Turbomolecular Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

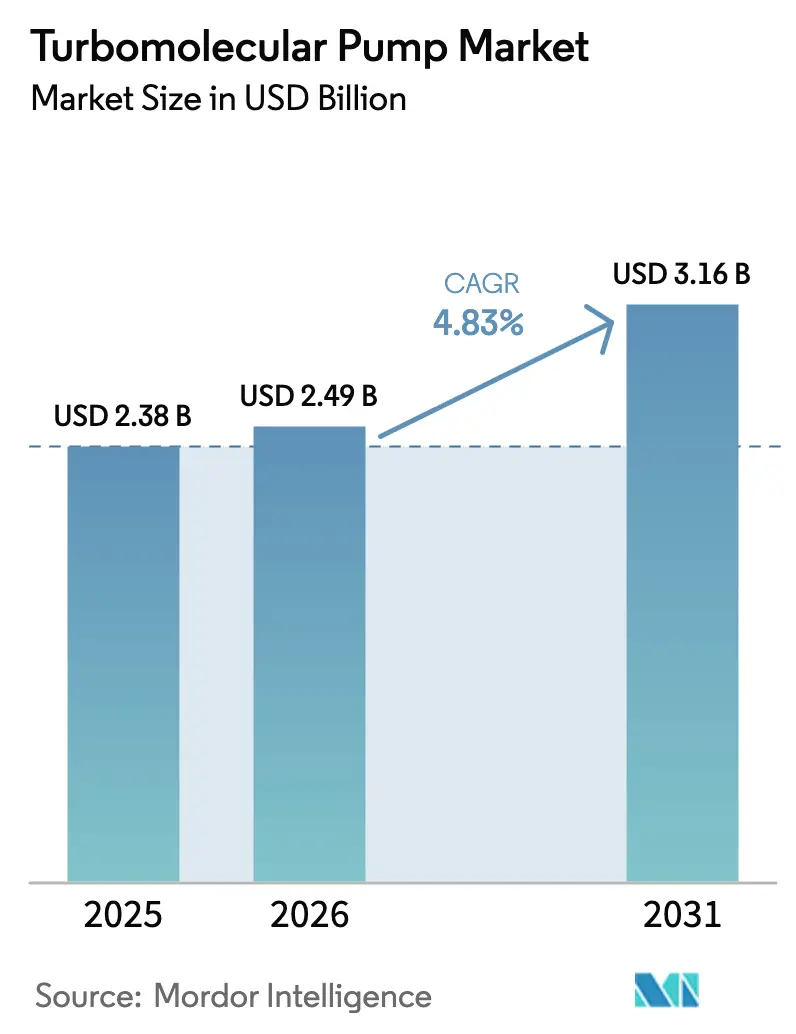

| Market Size (2026) | USD 2.49 Billion |

| Market Size (2031) | USD 3.16 Billion |

| Growth Rate (2026 - 2031) | 4.83% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Turbomolecular Pump Market Analysis by Mordor Intelligence

The turbomolecular pump market size was valued at USD 2.38 billion in 2025 and estimated to grow from USD 2.49 billion in 2026 to reach USD 3.16 billion by 2031, at a CAGR of 4.83% during the forecast period (2026-2031). Robust capital spending in semiconductor fabs, coupled with a decisive migration toward magnetically levitated (maglev) designs, anchors steady demand momentum. End-users also value rising pump capacities-now surpassing 3,000 l/s-for higher wafer throughput, thin-film efficiency, and emerging quantum-computing vacuum tolerances. In parallel, energy-efficiency mandates and net-zero agendas are pressing manufacturers to trim power draw and introduce predictive-maintenance software that keeps pumps in service longer with fewer unplanned stoppages. On the supply side, rare-earth magnet risk is prompting firms to dual-source materials and redesign rotors to tolerate magnet mixtures with lower dysprosium content. These converging dynamics sustain a balanced growth trajectory for the turbomolecular pump market despite cyclical swings in semiconductor equipment orders.

Key Report Takeaways

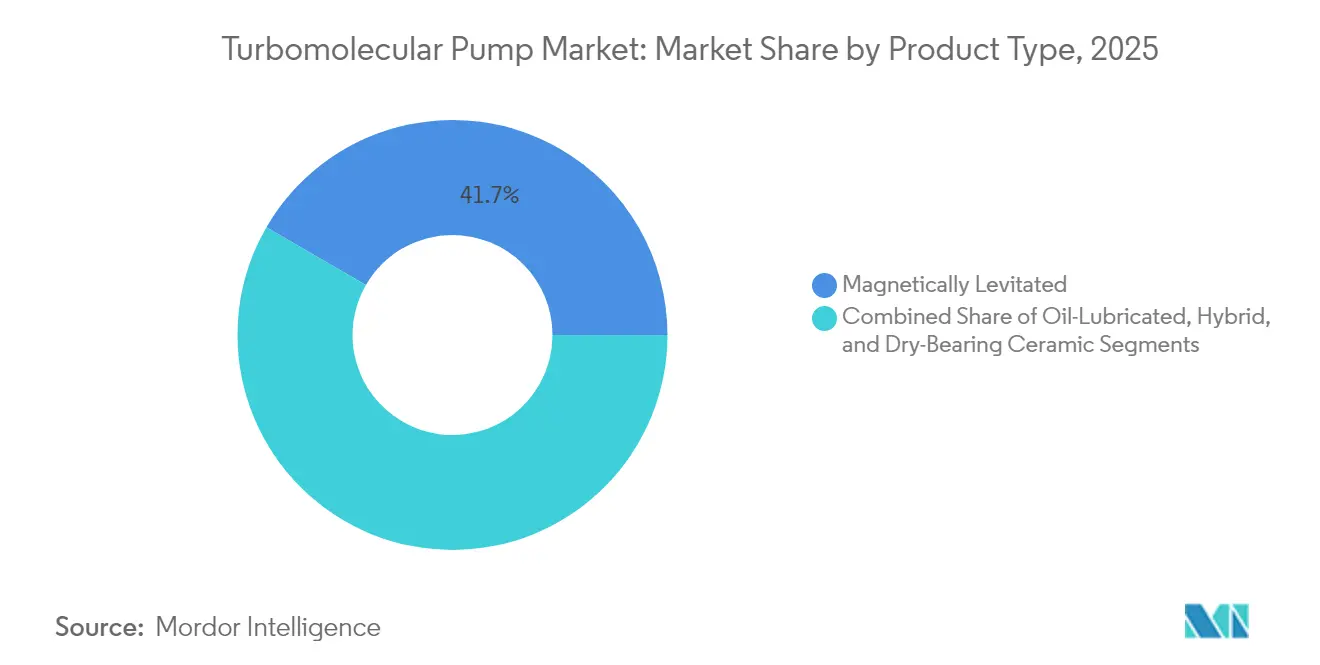

- By product type, magnetically levitated designs held 41.65% of the turbomolecular pump market share in 2025 and are projected to expand at a 4.95% CAGR to 2031.

- By bearing design, magnetic bearings controlled 55.45% revenue share in 2025, while hybrid bearings are set to record the highest 4.78% CAGR through 2031.

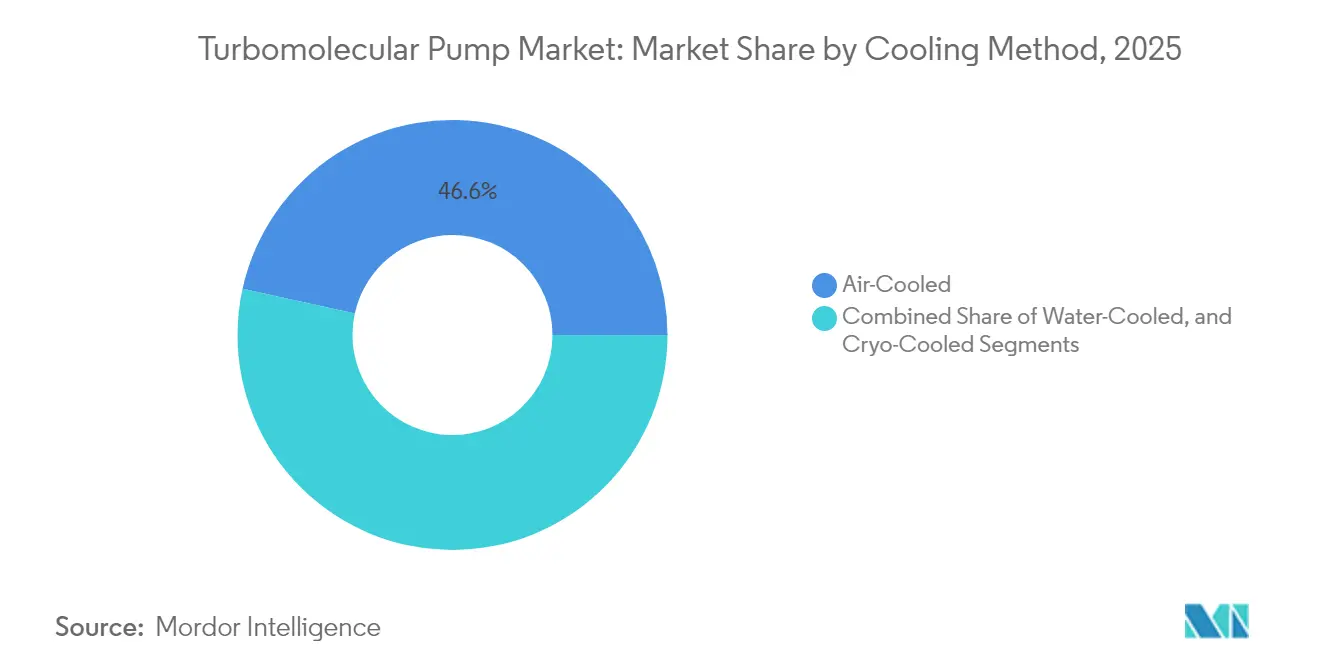

- By cooling method, air-cooled units accounted for 46.55% share of the turbomolecular pump market size in 2025; water-cooled models will grow at a 4.75% CAGR to 2031.

- By pumping-speed capacity, 1,000–3,000 l/s pumps captured 43.60% of the turbomolecular pump market size in 2025, but above 3,000 l/s is forecasted to have the fastest 4.96% CAGR.

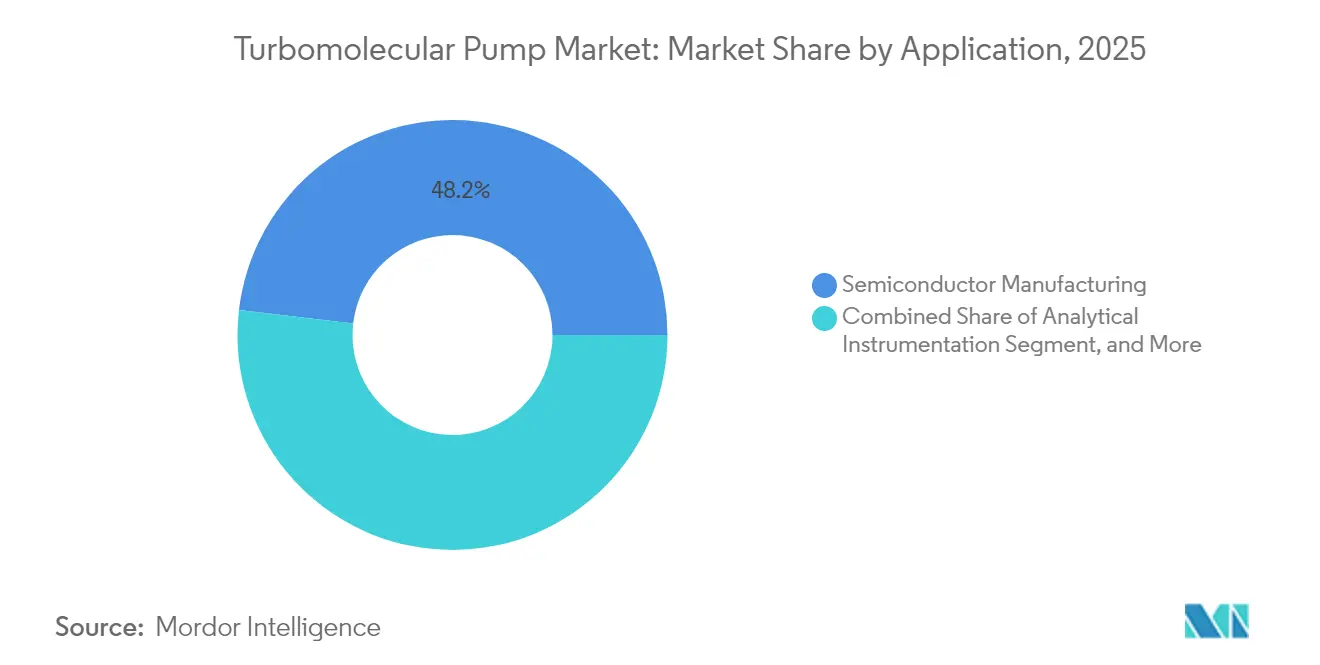

- By application, semiconductor manufacturing led with 48.15% revenue share in 2025, while thin-film & photovoltaic is advancing at a 5.04% CAGR through 2031.

- By end-user industry, electronics & semiconductor companies commanded 50.40% of the turbomolecular pump market share in 2025; research institutes are set to post a 4.70% CAGR until 2031.

- Regionally, Asia Pacific dominated with a 45.70% slice of the turbomolecular pump market in 2025 and is recording the highest 5.03% CAGR to 2031.

- Edwards Vacuum, Pfeiffer Vacuum, and Ebara Corporation jointly held about 51.60% of global sales in 2025, reflecting moderate concentration within the turbomolecular pump market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Turbomolecular Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor CAP-EX super-cycle | 1.20% | East Asia, North America | Medium term (2-4 years) |

| Rapid R&D expansion in life-science mass-spec labs | 1.00% | North America, Europe | Medium term (2-4 years) |

| Growing demand from analytical instrumentation OEMs | 0.70% | Global | Long term (≥ 4 years) |

| Shift toward magnetically levitated, oil-free designs | 0.50% | Global | Long term (≥ 4 years) |

| Quantum-computing vacuum-chamber build-outs | 0.40% | North America, Europe | Long term (≥ 4 years) |

| Fuel-cell stack manufacturing for hydrogen economy | 0.20% | Europe, North America, East Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Semiconductor CAP-EX Super-Cycle

Surging investments in next-generation fabs for AI and automotive chips are reinforcing the turbomolecular pump market. Leading manufacturers in East Asia and newly legislated U.S. foundries continue to request higher pumping speeds and tighter base pressures to handle sub-5 nm deposition steps. This distributed build-out spreads order flow across multiple geographies and vendor tiers, cushioning suppliers against localized slowdowns.

Life-Science Mass-Spectrometry Expansion

Pharmaceutical pipeline acceleration and proteomics research have elevated demand for compact, low-vibration pumps that safeguard mass-spectrometer baselines. Shimadzu and Thermo Fisher are retrofitting instruments with 60 l/s–200 l/s class turbomolecular pumps that balance throughput and desktop form factors.[1]Machiko Ishikawa, “Shimadzu Integrated Report 2024,” shimadzu.com Miniaturization trends are widening the addressable installed base far beyond central labs.

Analytical Instrumentation OEM Growth

Electron microscopy, surface analysis, and X-ray diffraction system builders are ordering bespoke pump packages that fit within tight chambers yet sustain high hydrogen pumping speeds. A dedicated pump segment for electron microscopy alone is expected to more than double to USD 275 million by 2033. The turbomolecular pump market, therefore, benefits from OEM co-development cycles that lock in long-term supply contracts.

Magnetically Levitated Design Shift

Oil-free maglev designs extend service intervals to 80,000 hours, eliminate hydrocarbon backstreaming, and cut vibration to picometer levels. Leybold’s TURBOVAC MAG 3207 iS and Edwards’ nEXT3207M typify this leap, each delivering ~3,000 l/s in a contamination-free format. Adoption curves are steepest in advanced lithography nodes and quantum-computing chambers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High maintenance & operational cost | -0.6% | Global | Short term (≤ 2 years) |

| Volatility in semiconductor equipment spending | -0.4% | East Asia, North America | Medium term (2-4 years) |

| Critical rare-earth magnet supply risk | -0.3% | Global, China-dependent supply chains | Medium term (2-4 years) |

| Net-zero regulations on pump energy intensity | -0.2% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Maintenance and Operational Costs

Conventional bearing pumps need frequent oil changes and replacements, while every turbomolecular set-up demands an auxiliary backing pump, effectively doubling capital and service outlays. Although AI-driven monitoring tools like xPump can slash unscheduled downtime, smaller research labs view these add-ons as prohibitively expensive.[2]Robotics Tomorrow, “AI/ML-Based Pump Monitoring & Predictive Maintenance System,” roboticstomorrow.com

Volatility in Semiconductor Equipment Spending

Historically abrupt fab-equipment pullbacks compress pump orders and stretch supplier working-capital cycles. Atlas Copco documented a previous contraction when display and semiconductor Cap-EX receded, emphasizing the sector’s sensitivity to macro oscillations.[3]Atlas Copco Group, “Annual Report 2024,” atlascopcogroup.com Manufacturers hedge with service revenue and diversification into analytical instrumentation to steady cash flows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Magnetically Levitation Raises the Bar

Maglev pumps generated 41.65% revenue in 2025, underscoring the turbomolecular pump market shift away from oil-lubricated models. The segment will grow at 4.95% CAGR, extending the turbomolecular pump market size advantage, as fabs and thin-film coaters specify ultra-clean operation. Magnetic levitation also lowers total lifecycle costs despite higher upfront prices. Oil-lubricated pumps remain prevalent where cost sensitivity eclipses contamination risk, particularly in legacy coating lines.

Advances in rotor dynamics, permanent-magnet strength, and integrated drive electronics curb the risk of catastrophic rotor drop while trimming vibration below 0.1 m/s². This reliability profile attracts quantum-computing OEMs that cannot tolerate particulate or hydrocarbon residue. By 2031, maglev devices are forecast to surpass 45.10% of the overall turbomolecular pump market share, further cementing their leadership within the high-yield semiconductor and research installations.

By Bearing Design: Magnetic Bearings Command Reliability

Magnetic bearings captured 55.45% of 2025 revenue alongside a 4.65% CAGR outlook, reflecting demand for a contact-free operation that eliminates wear debris. Ceramic ball bearings continue to serve corrosive gas processes because they better withstand halogen exposure. Hybrid variants—combining ceramic contact bearings at low speed with magnetic stabilization at high speed—address mid-tier budgets seeking longer life without full maglev expense.

The turbomolecular pump market size for magnetic-bearing pumps is poised to expand as fabs increase tool counts per cleanroom and extend preventive maintenance windows. Field data report mean-time-between-services above eight years, aligning with fab production intervals and minimizing production stoppages.

By Cooling Method: Air-Cooled Efficiency Widens Use Cases

Air-cooled units represented 46.55% of sales in 2025 and will match a 4.72% CAGR to 2031. Simplified installation-with no water loop-makes air cooling attractive for retrofits, mobile analytical devices, and universities. Enhanced fin geometry and higher-flow radial fans now accommodate pumping duties once restricted to water-cooled rigs, stretching the applicability envelope of the turbomolecular pump market.

Water-cooled units remain essential in high-density tool sets where ambient heat load already stresses HVAC limits. Cryo-assisted cooling is reserved for ultra-high-vacuum physics experiments, carrying a small share but commanding premium prices.

By Pumping-Speed Capacity: >3,000 l/s Segment Gains Momentum

Tools handling 200 mm–300 mm wafers, OLED coatings, and sputtering lines increasingly request >3,000 l/s pumps. This capacity tier, though smaller today, will grow at a 4.96% CAGR, outpacing mid-range segments. Manufacturers such as Edwards and Leybold released compact 3,200 l/s-class maglev models that fit into existing tool footprints, underpinning the upwards migration in the turbomolecular pump market.

Conversely, the <300 l/s micro-pump niche is growing inside point-of-care mass-spec gadgets and portable residual-gas analyzers. Pfeiffer’s 10 Neo is one exemplar, illustrating market bifurcation into very large and very small pump classes that both enlarge total addressable revenue.

By Application: Thin-Film Surge Propels Diversification

Semiconductor lines consumed 48.15% of revenues in 2025, yet thin-film & photovoltaic lines are speeding ahead with a 5.04% CAGR as solar manufacturers deploy perovskite tandem cells and low-defect metal-oxide TFT layers. The turbomolecular pump market benefits because each thin-film reactor bank demands identical vacuum purity specifications as semiconductor tools.

Electron microscopes, surface profilers, and X-ray diffractometers together present a robust secondary demand cluster. Research & development, aerospace simulation, and medical imaging collectively maintain double-digit revenue contributions, stabilizing the turbomolecular pump market against semiconductor cyclicality.

By End-user Industry: Electronics Makers Remain the Anchor

Electronics and semiconductor players held 50.40% of 2025 spending. Aggressive node shrinks continue to raise vacuum stringency, ensuring the turbomolecular pump market retains this anchor customer set. Research institutes follow-propelled by projects such as European Spallation Source and U.S. quantum-computing labs-adopting larger pumps with specialized hydrogen throughput characteristics.

Industrial coatings firms add predictable aftermarket service volume because pumps in optical-coating chambers accumulate contaminant layers faster, shortening cleaning cycles and catalyzing consumables sales.

Geography Analysis

Asia Pacific’s 45.70% slice in 2025 is tied directly to its pre-eminent semiconductor capacity and growing solar-panel exports. Regional CAGRs of 5.03% will sustain dominance, aided by continued subsidies for chip sovereignty in mainland China and fab expansions in Japan, South Korea, and Taiwan. Maglev pump penetration here exceeds 50% of new tool installs, reflecting customer preference for contamination-free chambers.

Europe ranks second, shaped by its deep research infrastructure and rapid quantum-computing investments. EU energy-efficiency directives spur pump OEMs to release lower-wattage drives and intelligent standby modes to win public-sector bids. Germany hosts several large optical-coating lines, while France and Sweden channel funding into fusion and particle-accelerator projects that specify ultra-high-vacuum pumps.

North America trails closely, benefitting from the CHIPS Act build-out and a thriving life-science cluster. Analytical instrument makers in the United States integrate increasingly compact pumps, reinforcing domestic component sourcing. Canada’s space-simulation facilities, including thermal-vacuum chambers for satellite testing, add niche demand for >3,000 l/s pumps with cryogenic trapping accessories.

Competitive Landscape

Market concentration is moderate: the top three suppliers—Edwards Vacuum, Pfeiffer Vacuum, and Ebara Corporation—collectively controlled roughly 52% of 2024 revenue. They leverage broad product portfolios, global service networks, and cohesive upgrade pathways that lock in customers over multiple tool lifecycles. Mid-tier specialists such as Agilent and Shimadzu focus on analytical instrumentation niches, providing counterweight competition.

Corporate strategies revolve around energy-efficiency breakthroughs, smart-connected monitoring, and application-specific customization. Edwards’ nEXT-series upgrade adds cloud-based diagnostics, while Pfeiffer employs edge computing for vibration analysis. Partnerships with fab OEMs provide early-stage design wins, effectively embedding pump models inside new process modules. Rare-earth sourcing concerns have also spurred vertical alliances with magnet suppliers and recycling ventures to secure NdFeB inventories.

White space is emerging in hydrogen fuel-cell stack manufacturing and fusion-energy pilots. Suppliers are engineering pumps that tolerate humid, corrosive gases and pulsed-operation cycles. Those who pivot quickest into these adjacencies will bolster resilience against semiconductor downturns and capture incremental turbomolecular pump market share.

Turbomolecular Pump Industry Leaders

Edwards Vacuum

Ebara Corporation

Pfeiffer Vacuum GmbH

Leybold GmbH

Agilent Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Leybold launched the TURBOVAC MAG 2807 iS and 3207 iS models with maglev rotors and 3,000 l/s speeds for contamination-free industrial coating and research environments.

- February 2025: Edwards Vacuum unveiled nEXT2807M and nEXT3207M, offering maintenance-free operation up to 80,000 hours and 3,200 l/s pumping, aimed at cutting energy consumption in fab tools.

- February 2025: xPump, an AI-based predictive-maintenance platform, rolled out on turbomolecular pumps with integrated EPX backing stages, helping fabs avert unplanned downtime.

- August 2024: Pfeiffer Vacuum introduced HIPACE 10 Neo, the smallest high-power turbopump for portable instrumentation.

Global Turbomolecular Pump Market Report Scope

The Turbomolecular Pumps are a significant choice for achieving high vacuum pressures. User-friendly and demanding less maintenance than diffusion pumps, these pumps offer several advantages. Their compact size eliminates the need for water cooling and swiftly attains the desired vacuum level. Furthermore, they ensure a high level of purity. Capable of operating across a rough vacuum, high vacuum, and Ultra-High Vacuum (UHV) ranges, Turbomolecular pumps maintain a consistent pumping speed of up to 4000 litres per second.

The study tracks the revenue accrued through the sale of turbomolecular pump types by various players globally. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report's scope encompasses market sizing and forecasts for the various market segments.

The turbomolecular pump market is segmented by product type (oil-lubricated, hybrid turbomolecular pumps, magnetically levitated, and air-cooled turbomolecular pumps), application (analytical instrumentation, industrial vacuum processing, research and development, semiconductor manufacturing, and others), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Oil-Lubricated |

| Hybrid |

| Magnetically Levitated |

| Dry-Bearing Ceramic |

| Magnetic Bearing |

| Ceramic Ball Bearing |

| Hybrid Bearing |

| Air-Cooled |

| Water-Cooled |

| Cryo-Cooled |

| Less than 300 l/s |

| 300 - 1 000 l/s |

| 1 000 - 3 000 l/s |

| Above 3 000 l/s |

| Analytical Instrumentation |

| Semiconductor Manufacturing |

| Industrial Vacuum Processing |

| Thin-Film and Photovoltaic |

| Research and Development |

| Aerospace and Space Simulation |

| Medical and Life Science |

| Others |

| Electronics and Semiconductor |

| Research Institutes and Academia |

| Industrial Manufacturing |

| Energy and Environment |

| Aerospace and Defense |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Middle East | Turkey |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Product Type | Oil-Lubricated | |

| Hybrid | ||

| Magnetically Levitated | ||

| Dry-Bearing Ceramic | ||

| By Bearing Design | Magnetic Bearing | |

| Ceramic Ball Bearing | ||

| Hybrid Bearing | ||

| By Cooling Method | Air-Cooled | |

| Water-Cooled | ||

| Cryo-Cooled | ||

| By Pumping-Speed capacity | Less than 300 l/s | |

| 300 - 1 000 l/s | ||

| 1 000 - 3 000 l/s | ||

| Above 3 000 l/s | ||

| By Application | Analytical Instrumentation | |

| Semiconductor Manufacturing | ||

| Industrial Vacuum Processing | ||

| Thin-Film and Photovoltaic | ||

| Research and Development | ||

| Aerospace and Space Simulation | ||

| Medical and Life Science | ||

| Others | ||

| By End-user Industry | Electronics and Semiconductor | |

| Research Institutes and Academia | ||

| Industrial Manufacturing | ||

| Energy and Environment | ||

| Aerospace and Defense | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East | Turkey | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected size of the turbomolecular pump market by 2031?

The turbomolecular pump market is forecast to reach USD 3.16 billion by 2031, growing at a 4.83% CAGR during the forecast period (2026-2031) from its USD 2.38 billion level in 2025.

Which region will grow fastest in the turbomolecular pump market?

Asia Pacific will post the highest 5.03% CAGR, driven by expanding semiconductor and photovoltaic capacity in China, Japan, South Korea, and Taiwan.

Why are magnetically levitated turbomolecular pumps gaining share?

Maglev pumps remove hydrocarbon contamination and extend maintenance intervals to about 80,000 hours while enabling higher speeds, making them ideal for advanced lithography, quantum computing, and precision thin-film processes.

How do maintenance costs affect turbomolecular pump adoption?

High maintenance and operational expenses, including the need for backing pumps and specialist service, limit uptake in price-sensitive labs, trimming the market’s near-term CAGR by an estimated 0.6 percentage points.

Which application segment is expanding most rapidly?

Thin-film and photovoltaic manufacturing is the fastest-growing application, advancing at a 5.04% CAGR through 2031 as global solar investments accelerate and perovskite tandem cell production scales.

Who are the leading turbomolecular pump vendors?

Edwards Vacuum, Pfeiffer Vacuum, and Ebara Corporation head the field, collectively holding around 51.60% of 2025 revenue and emphasizing energy-efficient, maglev, and smart-connected pump portfolios.

Page last updated on: