Inductor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 11.76 Billion |

| Market Size (2031) | USD 14.47 Billion |

| Growth Rate (2026 - 2031) | 4.23% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Inductor Market Analysis by Mordor Intelligence

The Inductor Market size is expected to grow from USD 11.28 billion in 2025 to USD 11.76 billion in 2026 and is forecast to reach USD 14.47 billion by 2031 at 4.23% CAGR over 2026-2031. Robust demand from electric-vehicle powertrains, 5G radio access networks, and edge AI servers is driving steady expansion in the inductor market, even as smartphone unit growth plateaus. Supply chains are shifting toward thin-film and nanocrystalline solutions that deliver ultra-low core loss above 1 MHz, while end users are tightening electromagnetic interference limits, which favor shielded constructions. Asia Pacific anchors capacity, yet regional reshoring in North America and Europe is accelerating to mitigate geopolitical risks and raw material price swings. Competitive differentiation now centers on vertical integration of ferrite powders, automated winding equipment, and co-packaging of integrated magnetics with wide-bandgap switches.

Key Report Takeaways

- By Inductor type, fixed inductors commanded 42.52% of the inductor market size in 2025; thin-film devices are growing at the fastest 4.91% CAGR to 2031.

- By end-user vertical, consumer electronics held 34.37% of the inductor market share in 2025, while automotive applications are forecast to expand at a 5.82% CAGR through 2031.

- By core material, ferrite cores led with 55.16% revenue share in 2025, whereas nanocrystalline and amorphous alloys are the quickest-rising segment at a 5.16% CAGR through 2031.

- By mounting technique, surface-mount technology dominated with a 68.63% share in 2025, while embedded-PCB inductors are expected to grow at a 6.43% CAGR through 2031.

- By shielding, shielded constructions accounted for 60.53% of the 2025 revenue and are projected to advance at a 5.11% CAGR through 2031.

- By geography, Asia-Pacific commanded 36.23% of the inductor market share in 2025 and is poised to grow at 6.51% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Inductor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for miniaturized consumer electronics | +0.6% | Global with focus in Asia Pacific and North America | Short term (≤ 2 years) |

| Electrification of automotive sector (EVs) | +1.2% | China, Europe, North America | Medium term (2-4 years) |

| Expansion of 5G and high-speed communications | +0.8% | Asia Pacific core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Growth in renewable energy and power electronics | +0.7% | Europe and Asia Pacific, emerging in Middle East | Long term (≥ 4 years) |

| Adoption of GaN/SiC power stages | +0.9% | North America and Europe, expanding to Asia Pacific | Medium term (2-4 years) |

| On-device AI in edge servers | +0.5% | North America and Asia Pacific data-center hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Electrification Of Automotive Sector

Battery-electric and plug-in hybrid vehicles captured 18% of global light-duty vehicle sales in 2025, and regulators aim for a penetration of more than 35% by 2030.[1] International Energy Agency, “Global EV Outlook 2025,” iea.org Each electrified platform integrates 150-300 inductors across traction inverters, on-board chargers, and DC-DC converters, lifting average content well above internal combustion levels. High-voltage 800 V buses require coupled inductors with saturation currents exceeding 200 A and leakage inductance under 50 nH to minimize switching losses. AEC-Q200 testing requires a 1,000-hour life at 150 °C, which restricts the qualified supplier pool and raises entry barriers. Tesla lowered per-vehicle inductor costs by 12% in 2025 through dual sourcing and design-for-manufacture initiatives.

Expansion Of 5G And High-Speed Communications

Global 5G base-station count exceeded 4 million in 2025, with China installing 60% of the sites. Massive-MIMO arrays integrate dozens of millimeter-wave inductors per RF front-end, each requiring self-resonant frequencies above 10 GHz. Murata reported 35% annual growth in demand for multilayer inductors rated for >10 GHz service. ETSI EN 301 908 tightened spurious-emission limits, compelling higher-Q designs that boost inductor market adoption. With mid-band traffic per user tripling to 35 GB per month in 2025, operators continue to densify networks, sustaining long-term order visibility.

Adoption Of GaN/SiC Power Stages

Gallium nitride and silicon carbide devices switch five times faster than silicon MOSFETs, pushing operating frequencies beyond 500 kHz. Infineon recorded 48% year-over-year GaN revenue growth in 2025, mainly from server and solar inverters. Standard ferrites incur >500 mW/cm³ core loss at 1 MHz, whereas nanocrystalline cores cut loss below 100 mW/cm³, enabling 98.5% converter efficiency in Wolfspeed demonstrations. Interleaved topologies favor coupled inductors that reduce ripple and capacitor count, reinforcing a premium segment within the inductor market.

On-Device AI In Edge Servers

Inference accelerators now draw peak currents beyond 400 A at sub-1 V rails, triple 2022 figures. Texas Instruments specifies multiphase buck converters using inductors with <0.3 mΩ DC resistance and saturation above 50 A to keep transients within 50 mV. NVIDIA’s next-generation GPU consumes 700 W, necessitating 12-phase regulators with integrated coupled inductors. Eaton disclosed that shipments of high-current molded inductors for AI doubled in 2025 as cloud providers adopted more edge deployments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in copper and ferrite prices | -0.4% | Global, acute in Asia Pacific manufacturing hubs | Short term (≤ 2 years) |

| Global supply-chain disruptions | -0.3% | Global, concentrated in Asia Pacific and Europe | Short term (≤ 2 years) |

| Thermal management challenges in embedded inductors | -0.2% | North America and Europe advanced-packaging centers | Medium term (2-4 years) |

| Integrated passive devices eroding discrete demand | -0.3% | Global, led by Asia Pacific consumer electronics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Copper and Ferrite Prices

Copper accounted for 40-50% of wire-wound inductor cost structures, and London Metal Exchange spot prices fluctuated between USD 8 200 and USD 10 500 per ton in 2025. China controls about 70% of manganese-zinc ferrite capacity, and rare-earth export quotas imposed in early 2025 extended lead times from 8 to 16 weeks.[2]United States Geological Survey, “Mineral Commodity Summaries 2025 – Rare Earths,” usgs.gov Mid-tier suppliers lacking hedging programs saw margin compression of 200-300 basis points, whereas vertically integrated majors stabilized input costs. Rising prices are nudging designers toward air-core alternatives for non-critical roles, though inductance density penalties limit broader substitution.

Thermal Management Challenges in Embedded Inductors

Embedding magnetic cores inside PCB substrates trims board area yet elevates thermal stress. IEEE testing showed a 15% inductance drop at 130 °C in a 48 V automotive DC-DC module, breaching ripple specifications. AT&S reported embedded-inductor module yields below 85% in 2025 due to delamination and coefficient of thermal expansion mismatch. Metal-composite or air-core spirals offer higher temperature headroom but deliver 30-40% lower inductance density, forcing trade-offs between footprint and efficiency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Inductor Type: Thin-Film Architectures Reshape RF And High-Frequency Design

Thin-film devices captured notable momentum and are forecast to expand at a 4.91% CAGR to 2031. This slice of the inductor market benefits from RF modules that require self-resonant frequencies above 20 GHz and tolerance within ±2%. Fixed inductors retained 42.52% revenue share in 2025, supplying cost-sensitive DC-DC converters and lighting drivers. Sputtered copper traces on ceramic substrates shrink footprints to 0.4 mm x 0.2 mm, a level now entering volume production for millimeter-wave power amplifiers. Coupled inductors are gaining prominence in multiphase voltage regulators for AI accelerators, reducing the need for output capacitor banks by nearly half.

Thin-film adoption is spreading beyond phones into 5G base stations, where high-Q performance improves spectral masks. Meanwhile, molded and wire-wound designs dominate solar inverters and motor drives that demand >100 µH inductance and >100 A current ratings. Multilayer ceramic inductors remain competitive below 5 GHz but are ceding high-frequency sockets to thin-film options. This bifurcation highlights the inductor market's segmentation between price-driven mass volumes and performance-driven premium niches. Designers weigh cost, saturation, and self-resonance as they transition from legacy wire-wound architectures to thin-film solutions.

By Core Material: Nanocrystalline Alloys Meet Wide-Bandgap Needs

Ferrite cores accounted for 55.16% of shipments in 2025, reflecting scale economics and acceptable losses below 500 kHz. However, nanocrystalline and amorphous alloys are expected to climb at a 5.16% CAGR as GaN and SiC converters switch near 1 MHz. Hitachi Metals documented a 20% volume reduction in a 10 kW solar inverter when replacing ferrite with nanocrystalline ribbon, while core loss fell by two-thirds. IEC 60404 measurement standards allow designers to benchmark these materials against ferrites with confidence.

Iron-powder composites offer higher saturation than ferrite but lower permeability than amorphous ribbons, making them suitable for high-current automotive coils. Air and ceramic cores deliver zero hysteresis, yet have low inductance density, limiting their usage to RF tuning. The shift toward high-frequency, high-temperature operation elevates nanocrystalline alloys from a niche to a mainstream technology, injecting fresh competition into the inductor market.

By Mounting Technique: Embedded PCB Inductors Pursue Sub-Millimeter Heights

Surface-mount technology commanded 68.63% of revenue in 2025 and remains the workhorse for automated pick-and-place lines. Embedded and integrated PCB inductors, projected to grow at a 6.43% CAGR, eliminate discrete packages and cut parasitic inductance by 30%. Apple’s 2025 flagship phone utilized embedded ferrite coils to reduce its total thickness by 0.3 mm. The advance aligns with thinner wearables and augmented-reality headsets that tolerate less than 0.5 mm z-height.

Through-hole components keep relevance in traction inverters where >50 A currents and 20 G vibration demand rugged pins. Yet OEM roadmaps increasingly favor embedded magnetics in power-module substrates to streamline assembly. Thermal buildup above 120 °C remains the adoption hurdle, driving R&D into metal-powder cores and microchannel cooling.

By Shielding: Regulatory Pressure Elevates Shielded Designs

Stricter CISPR 25 and IEC 60601 limits led shielded constructions to 60.53% revenue share in 2025, and they will advance at 5.11% CAGR. Magnetic enclosures cut radiated emissions by up to 40 dB, ensuring compliance for ADAS, medical imaging, and 5G radios. Unshielded inductors still appeal in portable gadgets where board-level filtering suffices and every milliohm of DC resistance counts.

In automotive domains, ISO 11452 mandates system-level EMC validation, tilting selection toward shielded variants, especially for 48 V battery rails. The trade-off between efficiency and noise will continue to push the inductor market toward shielded form factors as wireless interfaces proliferate.

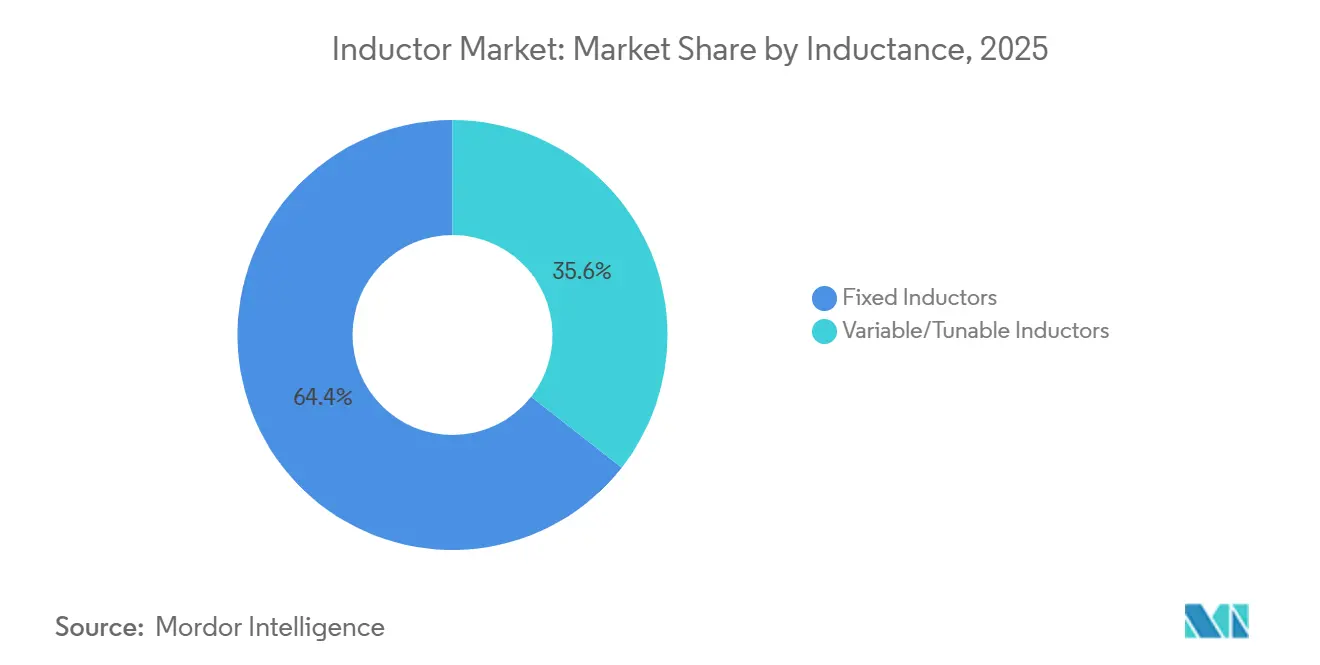

By Inductance: Variable Devices Enable Adaptive Systems

Non-tunable (fixed-inductance) products accounted for 64.42% of 2025 sales, powering converters where the values remain constant. Variable/tunable inductors, poised for a 6.76% CAGR through 2031, support antenna tuning and adaptive power delivery. Qualcomm integrated tunable elements into its RF360 platform to achieve 1.5 dB of radiated-power efficiency across 5G bands. Millimeter-wave deployments amplify the need for real-time impedance matching, boosting this specialized corner of the inductor market.

Mechanical, MEMS, or varactor-controlled products command premium prices due to tighter tolerances. While fixed coils will dominate high-current pathways, tunable options will proliferate in software-defined radios and user-equipment antenna arrays, carving out a resilient growth pocket.

By End-User Vertical: Automotive Electrification Leads Growth

Automotive applications are projected to grow at a market-leading 5.82% CAGR through 2031, driven by increasing inductor counts per electric drivetrain. Consumer electronics retained a 34.37% stake in 2025, yet unit saturation tempers future expansion. Telecommunications infrastructure benefits from 5G densification, with each macro cell embedding 200-400 inductors. Renewable energy installers specify high-power nanocrystalline cores for solar and wind converters, aligning with global decarbonization targets.[3]International Renewable Energy Agency, “Renewable Capacity Statistics 2025,” irena.org

Aerospace, defense, and medical equipment pay premium prices for radiation-hardened or sterilizable parts, but their volumes remain comparatively low. The divergence highlights the split in the inductor market between vast commodity demand and specialized, high-margin segments.

Geography Analysis

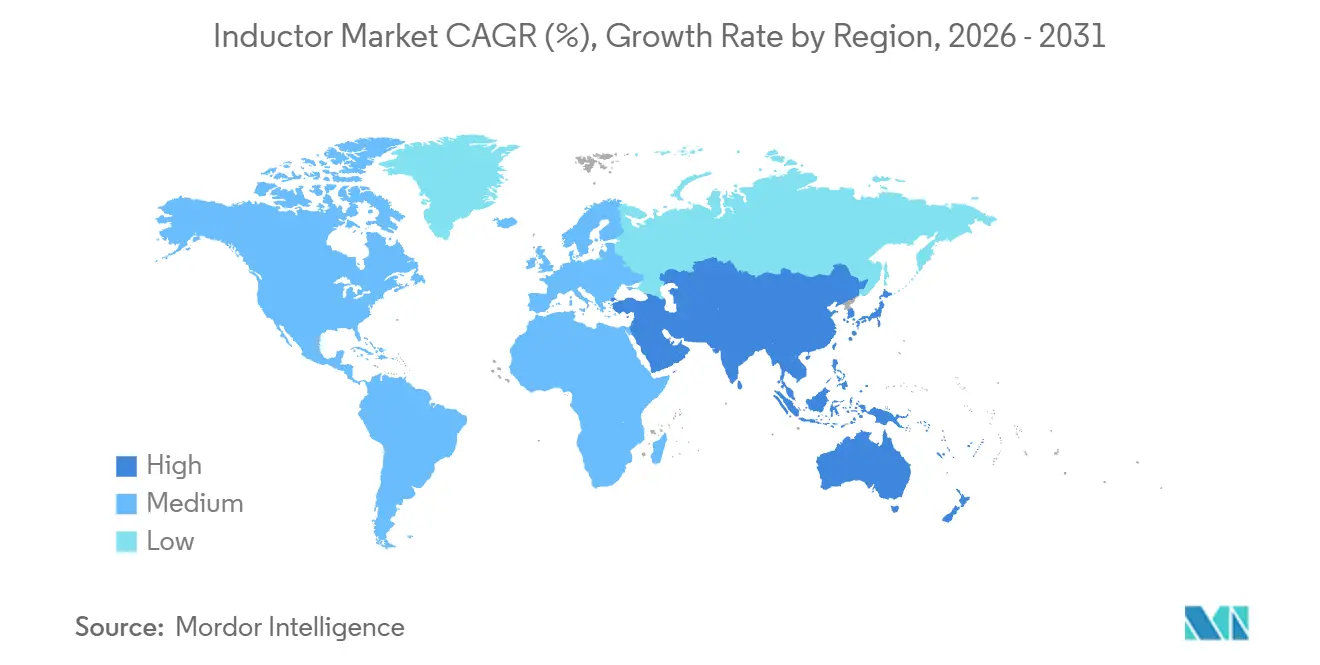

The Asia Pacific region held 36.23% of the 2025 revenue and is projected to advance at a 6.51% CAGR through 2031. China’s vertically integrated ferrite chain supplies 60% of global output, while Japan leads multilayer and thin-film manufacturing. South Korea integrates inductors within advanced packages for logic foundries, and Taiwan boosts capacity for high-current molded devices. India’s Production-Linked Incentive scheme attracted USD 1.2 billion to passive components in 2025, although inductor production still lags behind that of capacitors and resistors.

North America garnered a 24% share in 2025, driven by domestic EV tax credits and the expansion of edge-data-center footprints. U.S. suppliers specialize in custom wire-wound and coupled inductors for aerospace and medical sectors. Canada’s renewable buildout and Mexico’s vehicle assembly lines add steady baseline demand. Europe captured approximately 22% of the revenue, with automotive electrification, under the Fit for 55 package, and offshore wind projects driving the demand for high-power components.[4]European Commission, “Fit for 55 Package,” ec.europa.eu Germany anchors design activity, and Czech plants acquired by multinational vendors extend regional scale.

The Middle East and Africa remain emerging territories, with demand tied to hyperscale data centers and off-grid solar. Latin America follows Brazilian EV production and Argentine wind farms, but economic volatility dampens capital flows. These regional trends illustrate how manufacturing scale, policy incentives, and energy transitions shape the distribution of the global inductor market.

Note: Segment Growth Rate of all individual regions available upon report purchase

Competitive Landscape

The inductor market exhibits moderate consolidation, with the top five suppliers accounting for roughly 45% of the 2025 revenue, leaving ample room for niche challengers. Japanese and Taiwanese firms dominate multilayer and SMT categories through end-to-end ferrite synthesis and automated assembly. European and North American specialists defend wire-wound and aerospace-grade niches that require extensive qualification.

Patent filings for integrated magnetics and multiphase coupled coils increased 22% year-over-year to 320 grants in 2025, with TDK, Murata, and Infineon leading the way. Chinese vendors, such as Sunlord and Codaca, are leveraging domestic EV demand and cost advantages to gain market share, as evidenced by Sunlord’s 28% revenue surge in 2025. Strategic moves include co-location with wafer foundries for embedded inductors and partnerships between passive-component makers and wide-bandgap semiconductor houses.

Technology roadmaps emphasize DC resistance below 0.5 mΩ, self-resonance above 10 GHz, and embedded designs with a z-height of under 0.3 mm. Compliance hurdles such as AEC-Q200, IEC 60950, and MIL-PRF-27 extend qualification cycles to up to three years, shielding incumbents from rapid commoditization. Nevertheless, the quest for smaller, cooler, and quieter power stages keeps competitive pressure intense across the inductor market.

Inductor Industry Leaders

TDK Corporation

Murata Manufacturing Co. Ltd

Vishay Intertechnology Inc.

Panasonic Holdings Corporation

Taiyo Yuden Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: TDK broke ground on a USD 180 million thin-film inductor expansion in Akita, Japan, to triple monthly capacity for millimeter-wave and automotive radar parts.

- October 2025: Murata released a 150 °C-rated nanocrystalline power inductor qualified to AEC-Q200 Grade 0 for SiC traction inverters.

- September 2025: Vishay acquired a Czech specialty inductor firm for USD 85 million, adding high-power coupled inductor capabilities.

- August 2025: Samsung Electro-Mechanics reported KRW 420 billion (USD 315 million) in quarterly inductor revenue and earmarked KRW 150 billion (USD 112 million) for capacity expansion.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, we track the global inductors market as all factory-built passive components that store energy in a magnetic field, spanning power, RF/high-frequency, multilayer, coupled, thin-film, and molded constructions sold as finished surface-mount, through-hole, or embedded parts across every end-use vertical.

Scope exclusion: loose ferrite beads, cores sold without windings, and inductors already integrated inside transformers are left outside the study.

Segmentation Overview

- By Inductor Type

- Power Inductors

- RF/High-Frequency Inductors

- Coupled Inductors

- Multilayer Inductors

- Thin-Film Inductors

- Molded/Wire-Wound Inductors

- By Core Material

- Air/Ceramic Core

- Ferrite Core

- Iron and Metal-Alloy Core

- Nanocrystalline and Amorphous Core

- By Mounting Technique

- Surface-Mount Technology (SMT)

- Through-Hole Technology (THT)

- Embedded/Integrated PCB Inductors

- By Shielding

- Shielded

- Unshielded

- By Inductance

- Fixed Inductors

- Variable/Tunable Inductors

- By End-User Vertical

- Automotive

- Aerospace and Defense

- Communications and 5G Infrastructure

- Consumer Electronics and Computing

- Industrial and Power

- Healthcare and Medical Devices

- Renewable Energy Systems

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Rest of Asia Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with component engineers at contract manufacturers, sourcing leads at EV and 5G infrastructure OEMs, and regional distributors helped us validate average selling prices, qualification cycles (AEC-Q200), and lead-time swings that desk sources could not resolve. Feedback from Asia-Pacific and North American respondents ensured geographic nuances were captured.

Desk Research

Our analysts first mapped import-export traces for HS 850450 and related codes using portals such as UN Comtrade, ITC Trade Map, and China Customs, and then benchmarked shipment trends with quarterly production tallies from JEITA and IPC. Regulatory filings, public 10-Ks, and investor decks from leading passive component makers grounded price and mix shifts, while academic journals on wide-bandgap power electronics clarified frequency and thermal parameters that redefine inductor design windows. Paid data pulls from D&B Hoovers and Dow Jones Factiva supplemented competitive revenue splits. This list is illustrative; many additional open and subscription sources informed cross-checks.

Market-Sizing & Forecasting

We constructed a top-down model that rebuilds global demand from production and trade data, which is then sanity-checked through selective bottom-up rolls of sampled ASP × unit volumes gleaned from channel conversations. Key variables like smartphone output, EV production, 5G macro-site additions, average coil count per power module, and ferrite price movements drive both the historical base and a multivariate-regression forecast through 2030. Gaps in bottom-up granularity are bridged by normalized utilization factors derived from primary research.

Data Validation & Update Cycle

Outputs undergo variance scans against independent electronics indices before a senior analyst signs off, and reports refresh annually with interim revisions when material events (for example, copper price spikes) trigger re-runs.

Why Mordor's Inductors Baseline Commands Confidence

Published values often diverge because firms pick different component mixes, price assumptions, and refresh cadences.

Our disciplined scope and annual rebuild keep numbers aligned with real trade flows and live ASPs.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 11.28 bn (2025) | Mordor Intelligence | - |

| USD 6.00 bn (2023) | Global Consultancy A | excludes multilayer chips, uses 2023 ASPs frozen for forecast |

| USD 4.46 bn (2024) | Industry Analyst B | counts only power inductors, limited Asia trade validation |

The comparison shows how narrower scopes or static pricing compress totals, whereas Mordor's blended topology, live pricing loops, and yearly updates give decision-makers a balanced, transparent baseline they can reliably build on.

Key Questions Answered in the Report

What is the current size of the inductor market?

The global inductor market size reached USD 11.76 billion in 2026 and is forecast to grow to USD 14.47 billion by 2031.

Which segment is growing fastest in the inductor market?

Automotive applications are expanding at a 5.82% CAGR as electric-vehicle powertrains require significantly more inductors than combustion platforms.

Why are nanocrystalline cores gaining popularity?

Nanocrystalline alloys cut core loss at 1 MHz by more than 60% versus ferrite, making them ideal companions for GaN and SiC power stages.

How will 5G deployments influence inductor demand?

Each massive-MIMO 5G base station integrates hundreds of high-frequency inductors, supporting sustained demand as operators densify mid-band and millimeter-wave networks.

What are the main risks facing inductor suppliers?

Raw-material price volatility, particularly in copper and ferrite, plus thermal challenges in embedded designs, can squeeze margins and delay new product introductions.

Page last updated on: