Magnetics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

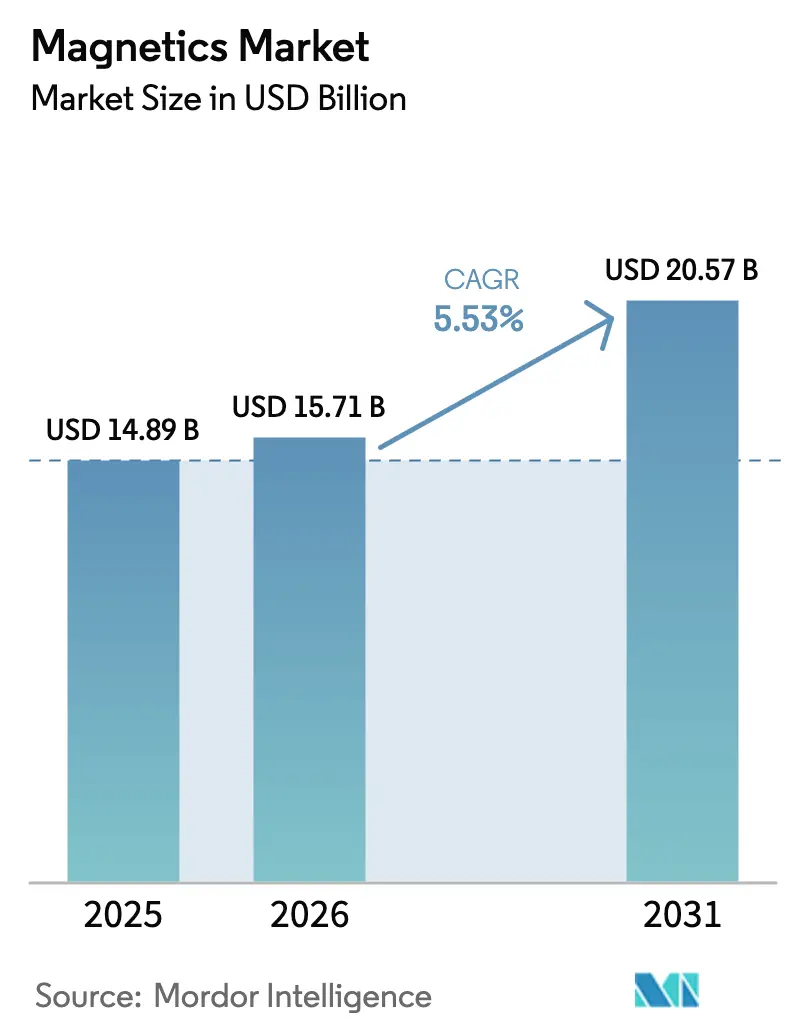

| Market Size (2026) | USD 15.71 Billion |

| Market Size (2031) | USD 20.57 Billion |

| Growth Rate (2026 - 2031) | 5.53% CAGR |

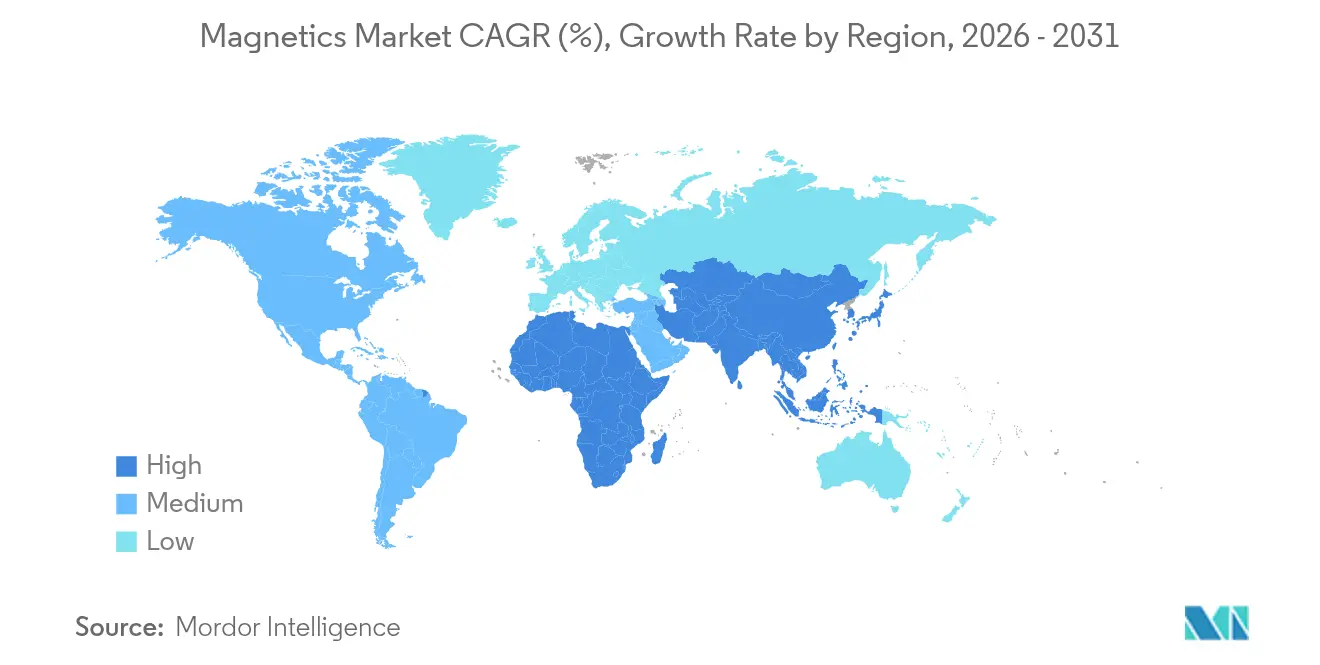

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Magnetics Market Analysis by Mordor Intelligence

Magnetics market size in 2026 is estimated at USD 15.71 billion, growing from 2025 value of USD 14.89 billion with 2031 projections showing USD 20.57 billion, growing at 5.53% CAGR over 2026-2031. Growth hinges on the shift from silicon to wide-bandgap (SiC/GaN) power electronics, which require magnetic components that operate efficiently above 100 kHz while withstanding junction temperatures beyond 200 °C. Electric-vehicle (EV) traction inverters, medium-voltage renewable-energy inverters, and 5G base-station power modules form the core demand clusters. Together, these applications accelerate adoption of nanocrystalline and amorphous alloys that deliver 50-70% lower core losses than conventional ferrites. Meanwhile, China’s 2024 rare-earth regulations tighten upstream supply and re-orient investment toward rare-earth-free magnetic designs.[1]Reuters Staff, “China Issues Rare Earth Regulations to Further Protect Domestic Supply,” Reuters, reuters.com

Key Report Takeaways

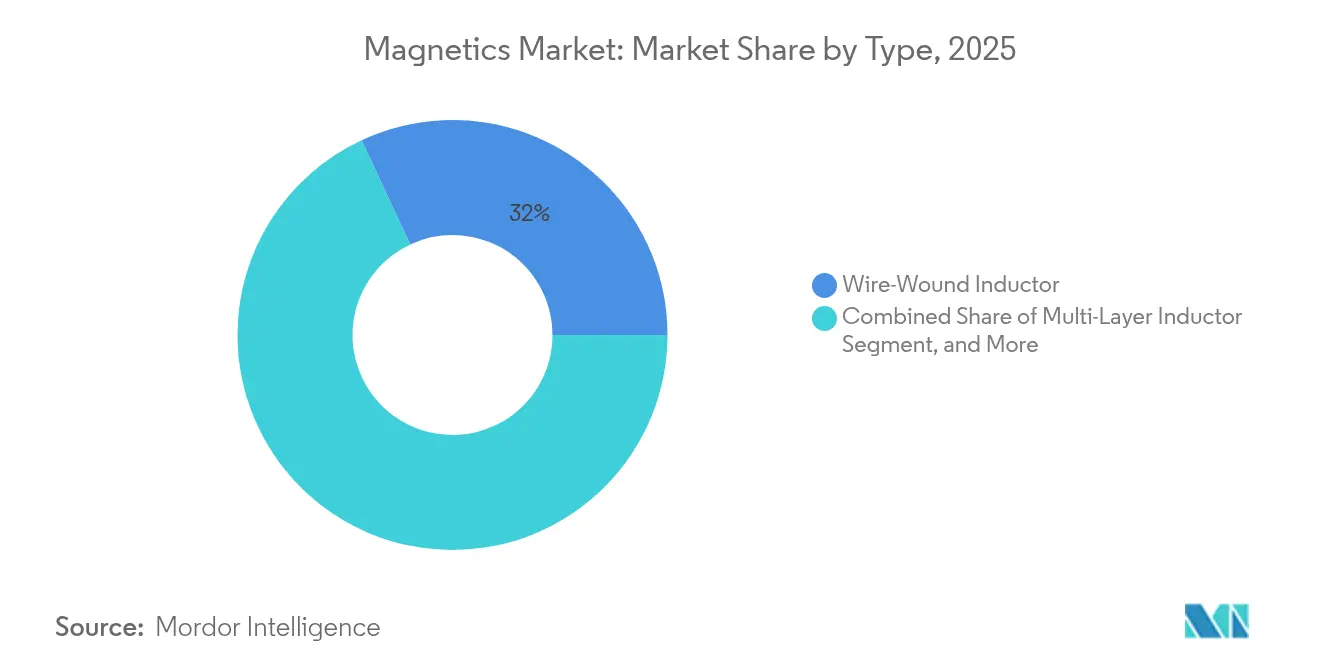

- By type, wire-wound inductors led the Magnetics market share with 31.95% revenue in 2025, whereas thin-film inductors are projected to expand at a 5.88% CAGR through 2031.

- By core material, ferrites accounted for 46.05% of the Magnetics market size in 2025, while nanocrystalline and amorphous alloys are advancing at a 7.1% CAGR to 2031.

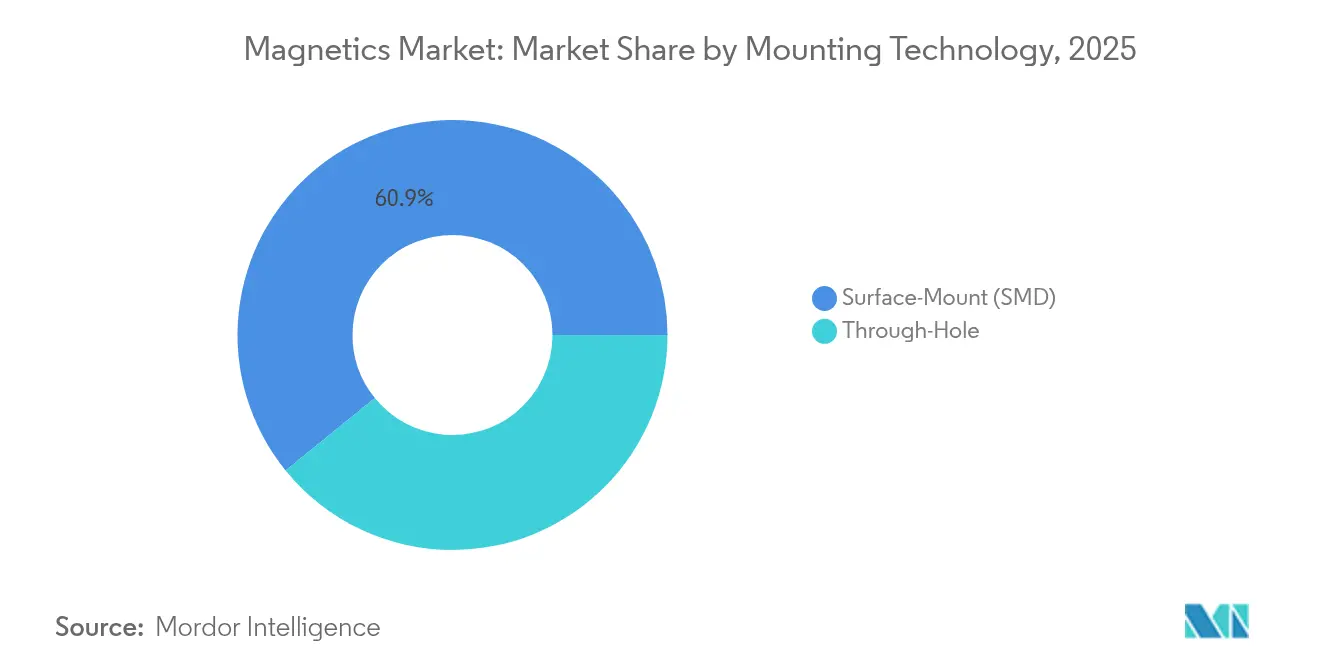

- By mounting technology, surface-mount devices (SMD) held 60.85% revenue share in 2025; through-hole products are recording a 5.62% CAGR owing to high-current EV uses.

- By end-user application, EV/HEV commanded 28.25% of the Magnetics market share in 2025; solar- and wind-power applications are growing fastest at an 7.74% CAGR.

- By geography, China accounted for 40.35% of global revenue in 2025, whereas Southeast Asia is forecast to post a 7.32% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Magnetics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in SiC/GaN Power Electronics Requiring High-Frequency Magnetics | +1.8% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| EV Traction-Inverter Adoption Driving High-Current Inductors | +2.1% | Global, led by China, EU, North America | Short term (≤ 2 years) |

| Renewable-Energy Inverter Installations Boosting Ferrite-Core Demand | +1.4% | Global, with emphasis on APAC and Europe | Medium term (2-4 years) |

| 5G Base-Station Densification Requiring RF Chokes and Filters | +0.9% | Global, accelerated in APAC and North America | Short term (≤ 2 years) |

| Miniaturization in Wearables Fueling Thin-Film Inductors | +0.6% | Global, concentrated in consumer electronics hubs | Long term (≥ 4 years) |

| China's Localization Incentives for Ferrite and Nanocrystalline Cores | +0.7% | China domestic, spillover to Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in SiC/GaN Power Electronics Requiring High-Frequency Magnetics

SiC power-device revenue reached USD 1.8 billion in 2024 and is on track to exceed USD 10 billion by 2030, with automotive channels taking 70% of demand.[2]Staff Writer, “What Is the Future for SiC in Europe?” Evertiq, evertiq.com These devices switch 5-10 times faster than silicon, forcing designers to adopt magnetic cores that maintain low losses above 100 kHz. Nanocrystalline and amorphous alloys respond with 50-70% lower core loss versus ferrites but come at premium cost.[3]Shuai Zhang et al., “Low-Loss Soft Magnetic Materials and Their Application in Power Conversion,” Materials, mdpi.com Coupled with operating junction temperatures above 200 °C, the performance gap accelerates R&D toward thermally stable, high-frequency magnetic architectures.

EV Traction-Inverter Adoption Driving High-Current Inductors

Premium EV platforms migrating from 400 V to 800 V battery packs require inductors rated beyond 160 A and 1200 V insulation. New dual-winding topologies cut DC resistance by 30% while preserving efficiency under 50 kW/L power-density targets. Three-level inverter designs have reduced harmonic losses by 75% and sliced energy use 30% in fleet trials.

Renewable-Energy Inverter Installations Boosting Ferrite-Core Demand

Medium-voltage PV string inverters operating at 1,500 VAC shrink copper and aluminum use 75% while boosting conversion efficiency. Such designs still rely on large ferrite cores that balance cost and moderate-frequency performance. Amorphous-alloy transformers further optimize efficiency under harmonic-rich PV waveforms, although cost remains an adoption hurdle.

5G Base-Station Densification Requiring RF Chokes and Filters

Dense 5G rollouts need magnetics tailored to millimeter-wave bands, where yttrium-iron-garnet thin films deliver sub-5.1 dB insertion loss.. Doped NiZn ferrites achieve quality factors above 19 at 1 MHz for current-sensing, while new automotive-grade common-mode filters hold 130 µH inductance with 30% lower capacitance to support 10BASE-T1S Ethernet.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rare-Earth (NdFeB) Price Volatility Impacting High-Performance Inductors | -1.2% | Global, particularly affecting premium applications | Short term (≤ 2 years) |

| Stricter RoHS/REACH Limits on Leaded Ferrites | -0.8% | Europe and North America, with global spillover | Medium term (2-4 years) |

| Thermal-Management Challenges in High-Current Magnetics | -0.9% | Global, concentrated in automotive and industrial | Short term (≤ 2 years) |

| Integration of Passives (IPD) Shrinking Discrete Inductor Sockets | -0.7% | Global, led by consumer electronics and mobile | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rare-Earth (NdFeB) Price Volatility Impacting High-Performance Inductors

Neodymium magnet demand could triple by 2035, whereas capacity may only double, stoking sustained price swings.[4]James Temple, “How New Magnets Could Accelerate Climate Action,” MIT Technology Review, technologyreview.com China’s export controls add near-term volatility, forcing OEMs to hedge via recycling and alternative alloys. Iron-nitride magnets and AI-generated formulations show promise but need high-current validation.

Stricter RoHS/REACH Limits on Leaded Ferrites

The EU is reviewing lead exemptions for high-melting-point solders, creating phased bans through 2027 that pressure magnetics makers to qualify lead-free ferrites. Lead-free EMI filters have passed AEC-Q101, proving feasible in select automotive contexts. However, high-temperature applications above 200 °C still lean on leaded compositions, driving transition costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Wire-Wound Dominance Faces Thin-Film Disruption

Wire-wound inductors captured 31.95% of the Magnetics market in 2025, retaining primacy in high-current EV, industrial, and renewable-energy converters. Their simple geometry combines low cost and thermal robustness. Yet thin-film inductors are slated to grow 5.88% annually, propelled by demand for tiny footprints in smartphones, wearables, and 5G RF front-ends. Multi-layer ceramic inductors fill a mid-range niche for moderate-current, size-constrained designs, particularly in automotive ADAS and telecom base-stations. EMI filters and current-sense transformers also rise on tougher electromagnetic-compatibility standards, aided by novel dual-winding structures that cut DC resistance without inflating size.

Thin-film manufacturing improvements, such as 3D roll-up architectures, now deliver inductance densities 100× higher than legacy wire-wound equivalents, narrowing the cost-performance gap. As advanced deposition reaches scale, price erosion will likely accelerate adoption in consumer devices. In parallel, RF/power transformers optimized for SiC/GaN inverters move design goals toward switching beyond 100 kHz while guaranteeing thermal stability at 200 °C junction conditions. Current-sense transformers capable of measuring up to 40 A at 1 MHz support real-time protection in PV and EV chargers.

By Core Material: Ferrite Leadership Challenged by Advanced Alloys

Ferrite accounted for 46.05% of Magnetics market revenue in 2025, favored for cost and satisfactory performance below 1 MHz. Nanocrystalline and amorphous alloys, however, advance at 7.1% CAGR, driven by SiC-based converters that demand minimal loss at 100 kHz-1 MHz switching. Powdered-iron cores serve high-flux, temperature-stable EV traction inverters that experience >1,000 thermal cycles annually. Permalloy variants handle precision sensors requiring low coercivity and high permeability; polymer-coated composites further suppress eddy currents.

Soft-magnetic composites, featuring isotropic flux paths and fewer eddy currents, enter the conversation for high-frequency motors and distribution transformers. Advanced Fe-Si composites now reach permeability above 126 at 10 kHz while keeping mechanical strength. Vortex-based composites sustain stability up to 1 GHz, opening doors for ultra-high-frequency filters.

By Mounting Technology: SMD Prevalence Drives Automation

Surface-mount devices held 60.85% of the Magnetics market in 2025 owing to compatibility with automated reflow lines and shrinking PCB real estate. Advanced SMD packages incorporate copper heat spreaders and thermal vias, allowing dissipation above 10 W in sub-10 mm² footprints without derating. Through-hole magnetics persist in EV chargers and motor drives, where mechanical ruggedness supersedes miniaturization, supporting 5.62% CAGR through 2031. Hybrid approaches mix SMD efficiency with solder-pin anchoring, enabling automated placement and high vibration tolerance.

SMD adoption grows rapidly in high-speed telecom gear that benefits from shorter interconnects and reduced parasitics. Conversely, traction inverters and rail converters continue favoring through-hole toroidal inductors for 800 VDC bus coupling. The magnetics industry is thereby engineering novel lead-frame-on-package concepts that deliver SMD compatibility but withstand 1,000+ thermal cycles at 125 °C ambient.

By End-User Application: EV Leadership Accelerates Renewable Growth

EV/HEV applications captured 28.25% of Magnetics market revenue in 2025, anchored by traction inverters, onboard chargers, and DC-DC converters. Continental’s rotor-temperature sensor lowers tolerance from 15 °C to 3 °C, enabling magnet mass reduction without torque loss. Renewable-energy inverters represent the fastest-growing application at 7.74% CAGR, fueled by medium-voltage PV strings and wind-turbine converters that need large ferrite cores and amorphous transformers for harmonic-rich environments.

Industrial motor and UPS systems adopt synchronous-reluctance motors that meet IE4 efficiency without rare-earth magnets. Consumer electronics reinforce thin-film inductor demand, integrating wireless-charging coils and PMIC inductors under 1 mm². Medical, aerospace, and telecom infrastructure round out demand, each imposing unique reliability and qualification thresholds that drive bespoke magnetic designs.

Geography Analysis

Asia-Pacific anchored the Magnetics market with China alone generating 40.35% of global revenue in 2025. Government caps on rare-earth mining and fresh export licence mandates steer value capture toward domestic manufacturers while nudging foreign OEMs to localize production. Southeast Asia surfaces as the fastest-growing sub-region at 7.32% CAGR, driven by Thai, Vietnamese, and Malaysian initiatives that entice foreign direct investment for magnetics plants aimed at EV and renewable-energy exports. Japan extends leadership in high-precision alloys, while India’s Premo-Delta joint venture adds ferrite capacity for regional supply resilience.

North America and Europe accounted for roughly 34.78% of 2025 demand, both leveraging regulatory pushes for clean transport and grid upgrades. The Biden administration’s incentives for EV and advanced manufacturing boost domestic sourcing, evidenced by a USD 20 million magnet-recycling plant breaking ground in New York. Europe tightens RoHS/REACH frameworks, spurring R&D into lead-free ferrites and boosting recycled magnet supplies via French initiatives such as MagREEsource.

South America, the Middle East, and Africa collectively held below 14.87% share in 2025. Brazil leads South American consumption through industrial drives and emerging PV projects. The Gulf Cooperation Council invests in 1.5 kV solar farms that require large ferrite transformers, while South Africa upgrades mining electrification, increasing demand for rugged magnetics. As local assembly capabilities expand, the Magnetics market may see regional component lines emerge to mitigate freight costs and currency swings.

Competitive Landscape

The Magnetics market remains moderately fragmented, with the top five suppliers holding well under 40% combined revenue. Established leaders-TDK Corp., Vishay Intertechnology, Würth Elektronik, and Murata-anchor high-reliability and automotive portfolios. Their edge stems from proprietary materials science, vertical integration, and global application-engineering teams. Mid-tier competitors in China and Southeast Asia undercut prices in commodity SMD inductors and ferrite cores, adding capacity as rare-earth regulations favor domestic producers.

Strategic themes include (1) materials innovation, such as rare-earth-free iron-nitride magnets and vortex-based soft-magnetic composites; (2) sustainability, highlighted by vertical integration of recycling flows; and (3) design-for-system solutions, combining magnetics, capacitors, and thermal substrates in co-packaged modules. Consolidation gains pace: Permag merged three Chinese magnet players in June 2025 to pool R&D and purchasing heft . Bel Fuse’s USD 400 million buy of Enercon expands its Signal Transformer unit, reflecting broader appetite for scale in power-magnetics niches.

Progress in AI-assisted material discovery and additive-manufacturing windings widens competitive moats for innovators. However, tight automotive qualification cycles and supply-chain traceability requirements present entry barriers that continue to shelter incumbents in safety-critical segments.

Magnetics Industry Leaders

TDK Corporation

Yageo Corporation

Meritek Electronics Corporation

AVX Corporation (Kyocera Group)

Vishay Intertechnology

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Three rare-earth magnet producers merged under the name Permag, forming a larger entity focused on permanent-magnet innovation.

- June 2025: Premo and Delta created a soft-ferrite joint venture in India to widen Asian supply and cut logistical exposure.

- April 2025: Cyclic Materials invested over USD 20 million in its first US magnet-recycling plant to heighten supply resilience.

- April 2025: China began export-licence controls on medium-to-heavy rare-earth elements such as dysprosium and terbium.

- January 2025: Arnold Magnetic Technologies opened a new Thailand facility to serve regional demand.

Global Magnetics Market Report Scope

Magnetic components are widely adopted in both advanced industrial and common household appliances, ranging from refrigerators and televisions to telecommunication devices. Magnetics plays a crucial role in cars, monitoring voltage in power supplies for dashboard displays, interior and exterior lighting, climate control, and other systems. These components are used in cell phones, computers, communication systems, and other electronic products. These components help in optimizing power efficiency.

The magnetics market is segmented by type (wire-wound inductor, multi-layer inductor, thin film inductor, ferrite cores and EMC components, EMI filters, RF/power transformers, current sense, and other transformers), end-user application (photovoltaics and wind, EV/HEV, industrial [Motors/UPS], rail/transportation, consumer electronics, and other end-user applications), geography (China, Japan, United States, Taiwan, Southeast Asia, South Korea, Europe, Rest of the World). The report offers market forecasts and size in value (USD) for all the above segments.

| Wire-Wound Inductor |

| Multi-Layer Inductor |

| Thin-Film Inductor |

| Ferrite Cores and EMC Components |

| EMI Filters |

| RF/Power Transformers |

| Current-Sense and Other Transformers |

| Ferrite |

| Powdered Iron |

| Nanocrystalline/Amorphous |

| Permalloy and Other Alloys |

| Surface-Mount (SMD) |

| Through-Hole |

| Photovoltaics and Wind |

| EV/HEV |

| Industrial (Motors/UPS) |

| Rail/Transportation |

| Consumer Electronics |

| Other End-User Applications |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Rest of South America | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Type | Wire-Wound Inductor | ||

| Multi-Layer Inductor | |||

| Thin-Film Inductor | |||

| Ferrite Cores and EMC Components | |||

| EMI Filters | |||

| RF/Power Transformers | |||

| Current-Sense and Other Transformers | |||

| By Core Material | Ferrite | ||

| Powdered Iron | |||

| Nanocrystalline/Amorphous | |||

| Permalloy and Other Alloys | |||

| By Mounting Technology | Surface-Mount (SMD) | ||

| Through-Hole | |||

| By End-User Application | Photovoltaics and Wind | ||

| EV/HEV | |||

| Industrial (Motors/UPS) | |||

| Rail/Transportation | |||

| Consumer Electronics | |||

| Other End-User Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current Magnetics market size and expected growth?

The Magnetics market size is USD 15.71 billion in 2026 and is projected to reach USD 20.57 billion by 2031 at a 5.53% CAGR.

Which application segment leads demand?

EV/HEV traction inverters lead with 28.25% Magnetics market share in 2025, driven by 800 V battery architectures that push current and voltage ratings higher.

Why are nanocrystalline and amorphous alloys gaining traction?

They offer 50–70% lower core loss than ferrites at ≥100 kHz, making them ideal for SiC/GaN power electronics that dominate next-generation inverters.

How will China’s rare-earth policies influence supply?

Annual mining caps and export licences enacted in 2024–2025 tighten global supply, incentivizing recycling and rare-earth-free magnetic materials

What technology trend most threatens discrete inductors in mobile devices?

Integrated passive devices can combine inductors, capacitors, and resistors on a single substrate, reducing board space up to 80% and shrinking discrete sockets.

Which region will grow fastest through 2031?

Southeast Asia will grow at a 7.32% CAGR as companies diversify production away from China and invest in local EV and renewable-energy supply chains

Page last updated on: