Solid State Relay Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

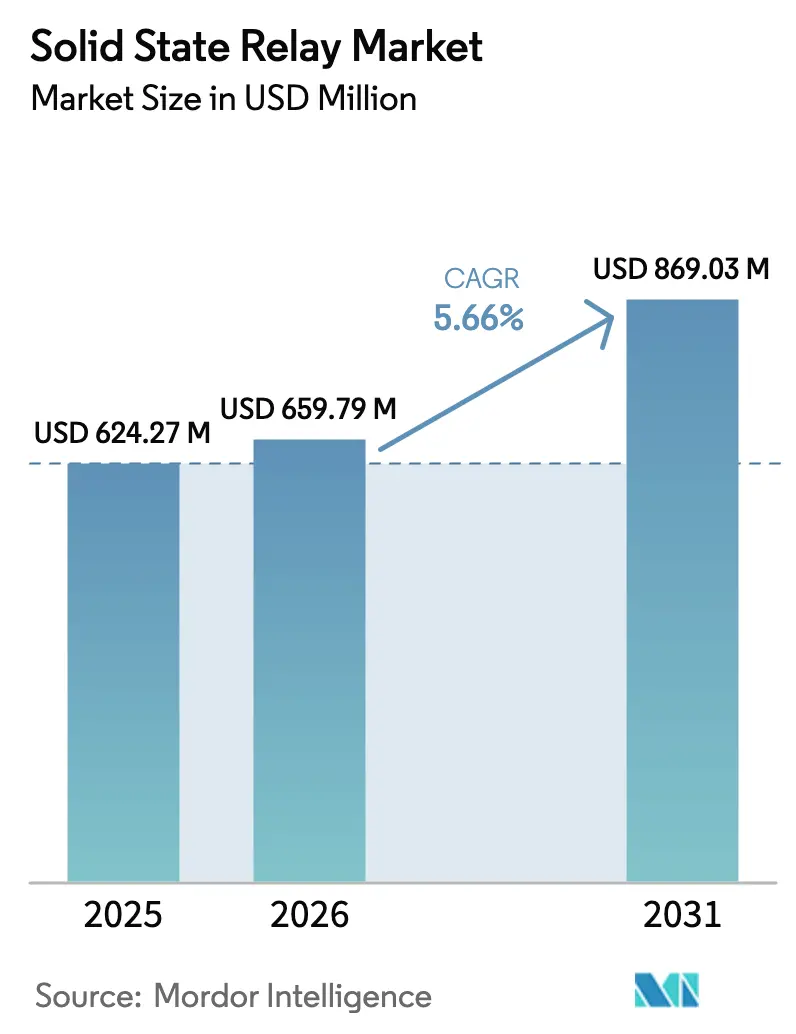

| Market Size (2026) | USD 659.79 Million |

| Market Size (2031) | USD 869.03 Million |

| Growth Rate (2026 - 2031) | 5.66% CAGR |

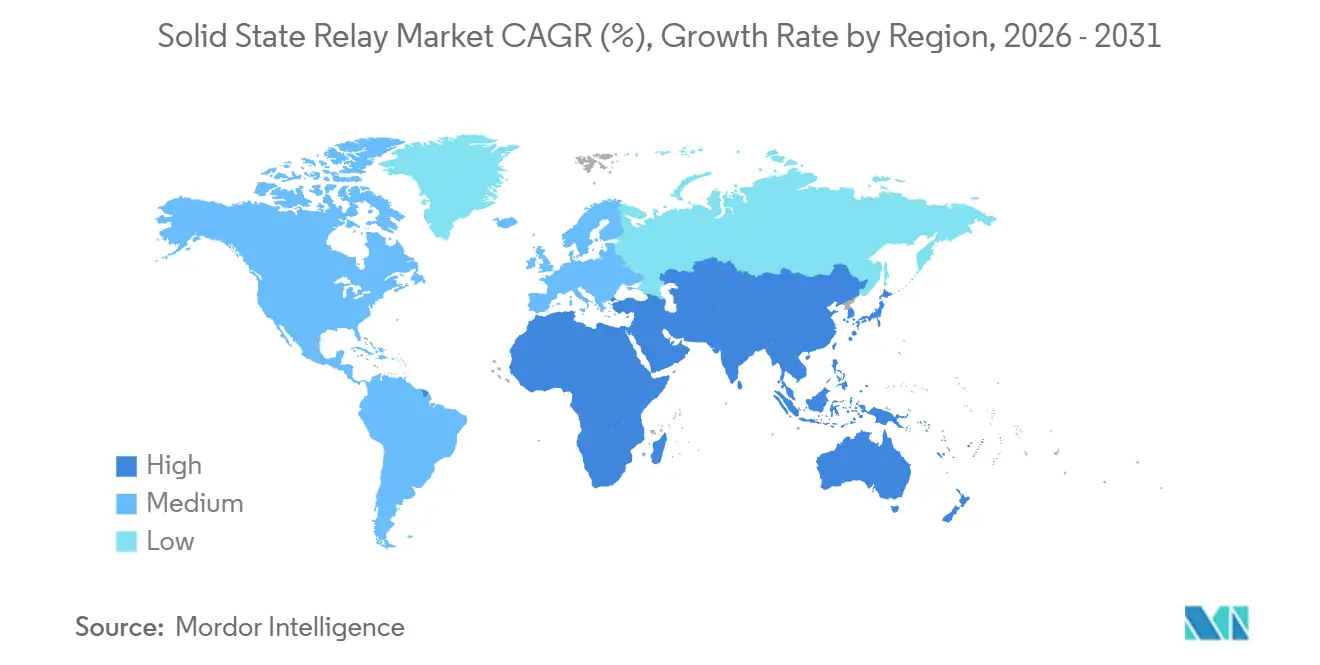

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Solid State Relay Market Analysis by Mordor Intelligence

The Solid State Relay Market size is projected to expand from USD 624.27 million in 2025 and USD 659.79 million in 2026 to USD 869.03 million by 2031, registering a CAGR of 5.66% between 2026 to 2031. Growth is shaped by utilities swapping electromechanical contactors for arc-free switching, factory owners upgrading to Industry 4.0 cabinets, and device makers shrinking power-control footprints with wide-bandgap semiconductors. Manufacturers are using gallium nitride and silicon carbide dies to cut on-state losses, operate beyond 175 °C junction temperature, and eliminate bulky heat sinks in compact enclosures such as medical imaging gantries and quantum-computing cryostats. Asia Pacific dominates shipments because China, Japan, and South Korea lead in photovoltaic inverters and EV chargers, while the Middle East posts the fastest regional CAGR as Saudi Arabia and the United Arab Emirates build gigawatt-scale solar farms that demand contact-less switching for module-level power electronics. Industrial OEM applications still hold the largest revenue slice, yet energy and infrastructure installations are expanding more quickly as utilities deploy solid-state transfer switches that prevent arc erosion during grid-edge islanding events. Competitive pressure comes from semiconductor specialists that integrate gate-driver ICs and undercut traditional relay makers on bill-of-material costs, but incumbents retain an edge through in-house phototriac production and broad safety certification portfolios.

Key Report Takeaways

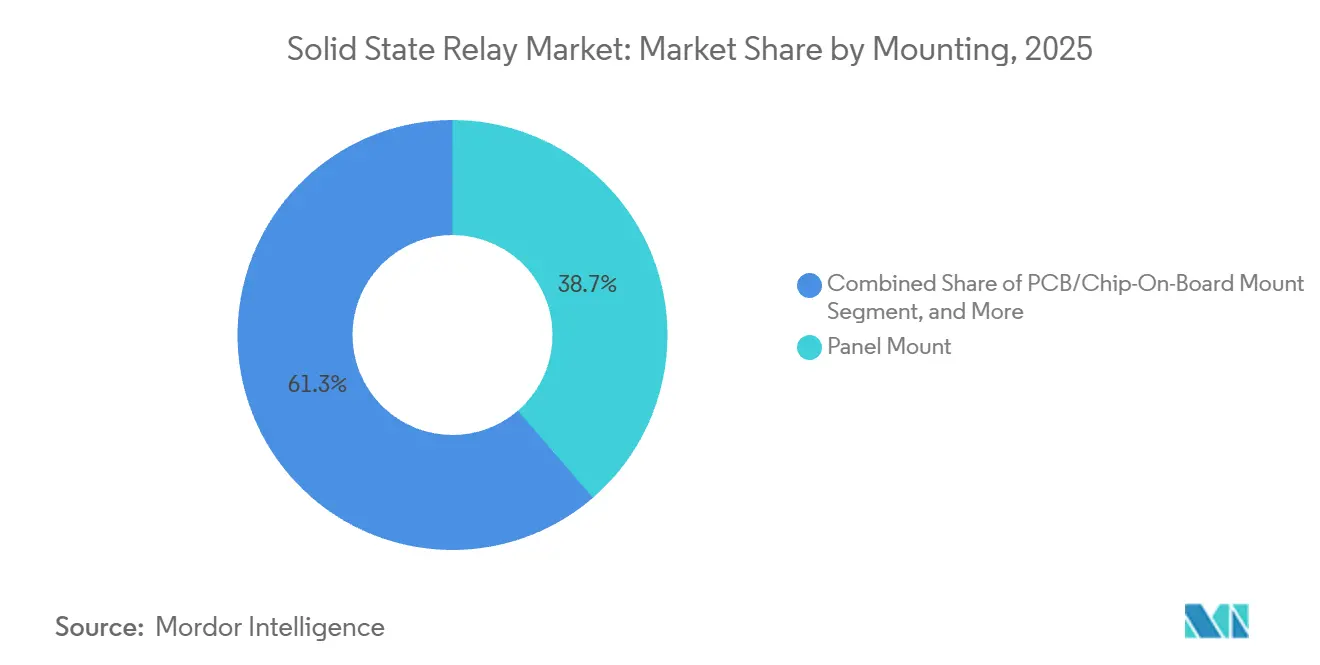

- By mounting configuration, panel-mount designs led with 38.67% of the solid state relay market share in 2025, while DIN-rail variants are forecast to register a 7.11% CAGR through 2031.

- By output type, AC devices accounted for 46.23% of revenue in 2025; three-phase units are the fastest-growing, advancing at a 6.42% CAGR to 2031.

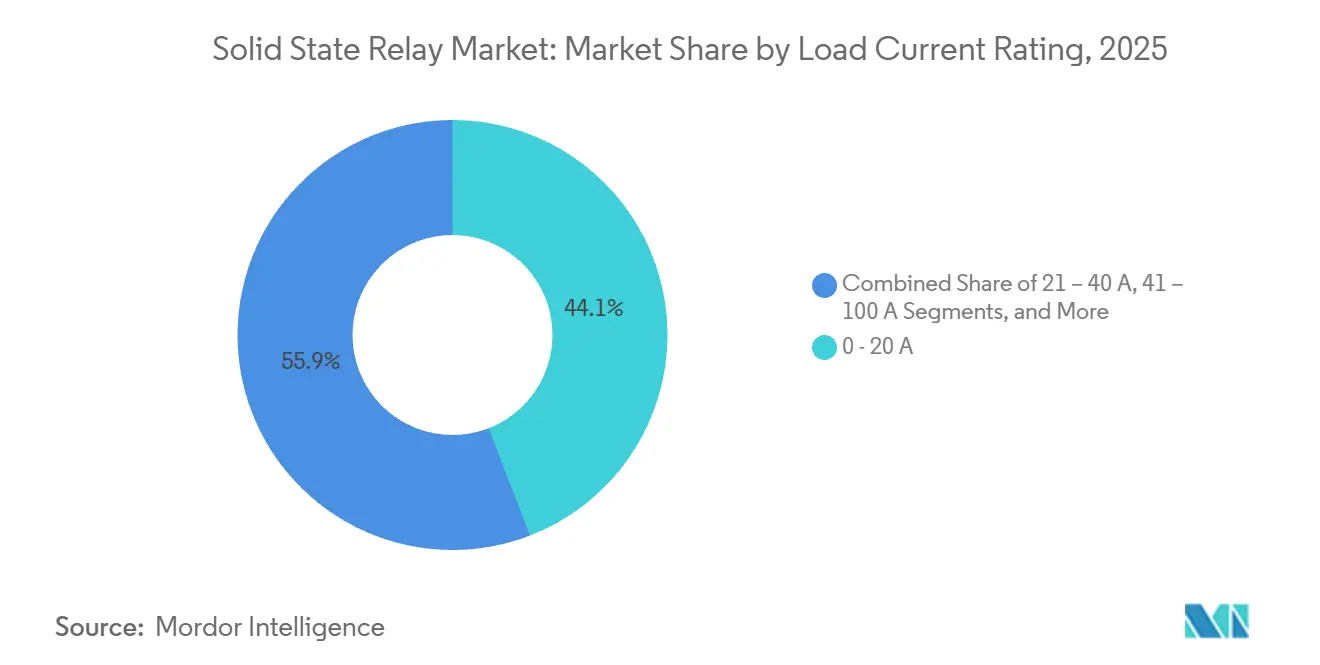

- By load-current rating, the 0-20 ampere bracket accounted for 44.13% of the solid state relay market size in 2025, whereas ratings above 100 amperes are poised to grow at a 6.64% CAGR through 2031.

- By application, industrial OEMs accounted for 31.26% of revenue in 2025, whereas energy and infrastructure installations are projected to expand at a 7.38% CAGR through 2031.

- By geography, Asia Pacific captured 42.32% of sales in 2025, whereas the Middle East is expected to post the fastest regional growth at a 7.23% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Solid State Relay Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing PV and Wind Farm Installations Demanding Arc-Free Switching | +0.8% | Global, concentrated in Asia Pacific, Middle East, and North America | Medium term (2-4 years) |

| Rising Retrofit of Electromechanical Relays in Smart Factories (Europe-led) | +0.9% | Europe (Germany, France, Italy), spillover to North America | Short term (≤ 2 years) |

| Grid-Edge Deployment of Solid-State Transfer Switches in North America Distribution Networks | +0.7% | North America (United States, Canada), early adoption in California and Texas | Medium term (2-4 years) |

| Miniaturisation Push in Medical Devices Elevating SSR Adoption (Asia Pacific OEMs) | +0.6% | Asia Pacific (Japan, South Korea, Taiwan), exports to global markets | Long term (≥ 4 years) |

| HVAC OEM Shift to Mercury-Free Components in Nordics and DACH Region | +0.5% | Europe (Sweden, Norway, Denmark, Germany, Austria, Switzerland) | Short term (≤ 2 years) |

| Growing Adoption of GaN SSRs in Quantum Computing Cryogenic Controls | +0.4% | North America and Europe (research hubs), limited commercial scale | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing PV and Wind Farm Installations Demanding Arc-Free Switching

More than 500 GW of new solar and wind capacity came online during 2024, and the associated inverter, battery, and tracker systems now require sub-millisecond disconnection that electromechanical contactors cannot guarantee without arc erosion.[1]National Renewable Energy Laboratory, “Medium-Voltage Power Electronics for Utility Use,” NREL.GOV Solid state relays meet IEEE 1547-2018 anti-islanding response times, eliminate arc flash events, and support SunSpec rapid-shutdown protocols embedded in California’s Title 24 building code. Utilities view SSRs as foundational elements in modular power blocks that combine bidirectional AC and DC paths, allowing asset owners to defer transmission upgrades while raising renewable penetration. Wind-turbine pitch systems have already shifted from hydraulic to electric servo drives, and three-phase SSRs prevent voltage transients that once tripped supervisory controllers. As bifacial modules and single-axis trackers lift daily switching cycles, the 10-million-cycle lifetime of SSRs neutralizes the higher acquisition price.

Rising Retrofit of Electromechanical Relays in Smart Factories

German, French, and Italian manufacturers are converting legacy panels to DIN-rail SSRs so that Ethernet and fieldbus links remain immune to electromagnetic noise from contact arcing. The German government earmarked EUR 1.2 billion (USD 1.41 billion) in 2024 for Industry 4.0 pilots, many of which specify touch-safe DIN modules that technicians can hot-swap without full line shutdowns. New three-phase contactors with embedded NRG BUS measurement let operators align power trends with machine cycles, creating a data loop that boosts energy efficiency. EU Ecodesign Regulation 2023/826 caps standby power at 0.5 W, favoring SSRs that draw microamp currents. In food-processing plants, sealed SSR housings prevent lubricant and particulate contamination, an increasingly decisive procurement criterion.

Grid-Edge Deployment of Solid-State Transfer Switches

Utilities in California and Texas install solid-state transfer switches at distribution nodes to keep critical loads online during wildfire-driven power-shutoff events. These switches pair 600 V, 100 A SSR modules with optical gate isolation, cutting the 50 ms delay typical of motor-driven transfer devices to sub-cycle intervals and avoiding voltage sag. DOE guidelines released in 2024 emphasize deterministic low-latency relaying, a specification met by SSR gate drivers communicating over IEC 61850 with jitter below 1 ms. Pilot circuits equipped with SSR-based reclosers coordinate seamlessly with inverter-based resources, providing underfrequency shedding without detaching net-generating feeders. Ongoing research into 15 kV silicon-carbide converters will further raise voltage requirements, strengthening demand for high-voltage SSR stacks.

Miniaturization Push in Medical Devices

Handheld ultrasound probes, surgical cautery pens, and wearable infusion pumps need relay footprints under 10 mm², a target only attainable with surface-mount SSRs that merge phototriac and gate-driver circuits in SOP-4 or SSOP outlines. Updated IEC 60601-1 guidance in Japan now tests leakage current on every patient-connected switch, and SSRs pass without the relay creepage distances mechanical contacts require. South Korean dental X-ray makers use SSR pulse control to cut patient radiation by 30% compared with thyratron solutions. Single-use endoscopic tools benefit from SSR disposability because there is no incentive to invest in gold-plated contacts for one-time instruments. As component counts in connected health wearables climb, SSRs free valuable board space for RF, sensing, and battery circuits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Up-Front Cost Versus Electromechanical Relays | -0.6% | Global, most pronounced in price-sensitive building equipment and consumer electronics segments | Short term (≤ 2 years) |

| Thermal Management Challenges Beyond 40 A Load Current | -0.5% | Global, particularly in industrial automation and energy infrastructure applications | Medium term (2-4 years) |

| Electromagnetic Interference Susceptibility in High-Frequency Rail Traction | -0.4% | Europe and Asia Pacific rail networks | Medium term (2-4 years) |

| Limited Field-Replaceability in Mission-Critical Utilities | -0.3% | North America and Europe utility sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher Up-Front Cost Versus Electromechanical Relays

SSRs still command a 200%–400% premium over like-for-like contactors because their bill of materials adds optocouplers, snubber networks, and thermal pads. OMEGA’s SSRDIN600 single-phase units list at AUD 184–228 (USD 120–148) versus AUD 40–60 for mechanical DIN relays, a gap that stalls adoption in HVAC compressors and white goods where replacement cycles exceed 10 years. Without standardized total-cost-of-ownership tools, facilities managers focus on first cost rather than downtime avoidance. Three-phase SSR contactors priced at AUD 550–565 (USD 358–367) also face competition from soft-start motor controllers that use thyristors without optical isolation. Rising automation in coil-winding and contact-stamping lines continues to push electromechanical relay prices downward faster than semiconductor cost curves.

Thermal Management Challenges Beyond 40 A Load Current

Silicon thyristor SSRs dissipate 1–2 W per ampere, requiring aluminum heat sinks that swell cabinet depth and add 200-600 g mass. Littelfuse’s SRP1 series, for instance, must be derated to 40 °C ambient unless forced-air cooling is added. In IP65 enclosures, heat buildup risks thermal runaway, a failure mode absent in contactors where coil heating is decoupled from load current. Weidmüller’s PSSR devices drop from 20 A at 55 °C to 12 A at 65 °C, complicating sizing in plastics extrusion lines. Silicon-carbide switches promise 70% lower losses, but these parts remain in sampling and lack the field history utilities expect.[2]Infineon Technologies AG, “New Solid-State Isolators with 70% Lower Power Dissipation,” INFINEON.COM Extra thermal-interface materials add USD 2–5 per unit and need periodic replacement under vibration, trimming the maintenance-free argument.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mounting: DIN-Rail Variants Cement Gains in Modular Cabinets

Panel-mount relays retained a 38.67% revenue slice in 2025, reflecting deep penetration of legacy machinery that favors screw-mounted devices on open backplates. The solid state relay market now tilts toward DIN-rail products that promise tool-less replacement, and these modules are on track for a 7.11% CAGR to 2031. Omron’s G3PE line reduces install time from 15 minutes to under 2 minutes by snapping onto standard rails, freeing technicians to perform maintenance during brief line pauses rather than full shutdown windows. Food-processing and pharmaceutical plants further endorse DIN form factors because touch-safe polycarbonate covers support stringent hygiene audits.

Demand also comes from European retrofit programs that integrate predictive maintenance via OPC UA. Carlo Gavazzi’s NRG-enabled contactors stream cycle counts and thermal headroom so operators can swap a failing module before unplanned outage. Although panel-mount units continue to dominate bespoke semiconductor equipment where vibration tolerance is critical, the robust clip mechanism of new DIN housings narrows that gap. PCB and chip-on-board SSRs thrive in consumer appliances because automated reflow drives cost down at scale, yet those segments struggle with sticker price. Plug-in SSRs survive in utility protection racks where octal sockets provide standardization that simplifies spares logistics. The drift toward DIN-rail also aligns with IEC 62314, which calls for finger-safe terminals that shield end users from live parts.

By Output Type: Three-Phase Devices Accelerate on Motor-Control Upgrades

AC SSRs covered 46.23% of 2025 revenue thanks to broad use in resistive heaters and lighting panels, but three-phase relays earn the growth spotlight with a 6.42% CAGR forecast through 2031. Industrial plants are modernizing star-delta and soft-start motor circuits, replacing bulky contactors whose vibrations and contact bounce shorten service life. Carlo Gavazzi’s latest RGC3P integrates metering so users can spot rising current harmonics that often precede bearing wear. In plastics extrusion, zero-cross switching eliminates voltage spikes that otherwise scar winding insulation.

DC SSRs remain vital to battery energy-storage systems and EV chargers, yet they battle intelligent power modules that embed drivers and temperature sensing in one package. Hybrid AC/DC relays hold niche positions in UPS systems where control logic sits on DC but load circuits switch AC, safeguarding continuity with minimal parts. For HVAC chillers in Europe, SSRs help meet standby power ceilings established by Ecodesign Regulation 2023/826 because they draw microamp control current in the off state.[3] European Commission, “Regulation (EU) 2023/826 on Ecodesign Requirements,” EUROPA.EU As wide-bandgap devices enter mass production, three-phase SSRs rated to 660 V and 45 A will shrink further, blurring lines between relay, starter, and drive.

By Load Current Rating: High-Current Designs Tap Heavy-Industry Demand

Relays below 20 A contributed 44.13% of the solid state relay market size in 2025, buoyed by process controls, medical tools, and consumer appliances. Above 100 A, however, comes the structural uptrend, with this bracket targeting a 6.64% CAGR to 2031. Aluminum smelters and arc furnaces need contact-less switching that endures surge currents at cold start without welding contacts. Infineon’s silicon-carbide isolators unlock custom SSR stacks exceeding 1,000 V and 100 A while shrinking thermal footprints.

Yet thermal removal remains a hurdle. Engineers often parallel multiple 75 A SCR modules linked by current-sharing chokes, trading silicon cost for manageable heat dissipation. Emerging SiC designs may run at 150 A without liquid cooling, but their cost premium keeps adoption selective. Meanwhile, multi-channel low-current modules gain traction in distributed I/O blocks; eight or sixteen SSRs share one logic connector, trimming cabinet wiring.

By Application: Utilities Propel the Fastest Revenue Climb

Industrial OEM machinery produced 31.26% revenue in 2025, ranging from robot grippers to CNC brake circuits. The energy and infrastructure segment is set to rise 7.38% each year through 2031 as utilities roll out solid-state transfer switches and medium-voltage converters that handle bidirectional flows from rooftop solar and community storage.[4]U.S. Department of Energy, “OE Report: Solid State Power Substation Technology Roadmap,” ENERGY.GOV In building equipment, HVAC makers weigh SSRs against price ceilings, limiting penetration to premium lines touting silent operation.

Food and beverage processors adopt SSRs inside sterilizers and conveyors where lubricants and arcing particles violate hygiene rules. Transportation sees SSR growth in EV chargers and rail signaling relays that must switch hundreds of times per day. Healthcare fills the miniaturization niche, embedding SOP-4 devices in portable pumps and scanners. Automotive engineers evaluate SSR battery disconnects that satisfy ISO 26262 diagnostics, though wide-scale rollout awaits lower SiC costs.

Geography Analysis

Asia Pacific retained 42.32% revenue in 2025 because China controls the vertical stack of phototriac dies, SCR wafers, and heat-sink extrusion, letting domestic vendors undercut imported parts by up to 50% while meeting UL 508 and IEC 62314 certifications. Japan and South Korea supplement demand with high-density EV charging stations that rely on rapid AC switching, and Taiwan’s medical-electronics cluster specifies miniaturized SSRs for export-grade devices.

North America follows, propelled by United States utilities that equip substations with SSR-based reclosers to avoid flicker during wildfire preventive shutoffs. California and Texas dominate pilot projects, while Canada aligns adoption through feeder-automation funding. Mexico absorbs steady orders for SSR-controlled packaging and automotive lines serving the North American trade block.

Europe leverages Industrie 4.0 grants and mercury-free directives. Germany, France, and the United Kingdom replace mechanical relays to comply with Regulation 2017/852 banning mercury switches in electrical equipment. DIN-rail units paired with predictive-maintenance analytics gain favor in retrofit programs supported by the EUR 1.2 billion (USD 1.41 billion) smart-factory budget.

The Middle East secures the fastest CAGR at 7.23% as Saudi Arabia’s Vision 2030 funds gigawatt solar parks and the United Arab Emirates installs battery storage at the Mohammed bin Rashid Al Maktoum Solar Park. Utilities there choose SSRs for module-level power optimizers that must disconnect strings in milliseconds during sandstorm faults.

South America applies SSRs in remote mining and soy-processing plants, where limited technician access elevates the value of maintenance-free switches. Africa’s early deployments focus on telecom base stations and off-grid solar microgrids in Kenya and South Africa because low quiescent draw extends battery life.

Competitive Landscape

The solid state relay market hosts moderate concentration. Omron, Panasonic, and Carlo Gavazzi keep share through vertically integrated phototriac output and broad safety listings, while Infineon, Vishay, and Broadcom target cost per channel by monolithically integrating gate drivers. Littelfuse differentiates with epoxy-free copper substrates that lower junction temperature and lift surge ratings. Carlo Gavazzi’s RGC3P family melds switching and NRG metering, giving customers harmonic signatures that feed predictive maintenance algorithms.

White-space opportunity lies in medium-voltage SSRs above 1 kV, where silicon-carbide modules could displace vacuum contactors in grid feeders. Another pocket is ultraminiature relays below 10 mm² for smart wearables. Chinese entrants challenge incumbents by leveraging domestic supply chains that shorten lead times and slash prices while still clearing IEC testing.

Strategic moves underscore the competitive tempo. Omron’s partnership with Cognizant embeds diagnostics that push cycle counts to cloud dashboards, foreshadowing service-based revenue. Rockwell Automation’s M100 electronic motor starter folds relay, overload, and Ethernet connectivity into one DIN-rail unit, redefining buying criteria for motor-control cabinets. Littelfuse publishes open reliability test results to sway specifiers toward its assemblies, positioning technical transparency as a sales lever.

Solid State Relay Industry Leaders

ABB Ltd.

Omron Corporation

Panasonic Holdings Corp.

Carlo Gavazzi Holding AG

Sensata Technologies (Crydom)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Littelfuse began sampling a dual-channel silicon-carbide SSR stack rated 1,200 V at 50 A per channel, targeting medium-voltage reclosers in United States distribution feeders.

- November 2025: Littelfuse introduced the CPC1601M load-powered latching relay for smart HVAC controls, dropping standby draw below 0.5 W to meet EU Ecodesign thresholds.

- September 2025: Littelfuse updated SRP1-ME datasheets with new thermal curves and guidance on parallel operation above 60 A.

- August 2025: Carlo Gavazzi unveiled RGC2P and RGC3P three-phase contactors featuring integrated NRG BUS energy monitoring.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the solid-state relay (SSR) market as all factory-built switching devices that use power semiconductors instead of mechanical contacts to control AC, DC, or AC/DC loads across industrial, building, mobility, and infrastructure applications. According to Mordor Intelligence, the scope tracks only complete packaged SSR units sold through direct and indirect channels in original-equipment and retrofit projects.

Scope exclusion: Modules integrated inside power converters, solid-state circuit breakers, and electromechanical or reed relays are outside this assessment.

Segmentation Overview

- By Mounting

- Panel Mount

- PCB/Chip-On-Board Mount

- DIN-Rail Mount

- Plug-in/Socket Mount

- By Output Type

- AC Solid-State Relay

- DC Solid-State Relay

- AC/DC Hybrid Relay

- Three-Phase Solid-State Relay

- By Load Current Rating

- 0 - 20 A

- 21 - 40 A

- 41 - 100 A

- Above 100 A

- By Application

- Energy and Infrastructure (Renewables, Grid-Edge, UPS)

- Industrial OEM (Robotics, CNC, Packaging)

- Building Equipment (HVAC, Elevators, Fire Safety)

- Food and Beverage Processing

- Automotive and Transportation (EV Chargers, Railway Signalling)

- Industrial Automation (PLCs, Motion Control)

- Healthcare and Medical Devices

- Consumer Electronics and White Goods

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Kenya

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with component makers, contract manufacturers, automation OEM engineers, and regional distributors across Asia-Pacific, North America, and Europe clarified average selling prices, heat-dissipation limits, and channel mix trends. These conversations let us stress-test secondary findings, plug data gaps, and fine-tune growth assumptions.

Desk Research

Our analysts first mined open data sets such as UN Comtrade trade codes for 853649, International Energy Agency solar and wind capacity additions, and IEC 61810 standards updates that trigger design refresh cycles. Industry association briefs from SEMI, IEEE Power Electronics Society, Japan Electronics and Information Technology Industries Association, plus company 10-K filings and investor decks supplied baseline shipment, pricing, and design-win clues. Subscription sources like D&B Hoovers for vendor financials and Dow Jones Factiva for shipment-level news helped refine regional splits. The sources listed here illustrate the wider pool consulted; many additional public records and academic papers were also reviewed to validate data points.

Market-Sizing & Forecasting

A top-down pool was built by reconstructing global SSR demand from production and trade statistics, which are then sliced by mounting type and load current using installation ratios shared by interviewees. Select bottom-up checks, panel-mount supplier roll-ups, and sampled ASP × volume for PCB relays anchor the totals. Key model drivers include new PV inverter shipments, EV battery-management unit counts, industrial robot installations, and average panel-mount ASP progression. A multivariate regression links these indicators to historical SSR revenues before an ARIMA overlay projects five-year trajectories. Where bottom-up totals diverged beyond five percent, inputs were revisited or weighted averages applied.

Data Validation & Update Cycle

Outputs pass a three-layer review that screens out unit-price anomalies, region-share outliers, and year-on-year jumps. Senior analysts sign off only after reconciling variances with independent import data. Models refresh annually, with interim updates if tariff shifts, major plant expansions, or mergers materially alter the baseline.

Why Our Solid-state Relay Baseline Commands Reliability

Published numbers often vary because firms apply different device definitions, bundle allied components, or freeze exchange rates at divergent points.

Key gap drivers include (a) others merging SSRs with solid-state breakers and opto-isolated switches, inflating totals; (b) aggressive EV adoption assumptions without cross-checking charger rollout pacing; and (c) longer refresh cycles that miss recent ASP easing in Asia.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 624 million | Mordor Intelligence | - |

| USD 1.65 billion (2024) | Global Consultancy A | Bundles SSRs with hybrid relays and uses list prices without regional discounts |

| USD 1.54 billion (2024) | Industry Association B | Counts integrated SSR chips inside inverters and extrapolates EV sales using a single high-growth scenario |

Our comparison shows that Mordor's disciplined scope selection, dual-path modeling, and annual refresh cycle yield a balanced, transparent baseline that decision-makers can trace back to explicit variables and repeatable steps.

Key Questions Answered in the Report

How large is the global solid state relay market in 2026?

The solid state relay market size reached USD 659.79 million in 2026, and it is forecast to climb to USD 869.03 million by 2031.

Which mounting configuration is growing fastest?

DIN-rail variants are expanding at a 7.11% CAGR because modular cabinets shorten replacement time and comply with touch-safe IEC 62314 requirements.

What drives three-phase solid state relay adoption?

Industrial facilities retrofit three-phase relays to cut voltage transients in motor starters, supporting a 6.42% CAGR through 2031.

Why is the Middle East posting the quickest regional growth?

Gigawatt-scale solar farms in Saudi Arabia and the United Arab Emirates need arc-free switching at module level, lifting regional demand at a 7.23% CAGR.

What is the primary restraint to wider SSR penetration?

Higher up-front cost versus electromechanical relays, often 200%–400% more expensive, delays uptake in price-sensitive HVAC and consumer appliances.

How do wide-bandgap semiconductors influence future designs?

Gallium nitride and silicon carbide cut on-state losses and allow junction temperatures above 175 °C, enabling compact SSRs suited to medical and quantum-computing gear.

Page last updated on: