Oral Care Products Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 34.36 Billion |

| Market Size (2031) | USD 44.91 Billion |

| Growth Rate (2026 - 2031) | 5.50% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oral Care Products Market Analysis by Mordor Intelligence

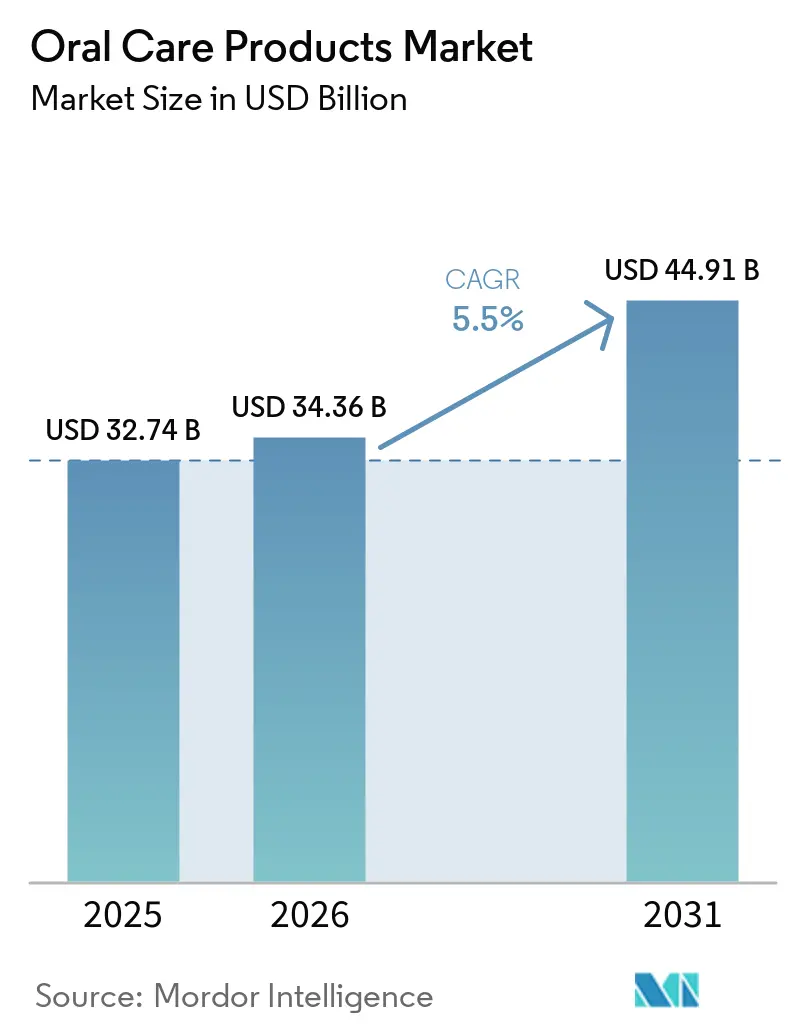

The Oral Care Products Market size is projected to expand from USD 32.74 billion in 2025 and USD 34.36 billion in 2026 to USD 44.91 billion by 2031, registering a CAGR of 5.5% between 2026 to 2031.

The growing demand for preventive health, the rise of digital-first distribution, and the swift commercialization of microbiome science are shaping competitive dynamics more forcefully than top-line growth suggests. Asia-Pacific leads with strong momentum as public-sector campaigns, rising incomes, and localized formulas converge. Meanwhile, mouthwashes infused with probiotics and alcohol-free agents are outpacing the core toothpaste category, and online retail is compressing shelf space for secondary brands. Insurers and corporate wellness programs are also subsidizing smart devices, creating fresh B2B2C channels and shortening product life cycles.

Key Report Takeaways

- By product type, toothpaste captured 34.83% of revenue in 2025, while mouthwashes and rinses are forecast to expand at a 6.24% CAGR through 2031.

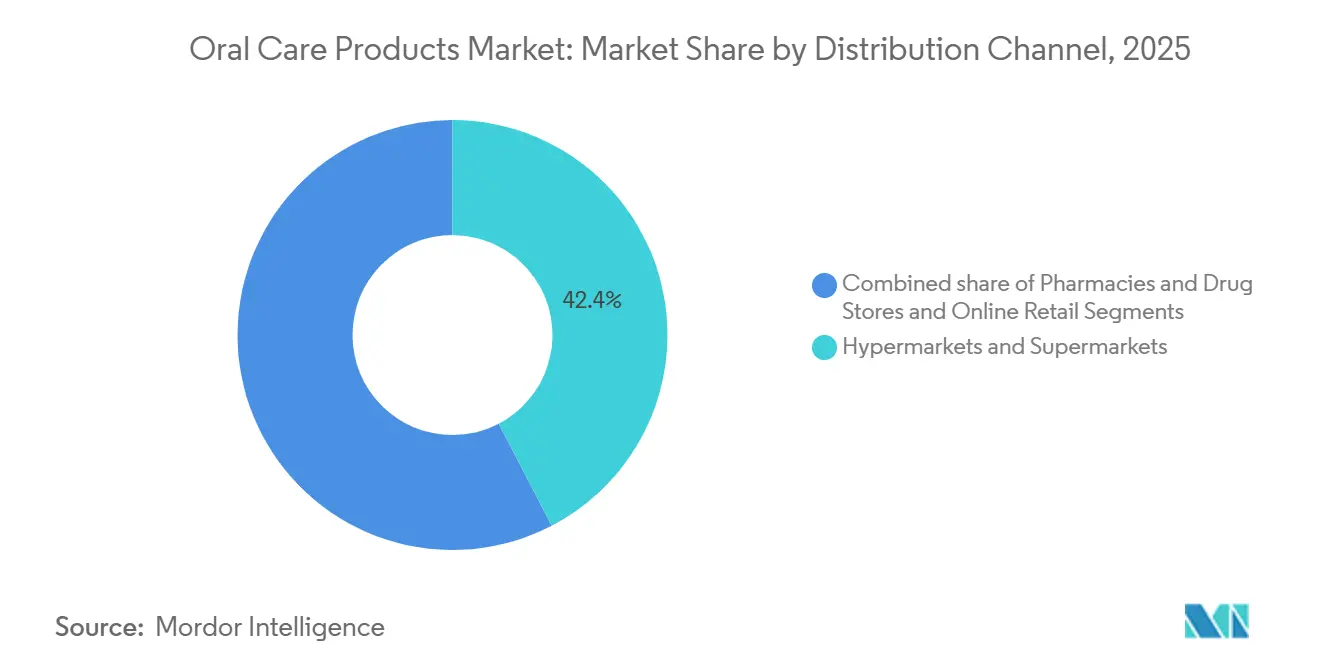

- By distribution channel, hypermarkets and supermarkets accounted for 42.36% of sales in 2025, whereas online retail is expected to grow at a 6.42% CAGR through 2031.

- By end-user, adults accounted for 61.56% of demand in 2025, and the children's segment is projected to advance at a 5.87% CAGR through 2031.

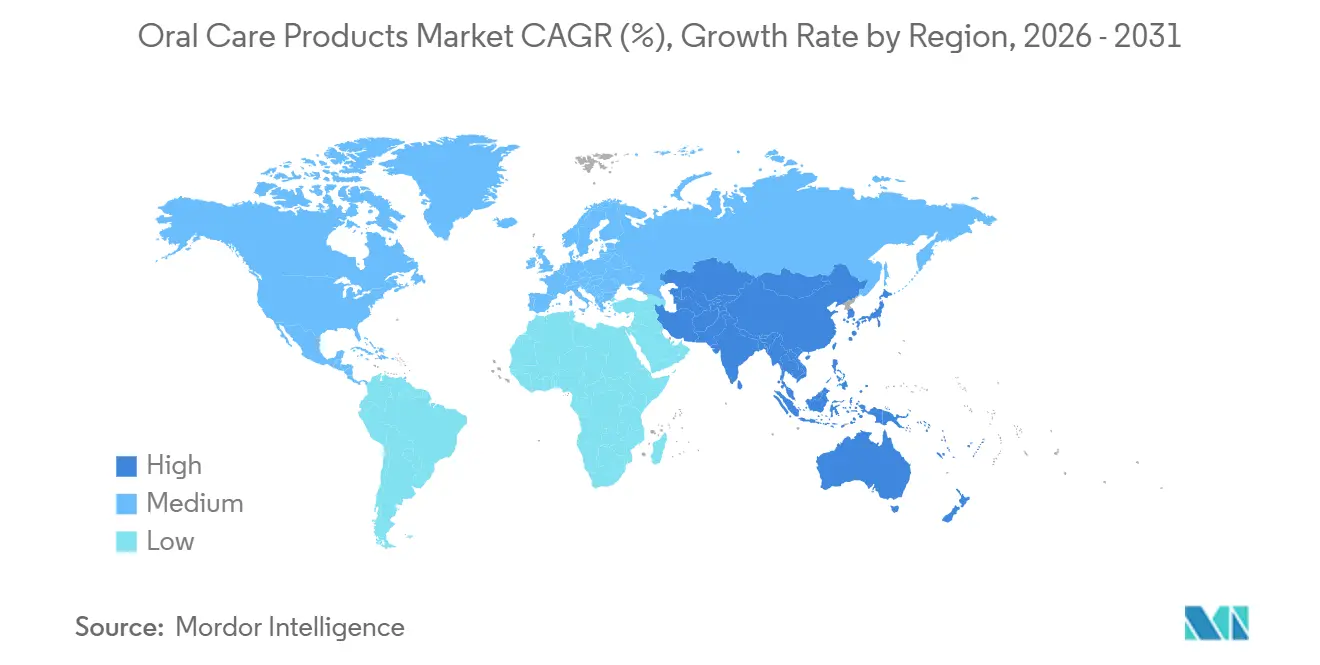

- By geography, Asia-Pacific accounted for 32.40% of 2025 revenue and is poised for a 6.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Oral Care Products Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating global prevalence of dental caries and periodontal diseases | +1.2% | Global, with acute burden in South Asia, Sub-Saharan Africa, Latin America | Long term (≥ 4 years) |

| Rapid expansion of e-commerce and direct-to-consumer distribution | +0.9% | North America, Europe; APAC accelerating post-2024 | Medium term (2-4 years) |

| Rising disposable incomes and urbanization in emerging markets | +0.8% | India, Indonesia, Vietnam, Middle East & Africa | Long term (≥ 4 years) |

| Integration of oral microbiome probiotics into daily hygiene regimens | +0.6% | North America, EU early adopters; APAC premium segments | Medium term (2-4 years) |

| Payor incentivization of preventive oral health within value-based contracts | +0.4% | United States, Germany, Netherlands | Short term (≤ 2 years) |

| Corporate wellness programs subsidizing smart oral devices | +0.3% | North America, Western Europe, urban China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Global Prevalence of Dental Caries and Periodontal Diseases

World Health Organization data indicate that 3.5 billion people live with oral diseases, underscoring the steady demand for daily-use solutions that promise clinical-grade results[1]. Manufacturers are increasing active-ingredient loads and combining whitening with enamel repair, as seen in Colgate-Palmolive’s 2024 Elixir toothpaste. The non-discretionary nature of oral care buffers category volumes during economic downturns and sustains growth in both mature and developing countries.

Rapid Expansion of E-Commerce and Direct-to-Consumer Distribution

Subscription models and social media discovery drove e-commerce penetration above 25% of total category sales in North America and Europe in 2025, while China’s Tmall and JD.com surpassed 30%. Digital-native brands bypass shelf constraints and maintain healthier margins, prompting incumbents to launch their own proprietary direct-to-consumer (D2C) portals and data-driven replenishment programs.

Rising Disposable Incomes and Urbanization in Emerging Markets

Higher earnings in India, Indonesia, and Vietnam are spurring the trial of premium products, ranging from herbal toothpaste to electric toothbrushes. At the same time, Gulf Cooperation Council markets demand halal and alcohol-free variants. Urban consumers are increasingly adopting interdental tools and whitening strips, driving incremental value growth.

Integration of Oral Microbiome Probiotics into Daily Hygiene Regimens

Products featuring Lactobacillus reuteri and Streptococcus salivarius gained traction in pharmacies in 2025 for the relief of gingivitis and halitosis. Patents filed by Colgate-Palmolive and Unilever signal intent to scale probiotic-infused pastes, validating the long-term shift from antibacterial to microbiome-balancing strategies.

Restraints Impact Analysis of Oral Care Products Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Scrutiny Of Fluoride And Titanium Dioxide In Oral Formulations | -0.5% | European Union focus, fluoride debates in North America and Australia | Medium term (2-4 years) |

| Volatility In Raw Material Prices For Sorbitol, Silica, And Packaging Plastics | -0.4% | Global, acute pressure in Asia-Pacific and Latin America | Short term (≤ 2 years) |

| Supply-Chain Emissions Targets Limiting Aerosol Propellant Use In Whitening Sprays | -0.3% | North America and Europe, with emerging adoption in Japan | Medium term (2-4 years) |

| Data Privacy Concerns Around Connected Toothbrush Usage Analytics | -0.2% | North America and European Union | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Scrutiny of Fluoride and Titanium Dioxide in Oral Formulations

The European Food Safety Authority ruled titanium dioxide unsafe, triggering reformulation or withdrawal of whitening pastes across member states[2]. Parallel debates over fluoride in North America add complexity, compelling brands to supply both fluoride-free and fluoride-rich options, which raises SKU counts and inventory costs.

Volatility in Raw-Material Prices for Sorbitol, Silica, and Packaging Plastics

Energy shocks and tight corn-syrup supply widened spot price swings for sorbitol to USD 800–1,100 per metric ton in 2025, squeezing margins particularly in price-sensitive APAC markets. Colgate-Palmolive attributed a 150-basis-point gross-margin dip in 2024 to input inflation[3]. Smaller regional players with limited hedging options face pressure to consolidate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Oral Care Products Market Segment Analysis

By Product Type:

Probiotics Propel Mouthwash GrowthMouthwashes and rinses are projected to lead value expansion, climbing at 6.24% CAGR on the back of alcohol-free and probiotic formulas that rebalance the oral microbiome. Toothpaste still generated 34.83% of 2025 revenue, thanks to whitening and sensitivity-relief sublines; however, the share is gradually shifting to functional rinses and smart brushes. The oral care products market size for mouthwashes is expected to exceed USD 11 billion by 2031, based on current growth trajectories.

Smart electric toothbrushes, boosted by AI guidance and app gamification, command premium price points, while interdental brushes and floss benefit from dentist-driven awareness. Colgate-Palmolive’s launch of a probiotic mouthwash in 2024 and Unilever’s enzyme-activated whitening paste illustrate sustained innovation. Overall, the oral care products market continues to bifurcate between high-volume toothpaste and higher-margin adjunct categories.

By Distribution Channel:

E-Commerce Disrupts Shelf DominanceHypermarkets and supermarkets captured 42.36% of 2025 sales, but online retail is expected to chalk up the fastest gains at 6.42% CAGR through 2031. Direct-to-consumer brands such as Quip leverage subscription replenishment to improve lifetime value, forcing incumbents to optimize digital merchandising and last-mile fulfillment.

Pharmacies retain importance for therapeutic SKUs, while big-box retailers expand private labels to defend foot traffic. The oral care products market is increasingly shaped by data-driven targeting, with digital shelves placing smaller challenger brands one click away from category leaders. As a result, margins hinge on supply chain agility and disciplined customer acquisition costs.

By End-User:

Gamification Unlocks Children’s GrowthAdults represented 61.56% of 2025 demand, yet the children segment is poised for a 5.87% CAGR through gamified brushing experiences and sugar-free flavors. Philips Sonicare For Kids and Oral-B Junior use Bluetooth connectivity to reward consistent brushing, converting short-attention-span users into loyal customers.

Elderly consumers continue to demand sensitivity-relief pastes and denture-care solutions, underscoring the need for age-tailored products. Brands investing in pediatric lines today aim to create lifetime customer value, underscoring how the oral care products market rewards early habit formation backed by engaging digital ecosystems.

Geography Analysis

APAC Oral Care Products Market

The Asia-Pacific region dominated with 32.40% revenue in 2025 and is forecasted to grow at a 6.89% CAGR as government campaigns and mobile-commerce growth accelerate uptake. India’s school-based fluoride-rinse programs and China’s live-stream shopping contribute to both wider penetration and premium trading-up. Japan’s aging demographic drives demand for sensitive and denture-care products, while Indonesia and Vietnam experience double-digit growth in electric toothbrush adoption.

North America and Europe Oral Care Products Market

North America and Europe are expected to maintain modest growth, buoyed by premiumization and value-based insurance schemes. U.S. carriers subsidize smart brushes, and Germany reimburses high-fluoride pastes, channeling demand into evidence-backed products. The swift reformulation of products influences the oral care products market share in Europe to comply with titanium-dioxide restrictions, a capability that favors scaled incumbents.

South America and MEA Oral Care Products Market

The Middle East and Africa are registering an accelerating consumption of halal-certified and alcohol-free rinses. At the same time, South America balances economic volatility with steady toothpaste volumes in Brazil and Argentina. Urban centers such as São Paulo and Dubai present concentrated opportunities for whitening and smart devices, confirming the geographic spread of premium niches.

Competitive Landscape

Colgate-Palmolive, Procter & Gamble, Unilever, Haleon, and Church & Dwight collectively held nearly 60% of the global revenue in 2025; yet, agile entrants are eroding their share in high-growth pockets. Colgate-Palmolive’s takeover of Kolibree and Procter & Gamble’s AI-enabled Oral-B iO Series exemplify incumbent moves to defend leadership through connected hardware.

BioGaia and BLIS Technologies carve out microbiome niches via pharmacy partnerships and clinical evidence. Philips Sonicare 9900 Prestige sets the bar for smart brushes, prompting rival launches and deepening data-driven engagement. Regulatory mastery and scale still confer advantages, but speed in reformulating ingredients and iterating direct-to-consumer (D2C) models increasingly defines the competitive edge.

Retailer private labels and influencer-fronted challenger brands intensify pricing pressure, especially online. Consequently, the oral care products industry emphasizes portfolio differentiation through science-based claims, sustainable packaging, and omnichannel availability to sustain margins.

Oral Care Products Industry Leaders

Colgate-Palmolive Company

Procter & Gamble Co.

Unilever PLC

Johnson & Johnson (Kenvue)

GlaxoSmithKline

- *Disclaimer: Major Players sorted in no particular order

Oral Care Products Market Companies Covered in this Report

- Church & Dwight

- Colgate-Palmolive Company

- Dabur India Ltd.

- Dentsply Sirona

- Dr. Fresh

- GC International AG

- GlaxoSmithKline

- Henkel

- Himalaya

- Straumann Group

- Kenvue

- Koninklijke Philips

- Lion

- Panasonic Holdings Corp.

- Procter & Gamble

- Solventum

- Sunstar Suisse

- Unilever

- Water Pik

- Young Innovations, Inc.

Recent Industry Developments in Oral Care Products Market

- January 2026: Propr, an innovative oral care company, launched Propr Brush. This revolutionary toothbrush is designed to gently clean teeth and gums while reducing the damage associated with traditional brushes. The new product aims to improve oral health with advanced, gentle cleaning technology.

- December 2025: Toothpod, a startup from the University of Toronto launched a new "smart" dental gum. The gum is designed to support oral health on the go. It contains ingredients that promote remineralization, combat microbes, and reduce inflammation when a toothbrush isn't accessible.

- September 2025: Clove Oral Care has announced its entry into the consumer oral care market with a new line of clinically tested, customized toothpaste and toothbrushes. The launch aims to enhance preventive care and oral health education in India with dentist-perfected solutions. The products are now available online on their website, Amazon, Flipkart, and select modern trade outlets.

- October 2025: TheraBreath, one of the leading alcohol-free mouthwash brands in the United States, announced the launch of a new line of dentist-formulated toothpastes. These premium toothpastes, containing stannous fluoride, are designed to complement their popular rinses for enhanced oral care. The new products aim to provide superior flavor and long-lasting fresh breath.

Oral Care Products Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the global oral care products market as the annual retail and institutional sales of toothpastes, toothbrushes and heads, mouthwashes or rinses, dental accessories such as floss, water jets, breath fresheners, cosmetic whitening kits, denture cleansers, and other over-the-counter cleaning products that consumers and dental professionals purchase for use at home. According to Mordor Intelligence, professional dental procedures, prescription therapeutics, and clinic services remain outside this scope.

Scope exclusion: We exclude in-clinic treatments, prescription-only mouth rinses, and dental equipment from the addressed market.

Segments Covered in This Report

- By Product Type

- Toothpaste

- Pastes

- Gels

- Powders

- Polishes

- Toothbrushes & Accessories

- Manual

- Power (Oscillating, Sonic, Ultrasonic)

- Battery-Powered Toothbrushes

- Replacement Toothbrush Heads

- Mouthwashes / Rinses

- Non-Medicated Mouthwashes

- Medicated Mouthwashes

- Dental Accessories / Ancillaries

- Dental Flosses

- Breath Fresheners

- Cosmetic Dental Whitening Products

- Dental Water Jets

- Dental Products

- Fixatives

- Other Denture Products

- Dental Prosthesis Cleaning Solutions

- Toothpaste

- By Distribution Channel

- Hypermarkets & Supermarkets

- Pharmacies & Drug Stores

- Online Retail

- By End-User

- Children (0–12 Yrs)

- Adolescents (13–17 Yrs)

- Adults (18–59 Yrs)

- Geriatric (60+ Yrs)

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East And Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed upstream ingredient suppliers, retail buyers, practicing dentists, and digital-first oral-care start-ups across North America, Europe, Asia-Pacific, and Latin America. These conversations confirmed price corridors, penetration rates, and emerging consumer preferences, filling gaps left by secondary data.

Desk Research

We started by mapping category demand through public datasets from bodies such as the World Health Organization, World Customs Organization trade codes, the American Dental Association, Eurostat retail panels, and national health surveys that track caries prevalence and oral-hygiene habits. Company 10-K filings, investor decks, and retail scanner feeds then provided brand share trends and average selling prices.

To refine regional splits, our analysts accessed D and B Hoovers for company revenue breakouts and Dow Jones Factiva for shipment-level news, and we referenced patent counts in Questel to gauge innovation cycles. The desk sources listed are illustrative, and many other open or subscription references informed data collection, validation, and clarification.

Market-Sizing & Forecasting

A blended top-down reconstruction of national retail sales, built from production, import-export, and household-expenditure series, formed the initial 2025 baseline. We cross-checked totals with selective bottom-up approximations derived from sampled unit volumes and channel-specific average prices before calibrating for inventory carryover. Key model drivers include population by age band, caries incidence, per-capita toothpaste usage, electric-brush penetration, e-commerce share, and ingredient cost trends. Five-year outlooks were generated through multivariate regressions combined with scenario analysis on disposable income and preventive-care uptake.

Data Validation & Update Cycle

Outputs pass through anomaly scans, peer reviews, and senior analyst sign-off. The dataset refreshes annually, with interim updates triggered by material events such as regulatory changes or large acquisitions, so clients receive the latest view.

How Mordor Intelligence's Oral Care Products Market Size Compares to Other Published Estimates

Published values often diverge because firms differ in product basket, channel mix, and refresh cadence, and our disciplined variable selection keeps estimates grounded.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 34.98 B | Mordor Intelligence | |

| USD 33.63 B (2024) | Regional Consultancy A | limited geography and offline-only sales tracking |

| USD 37.21 B | Global Consultancy B | includes therapeutic rinses and orthodontic wax |

| USD 39.94 B | Industry Association C | shipment multipliers without retail price validation |

We observe that once scope, channels, and price verification are aligned, Mordor's balanced baseline emerges as the most transparent and repeatable starting point for strategic decisions.

Key Questions Answered in the Report

What is the current value of the oral care products market?

The oral care products market size is USD 34.36 billion in 2026.

How fast is the global market growing to 2031?

It is projected to grow at a 5.50% CAGR, reaching USD 44.91 billion by 2031.

Which product segment is expanding the quickest?

Probiotic-infused mouthwashes and rinses are forecast for the highest 6.24% CAGR through 2031.

Where is regional growth strongest?

Asia-Pacific leads with a 6.89% CAGR, backed by rising incomes and public-health initiatives.

How are insurers influencing demand?

U.S. and European insurers subsidize smart brushes and high-fluoride pastes, linking usage data to premium reductions.

Which players dominate connected toothbrush technology?

Philips Sonicare and Procter & Gamble's Oral-B head the smart-brush segment with AI-enabled models.

Page last updated on: