Margarine Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 24.08 Billion |

| Market Size (2031) | USD 26.7 Billion |

| Growth Rate (2026 - 2031) | 2.10% CAGR |

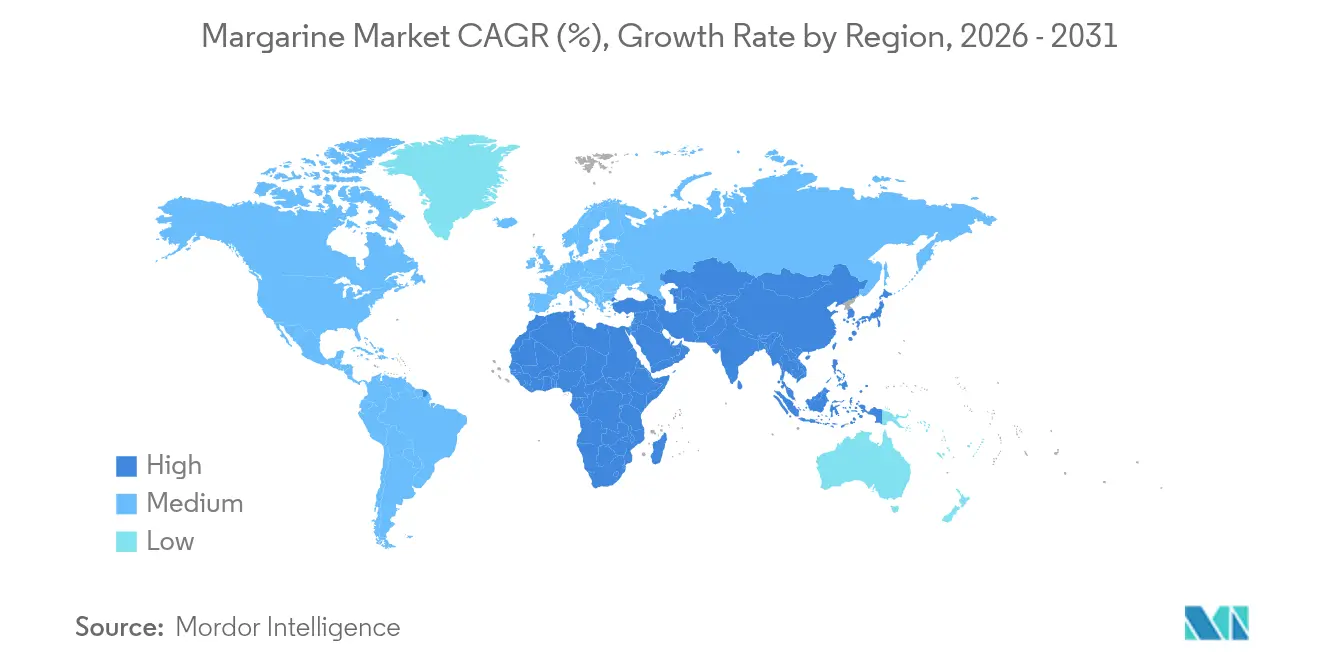

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

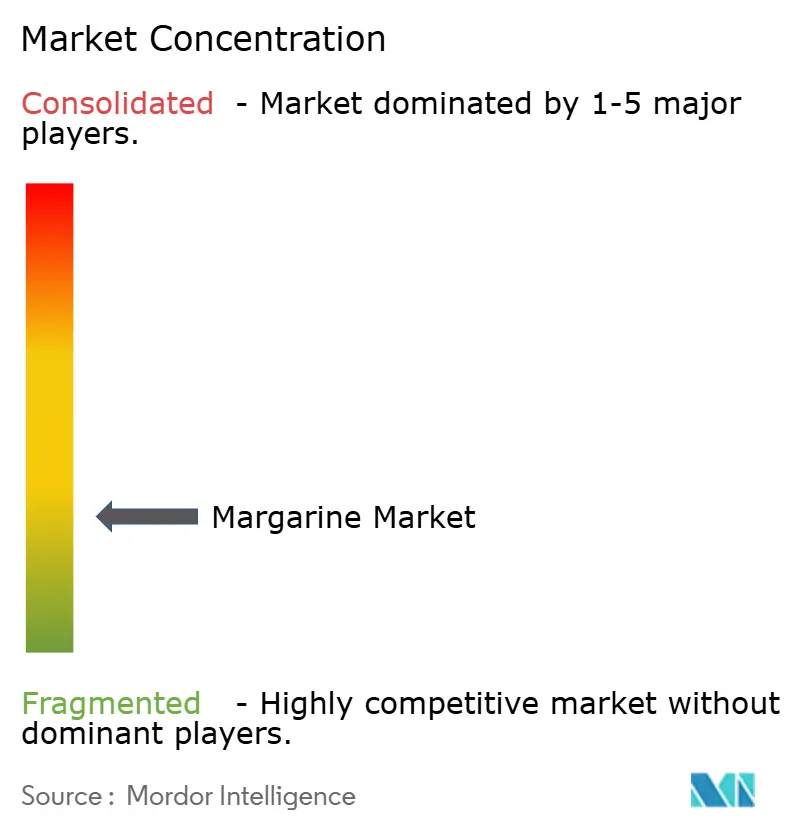

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Margarine Market Analysis by Mordor Intelligence

Margarine market size in 2026 is estimated at USD 24.08 billion, growing from 2025 value of USD 23.58 billion with 2031 projections showing USD 26.7 billion, growing at 2.10% CAGR over 2026-2031. The market growth reflects the industry's adaptation to trans-fat elimination regulations while benefiting from plant-based innovations, fortified products, and increased industrial demand. Regulations from the Food and Drug Administration (FDA) and World Health Organization (WHO) have driven the adoption of zero-trans processing technologies, requiring higher capital investments but enhancing consumer confidence. The shift to zero-trans processing has necessitated significant equipment upgrades and process modifications across manufacturing facilities. Enzymatic interesterification has become a standard production method due to its energy efficiency and ability to maintain product consistency. Additionally, the European Union's Deforestation-Free Regulation has prompted manufacturers to develop palm-oil-free formulations, affecting supply chain dynamics and production costs[1]Source: European Parliament and Council of the European Union, “Regulation (EU) 2023/1115 on Deforestation-Free Supply Chains,” europa.eu. This transition has led companies to explore alternative oil sources, including sunflower, rapeseed, and soybean oils, while investing in research and development to maintain product quality and functionality.

Key Report Takeaways

- By type, soft margarine led with 54.68% of the margarine market share in 2025; liquid margarine is projected to expand at a 5.60% CAGR through 2031.

- By fat content, regular (> 80% fat) accounted for 59.72% of the margarine market size in 2025, while light (< 40% fat) is forecast to grow at 6.00% CAGR.

- By oil source, palm-oil formulations held 44.88% revenue share in 2025; soybean-oil variants are expected to record a market-leading 6.80% CAGR to 2031.

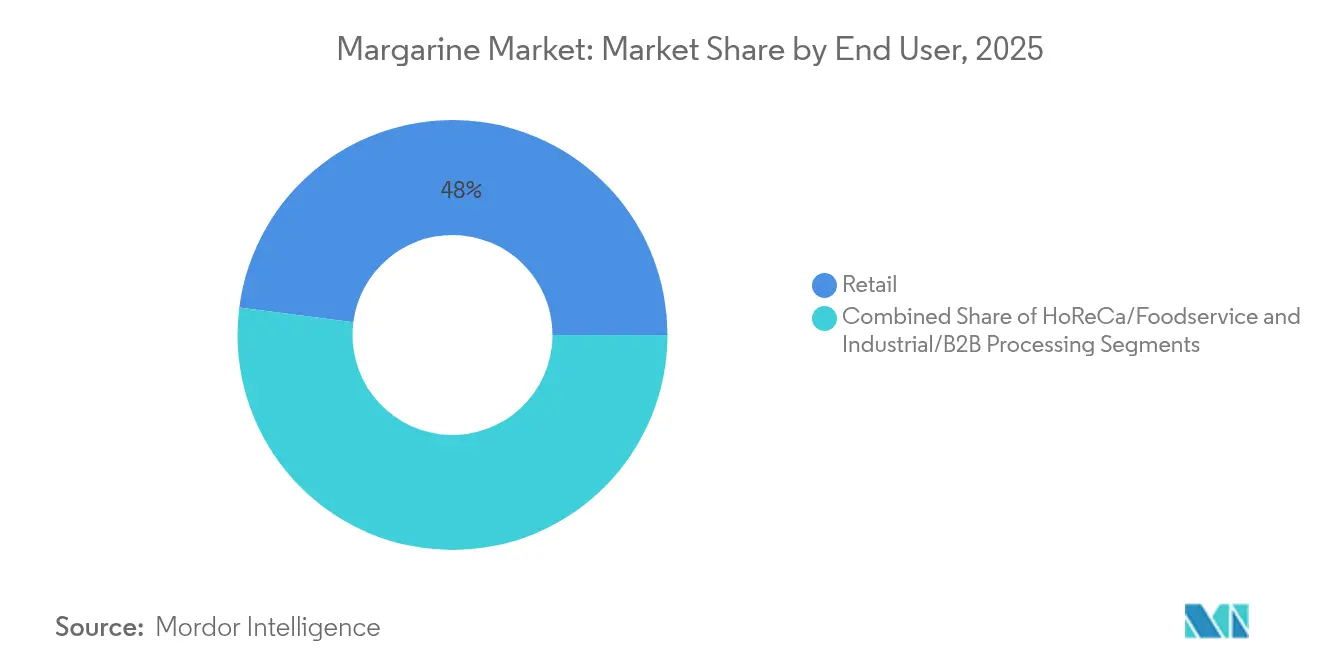

- By end user, the household segment commanded 47.95% of the global margarine market in 2025; the HoReCa channel shows the fastest growth at 6.20% CAGR.

- By packaging, tubs and cups represented 40.05% sales in 2025; sachets and pouches represent the fastest-growing format with a 6.60% CAGR.

- By region, Europe retained 29.85% of the margarine market in 2025; Asia-Pacific is the fastest-growing geography with a 6.30% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Margarine Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Premiumization of margarine through low-fat and fortified variants | +0.4% | Global, with early gains in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Surge in industrial demand from frozen bakery manufacturers | +0.6% | North America and Europe, spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Palm-oil-free formulations gaining traction due to sustainability regulations | +0.3% | Europe core, expanding to North America and Australia | Long term (≥ 4 years) |

| Growth of plant-based spreads | +0.5% | Global, with concentration in developed markets | Medium term (2-4 years) |

| Rising sunflower-oil supply from ukraine boosting cost competitiveness | +0.2% | Global, with primary impact in Europe and Middle East | Short term (≤ 2 years) |

| Expansion of private-label margarine in discount retail formats | +0.3% | Global, with acceleration in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premiumization of margarine through low-fat and fortified variants

The increasing focus on health and wellness among consumers worldwide has fundamentally transformed spreads from basic commodity alternatives into functional food products with targeted nutritional benefits. Fortified spreads now provide essential micronutrient benefits through carefully selected vitamins and minerals, enabling manufacturers to implement strategic premium pricing approaches that effectively manage raw material cost fluctuations in the global market. Advanced liquid formulations with significantly reduced saturated fat content successfully maintain optimal texture, consistency, and baking performance in cakes, pastries, and other baked goods. Comprehensive Vitamin A fortification programs implemented across various Asian markets have demonstrated substantial measurable improvements in retinol levels among children, directly addressing critical nutritional deficiencies in these populations. In developed markets, spreads containing specific plant sterols have consistently demonstrated robust clinical efficacy in reducing LDL cholesterol levels by significant percentages, firmly establishing their position as scientifically validated health-beneficial food products in the daily diet.

Surge in industrial demand from frozen bakery manufacturers

The industrial margarine market is experiencing growth driven by increased production from frozen bakery manufacturers responding to rising convenience food consumption. The segment benefits from specialized margarine formulations designed for automated processing and longer shelf life. CSM Ingredients' Crema facility demonstrates this expansion through new production lines that boost capacity to over 70,000 tons annually, focusing on frozen bakery applications where margarine offers improved sustainability metrics compared to animal-based alternatives. Moreover, Bunge's margarine portfolio for bakery applications showcases the technical requirements of the industry, providing specialized hardstocks that ensure consistent performance across various baking applications, from cookies to bread products. Industrial margarine's functionality in laminated products and stability during freeze-thaw cycles makes it particularly valuable for frozen bakery distribution. Manufacturers utilize advanced emulsifier technologies to produce stable food emulsions across hard, soft, and liquid margarine variants, each optimized for specific industrial requirements. The increased industrial demand aligns with the broader market shift toward processed convenience foods, where margarine's technical properties support efficient large-scale food manufacturing operations.

Palm-oil-free formulations gaining traction due to sustainability regulations

The European Union's Deforestation-Free Regulation requires complete plantation-level traceability by December 2024. This regulation is accelerating palm oil substitution efforts among suppliers, even as palm oil continues to account for 45% of 2024 inputs in the European market. The regulation mandates detailed documentation of supply chain origins, environmental impact assessments, and verification of deforestation-free practices. Companies must implement comprehensive monitoring systems and maintain records of their palm oil sources, including satellite imagery and geolocation data for plantations. While shea butter and high-oleic seeds emerge as primary alternatives, life-cycle analyses indicate that complete palm oil substitution may increase global land-use pressures. Manufacturers must balance technical feasibility, consumer preferences, and sustainability goals while navigating the evolving regulatory requirements. This includes implementing robust traceability systems, conducting regular supplier audits, developing alternative sourcing strategies, and investing in supply chain transparency technologies that align with both regulatory compliance and environmental sustainability objectives. The transition also requires significant investment in research and development to optimize alternative oil processing methods and ensure product quality consistency.

Growth of plant-based spreads

The plant-based spreads market has evolved beyond traditional margarine, as manufacturers develop sophisticated alternatives that match dairy butter's functionality while offering enhanced sustainability benefits. This evolution reflects changing consumer preferences and technological advancements in food production. Flora Food Group's transformation into Upfield exemplifies this significant market shift, with the company generating EUR 3.3 billion in net sales in 2025. The company made strategic investments in Kansas manufacturing facilities to reduce dependence on European imports and enhance its plant-based cream and cream cheese production capabilities, demonstrating its commitment to market expansion and operational efficiency. Technological advancements have enabled plant-based alternatives to achieve superior dairy-like taste and performance characteristics. Companies like Willicroft are pioneering innovative approaches, using advanced fermentation processes to create products that accurately replicate traditional butter characteristics while maintaining strict plant-based credentials. These developments represent a significant step forward in meeting consumer demands for sustainable, high-quality alternatives to dairy products.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Trans-fat ban compliance raising reformulation costs in emerging markets | -0.3% | Emerging markets, with concentration in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Volatility in vegetable-oil prices linked to climate-induced yield shifts | -0.4% | Global, with primary impact in import-dependent regions | Short term (≤ 2 years) |

| Negative health perception versus butter | -0.2% | Developed markets, particularly North America and Europe | Long term (≥ 4 years) |

| Import tariff escalations on palm oil | -0.3% | Import-dependent regions, particularly Asia and Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Trans-fat ban compliance raising reformulation costs in emerging markets

The elimination of trans-fats presents significant challenges for manufacturers in emerging markets, who must balance technological investments and product reformulation with maintaining affordable prices. These manufacturers face substantial financial pressures in upgrading their production facilities, developing new formulations, and sourcing alternative ingredients while ensuring their products remain accessible to price-sensitive consumers. Malaysia's implementation of strict trans-fat regulations from September 2025, which will prohibit food containing more than 2g/100g of fat in trans fatty acids, demonstrates the increasing regulatory requirements in emerging markets to align with WHO recommendations[2]Source: Ministry of Health Malaysia, “Guidelines on Trans-Fatty Acid Limits in Food,” moh.gov.my. Thailand's trans-fat reduction program succeeded through extensive public-private collaboration, highlighting the need for institutional coordination in markets with limited regulatory capacity. India's reformulation studies indicate that while technical solutions are available, manufacturers face obstacles in maintaining product texture and managing increased palm oil costs. Small and medium-sized producers particularly struggle with the technical expertise required for reformulation and the financial implications of switching to alternative ingredients. The compliance requirements create market entry barriers and may lead to industry consolidation as smaller manufacturers struggle to meet regulations while keeping prices competitive, potentially reshaping the competitive landscape in these emerging markets.

Volatility in vegetable-oil prices linked to climate-induced yield shifts

Climate-related disruptions in agriculture have created significant instability in vegetable oil markets. This instability has compelled margarine manufacturers to implement advanced hedging strategies and adaptable formulation methods to sustain profitability during periods of fluctuating raw material costs. The Ukraine conflict highlights how geopolitical events intensify climate-related challenges, as supply chain disruptions have required manufacturers to procure oils from different regions at higher costs while meeting established product quality standards. Supply chain difficulties intensified by global events have led companies to modify their sourcing and formulation approaches. Cargill's Fatitudes research indicates that over 50% of consumers now examine fats and oils content in packaged products, increasing demand for transparency during price fluctuations. High-oleic sunflower oil contracts include quality premiums necessary for margarine production requirements, though price sensitivity remains significant as manufacturers work to balance cost control with performance requirements. These market conditions have driven strategic changes toward more diverse oil-sourcing portfolios and extended supply agreements, while potentially increasing the adoption of alternative solutions such as Savor's carbon-based fats that operate independently of traditional agricultural systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Liquid Variants Drive Automation

Liquid margarines gained market share as food manufacturers automated high-volume production lines. While soft spreads maintained 54.68% of 2025 revenue, liquid formats achieved the highest growth rate at 5.60% CAGR. Industrial bakeries prefer pumpable oils that reduce labor requirements and enhance measurement precision. The liquid margarine market is projected to reach USD 5.32 billion by 2031, driven by enzymatic structuring technologies that preserve air incorporation and crumb texture. Soft variants remain dominant in retail refrigerated sections, providing consumers versatility for cooking, baking, and spreading. Hard margarines maintain a specific segment in laminated pastry production where precise melting points are essential.

The shift toward liquid formats supports product premiumization. Reduced saturated fat content aligns with EU front-of-pack labeling requirements, which increasingly influence urban millennial purchasing decisions. Manufacturing facilities that implement continuous micro-crystallization technology report improved production efficiency and reduced energy consumption, enhancing cost effectiveness. This transition demonstrates how the margarine market is evolving its product offerings to meet industrial automation needs while maintaining traditional consumer demand.

By Fat Content: Light Formulations Accelerate

Regular spreads (>80% fat) maintain a dominant 59.72% market share in 2025, primarily due to their superior taste profile, enhanced mouthfeel, and exceptional baking performance in both domestic and commercial applications. Light variants (<40% fat) are experiencing 6.00% annual growth, driven by increasing consumer focus on calorie reduction and health-conscious dietary choices. Manufacturers are improving light spreads through advanced multilamellar emulsions that maintain structural stability during prolonged refrigeration while preserving essential nutrients, particularly vitamins A and D.

Mid-range spreads (40-80% fat) serve as an effective compromise, particularly in emerging market HoReCa segments where chefs require acceptable texture and spreadability at lower costs than butter. Current innovation focuses on sophisticated botanical flavor extracts and advanced salt micro-encapsulation techniques to achieve comparable sensory qualities with reduced fat content. These technological developments enable the margarine market to align with current dietary guidelines while maintaining the indulgent characteristics essential for consumer acceptance across various demographic segments and usage occasions.

By Oil Source: Soybean Innovation Leads

Palm oil maintains a dominant 44.88% volume share in 2025, while increasing environmental and sustainability concerns drive food manufacturers and consumer brands to actively explore diverse feedstock alternatives. Soybean-based formulations lead market growth with a 6.80% CAGR, supported by technological advancements in processing methods. High-oleic varieties provide superior oxidative stability comparable to hydrogenated palm oil, enabling manufacturers to achieve zero-trans fat labels while meeting growing consumer demand for clean-label requirements. Rapeseed/canola oil appeals to premium market segments due to its beneficial omega-3 fatty acid content and nutritional profile, and sunflower oil remains essential in European markets because of its characteristic neutral flavor profile and versatile applications.

Enzymatic interesterification technology effectively maintains natural antioxidant compounds, significantly extending product shelf life and substantially reducing process-induced contaminants. Recent regulatory approval for stearidonic acid soybean test batches creates extensive opportunities for manufacturers to develop new functional health claims. Companies increasingly implement sophisticated blended-oils approaches to effectively manage raw material price fluctuations and supply chain uncertainties, demonstrating that feedstock flexibility has become a fundamental operational requirement for successful margarine market participants.

By End User: HoReCa Segment Surges

Households accounted for 47.95% of the 2025 turnover, while restaurants, hotels, and catering outlets demonstrated strong growth at 6.20% CAGR. The significant rise in commodity prices prompted extensive menu-engineering initiatives to reduce operating costs, leading to a substantial decrease in butter usage across food service establishments. Commercial establishments increasingly prefer alternatives due to their higher smoke points and extended shelf life, which significantly improve kitchen efficiency and operational workflow. The widespread adoption of portion-controlled sticks and pump-dispensed liquid cartons substantially reduces waste generation and labor requirements, making them particularly attractive for high-volume operations.

Industrial food processors, particularly in frozen pizza and confectionery manufacturing, maintain comprehensive and rigorous product specifications throughout their production processes. Their specialized research and development teams work extensively with suppliers to develop sophisticated, customized fat systems that perform consistently in high-shear mixers and tunnel ovens across various production conditions. This in-depth collaborative approach significantly increases switching costs and strengthens long-term supplier relationships, creating lasting partnerships within the industry.

By Packaging Type: Convenience Formats Expand

Tubs and cups maintain a 40.05% revenue share in 2025, remaining the preferred household packaging formats due to their durability, ease of storage, and reusability features. Sachets and pouches demonstrate 6.60% CAGR by 2031, driven by emerging market retailers offering single-use portions at price points matching daily wage budgets, particularly in regions with limited refrigeration infrastructure. The foodservice sector favors sticks and blocks for pre-portioned baking needs, enabling precise measurements and reducing waste in commercial kitchens, while industrial operations primarily use 10-kg bag-in-box and drum formats for bulk processing efficiency. In Europe, compostable paper films and plastic-free molded fibers are increasing in adoption, influenced by extended producer-responsibility fees that increase traditional resin costs. These evolving packaging choices now significantly influence brand perception and consumer purchasing decisions across retail channels.

Equipment manufacturers report significant growth in high-speed vertical-form-fill-seal machinery for margarine pouches, enabled by material reduction capabilities and enhanced optical inspection systems that ensure seal quality and product freshness. The machinery improvements include advanced temperature control mechanisms, automated quality checks, and real-time monitoring systems. The convergence of sustainability requirements, user convenience, and cost considerations continues to transform margarine packaging and distribution methods from production facilities to consumer storage, with manufacturers investing in research and development to optimize packaging solutions for different market segments.

Geography Analysis

Europe accounted for 29.85% of global revenue in 2025, maintaining its leadership position due to established consumption patterns, broad acceptance of fortified products, and advanced palm-oil-free product development. The market shows low single-digit growth as it matures and consumers shift toward premium plant-based butter alternatives. Clear regulations on labeling and deforestation have improved supply-chain transparency, enabling brands to differentiate themselves through verified sustainable sourcing.

Asia-Pacific demonstrates strong growth potential with a projected 6.30% CAGR through 2031. This growth stems from urbanization, increasing disposable incomes, and expanding frozen-bakery adoption. Chinese quick-service restaurants increasingly adopt liquid margarine for cost management, while Indian refiners seek tariff adjustments to obtain competitive oil supplies.

North America maintains mid-single-digit growth, with zero-trans and non-GMO products becoming standard market requirements. Industrial bakeries transition to high-oleic blends, using domestic soybeans to minimize imported oil dependencies. Latin America and the Middle East/Africa represent smaller but growing markets. The expansion of discount retailers supports private label spread sales, while government-mandated vitamin-A fortification programs strengthen margarine's position in public health initiatives, especially in regions addressing micronutrient deficiencies.

Competitive Landscape

The market exhibits fragmentation, including global corporations, regional specialists, and emerging plant-based product manufacturers. Prominent players in the market include Conagra Brands Inc., Upfield BV, Bunge Limited, Wilmar International Ltd., and Vandemoortele NV. Companies are strategically realigning their portfolios. Research and development focus on technological advancements, including enzymatic interesterification, carbon-captured synthetic fats, and mycoprotein matrices that aim to match dairy performance with reduced environmental impact.

Companies with certified deforestation-free supply chains gain preferential retail placement in European and Japanese markets. Sustainable packaging innovations, including molded-fiber containers and compostable sachets, enhance brand value and meet retailer sustainability requirements. In emerging markets, companies utilize flexible manufacturing and local partnerships to access growing discount retail chains, while private-label manufacturing supports capital investment through steady revenue streams.

Market evolution and strategic opportunities include fortified spreads for children in nutritionally deficient regions and bakery margarines marketed as egg substitutes. Emerging companies developing air-based fats seek development partnerships with established manufacturers to address raw material supply risks. Traditional manufacturers must decide whether to partner with, acquire, or compete against these new entrants as the margarine market evolves into a broader plant-based fats category.

Margarine Industry Leaders

-

Conagra Brands, Inc

-

Upfield BV

-

Bunge Limited

-

Wilmar International Ltd.

-

Vandemoortele NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: BlueBand (Flora Food Group) introduced a larger margarine pack for food MSMEs and launched the "BlueBand Professional UMKM Star #AhlinyaRasaSukses" program, which includes a 500g margarine product for bakeries.

- November 2024: In Kragujevac, Serbia, Puratos Group unveiled a cutting-edge margarine production facility. With a hefty investment of seven million euros, the facility not only bolsters Puratos' production capabilities and diversifies its product range but also plays a pivotal role in Serbia's economic landscape by generating new employment opportunities and championing sustainable practices.

- April 2024: The United Kingdom supermarkets welcomed the debut of "Flora Tubs," touted as the "world's first" paper margarine tub. Notably, the tub is entirely recyclable with paper and cardboard household waste, thanks to its absence of a plastic liner. Marketed as a product crafted from natural ingredients, it proudly boasts being 100% plant-based, dairy-free, and devoid of palm oil.

- March 2024: Vandemoortele expanded its product portfolio with the introduction of baking and frying margarine. The Belgian brand launched its first 100% plant-based product: Vandemoortele Baking & Frying. Vandemoortele, an established brand in Belgian households, offers a range of products including mayonnaises, culinary oils, vinaigrettes, frying oils, and margarines.

Global Margarine Market Report Scope

Margarine is a spread manufactured from animal fats and vegetable oil and is generally used as a substitute for butter. The global margarine market is segmented by type, end user, and geography. By type, margarine is segmented into hard, soft and liquid margarine. By end user, the market is segmented into household consumers, HoReCa and industrial. By Geography, the market is segmented into North America, Europe, Asia-Pacific, South America, Middle East & Africa. The market sizing has been done in value terms in USD for all the above mentioned segments.

| Hard |

| Soft |

| Liquid |

| Regular (>80% Fat) |

| Low-Fat (40-80% Fat) |

| Light (<40% Fat) |

| Palm-Oil-Based |

| Soybean-Oil-Based |

| Rapeseed/Canola-Oil-Based |

| Others |

| Retail | Supermarkets/Hypermarkets |

| Convenience and Grocery Stores | |

| Online Retail Stores | |

| Other Channels | |

| HoReCa/Foodservice | |

| Industrial/B2B Processing |

| Tubs and Cups |

| Sticks and Blocks |

| Sachets and Pouches |

| Bulk (10 kg+) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Hard | |

| Soft | ||

| Liquid | ||

| By Fat Content | Regular (>80% Fat) | |

| Low-Fat (40-80% Fat) | ||

| Light (<40% Fat) | ||

| By Oil Source | Palm-Oil-Based | |

| Soybean-Oil-Based | ||

| Rapeseed/Canola-Oil-Based | ||

| Others | ||

| By End User | Retail | Supermarkets/Hypermarkets |

| Convenience and Grocery Stores | ||

| Online Retail Stores | ||

| Other Channels | ||

| HoReCa/Foodservice | ||

| Industrial/B2B Processing | ||

| By Packaging Type | Tubs and Cups | |

| Sticks and Blocks | ||

| Sachets and Pouches | ||

| Bulk (10 kg+) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the global margarine market in 2026?

The global margarine market stands at USD 24.08 billion in 2026 and is projected to grow to USD 26.7 billion by 2031.

Which region is expanding the fastest?

Asia-Pacific shows the strongest trajectory, advancing at a 6.30% CAGR thanks to rising frozen-bakery output and middle-class consumption growth.

Why are liquid margarines gaining popularity?

Liquid formats enable automated dispensing that reduces labor, deliver stable performance in industrial bakeries, and support lower saturated-fat recipes without losing functionality.

What is driving HoReCa-sector demand for margarine?

Restaurants and caterers are substituting butter with margarine to manage costs, leverage higher smoke points, and reduce operational waste, leading to a 6.20% CAGR for the channel.

Page last updated on: