Relay Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.64 Billion |

| Market Size (2031) | USD 12.67 Billion |

| Growth Rate (2026 - 2031) | 5.63% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia |

| Market Concentration | Medium |

Major Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Relay Market Analysis by Mordor Intelligence

relay market size market size in 2026 is estimated at USD 9.64 billion, growing from 2025 value of USD 9.13 billion with 2031 projections showing USD 12.67 billion, growing at 5.63% CAGR over 2026-2031. Its current expansion reflects resilient demand for reliable switching solutions across electrification, renewable integration, and industrial automation. Solid-state devices are the fastest-growing relay class, yet electromechanical products continue to dominate high-current and harsh-environment use cases. Microgrid rollouts across Asia and Africa, rapid electric vehicle (EV) adoption, and the shift toward IEC-61850 digital substations in Europe and North America are reshaping sourcing strategies, technology roadmaps, and revenue pools within the relay market. Vendors able to balance cost-competitive electromechanical lines with advanced solid-state portfolios are best positioned to tap mounting opportunities in 800 V EV platforms, 5G radio units, and smart HVAC systems.

Key Report Takeaways

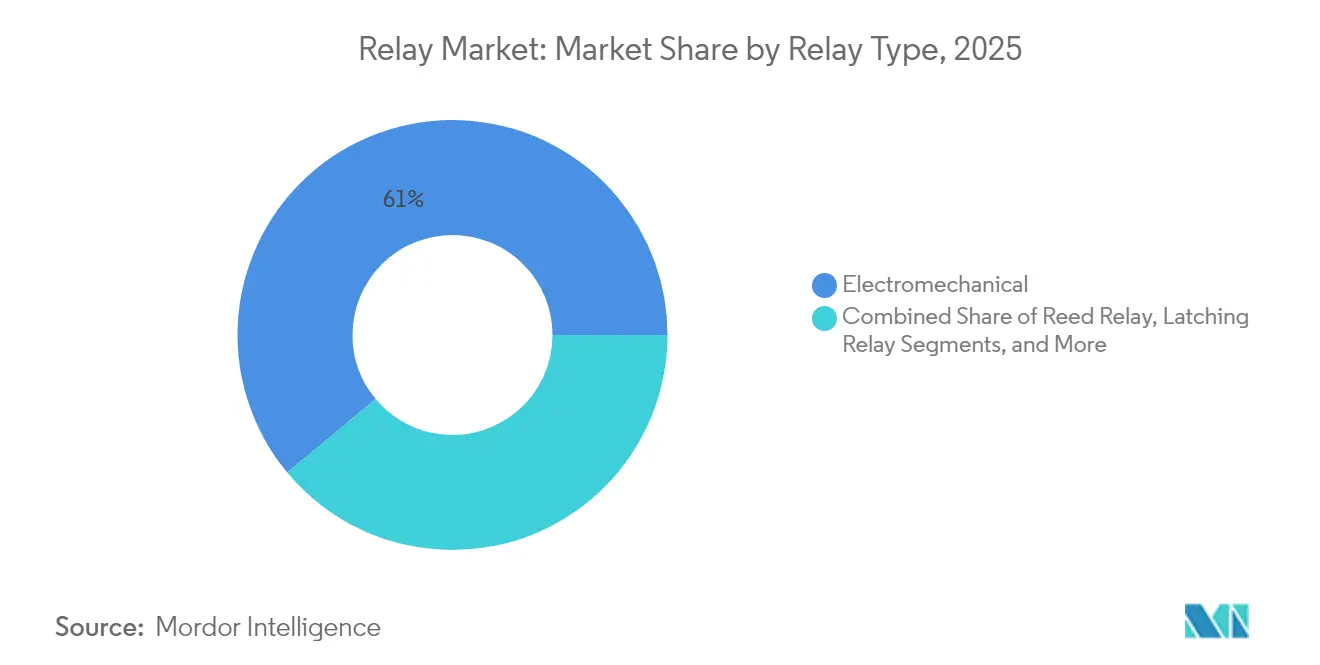

- By relay type, electromechanical devices led with 61.05% of relay market share in 2025, whereas solid-state relays are forecast to expand at a 6.82% CAGR through 2031.

- By voltage rating, low-voltage (<100 V) devices accounted for 44.62% of the relay market size in 2025; high-voltage (>1 kV) solutions are projected to rise at a 6.12% CAGR.

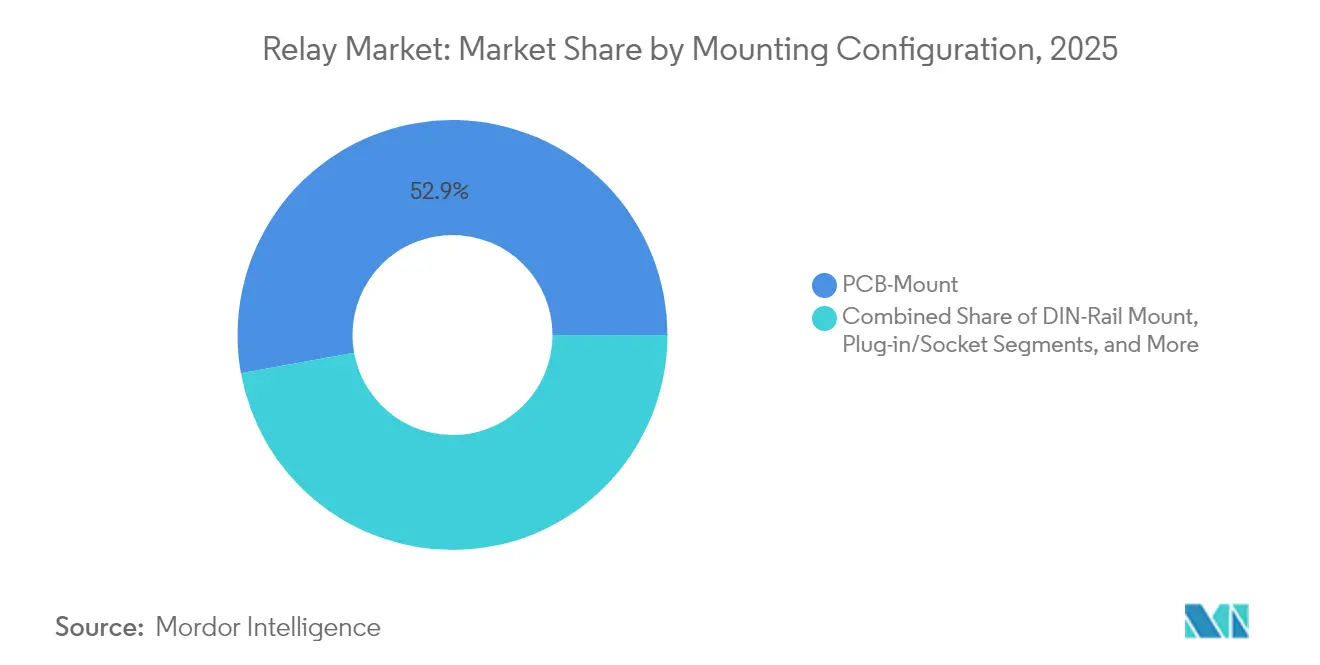

- By mounting configuration, PCB-mount products captured 52.85% of relay market share in 2025; DIN-rail units record the highest growth outlook at 5.73% CAGR.

- By end-user industry, automotive and e-mobility dominated with 28.55% revenue contribution in 2025, while energy and power applications will grow at 7.78% CAGR.

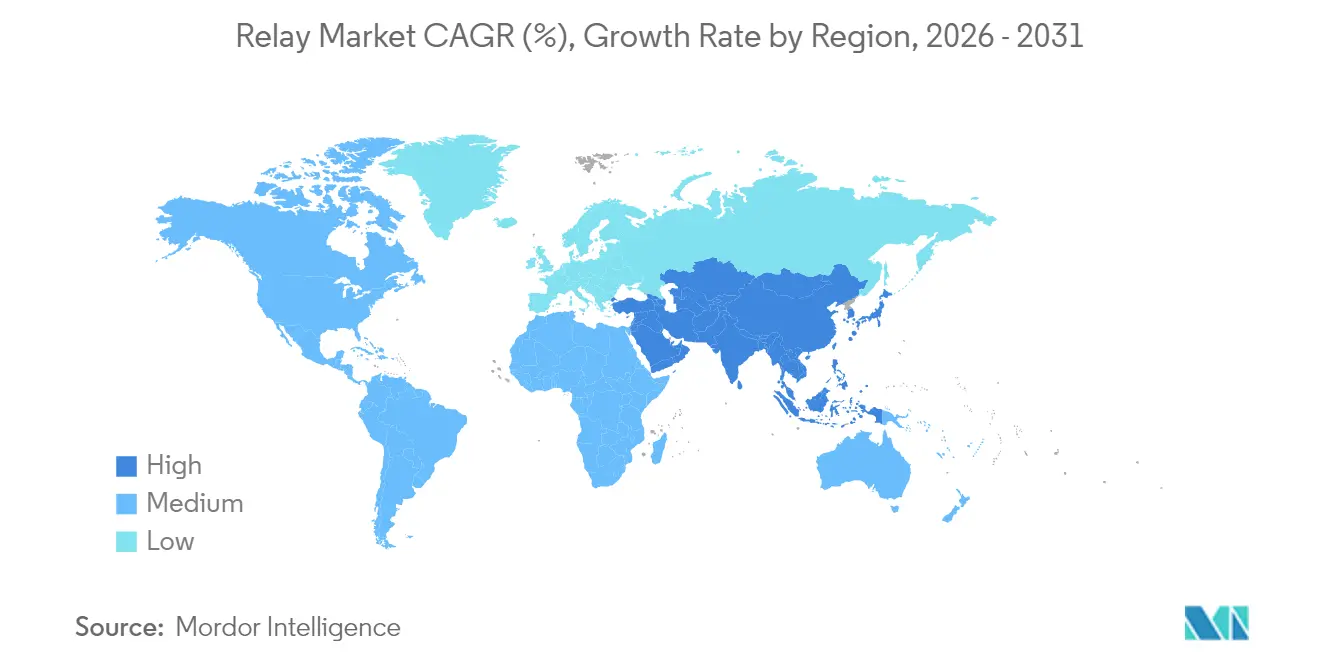

- By geography, Asia held a 43.78% relay market share in 2025; the Middle East is poised for 5.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Relay Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Decentralized renewable microgrids accelerating demand for protective relays | +1.20% | Asia, Africa | Medium term (2–4 years) |

| Surge in on-board DC power electronics in EVs requiring high-voltage solid-state relays | +1.80% | Global (China, Europe, North America) | Short term (≤ 2 years) |

| Retrofitting of aging T&D infrastructure with IEC-61850 digital substations | +0.90% | Europe, North America | Long term (≥ 4 years) |

| Proliferation of compact 5G radio units driving reed and PhotoMOS relays | +0.70% | Global, led by Asia-Pacific | Short term (≤ 2 years) |

| Safety-critical redundancy mandates in autonomous industrial robots boosting latching PCB relays | +0.50% | North America, Europe, Japan | Medium term (2–4 years) |

| Energy-efficient building codes in the Middle East stimulating smart HVAC relays with IoT connectivity | +0.30% | Middle East, expanding into APAC | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Decentralized Renewable Microgrids Accelerating Demand for Protective Relays in Medium-Voltage Distribution

Rural electrification programs across Asia and Africa are pivoting toward hybrid solar-battery microgrids. Bidirectional power flows, variable fault currents, and frequent islanding events make adaptive directional overcurrent relays indispensable for safe, reliable distribution. Grid operators increasingly favor devices with IEC 61850 communication and synchrophasor support, ensuring seamless coordination among multiple distributed generation sources while reducing blackout risk.[1]MDPI, “Optimal Microgrid Protection Coordination for Directional Overcurrent Relays,” mdpi.com Lower component costs and multiyear government subsidies further strengthen market pull, positioning protective relays as a core element of emerging-market energy access strategies.

Surge in On-Board DC Power Electronics in EVs Requiring High-Voltage Solid-State Relays

EV platforms are shifting from 400 V to 800 V architectures to enable faster charging and lighter cabling. High-voltage solid-state relays capable of 250 A continuous current, such as TE Connectivity’s EVC 250-800, now underpin battery disconnect, pre-charge, and fast-charge circuits.[2]TE Connectivity, “EVC 250-800 Main Contactor,” te.com Hydrogen-gas arc suppression and ceramic insulation, pioneered by Panasonic, support compact footprints inside crowded power-electronics bays. As premium EV volumes rise, the relay market rapidly migrates toward low-loss, arc-free switching solutions that can withstand elevated ambient temperatures, vibration, and repetitive load cycling.

Retrofitting of Aging T&D Infrastructure with IEC-61850 Digital Substations

More than 79,000 North American substations exceed 40 years of service life, prompting utilities to adopt digital secondary systems to curb maintenance costs and accommodate distributed renewables. IEC 61850-compliant protection relays replace hard-wired copper with Ethernet-based GOOSE messaging, cutting installation wiring by up to 40% and enabling remote firmware updates. European utilities lead full digital rollouts, deploying non-conventional instrument transformers that feed sampled values directly into multifunction relays for precise fault isolation and predictive asset managemen.

Proliferation of Compact 5G Radio Units Driving Reed and PhotoMOS Relays for RF Switching

Massive multiple-input multiple-output (MIMO) radios and small-cell deployments squeeze board area while raising frequency demands. Reed relays and PhotoMOS devices deliver sub-0.2 dB insertion loss, wide-bandwidth isolation, and micro-second switching essential to beamforming modules in 5G and emerging 6G nodes. Their optical isolation also supports smart meters, battery monitoring, and railway communications, sustaining outsized growth in telecom-driven relay market niches.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid price erosion in commodity electromechanical relays undermines vendor margins | -0.80% | Global, especially Asia-Pacific | Short term (≤ 2 years) |

| Solid-state relay thermal management issues above 60 A limit heavy-duty penetration | -0.60% | Global industrial and automotive segments | Medium term (2–4 years) |

| Counterfeit low-quality relays from informal Asian suppliers introduce reliability risks | -0.40% | Global supply chains | Short term (≤ 2 years) |

| Substitution threat from power semiconductor switches (MOSFET/IGBT modules) | -0.70% | Global, high-performance applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Price Erosion in Commodity Electromechanical Relays Undermines Vendor Margins

Chinese manufacturers have intensified price-based competition, lowering average selling prices in standard relay categories by double-digit percentages since 2024.[3]ARC Advisory Group, “China’s IA Market Enters New Phase of Price-Driven Rivalry,” arcweb.com Global distributors respond by demanding shorter lead times and value-added testing to differentiate quality. Margins narrow, compelling incumbents to redeploy capacity toward higher-value designs-HV contactors, smart safety relays, and IoT-enabled modules-to preserve profitability within the relay market.

Solid-State Relay Thermal Management Issues Above 60 A Limiting Heavy-Duty Penetration

Junction temperatures approaching 150 °C and solder-joint fatigue restrict solid-state devices in high-current industrial drives and commercial EV chargers. Costly heat sinks and liquid-cooling plates erase size and efficiency gains versus electromechanical counterparts.[4]Intelligent Power Today, “SSR Lifetime and Degradation Mechanisms,” intelligent-power-today.com Suppliers explore wide-band-gap semiconductors and novel package materials, yet mainstream 100 A-plus adoption remains constrained through the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Relay Type: Solid-State Innovation Challenges Electromechanical Dominance

Electromechanical devices held 61.05% of relay market share in 2025, benefiting from proven durability, arc-handling capacity, and competitive cost within industrial motor control and grid protection. Designers value the class’s full galvanic isolation and tolerance for 2 kA surge currents, traits that keep demand steady in harsh mining, marine, and rail traction settings where thermal limits rule out semiconductor switches. At the same time, the fastest-growing slice of the relay market size is solid-state, advancing 6.82% CAGR as automotive OEMs migrate to 800 V battery systems and telecom operators densify 5 G nodes that require low-leakage, micro-second switching.

Solid-state relays ride the cost curve of SiC and GaN devices, offering arc-free longevity that appeals to EV battery disconnect units, photovoltaic rapid-shutdown boxes, and medical imaging where contact bounce is unacceptable. Hybrid formats merge MOSFET speed with mechanical isolation to blunt substitution threats from pure semiconductor modules, although adoption remains modest due to higher bill-of-materials cost and validation overheads. Electromechanical vendors respond with latching coils and low-resistance alloys that shave 20 mΩ from contact paths, while niche players such as KG Technologies expand the relay industry patent pool for smart-meter latching designs that cut standby loss to near-zero.

By Voltage Rating: High-Voltage Applications Drive Innovation

Low-voltage designs below 100 V captured 44.62% of relay market share in 2025 on the back of standardized footprints inside consumer electronics, wearables, and building automation. Growth is steady but muted, with margin pressure from commodity Asian suppliers spurring incumbents to automate SMT placement and adopt composite plastics that shrink package height by 15%. Medium-voltage relays between 100 V and 1 kV remain workhorses of motor control centers and photovoltaic string combiners, where ruggedized contacts and varnish-sealed coils withstand daily temperature swings on factory floors and desert solar farms.

Above 1 kV, demand accelerates at a 6.12% CAGR as ultra-fast EV chargers, offshore wind converters, and battery-energy-storage inverters standardize 1 ,500 V DC buses. Vacuum and gas-filled architectures dominate this relay market segment, delivering arc-quenching performance that mechanical air gaps cannot match. Mitsubishi Electric’s 3.3 kV HVIGBT modules underscore the downstream pull for companion relays with expanded creepage distances, polymer insulators, and integrated temperature sensors. Suppliers unable to certify products to IEC 62955 and UL 1973 face dwindling share as system integrators lock in qualified high-voltage partners.

By Mounting Configuration: PCB Integration Drives Miniaturization

PCB-mount products commanded 52.85% relay market share in 2025, propelled by automated pick-and-place lines that lower assembly labor and reflow-solder profiles. The relay market size here grows in sync with automotive electronic control units, data-center power distribution, and satellite communication payloads that prioritize mass, vibration, and board real estate. OMRON’s G9KA series exemplifies the shift, handling 800 V/200 A yet standing one-third the height of legacy contactors while posting 0.2 mΩ contact resistance.

DIN-rail formats expand fastest at 5.73% CAGR, favored in industrial control cabinets and commercial HVAC panels where hot-swap serviceability trumps PCB density. Tool-free spring clamps and NFC-programmable timers shorten commissioning cycles, critical for contractors racing to meet energy-efficiency codes. Panel-mount and plug-in sockets persist in backup-power and rail-signaling niches where field crews demand rapid relay replacement without full board removal, but their share drifts lower as modular IO slices and distributed I/O drops spread throughout smart factories.

By End-User Industry: Automotive Leadership Faces Renewable Energy Challenge

Automotive and e-mobility applications generated 28.55% of relay market revenue in 2025, spanning traction inverters, battery disconnect units, DC-fast chargers, and ADAS sensor fusion boxes that rely on fail-safe latching logic. ISO 26262 and ASIL-D mandates continue to add redundant paths, expanding bill-of-materials counts even as EV makers trim component footprints. Tier-1s now co-design solid-state contactors with relay suppliers to withstand 2,500 V transients and -40 °C cold-crank events, reinforcing the relay market’s pivotal place in vehicle electrification.

Energy and power users, especially renewables, represent the fastest-moving slice at 7.78% CAGR through 2031 as utilities retrofit feeders with microgrid-ready protective devices and EPCs build 500 MW hybrid solar-storage parks. Grid codes require fast fault-clearing down to a 4 ms window, steering purchases toward multifunction digital relays that merge distance, overcurrent, and synchrophasor reporting. Industrial automation, telecom, and building management remain steady consumers, while aerospace and defense secure premium-price hermetic units validated for radiation and wide-temperature operation.

Geography Analysis

Asia commanded 43.78% of relay market share in 2025, anchored by China’s component fabs, Japan’s high-voltage innovation, and South Korea’s telecom-grade RF assembly lines. Regional OEMs pair vertical integration with government incentives that trim duty and logistics cost, enabling aggressive price points that reshape global sourcing patterns. Southeast Asian economies add a second engine as contract manufacturers relocate to Vietnam, Thailand, and Malaysia to diversify supply chains.

North America focuses investment on grid modernization and safety-critical robotics. Federal infrastructure packages channel capital into IEC 61850 protection upgrades, digital substation retrofits, and autonomous warehouse fleets that depend on latching PCB relays. Aerospace primes drive demand for hermetically sealed, radiation-tolerant units, while Silicon Valley cloud operators procure thousands of low-on-resistance PCB devices for data-center busbars.

Europe blends decarbonization policy with mature industrial automation ecosystems, rewarding suppliers that certify products for CE marking, RoHS, and functional-safety standards. Utilities deploy non-conventional instrument transformers feeding sampled-value streams into digital relays, shrinking copper runs and enabling remote firmware updates. The Middle East records the fastest growth at 5.95% CAGR as smart-city programs and stringent building codes embed IoT-ready HVAC relays across commercial towers. Africa, though smaller in absolute terms, emerges as a frontier for medium-voltage protective relays tied to solar-battery microgrid rollouts that electrify rural communities.

Competitive Landscape

The competitive field shows moderate concentration: the top five brands control roughly 45% of global relay market revenue. TE Connectivity, Omron, Panasonic, Siemens, and Schneider Electric leverage global distribution, application engineering, and vertically integrated coil, spring, and contact fabrication to defend incumbency. TE Connectivity extends reach with the EVC 250-800 high-voltage EV contactor, while Panasonic widens PhotoMOS portfolios targeting 5 G radios and smart meters.

Mid-tier specialists such as Song Chuan, American Zettler, and Hongfa exploit focused product lines and cost advantages to win commodity contracts and region-specific tenders. Strategic acquisitions continue: Wabtec’s USD 110 million Fanox deal brings rail-qualified relays into its transit suite, and Schneider’s minority stake in a GaN-device start-up positions it for hybrid relay modules. Technology disruption looms from Infineon and Toshiba, which tout GaN and SiC switches that slash energy loss by up to 60% and shrink system size 40%, tempting OEMs to bypass traditional contactors in high-frequency applications.

Suppliers counter by embedding diagnostics, NFC configuration, and predictive-maintenance hooks into premium lines, creating software-rich ecosystems that raise switching reliability metrics. Vertical integration of silver-nickel contact plating, ceramic sealing, and high-speed coil winding protects margins against commodity price erosion, while joint R&D with vehicle, inverter, and telecom customers locks in design wins through 2030.

Relay Industry Leaders

TE Connectivity

American Zettler

Churod Electronics

Omron

Panasonic

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Nexans and SNCF Réseau deployed the first superconducting fault-current limiter for rail, enhancing network resilience.

- May 2025: Siemens released the SIRIUS 3RC7 intelligent link module, enabling AI-based fault detection across industrial controls

- April 2025: Mitsubishi Electric began sampling 3.3 kV XB-series HVIGBT modules with 15% lower switching loss and extended SOA.

- March 2025: SES partnered with Lynk Global on MEO-Relay services to route direct-to-device traffic.

- March 2025: Renesas, CG Power, and Stars Microelectronics committed INR 7,600 crores to a high-volume OSAT plant in India.

- February 2025: Infineon’s CoolGaN power transistors cut heat-sink mass by 50% in SounDigital’s 1,500 W amplifier.

Global Relay Market Report Scope

A relay acts as a switch and is used to switch connections between different circuits. Electrical relays are generally utilized for switching radio frequencies, signals, high current circuits when utilizing a lower current circuit, and loads such as a motor, resistive, inductive, lamp, and capacitive applications. The relays are helpful when an existing circuit or in-line switch cannot manage the needed current. Among product types, electromechanical and solid state relays are the two major types of relays that have been considered in the scope of this market report.

The end-user applications considered part of the study include aerospace, defense, military, automotive, communications, energy and power, industrial, and others in various geographies. Also, the study includes the impact of COVID-19 on the market.

Relay Market is segmented by product type (electromechanical, solid state), by end-user application (aerospace, defense and military, automotive, communications, energy and power, industrial), and geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa). The report offers market forecasts and size in value (USD) for all the above segments.

| Electromechanical |

| Reed Relay |

| Latching Relay |

| Solid-State Relay (SSR) |

| PhotoMOS/Optically-Isolated |

| IGBT/MOSFET-Based |

| Hybrid Relay |

| Low Voltage (Less than 100 V) |

| Medium Voltage (100-1000 V) |

| High Voltage (Above 1000 V) |

| PCB-Mount |

| DIN-Rail Mount |

| Plug-in/Socket |

| Panel/Chassis Mount |

| Automotive and E-Mobility |

| Energy and Power (T&D, Renewables) |

| Industrial Automation and Robotics |

| Telecommunications and 5G Infrastructure |

| Aerospace and Defense |

| Consumer Electronics and Appliances |

| Building Automation/HVAC |

| Rail and Mass Transit |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Rest of South America | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Relay Type | Electromechanical | ||

| Reed Relay | |||

| Latching Relay | |||

| Solid-State Relay (SSR) | |||

| PhotoMOS/Optically-Isolated | |||

| IGBT/MOSFET-Based | |||

| Hybrid Relay | |||

| By Voltage Rating | Low Voltage (Less than 100 V) | ||

| Medium Voltage (100-1000 V) | |||

| High Voltage (Above 1000 V) | |||

| By Mounting Configuration | PCB-Mount | ||

| DIN-Rail Mount | |||

| Plug-in/Socket | |||

| Panel/Chassis Mount | |||

| By End-user Industry | Automotive and E-Mobility | ||

| Energy and Power (T&D, Renewables) | |||

| Industrial Automation and Robotics | |||

| Telecommunications and 5G Infrastructure | |||

| Aerospace and Defense | |||

| Consumer Electronics and Appliances | |||

| Building Automation/HVAC | |||

| Rail and Mass Transit | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the relay market and its growth outlook?

The relay market is valued at USD 9.64 billion in 2026 and is projected to reach USD 12.67 billion by 2031, growing at a 5.63% CAGR.

Which relay type is expanding fastest through 2031?

Solid-state relays lead future growth with a 6.82% CAGR thanks to rising demand in EV powertrains and 5G telecom hardware.

Why are high-voltage relays gaining attention?

Ultra-fast EV chargers, 800 V vehicle architectures, and renewable energy inverters require reliable switching above 1 kV, driving a 6.12% CAGR in high-voltage relay shipments

What factors make Asia the leading relay market region?

Asia benefits from integrated manufacturing clusters, large domestic EV and telecom sectors, and competitive component pricing, delivering a 43.78% revenue share in 2025.

How are digital substations influencing relay demand?

Utilities in Europe and North America are replacing legacy devices with IEC 61850 multifunction relays that reduce wiring, enhance interoperability, and enable predictive maintenance.

Which restraint most threatens relay vendors’ margins in the near term?

Rapid price erosion in commodity electromechanical products, driven by aggressive Asian competitors, is eroding margins and steering incumbents toward higher-value niches.

Page last updated on: