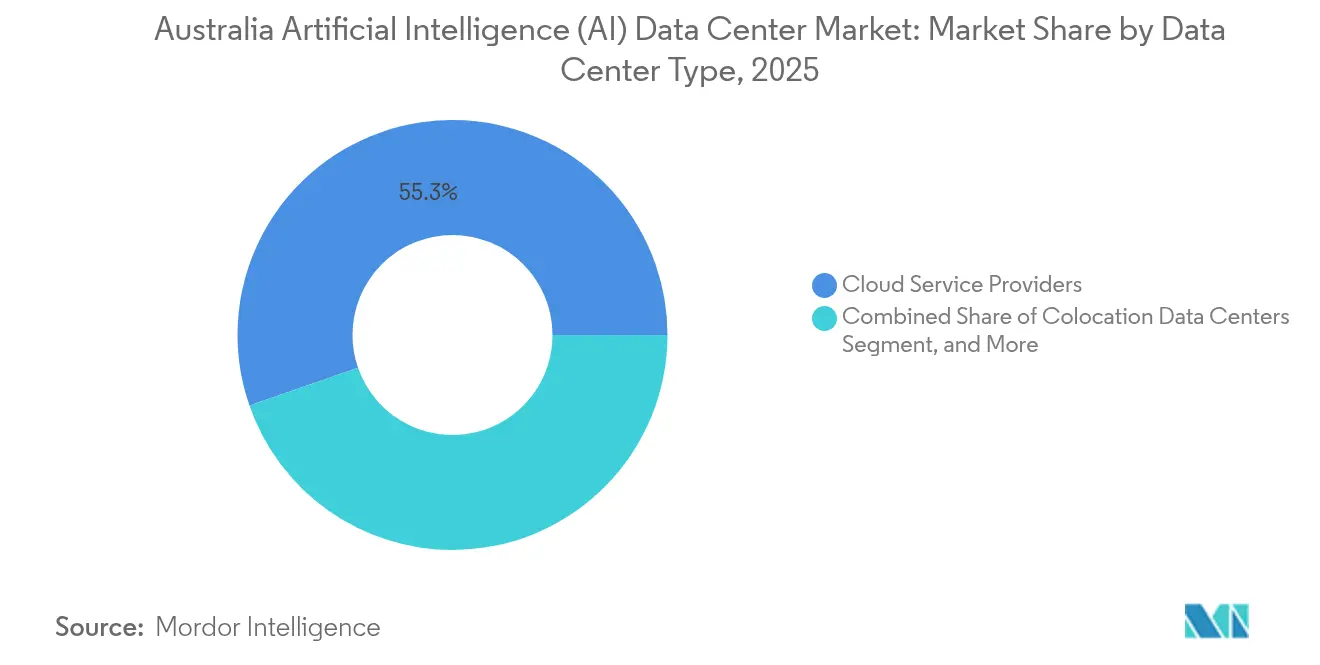

- By data center type, cloud service providers held 55.32% of the Australian artificial intelligence data center market share in 2025, while colocation facilities are expected to advance at a 21.58% CAGR through 2031.

- By component, software captured 45.43% of the Australian artificial intelligence data center market size in 2025; however, hardware is projected to grow at a 21.10% CAGR between 2026 and 2031.

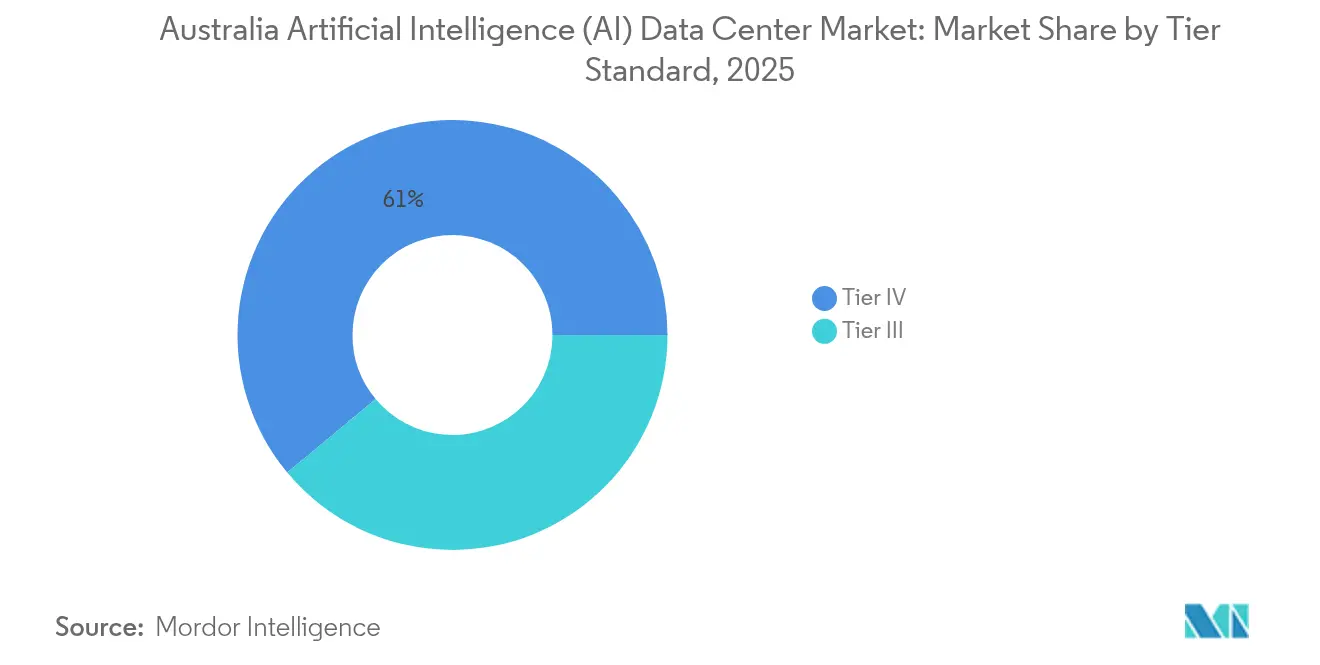

- By tier standard, Tier IV sites commanded a 61.05% market share of the Australian artificial intelligence data center market in 2025; Tier III facilities are expected to show the fastest expansion at a 22.05% CAGR to 2031.

- By end-user industry, IT and ITES led the Australian artificial intelligence data center market, accounting for a 33.52% revenue share in 2025. Meanwhile, Internet and Digital Media workloads are forecast to grow at a 20.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

National developments in Australia connect differently with activity unfolding across other parts of the world. In the global artificial intelligence (ai) data center market coverage, Mordor Intelligence integrates these into a single analytical framework.

Australia Artificial Intelligence (AI) Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising AI workloads and high-density racks | +4.2% | Sydney, Melbourne, Perth | Medium term (2-4 years) |

| Surge in hyperscale cloud investments | +5.8% | Sydney and Melbourne metros | Short term (≤ 2 years) |

| Data-sovereignty mandates | +3.1% | Nationwide, defense-led | Long term (≥ 4 years) |

| Submarine-cable and domestic fiber upgrades | +2.7% | Coastal cities | Medium term (2-4 years) |

| Exemption from U.S. AI-chip export rules | +2.9% | Nationwide | Short term (≤ 2 years) |

| Renewable PPAs mitigating power costs | +1.6% | Renewable-rich states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising AI Workloads Driving High-Density Compute Demand

Compute densities exceeding 30 kW per rack have become commonplace in the Australian artificial intelligence data center market as enterprises train transformer models for financial trading, radiology imaging, and predictive maintenance. NEXTDC’s M3 Melbourne campus already features 40 kW liquid-cooled racks, while AirTrunk’s SYD2 blueprint envisions 50 kW deployments.[1]NEXTDC Limited, “Investor Presentation Q3 2024,” Nextdc.com The Australian Computer Society forecasts annual AI workload growth of 180% through 2027, necessitating operators to allocate 35-40% of total build budgets to upgraded power infrastructure, a steep increase from the 20-25% norm for legacy sites. Higher rack densities also compress usable white space, spurring demand for modular phases that can be activated as utilization ramps.

Surging Cloud and Hyperscale Investments by Global Providers

Microsoft’s AUD 5 billion outlay through 2026 targets 20,000 GPUs across Sydney and Melbourne, reinforcing the Australian artificial intelligence data center market as a regional hub. AWS is adding EC2 P5 (H100) instances to its Sydney region, and Google Cloud brought Vertex AI to Melbourne in 2024, ensuring sub-20 ms latency for inference traffic. Collectively, hyperscalers announced USD 8.2 billion in new capacity during 2024-2025, a 67% jump over the prior biennium. Investment gravitates toward the two primary metros, yet edge sites in Perth and Brisbane are attracting follow-on spend aimed at latency-sensitive mining and telecom clients.

Government Data-Sovereignty Mandates Stimulating Local Hosting

Canberra’s Hosting Certification Framework obliges federal agencies and critical-infrastructure operators to process sensitive workloads onshore, effectively funneling new demand toward certified Tier IV campuses. Macquarie Data Centers secured AUD 350 million in contracts in 2024 to build isolated halls for defense AI applications, including autonomous systems and threat-detection algorithms. The mandates have inflated pricing power for sovereign hosting environments, enabling operators to command premium rates and higher utilization relative to retail colocation floors.

Expansion of Submarine-Cable and Domestic Fiber Connectivity

The Australia-Singapore Cable, which has been live since 2024, brings 40 Tbps to Perth, reducing latency for cross-region model training.[2]Vocus Group, “Media Centre,” Vocus.com.au Southern Cross NEXT, scheduled for completion in 2025, will deliver 72 Tbps of capacity between Sydney and Los Angeles, ensuring rapid disaster-recovery replication. Onshore, NBN Co is upgrading metro loops to 10 Gbps enterprise links, with AUD 2.1 billion earmarked for the 2024-2025 period. Operators report 25-30% lower data-transfer costs for AI pipelines that frequently synchronize petabyte-scale training sets across multiple facilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-capacity limits in primary metros | −2.8% | Sydney and Melbourne | Short term (≤ 2 years) |

| Supply-chain delays for AI hardware | −1.9% | Nationwide | Medium term (2-4 years) |

| Emerging Scope-3 reporting rules | −1.2% | Nationwide | Long term (≥ 4 years) |

| Shortage of liquid-cooling-skilled technicians | −1.4% | Major metros | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid-Capacity Constraints in Sydney and Melbourne Metros

Data centers already consume 5% of local electricity demand in Sydney and Melbourne and could account for up to 15% by 2030, according to AEMO. Ausgrid must inject AUD 1.2 billion into its Sydney network, while Citipower’s Melbourne upgrades carry similar price tags.[3]Ausgrid, “Network Investment Plan 2024,” Ausgrid.com.au Lead times for 10 MW connections have stretched to 18 months, delaying several launches inside the Australian artificial intelligence data center market. Some operators are pre-leasing capacity in Perth and Adelaide as a hedge, though those metros offer less skilled labor and thinner fiber routes.

Supply-Chain Delays for AI-Specific Hardware and Components

NVIDIA, AMD, and specialized immersion-cooling suppliers remain capacity-constrained, extending server lead times to 12-18 months and pushing hardware costs 15-25% above 2023 levels. Operators now secure multi-year supply agreements before breaking ground, ensuring that equipment arrivals align with commissioning schedules. Smaller entrants lack the purchasing clout to obtain GPU allocations, reinforcing the scale advantages of incumbent hyperscalers in the Australian artificial intelligence data center market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Hyperscale Dominance Meets Colocation Acceleration

The Australia artificial intelligence data center market recorded 55.32% of capacity under cloud service providers in 2025, equal to a USD 0.98 billion slice of the Australia artificial intelligence data center market size. Colocation’s 21.58% CAGR through 2031 will outpace overall industry growth as enterprises pursue hybrid strategies that isolate sensitive training data yet tap cloud elasticity for burst workloads. Microsoft’s Azure footprint, AWS’s fourth availability zone, and Google Cloud’s Melbourne launch illustrate hyperscale momentum, but NEXTDC’s 34% revenue surge in 2024 attests to rising corporate preference for bespoke power-and-cooling profiles. Edge nodes in mining and agriculture push compute closer to sensors, trimming backhaul latency to sub-10 ms for autonomous haul trucks and harvesters.

Second-order effects include colocation providers inking long-term renewable PPAs to woo tenants with carbon-neutral SLAs, and hyperscalers leasing entire halls within third-party sites to accelerate time to market. These dynamics deepen supplier relationships across the Australian artificial intelligence data center market and may compress wholesale pricing once additional capacity in secondary cities goes live after 2026.

By Component: Software Leadership Yields to Hardware Acceleration

Software accounted for 45.43% of spending in 2025, reflecting enterprise investment in model-development frameworks. Yet hardware is on a 21.10% CAGR clip as the Australian artificial intelligence data center market transitions to liquid-cooled GPU clusters. Power distribution consumes 35-40% of hardware budgets, which is double the share in traditional halls, while cooling claims another sizable portion due to direct-to-chip and immersion systems. The Australian artificial intelligence data center market size for hardware is therefore set to eclipse software expenditure by 2028.

Services revenues, ranging from integration to managed inference pipelines, form a crucial annuity stream as operators struggle with talent shortages in high-density design. Vendors are bundling white-glove deployment assistance with service-level commitments that guarantee model-training throughput, effectively transforming infrastructure financing into an operational expense for many mid-market clients.

By Tier Standard: Tier IV Dominance with Tier III Momentum

Tier IV installations controlled 61.05% of the Australian artificial intelligence data center market share in 2025, catering to finance algorithms, hospital imaging, and other non-stop workloads. Tier III sites, however, register a 22.05% CAGR as startups, SaaS vendors, and research labs accept 99.982% availability to temper capital outlays. AirTrunk’s SYD2 received Tier IV certification and features N+1 redundancy across all subsystems. Conversely, modular Tier III pods can be erected within eight months, appealing to firms piloting generative AI prototypes without committing to the hefty cost premiums of fully fault-tolerant plants.

Regulatory guidance from the Australian Communications and Media Authority emphasizes service resilience for telecom networks, nudging carriers toward Tier IV; yet cost-sensitive digital media houses gravitate to Tier III for batch content generation workflows that tolerate brief maintenance windows.

By End-User Industry: IT Leadership with Media Acceleration

IT and ITES companies consumed 33.52% of the capacity in 2025, but Internet and Digital Media are expected to be the fastest risers at a 20.98% CAGR, driven by video-streaming personalization and large-scale recommendation engines. Banks are embedding real-time fraud detection models, healthcare operators are rolling out AI-driven radiology triage tools, and mining consortia are deploying edge inference rigs 1,000 km from major metropolitan areas. Telstra alone earmarked AUD 800 million for AI-enabled network management through 2026.

These verticals share a common need for sovereign hosting, low-latency interconnects, and predictable power costs, three hallmarks that differentiate premium providers within the Australian artificial intelligence data center market. As workloads diversify, operators are offering vertical-specific compliance zones, such as health data enclaves that satisfy the Australian Privacy Principles and banking halls that align with APRA Prudential Standards.

Geography Analysis

Sydney houses 44.60% of the national capacity, thanks to its dense fiber infrastructure, cloud on-ramps, and proximity to Australia’s finance sector. Melbourne follows at 30.10%, buoyed by Google Cloud’s regional presence and Equinix’s ME1 expansion, both of which fuel double-digit leasing growth among software firms and universities. Together, the two metros are forecast to grow at roughly 19.52% CAGR but face acute grid pressure that could cap incremental builds until transmission upgrades roll out post-2027.

Perth, now accounting for 12.40% of the Australian artificial intelligence data center market size, is scaling at a 25% CAGR on the back of the Australia-Singapore Cable, which opens a west-facing route to Asian model repositories. Brisbane and Adelaide together represent 12.90%; they attract disaster-recovery footholds and edge hubs that service eastern mining corridors and defense installations. Regional diversification also aligns with antitrust scrutiny by the Australian Competition and Consumer Commission, which encourages dispersion to curb single-city dependency.

A comparison of historical and forecast rates reveals acceleration: the Australian artificial intelligence data center market expanded at a 15.8% CAGR during 2020-2024 but is expected to reach 19.65% through 2031, underscoring how GPU exemptions, sovereign mandates, and hyperscale ambitions converge to unlock new capacity across the continent.

Mordor Intelligence's coverage of the artificial intelligence (ai) data center market extends across other regions including North America, South America, and Europe, while country-specific intelligence is also available for China, Japan, Canada, Chile, Germany, and South Africa, each offering a view on the jurisdiction-level dynamics as applicable.

Competitive Landscape

The top five operators control roughly 60% of the national installed power, resulting in a moderate concentration profile for the Australian artificial intelligence data center market. NEXTDC and AirTrunk lead colocation volumes with purpose-built liquid-cooled halls; each boasts sub-1.3 PUE designs and announces 100% renewable PPAs to court ESG-focused tenants. Hyperscalers, including Microsoft, AWS, and Google, pursue a mix of self-builds and wholesale leases, accelerating deployment while hedging against regulatory exposure.

Strategic differentiation now centers on cooling innovation. Immersion and direct-to-chip solutions already account for 40% of new builds and are on track to surpass chill-water as the standard within two years. Operators also provide AI-optimized network fabrics that guarantee a switch latency of less than 200 ns, crucial for model parallelism across thousands of GPUs.

M&A talk is rising as regional players seek to scale up and negotiate hardware allocations. Meanwhile, edge-centric developers target mining, agritech, and regional telcos with 1-3 MW campuses that include on-site battery storage and solar arrays to bypass thin local grids. The interplay between hyperscale mass and niche edge strategy will shape competitive intensity through the decade.

Australia Artificial Intelligence (AI) Data Center Industry Leaders

AirTrunk Operating Pty Ltd.

NEXTDC Limited

Canberra Data Centres Pty Limited

Equinix, Inc.

Digital Realty Trust, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: NEXTDC announced an AUD 1.2 billion capital investment program through 2027, targeting AI-optimized facility development across Sydney, Melbourne, and Perth with liquid cooling infrastructure and renewable energy integration. The investment includes the expansion of M3 Melbourne and the commencement of construction on the P2 Perth facility, featuring 60 kW rack configurations.

- September 2025: AirTrunk completes acquisition of 25-hectare site in Brisbane for AUD 320 million hyperscale development, targeting 100 MW capacity with direct submarine-cable connectivity and 100% renewable energy sourcing through solar PPA agreements with Origin Energy.

- August 2025: Microsoft expands Azure AI infrastructure investment to AUD 7.8 billion through 2028, adding 15,000 additional GPU units across Australian facilities and launching Azure OpenAI services with local data residency for government and enterprise customers.

- July 2025: Equinix invests AUD 450 million in the SY6 Sydney facility development, incorporating immersion cooling technology and 45 kW rack density to serve enterprise AI workloads that require sub-5 ms latency for real-time inference applications.

- June 2025: Digital Realty Trust partners with Macquarie Technology Group in a AUD 680 million joint venture for a Western Sydney hyperscale campus, targeting a 120 MW capacity with a dedicated renewable energy microgrid and advanced liquid cooling systems.

- May 2025: Amazon Web Services announces AUD 2.1 billion investment in Australian infrastructure expansion, including new availability zones in Perth and Adelaide with AI-specific instance types and local machine-learning services.

Australia Artificial Intelligence (AI) Data Center Market Report Scope

The research encompasses the full spectrum of AI applications in data centers, covering hyperscale, colocation, enterprise, and edge facilities. The analysis is segmented by component, distinguishing between hardware and software. Hardware considerations include power, cooling, networking, IT equipment, and more. Software technologies under scrutiny encompass machine learning, deep learning, natural language processing, and computer vision. The study also evaluates the geographical distribution of these applications.

Additionally, it assesses AI's influence on sustainability and carbon neutrality objectives. A comprehensive competitive landscape is presented, detailing market players engaged in AI-supportive infrastructure, encompassing both hardware and software utilized across various AI data center types. Market size is calculated in terms of revenue generated by products and solutions providers in the market, and forecasts are presented in USD Billion for each segment.

| Cloud Service Providers |

| Colocation Data Centers |

| Enterprise / On-Premises / Edge |

| Hardware | Power Infrastructure |

| Cooling Infrastructure | |

| IT Equipment | |

| Racks and Other Hardware | |

| Software Technology | Machine Learning |

| Deep Learning | |

| Natural Language Processing | |

| Computer Vision | |

| Services | Managed Services |

| Professional Services |

| Tier III |

| Tier IV |

| IT and ITES |

| Internet and Digital Media |

| Telecom Operators |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Manufacturing and Industrial IoT |

| Government and Defense |

| By Data Center Type | Cloud Service Providers | |

| Colocation Data Centers | ||

| Enterprise / On-Premises / Edge | ||

| By Component | Hardware | Power Infrastructure |

| Cooling Infrastructure | ||

| IT Equipment | ||

| Racks and Other Hardware | ||

| Software Technology | Machine Learning | |

| Deep Learning | ||

| Natural Language Processing | ||

| Computer Vision | ||

| Services | Managed Services | |

| Professional Services | ||

| By Tier Standard | Tier III | |

| Tier IV | ||

| By End-User Industry | IT and ITES | |

| Internet and Digital Media | ||

| Telecom Operators | ||

| Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial IoT | ||

| Government and Defense | ||

Key Questions Answered in the Report

How fast will artificial-intelligence data centers grow in Australia through 2031?

Capacity is projected to climb from USD 1.78 billion in 2025 to USD 5.22 billion by 2031, reflecting a 19.65% CAGR.

Which Australian cities attract the most AI data center investment?

Sydney and Melbourne account for roughly 74.70% of national capacity thanks to mature fiber, cloud on-ramps and deep talent pools.

Why are liquid-cooled racks becoming standard in new Australian sites?

Training large language models pushes rack densities beyond 30 kW, and liquid cooling maintains thermal stability while keeping PUE below 1.3.

What role do government data-sovereignty rules play?

Canberra’s Hosting Certification Framework obliges agencies and critical-infrastructure firms to keep sensitive workloads onshore, funneling demand to certified Tier IV campuses.

How are operators addressing grid-capacity bottlenecks?

Providers are signing renewable PPAs, pre-leasing secondary-city land and coordinating with utilities on multi-year transmission-upgrade roadmaps.

Page last updated on: