Anastomosis Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.33 Billion |

| Market Size (2031) | USD 5.63 Billion |

| Growth Rate (2026 - 2031) | 5.37% CAGR |

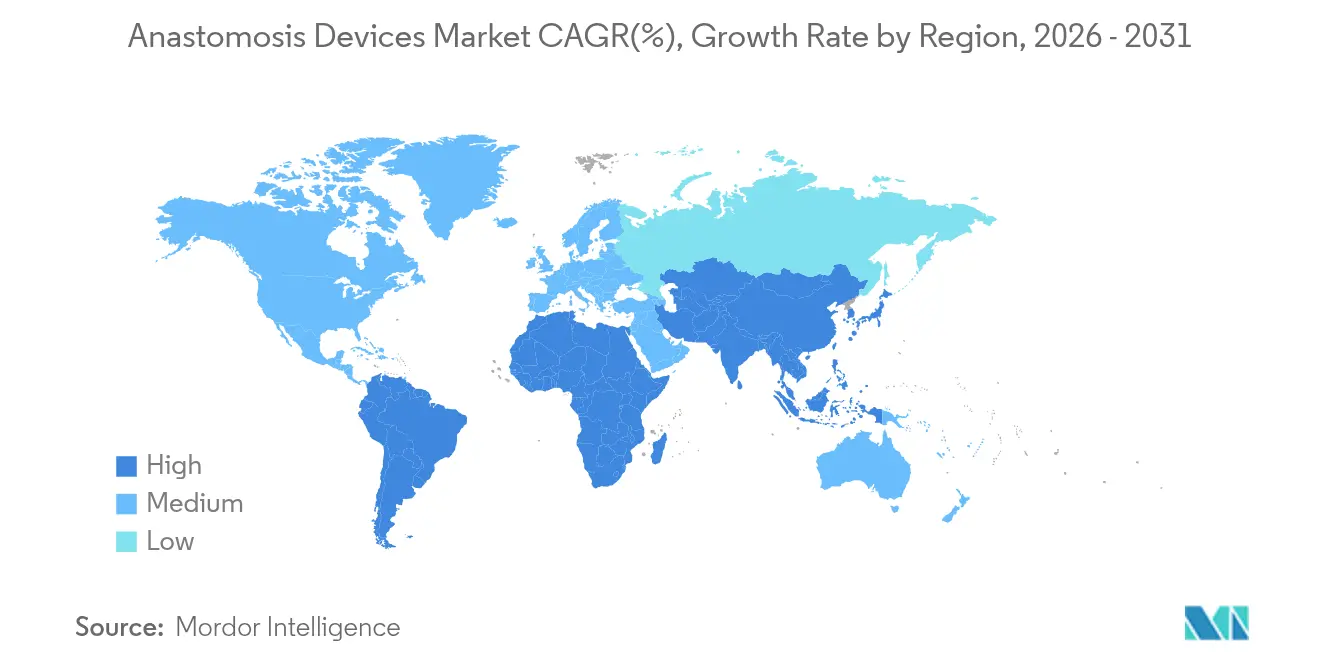

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

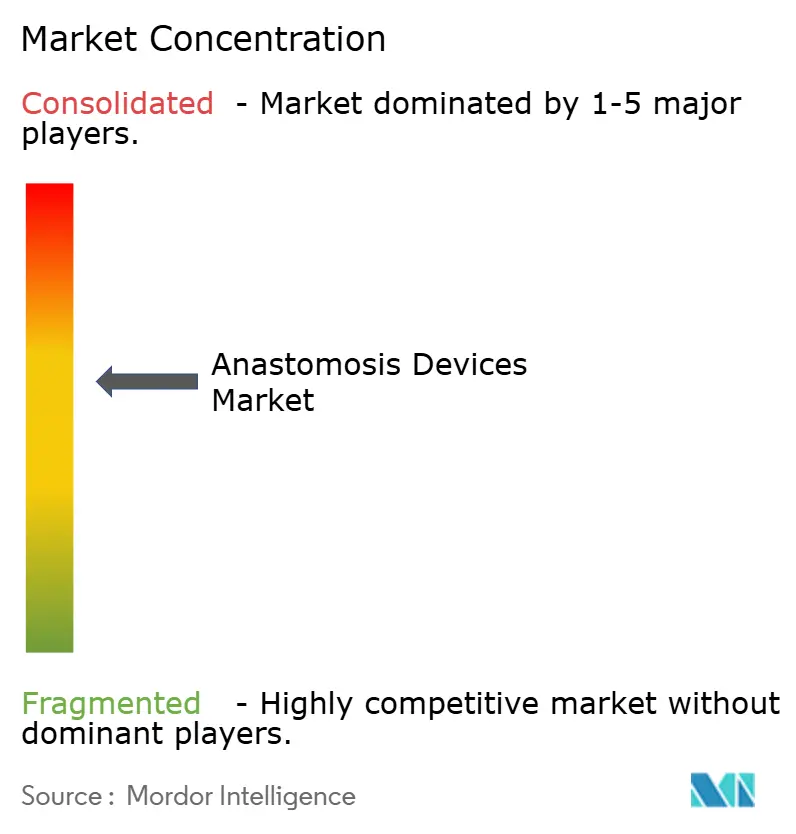

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anastomosis Devices Market Analysis by Mordor Intelligence

The anastomosis devices market size in 2026 is estimated at USD 4.33 billion, growing from 2025 value of USD 4.11 billion with 2031 projections showing USD 5.63 billion, growing at 5.37% CAGR over 2026-2031. Consistent demand for dependable tissue‐connection solutions in cardiovascular, gastrointestinal and bariatric surgeries anchors this expansion. Growth momentum flows from rapid adoption of robotic-assisted connectors, rising use of bioabsorbable and hydrogel materials, and steady procedure volumes in aging populations. Manufacturers are funnelling R&D budgets toward AI-enabled stapling platforms and suture-less magnetic devices, which promise quicker healing and fewer leaks. Simultaneously, care is shifting to outpatient settings, prompting ambulatory surgical centers (ASCs) to specify lightweight, single-use systems that trim turnaround time. Yet recalls and price pressure under value-based care are tempering overall revenue acceleration.

Key Report Takeaways

- By product type, surgical staplers led with 40.78% of the anastomosis devices market share in 2025, while compression and magnetic rings & clips are projected to expand at a 7.55% CAGR through 2031.

- By usage, disposables accounted for 67.92% of the anastomosis devices market size in 2025; reusable platforms are poised for a 7.24% CAGR to 2031.

- By device technology, manual systems held 47.76% revenue share in 2025, whereas robotic-assisted and automated connectors are set for a 8.88% CAGR through 2031.

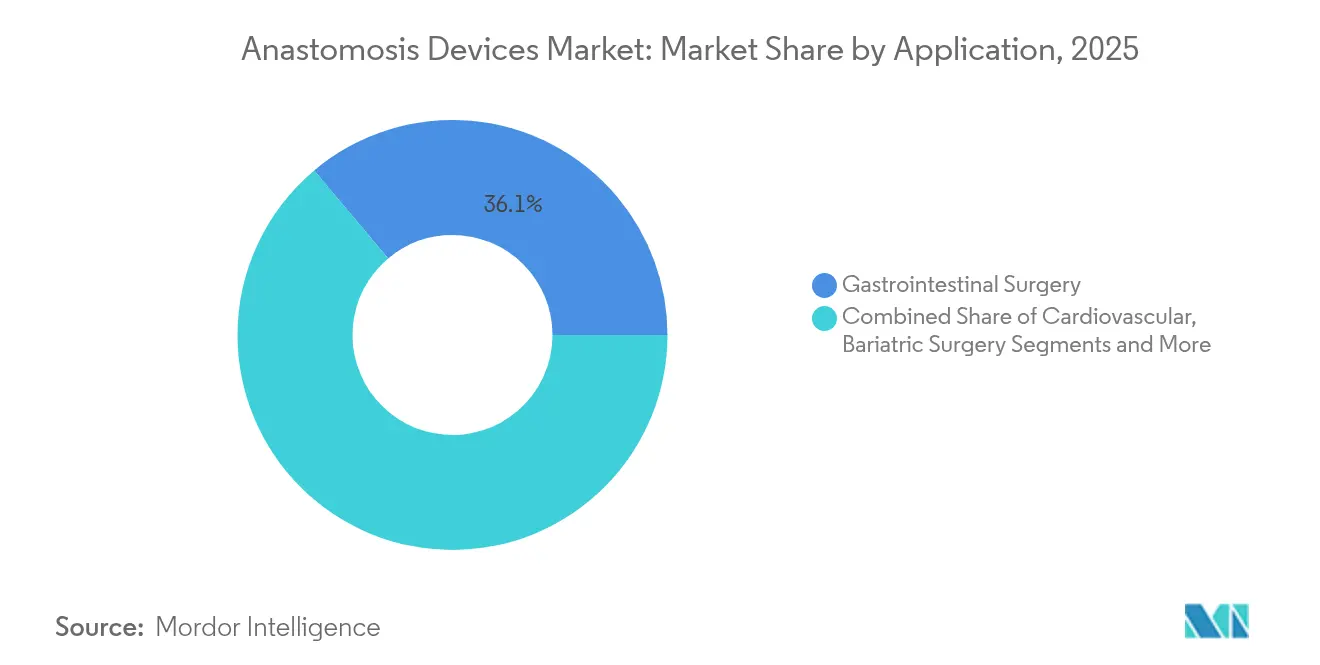

- By application, gastrointestinal surgery contributed 36.12% of 2025 revenue; bariatric and metabolic procedures show the fastest trajectory at a 9.04% CAGR to 2031.

- By end user, hospitals captured 68.74% of global sales in 2025, while ASCs are forecast to grow at 8.33% CAGR through 2031.

- By region, North America commanded 38.12% of 2025 revenue; Asia-Pacific is the fastest-growing geography at an 8.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Anastomosis Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising volume of surgeries and mounting chronic disease burden | +1.2% | Global, strongest in North America, Europe, Japan | Long term (≥ 4 years) |

| Growing adoption of minimally-invasive stapling and sealant technologies | +0.9% | North America and EU lead, APAC rapidly catching up | Medium term (2-4 years) |

| Technological advancement in surgical stapling and suturing devices | +0.8% | Global, R&D centres in US, Germany, China | Medium term (2-4 years) |

| Emergence of suture-less magnetic & nitinol compression devices | +0.6% | APAC core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Robotic assistance enabling automated vessel anastomosis | +0.7% | North America & EU, expanding to APAC premium markets | Medium term (2-4 years) |

| Value-based care focus on post-surgical complications | +0.5% | North America leading, EU following | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising volume of surgeries and mounting chronic disease burden

Surgical procedures keep climbing as populations age and obesity, diabetes and cardiovascular disease spread across both developed and emerging regions. CMS proposed USD 7.4 billion in 2025 ASC payments—USD 202 million more than 2024—while adding 20 extra procedures to the ASC list, signaling higher case throughput.[1]Centers for Medicare & Medicaid Services, “CMS Releases 2025 Proposed Medicare Payment Rule,” ascfocus.orgSingle-anastomosis bariatric techniques such as SADI-S have delivered complete diabetes remission in Chinese cohorts, underlining procedure efficacy and demand. Each incremental case translates into multiple tissue connections, thereby raising unit consumption of anastomosis devices market products. In parallel, robotic platforms are broadening eligibility for complex gastrointestinal reconstructions, indirectly lifting device volumes. Hospitals and ASCs alike are therefore replenishing inventories of circular staplers, linear cutters and magnetic rings to keep pace with caseload growth.

Growing adoption of minimally-invasive stapling and sealant technologies

Laparoscopic and robotic workflows reduce trauma and shorten recovery, so surgeons increasingly favor powered staplers, smart sealants and articulating reloads. ETHICON’s ECHELON Powered Stapler cut bleeding complications by 73% and leaks by 85% versus manual peers. Intuitive’s SureForm features 120° articulation plus SmartFire tissue sensing, ensuring even clamp pressure and staple formation.[2]Intuitive Surgical, “SureForm Stapler with SmartFire,” intuitive.com These performance gains justify premium pricing, helping the anastomosis devices market sustain mid-single-digit growth. Investor confidence is evident, as Lexington Medical attracted growth capital to widen distribution of its minimally-invasive staplers across 35 nations. Convergence between robotics and intelligent fastening elevates technical barriers for late entrants but boosts clinical outcomes.

Technological advancement in surgical stapling and suturing devices

Innovation now targets transformative leaps in leak mitigation and workflow efficiency rather than incremental tweaks. Medtronic’s EEA Circular Stapler with Tri-Staple technology delivered 80% fewer leaks and 140% higher perfusion than rival systems. AI-driven software such as ColonPRO improved polyp-detection accuracy by 9% during colonoscopy, hinting at similar gains in intraoperative anastomosis quality. Investigators have also 3D-printed biodegradable vascular staplers that tailor fit to patient anatomy, foreshadowing custom implants. Sensor-enabled clamps already provide real-time compression metrics, helping surgeons fine-tune firing decisions. Collectively these upgrades cement longer-term demand for premium systems within the anastomosis devices market.

Emergence of suture-less magnetic & nitinol compression devices

Magnetic compression and nitinol rings realign tissue edges without leaving permanent metallic staples. GI Windows Medical secured FDA breakthrough status for a self-forming magnetic device designed for small-bowel anastomosis, accelerating its path to commercial launch.[3]GI Windows Medical, “US FDA Grants Breakthrough Designation for Self-Forming Magnetic Compression Device,” gsmedtech.com The MagDI System later received Class II clearance for duodeno-ileal bypass creation, validating regulatory acceptance of magnetics. Nitinol’s shape memory enables self-expanding couplers that apply uniform pressure as tissue swells, encouraging leak-free healing. Emerging bioabsorbable magnets further minimize foreign‐body risk once healing completes. Surgeons now view these suture-less systems as attractive solutions for delicate pediatric, bariatric and transplant cases, bolstering specialty demand in the anastomosis devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to catheter-based alternatives reducing CABG volumes | -0.8% | North America & EU | Medium term (2-4 years) |

| High capital and single-use costs of advanced staplers/connectors | -0.6% | Global; acute in cost-sensitive markets | Short term (≤ 2 years) |

| Device malfunctions and recalls affecting surgeon confidence | -0.4% | Global; regulatory attention in US/EU | Short term (≤ 2 years) |

| Limited clinical evidence slowing approvals of bioabsorbable glues | -0.3% | Global, varied regulatory thresholds | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift to catheter-based alternatives reducing CABG volumes

Percutaneous coronary interventions and TAVR now treat coronary and valvular disease once reserved for open bypass, cutting surgical case volumes. Boston Scientific’s cardiovascular revenue surged 26.2% in Q1 2025 on interventional cardiology demand. Medtronic’s Evolut FX+ received FDA approval with easier coronary access, further diverting patients from surgical grafting. Cardiovascular surgeons in mature markets therefore require fewer vascular staplers and couplers, dampening one high-value segment of the anastomosis devices market. Emerging economies still rely on CABG due to limited cath-lab infrastructure, partially offsetting the decline.

High capital and single-use costs of advanced staplers/connectors

Operating budgets remain tight as reimbursement gains lag inflation. A study showed robotic stapling can cost EUR 1,500–2,000 per case versus EUR 54 for manual suturing. CMS’s 2.6% ASC rate update for 2025 provides only modest relief. Hospitals are trialling real-time cost dashboards that trimmed thoracoscopic disposable spend by 22.7%. High up-front and per-case costs slow uptake of next-gen connectors, especially in middle-income nations, tempering revenue escalation in the anastomosis devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Usage: Disposables remain dominant while reusables gain ground

Disposables secured 67.92% of the anastomosis devices market share in 2025, driven by zero-reprocessing convenience and strict infection-control protocols. Hospitals appreciate the predictable turnaround and simplified logistics, especially when high case volume stresses central-sterile departments. Many institutions embed single-use staplers into procedure packs, streamlining setup and inventory tracking. However, heightened environmental scrutiny and budget oversight are nudging procurement teams toward reusable loaders and reinforced reload cartridges. The reusable cohort is growing at 7.24% CAGR, reflecting maturation of low-temperature sterilization and validated cleaning workflows. High-volume ASCs now calculate lower total cost of ownership when cases surpass specific break-even counts, improving the segment’s prospects.

Surgeons initially voiced reliability concerns about reusable jaws and knife edges, yet iterative engineering now delivers cycle counts exceeding 50 sterilizations without staple line compromise. Capital-purchase models with vendor-managed inventory further soften adoption hurdles. While disposables will continue dominating the anastomosis devices market for the forecast period, dual-track strategies that pair single-use reloads with reusable handles are becoming common, especially in Europe’s eco-conscious facilities.

By Product Type: Staplers lead, compression devices accelerate

Staplers generated 40.78% of 2025 revenue and remain the default choice thanks to decades of outcome data and surgeon familiarity. Modern linear and circular variants boast triple-row staples, variable height closed-anvil designs, and refined knife blades that minimize tissue drag. Competitive benchmarking shows ETHICON PROXIMATE linear cutters achieve 34% higher leak-pressure thresholds versus alternate brands. Continuous enhancements ensure sustained demand across colorectal, bariatric and thoracic disciplines, anchoring value for incumbent suppliers.

Compression and magnetic rings & clips, although currently smaller in dollars, outpace other categories at 7.55% CAGR through 2031. FDA breakthrough designations signal clinical promise, and early studies reveal lower inflammatory profiles and elimination of retained hard-metal artifacts. Sutureless compression resonates with pediatric and transplant surgeons who prioritize growth accommodation and minimal implant burden. Success stories in animal models and initial human trials are setting the stage for broader reimbursement approval, fueling fresh momentum in the anastomosis devices market.

By Device Technology: Manual persists, robotics surges

Manual systems preserved 47.76% revenue share in 2025 since direct tactile feedback remains invaluable for tailoring bite depth and tension across heterogeneous tissue. Surgeons also appreciate the ability to troubleshoot bleeding immediately after the fire, a nuance still challenging for automation. Powered staplers bridge convenience and surgeon control by lowering squeeze force, particularly beneficial in lengthy bariatric sleeves.

Robotic-assisted connectors are the fastest-rising slice at 8.88% CAGR, thanks to precision articulation and data-rich interfaces. The da Vinci SureForm supplies 120° articulation, enabling deep pelvic anastomosis without rescoping. Automated connectors are now entering trials, aiming to standardize distance between bites and ensure perfect lumen alignment. While capital intensive, these innovations attract flagship academic centers that anchor early adoption curves in the anastomosis devices market.

By Material: Metallic reliability challenged by bioabsorbables

Metallic frames-chiefly stainless steel, titanium and nitinol-underpinned 53.91% of sales in 2025 owing to their strength and corrosion resistance. Nitinol’s shape memory lets couplers expand gently, aligning edges without surgeon micromanagement. Still, the permanence of metal invites long-term artifact concerns in imaging and growth-related complications in pediatrics. Consequently, bioabsorbable polymers and hydrogel composites are climbing at 8.72% CAGR by delivering temporary support that dissolves once healing finalizes. Marine-inspired hydrogel barriers demonstrated improved vascularisation and reduced adhesions in animal anastomoses. Advances in processing are lifting mechanical thresholds, helping bioabsorbables encroach on metallic hegemony in the anastomosis devices market.

Polymer alternatives such as PEEK and polypro ¬pylene serve niches where radiolucency eases post-operative imaging. Drug-eluting layers that release anti-inflammatory agents or growth factors deepen differentiation. As suppliers lock in scalable extrusion and 3D-printing lines, unit cost gaps with metal narrow, making bioabsorbables commercially attractive.

By Application: Gastrointestinal dominance, bariatric momentum

Gastrointestinal (GI) surgery claimed 36.12% of 2025 revenue, benefitting from large procedure volumes in colorectal cancer, Crohn’s disease and ulcerative colitis. Multi-quadrant resections often need two or more anastomoses, multiplying device count per case. Enhanced recovery protocols prioritise leak-free staple lines to avoid costly readmissions, ensuring steady demand for premium reloads within the anastomosis devices market size for this segment.

Bariatric and metabolic operations are expanding fastest at 9.04% CAGR, propelled by global obesity prevalence. Sleeve gastrectomy and SADI-S procedures each rely on long staple lines plus one critical duodeno-ileal connection. Early Chinese experience reported zero leak-related mortality, bolstering surgeon confidence. Emerging economies with rising BMI profiles now reimburse bariatric surgery, widening addressable volume. Cardiovascular, organ transplant and dialysis access remain important but slower-growing domains, often requiring specialty connectors with premium ASPs.

By End User: Hospitals remain anchor, ASCs eclipse growth

Hospitals absorbed 68.74% of worldwide revenue in 2025, reflecting their role in high-acuity reconstructions, trauma and transplant cases that demand broad device catalogues on hand. Centralised purchasing negotiates volume discounts and fosters vendor standardisation. Training fellowships also expose residents to branded systems, reinforcing institutional loyalty in the anastomosis devices market.

ASCs, however, are sprinting ahead at 8.33% CAGR as payers squeeze inpatient reimbursements. CMS’s 2025 proposal lifts ASC payments to USD 7.4 billion and adds 20 procedures to the covered list. Surgeons cherish faster turnover and patient satisfaction, while operators value lower facility overhead. Device makers now craft compact, sterile-packed kits tailored to ASC floorplans, courting this growth pocket. Specialty clinics devoted to bariatric or colorectal care further diversify channels, adopting advanced materials to differentiate outcomes.

Geography Analysis

North America controlled 38.12% of global revenue in 2025, underpinned by concentrated R&D clusters, early technology adoption and robust reimbursement pathways. FDA breakthrough and 510(k) programs accelerate time-to-market for novel compression devices, while large integrated health networks enable swift rollouts across multiple states. Nonetheless, value-based purchasing exerts downward pressure on price, compelling suppliers to emphasise evidence of reduced readmission and leak rates to sustain margin.

Europe follows with strong yet varied demand shaped by national procurement rules and the Medical Device Regulation’s heightened evidence bar. Germany and France champion robotic stapling adoption due to high hospital capital budgets, whereas Southern European systems prioritise cost-effectiveness. Post-Brexit regulatory divergence necessitates separate UK certifications, elongating launch timelines and modestly restraining short-term growth in the anastomosis devices market.

Asia-Pacific registers the fastest CAGR at 8.55% through 2031, thanks to rising disposable incomes, infrastructure expansion and government healthcare investments. Retrospective analysis of 827 robotic SADI-S patients in a Chinese center showed complication rates comparable to gastric bypass, validating local skill levels. Japan’s super-aged demographic demands leak-proof vascular and GI anastomoses, while South Korea’s medical-tourism clusters adopt cutting-edge staplers to attract overseas patients. India implemented a marketing conduct code in 2024, signalling maturing regulatory oversight that encourages multinational entrants. Diverse income tiers generate parallel demand for premium robotic reloads and economical manual staplers, broadening the anastomosis devices market footprint.

Competitive Landscape

The anastomosis devices market is moderately consolidated. Medtronic, Johnson & Johnson and Boston Scientific leverage extensive patent estates, global service teams and recurring reload revenue to secure hospital contracts. Boston Scientific’s USD 1.26 billion Silk Road Medical acquisition reinforced its position in neurovascular access, combining stroke-prevention devices with anastomotic expertise. Merit Medical’s USD 120 million Biolife purchase broadened its haemostatic range, enhancing complementary offerings for post-anastomosis care.

Technology differentiation shapes new entrants’ prospects. Phraxis gained FDA clearance in May 2025 for its Endoforce Connector, a minimally invasive fistula coupler for dialysis access, demonstrating how niche innovation can pierce incumbent walls. GI Windows and Ossio are racing to secure human data for magnetic and bio-integrative staples respectively, positioning themselves as disruptors. Meanwhile, large strategics pursue ecosystem plays: Karl Storz agreed to acquire Asensus Surgical, bringing in digital laparoscopy insights that mesh with stapling portfolios.

Regional manufacturers are also rising. Chinese OEMs supported by domestic procurement quotas offer cost-competitive manual staplers, capturing mid-tier hospitals. Indian firms emphasise reusable platforms aligned with sustainability mandates. Competitive intensity thus spans premium tech battles and price-driven skirmishes, ensuring innovation pipelines remain robust over the forecast horizon.

Anastomosis Devices Industry Leaders

Medtronic plc

Johnson & Johnson

Baxter

B. Braun SE

Boston Scientific Corp

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Johnson & Johnson MedTech introduced a surgical stapler built for complex tissue layers, aiming to cut leaks in challenging GI sites.

- May 2025: Phraxis Inc. received FDA approval for its Endoforce Connector for venous dialysis anastomosis, avoiding surgical dissection and reducing trauma.

- May 2025: Merit Medical finalised a USD 120 million purchase of Biolife, adding StatSeal and WoundSeal haemostatic products to its stable.

- May 2025: Lexington Medical secured growth funding from Ampersand Capital Partners to accelerate its minimally invasive stapling portfolio across 35 countries.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global anastomosis devices market as manufacturer-level revenues from staplers, sutures, clips, rings, sealants, and automated systems used to create surgical connections in cardiovascular, gastrointestinal, bariatric, and other procedures. According to Mordor Intelligence, values cover new single-use and reusable devices sold to hospitals and ambulatory centers worldwide.

Scope exclusion: Veterinary devices, training rigs, and home-use wound closure kits lie outside this scope.

Segmentation Overview

- By Usage

- Disposable

- Reusable

- By Product Type

- Surgical Staplers

- Surgical Sutures

- Surgical Sealants & Adhesives

- Compression / Magnetic Rings & Clips

- By Device Technology

- Manual

- Powered

- Robotic-assisted / Automated Connectors

- By Material

- Metallic (Stainless Steel, Titanium, Nitinol)

- Polymer (PP, ABS, PEEK)

- Bio-absorbable / Hydrogel

- By Application

- Cardiovascular Surgery

- Gastrointestinal Surgery

- Bariatric & Metabolic Surgery

- Organ Transplant & Dialysis Access

- Others (Thoracic, Neuro, Urology)

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed practicing surgeons, sterile-processing leads, and distributors across North America, Europe, and Asia-Pacific to test throughput assumptions, narrow average selling price ranges, and sense-check uptake of robotic stapling technologies.

Desk Research

We mapped procedure pools and device flows through tier-1 public sources such as OECD Health Statistics, WHO Global Health Observatory, CMS inpatient DRG files, Eurostat surgical registers, and the US FDA MAUDE recall database, which anchor volume and safety signals. Trade bodies like the American College of Surgeons, plus patent analytics from Questel, helped us gauge innovation speed and material shifts.

Company 10-Ks, IPO prospectuses, investor decks, and customs shipment data extracted via Volza supplied pricing corridors and directional trade clues before entering our working sheets. The sources named above illustrate the breadth of desk study; many additional references aided validation and clarification.

Market-Sizing & Forecasting

A top-down reconstruction of global major-surgery volumes, split by specialty, set the 2025 baseline and was corroborated with selective bottom-up supplier roll-ups. Core variables include worldwide surgery count, cardiovascular surgery share, disposable penetration, median device price, recall incidence, and hospital capital budgets. Multivariate regression paired with scenario analysis projects each driver, while exponential smoothing trends historical series. Interview-based ranges bridge any residual data gaps.

Data Validation & Update Cycle

Model outputs pass anomaly screens, peer review, and an external expert checkpoint before sign-off. We refresh every twelve months and issue interim revisions when recalls, guideline changes, or major M&A materially alter the market.

Why Mordor's Anastomosis Devices Baseline Inspires Confidence

Published estimates often diverge, driven by mismatched scopes, price levels, and update cadences.

We foreground manufacturer revenue, a clearly defined procedure basket, and annual refreshes that keep our numbers synchronized with real-time signals. Key gap drivers versus alternate publications include inclusion of veterinary demand, legacy procedure mixes, or hospital purchase-price bases rather than factory gate values.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.11 B | Mordor Intelligence | none |

| USD 4.42 B | Regional Consultancy A | Includes veterinary demand and retail mark-ups |

| USD 3.57 B | Trade Journal B | Uses 2019 procedure mix and lower disposable share |

| USD 5.35 B (2024) | Global Consultancy C | Applies hospital purchase prices and optimistic ASP inflation |

The comparison shows that Mordor's disciplined scope selection, transparent variables, and frequent updates provide a balanced, repeatable baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the expected value of the anastomosis devices market by 2031?

The anastomosis devices market is projected to reach USD 5.63 billion by 2031 at a 5.37% CAGR.

Which product segment currently leads revenue?

Surgical staplers lead with 40.78% of global revenue in 2025 due to extensive clinical validation and surgeon familiarity.

Why are ambulatory surgical centers important to future growth?

ASCs are expanding case volumes rapidly and are forecast to grow device purchases at 8.33% CAGR as more procedures shift to outpatient care.

Which geographic region will grow the fastest?

Asia-Pacific is the fastest-growing region, advancing at an 8.55% CAGR through 2031 on the back of infrastructure investment and rising chronic disease prevalence.

What technology trends are reshaping competition?

Robotic-assisted stapling, AI-enabled guidance, and suture-less magnetic compression devices are differentiating next-generation platforms and attracting investment.

Page last updated on: