Neurothrombectomy Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

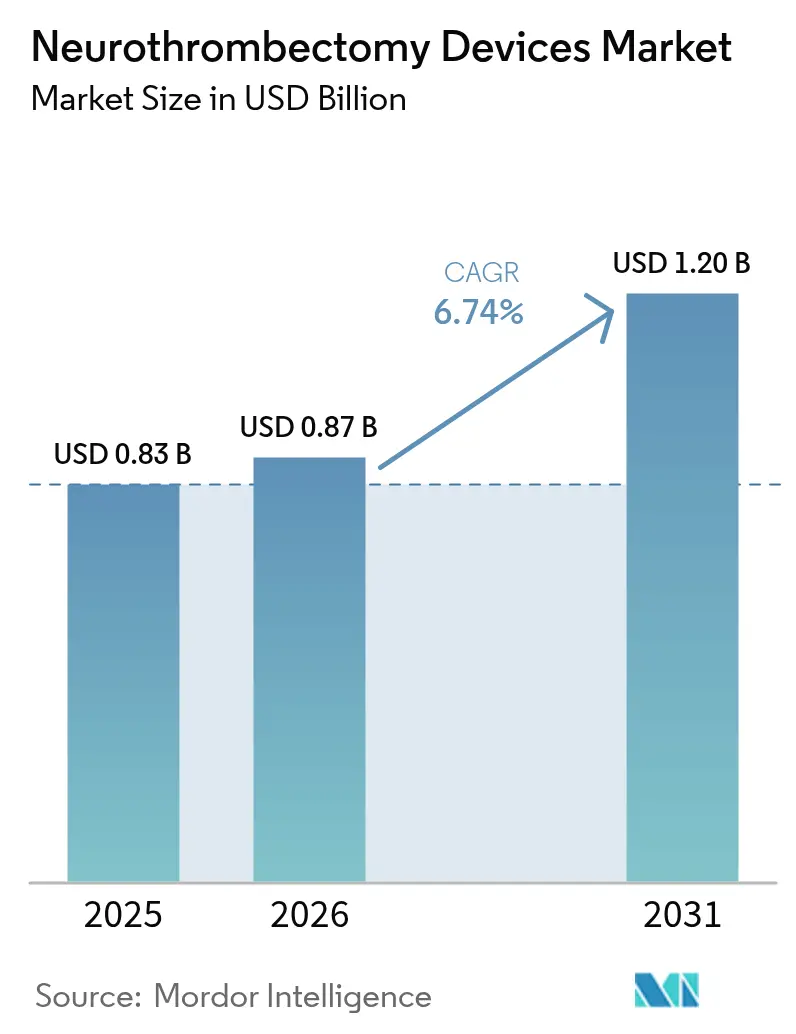

| Market Size (2026) | USD 0.87 Billion |

| Market Size (2031) | USD 1.20 Billion |

| Growth Rate (2026 - 2031) | 6.74% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neurothrombectomy Devices Market Analysis by Mordor Intelligence

The Neurothrombectomy Devices Market size is projected to be USD 0.83 billion in 2025, USD 0.87 billion in 2026, and reach USD 1.20 billion by 2031, growing at a CAGR of 6.74% from 2026 to 2031.

This steady climb reflects a maturing technology cycle that followed the post-DAWN trial surge, with hospitals now optimizing patient selection through automated perfusion imaging and streamlined hub-and-spoke networks. Aspiration techniques that lower fluoroscopy time and reduce device exchanges are gaining traction among U.S. and European operators, while China’s mandate for tertiary stroke-center accreditation is lifting procedure volumes across more than 2,000 hospitals. AI-driven triage platforms such as Viz.ai and RapidAI compress door-to-puncture times by roughly 20 minutes, helping community hospitals meet guideline-recommended treatment windows. At the same time, reimbursement certainty under Medicare MS-DRG 023-027, category-C1 coverage in Japan, and harmonized European Stroke Organisation guidelines continue to make large-vessel occlusion treatment financially viable for care providers.[1]Centers for Disease Control and Prevention, “Stroke Facts,” cdc.gov

Key Report Takeaways

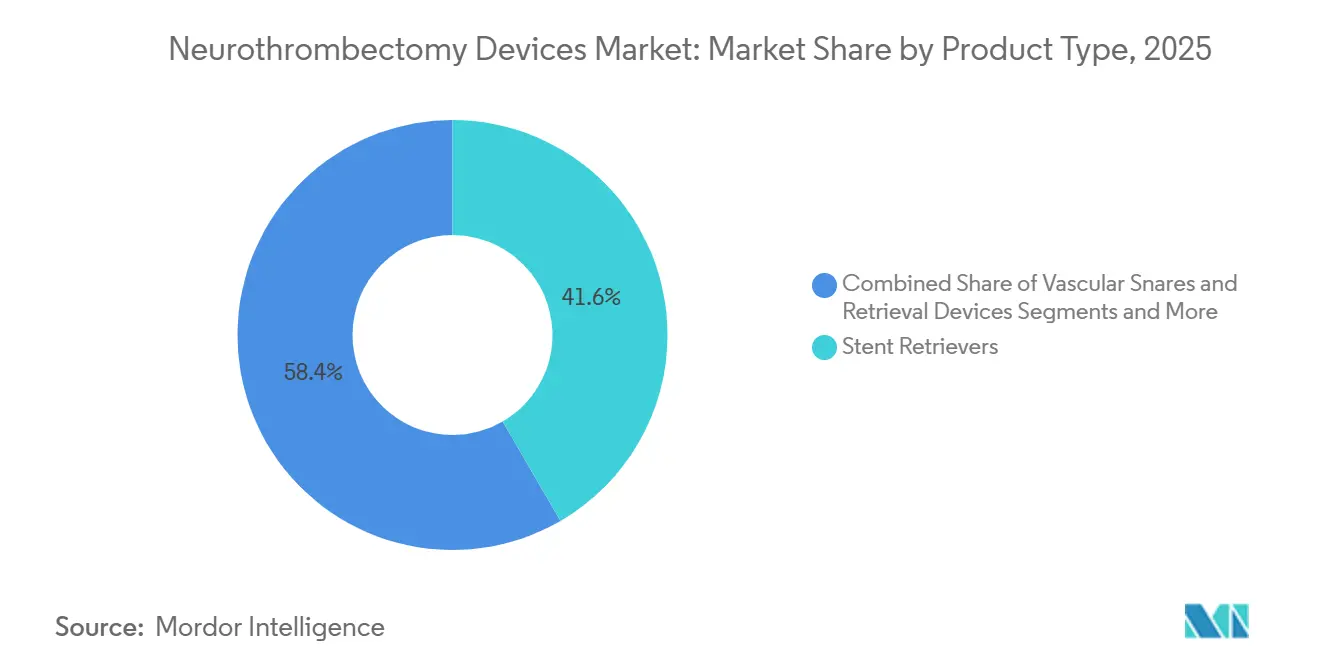

- By product type, stent retrievers led with 41.62% revenue share in 2025, while aspiration devices are forecast to expand at a 10.13% CAGR to 2031.

- By access route, trans-femoral techniques held 76.13% of the neurothrombectomy devices market share in 2025, but trans-radial and brachial approaches are pacing at a 9.34% CAGR through 2031.

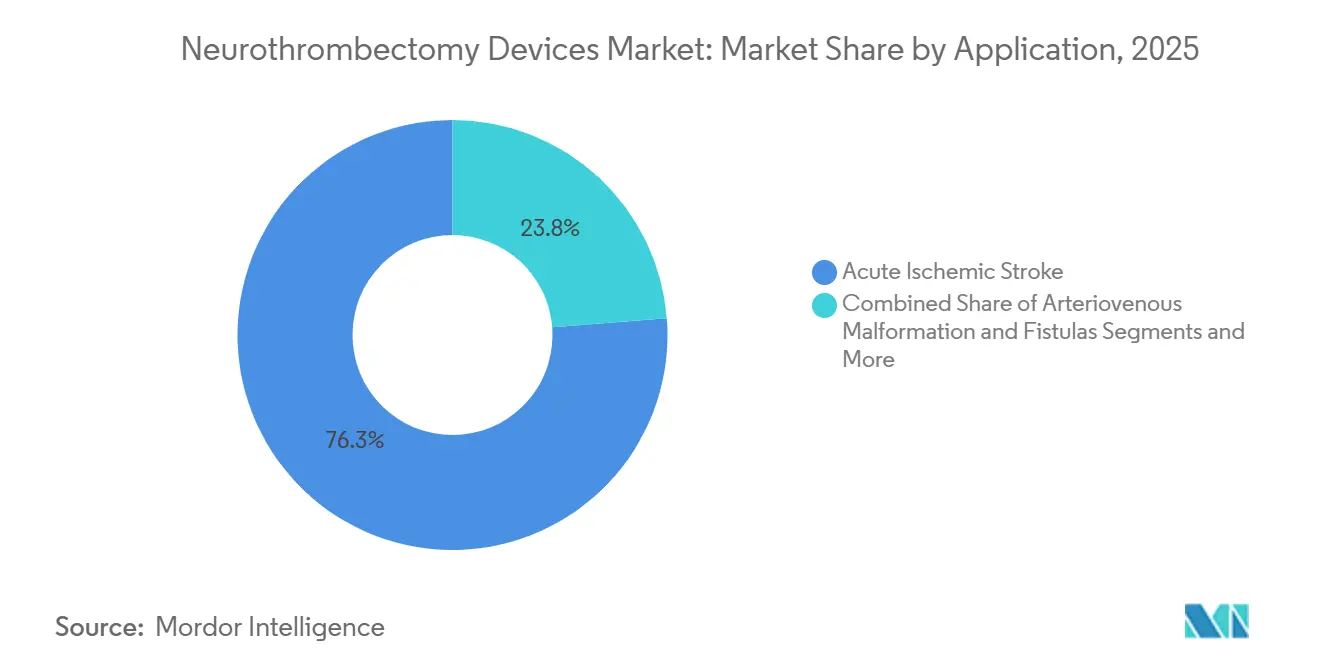

- By application, acute ischemic stroke accounted for 76.25% of the neurothrombectomy devices market size in 2025, whereas arteriovenous malformations and fistulas are advancing at an 8.64% CAGR to 2031.

- By treatment window, procedures within 6 hours held 66.91% share in 2025, yet the 6-to-24-hour cohort is growing at a 10.35% CAGR during the forecast period.

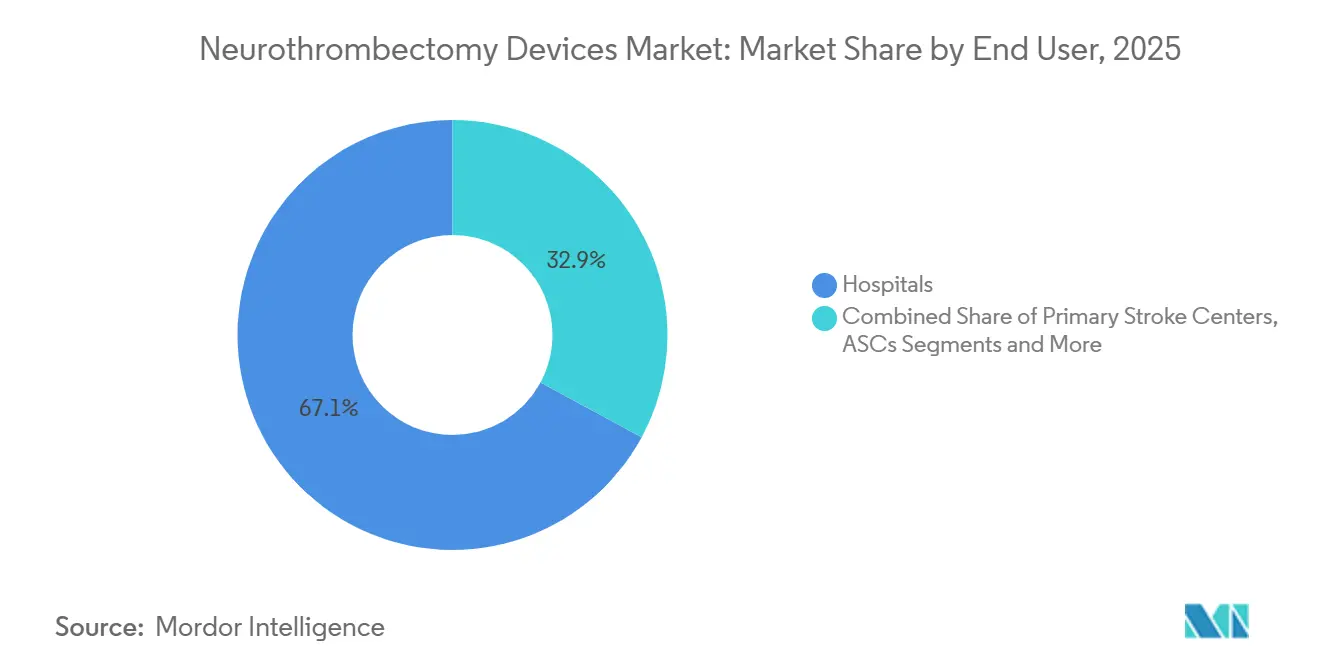

- By end user, hospitals commanded 67.12% share in 2025; ambulatory surgical centers deliver the fastest growth at an 8.13% CAGR through 2031.

- By geography, North America captured 39.13% of 2025 revenue, while Asia-Pacific is on course for the highest regional CAGR at 8.12% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Neurothrombectomy Devices Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Incidence of Acute Ischemic Stroke | +1.2% | APAC, Europe, North America | Long term (≥ 4 years) |

| Expansion of Treatment Guidelines and Reimbursement Coverage | +1.5% | North America, Western Europe | Medium term (2-4 years) |

| Technological Advances in Stent Retrievers and Aspiration Catheters | +1.0% | Global | Medium term (2-4 years) |

| Growing Adoption in Emerging Markets | +1.3% | China, India, Latin America | Long term (≥ 4 years) |

| AI-Enabled Stroke Triage Platforms | +0.9% | North America, Western Europe | Short term (≤ 2 years) |

| Telestroke and Remote Proctoring | +0.6% | Rural U.S., Europe, India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global Incidence of Acute Ischemic Stroke

The World Health Organization logged 11.95 million strokes in 2021, 87% of which were ischemic, and aging populations in Japan, Germany, and the United States continue to nudge the caseload upward by 2-3% each year.[2]World Health Organization, “Stroke Statistics,” who.int China alone records nearly 3 million new events annually, while India’s incidence rises 4% per year as urban lifestyles fuel hypertension and diabetes. These epidemiological pressures stretch thrombolysis capacity, given that tissue plasminogen activator fails to recanalize 60-70% of large-vessel occlusions. Health systems are therefore prioritizing neurothrombectomy suite build-outs, expanding eligibility to late presenters, and investing in specialist training programs to keep pace with demand.

Expansion of Treatment Guidelines and Reimbursement Coverage

Updated 2026 AHA/ASA guidelines endorse mechanical thrombectomy up to 24 hours after the last known well time when perfusion imaging shows salvageable penumbra.[3]American Heart Association, “2026 Guideline for the Early Management of Patients With Acute Ischemic Stroke,” ahajournals.org Medicare reimburses these procedures under MS-DRG 023-027 at USD 7,200-8,500, and similar policy shifts in Germany, France, and Japan cut hospital payback times on biplane angiography equipment to under five years. Coverage clarity encourages capital spending and helps smaller community hospitals justify staff expansion, moving the neurothrombectomy devices market toward broader geographic penetration.

Technological Advances in Stent Retrievers and Aspiration Catheters

Penumbra’s Lightning Flash 2.0 and Medtronic’s React 71 aspiration lines introduce variable-stiffness shafts and vacuum-assist pumps that trim median procedure times below 40 minutes. Cerenovus’ Cereglide 71 intermediate catheter features a low-profile distal tip that tackles tortuous intracranial anatomy without vessel trauma. These refinements reduce distal embolization risk, cut contrast use, and lower anesthesia exposure, while the 510(k) pathway for aspiration devices lets manufacturers iterate faster than PMA-regulated stent retrievers.

Growing Adoption in Emerging Markets

China requires every tertiary hospital to run a certified stroke center, propelling device uptake across 2,000 sites, while domestic vendors price retrievers 40-50% below Western imports. India’s telestroke networks link rural district hospitals to urban specialists, and Brazil’s Unified Health System has started paying for thrombectomy in public centers. These initiatives expand the addressable neurothrombectomy devices market, although workforce shortages and fragmented supply chains temper the pace.

Restraints Impact Analysis of Neurothrombectomy Devices Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Device and Procedure Costs in Low-Resource Settings | –0.8% | Sub-Saharan Africa, South Asia | Long term (≥ 4 years) |

| Stringent Regulatory and Clinical-Trial Requirements | –0.5% | North America, EU | Medium term (2-4 years) |

| Shortage of Neuro-Interventional Specialists in Rural Areas | –0.6% | Rural U.S., Eastern Europe, India | Long term (≥ 4 years) |

| Supply-Chain Fragility for Nitinol and Polymer Components | –0.4% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Device and Procedure Costs in Low-Resource Settings

A single thrombectomy can cost USD 15,000-40,000, exceeding the annual per-capita health spend in South Asia by up to 200 times. India’s Ayushman Bharat covers only USD 1,800 per case, forcing hospitals either to forgo treatment or absorb losses. Similar gaps exist across sub-Saharan Africa and rural Latin America, where import tariffs and currency volatility further inflate prices, limiting neurothrombectomy access to donor-funded pilots.

Restraints Impact Analysis of Neurothrombectomy Devices Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device & procedure cost in emerging markets | -1.4% | APAC, South America, MEA | Medium term (2-4 years) |

| Shortage of trained neuro-interventionists outside urban centers | -1.1% | Global, particularly acute in rural areas | Long term (≥ 4 years) |

| Supply-chain vulnerability for nitinol & platinum-iridium alloys | -0.9% | Global, with acute impact on specialized manufacturers | Short term (≤ 2 years) |

| Reimbursement delays for posterior-circulation thrombectomies | -0.7% | North America & Europe, selective payer policies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory and Clinical-Trial Requirements

The FDA’s 21 CFR 882.5600 classification mandates PMA filings backed by randomized trials enrolling at least 200 patients, a hurdle that inflates per-patient trial cost to USD 50,000. Europe’s Medical Device Regulation adds post-market audit layers that can stretch certification timelines to three years, disadvantages small innovators, and slows the release cadence of next-generation retrieval architectures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Neurothrombectomy Devices Market Segment Analysis

By Product Type:

Aspiration Momentum Picks UpStent retrievers secured 41.62% of 2025 revenue, yet aspiration catheters are advancing at a 10.13% CAGR, nearly double the overall neurothrombectomy devices market rate. Lower exchange counts and shorter fluoroscopy times make direct aspiration USD 2,000-3,000 cheaper per case. Combined aspiration-stent systems are emerging but await long-term outcome data. Balloon guide catheters maintain steady demand because proximal flow arrest minimizes emboli, whereas vascular snares remain a niche rescue option.

Second-generation aspiration platforms such as Medtronic React and Stryker Catalyst use graduated shaft stiffness for pushability while keeping soft distal tips. The ADAPT protocol now guides about 40% of U.S. thrombectomy first passes, though stent retrievers still dominate distal M2/M3 cases where small vessels hamper catheter delivery. Faster 510(k) cycles encourage more new entrants, intensifying price competition and broadening the neurothrombectomy devices market choice set.

By Access Route:

Radial Techniques Challenge Femoral DominanceTrans-femoral access held 76.13% share in 2025, sustained by larger vessel caliber and operator familiarity, yet radial and brachial entry sites are climbing at a 9.34% CAGR. Radial access cuts groin complications and supports same-day discharge, a selling point for ambulatory centers. Direct carotid puncture serves <3% of cases but grows 8-9% where arch tortuosity blocks traditional routes.

Learning curves of 20-30 cases elevate fluoroscopy times early on, but Japanese registry data show parity with femoral success once skills mature. Slender 6-French guide systems can limit inner lumen for large aspiration catheters, occasionally forcing access crossover mid-procedure, yet patient-reported comfort scores favor radial entry.

By Application:

Off-Label Uses Gain GroundAcute ischemic stroke contributed 76.25% of 2025 procedures, driven by a persistent global caseload near 12 million events annually. Off-label uses in arteriovenous malformations and fistulas expand at an 8.64% CAGR as operators employ aspiration catheters to clear intraprocedural thrombus. Cerebral aneurysm thrombosis, while rare, leverages retrieval devices to protect distal territories when sac clotting threatens flow.

Large-core trials such as SELECT2 and ANGEL-ASPECT enrolled >2,000 patients and widened eligibility to ASPECTS 3-5, enlarging the neurothrombectomy devices market size without inflating stroke incidence. Basilar artery evidence remains mixed, so most payers reimburse under existing stroke DRGs rather than create new codes.

By Treatment Window:

Imaging Extends EligibilityProcedures inside 6 hours still account for 66.91% of volume, reflecting early-trial legacies, yet 6-to-24-hour cases are growing 10.35% per year thanks to CT perfusion and automated mismatch software. Wake-up strokes constitute a smaller but rising cohort because collateral-rich tissue may stay salvageable well past 24 hours.

RapidAI and Brainomix generate perfusion maps within five minutes, enabling community hospitals to triage late presenters without on-site neuroradiologists. Extended-window growth is faster in low- and middle-income countries where transport delays make early arrival rare, whereas the sub-6-hour segment in high-income regions edges toward saturation.

By End User:

ASC Models EmergeHospitals controlled 67.12% of 2025 spending, justified by USD 2-3 million biplane labs and on-site neuro-ICUs. Ambulatory surgical centers are advancing 8.13% annually, treating NIHSS <10 patients under conscious sedation and discharging within 23 hours. However, CMS approval for ASC thrombectomy remains state-dependent, and liability insurers demand higher cover because intensive care beds are off-site.

Device makers now bundle guide catheters, aspiration systems, and hemostasis patches in single-use trays tailored for ASCs, shrinking setup time and inventory costs. Primary stroke centers continue to act mainly as referring hubs, stabilizing patients and organizing transport to thrombectomy-capable facilities.

Geography Analysis

North America Neurothrombectomy Devices Market

North America held 39.13% share in 2025, anchored by 1,600 neurointerventionalists, 1,500+ thrombectomy-capable centers, and robust Medicare reimbursement. Canada’s provincial stroke networks lift access yet still perform about 30% fewer procedures per capita than the United States because of longer imaging queues. Mexico presents a two-tier structure: private hospitals in major metros match U.S. standards, while public facilities lack specialists, leaving up to 80% of candidates untreated.

APAC Neurothrombectomy Devices Market

Asia-Pacific is the fastest-growing region at an 8.12% CAGR, underpinned by China’s nationwide stroke-center mandate and India’s hub-and-spoke telestroke rollouts. Chinese device makers already own ~25% domestic share through prices that undercut imports by 40-50%, pressuring multinationals to localize production. Japan’s aging society sustains roughly 300,000 strokes yearly, with local firms Asahi Intecc and Terumo supplying anatomy-specific microcatheters, while India’s penetration lingers below 2% because only 200 specialists serve 1.4 billion people.

EMEA Neurothrombectomy Devices Market

Europe led by Germany, France, and the United Kingdom, each treating 15-20% of large-vessel occlusions. Updated 2024 ESO guidelines narrowed cross-border practice gaps, and EU structural funds help Poland, the Czech Republic, and Hungary add new labs at 9-10% annual growth. Southern regions like Andalusia and Sicily remain underserved due to specialist shortages, although GCC states in the Middle East are investing aggressively in Western-staffed comprehensive centers. Sub-Saharan Africa represents <1% share because device costs far exceed national health budgets.

Regulatory Landscape

In the United States, neurothrombectomy devices fall under a mature FDA framework that combines high-risk controls with faster access for some catheter-based systems. FDA guidance for pre-clinical and clinical studies shapes evidence generation, and recent 510(k) clearances such as Phenox pRESET Delta in February 2025 and Akura Thrombectomy System in November 2025 point to continued reliance on substantial-equivalence pathways for many thrombectomy-adjacent device submissions. This tends to speed product refresh cycles versus trial-heavy routes.

In Europe, implementation of the EU Medical Device Regulation (MDR) continues to affect timelines and post-market obligations, while policy work aims to reduce friction and improve predictability. In May 2026, the European Commission adopted Implementing Regulation (EU) 2026/977 to set more uniform requirements for conformity assessment and notified bodies. In June 2026, ESMINT and partner societies published physician-driven consensus standards on clinical evidence for high-risk endovascular stroke devices, indicating more harmonized expectations alongside ongoing MDR revision efforts. In Japan, PMDA oversight and reimbursement-linked commercialization remain central to adoption, illustrated by Terumo Neuro launching the WovenEndoBridge 17 system in May 2026 following regulatory approval in November 2025.

Value Chain Analysis

The neurothrombectomy devices value chain begins with specialized raw materials, including nitinol and high-performance polymers, and moves into precision component fabrication such as braiding, laser cutting, coating, and micro-molding. Cleanroom assembly, sterilization, and batch release follow under stringent quality systems. OEMs and contract manufacturers must validate performance characteristics such as trackability, kink resistance, radiopacity, and aspiration flow, then support regulatory documentation and clinical evidence generation tied to hospital formulary decisions and neurointerventional lab standardization.

Downstream, distribution relies on a mix of direct sales to comprehensive stroke centers and group purchasing or tender channels for multi-hospital networks. Training, case support, and procedural workflow integration are emphasized across guide catheters, intermediate/aspiration catheters, and retrieval platforms. 2026 clearances show how innovation moves through this chain: Perfuze secured FDA 510(k) clearance in March 2026 for the Millipede88 super-bore aspiration catheter for standalone direct aspiration, while Penumbra received FDA clearance in June 2026 for THUNDERBOLT, a computer-assisted vacuum thrombectomy platform. This increases the role of software-assisted consoles alongside disposable catheters and consumables.

Competitive Landscape

The four key players includes Medtronic, Stryker, Penumbra, and Cerenovus. Medtronic booked USD 9.846 billion in FY2025 neuroscience revenue and bundles Solitaire X retrievers with React aspiration and Pipeline flow-diversion stents under volume contracts. Stryker generated USD 1.307 billion in 2024 neurovascular sales and added hemorrhage technology via its 2024 buyout of NICO Corporation. Penumbra still leads aspiration innovation with the Lightning platform, while Cerenovus exploits Johnson & Johnson’s supply chain to push EmboTrap and Cereglide in Europe and Asia.

Start-ups are exploiting patent expiries on early retrievers. Imperative Care raised USD 260 million to commercialize the Zoom combined system that cut procedure times 25% in its IMPERATIVE trial. Rapid Medical’s Comaneci flow-arrest device and Perflow’s ANAIS funnel catheter tackle niche clot morphologies. FDA PMA costs and MDR audits favor capital-rich incumbents, yet Asian biosimilar contenders now market retrievers at half Western prices in cost-sensitive regions, testing brand loyalty and compressing margins across the neurothrombectomy devices market.

Neurothrombectomy Devices Industry Leaders

Medtronic plc

Stryker Corporation

Johnson & Johnson

Penumbra, Inc.

Terumo Corporation

- *Disclaimer: Major Players sorted in no particular order

Neurothrombectomy Devices Market Companies Covered in this Report

- Abbott Laboratories

- Acandis GmbH & Co. KG

- AngioDynamics

- Argon Medical Devices

- Asahi Intecc Co., Ltd.

- Boston Scientific

- Imperative Care

- Inari Medical

- Johnson & Johnson

- Medtronic

- MicroPort

- MicroVention

- Penumbra

- Perflow Medical

- Phenox

- Rapid Medical

- Shanghai HeartCare Medical Technology

- Straub Medical

- Stryker

- Terumo

- ZYLOX-Tonbridge Medical Technology

Market Opportunities and Future Outlook

Technology whitespace is emerging around larger-bore aspiration, adjustable retrieval mechanics, and computer-assisted vacuum thrombectomy platforms that target faster clot ingestion and fewer device exchanges. Multiple 2026 U.S. clearances demonstrate the pace of iteration and support differentiated value propositions focused on first-pass success and workflow simplification. Examples include Verge Medicals RoVo Mechanical Thrombectomy System (FDA 510(k) clearance in January 2026), Perfuzes Millipede88 super-bore aspiration catheter (March 2026), Rapid Medicals TIGERTRIEVER 25 adjustable device (April 2026), and Penumbras THUNDERBOLT computer-assisted vacuum thrombectomy platform (FDA clearance in June 2026, along with a CE mark in June 2026).

Portfolio integration across the procedure continuum is another opportunity area as providers increasingly standardize thrombectomy trays and purchasing at the system level. Medtronics completion of the USD 550 million acquisition of Scientia Vascular in June 2026 illustrates this consolidation theme, with an intent to combine access products (guidewires and catheters) with established neurovascular therapeutic lines. That structure can support bundled contracting and tighter interoperability across devices used from groin or radial access through intracranial clot engagement.

Recent Industry Developments in Neurothrombectomy Devices Market

- July 2026: Penumbra enrolled the first patient in its FORWARD study evaluating mechanical thrombectomy and computer-assisted vacuum thrombectomy (CAVT) for distal acute ischemic stroke. The study design supports prospective evidence generation in more complex distal territories, extending validation beyond core large-vessel occlusion use cases.

- June 2026: Medtronic completed its USD 550 million acquisition of Scientia Vascular to integrate specialized neurovascular access products with its existing therapeutic portfolio. The transaction strengthens end-to-end coverage for stroke procedures and supports broader portfolio bundling across guidewires, catheters, and thrombectomy systems.

- July 2025: Stryker announced the launch of the InThrill Thrombectomy System under Inari Medical, expanding its thrombectomy technology set. The launch adds another platform option for hospitals evaluating device performance, training needs, and procedural standardization across their neurointerventional labs.

Neurothrombectomy Devices Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers the revenue generated from devices used in neurothrombectomy procedures to remove or break blood clots in the brain, mainly in acute ischemic stroke care. It includes the device and procedure-linked consumables sold for use across relevant hospital and stroke-care settings.

Scope exclusions: Adjacent neurovascular tools used only for aneurysm coiling, flow diversion, or intracranial stenting without a thrombectomy procedure are excluded.

Segments Covered in This Report

- By Product Type

- Stent Retrievers

- Aspiration Devices

- Combined Aspiration–Stent Systems

- Balloon Guide Catheters

- Vascular Snares & Retrieval Devices

- By Access Route

- Trans-femoral

- Trans-radial / Brachial

- Direct Carotid / Percutaneous

- By Application

- Acute Ischemic Stroke

- Cerebral Aneurysm Thrombosis

- Arteriovenous Malformations & Fistulas

- By Treatment Window

- ≤ 6 Hours From Symptom Onset

- > 6 to 24 Hours (Extended Window)

- > 24 Hours (Late-Presenter / Wake-Up Stroke)

- By End User

- Hospitals

- Primary Stroke Centers

- Ambulatory Surgical Centers

- Emergency & Specialty Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the treated stroke pool and the clinical pathway that drives device demand, then aligning it with procedure guidance and outcomes reporting. We refer to public stroke burden and mortality dashboards from sources such as the World Health Organization, along with surveillance and healthcare utilization statistics from sources such as the US CDC and other national health agencies.

To anchor procedure readiness and adoption signals, we also use regulatory and safety disclosures from sources such as the US FDA and the European Medicines Agency, and clinical evidence summaries from peer reviewed journals and conference proceedings in interventional neurology. Additional context comes from device maker public filings and investor decks, association websites related to stroke systems of care, and reputable press coverage of guideline updates. Where a gap exists on company revenue splits or pricing direction, we also lean on approved paid subscriptions for company financials and intelligence and for patent databases to validate innovation activity. The sources listed here are illustrative only, and many other public and paid references were also used for data collection, cross checks, and clarification.

Primary Interviews and Surveys

Primary inputs were used to convert the stroke patient pool into a realistic procedure volume and a usable pricing range, and then to pressure test adoption assumptions. We spoke with a mix of clinicians, hospital procurement stakeholders, distributors, and product specialists across major regions so that reimbursement structures, care pathways, and device mix changes were reflected in the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 14% | APAC: 49% |

| Mid tier: 50% | Functional/Unit leaders: 31% | EMEA: 32% |

| Smaller Players: 19% | Managers: 55% | Americas: 19% |

Market-Sizing & Forecasting

The core sizing logic uses a top-down build that reconstructs demand from stroke incidence, eligibility by treatment window, and the share of patients routed to thrombectomy-capable centers, which is then converted into procedure volumes. Those volumes are priced using an ASP range that reflects device mix in routine practice (for example, stent retrievers versus aspiration-first approaches, and the use of balloon guide catheters) and is adjusted by region to reflect reimbursement and purchasing patterns.

To keep the totals grounded, we corroborate the result with selective bottom-up checks such as sampled hospital usage patterns, channel feedback on unit volumes, and supplier revenue exposure where it is publicly discussed. Key inputs that we track include large vessel occlusion treatment rates, changes in the 6 to 24 hour treatment window share, average devices used per case, procedure growth at primary and comprehensive stroke centers, and price movement tied to catheter and combined system demand. Forecasts are produced using scenario analysis, where procedure growth and ASPs are flexed around expected capacity expansion and clinical practice shifts, and then aligned with what experts see as feasible for their region. When a country data point is thin, we fill gaps using proxy indicators like stroke care infrastructure and historical uptake patterns, and then re-check the implied procedures per center for reasonableness.

Data Validation & Update Cycle

We validate the model through multiple checks so the final number is not driven by a single input. Outputs are compared against independent signals such as reported stroke procedure activity, device launch timing, and visible reimbursement or guideline changes, and then variances are reviewed before sign off.

If an anomaly shows up, such as a sudden jump in implied procedures per site or an ASP that does not match what buyers report, the assumptions are revisited and primary contacts may be re-approached to confirm what changed. Reports are refreshed annually, and interim updates are made when material events occur that can shift volumes or pricing. Before delivery, an analyst completes a final pass so clients receive the most current view available at that time.

Mordor Intelligence's Neurothrombectomy Devices Market Sizing Compared With Other Published Estimates

Published market sizes for neurothrombectomy devices often vary because the counted products, the procedure definition, and the year assumptions are not consistent across publishers. Differences also come from how each estimate converts clinical activity into device revenue, especially when countries have uneven reporting of stroke procedures.

Adjunct neurovascular devices used only for aneurysm coiling and flow diversion sit outside Mordor Intelligence's scope, which narrows the revenue pool compared with estimates that treat the full neurovascular intervention basket as one market. Gaps can also come from how firms treat the 6 to 24 hour window expansion, whether balloon guide catheters and accessory usage are priced as part of the average case, and if currency conversion is taken at an annual average rate or at a point in time.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.83 B (2025) | |

| Trade Journal A | USD 0.74 B (2024) | Uses an earlier base year and a longer horizon, and the sizing logic is not clearly tied to treated patient eligibility by time window, which can understate near term procedure acceleration. |

| Regional Consultancy B | USD 0.76 B (2025) | Applies conservative ASP assumptions and appears to focus on a narrower device bundle per case, which can miss revenue from common accessory usage in routine thrombectomy workflows. |

Across the three figures, the spread mainly traces back to what is counted per procedure and how quickly eligibility and capacity expansion are translated into volume growth. By keeping the inputs tied to procedure volumes, device mix, and region specific pricing checks, the sizing steps stay easy to follow and can be repeated when new clinical or reimbursement signals emerge.

Key Questions Answered in the Report

How fast is the neurothrombectomy devices market expected to grow between 2026 and 2031?

The market is projected to expand from USD 0.874 billion in 2026 to USD 1.19 billion by 2031, at a 6.47% CAGR.

Which product category is advancing the quickest?

Aspiration devices are projected to grow at a 10.13% CAGR through 2031 due to lower procedure times and costs.

What region shows the highest future growth?

Asia-Pacific is forecast to post an 8.12% CAGR, driven by mandated stroke-center rollouts in China and India.

Why are ambulatory surgical centers gaining share?

ASCs handle stable, small-core infarct cases under conscious sedation, enabling 23-hour discharge and trimming facility costs.

What limits adoption in low-income countries?

Device costs of USD 15,000-40,000 per case, scarce insurance coverage, and import tariffs keep penetration below 2% of eligible patients.

Page last updated on: