Turmeric Oleoresin Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

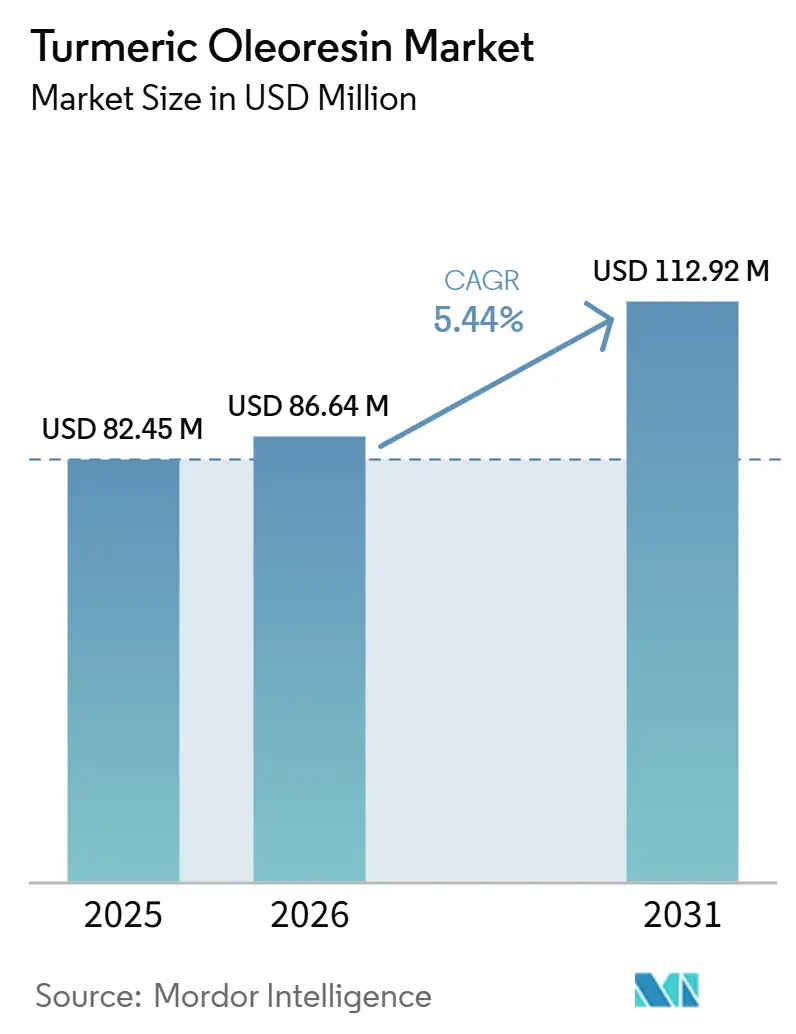

| Market Size (2026) | USD 86.64 Million |

| Market Size (2031) | USD 112.92 Million |

| Growth Rate (2026 - 2031) | 5.44% CAGR |

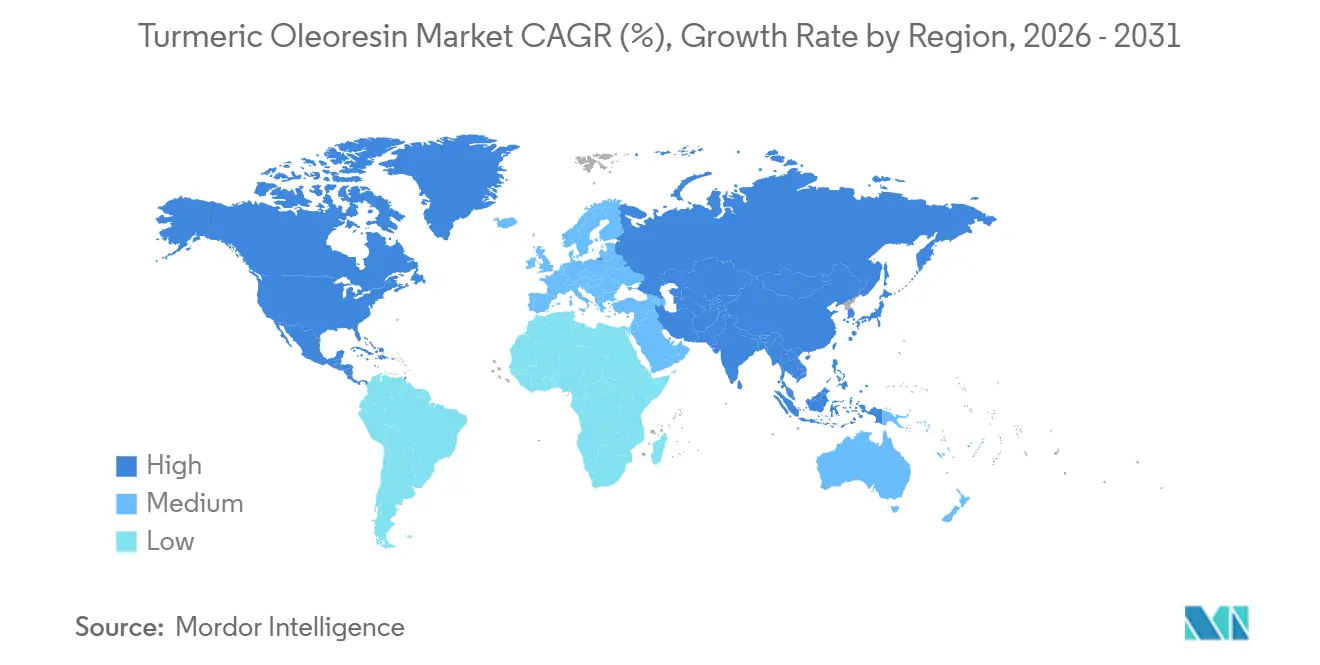

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Turmeric Oleoresin Market Analysis by Mordor Intelligence

The turmeric oleoresin market size is expected to grow from USD 82.45 million in 2025 to USD 86.64 million in 2026 and is forecast to reach USD 112.92 million by 2031 at 5.44% CAGR over 2026-2031. The growth of the turmeric oleoresin market reflects a structural shift in food manufacturing, as regulatory action pushes large buyers to replace petroleum-based colors with plant-derived alternatives in mainstream applications. Curcumin, or E100, is recognized under U.S., European, and Indian food frameworks, strengthening turmeric oleoresin’s position among manufacturers seeking a single ingredient that can support both color and flavor in reformulated products. India’s spice oil and oleoresin export volumes increased from 16,997 tonnes in the prior year to 20,940 tonnes in 2024-25, indicating that global procurement channels had already scaled purchases before the next round of food color reformulations moved into full implementation. The turmeric oleoresin market is also benefiting from broader nutraceutical use, as newer water-dispersible and bioavailability-enhanced curcumin formats help the ingredient expand beyond basic coloring demand into higher-value health applications.

Key Report Takeaways

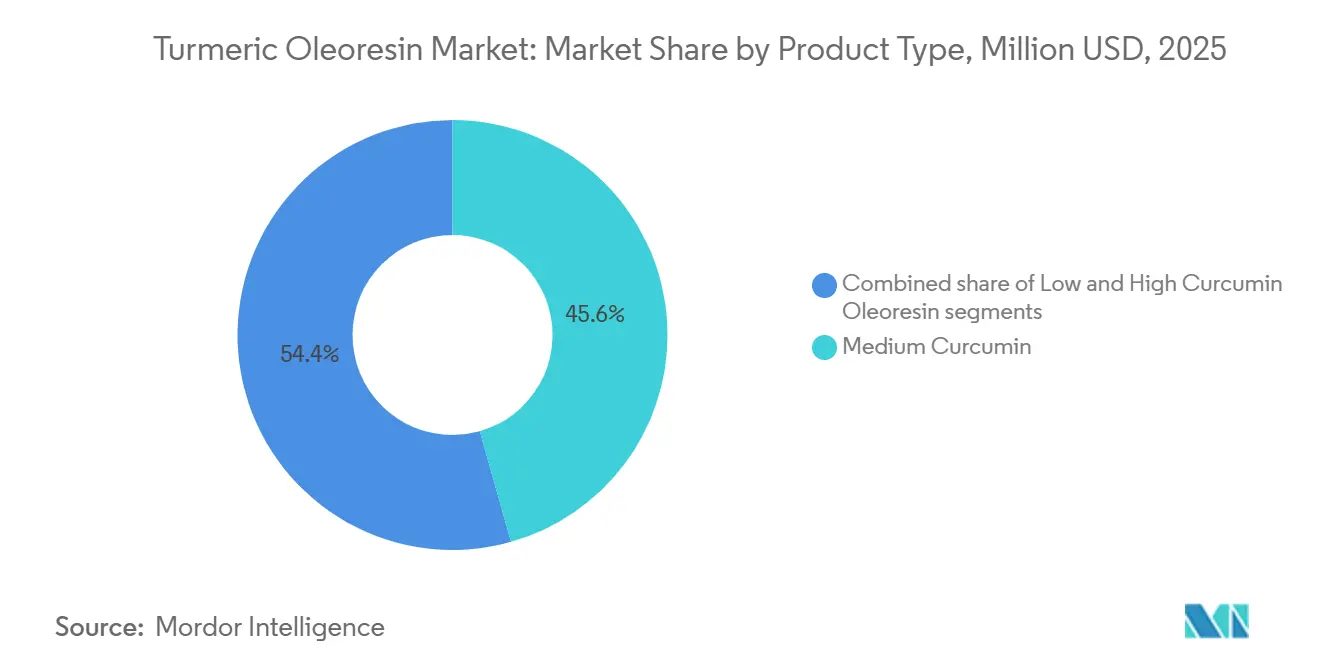

- By product type, medium-curcumin oleoresin led with 45.61% revenue share in 2025, while high-curcumin oleoresin is forecast to expand at a 6.17% CAGR through 2031.

- By extraction method, solvent extraction held 65.49% share in 2025, while supercritical CO2 extraction recorded the highest projected CAGR at 6.51% through 2031.

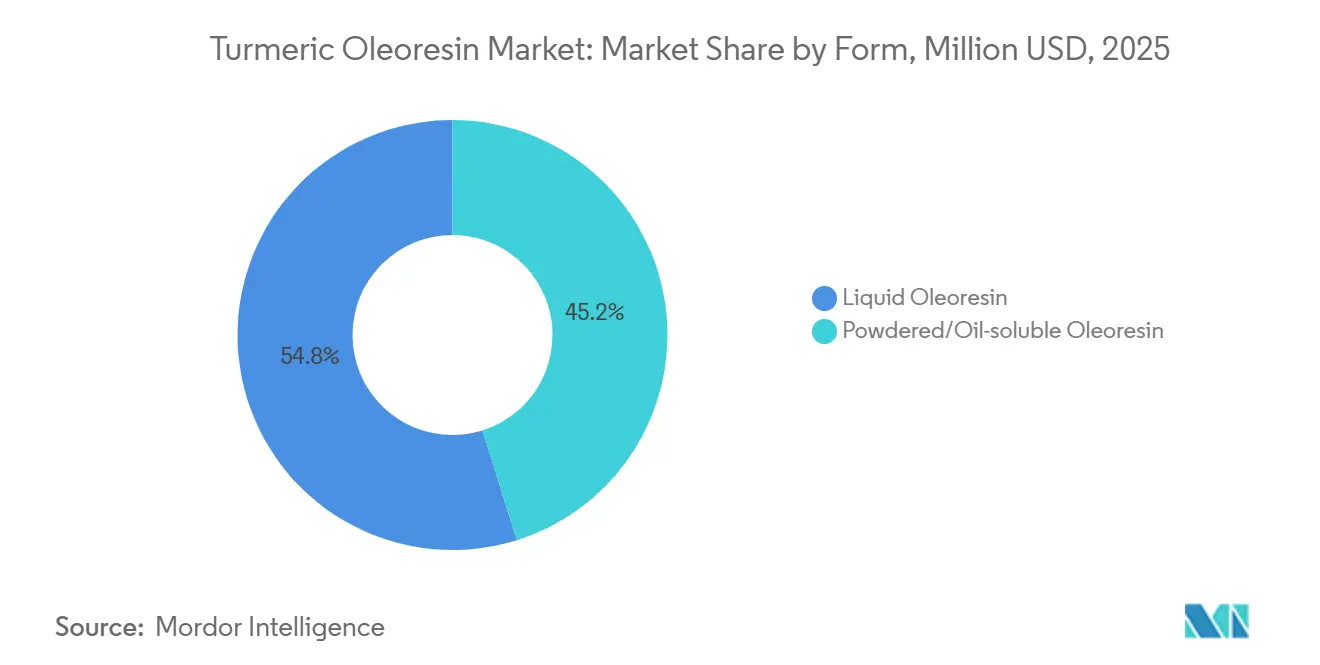

- By form, liquid oleoresin accounted for 54.84% share in 2025, while powdered oleoresin is advancing at a 7.15% CAGR through 2031.

- By application, food and beverages captured 41.08% share in 2025, while nutraceuticals are projected to grow at a 7.39% CAGR through 2031.

- By geography, Asia-Pacific held 40.94% share in 2025, while North America is forecast to grow at a 7.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Turmeric Oleoresin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |

|---|---|---|---|---|

| Rising demand for natural food colorants and flavoring ingredients | +1.5% | Global, with early adoption in North America and Europe | Short term (≤ 2 years) | |

| Growing use of turmeric oleoresin in functional foods and beverages | +1.0% | Global, with strong momentum in Asia-Pacific | Medium term (2-4 years) | |

| Expanding application in pharmaceutical and nutraceutical formulations | +0.9% | North America and Europe, with spillover to Asia-Pacific | Long term (≥ 4 years) | |

| Increasing consumer preference for clean-label food products | +0.8% | North America and Europe, with growing relevance in Asia-Pacific | Medium term (2-4 years) | |

| Growing adoption in cosmetics and personal care products | +0.4% | Global, concentrated in Asia-Pacific and Europe | Medium term (2-4 years) | |

| Advancements in high-purity and water-dispersible turmeric oleoresin formulations | +0.5% | Global, concentrated in advanced manufacturing regions | Long term (≥ 4 years) | |

| Source: Mordor Intelligence | ||||

Rising demand for natural food colorants and flavoring ingredients

The FDA’s April 2025 directive phased out all petroleum-based synthetic dyes from the U.S. food supply and targeted FD&C Red No. 40, Yellow No. 5, Yellow No. 6, Green No. 3, Blue No. 1, and Blue No. 2 by the end of 2026, making it the most material regulatory event for the turmeric oleoresin market during the forecast period[1]Food and Drug Administration, "HHS, FDA to Phase Out Petroleum-Based Synthetic Dyes in Nation’s Food Supply", fda.gov. Curcumin E100 held dual approval as both a colorant and a flavoring agent under FDA and EFSA frameworks, which gave it a functional advantage over single-purpose natural alternatives, such as annatto or paprika, as food manufacturers consolidated ingredient lists during reformulation. In February 2026, the FDA updated its “no artificial colors” voluntary labeling framework, allowing manufacturers to display the claim as long as their products did not contain petroleum-based dyes. This change directly created brand-level incentives to reformulate and communicate reformulation. Importantly, the FDA simultaneously fast-tracked new natural color approvals, including butterfly pea flower, gardenia blue, and Galdieria extract, which meant turmeric oleoresin competed within an expanding natural colorant palette rather than benefited from a captive market.

Growing use of turmeric oleoresin in functional foods and beverages

Functional foods and beverages create a convergence point where turmeric oleoresin delivers natural color, flavor modification, and bioactive properties, a value proposition that commodity synthetic colorants cannot replicate. India’s food sector is increasing the use of turmeric-based actives in fortified dairy products, health beverages, and bakery products, reflecting a value-added shift from commodity spice powder to standardized oleoresin. Major oleoresin producers are expected to increase curcumin output, specifically targeting nutraceutical and functional food buyers that require tighter curcuminoid specifications than food-grade products can reliably deliver. A second-order dynamic is emerging as functional food manufacturers shift from unprocessed turmeric powder to standardized oleoresin: the average selling price across the overall market rises because oleoresin commands a premium over raw turmeric due to its consistent color index, defined curcuminoid content, and residual solvent compliance.

Expanding application in pharmaceutical and nutraceutical formulations

Growing consumer focus on preventive healthcare and natural wellness products has significantly increased the adoption of turmeric oleoresin across pharmaceutical and nutraceutical applications. Owing to its high concentration of curcuminoids, the ingredient is widely used in dietary supplements, herbal medicines, capsules, tablets, and functional health formulations that support immunity, joint health, digestive health, and overall wellness. Pharmaceutical companies are also incorporating turmeric oleoresin into formulations targeting inflammation and other chronic health conditions due to its well-established bioactive properties. Rising demand for plant-based and clean-label ingredients further strengthens its appeal among manufacturers. In addition, continuous advancements in extraction techniques and bioavailability enhancement are improving product efficacy, encouraging wider commercialization and supporting sustained market expansion.

Increasing consumer preference for clean-label food products

Rising consumer awareness regarding ingredient transparency and natural food products is encouraging food manufacturers to replace synthetic additives with plant-based alternatives such as turmeric oleoresin. Its ability to provide natural color, flavor, and antioxidant benefits aligns well with the growing demand for clean-label formulations across processed foods, beverages, dairy products, and snacks. Consumers increasingly prefer products with recognizable, minimally processed ingredients, prompting brands to reformulate their offerings using natural extracts. According to research by the CBI Ministry of Foreign Affairs, clean-label products are projected to account for more than 70% of product portfolios in 2025 and 2026, up from 52% in 2021[2]Source: CBI MInistry of Foreigh Affairs, “Which trends offer opportunities”, cbi.eu. This strong shift toward clean-label product development is accelerating the incorporation of turmeric oleoresin into food formulations and supporting sustained market growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in turmeric raw material prices due to seasonal supply | -1.2% | India-centric, with global spillover | Short term (≤ 2 years) |

| Fluctuations in curcumin content affecting product standardization | -0.8% | Global, particularly India and Southeast Asia | Medium term (2-4 years) |

| High production and solvent extraction costs | -0.6% | Global, highest in advanced extraction markets | Long term (≥ 4 years) |

| Competition from alternative natural colorants and lower-cost synthetic colors | -0.5% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in turmeric raw material prices due to seasonal supply

Fluctuations in turmeric raw material prices present a significant challenge for manufacturers of turmeric oleoresin, as the industry relies heavily on a stable supply of high-quality turmeric rhizomes. Production is influenced by seasonal harvest cycles, changing weather conditions, pest infestations, and variations in crop yields, all of which can lead to supply shortages and price volatility. These unpredictable cost fluctuations increase production expenses and make long-term procurement planning more difficult for processors. Small and medium-sized manufacturers are particularly affected, as they often have limited capacity to absorb rising raw material costs. Consequently, inconsistent input prices can reduce profit margins, disrupt supply chains, and create pricing uncertainties across the turmeric oleoresin market.

Fluctuations in curcumin content affecting product standardization

Variations in the curcumin content of turmeric caused by differences in cultivar, geographical origin, soil conditions, climate, and harvesting practices create challenges in maintaining consistent oleoresin quality. Manufacturers must ensure standardized curcumin concentrations to meet food, pharmaceutical, and nutraceutical industry specifications, often requiring additional testing and processing steps. These quality inconsistencies increase production complexity, processing costs, and batch-to-batch variability. Meeting stringent regulatory and customer requirements for standardized formulations also becomes more difficult when raw material quality fluctuates. As a result, inconsistent curcumin levels can affect product reliability, limit manufacturing efficiency, and hinder broader adoption of turmeric oleoresin in high-value applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Premium Curcumin Concentration Drives Upgrade Cycle

Medium-curcumin turmeric oleoresin accounted for the largest revenue share of 45.61% in 2025, reflecting its broad acceptance across multiple end-use industries. The segment benefits from its balanced concentration of curcuminoids, making it suitable for food, beverage, nutraceutical, and cosmetic applications where both functionality and cost efficiency are important. Manufacturers favor medium-curcumin oleoresin because it offers consistent color, flavor, and bioactive performance without the higher production costs associated with premium-grade extracts. Its versatility allows it to be incorporated into a wide range of formulations, including seasonings, processed foods, dietary supplements, and personal care products.

High-curcumin turmeric oleoresin is projected to register the fastest CAGR of 6.17% through 2031, driven by rising demand for high-potency botanical ingredients in health-focused applications. Increasing consumer awareness of curcumin's antioxidant and anti-inflammatory properties has accelerated the adoption of high-curcumin extracts in nutraceuticals, pharmaceuticals, and functional foods. The segment is also benefiting from expanding clinical research supporting curcumin-based formulations for preventive healthcare and wellness products.

By Extraction Method: Technology Bifurcation Reshapes Supplier Positioning

Solvent extraction dominated the turmeric oleoresin market in 2025, accounting for 65.49% of the total revenue share, owing to its high extraction efficiency, commercial scalability, and cost-effectiveness. The method has been widely adopted by manufacturers because it enables the recovery of high yields of curcuminoids, essential oils, and other valuable bioactive compounds from turmeric rhizomes. Its well-established industrial processes and compatibility with large-scale production make it the preferred extraction technique for supplying the food, beverage, pharmaceutical, and nutraceutical industries.

Supercritical CO₂ extraction is projected to record the fastest CAGR of 6.51% through 2031, driven by increasing demand for premium-quality botanical extracts and environmentally sustainable processing technologies. Unlike conventional solvent-based methods, supercritical CO₂ extraction produces solvent-free oleoresins while preserving heat-sensitive bioactive compounds and volatile constituents. As regulatory standards and quality expectations continue to rise, supercritical CO₂ extraction is expected to play an increasingly important role in the future growth of the turmeric oleoresin market.

By Form: Powder Formats Drive Next-Phase Value Capture

Liquid turmeric oleoresin accounted for the largest market share of 54.84% in 2025, supported by its widespread use across food processing, beverage manufacturing, pharmaceuticals, and industrial ingredient applications. The liquid form offers excellent solubility in oil-based systems, enabling uniform distribution of color, flavor, and bioactive compounds in a variety of formulations. Its ease of handling during industrial-scale production and compatibility with automated processing equipment make it the preferred choice for large manufacturers. Liquid oleoresin also provides greater formulation flexibility, allowing producers to achieve precise dosage and consistent product quality.

Powdered turmeric oleoresin is projected to register the fastest CAGR of 7.15% through 2031, driven by increasing demand for convenient, shelf-stable, and easy-to-handle ingredient formats. Powdered oleoresin is gaining popularity in dry food mixes, dietary supplements, bakery products, instant beverages, and nutraceutical formulations due to its ease of storage, transportation, and incorporation into powdered blends. The segment also benefits from improved stability, reduced risk of leakage during distribution, and enhanced compatibility with encapsulated and dry-processing applications. As demand for convenient and value-added natural ingredients continues to rise, the powdered form is expected to witness robust growth throughout the forecast period.

By Application: Nutraceuticals Reshape the Demand Profile Beyond Food

Food and beverages represented the largest application segment, accounting for 41.08% of the turmeric oleoresin market in 2025. The segment's leadership is driven by the widespread use of turmeric oleoresin as a natural colorant, flavoring agent, and functional ingredient across processed foods, sauces, seasonings, dairy products, beverages, and ready-to-eat meals. Increasing consumer preference for clean-label products and natural food additives has encouraged manufacturers to replace synthetic ingredients with plant-derived alternatives such as turmeric oleoresin. Its excellent coloring properties, stability, and concentrated flavor profile make it highly suitable for large-scale food processing applications.

Nutraceuticals are projected to register the fastest CAGR of 7.39% through 2031, fueled by growing consumer interest in preventive healthcare and natural wellness solutions. Rising awareness of curcumin's antioxidant, anti-inflammatory, and immune-supporting properties has significantly increased the use of turmeric oleoresin in dietary supplements, functional nutrition products, and herbal formulations. The expanding aging population, coupled with increasing incidences of chronic lifestyle-related conditions, is driving demand for botanical ingredients with scientifically supported health benefits. As health-conscious consumers increasingly seek plant-based functional ingredients, the nutraceutical segment is expected to remain the fastest-growing application area in the turmeric oleoresin market through the forecast period.

Geography Analysis

Asia-Pacific dominated the turmeric oleoresin market in 2025, accounting for 40.94% of the global market share, supported by abundant turmeric cultivation, well-established extraction industries, and strong domestic consumption. India remains the leading producer and exporter of turmeric oleoresin, benefiting from favorable agro-climatic conditions, extensive processing infrastructure, and a mature spice industry. Rising demand from the food, pharmaceutical, nutraceutical, and cosmetic sectors across countries such as China, Japan, and Southeast Asia continues to strengthen regional consumption. Increasing investments in value-added spice extracts, expanding export capabilities, and supportive government initiatives promoting spice processing further reinforce Asia-Pacific's leadership in the global turmeric oleoresin market.

North America is projected to register the fastest CAGR of 7.27% through 2031, driven by increasing consumer preference for natural ingredients and clean-label products. Growing awareness of curcumin's antioxidant and anti-inflammatory properties has accelerated the incorporation of turmeric oleoresin into dietary supplements, functional foods, beverages, and personal care formulations. The region's advanced food processing industry, robust nutraceutical sector, and continuous product innovation are creating sustained demand for high-quality botanical extracts. Additionally, increasing adoption of plant-based ingredients by food manufacturers and rising investments in natural health products continue to support strong market expansion across the United States and Canada.

Europe, South America, and the Middle East and Africa present emerging growth opportunities for the turmeric oleoresin market, supported by expanding applications across industries. Europe is seeing increased demand for natural food colorants, organic ingredients, and botanical extracts in food and cosmetics. However, entering the market requires strict compliance with EU food safety regulations, such as Maximum Residue Levels and Good Manufacturing Practices[3]CBI, "Entering the European market for curcuma longa (turmeric)", www.cbi.eu. South America is increasing consumption through growth in processed food manufacturing and herbal wellness products. Meanwhile, the Middle East and Africa is experiencing steady market development as demand rises for natural flavoring agents, traditional herbal products, and functional ingredients, supported by improved food processing capabilities and growing consumer awareness of plant-based health solutions.

Competitive Landscape

The turmeric oleoresin market shows moderate concentration. The companies in the market compete on extraction technology, product purity, curcumin concentration, regulatory compliance, and long-term customer relationships rather than pricing alone. Leading producers use strong technical expertise and vertically integrated sourcing networks to maintain consistent quality and meet the stringent requirements of food, nutraceutical, pharmaceutical, and cosmetic manufacturers. High entry barriers related to advanced extraction processes, quality certifications, and global distribution capabilities strengthen the position of established participants.

Synthite Industries Pvt. Ltd. remains one of the most influential participants in the turmeric oleoresin market, supported by extensive spice extraction capabilities and large-scale manufacturing infrastructure. The company, recognized as the world’s largest spice extract producer, is projected to report a group turnover of approximately INR 1,700 crore (around USD 204 million) in 2026, reflecting its strong global commercial presence. Its broad turmeric extract portfolio, investments in advanced extraction technologies, and long-standing partnerships with multinational food and ingredient companies reinforce its competitive advantage.

Arjuna Natural Pvt. Ltd. differentiates itself through innovation and intellectual property, particularly with its flagship BCM-95® turmeric extract, which is protected by 42 global patents and backed by extensive scientific and clinical research. This evidence base helps the company secure premium positioning in the nutraceutical and pharmaceutical sectors, where efficacy and regulatory documentation remain critical purchasing factors. Other companies, including Kancor Ingredients Limited, Akay Natural Ingredients Pvt. Ltd., Universal Oleoresins, and Plant Lipids Private Limited, intensify competition through investments in sustainable sourcing, customized formulations, and application-specific ingredient development. As global demand for natural botanical extracts expands, companies increasingly compete on innovation, traceability, standardized active compounds, and consistent product quality.

Turmeric Oleoresin Industry Leaders

-

Northern Solvents Private Limited

-

MANE Group

-

Universal Oleoresins

-

Synthite Industries Pvt. Ltd.

-

Arjuna Natural Pvt. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: India's National Commodity & Derivatives Exchange Limited (NCDEX) imposed a 2.5% event-based Additional Surveillance Margin on turmeric futures contracts, reflecting structural supply tightness caused by weather-affected crop cycles. These conditions reduced new production to an estimated 7.4–7.5 million bags, compared with a combined annual demand of approximately 14 million bags. The margin requirement directly increases the cost of carry for oleoresin extractors that use futures to hedge input costs.

- March 2025: Synthite Industries announced a strategic expansion in Kerala focused on bio-manufacturing and non-solvent extraction technologies. The company identified advanced processing, rather than large-scale commodity manufacturing, as its next phase of competitive growth. This shift indicates a deliberate move toward pharmaceutical and premium cosmetic grades, where extraction technology, rather than volume throughput, drives margins.

- February 2025: Oterra A/S inaugurated a new natural color blending and application center in Kochi, Kerala, at its Akay Natural Ingredients subsidiary. The facility enables the direct supply of turmeric-based yellow and orange color blends to customers in India, Asia-Pacific, and the Middle East. It replaces the earlier European processing-and-reimport model, significantly reducing lead times and operational costs for regional customers.

Global Turmeric Oleoresin Market Report Scope

Turmeric oleoresin is a concentrated natural extract obtained from the rhizomes of the turmeric plant (Curcuma longa) using solvent extraction. The turmeric oleoresin market is segmented by product type, extraction method, form, application and geography. Based on product type, the market is segmented into high-curcumin oleoresin (≥40% CV), medium-curcumin oleoresin (25–40% CV) and low-curcumin oleoresin (<25% CV). Based on extraction method, the market is segmented into solvent extraction, supercritical CO₂ extractiona and pressurized liquid extraction. Based on form, the market is segmented into liquid oleoresin and powdered/oil soluble oleoresin. Based on application, the market is segmented into food and beverages, pharmaceuticals, nutraceuticals, cosmetics and personal care, animal feed and other uses. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. For each segment, the market sizing and forecasting have been done in value terms (USD million).

| High-Curcumin Oleoresin (≥40% CV) |

| Medium-Curcumin Oleoresin (25–40% CV) |

| Low-Curcumin Oleoresin (less than 25% CV) |

| Solvent Extraction |

| Supercritical CO₂ Extraction |

| Pressurized Liquid Extraction |

| Liquid Oleoresin |

| Powdered/Oil Soluble Oleoresin |

| Food and Beverages |

| Pharmaceuticals |

| Nutraceuticals |

| Cosmetics and Personal Care |

| Animal Feed and Other Uses |

| North America |

| Europe |

| Asia-Pacific |

| South America |

| Middle East and Africa |

| By Product Type | High-Curcumin Oleoresin (≥40% CV) |

| Medium-Curcumin Oleoresin (25–40% CV) | |

| Low-Curcumin Oleoresin (less than 25% CV) | |

| By Extraction Method | Solvent Extraction |

| Supercritical CO₂ Extraction | |

| Pressurized Liquid Extraction | |

| By Form | Liquid Oleoresin |

| Powdered/Oil Soluble Oleoresin | |

| By Application | Food and Beverages |

| Pharmaceuticals | |

| Nutraceuticals | |

| Cosmetics and Personal Care | |

| Animal Feed and Other Uses | |

| By Geography | North America |

| Europe | |

| Asia-Pacific | |

| South America | |

| Middle East and Africa |

Key Questions Answered in the Report

What is the current size of the turmeric oleoresin business and where is it headed by 2031?

The turmeric oleoresin market stood at USD 82.45 million in 2025, reached USD 86.64 million in 2026, and is projected to reach USD 112.92 million by 2031 at a 5.44% CAGR.

Why is demand rising so quickly in food and beverage applications?

The largest reason is regulatory reformulation, especially the U.S. phase-out of petroleum-based synthetic dyes, which is pushing packaged food brands toward plant-derived color systems.

Which application area is growing the fastest?

Nutraceuticals is the fastest-growing application, with a projected 7.39% CAGR through 2031, supported by continued interest in clinically supported curcumin formulations.

Which region leads global demand today?

Asia-Pacific leads with 40.94% share in 2025, supported by India’s raw material base, extraction capacity, and strong position in pharma-grade curcumin supply.

Page last updated on: