Stepper Motor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

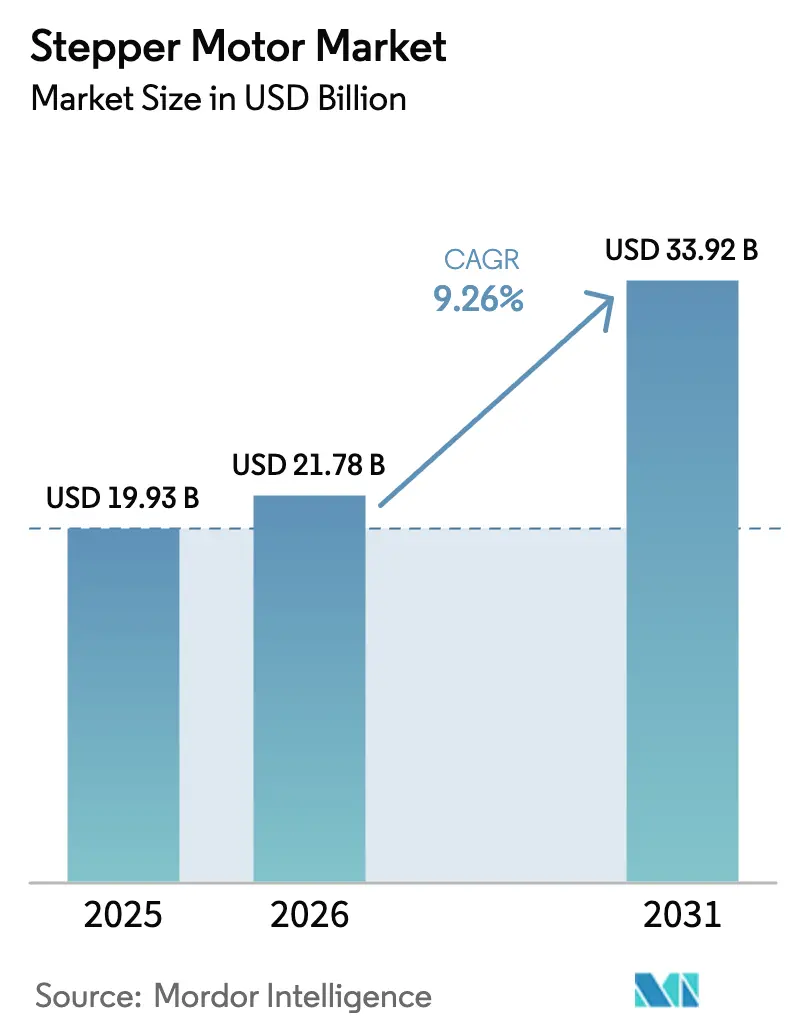

| Market Size (2026) | USD 21.78 Billion |

| Market Size (2031) | USD 33.92 Billion |

| Growth Rate (2026 - 2031) | 9.26% CAGR |

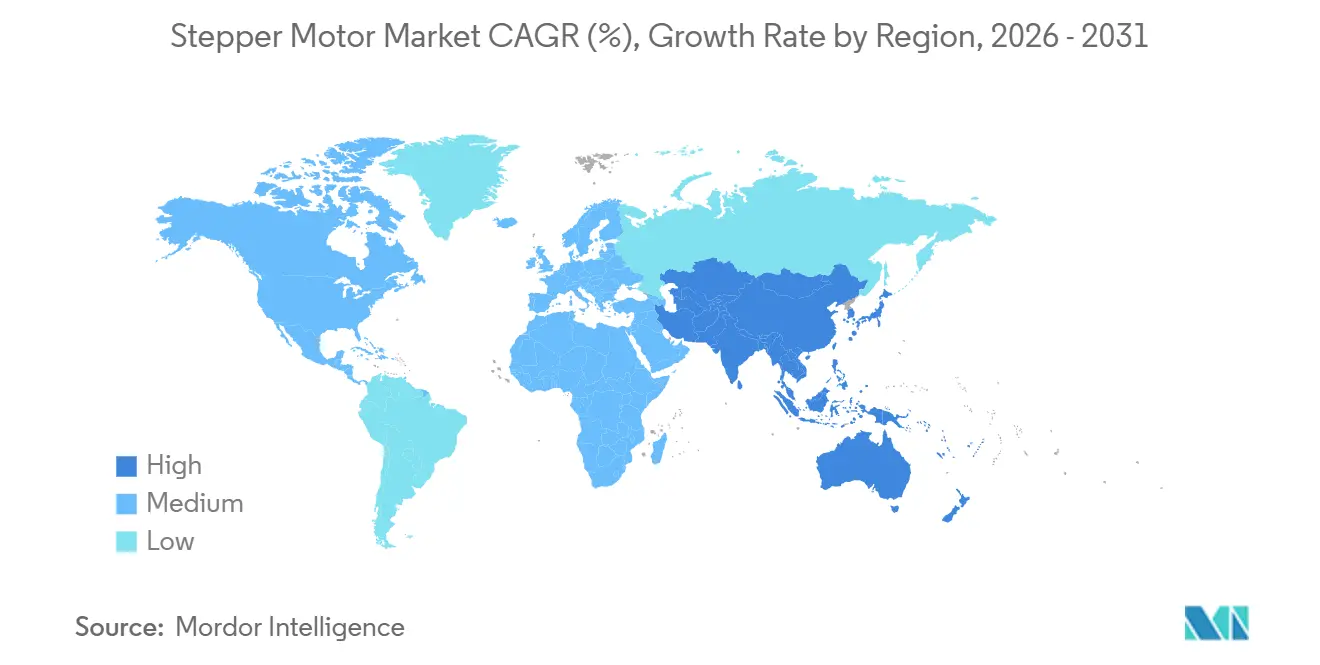

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

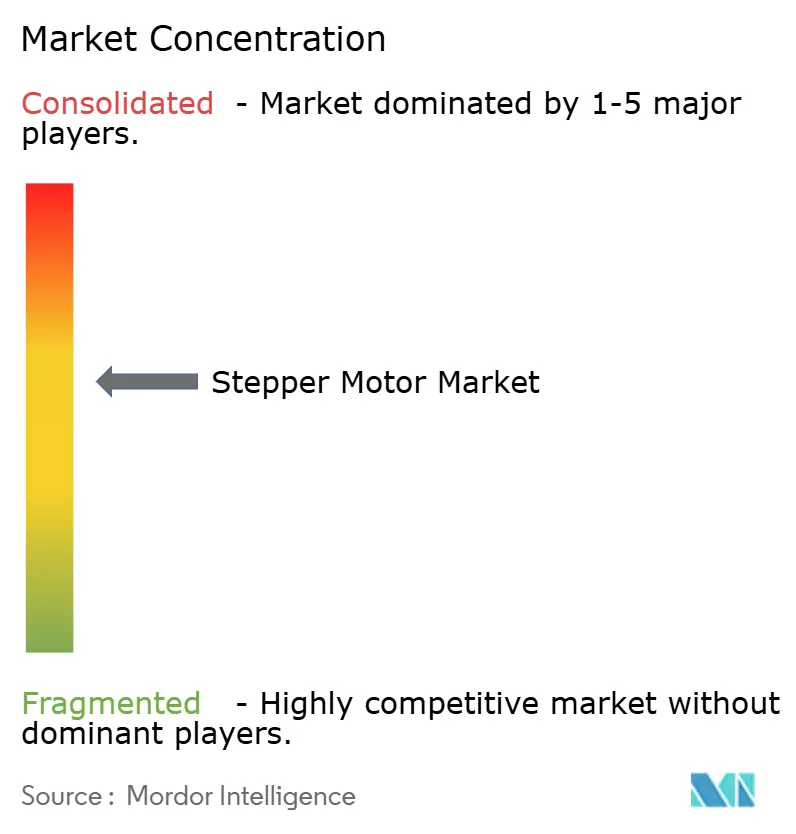

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Stepper Motor Market Analysis by Mordor Intelligence

The stepper motor market size was valued at USD 19.93 billion in 2025 and is estimated to grow from USD 21.78 billion in 2026 to reach USD 33.92 billion by 2031, at a CAGR of 9.26% during the forecast period (2026-2031). Semiconductor packaging investments, a surge in collaborative-robot deployments, and the migration from open-loop to closed-loop motion architectures underpin this trajectory. Energy-efficiency mandates, particularly in the European Union, amplify demand for closed-loop designs, while variable-reluctance motors gain favor where thermal efficiency outweighs torque density. Pricing pressure from vertically integrated Chinese suppliers tempers margin expansion, yet firmware-upgradable controllers and predictive-maintenance analytics create new value pools. Overall, the stepper motor market moves toward smarter, network-ready axes that balance cost, precision, and sustainability.

Key Report Takeaways

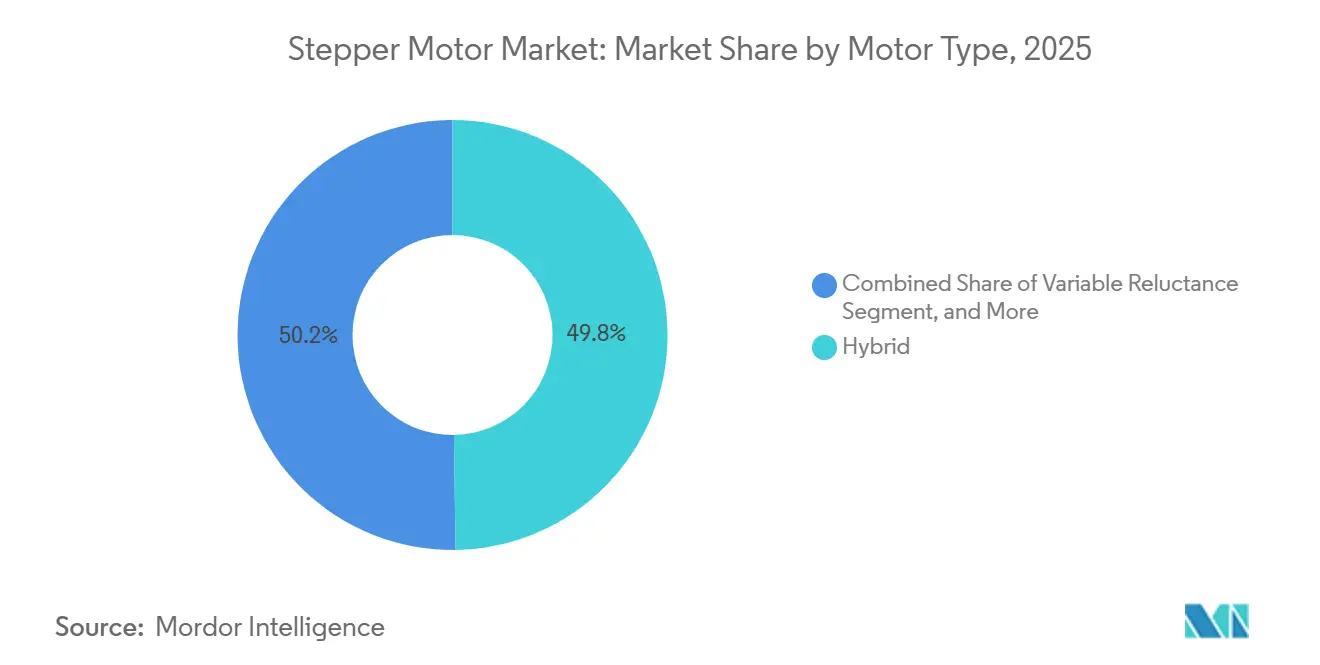

- By motor type, hybrid units led with 49.78% stepper motor market share in 2025, while variable-reluctance designs are set to post the fastest 9.87% CAGR between 2026-2031.

- By drive technique, open-loop architectures accounted for 63.47% of the stepper motor market in 2025, whereas closed-loop systems are projected to grow the fastest at a 9.61% CAGR through 2031.

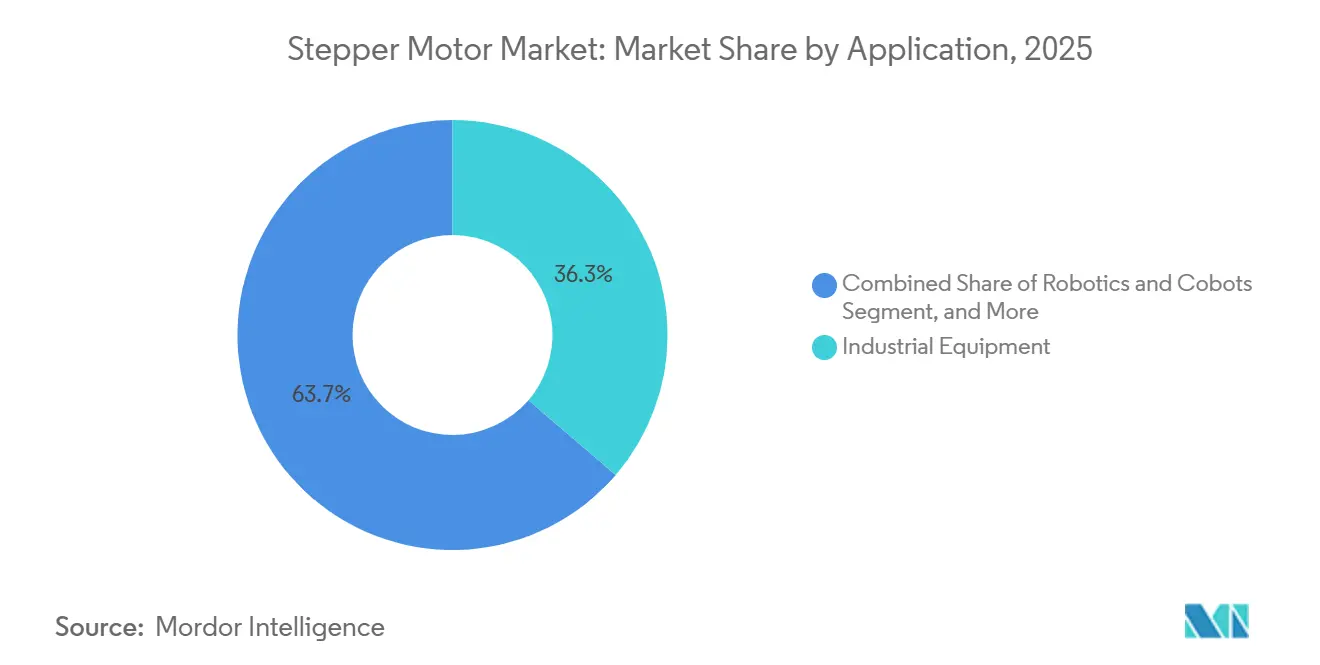

- By application, industrial equipment commanded 36.29% revenue share in 2025, while robotics and cobots are forecast to advance at the highest CAGR of 10.24% during 2026-2031.

- By end-user industry, manufacturing and industrial automation accounted for 42.33% of the stepper motor market share in 2025, whereas semiconductor and electronics end-users are expected to expand at a 10.68% CAGR over the same period.

- By geography, Asia-Pacific captured 48.91% of the stepper motor market in 2025 and is also anticipated to register the fastest CAGR of 10.29% up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Stepper Motor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Robotics and Collaborative Automation | +2.3% | Global, Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Surge in Semiconductor Packaging Equipment Investments | +1.9% | Asia-Pacific core (China, Taiwan, South Korea), spill-over to North America | Short term (≤2 years) |

| Rising Demand for Precision Motion Control in Medical Devices | +1.8% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Expansion of 3-D Printing and Desktop Manufacturing Ecosystems | +1.5% | Global, early gains in North America and Europe | Long term (≥4 years) |

| Shift to Energy-Efficient Closed-Loop Stepper Solutions | +1.2% | Europe core, North America and Asia-Pacific following | Medium term (2-4 years) |

| Emergence of In-Field Firmware-Upgradable Motor Controllers | +0.8% | Global, early adoption in North America and Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Robotics and Collaborative Automation

Collaborative-robot installations climbed to 64,542 units in 2024, a 12% year-on-year rise that highlights manufacturers’ pivot toward flexible automation cells where humans share workspaces with machines.[1]International Federation of Robotics, “World Robotics Report 2024,” ifr.org Stepper motors dominate cobot joints with payloads under 10 kg because their intrinsic detent torque provides passive braking during power loss, avoiding the costly redundant safety circuits required by servos. ISO 10218 and ISO/TS 15066 standards cap allowable joint forces, indirectly pushing motor makers to optimize torque constants and thermal envelopes. Asia-Pacific remains the leading adopter of cobot cells as electronics assemblers retrofit manual lines. Suppliers such as MinebeaMitsumi ship sub-5 mm hybrid motors for humanoid prototypes, aiming for a JPY 3 trillion (USD 20.3 billion) addressable market by 2030. Together, these forces accelerate the stepper motor market’s penetration of next-generation robotics.

Surge in Semiconductor Packaging Equipment Investments

Global semiconductor-equipment outlays reached USD 109 billion in 2024, with advanced-packaging tools forming the fastest-growing slice.[2]SEMI, “Global Semiconductor Equipment Sales,” semi.org China alone spent USD 36.9 billion, up 12.1%, while Taiwan’s USD 32.6 billion reflected TSMC’s multiyear USD 65 billion capex plan. Closed-loop steppers position die bonders, wire bonders, and inspection stages to ±1 µm across 300 mm wafers; encoder resolutions now exceed 10,000 counts per revolution. Intel’s USD 20 billion Arizona expansion will consume 15,000-20,000 axes, providing a near-term demand spike for North American motion suppliers. In aggregate, semiconductor investment is now the single largest incremental contributor to stepper motor market growth over the next two years.

Rising Demand for Precision Motion Control in Medical Devices

Closed-loop steppers deliver sub-micron repeatability at 40-60% of the cost of a servo system, making them the de facto choice for syringe pumps, liquid-handling robots, and diagnostic analyzers. The U.S. FDA’s 2024 electromagnetic-compatibility guidance, aligned with IEC 60601-1-2, raises immunity requirements to 10 V m⁻¹, pushing OEMs toward shielded cabling and ferrite chokes. Vendors such as Faulhaber and Sanyo Denki maintain ISO 13485 systems that streamline 510(k) submissions, reinforcing their competitive positions. Surgical-robot volumes exceeding 1 million procedures annually further expand installed-axis counts, although piezo actuators nibble at MRI-compatible niches.[3]IEEE, “Torque Comparison of Hybrid Stepper and Servo Motors,” ieee.org Overall, healthcare’s quality and compliance demands sustain premium pricing in the stepper motor market.

Expansion of 3-D Printing and Desktop Manufacturing Ecosystems

The installed base of desktop 3-D printers surpassed 2 million units in 2024, growing at mid-teens rates as educators, hobbyists, and micro-factories favor units under USD 1,000. NEMA 17 hybrid steppers remain ubiquitous because they hold position without feedback and integrate easily with open-source firmware. Trinamic’s TMC2209 driver IC cuts audible noise below 40 dB, removing a key adoption barrier. Nevertheless, high-end models such as Bambu Lab’s P2S use closed-loop servos to achieve print speeds>300 mm s⁻¹, highlighting an emerging performance split. For the mass-volume sub-USD 1,000 segment, stepper motors are expected to retain design-win dominance through at least 2031.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Performance Limits Versus Servo and BLDC Motors | -1.4% | Global, higher impact in North America and Europe (high-speed applications) | Medium term (2-4 years) |

| Price Pressure From Low-Cost Asian Manufacturers | -1.1% | Global, highest impact in price-sensitive segments across all regions | Short term (≤2 years) |

| Integrated Smart Actuators Cannibalising Discrete Motors | -0.7% | North America and Europe, emerging in Asia-Pacific | Long term (≥4 years) |

| Thermal-Management Challenges in Compact Designs | -0.5% | Global, focus on consumer electronics and portable devices | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Performance Limits Versus Servo and BLDC Motors

Torque roll-off beyond 1,500 rpm and lower torque-to-inertia ratios constrain stepper adoption in high-speed pick-and-place, CNC, and conveyor systems. IEEE comparative testing shows a 200-step hybrid stepper loses 60% of rated torque at 2,000 rpm, while a frameless servo retains 90%. Although stepper axes cost USD 150-300, servos priced at USD 400-800 cut cycle times up to 60%, justifying the premium in throughput-critical equipment. Resonance in the 200-800 rpm range introduces additional vibration, requiring microstepping or damping solutions. Consequently, stepper motors capture <15% of the multi-axis CNC market and remain marginal in automotive final-assembly lines.

Price Pressure from Low-Cost Asian Manufacturers

Changzhou Leili, MOONS’ Electric, and other Chinese suppliers quote hybrid NEMA 17 motors at 30-40% below Japanese and European peers, leveraging automated winding lines and minimum order sizes of 500 units. Import data place Leili exports to the United States at hundreds of shipments annually, revealing deep penetration of tier-one OEM supply chains. Western incumbents counter with broader catalogs and ISO 13485 or automotive-grade documentation, yet sacrifice gross margin to remain competitive. STMicroelectronics noted a 26.6% year-on-year decline in Q3 2024 motor-driver revenue, linking the slide partly to Chinese fab oversupply. Margin compression will persist across commodity frame sizes, especially in consumer appliances and entry-level 3-D printers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Motor Type: Variable-Reluctance Efficiency Upswing

Hybrid designs accounted for the largest share of the stepper motor market in 2025, with a 49.78% share, and are favored for delivering more than 2 N m of holding torque in widely used NEMA 23 frames. Demand now pivots toward variable-reluctance units, which are projected to advance at a 9.87% CAGR through 2031 because they cut copper losses 20-30% by eliminating permanent magnets, an advantage in HVAC actuators and automotive clusters. Permanent-magnet models remain relevant in camera autofocus modules and office peripherals where peak torque sits below 0.5 N m and duty cycles are intermittent.

Miniaturization keeps hybrids in the spotlight as MinebeaMitsumi begins mass production of 3.3 mm motors that fit smart-watch haptics and humanoid finger joints. Variable-reluctance makers counter with lower bill-of-materials cost, easing price pressure as neodymium prices fluctuate. Supply-chain efficiency also matters: automated lamination stamping and winding have trimmed hybrid unit costs 40% since 2015, while torque-per-ampere has risen 15-20%. The result is a balanced competitive field in which energy efficiency, raw-material volatility, and product miniaturization each steer OEM design decisions.

By Drive Technique: Closed-Loop Adoption Accelerates

Open-loop systems dominated deployments in 2025, supported by sub-USD 120 bills of material and decades of installed-base familiarity. Growing electricity rates and corporate sustainability targets now push buyers toward closed-loop architectures that reduce energy use by more than 40% by modulating phase current based on real-time encoder feedback. Forecasts show closed-loop shipments expanding at a 9.61% CAGR to 2031, helped by predictive-maintenance features that stream torque and temperature data to plant historians.

Technology vendors speed the transition. Oriental Motor’s αSTEP family closes the loop at 4 kHz and eliminates the need for external motion controllers, reducing cabinet wiring in multi-axis gantries. Parker Hannifin’s Compax3 stepper-emulation mode lets integrators replace legacy axes without rewriting motion profiles, lowering retrofit risk. Cooler winding temperatures, often 15-20 °C lower than open-loop counterparts, extend bearing life and allow sealed enclosures in clean-room or medical devices. Together, energy savings, simpler wiring, and longer service intervals underpin a decisive shift toward feedback-rich motion systems.

By Application: Robotics Drives the Next Growth Wave

Industrial equipment, from CNC indexers to textile machinery, accounted for 36.29% of 2025 revenue but now records single-digit growth as automation penetration matures in developed economies. Robotics and cobots are the fastest-growing segment, forecast to grow at a 10.24% CAGR, buoyed by 64,542 collaborative robots shipped in 2024 that rely on stepper detent torque for passive braking in shared workspaces. Medical and laboratory devices select closed-loop steppers for sub-micron dosing while meeting FDA electromagnetic-compatibility rules aligned with IEC 60601-1-2.

In desktop 3-D printing, NEMA 17 hybrids remain dominant because open-source firmware ecosystems simplify tuning, though professional printers are shifting to servos for speeds>300 mm s⁻¹. Automotive gauge clusters, HVAC flaps, and camera pan-tilt heads round out steady but lower-margin uses where low cost per axis is paramount. Overall market opportunity centers on cobots with payloads under 10 kg, surgical instruments, and additive-manufacturing gantries, where precision, safety, and compact packaging align squarely with stepper strengths.

By End-User Industry: Semiconductor Tools Lead Spending Intentions

Manufacturing and industrial automation accounted for 42.33% of 2025 demand, driven by packaging-line upgrades and the shift from pneumatic cylinders to electric actuators. Semiconductor and electronics customers are set to grow fastest at a 10.68% CAGR as global equipment purchases hit USD 109 billion in 2024, with China’s USD 36.9 billion outlay underscoring the urgency of domestic chip capacity. Healthcare and life-science firms adopt closed-loop steppers to achieve sub-micron positioning at 40-60% of the cost of a servo system, reinforcing supplier margins in regulated markets.

Automotive programs remain steady, absorbing millions of low-torque motors for instrument clusters and HVAC dampers, though higher-power seat and sunroof drives migrate to brushless DC. Aerospace and defense niches demand radiation-tolerant units that meet MIL-STD-810 or ECSS standards, where premium pricing offsets small volumes. Consumer appliances, office equipment, and smart-home gadgets round out the landscape, emphasizing ultra-low pricing that favors vertically integrated Chinese producers. As semiconductor capital spending cycles peak, electronics makers will overtake factory-automation buyers as the prime catalyst of stepper procurement through 2031.

Geography Analysis

Asia-Pacific accounted for 48.91% of the stepper motor market share in 2025 and is projected to grow at a 10.29% CAGR through 2031. China led regional semiconductor-equipment spending at USD 36.9 billion in 2024, reflecting its drive for fab self-sufficiency. Taiwan followed, buoyed by TSMC’s multiyear USD 65 billion program to add advanced packaging capacity. Japan remains the design hub, where MinebeaMitsumi, Sanyo Denki, and Oriental Motor collectively generated stepper-motor revenue above JPY 500 billion (USD 3.4 billion) in fiscal 2025. India’s Production Linked Incentive scheme channels USD 26 billion into electronics and pharmaceuticals, opening fresh opportunities for motion-control vendors.

North America held a mid-teen percentage share in 2025, anchored by Intel’s USD 20 billion Arizona fab that alone will require thousands of closed-loop axes. Clustered medical device manufacturing in Massachusetts and California favors suppliers with ISO 13485 certification, bolstering premium, closed-loop shipments. Federal tax incentives aimed at reshoring electronics assembly are boosting demand in Mexico’s border maquiladoras and the U.S. Midwest. Canada’s automation push in food processing and mining rounds out regional growth.

Europe commands a solid share powered by Germany’s machine-tool sector and EU energy-efficiency directives that accelerate closed-loop retrofits. South America’s expansion is concentrated in Brazil’s automotive supply chain and Argentina’s agricultural-machinery upgrades, both of which favor cost-optimized NEMA 23 hybrids. The Middle East and Africa remain nascent, yet logistics automation in the United Arab Emirates and Saudi Arabia’s smart-factory initiatives create beachheads for motion-system integrators. Across emerging regions, voluntary IE4-level efficiency goals, even for sub-kilowatt motors, encourage OEMs to leapfrog directly to feedback-rich designs.

Competitive Landscape

The stepper-motor arena remains moderately fragmented: MinebeaMitsumi, Sanyo Denki, and MOONS’ Electric together ship more than 10 million hybrid units a year yet account for under 30% of combined revenue, leaving ample room for regional specialists and contract manufacturers. Vertical integration gives MinebeaMitsumi cost insulation through in-house bearings and driver ICs, while Oriental Motor competes on a 50,000-SKU catalog that enables same-week delivery of custom shafts, flanges, and encoder options.

Chinese producers leverage automated winding lines and 500-unit minimum orders to undercut Japanese and European quotes by 30-40%, reshaping commodity pricing for NEMA 17 and NEMA 23 motors. Western suppliers defend their share with firmware-upgradable controllers, predictive-maintenance analytics, and regulatory documentation for medical or aerospace programs. STMicroelectronics and Texas Instruments accelerate the trend by integrating current-sense and EMI-mitigation blocks into single-chip drivers, trimming external components and layout time.

Strategic moves punctuate the landscape. Nidec’s 2024 purchase of Mitsubishi Heavy Industries’ machine-tool arm secures rotor-lamination know-how critical for low-torque-ripple designs. Parker Hannifin’s Compax3 stepper-emulation firmware allows OEMs to replace open-loop axes without rewriting motion profiles, unlocking retrofit revenue. Renesas embedded over-the-air update capability in its RX MCU line, enabling 3-D printer fleets to remotely retune microstepping and reduce service visits. Together, cost pressure, digital-service layers, and selective acquisitions define an intensely competitive yet innovation-rich market.

Stepper Motor Industry Leaders

AMETEK Inc.

Anaheim Automation Inc.

Arcus Technology Inc.

ElectroCraft Inc.

Regal Rexnord Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Parker Hannifin introduced the second-generation Compax3S drive, adding an embedded OPC UA server that lets OEMs stream torque, temperature, and energy data from closed-loop stepper axes directly to factory MES platforms for real-time analytics.

- September 2025: MinebeaMitsumi completed a USD 210 million expansion of its Hamamatsu plant and began mass production of 3.3 mm hybrid steppers, boosting annual output capacity by 120 million units to serve emerging humanoid-robot and wearable-device programs.

- June 2025: MOONS’ Electric launched the iStep closed-loop stepper package, a firmware-upgradable motor-and-drive set with integrated Wi-Fi that enables over-the-air microstep tuning and predictive-maintenance telemetry for desktop 3-D printers and laboratory automation.

- March 2025: Renesas Electronics released the RX72M+ microcontroller featuring dual-core architecture, dual Gigabit Ethernet, and a hardware motion engine delivering 128-microstep resolution, targeting multi-axis semiconductor-packaging equipment demanding sub-micron repeatability.

Global Stepper Motor Market Report Scope

The Stepper Motor Market Report is Segmented by Motor Type (Hybrid, Permanent Magnet, Variable Reluctance), Drive Technique (Open-Loop, and Closed-Loop), Application (Industrial Equipment, Robotics and Cobots, Medical and Laboratory Devices, Computing and 3-D Printing, Other Applications), End-User Industry (Manufacturing and Industrial Automation, Healthcare and Life Sciences, Semiconductor and Electronics, Automotive, Aerospace and Defense, Consumer Products, Other End-User Industries), and Geography (North America, South America, Europe, Asia Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hybrid |

| Permanent Magnet |

| Variable Reluctance |

| Open-Loop |

| Closed-Loop |

| Industrial Equipment |

| Robotics and Cobots |

| Medical and Laboratory Devices |

| Computing and 3-D Printing |

| Other Applications |

| Manufacturing and Industrial Automation |

| Healthcare and Life Sciences |

| Semiconductor and Electronics |

| Automotive |

| Aerospace and Defense |

| Consumer Products |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Motor Type | Hybrid | ||

| Permanent Magnet | |||

| Variable Reluctance | |||

| By Drive Technique | Open-Loop | ||

| Closed-Loop | |||

| By Application | Industrial Equipment | ||

| Robotics and Cobots | |||

| Medical and Laboratory Devices | |||

| Computing and 3-D Printing | |||

| Other Applications | |||

| By End-User Industry | Manufacturing and Industrial Automation | ||

| Healthcare and Life Sciences | |||

| Semiconductor and Electronics | |||

| Automotive | |||

| Aerospace and Defense | |||

| Consumer Products | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the stepper motor market in 2031?

It is forecast to reach USD 33.92 billion by 2031, expanding at a 9.26% CAGR from 2026.

Which motor type currently leads in market share?

Hybrid stepper motors held 49.78% market share in 2025, benefiting from high torque density without feedback.

Why are closed-loop stepper systems gaining adoption?

They cut energy use by more than 40%, provide stall detection, and supply real-time data for predictive maintenance, driving a 9.61% CAGR to 2031.

Which region is expected to grow fastest?

Asia-Pacific is forecast to register a 10.29% CAGR through 2031, propelled by semiconductor-equipment investments and vertical integration.

How do stepper motors compare with servos in high-speed tasks?

Stepper torque drops sharply above 1,500 rpm, while servos maintain up to 90% rated torque at 2,000 rpm, leading servos to dominate high-speed pick-and-place and CNC applications.

What strategic trend defines competition in this market?

Vertical integration and firmware-upgradable controllers help incumbents defend margin against low-cost Asian manufacturers offering 30-40% lower prices on standard frames.

Page last updated on: