Turbine Drip Oil Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

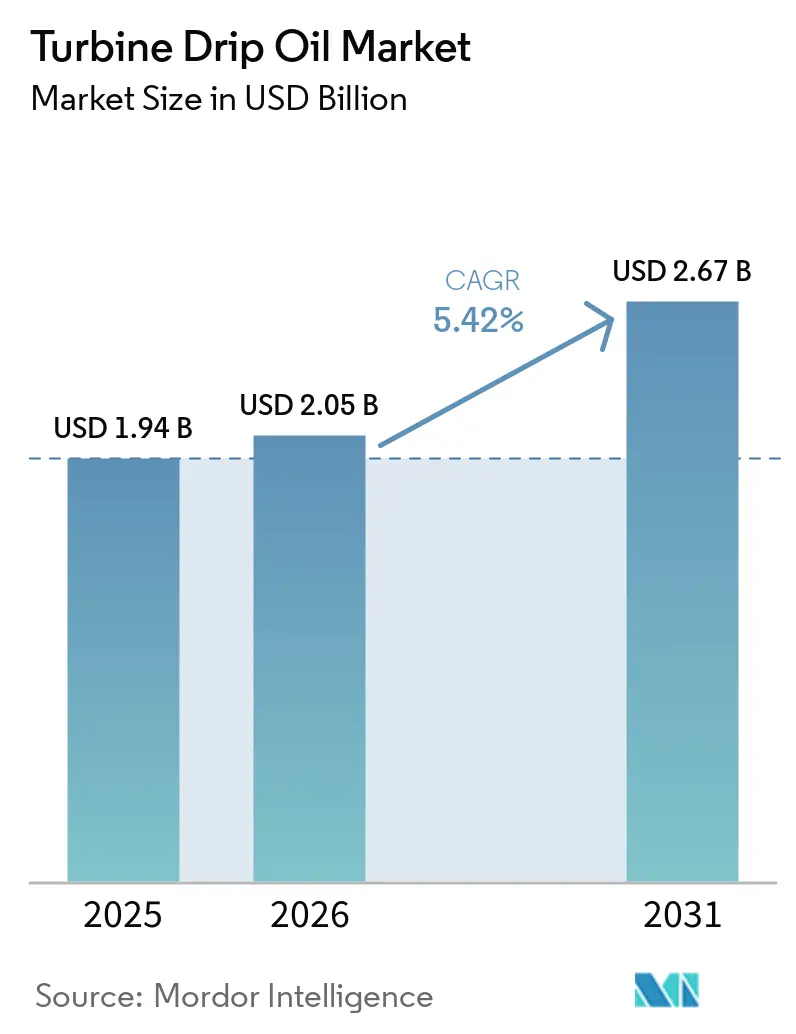

| Market Size (2026) | USD 2.05 Billion |

| Market Size (2031) | USD 2.67 Billion |

| Growth Rate (2026 - 2031) | 5.42% CAGR |

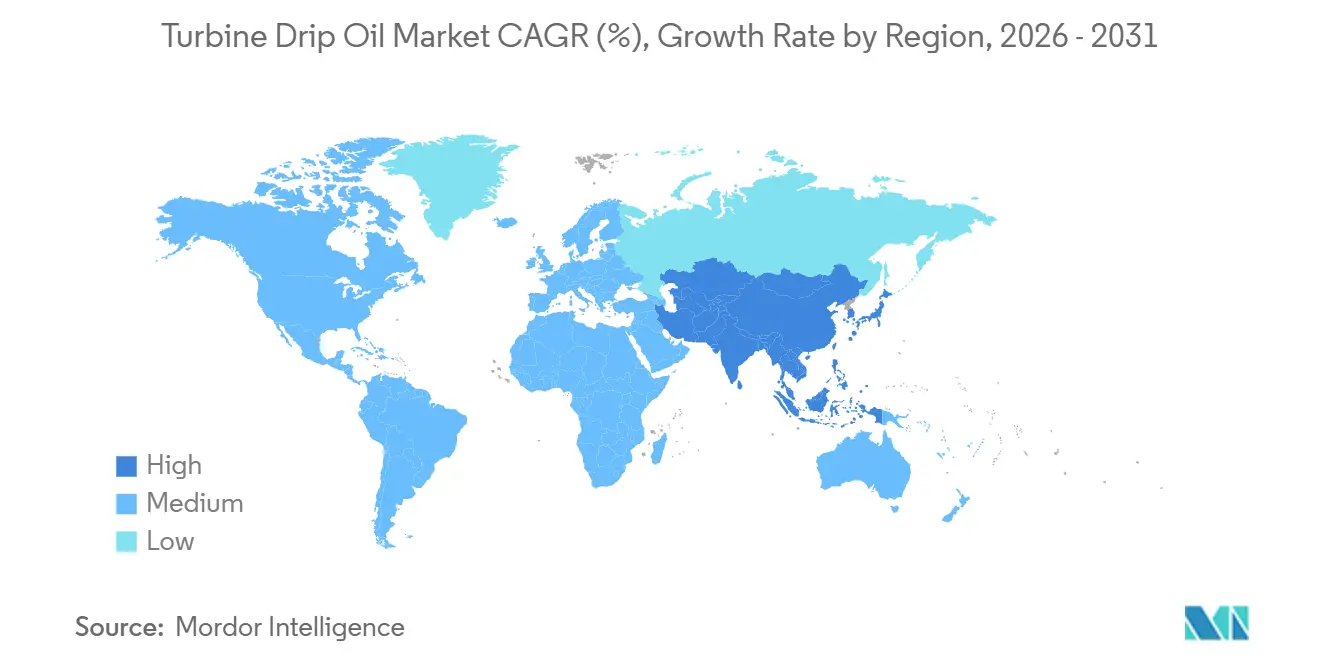

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

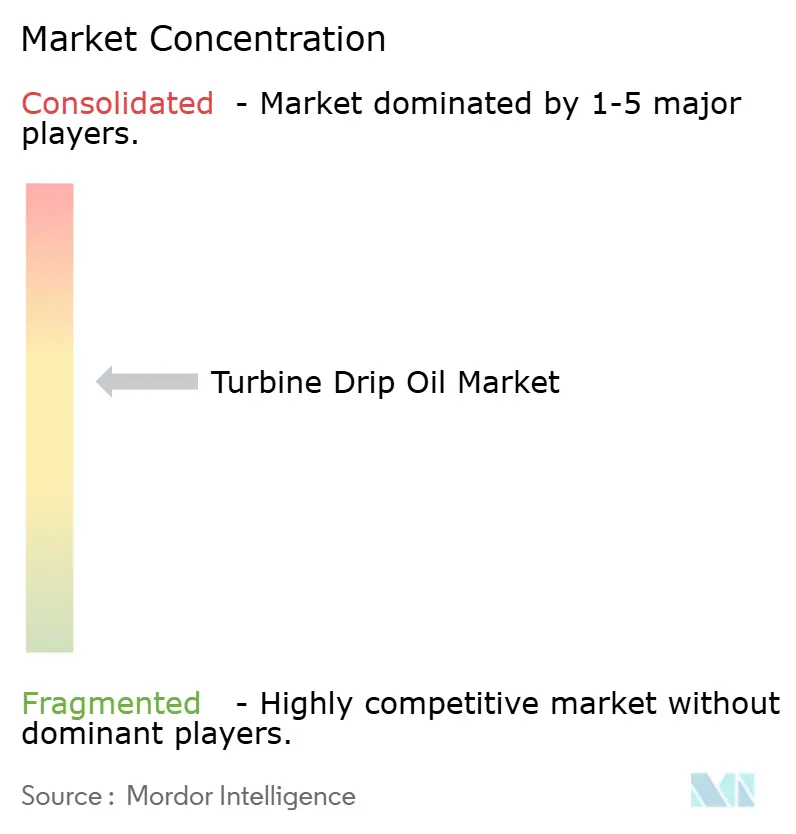

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Turbine Drip Oil Market Analysis by Mordor Intelligence

The Turbine Drip Oil Market size is projected to be USD 1.94 billion in 2025, USD 2.05 billion in 2026, and reach USD 2.67 billion by 2031, growing at a CAGR of 5.42% from 2026 to 2031. Demand stems from steam, gas, hydro and wind turbines as well as vertical turbine pumps used across power generation, oil and gas processing and industrial manufacturing.[1]Global Wind Energy Council, “Global Wind Report 2025,” gwec.net Energy-transition policies, LNG infrastructure buildouts and accelerated offshore-wind investment underpin volume growth even as coal retirements temper demand in OECD regions. OEM lubricant specifications are tightening around oxidation stability, demulsibility and varnish control, steering procurement toward Group III synthetics and bio-based formulations. Base-oil supply shocks such as the 2026 Pearl GTL outage continue to inject price volatility, but blenders with integrated refining positions can smooth cost swings and protect margin. Asia-Pacific anchors, global consumption owing to extensive thermal fleets, hydropower expansion and manufacturing CAPEX, while North America and Europe lead the shift to premium low-VOC and environmentally acceptable oils.

Key Report Takeaways

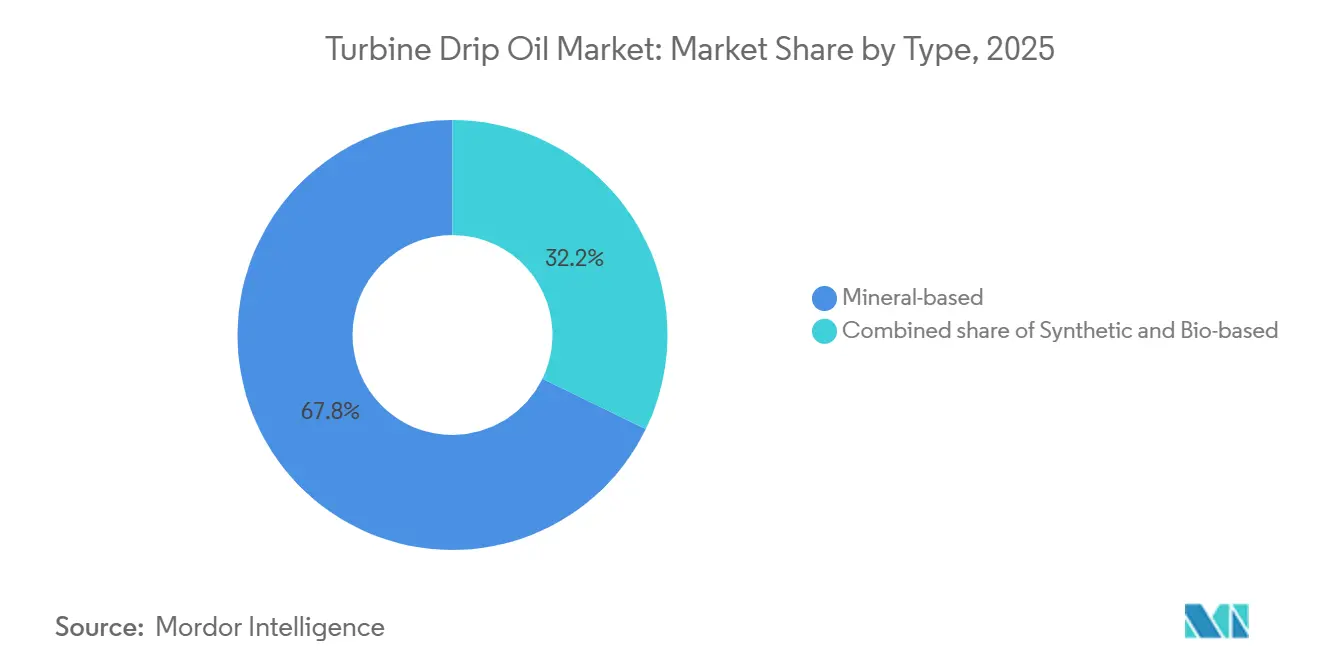

- By product type, mineral-based formulations accounted for 67.8% share of the turbine drip oil market size in 2025, and bio-based oils are growing at a 9.5% CAGR between 2026 and 2031.

- By viscosity grade, medium viscosity accounted for 49.1% share of the turbine drip oil market size in 202,5 and low viscosity is growing at a 7.4% CAGR between 2026-2031.

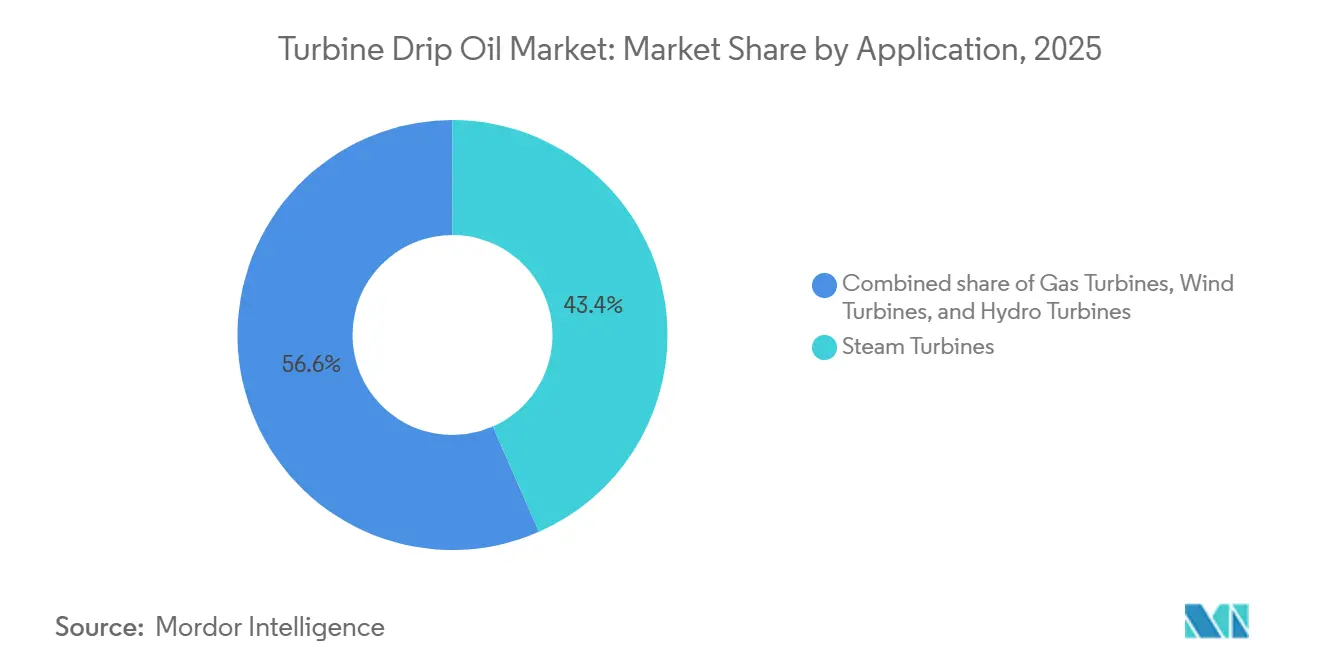

- By application, steam turbines led with 43.4% revenue share of the turbine drip oil market in 2025, whereas wind turbines are forecast to advance at an 8.7% CAGR to 2031.

- By end-user, power-generation utilities held 56.9% turbine drip oil market share in 2025; oil and gas recorded the highest projected CAGR at 6.8% through 2031.

- By geography, Asia-Pacific commanded 45.0% revenue in 2025 and is poised to expand at 6.3% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Turbine Drip Oil Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of Thermal & Hydro-Power Generation | +1.20% | Asia-Pacific core, spill-over Middle East & Africa | Medium term (2-4 years) |

| Demand from Industrial Turbines & Rotating Equipment | +0.90% | North America & Europe hubs, global adoption | Long term (≥ 4 years) |

| Industrial Expansion in Emerging Economies | +1.50% | India, ASEAN, Brazil, Middle East | Medium term (2-4 years) |

| Predictive-Maintenance-Driven Auto-Lubrication | +0.70% | North America & Europe early adopters | Long term (≥ 4 years) |

| OEM Shift to Premium Low-VOC Drip Oils | +0.60% | EU & North America leadership, global uptake | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growth of Thermal & Hydro-Power Generation

Lead times for H-class combined-cycle gas turbines now extend to 2030, reflecting a worldwide push to replace aging coal assets with high-efficiency gas units that reach about 60% thermal efficiency.[2]GE Vernova, “H-Class Orders and Projects,” gevernova.com New builds in Poland and the Dominican Republic will each consume premium ISO VG 46 drip oils designed for 16,000-hour drain intervals. Hydropower additions remain robust. China alone brought on 14.4 GW in 2024, maintaining demand for cost-effective ISO VG 46 mineral oils resistant to water ingress.[3]China Energy Portal, “Energy Statistics,” chinaenergyportal.org

Demand from Industrial Turbines & Rotating Equipment

Liquefaction plants, midstream compressor stations and refinery gas-compressor trains require rapid air-release oils (≤ 5 min per ASTM D3427) with viscosity indices above 140. Alaska LNG’s 800,000 HP refrigeration compressors and Venture Global’s Plaquemines Phase 2 expansion together translate into several hundred thousand liters of initial turbine oil fills.[4]Alaska LNG, “Project Overview,” alaskalnggasline.com Similar modernization programs at SaskEnergy and Energy Transfer demonstrate the upswing in synthetic ISO VG 32 consumption within North America’s gas grid.

Industrial Expansion in Emerging Economies

India’s USD 145 billion infrastructure outlay for fiscal 2025-2026 and rising manufacturing CAPEX are accelerating grid upgrades and distributed-generation installs, all of which require drip oils for auxiliary drives and feed pumps. ASEAN manufacturing clusters are likewise adopting localized mineral blends to avoid import duties, while Brazil’s irrigation pumps create steady ISO VG 32 demand under humid, tropical conditions, ANA.

Predictive-Maintenance-Driven Auto-Lubrication Adoption

IoT-enabled dispensers and machine-learning lubrication platforms cut unplanned turbine outages by about 15% and reduce oil consumption through precision dosing. Early adopters in wind farms report payback periods under 18 months thanks to avoided manual greasing rounds and extended drain intervals.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental & Safety Regulations | -0.80% | EU & North America strictest | Short term (≤ 2 years) |

| Shift Toward Renewable Energy Sources | -1.10% | Europe & North America lead | Long term (≥ 4 years) |

| Base-Oil Price Volatility & Supply Swings | -0.50% | Global, acute import-dependent regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Environmental & Safety Regulations

The EPA Vessel General Permit obliges stern-tube lubricants to exhibit > 90% biodegradability, pushing suppliers toward ester and PAG chemistries that cost up to twice conventional Group II oils. ECHA’s CLP rules classify certain untreated base stocks as carcinogenic, accelerating the shift to hydrotreated and synthetic alternatives in Europe. China’s GB 11120-2011 standard now requires viscosity indices ≥ 90 and flash points > 200 °C, phasing out low-quality mineral oils.

Shift Toward Renewable Energy Sources

Wind and solar captured the bulk of 2024 global capacity additions, trimming coal plant run-times and thereby reducing annual lubricant top-ups per installed megawatt. Although wind turbines are expanding at 8.7% CAGR, each nacelle holds only 200-400 L of oil compared with up to 15,000 L in a 500 MW steam unit, producing a structural headwind for overall volume demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Mineral Dominance With Accelerating Bio-Based Uptake

Mineral oils retained 67.8% share of the turbine drip oil market in 2025 on the back of favorable pricing, one-third to one-fifth of synthetic alternatives. These formulations deliver Turbine Oil Stability Test life of 2,000-4,000 h, adequate for hydro turbines and low-pressure steam units. Synthetics, while costlier, offer six-times-longer drain intervals and superior demulsibility, winning specifications in combined-cycle gas turbines. Bio-based oils, benefiting from EPA and EU ecolabel mandates, are advancing at 9.5% CAGR; trimethylolpropane ester research now yields viscosity indices near 160 and pour points below -40 °C.

By Viscosity Grade: Low-Viscosity Oils Gain Ground

Medium grades (ISO VG 32-68) still represent 49.1% of 2025 volume, but low-viscosity grades (ISO VG 15-32) are set to expand at 7.4% CAGR as OEMs chase energy-efficiency gains. Baker Hughes studies show that ISO VG 15-22 oils can cut mechanical losses by 5-15% versus ISO VG 32, translating to 0.3-0.5% plant-level fuel savings when natural-gas prices exceed USD 4 / MMBtu.

High-viscosity oils (ISO VG 100-150) are used in specialized applications like marine propulsion turbines and heavy-duty gearboxes, requiring thicker films to prevent metal-to-metal contact. Research by Baker Hughes and Eni showed VG 15-22 formulations reduce viscous losses by 5%-15% versus ISO VG 32, saving 0.3%-0.5% fuel in combined-cycle plants. Low-viscosity synthetics with viscosity indices above 140 are preferred for gas turbines, while wind turbines are shifting to ISO VG 130 oils to reduce grease use. Advanced additives and oxidation-stability testing ensure performance under thermal stress, meeting OEM requirements.

By Application: Wind Turbines Fastest Growing

Steam turbines delivered 43.4% of 2025 revenue owing to their large installed base and 8,000-15,000 L oil reservoirs. Gas turbines consume less per MW but mandate premium synthetics. Wind turbines contribute the quickest growth trajectory; 169 GW of global installations in 2025 underpin an 8.7% CAGR to 2031, albeit from smaller per-unit oil volumes.

The application landscape is diverging: legacy steam and hydro fleets in North America and Europe face retirement schedules (e.g., Germany's coal phase-out by 2030, 50% decline in U.S. coal capacity since 2010), reducing mineral oil demand. Asia-Pacific and Middle Eastern markets continue commissioning steam units operating through 2050. Combined-cycle gas turbines face rising capital costs and slowing orders. Wind turbines benefit from declining costs and policy support, ensuring installations through 2035. Agricultural irrigation in India, Brazil, and the U.S. drives demand for ISO VG 32 mineral oils, with California facing barriers to premium-efficiency pump adoption.

By End-User: Oil & Gas Leads Growth

Utilities held 56.9% of 2025 spend, locking in multi-year supply contracts with integrated majors. The oil and gas sector will record 6.8% CAGR through 2031 as LNG trains, gas-processing plants and midstream compressors adopt synthetic ISO VG 32 oils with 8,000-h drain intervals.

Manufacturing industries, including pulp and paper, mining, and food processing, use steam turbines for cogeneration and gas turbines for on-site power, requiring ISO VG 46 mineral oils for moderate thermal stress (60°C to 80°C). Marine and transportation sectors rely on turbine-driven systems for propulsion and auxiliary power, with EPA mandates driving environmentally acceptable lubricants. Mining operations use mineral-based oils with rust inhibitors for high-humidity environments. The "Others" category, including pulp and paper mills, is price-sensitive. Oil and gas electrification increases demand for lubricants, tolerating extreme temperatures and contamination.

Geography Analysis

Asia-Pacific commanded 45.0% revenue in 2025 and is projected to expand at 6.3% CAGR through 2031, supported by India's USD 145 billion infrastructure push and China's hydropower and wind roll-outs. Domestic capacity additions, combined with localized blending expansions by Indian Oil Corporation and ExxonMobil India, reinforce regional self-sufficiency in Group II and Group III output.

In North America and Europe, tight environmental regulations and decarbonization mandates stimulate demand for low-VOC synthetics and bio-based oils, but shrink volumes as coal fleets retire. LNG midstream investments and repowering of combined-cycle plants partially offset lost steam-turbine volumes.

Gulf petrochemical complexes require high-temperature synthetics, while Brazil's hydropower dominance sustains ISO VG 46 mineral demand. Argentina's Vaca Muerta pipeline projects and Egypt's gas-turbine additions present incremental, high-margin opportunities for suppliers with desert-climate lubricant portfolios. Saudi Arabia and the UAE are commissioning combined-cycle plants requiring premium synthetics for high temperatures and minimal maintenance. South Africa's aging coal fleet sustains mineral oil demand despite renewable energy efforts. Brazil's hydropower and wind sectors drive demand for ISO VG 46 oils and ISO VG 320 greases. Argentina's Vaca Muerta shale boosts synthetic oil use, while Egypt and Nigeria see incremental demand constrained by political and economic challenges.

Competitive Landscape

The turbine drip oil market is moderately concentrated: ExxonMobil, Shell, Chevron, TotalEnergies and Fuchs Petrolub are top players, leaving room for regional specialists such as Indian Oil Corporation, Bharat Petroleum, Sinopec Lubricants and ENEOS. Vertically integrated majors leverage captive Group III supply to hedge cost shocks, as illustrated by Shell rerouting Pearl GTL output internally after the 2026 outage. National oil companies are scaling base-oil capacity. HPCL’s Mumbai expansion will lift Group III output 61% by 2028 to reduce import dependence.

Technological differentiation centers on additive chemistry: ashless dispersants, advanced anti-wear compounds and foam suppressants that meet OEM varnish-control targets. Quaker Houghton and Petronas Lubricants are disrupting with OEM-approved ISO VG 15-22 blends and palm-oil-based bio-esters, respectively. Digital service bundles that couple oil-condition monitoring with just-in-time delivery are emerging as value-lock mechanisms, cutting customer inventory by up to 30% and boosting supplier stickiness.

OEM homologation remains a key barrier. GE Vernova’s GEK series, Siemens Energy’s TLV 9013 and Alstom’s HTGD 90 117 demand multi-year compatibility testing, favoring incumbents with established field-service networks. Standards bodies ASTM D4304, ISO 8068 and DIN 51515 provide baseline performance, yet proprietary OEM overlays ensure brand differentiation and sustain premium pricing.

Turbine Drip Oil Industry Leaders

ExxonMobil Corporation

Royal Dutch Shell plc

Chevron Corporation

TotalEnergies SE

Fuchs Petrolub SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Shell’s Pearl GTL facility damage curtailed Group III supply, elevating spot prices by about USD 2 / gal and tightening availability across Asia-Pacific.

- December 2025: SaskEnergy completed a CAD 60 million Unity compressor station upgrade, switching to Group III synthetics and doubling drain intervals.

- January 2025: Indian Oil Corporation began trial runs at its 672,000 tpa Manali lube complex, targeting eco-friendly transformer oils and premium turbine grades.

- November 2024: HPCL advanced a USD 551 million Mumbai refinery modernization to expand Group II+ and Group III base-oil output by 2028.

Global Turbine Drip Oil Market Report Scope

Turbine drip oil is a light-bodied lubricating oil specifically formulated for continuous, gravity-fed lubrication of bearings in vertical turbine pumps. Unlike conventional turbine oils used in closed-loop systems, drip oil is dispensed drop-by-drop to safeguard line shaft bearings, particularly in deep-well applications such as agricultural irrigation and municipal water systems.

The Turbine Drip Oil Market is segmented into type, viscosity grade, application, end-user, and geography. By type, the market is segmented into mineral-based, synthetic, and bio-based turbine drip oils. By viscosity grade, the market is segmented into low, medium, and high viscosity grades. By application, the market is segmented into steam turbines, gas turbines, wind turbines, and hydro turbines. By end-user, the market is segmented into power generation utilities, oil and gas, manufacturing, marine and transportation, and other end-user industries. The report also covers the market size and forecasts for the turbine drip oil market across major regions, including North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Mineral-based |

| Synthetic |

| Bio-based |

| Low Viscosity |

| Medium Viscosity |

| High Viscosity |

| Steam Turbines |

| Gas Turbines |

| Wind Turbines |

| Hydro Turbines |

| Power Generation Utilities |

| Oil and Gas |

| Manufacturing |

| Marine and Transportation |

| Others (Mining, Pulp and Paper) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Mineral-based | |

| Synthetic | ||

| Bio-based | ||

| By Viscosity Grade | Low Viscosity | |

| Medium Viscosity | ||

| High Viscosity | ||

| By Application | Steam Turbines | |

| Gas Turbines | ||

| Wind Turbines | ||

| Hydro Turbines | ||

| By End-user | Power Generation Utilities | |

| Oil and Gas | ||

| Manufacturing | ||

| Marine and Transportation | ||

| Others (Mining, Pulp and Paper) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What was the turbine drip oil market size in 2026 and what CAGR is expected to 2031?

The turbine drip oil market size reached USD 2.05 billion in 2026 and is forecast to grow at a 5.42% CAGR to USD 2.67 billion by 2031.

Which application segment is expanding fastest through 2031?

Wind turbines are projected to grow at an 8.7% CAGR, the fastest among all application segments.

Why are low-viscosity turbine oils gaining popularity?

OEM studies show ISO VG 15-22 oils can trim mechanical losses by up to 15% and deliver 0.3-0.5% fuel savings in combined-cycle plants when gas prices exceed USD 4 / MMBtu.

Which region leads global consumption?

Asia-Pacific commanded 45.0% of 2025 revenue and is set to expand at 6.3% CAGR through 2031 due to large thermal fleets and infrastructure CAPEX.

What regulatory trends are reshaping product formulations?

EPA Vessel General Permit and EU ecolabel criteria are driving adoption of biodegradable, low-VOC oils that meet stringent oxidation-stability and demulsibility thresholds.

Page last updated on: