Food & Beverage

2nd MayMarket Analysis of Synthetic Food Colorants for a Beverage Leader

5 Min Read

The Oryzenin Market is Segmented by Type (Isolates, Concentrates, and Hydrolysates), by Form (Dry, and Liquid), by Application (Bakery and Confectionery, Beverages, Sports and Energy Nutrition, Dairy Alternatives, Meat Substitutes, and Other Applications), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

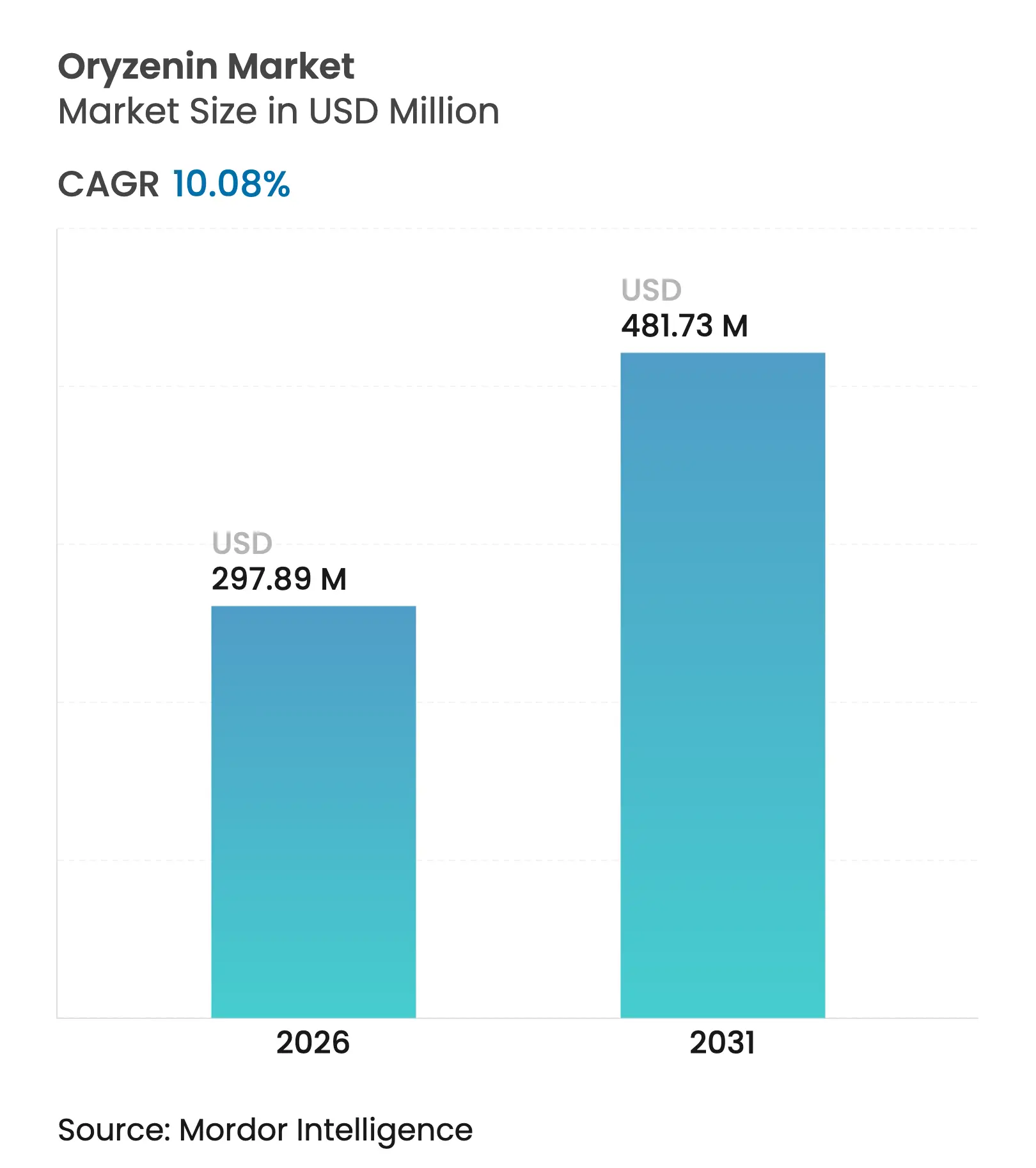

| Market Size (2026) | USD 297.89 Million |

| Market Size (2031) | USD 481.73 Million |

| Growth Rate (2026 - 2031) | 10.08 % CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

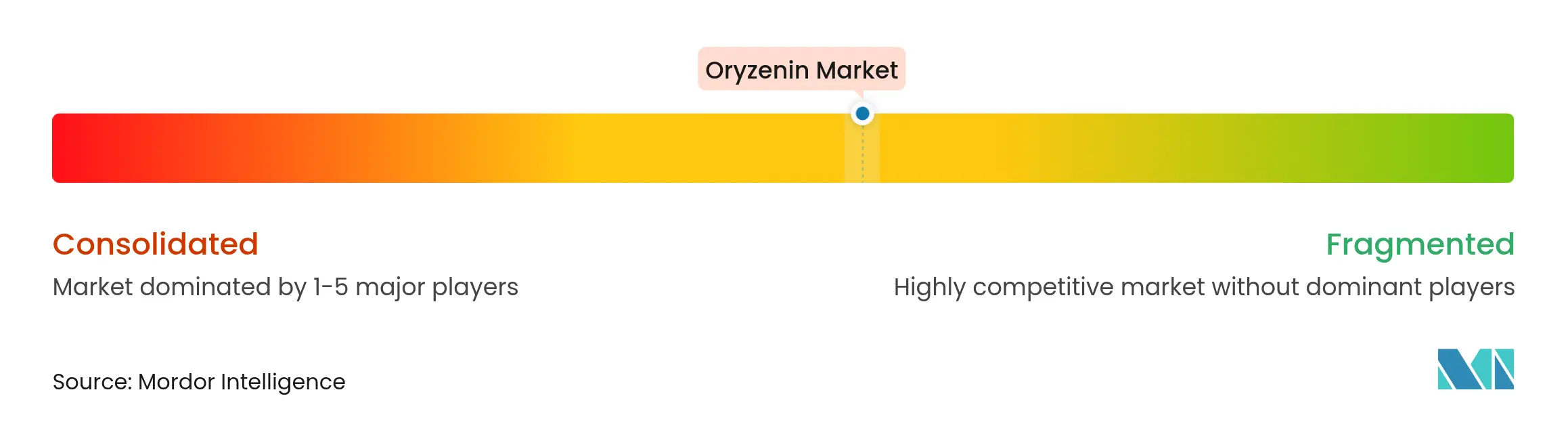

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

oryzenin market size in 2026 is estimated at USD 297.89 million, growing from 2025 value of USD 270.62 million with 2031 projections showing USD 481.73 million, growing at 10.08% CAGR over 2026-2031. The market growth is driven by oryzenin's hypoallergenic properties, plant-based nature, and suitability for clean-label and allergen-free products. The increasing prevalence of food allergies has led manufacturers and consumers to adopt rice-derived proteins like oryzenin as a safe, digestible, and non-GMO alternative. The market expansion is supported by growing consumer preference for sustainable, vegan, and organic diets across functional foods, nutraceuticals, infant nutrition, and sports supplements. Strict regulations in developed markets regarding ingredient labeling and clean-label requirements enhance oryzenin's market position. Improvements in extraction methods, microencapsulation, and enzymatic hydrolysis have enhanced product quality, taste, and solubility, making oryzenin a viable alternative to whey, casein, and pea proteins. The market continues to grow through product innovation, regulatory compliance, and increased adoption by major food and beverage manufacturers.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising demand for hypoallergenic plant proteins in infant nutrition Rising demand for hypoallergenic plant proteins in infant nutrition | +1.8% | Global, with early adoption in North America and European Union | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.8% | Geographic Relevance:Global, with early adoption in North America and European Union | Impact Timeline:Medium term (2-4 years) |

Increasing adoption of rice protein in texturized meat analogues Increasing adoption of rice protein in texturized meat analogues | +2.1% | North America and European Union core, expanding to Asia-Pacific | Short term (≤ 2 years) | |||

Growing application in sports nutrition and dietary supplements Growing application in sports nutrition and dietary supplements | +1.5% | Global, with premium positioning in developed markets | Short term (≤ 2 years) | |||

Expansion of functional food and beverage product portfolios Expansion of functional food and beverage product portfolios | +1.2% | Global, led by North America innovation hubs | Medium term (2-4 years) | |||

Regulatory approvals and GRAS status accelerating global commercialization Regulatory approvals and GRAS status accelerating global commercialization | +2.3% | North America leading, European Union following with novel foods framework | Long term (≥ 4 years) | |||

Growing demand for clean label and sustainable ingredients Growing demand for clean label and sustainable ingredients | +1.6% | Global, with premium markets driving adoption | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Demand for Hypoallergenic Plant Proteins in Infant Nutrition

Infant nutrition applications are driving oryzenin adoption as manufacturers respond to increasing food allergies and regulatory requirements for safer formulations. Rice protein's hypoallergenic properties make it advantageous compared to traditional allergens, with clinical studies showing similar muscle-building efficacy to whey protein without dairy allergen risks. While concerns about lead content in plant-based protein powders have emerged, rice protein producers like Axiom Foods have developed products such as Oryzatein 2.0 with no detectable lead levels, meeting Proposition 65 requirements [1]Source: Office of Environmental Health Hazard Assessment (OEHHA), "Proposition 65", oehha.ca.gov. Elemental formulas, primarily amino acid-based, are increasingly prescribed for pediatric conditions like cow's milk allergy and eosinophilic esophagitis, creating demand for hypoallergenic protein sources that support growth without adverse reactions. The Food and Drug Administration (FDA)'s enhanced GRAS review requirements, though extending development timelines, benefit established rice protein suppliers with proven safety profiles. This regulatory framework creates barriers to entry for new market participants while maintaining higher safety standards in infant nutrition.

Increasing Adoption of Rice Protein in Texturized Meat Analogues

Meat alternative manufacturers choose rice protein to solve taste and texture problems that have slowed plant-based meat growth. Rice protein's neutral flavor masks taste better than pea and soy alternatives. The International Food Information Council (IFIC) reports that in 2024, 71% of consumers want more protein in their diet [2]Source: International Food Information Council (IFIC), "2024 IFIC Food and Health Survey", foodinsight.org. However, taste issues have caused the plant-based protein market to stall, which is why manufacturers are turning to rice protein's mild flavor. Companies are developing new heat treatment methods to improve rice protein's solubility while keeping its emulsification properties, making it work better in meat alternatives that need specific textures. Manufacturers are also creating hybrid formulas by mixing rice and pea proteins, which research shows improves texture and keeps more beneficial compounds when processed at low temperatures. New precision fermentation techniques are making rice protein even better. These advances make rice protein a crucial ingredient in new meat alternatives that offer both good nutrition and taste that consumers enjoy.

Growing Application in Sports Nutrition and Dietary Supplements

Sports nutrition is the primary application segment for oryzenin, driven by consumer demand for organic, clean-label products. Rice protein has demonstrated effectiveness in muscle protein synthesis, comparable to whey protein, while meeting clean-label requirements preferred by health-conscious consumers. The introduction of NiHPRO, a hydrolyzed protein isolate that combines rice protein with pea protein and essential amino acids, has achieved a Digestible Indispensable Amino Acid Score (DIAAS) of 1.16, exceeding whey protein isolate while maintaining its vegan status. The increasing costs of whey protein have created favorable pricing for rice protein alternatives, enabling manufacturers to offer cost-effective formulations without compromising nutritional value. The segment continues to expand across diverse consumer groups, including women's health and GLP-1 users who require easily digestible protein options that meet their specific dietary needs.

Expansion of Functional Food and Beverage Product Portfolios

Beverage manufacturers are incorporating rice protein into functional formulations due to its superior solubility compared to other plant proteins and growing consumer demand for protein-enriched products. The high-protein beverage market growth has prompted manufacturers to select protein sources that maintain product clarity and neutral taste while delivering nutritional benefits. Rice protein's compatibility with precision fermentation technologies enables hybrid formulations that combine plant-based and fermented protein alternatives, addressing sustainability and functionality requirements. Manufacturers are overcoming formulation challenges through protein blending and advanced processing techniques that improve heat stability and shelf-life while maintaining the taste and texture that consumers expect.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Unpleasant off-flavour and poor solubility limiting use in beverages Unpleasant off-flavour and poor solubility limiting use in beverages | -1.4% | Global, particularly affecting premium beverage segments | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-1.4% | Geographic Relevance:Global, particularly affecting premium beverage segments | Impact Timeline:Short term (≤ 2 years) |

Higher production costs compared to soy and pea protein Higher production costs compared to soy and pea protein | -0.9% | Global, with cost sensitivity highest in emerging markets | Medium term (2-4 years) | |||

Climate-driven variability in rice production affecting raw material pricing Climate-driven variability in rice production affecting raw material pricing | -1.1% | Asia-Pacific core, with supply chain impacts globally | Long term (≥ 4 years) | |||

Technical challenges in extraction and processing of oryzenin from rice Technical challenges in extraction and processing of oryzenin from rice | -0.8% | Global, affecting scalability and quality consistency | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Unpleasant Off-Flavour and Poor Solubility Limiting Use in Beverages

Rice protein faces challenges in beverage applications due to its flavor profile and solubility limitations, despite improvements in processing methods. While rice protein has a milder taste than pea protein, its chalky texture and slight bitterness affect consumer acceptance in clear beverages. Companies such as Sensient and Cargill are developing flavor masking solutions using yeast extracts and modulation compounds, combined with sweeteners to enhance mouthfeel and taste. Processing methods, including enzymatic hydrolysis and lactic acid bacteria fermentation, have demonstrated effectiveness in reducing off-flavors by decreasing hexanal compounds. Beverage manufacturers are increasingly using hybrid protein formulations that combine rice protein with other sources to address these challenges while maintaining clean-label requirements.

Higher Production Costs Compared to Soy and Pea Protein

Rice protein production faces economic challenges due to higher processing costs and lower extraction efficiencies compared to soy and pea protein alternatives, limiting its market penetration in cost-sensitive applications. The extraction of oryzenin from rice bran requires multiple purification steps and specialized equipment, resulting in higher production costs than commodity plant proteins. Rice production variability further impacts costs, as climate-driven supply disruptions affect raw material pricing and availability. According to the United States Department of Agriculture (USDA), Japan experienced an 80% rice price increase in January 2025 compared to the previous year, necessitating government intervention through emergency reserve releases [3]Source: United States Department of Agriculture (USDA), "Continued High Prices for Japanese Table Rice Leads to High Import Demand and Release of Government Emergency Rice Supplies", www.fas.usda.gov. The industry is implementing technological innovations to improve extraction efficiency and reduce processing costs. Rice protein producers are forming strategic partnerships with technology suppliers to address cost challenges through process optimization and shared infrastructure investments.

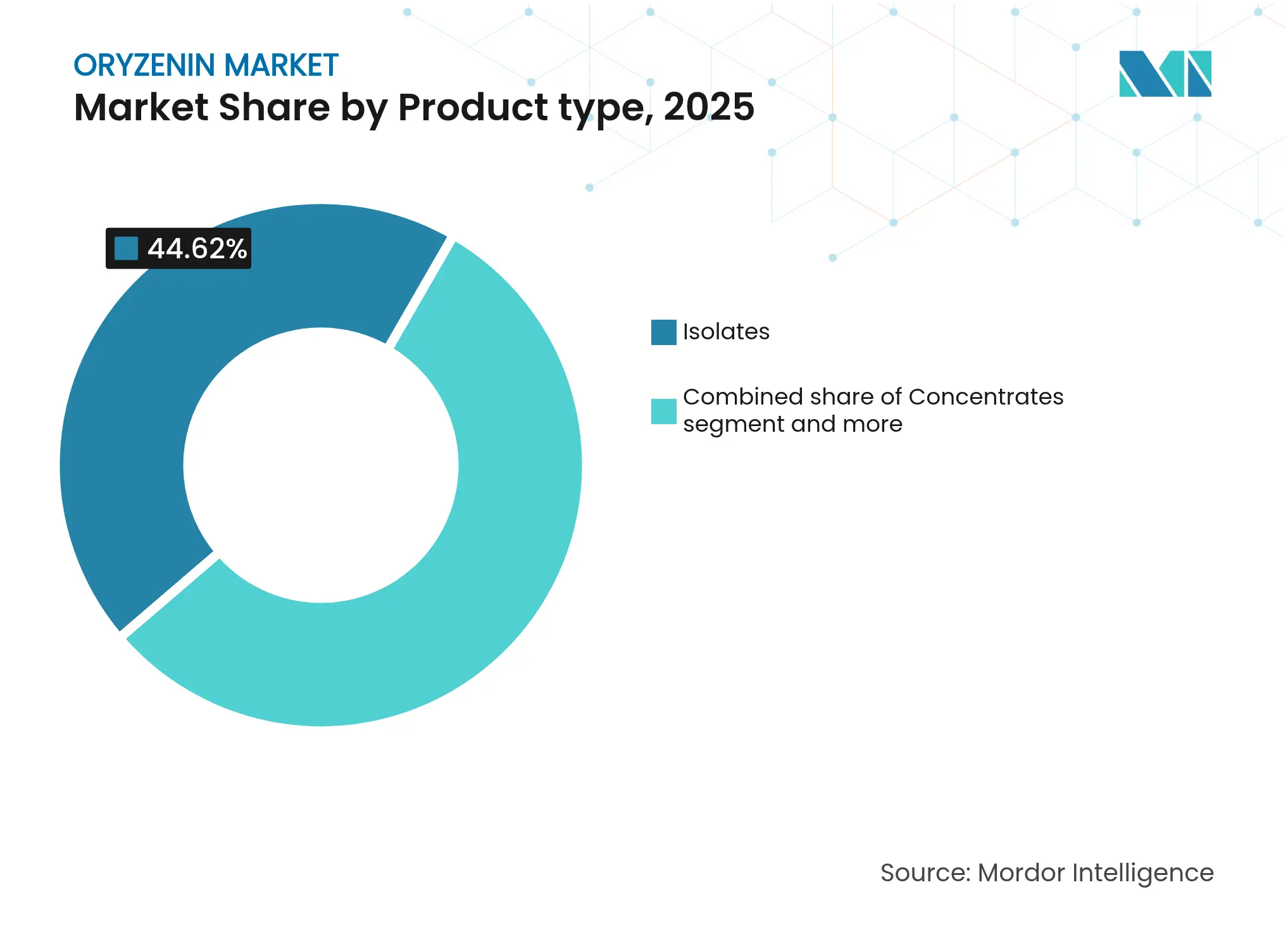

By Product Type: Isolates Dominate Despite Concentrates' Rapid Growth

Isolates command the largest market share at 44.62% in 2025, due to their high protein content and functional properties that meet requirements in sports nutrition and meat alternatives. The isolate segment's dominance is based on protein content and refined processing that removes most non-protein components, making it suitable for applications requiring high protein density and neutral flavor profiles. Concentrates represent the fastest-growing segment at 11.83% CAGR through 2031, as manufacturers seek balanced functionality at lower price points for bakery and confectionery applications. Hydrolysates serve a specialized niche, targeting applications requiring enhanced digestibility and rapid absorption, particularly in sports nutrition and clinical nutrition formulations where bioavailability is essential.

The product type segmentation shows market maturity, with manufacturers selecting protein forms based on specific functional requirements rather than cost alone. Isolates benefit from processing technologies that improve solubility and reduce off-flavors. Concentrates gain market share through processing methods that maintain nutritional value while reducing production costs, making them suitable for mass-market applications. The hydrolysates segment maintains premium pricing due to specialized processing requirements and applications in clinical and performance nutrition markets where enhanced bioavailability supports higher costs.

Note: Segment shares of all individual segments available upon report purchase

By Form: Dry Form Maintains Dominance Through Processing Advantages

Dry form rice protein holds 75.60% market share in 2025 and maintains the fastest growth rate at 12.55% CAGR through 2031. This dominance stems from its processing advantages, extended shelf life, and efficient transportation economics. Technological advances in spray-drying and microencapsulation have improved protein stability and functional properties while reducing moisture content to prevent microbial growth. Processing innovations have expanded applications through better particle size control and enhanced dispersibility, addressing traditional solubility challenges. The dry form benefits from efficient packaging and storage that reduce supply chain costs, particularly in international trade. The segment's growth continues through expanding applications in protein bars, baked goods, and supplement formulations, where dry ingredients provide formulation flexibility and processing convenience.

Liquid rice protein formulations fulfill specific requirements within the protein market, particularly in ready-to-drink (RTD) beverages, clinical nutrition, infant formulas, and functional sports drinks. These formulations provide immediate solubility, eliminating rehydration or dissolution steps. This characteristic enables straightforward integration into aqueous systems where homogeneity and rapid dispersion are essential, benefiting manufacturers by reducing processing complexity and improving production efficiency for time-sensitive products.

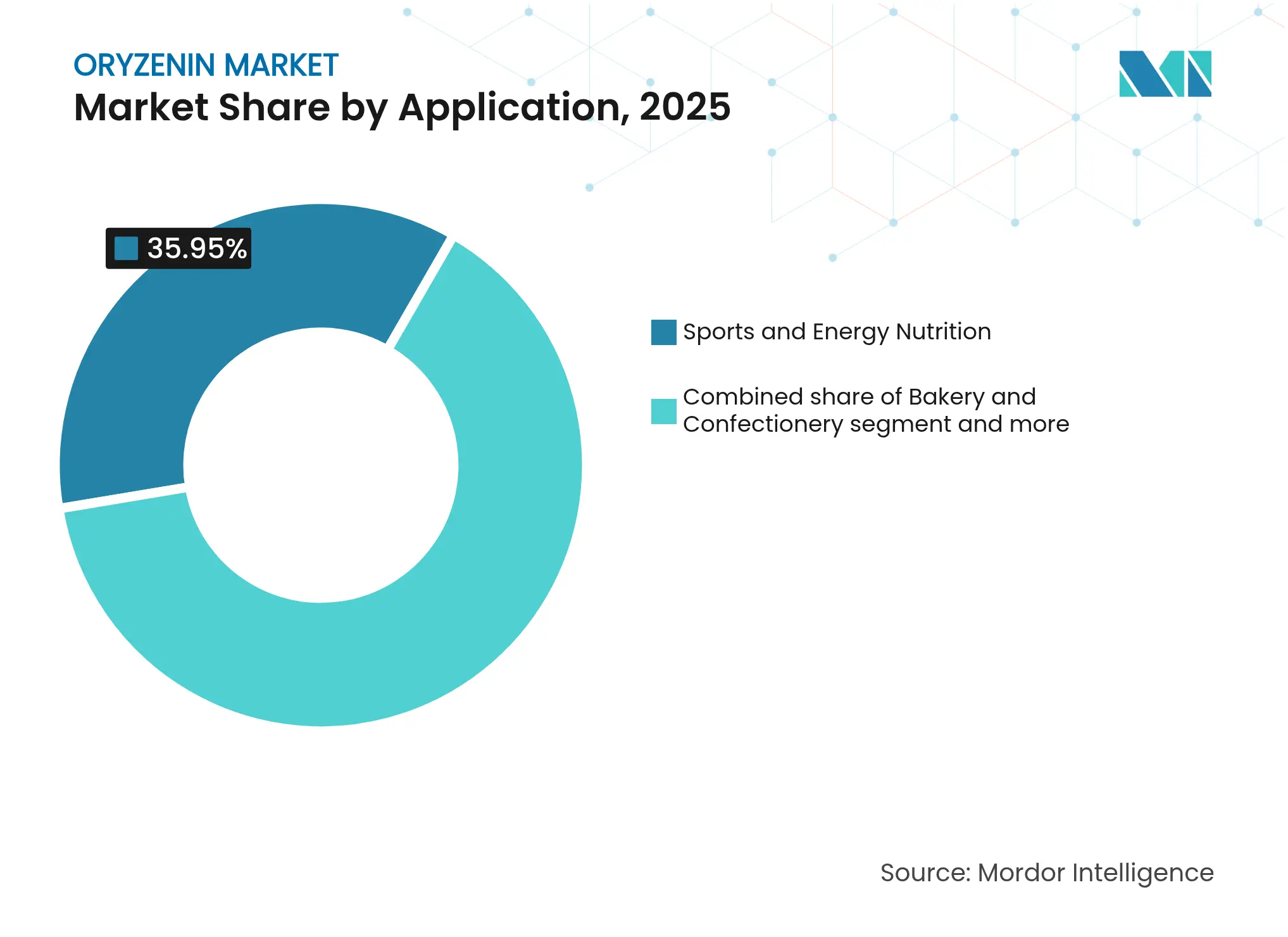

By Application: Sports Nutrition Leads While Meat Substitutes Accelerate

The Sports and Energy Nutrition segment maintains a dominant market position with 35.95% share in 2025, primarily attributed to rice protein's established hypoallergenic characteristics and scientifically validated muscle-building efficacy. This segment addresses the requirements of health-conscious consumers seeking dairy-free protein alternatives. The Meat Substitutes category demonstrates substantial market momentum with a projected CAGR of 11.62% through 2031, predominantly due to rice protein's inherent neutral flavor characteristics, which facilitate superior taste masking capabilities in plant-based meat formulations compared to conventional pea and soy variants. The beverage segment experiences technical constraints regarding rice protein's solubility parameters, although advancements in processing methodologies and flavor masking technologies are progressively expanding market opportunities.

The Dairy Alternatives segment exhibits significant market potential as manufacturers implement hypoallergenic protein sources that effectively replicate dairy protein functionality requirements. The Bakery and Confectionery segment successfully incorporates rice protein's gluten-free attributes and neutral flavor profile to achieve protein enhancement while maintaining established product specifications. Other Applications, including pet food and clinical nutrition, continue to expand due to rice protein's hypoallergenic benefits and broad regulatory acceptance.

Note: Segment shares of all individual segments available upon report purchase

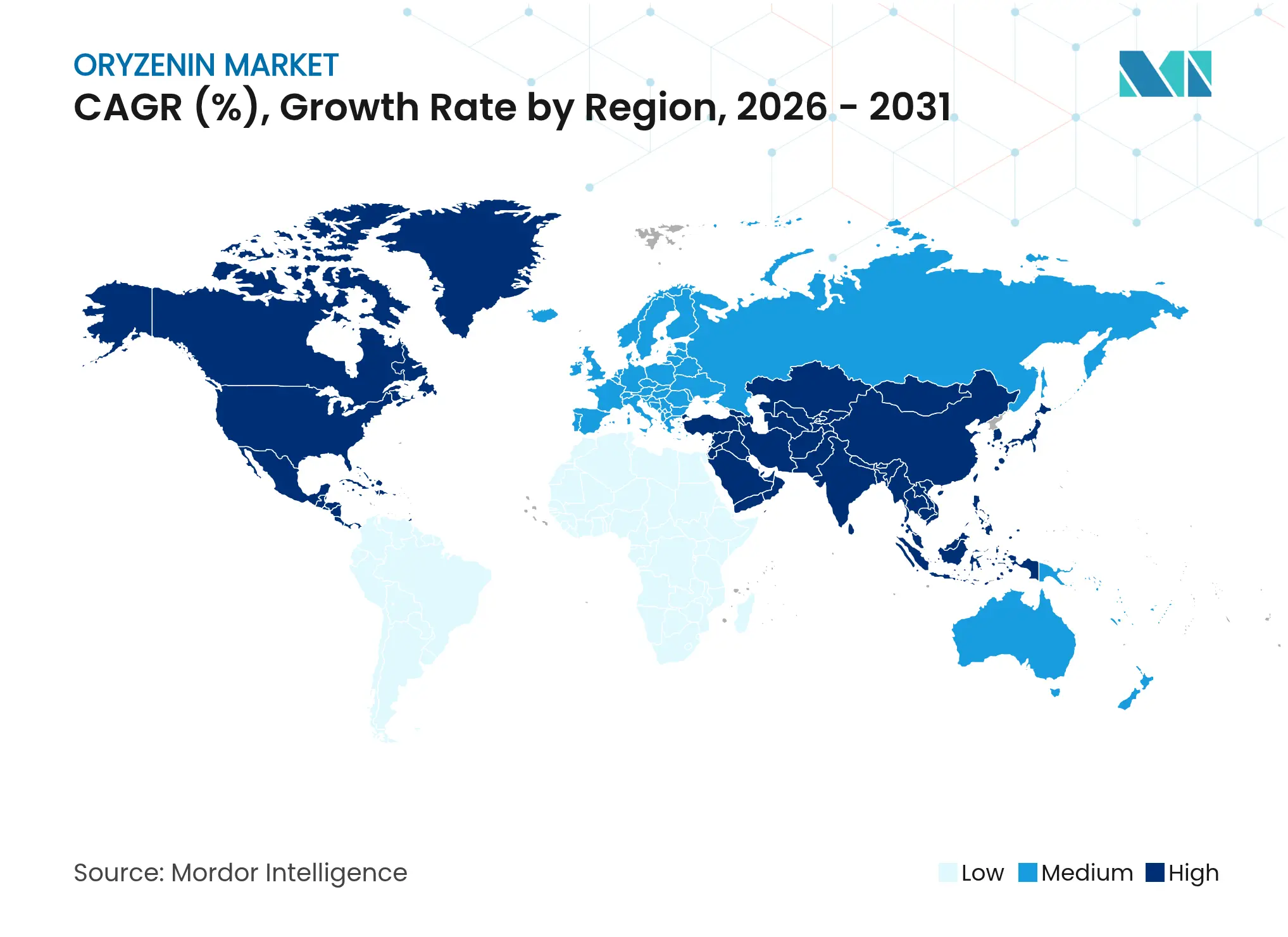

North America maintains market leadership with a 31.50% share in 2025, supported by regulatory classification for rice protein and established supply chain infrastructure. The region's efficient distribution network serves diverse application segments. Consumer preference for clean-label products and hypoallergenic protein alternatives drives market growth, particularly in sports nutrition and functional food applications. The Department of Health and Human Services (HHS) decision to eliminate self-affirmed GRAS pathways strengthens established rice protein suppliers while creating entry barriers for new companies. The region's advanced food processing capabilities and innovation ecosystem enable continuous product development and market expansion.

Asia-Pacific demonstrates the fastest growth at 11.35% CAGR through 2031. This growth stems from proximity to rice production sources, increasing plant-based protein demand, and government support for domestic protein production. The region benefits from cultural familiarity with rice and established processing infrastructure, resulting in lower production costs. Singapore's USD 14.8 million investment in the Centre for Precision Fermentation and Sustainability indicates regional commitment to alternative protein development. The development of drought-resistant rice varieties that require less water while maintaining yields offers solutions for stable raw material supply and market growth.

Europe presents strategic growth opportunities, characterized by strict regulatory requirements and increasing demand for sustainable, clean-label ingredients. The European Union's initiative to enhance domestic plant-based protein supply creates opportunities for rice protein integration, exemplified by Germany's EUR 38 million allocation for sustainable protein initiatives in 2023. European regulations favor natural additives and clean-label products, enhancing rice protein's potential in functional food applications. Research focusing on developing high-protein rice varieties through conventional breeding methods aligns with non-GMO regulations and positions Europe for domestic rice protein production to reduce import dependency.

Market Concentration

The oryzenin market demonstrates moderate fragmentation, with key market participants including Kerry Group PLC, Axiom Foods Inc., AIDP Inc., Südzucker AG, and Bioway Organic Group Ltd. These companies maintain their positions through regulatory compliance and technological advancements, while facing competition from new entrants offering specialized formulations.

Market leaders implement vertical integration strategies, managing the entire supply chain from rice procurement to final product distribution. This approach ensures consistent quality and optimizes costs, providing an advantage over smaller competitors. Companies differentiate themselves through technological investments in advanced extraction methods, flavor enhancement, and processing improvements to address traditional challenges in taste, solubility, and functionality.

Companies focus on obtaining GRAS status and reducing heavy metal content to meet food safety requirements. The market presents opportunities in hybrid protein formulations and precision fermentation applications, where rice protein serves as a foundation for enhanced nutrition and functionality. New market entrants are developing products that compete with traditional dairy and plant-based proteins while maintaining clean-label requirements to attract health-conscious consumers.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Oryzenin is a glutelin that is the main protein in rice. For consumers looking for lactose-free and allergen-free protein sources, it is a great substitute.

The Oryzenin Market is segmented by Type (Isolates, Concentrates, and Other Types), Application (Bakery and Confectionery, Beverages, Sports and Energy Nutrition, Dairy Alternatives, Meat Substitutes, and Other Applications), and Geography (North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. The report offers market size and values in (USD Million) during the forecast years for the above segments.

Market Analysis of Synthetic Food Colorants for a Beverage Leader

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.