Oleoresin Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

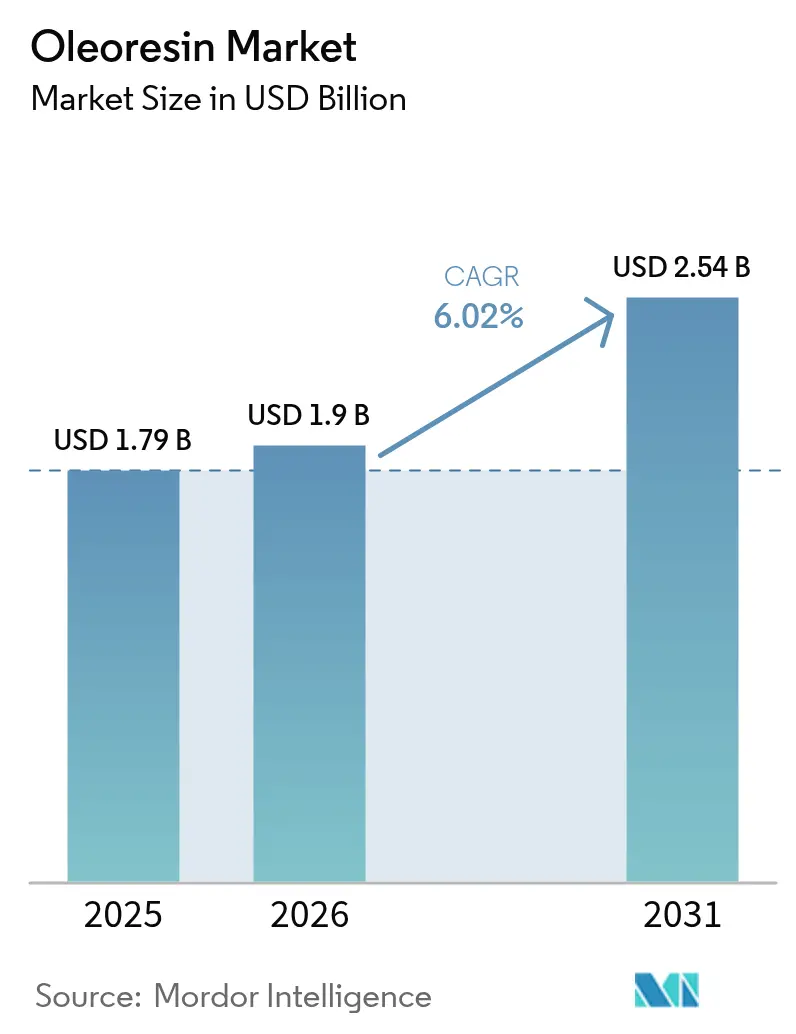

| Market Size (2026) | USD 1.9 Billion |

| Market Size (2031) | USD 2.54 Billion |

| Growth Rate (2026 - 2031) | 6.02% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Oleoresin Market Analysis by Mordor Intelligence

The oleoresin market size is expected to grow from USD 1.79 billion in 2025 to USD 1.9 billion in 2026 and is forecast to reach USD 2.54 billion by 2031 at 6.02% CAGR over 2026-2031. The market expansion is driven by increasing global demand for natural and clean-label ingredients across industries. Oleoresins are preferred over synthetic additives due to their stability, longer shelf life, concentrated flavor, and health benefits, including antioxidant, antimicrobial, and anti-inflammatory properties. Growing consumer health consciousness has increased the use of turmeric, black pepper, ginger, and capsicum oleoresins in nutraceuticals and functional foods. The market growth is further supported by improved extraction methods, such as supercritical CO₂ and solvent-free extraction, which enhance product quality and efficiency. Additionally, favorable regulations for natural ingredients and increased Research and Development investments are expanding oleoresin applications.

Key Report Takeaways

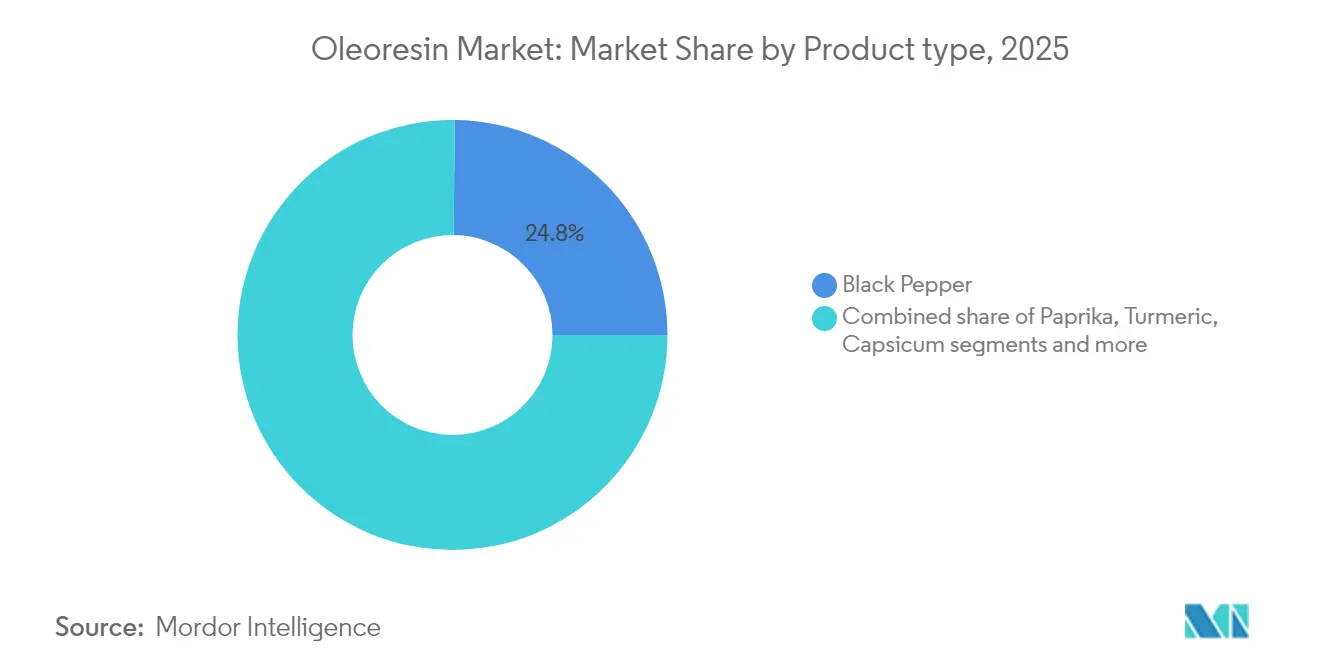

- By product type, black pepper led with 24.83% of oleoresin market share in 2025, while turmeric is forecast to climb at an 8.02% CAGR to 2031.

- By form, oil-soluble liquid variants accounted for 50.76% of the oleoresin market size in 2025; water-soluble liquids are the fastest rising at a 7.12% CAGR through 2031.

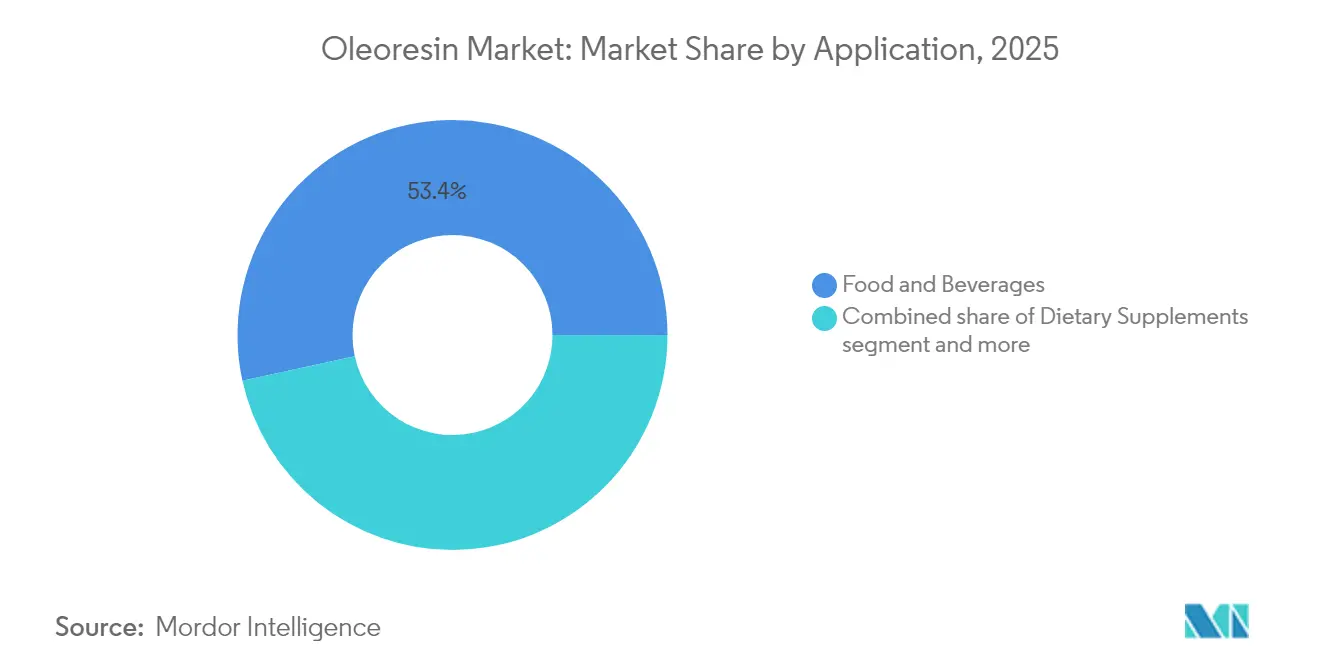

- By application, food and beverages dominated with 53.42% revenue contribution in 2025; dietary supplements are advancing at a 6.98% CAGR to the end of the decade.

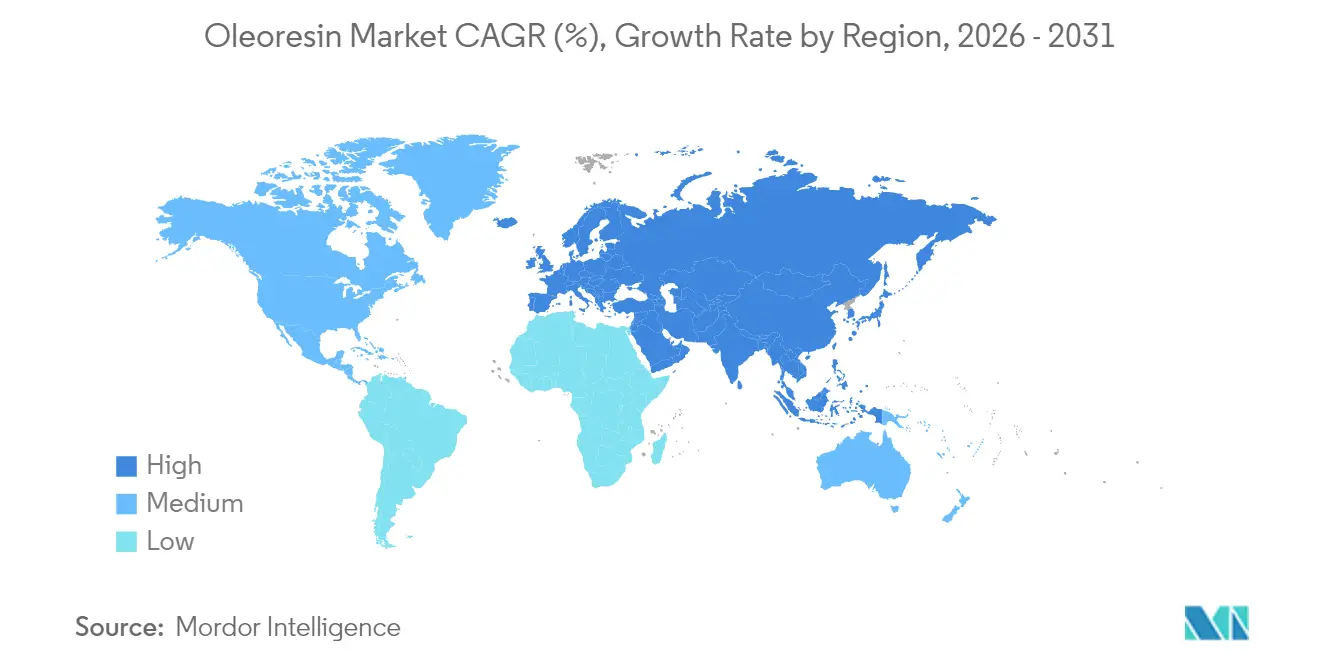

- By geography, Europe held 28.75% of 2025 revenue, but Asia-Pacific is projected to register a 6.78% CAGR, the quickest regional pace.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Oleoresin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory push for natural colors and flavors in processed foods | +1.8% | Global, with strongest impact in North America and European Union | Medium term (2-4 years) |

| Rising clean-label demand in food, beverages, and nutraceuticals | +1.5% | Global, led by North America and the Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Growing global demand for ethnic and spicy flavors | +1.2% | Global, with highest growth in North America and Europe | Medium term (2-4 years) |

| Extended shelf life and logistical advantages of oleoresins | +0.9% | Global, particularly beneficial for export-oriented markets | Long term (≥ 4 years) |

| Expanding use in personal care and cosmetic products | +0.7% | Global, with premium markets in North America and Europe | Long term (≥ 4 years) |

| Rising adoption in the nutraceutical industry for dietary supplements | +1.1% | Global, with fastest growth in Asia-Pacific and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Push for Natural Colors and Flavors in Processed Foods

Regulatory developments have significantly influenced oleoresin market dynamics, following the Food and Drug Administration's authorization of three natural color additives in 2025. The approved substances comprise butterfly pea flower extract, galdieria extract blue, and calcium phosphate for food applications. This regulatory modification demonstrates a systematic transition from petroleum-derived synthetic dyes, generating substantial opportunities for oleoresin manufacturers specializing in natural alternatives. The European Union's enforcement of Regulation 1334/2008 reinforces these requirements by mandating all food flavorings to be registered in the European Union flavoring database, thereby necessitating natural ingredient procurement. Furthermore, the European Food Safety Authority's scientific assessments of rosemary extracts and paprika oleoresins have established comprehensive protocols for natural ingredient utilization across multiple product categories, facilitating consistent market expansion.

Rising Clean-Label Demand in Food, Beverages, and Nutraceuticals

Consumer preferences for clean-label products are changing ingredient selection criteria, with oleoresins emerging as solutions that provide both functionality and label transparency. The clean-label movement includes sustainability credentials and processing methods, creating opportunities for oleoresin suppliers offering ethical sourcing and environmentally friendly extraction technologies. According to the International Food Information Council (IFIC), in 2023, approximately 29% of respondents in the United States regularly purchased food and beverages labeled as containing clean ingredients, which has directly influenced the demand for natural oleoresins in food applications [1]Source: International Food Information Council (IFIC), "2023 Food and Health Survey", foodinsight.org. The European market shows the highest clean-label adoption rate, with organic certification becoming a basic requirement for market entry. Beverage manufacturers are adapting to clean-label demands, incorporating water-soluble oleoresin formulations that provide natural coloring and flavoring while maintaining product clarity and stability. This trend enables premium pricing, as consumers are willing to pay more for products with clean-label credentials, creating potential for increased margins for oleoresin suppliers who meet these requirements.

Growing Global Demand for Ethnic and Spicy Flavors

The increasing globalization of culinary preferences generates substantial demand for ethnic flavor profiles, with oleoresins functioning as the primary delivery mechanism for authentic taste experiences in processed foods. Thai-Cajun and Middle Eastern-Mexican fusion seasonings demonstrate significant market presence, particularly among Millennial and Generation Z consumers who actively pursue diverse flavor combinations. This demographic transformation corresponds with the expansion of plant-based products, where manufacturers utilize specific spice profiles to enhance the flavor characteristics of meat alternatives, establishing new applications for oleoresins that provide consistent heat levels and complex flavor attributes. The applications extend beyond food manufacturing, as cosmetic producers incorporate spice-derived oleoresins for their antioxidant properties and sensory characteristics in natural skincare formulations.

Extended Shelf Life and Logistical Advantages of Oleoresins

Oleoresins offer significant stability advantages over traditional spices, making them valuable as supply chains face disruptions and manufacturers focus on inventory optimization. They provide extended shelf life compared to ground spices, require minimal storage space, and eliminate contamination risks associated with whole spice handling. These benefits result in reduced total ownership costs for food manufacturers. The logistical advantages of oleoresins become strategically important during supply chain volatility, as spice commodity markets experience price fluctuations and availability issues due to climate changes and geopolitical factors. Oleoresins enable manufacturers to maintain consistent product quality despite seasonal variations in raw material quality, meeting growing consumer demands for consistency across global markets. Their transportation efficiency is particularly beneficial for international trade, as oleoresins require less freight volume than equivalent spice quantities, reducing both logistics costs and carbon footprint.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs due to raw material price volatility and complex extraction processes | -1.4% | Global, with highest impact in cost-sensitive markets | Short term (≤ 2 years) |

| Limited availability of raw materials due to seasonal variations and climate conditions | -1.1% | Global, with particular impact on tropical spice origins | Medium term (2-4 years) |

| Competition from synthetic alternatives and flavor substitutes | -0.8% | Global, with strongest impact in price-sensitive applications | Long term (≥ 4 years) |

| Storage and handling challenges due to the sensitive nature of oleoresins | -0.5% | Global, with higher impact in regions with inadequate cold chain infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Production Costs Due to Raw Material Price Volatility and Complex Extraction Processes

Raw material price volatility poses a significant constraint on oleoresin market growth, as spice commodity prices fluctuate due to climate disruptions and geopolitical tensions. Black pepper prices have increased substantially due to strong domestic and export demand, creating cost pressures for oleoresin manufacturers. According to the Office of the Economic Adviser, the Wholesale Price Index of black pepper across India during the financial year 2024 reached 185.4, showing an increase from the previous year [2]Source: Office of the Economic Adviser, "Wholesale Price Index of black pepper across India", eaindustry.nic.in. Production costs across the supply chain have increased, with Indian spice markets experiencing higher expenses for fertilizer and labor. Extraction technology costs present additional challenges, as supercritical CO2 systems require significant capital investment and specialized expertise, despite offering better yield and quality compared to traditional solvent extraction methods.

Limited Availability of Raw Materials Due to Seasonal Variations and Climate Conditions

Climate-related disruptions are affecting raw material availability in the oleoresin market, as traditional spice-growing regions face increased weather volatility that impacts crop yields and quality. The seasonal nature of spice cultivation creates supply constraints, as most raw materials are harvested during specific periods, making manufacturers susceptible to weather-related crop failures. Climate change effects are evident in traditional growing regions, where changing rainfall patterns and temperature extremes affect crop quality and harvest timing. This has prompted oleoresin manufacturers to expand their sourcing locations and develop resilient supply chains. The geographic concentration of spice production increases market vulnerability, as disruptions in key growing areas affect global oleoresin availability, emphasizing the importance of supply chain diversification to manage risks while maintaining operational efficiency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Turmeric Drives Innovation Despite Black Pepper's Market Leadership

Black pepper oleoresin holds 24.83% market share in 2025, maintaining its dominant position through its applications in food, pharmaceutical, and cosmetic industries. Turmeric oleoresin exhibits the highest growth rate at 8.02% CAGR through 2031, driven by its expanding use in nutraceuticals and increased regulatory approvals for curcumin-based products. The growth difference between these segments reflects consumer preferences, as turmeric gains prominence due to its anti-inflammatory and antioxidant properties, particularly in dietary supplements and functional foods. Paprika oleoresin maintains a strong market presence by functioning as both a colorant and flavoring agent, especially in processed meat products, where it provides natural coloring while meeting clean-label standards.

Capsicum oleoresin fills specific applications requiring standardized heat levels, with demand increasing due to the rising popularity of spicy foods and the need for consistent pungency in commercial food production. Supercritical CO2 extraction technology improves product quality across segments by delivering higher purity levels and better preservation of bioactive compounds compared to conventional solvent methods. Ginger oleoresin sees increased use in beverages and confectionery, while garlic and onion oleoresins serve specific markets requiring sulfur compound preservation for authentic flavors. The segment dynamics align with industry trends toward functional ingredients, as demonstrated by turmeric's transformation from a traditional spice to a recognized health-promoting compound.

By Form: Water-Soluble Innovation Challenges Oil-Soluble Dominance

Oil-soluble liquid oleoresins hold 50.76% market share in 2025, due to their established use in fat-based food applications and traditional processing methods. Water-soluble liquid oleoresins are growing at 7.12% CAGR through 2031 as manufacturers adopt them for beverage and aqueous applications. The expansion of water-soluble variants stems from improvements in emulsification and encapsulation technologies, enabling stable dispersion in water-based systems while maintaining bioactivity and sensory properties. Powdered oleoresins serve specific applications requiring extended shelf life and ease of handling, particularly in dry seasoning blends and instant food products where moisture content must be controlled.

The evolution in oleoresin forms aligns with industry demands for application-specific solutions, as water-soluble variants enable product development in categories previously limited by traditional oil-soluble formats. Manufacturing processes differ across forms, with water-soluble variants requiring specialized emulsification equipment and stabilization technologies, creating entry barriers for smaller producers. Companies with strong research and development capabilities maintain competitive advantages, as successful water-soluble formulations require extensive knowledge of ingredient interactions and processing parameters.

By Application: Dietary Supplements Accelerate Beyond Traditional Food Uses

Food and beverages account for 53.42% of oleoresin applications in 2025, remaining the primary demand driver through their use in processed foods, condiments, and ready meals. Dietary supplements represent the fastest-growing application segment with a 6.98% CAGR through 2031, driven by increasing consumer focus on preventive healthcare and functional nutrition. The European Food Safety Authority (EFSA) evaluations have validated the safety of botanical extracts, supporting the expansion of oleoresins in nutraceutical formulations. In pharmaceutical applications, oleoresins provide standardized bioactive compound content, ensuring consistent dosing and therapeutic efficacy in medicinal products.

The cosmetics and personal care segment shows growth due to the edible beauty trend, which increases demand for food-grade ingredients in skincare products. Oleoresins serve both functional and natural product requirements in these formulations. While animal feed applications maintain steady demand, they face competition from synthetic alternatives in price-sensitive markets. New opportunities are emerging in biodegradable packaging and sustainable materials as circular economy adoption increases. This expansion demonstrates oleoresins' evolution from traditional flavoring ingredients to functional components that provide health, sustainability, and performance benefits across various end-use markets.

Geography Analysis

Europe holds a dominant 28.75% market share in 2025, driven by strict regulations favoring natural ingredients and robust supply chains connecting Germany, Spain, and the Netherlands with global oleoresin suppliers. The region's mature market emphasizes premium pricing for organic and sustainably sourced oleoresins as standard requirements. Supply chain traceability and environmental responsibility create opportunities for ethical suppliers, while the established food processing industry maintains consistent demand across applications

Asia-Pacific exhibits the highest growth rate at 6.78% CAGR through 2031, with India's position as the world's largest spice producer. The Ministry of Agriculture and Farmers Welfare reports India's spice production reached 11.8 million metric tons in fiscal year 2024, supporting the country's oleoresin manufacturing and export capabilities . China's significant paprika oleoresin imports influence market dynamics, with trade requirements emphasizing organic production and traceability standards.

North America demonstrates a mature market with strong regulatory frameworks supporting natural ingredients and clean-label demands. Food manufacturers' shift away from artificial ingredients creates opportunities for natural oleoresin alternatives. The region prioritizes supply chain resilience following pandemic disruptions, focusing on domestic sourcing and strategic inventory management. The advanced food processing industry, high consumer purchasing power, and expanding nutraceutical sector support premium oleoresin product growth.

Competitive Landscape

The oleoresin market demonstrates moderate fragmentation, characterized by a diverse competitive environment. The market structure encompasses established multinational corporations and specialized regional manufacturers, each utilizing distinct operational strengths to secure market position. Major market participants include Synthite Industries Ltd, Kalsec Inc., Mane SA, Plant Lipids Private Limited, and Oterra A/S, with their market presence supported by extensive research and development capabilities and comprehensive regulatory expertise.

The competitive dynamics are significantly influenced by technological advancement and regulatory compliance capabilities. Companies maintaining strong positions in the market have established their competitive advantage through patent-protected extraction technologies and adherence to stringent food safety regulations. This technological emphasis has created substantial barriers to entry, particularly for new market entrants lacking the necessary capital and technical expertise.

The market structure indicates an ongoing trend toward consolidation, primarily affecting smaller market participants who face challenges in maintaining technological competitiveness and regulatory compliance. However, the market presents strategic opportunities for organizations capable of vertical integration across the value chain, from raw material procurement to final product distribution. Companies that successfully implement advanced extraction methods, such as supercritical CO2 systems, demonstrate enhanced market positioning through superior product quality and environmental sustainability credentials.

Oleoresin Industry Leaders

-

Synthite Industries Ltd

-

Kalsec Inc.

-

Mane SA

-

Plant Lipids Private Limited

-

Oterra A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: OfBusiness has acquired Kerala-based Elixir Extracts Pvt Ltd for approximately USD 10 million. Elixir Extracts Pvt Ltd manufactures standardized natural extracts, essential oils, oleoresins, and flavors.

- August 2024: Kalsec Inc. opened its Mildenhall Finishing and Distribution Centre in the United Kingdom. The facility enhances service for European customers by offering increased flexibility, local customization options, and faster delivery times.

- February 2024: Ultra International formed a partnership with Ecospice Ingredients Pvt. Ltd. to expand the distribution of Indian spice oleoresins globally. The collaboration aims to increase the international market presence of Indian spice oleoresin extracts.

- May 2023: MANE KANCOR launched its largest manufacturing facility in Byadgi, Karnataka, India. The Byadgi facility processes a wide variety of spices and raw materials.

Global Oleoresin Market Report Scope

Oleoresins are naturally extracted from various plants and can induce color, holistic taste, aroma, and texture. The main ingredients of oleoresin are pigments, pungent constituents, essential oils, fixed oils, and natural antioxidants. The global oleoresin market is segmented into type, application, and geography. By product type, the market is segmented into paprika, black pepper, turmeric, capsicum, ginger, and other product types. By application, the market has been segmented into food and beverage, pharmaceuticals, cosmetics and personal care, and others. The food and beverage segment is further classified into bakery goods, spices and condiments, meat and seafood products, and others. By geography, the study provides key insights into the major regions, including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Paprika |

| Black Pepper |

| Turmeric |

| Capsicum |

| Ginger |

| Garlic |

| Onion |

| Others |

| Oil-Soluble Liquid Oleoresins |

| Water-Soluble Liquid Oleoresins |

| Powdered Oleoresins |

| Food and Beverages | Bakery Goods |

| Spices and Condiments | |

| Meat and Seafood Products | |

| Ready Meals and Snacks | |

| Other Food and Beverages | |

| Dietary Supplements | |

| Pharmaceuticals | |

| Cosmetics and Personal-Care | |

| Animal Feed and Pet Food |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Paprika | |

| Black Pepper | ||

| Turmeric | ||

| Capsicum | ||

| Ginger | ||

| Garlic | ||

| Onion | ||

| Others | ||

| By Form | Oil-Soluble Liquid Oleoresins | |

| Water-Soluble Liquid Oleoresins | ||

| Powdered Oleoresins | ||

| By Application | Food and Beverages | Bakery Goods |

| Spices and Condiments | ||

| Meat and Seafood Products | ||

| Ready Meals and Snacks | ||

| Other Food and Beverages | ||

| Dietary Supplements | ||

| Pharmaceuticals | ||

| Cosmetics and Personal-Care | ||

| Animal Feed and Pet Food | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the oleoresin market?

The oleoresin market stands at USD 1.9 billion in 2026 and is projected to reach USD 2.54 billion by 2031, growing at a 6.02% CAGR over 2026-2031.

Which product type holds the largest oleoresin market share?

Black pepper oleoresin leads with 24.83% revenue share in 2025.

Why are water-soluble oleoresins gaining popularity?

Advances in nano-emulsion and encapsulation allow water-soluble oleoresins to disperse cleanly in beverages, driving a 7.12% CAGR for this form.

Which region is expected to grow fastest?

Asia-Pacific is forecast to expand at a 6.78% CAGR through 2031, supported by India’s large spice base and expanding extraction capacity.

Page last updated on: