Saudi Arabia Artificial Intelligence (AI) Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

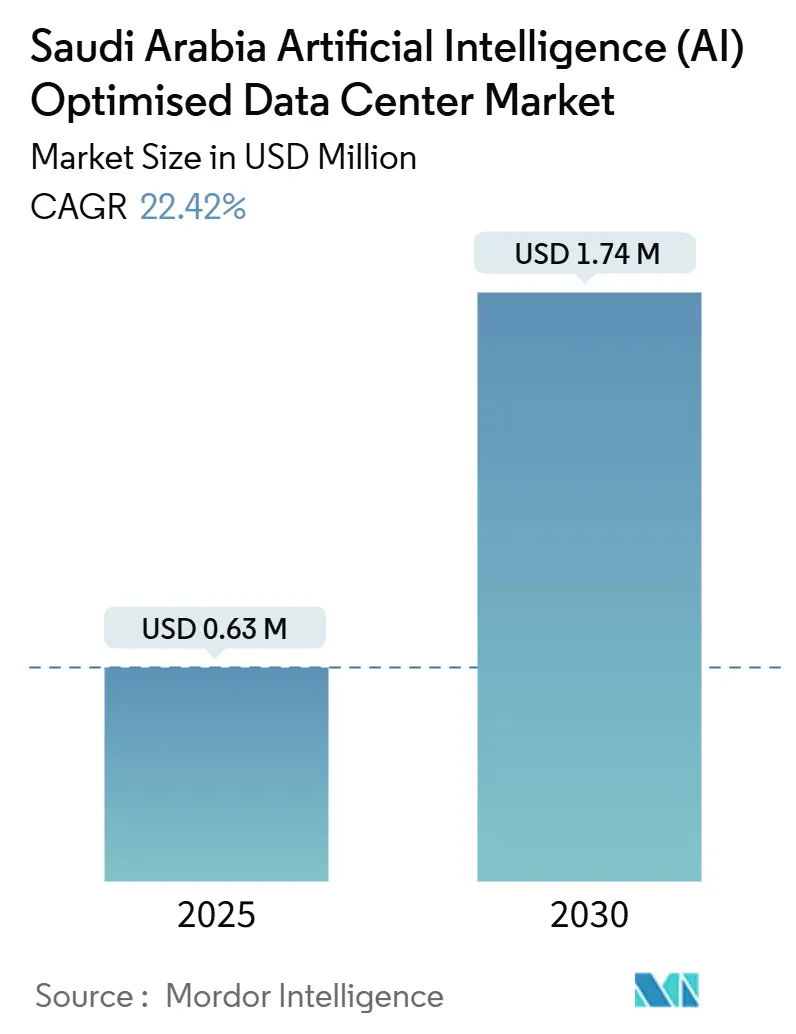

| Market Size (2025) | USD 0.63 Million |

| Market Size (2030) | USD 1.74 Million |

| Growth Rate (2025 - 2030) | 22.42% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Artificial Intelligence (AI) Data Center Market Analysis by Mordor Intelligence

The Saudi Arabia artificial intelligence data center market size stood at USD 0.63 billion in 2025 and is projected to reach USD 1.74 billion by 2030, reflecting a 22.42% CAGR over the forecast period. Rapid hyperscale build-outs, Vision 2030’s large-scale digital investments, and aggressive public-private partnerships together establish a robust foundation for AI workload hosting. Government data-sovereignty mandates and the Personal Data Protection Law (PDPL) stimulate local hosting, while 5G roll-outs catalyze edge infrastructure demand. Large sovereign wealth allocations, including Public Investment Fund initiatives, further accelerate capital inflows into high-density facilities. Meanwhile, sustainability pressures in the desert climate promote innovation in hybrid cooling and renewable power sourcing, opening new competitive niches around efficiency technologies.

Key Report Takeaways

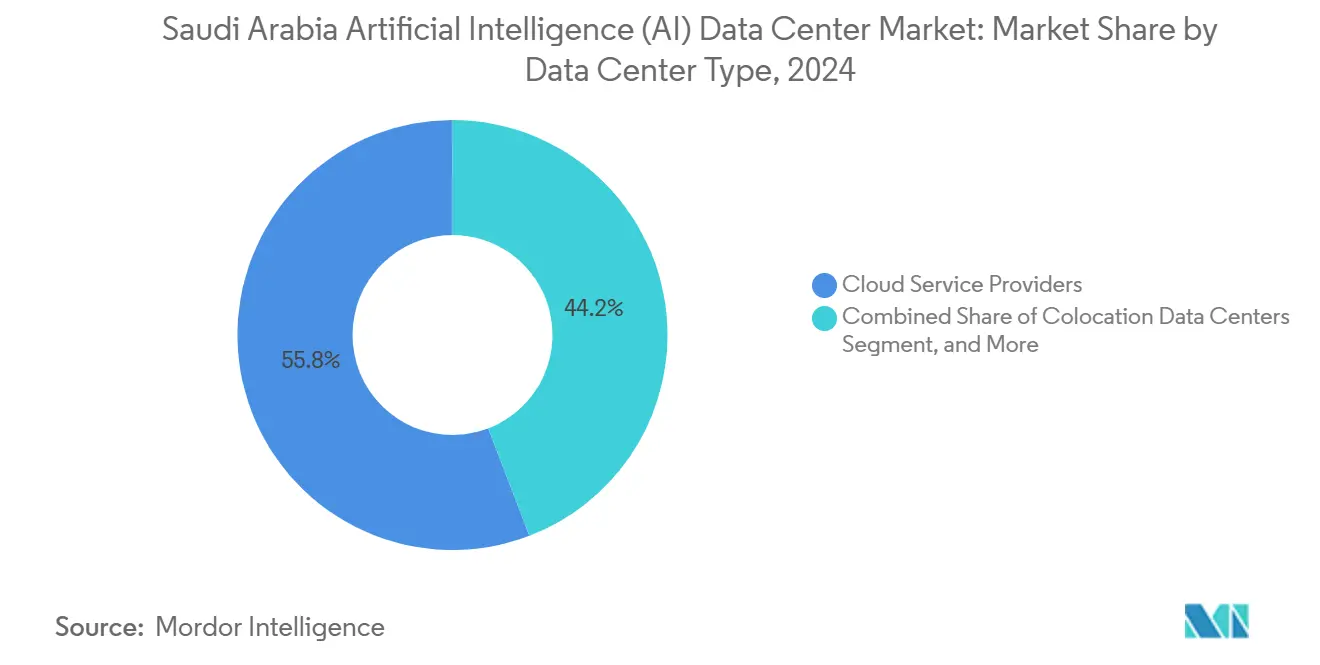

- By data center type, cloud service providers led with 55.82% of Saudi Arabia artificial intelligence data center market share in 2024, while colocation facilities are advancing at a 24.21% CAGR through 2030.

- By component, software held 45.83% share of the Saudi Arabia artificial intelligence data center market size in 2024; hardware is forecast to expand at a 23.92% CAGR between 2025-2030.

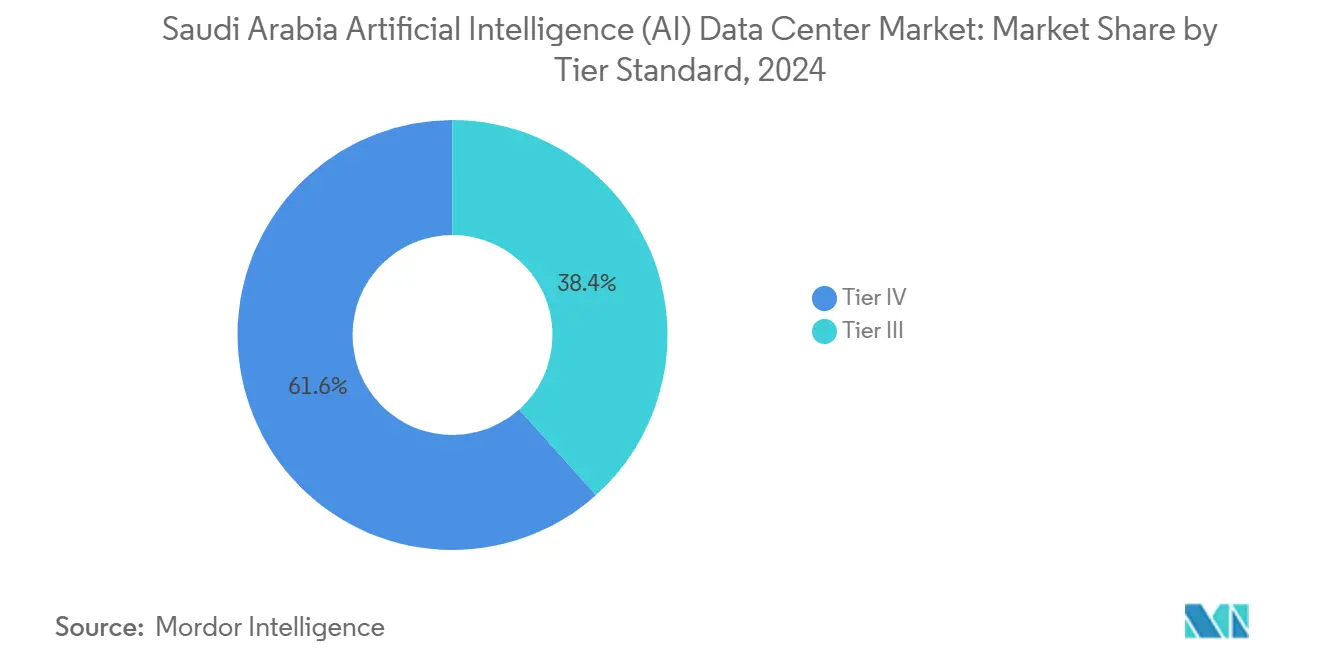

- By tier, Tier IV captured 61.63% of Saudi Arabia artificial intelligence data center market share in 2024, whereas Tier III is on course for a 24.12% CAGR through 2030.

- By end-user industry, IT and ITES commanded 33.82% revenue share in 2024 in the Saudi Arabia artificial intelligence data center market, while internet and digital media is the fastest-growing vertical at 23.67% CAGR to 2030

Figures recorded within Saudi arabia feed into a worldwide estimate while studying the global industry. Mordor Intelligence's artificial intelligence (ai) data center market size captures this aggregation.

Saudi Arabia Artificial Intelligence (AI) Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030-Driven Digital Transformation Investments | +6.8% | National, with concentration in Riyadh, Jeddah, NEOM | Long term (≥ 4 years) |

| Hyperscale Cloud Region Expansions by Global CSPs | +5.2% | National, with primary hubs in Riyadh and Jeddah | Medium term (2-4 years) |

| 5G Roll-out Accelerating Edge AI Workloads | +3.9% | National, with early deployment in major cities | Medium term (2-4 years) |

| NEOM's Smart-City AI Compute Demand Spike | +2.8% | NEOM region, with spillover to Western Province | Long term (≥ 4 years) |

| Government-Backed Data-Sovereignty Mandates | +2.1% | National, affecting all data center operations | Short term (≤ 2 years) |

| Geothermal District-Cooling Pilots for Desert DCs | +1.4% | Riyadh and Eastern Province pilot locations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision 2030-Driven Digital Transformation Investments

Project Transcendence allocates USD 100 billion toward AI programs, directly linking 66 of Vision 2030’s 96 strategic objectives to data-driven capabilities.[1]“AI is Powering Saudi Arabia’s Vision 2030 Transformation,” SAMENA Council, samenacouncil.org SDAIA’s public-private projects fuel continuous demand for sovereign compute, especially for Arabic language model training and specialized government analytics. Each public dollar spent triggers roughly USD 2.3 in private infrastructure deployment, ensuring durable capital inflows and anchoring long-term market stability. The scale attracts global technology vendors seeking a foothold in the Gulf, consolidating Riyadh’s status as a regional AI hub.

Hyperscale Cloud Region Expansions by Global CSPs

AWS committed USD 5.3 billion, while Microsoft scheduled completion of its local region for 2026, collectively reshaping the digital fabric of the Kingdom. Google Cloud partnered with the Public Investment Fund in October 2024, and Oracle launched a second Riyadh region in August 2024 with USD 1.5 billion invested.[2]Oracle Corporation, “Oracle Opens Second Cloud Region in Riyadh,” oracle.com These anchors justify further backbone investments in power, fiber, and cooling. Reduced latency and regulatory compliance entice enterprises to migrate AI workloads locally, while system integrators build layered services on top of hyperscale footprints.

5G Roll-out Accelerating Edge AI Workloads

Nationwide 5G deployment by STC, Mobily, and Zain enables sub-10 millisecond latency for edge-native applications. Smart-city surveillance, autonomous logistics, and industrial IoT rely on micro-data centers at tower sites. Telcos monetize tower real estate by installing edge nodes, creating new revenue lanes beyond connectivity. The distributed architecture complements centralized facilities, producing a tiered network that balances cost and performance for diverse AI workloads.

NEOM’s Smart-City AI Compute Demand Spike

The USD 5 billion DataVolt complex targets 1.5 GW of net-zero capacity by 2028, establishing the world’s largest single AI data center investment. Real-time urban twins, climate simulation, and cognitive traffic systems require petascale throughput, setting new global benchmarks for sustainability and density. NEOM’s showcase effect lures additional Gulf smart-city projects to the Kingdom, strengthening its stature as the preferred base for mega-scale AI experimentation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Energy and Water Costs for Cooling in Arid Climate | -4.2% | National, with highest impact in inland regions | Medium term (2-4 years) |

| Limited Availability of Advanced AI Chips | -3.8% | National, affecting all AI-capable facilities | Short term (≤ 2 years) |

| Cyber-Security Talent Shortage | -2.1% | National, with concentration in major cities | Medium term (2-4 years) |

| Evolving Cross-Border Data Transfer Regulations | -1.9% | National, affecting international operations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Energy and Water Costs for Cooling in Arid Climate

Data centers consume 2.3-2.8 liters of water per kWh, placing future 1,300 MW capacity on track to require volumes equal to 700,000 households by 2030.[3]“Meeting Data Centre Power Through Clean Energy?,” DCTC-KSA, dctc-ksa.com Peak summer temperatures of 45 °C push cooling to 40% of total operating costs. Dependence on desalination for 70% of potable water magnifies the expense, as facilities compete with residential users. Solar adsorption chillers and hybrid cooling cut costs by over 60%, but demand high upfront outlays and specialized maintenance skills. Operators therefore combine air-cooled and liquid solutions, optimizing seasonally to contain OPEX.

Limited Availability of Advanced AI Chips

U.S. export rules enacted in October 2024 limit access to Nvidia H-series GPUs, driving 20-30% premiums and 12-18 month lead times. Saudi initiatives diversify toward AMD, Qualcomm AI200/AI250, and partnerships with alternative vendors. Humain’s 200 MW commitment to Qualcomm racks starting 2026 illustrates multi-vendor hedging. While performance gaps exist versus frontier silicon, diversification sustains near-term build schedules and lessens dependency on a single supply chain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Cloud Dominance Drives Colocation Growth

Cloud service providers accounted for 55.82% of Saudi Arabia artificial intelligence data center market share in 2024, propelled by multi-billion-dollar region launches from AWS, Microsoft, Google Cloud, and Oracle. Typical builds span 20-100 MW with high-density racks and dedicated AI accelerators. These deployments ensure consistent availability of sovereign compute, catalyzing ecosystem growth.

Colocation, although smaller, is growing at a 24.21% CAGR as enterprises pursue hybrid strategies to meet PDPL mandates while retaining cloud connectivity. Providers such as DataVolt and Khazna expand campuses near metro cores, offering on-demand scalability and cross-connects to hyperscale nodes. Enterprise/edge sites remain niche but vital for low-latency industrial automation and defense-grade air-gapped workloads.

By Component: Hardware Acceleration Outpaces Software Growth

Software retained 45.83% revenue share in 2024, headed by machine learning frameworks tuned for Arabic language processing. Demand for localized NLP and vision stacks underscores sovereign-model ambitions. Managed MLOps suites help enterprises streamline deployment and monitoring across hybrid footprints.

Hardware, however, is accelerating at 23.92% CAGR as operators invest in servers exceeding 60 kW per rack, liquid cooling loops, and terabit-class networking. Increased power densities require upgraded switchgear and battery systems, steering sizeable capex toward electrical and mechanical plant upgrades. Services, spanning professional integration and managed hosting, round out spend as companies seek guidance on workload placement and cost optimization.

By Tier Standard: Tier IV Reliability Enables Tier III Growth

Tier IV facilities dominated with 61.63% share in 2024, offering 99.995% uptime vital for long-running AI training clusters. Full path redundancy and 96-hour backup safeguard against grid or mechanical failures. Hyperscalers default to this level to satisfy enterprise SLA commitments.

Tier III, advancing at 24.12% CAGR, balances N+1 redundancy with 20-30% capex savings. Enterprises deploying analytics or customer-facing AI find the availability profile sufficient, fuelling a wave of cost-optimized builds across Riyadh’s outskirts. ECC-2 guidelines published in 2024 encourage at least Tier III for critical workloads, steering the middle of the market to this standard.

By End-user Industry: IT Leadership Drives Media Innovation

IT and ITES held 33.82% of Saudi Arabia artificial intelligence data center market size in 2024, leveraging local infrastructure for software testing, system integration, and startup acceleration. Government incubators such as GAIA funnel capital into AI ventures, sustaining compute demand.

Internet and digital media, expanding at 23.67% CAGR, depends on real-time personalization, content moderation, and AR streaming. Local NLP innovators capitalize on Arabic dialect models, driving specialized throughput needs. BFSI, healthcare, and manufacturing accelerate adoption for fraud, imaging, and predictive maintenance respectively, often leveraging edge nodes for latency-sensitive inference.

Geography Analysis

Riyadh leads current capacity, clustering hyperscale zones and national regulators within proximity. STC/Center3, Mobily, and Oracle’s second cloud region anchor large campuses that serve financial institutions and government agencies requiring city-center latency.

Jeddah ranks second, benefiting from Red Sea cable landings that lower international transit costs. Facilities here support port automation, logistics analytics, and western-region smart-city projects. DataVolt’s First Technology Park project in eastern Riyadh underscores geographic diversification into secondary metros.

NEOM stands out as a future megahub. Its 1.5 GW net-zero complex aims to demonstrate desert-scale sustainability by 2028, leveraging 100% renewable energy and advanced cooling practices. Success could prompt replication across Gulf smart-city initiatives, effectively extending the Saudi Arabia artificial intelligence data center market into new coastal corridors.

Mordor Intelligence evaluates the artificial intelligence (ai) data center market across all key regional markets, including South America, Europe, and Asia, with deeper country-level insights covering United Arab Emirates, Spain, Brazil, China, United States, and India.

Competitive Landscape

Competition is moderate and dynamic. Incumbent telcos STC/Center3, Mobily, and Zain exploit fiber backbones and enterprise relationships to retain share. Global hyperscalers pour capital into standalone regions, rapidly scaling the Saudi Arabia artificial intelligence data center market through anchor tenancy. Equipment vendors Dell, HPE, and NVIDIA compete for high-density server contracts, while Schneider Electric and Vertiv supply integrated power and cooling solutions.

Strategic moves reveal vertical integration trends. AWS and Microsoft incorporate in-house AI accelerators into Saudi builds, reducing reliance on restricted U.S. GPUs. DataVolt and Tonomus leverage sovereign funding to launch giga-scale campuses positioned for PDPL compliance. Partnerships with alternative chip vendors such as Qualcomm illustrate hedging against supply chain risk.

Sustainable cooling and edge micro-facility design emerge as white-space opportunities. Providers able to deliver water-frugal solutions and modular nodes for 5G towers gain differentiation in an increasingly crowded landscape. The interplay between global scale and localized compliance expertise defines future competitive advantage.

Saudi Arabia Artificial Intelligence (AI) Data Center Industry Leaders

Cisco Systems

Schneider Electric Industries

ABB Ltd.

Alfa Laval Corporate AB

Vertiv Group Corp

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Nvidia Corp. and Advanced Micro Devices Inc. (AMD) will supply semiconductors to Saudi Arabian artificial intelligence company Humain for a USD 10 billion data center project. The initiative involves building AI infrastructure, including "AI factories" with a projected capacity of up to 500 megawatts, and aims to support the Kingdom’s growing demand for advanced AI technologies while adhering to local data storage mandates.

- May 2025: President Trump and Silicon Valley representatives have finalized a significant agreement with the United Arab Emirates to supply hundreds of thousands of advanced Nvidia chips annually. These chips will facilitate the establishment of one of the world’s largest data center hubs. Shipments are set to begin this year, with the majority allocated to U.S. cloud service providers and approximately 100,000 reserved for G42, an Emirati AI firm.

- February 2025: DataVolt secured a 55,000 m² plot from MODON in Riyadh’s First Technology Park for an AI-ready facility.

- January 2025: Dell Technologies signed a multi-billion-USD AI server supply agreement with a Middle Eastern sovereign wealth fund to deliver Blackwell-series GPU clusters.

Saudi Arabia Artificial Intelligence (AI) Data Center Market Report Scope

The research encompasses the full spectrum of AI applications in data centers, covering hyperscale, colocation, enterprise, and edge facilities. The analysis is segmented by component, distinguishing between hardware and software. Hardware considerations include power, cooling, networking, IT equipment, and more. Software technologies under scrutiny encompass machine learning, deep learning, natural language processing, and computer vision. The study also evaluates the geographical distribution of these applications.

Additionally, it assesses AI's influence on sustainability and carbon neutrality objectives. A comprehensive competitive landscape is presented, detailing market players engaged in AI-supportive infrastructure, encompassing both hardware and software utilized across various AI data center types. Market size is calculated in terms of revenue generated by products and solutions providers in the market, and forecasts are presented in USD Billion for each segment.

| Cloud Service Providers |

| Colocation Data Centers |

| Enterprise / On-Premises / Edge |

| Hardware | Power Infrastructure |

| Cooling Infrastructure | |

| IT Equipment | |

| Racks and Other Hardware | |

| Software | Technology |

| Machine Learning | |

| Deep Learning | |

| Natural Language Processing | |

| Computer Vision | |

| Services | Managed Services |

| Professional Services |

| Tier III |

| Tier IV |

| IT and ITES |

| Internet and Digital Media |

| Telecom Operators |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Manufacturing and Industrial IoT |

| Government and Defense |

| By Data Center Type | Cloud Service Providers | |

| Colocation Data Centers | ||

| Enterprise / On-Premises / Edge | ||

| By Component | Hardware | Power Infrastructure |

| Cooling Infrastructure | ||

| IT Equipment | ||

| Racks and Other Hardware | ||

| Software | Technology | |

| Machine Learning | ||

| Deep Learning | ||

| Natural Language Processing | ||

| Computer Vision | ||

| Services | Managed Services | |

| Professional Services | ||

| By Tier Standard | Tier III | |

| Tier IV | ||

| By End-user Industry | IT and ITES | |

| Internet and Digital Media | ||

| Telecom Operators | ||

| Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial IoT | ||

| Government and Defense | ||

Key Questions Answered in the Report

What is the current value of the Saudi Arabia artificial intelligence data center market?

The market is valued at USD 0.63 billion in 2025 and is projected to reach USD 1.74 billion by 2030.

Which data center type holds the largest revenue share in the Kingdom?

Cloud service providers account for 55.82% of total 2024 revenue, driven by multi-billion-USD hyperscale investments.

Which component segment is growing fastest?

Hardware is advancing at a 23.92% CAGR as operators deploy high-density AI servers and liquid cooling systems.

Why is Riyadh the primary location for AI data centers?

Riyadh hosts major government bodies, financial institutions, and multiple hyperscale regions, delivering strong demand and regulatory proximity.

How does Vision 2030 influence infrastructure growth?

Vision-linked public spending triggers matching private investment, ensuring long-term capital inflows and sustained data-center expansion.

Page last updated on: