Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

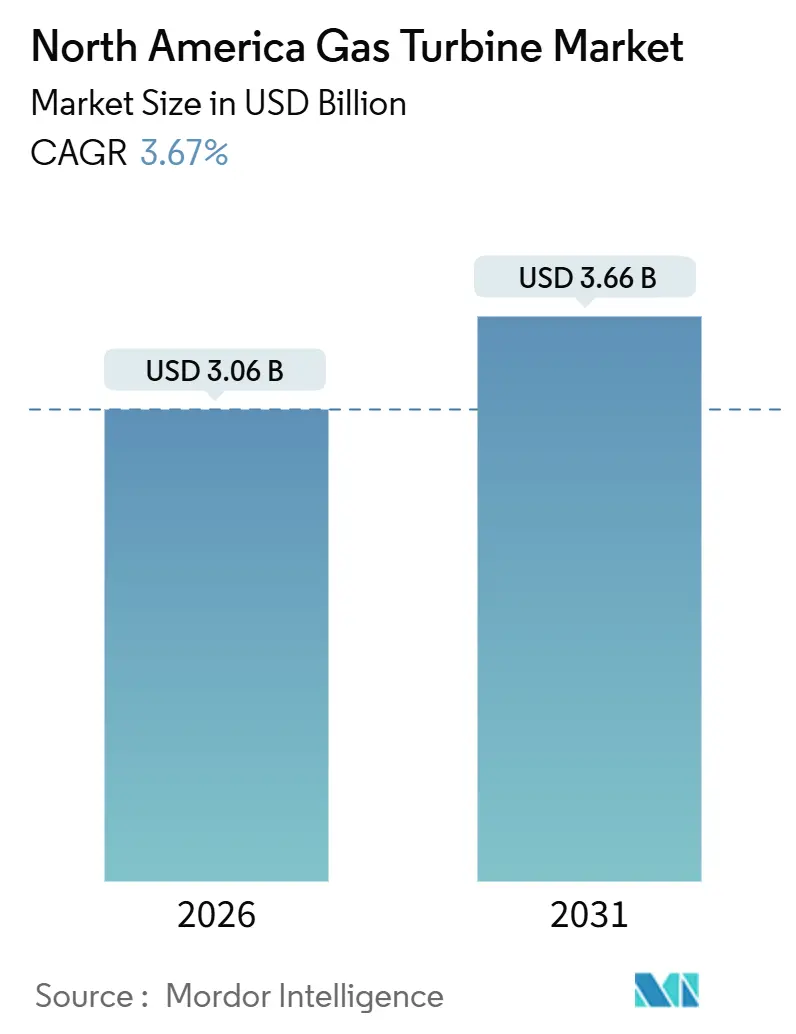

| Market Size (2026) | USD 3.06 Billion |

| Market Size (2031) | USD 3.66 Billion |

| Growth Rate (2026 - 2031) | 3.67% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Gas Turbine Market Analysis by Mordor Intelligence

The North America Gas Turbine Market size is estimated at USD 3.06 billion in 2026, and is expected to reach USD 3.66 billion by 2031, at a CAGR of 3.67% during the forecast period (2026-2031).

Utilities and independent power producers are pivoting from baseload deployment toward fast-ramping roles that backstop renewable variability and protect data-center uptime. Ample shale-gas output keeps Henry Hub prices near USD 3.22 per MMBtu in 2025, preserving a decisive fuel-cost edge over liquid alternatives and sustaining combined-cycle dispatch economics.[1]U.S. Energy Information Administration, “Short-Term Energy Outlook,” eia.gov Section 45V hydrogen production tax credits under the Inflation Reduction Act are already pulling forward orders for turbines certified to co-fire hydrogen blends.[2]U.S. Department of Energy, “Inflation Reduction Act Guidebook,” energy.gov Meanwhile, battery-storage price declines compel OEMs to sharpen peaker economics, integrate digital-twin analytics, and certify cycle efficiency improvements. Finally, supply-chain bottlenecks for large nickel-alloy forgings have lengthened delivery schedules for heavy-duty frames, prompting buyers to favor modular aeroderivative models that can be installed in phases.

Key Report Takeaways

- By operating cycle, combined-cycle units held 71.1% of the North America gas turbine market share in 2025, while simple-cycle configurations are advancing at a 5.3% CAGR through 2031.

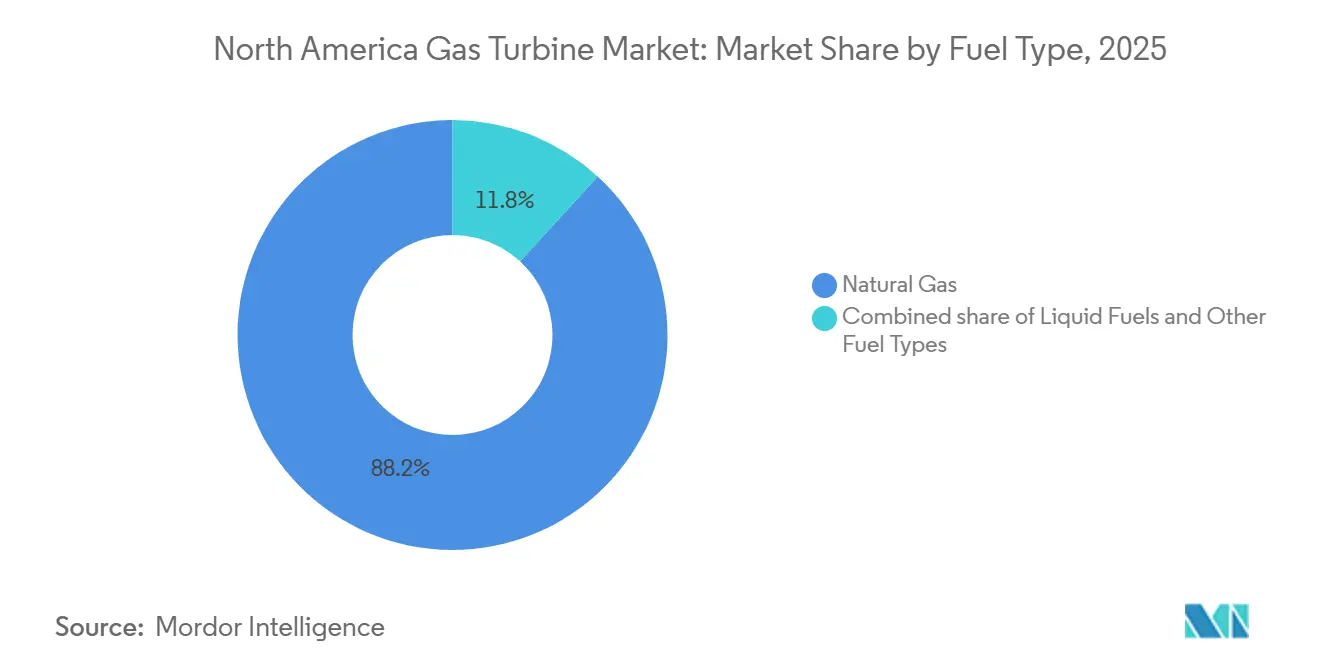

- By fuel type, natural gas accounted for 88.2% of the North America gas turbine market size in 2025; alternative fuels led by hydrogen and biogas are forecast to expand at a 9.9% CAGR to 2031.

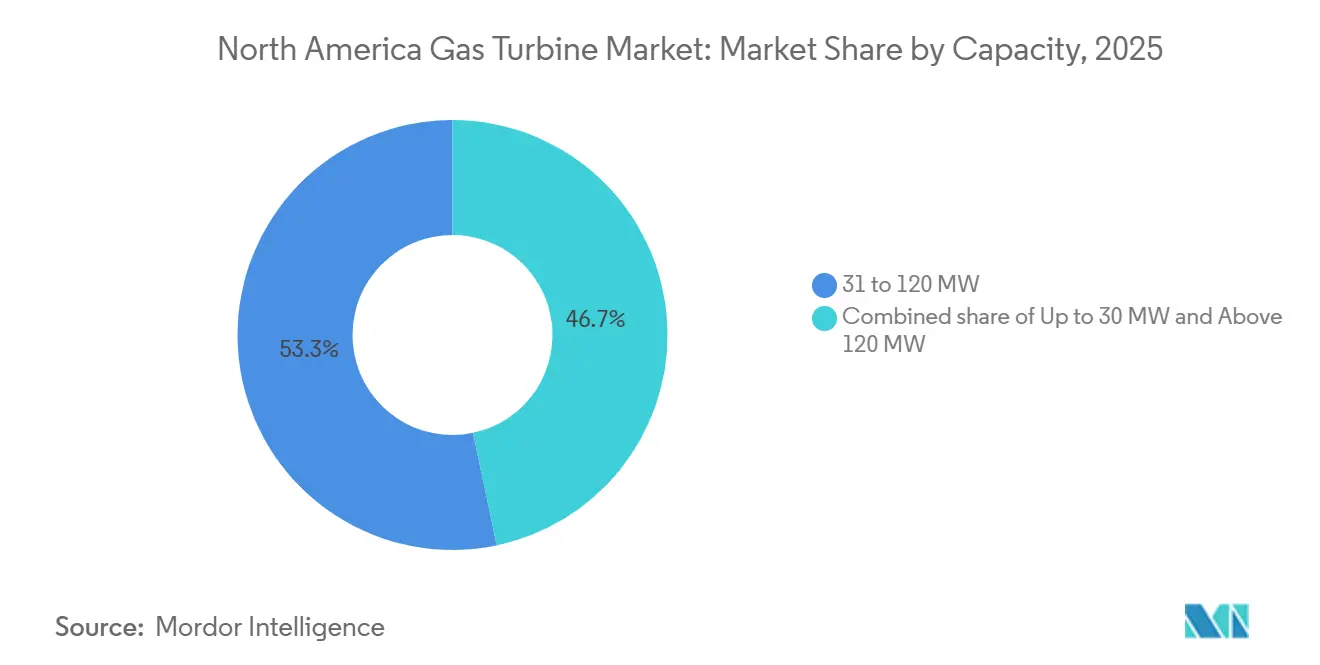

- By capacity bracket, turbines rated 31–120 MW captured 53.3% of the North America gas turbine market in 2025, whereas units above 120 MW are projected to grow at a 4.5% CAGR through 2031.

- By end user, the power-generation sector commanded 62.9% revenue share in 2025; oil-and-gas applications are on course for a 5.0% CAGR through 2031.

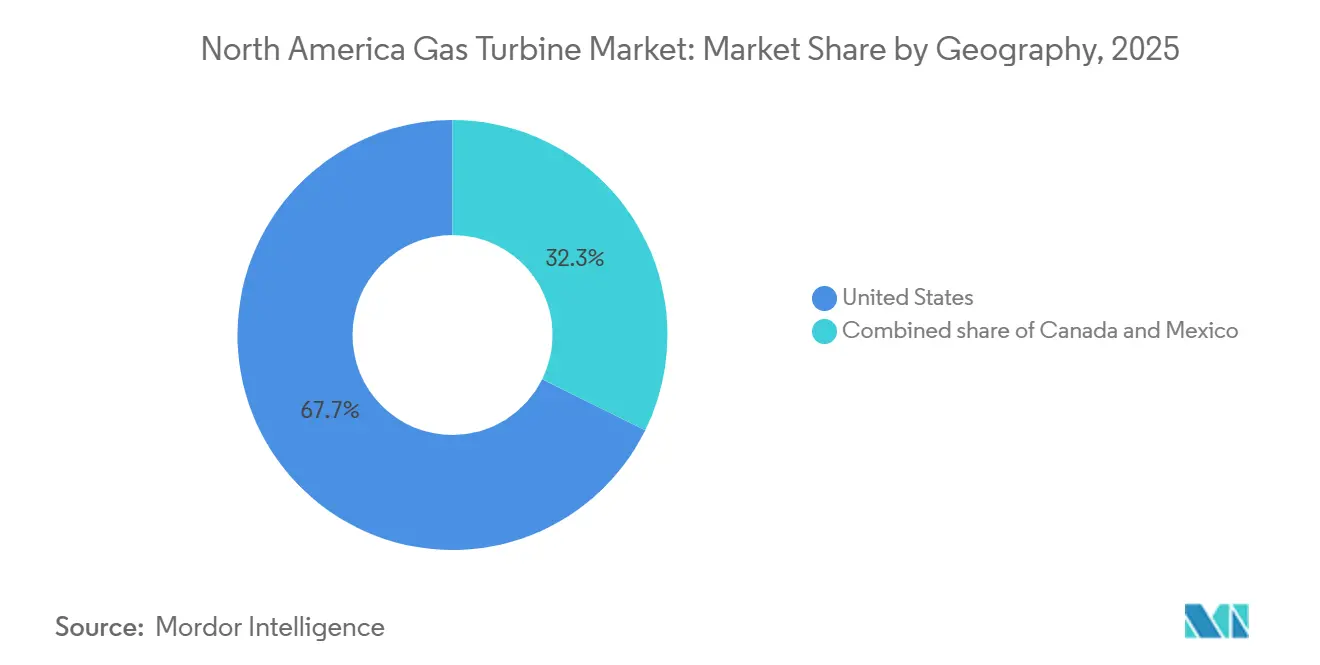

- By geography, the United States dominated with a 67.7% share in 2025 and is forecast to rise at a 4.1% CAGR to 2031.

- GE Vernova, Siemens Energy, and Mitsubishi Power together controlled more than half of utility-scale orders in 2025, underscoring a concentrated supplier landscape.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Gas Turbine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Abundant shale-gas supply keeps fuel costs low | +0.6% | United States basins with spillover to Canada and Mexico | Long term (≥ 4 years) |

| Rising renewable penetration drives fast-ramping capacity needs | +0.9% | United States ERCOT, CAISO, SPP; Canada Alberta, Ontario | Medium term (2-4 years) |

| Coal-to-gas fleet replacement programs | +0.7% | U.S. Southeast and Midwest | Medium term (2-4 years) |

| Data-center and AI load surges create local capacity deficits | +0.8% | U.S. Virginia, Texas, Oregon, Arizona | Short term (≤ 2 years) |

| IRA hydrogen-tax-credit pull-through for H₂-ready turbines | +0.5% | U.S. Gulf Coast and Intermountain West hubs | Long term (≥ 4 years) |

| Predictive-analytics upgrades lowering lifetime LCOE | +0.4% | North America, led by U.S. and Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Renewable Penetration Drives Fast-Ramping Capacity Needs

Cumulative U.S. wind and solar capacity reached 295 GW in 2024, compelling grid operators to maintain generators that can ramp from zero to full load in under 10 minutes. ERCOT’s operating-reserve demand curve prices scarcity events above USD 5,000 per MWh, rewarding aeroderivative turbines such as GE Vernova’s LM2500XPRESS that can achieve full output within five minutes.[3]Electric Reliability Council of Texas, “Operating Reserve Demand Curve Methodology,” ercot.com PJM Interconnection applies a similar valuation to fast-start resources after its 2025/2026 auction reforms lifted clearing prices to USD 269.92 per MW-day.[4]PJM Interconnection, “2025/2026 Base Residual Auction Report,” pjm.com The International Energy Agency projects that grids surpassing 40% renewable penetration need dispatchable reserves equal to at least 15% of peak load, a threshold already exceeded in California. Consequently, simple-cycle and open-cycle installations, despite lower thermal efficiency, gain prominence because their capital cost per MW of peaking capacity is 30%-40% below combined-cycle equivalents.

Data-Center & AI Load Surges Creating Local Capacity Deficits

Hyperscale and AI-training facilities consumed roughly 50 TWh in 2024 and continue to grow, often outpacing local grid headroom. A December 2024 order for 29 GE Vernova LM2500XPRESS units illustrates how data-center operators procure on-site fast-start generation to guarantee uptime. Loudoun County, Virginia, saw utilities file for 2.3 GW of new interconnection capacity in 2024, much of it earmarked for gas-fired combined heat and power that can island during disturbances. Similar procurement patterns appear in Texas, where real-time price volatility encourages behind-the-meter deployment. The shift toward modular arrays values dual-fuel capability, black-start readiness, and rapid installation over absolute heat-rate performance.

IRA Hydrogen-Tax-Credit Pull-Through for H₂-Ready Turbines

Final Section 45V regulations published in December 2024 offer up to USD 3.00 per kg incentive for near-zero-carbon hydrogen, accelerating orders for turbines certified to co-fire or eventually burn 100% hydrogen. The 485-MW Long Ridge Energy Terminal is already hydrogen-capable, while Utah’s Intermountain Power Project is installing Mitsubishi Power M501JAC turbines designed for 30% hydrogen blending. GE Vernova and Siemens Energy both list multiple heavy-duty frames with 100% hydrogen certificates. Temporal-matching rules that link electrolyzer output to turbine demand favor projects co-located with renewables or nuclear plants, nudging geographic clustering in hydrogen hubs.

Predictive-Analytics Upgrades Lowering Lifetime LCOE

OEMs embed digital-twin platforms to cut forced outages and extend hot-gas-path intervals. GE Vernova’s suite predicts component degradation six to eight weeks ahead, enabling maintenance when demand is low and avoiding capacity penalties. Siemens Energy’s Omnivise analytics report 20%-30% reductions in unplanned downtime, translating into meaningful margin protection for peaking units compensated through capacity markets. IEEE 2025 case studies show predictive maintenance lowers O&M costs by USD 2-4 per MWh, reducing lifetime LCOE by up to 8% when compounded. As regulators scrutinize cost recovery, software-enabled reliability is becoming a decisive bid parameter.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Falling battery-storage costs undermine new gas peakers | -0.5% | U.S. California, Texas, New York | Short term (≤ 2 years) |

| Tightening net-zero regulations on fossil assets | -0.4% | U.S. California, New York, Washington; Canada British Columbia, Quebec | Long term (≥ 4 years) |

| Supply-chain bottlenecks for forgings and nickel alloys | -0.3% | Global, acute in U.S. and Canada | Medium term (2-4 years) |

| ERCOT & PJM capacity-price volatility | -0.2% | U.S. Texas and Mid-Atlantic | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Falling Battery-Storage Costs Undermine New Gas Peakers

Utility-scale lithium-ion prices continue to decline and are expected to cross the cost-parity threshold with 4-hour simple-cycle turbines in 2026, according to U.S. Department of Energy trend analyses. California ISO has already contracted more than 6 GW of storage, displacing planned gas peakers, and ERCOT added 4.2 GW in 2024. Batteries offer instantaneous response and qualify for investment tax credits, eroding the earnings outlook for assets that rely primarily on scarcity pricing. Yet limitations in duration and grid-forming capability still leave a reliability niche for synchronous gas turbines, especially for events exceeding four hours or requiring inertial support. OEMs counter by marketing hydrogen-ready burners and carbon-capture retrofit kits to differentiate against storage.

Tightening Net-Zero Regulations on Fossil Assets

California’s Senate Bill 100 mandates 100% clean electricity by 2045, effectively shortening the economic life of new gas turbines unless they can demonstrate renewable-fuel or carbon-capture pathways. New York’s Climate Leadership and Community Protection Act sets a similar trajectory, adding emissions-credit costs that raise dispatch break-even prices. Washington’s cap-and-invest program imposes allowance costs expected to add USD 10-15 per MWh by 2030. Canada’s proposed Clean Electricity Regulations require net-zero generation by 2035, intensifying the risk of stranded assets. Developers in policy-aggressive regions increasingly demand shorter payback periods and flexible designs that can pivot to hydrogen or carbon capture.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Capacity: Mid-Range Dominance Meets Large-Turbine Acceleration

North America gas turbine market size for the 31–120 MW class reached USD 1.58 billion in 2025, representing a 53.3% share. The segment thrives on standardized engineering, compressed lead times, and suitability for both grid-connected and behind-the-meter customers. Industrial manufacturers adopt mid-range units for combined heat and power, while midstream gas operators use similar frames for compression stations. A second-order effect is risk mitigation: buyers can phase in capacity, limiting exposure to fuel-price swings and policy shifts. Maintenance intervals are shorter than those for microturbines, yet rebuilding costs remain manageable relative to heavy-duty frames.

Units above 120 MW, though smaller in count, are recording a 4.5% CAGR through 2031, a rate likely to lift their North America gas turbine market share to just under 30% by the end of the forecast horizon. Coal-to-gas replacement projects in the U.S. Southeast and Midwest predominantly adopt this size class because individual plants must replicate gigawatt-scale retiring baseload capacity. Duke Energy’s 2024 coal retirements in the Carolinas triggered procurement of new GE Vernova HA-class turbines rated at 826 MW in combined-cycle configuration. Supply-chain stress for nickel-based superalloys exposes this class to longer lead times, prompting OEMs to vertically integrate forging capacity.

By Operating Cycle: Efficiency Versus Flexibility Trade-Offs

Combined-cycle configurations commanded 71.1% of 2025 revenue, equal to USD 2.11 billion, confirming the cost-of-fuel advantage derived from 60%-plus thermal efficiency. The operating cycle’s higher capital intensity is offset by strong capacity factors under moderate gas prices, making it the preferred choice for utilities with mid-merit dispatch profiles. Recent builds pair gas turbines with supplementary duct firing and advanced HRSG designs, extracting incremental megawatts when reserve margins tighten.

Simple-cycle and open-cycle installations grow faster, at a 5.3% CAGR, even though their efficiency penalty can exceed 15 percentage points. The North America gas turbine market size for simple-cycle peakers is forecast to touch USD 1.25 billion by 2031 as capacity markets revise valuation for ramp speed and start reliability. ERCOT’s 2024 scarcity events highlighted revenue upside for assets capable of reaching nameplate in under ten minutes. Grid operators now procure portfolios that segment by duty cycle, combined-cycle for shoulder periods, and simple-cycle for peaks, rather than forcing one technology to cover all load shapes.

By Fuel Type: Natural Gas Lock-In and the Hydrogen Frontier

Natural gas remained dominant with an 88.2% share of 2025 installations, yet alternative fuels registered the steepest trajectory. For example, the Intermountain Power Project will commission hydrogen-capable M501JAC turbines in 2026, blending 30% hydrogen by volume. Pipeline infrastructure and transparent hub pricing lend natural gas an enduring appeal, but developers in California and the U.S. Northeast increasingly seek purchase agreements that allow cost pass-through for hydrogen or renewable natural gas.

The “other fuels” category, hydrogen, biogas, and synthetic e-fuels, grows at a 9.9% CAGR, a pace that could elevate its North America gas turbine market size to above USD 400 million by 2031. Federal tax incentives offset the high energy-density penalty of hydrogen, while landfill-gas-to-energy schemes underpin early biogas uptake. Combustor redesign to mitigate hydrogen flame speed and NOx formation is the central R&D challenge; GE Vernova’s 2024 patent for a hydrogen-optimized liner addresses exactly this issue.

By End-User Industry: Power-Generation Core, Oil-&-Gas Uptick

Power-generation entities consumed 62.9% of 2025 shipments, equivalent to USD 1.87 billion. Coal retirements remain the headline driver, especially where existing transmission and cooling infrastructure can be repurposed for combined-cycle replacements. Dispatchable reserve requirements tied to renewable penetration also support gas-turbine adoption among vertically integrated utilities.

Oil-and-gas operators demonstrate quicker expansion, clocking a 5.0% CAGR through 2031. LNG export terminals on the U.S. Gulf Coast need aeroderivative turbines for cryogenic compression, while Permian Basin midstream lines require incremental capacity as daily crude output exceeds 6 million barrels. Offshore platforms in the Gulf of Mexico replace aging turbines with more efficient models to reduce fuel burn and emissions, aligning with tightening air-quality rules.

Geography Analysis

The United States accounted for 67.7% of 2025 revenue and is forecast to expand at 4.1% CAGR to 2031 as coal-to-gas conversions and data-center load booms compound. PJM’s 2025/2026 auction clearing price of USD 269.92 per MW-day materially improves project viability for peaking assets. ERCOT’s revised reserve demand curve similarly elevates the business case for fast-start aeroderivative fleets. Section 45V tax credits steer hydrogen-ready orders toward Gulf Coast hubs, while shale-gas production exceeding 108.5 bcf/d preserves the fuel-cost advantage.

Canada’s market hinges on Alberta’s gradual coal phase-out and Ontario’s need for peaking capacity during multi-year nuclear refurbishments. The federal Clean Electricity Regulations propose net-zero fossil generation by 2035, compressing asset payback windows and persuading developers to negotiate carbon-capture readiness clauses. Provinces rich in hydro resources, notably British Columbia and Quebec, rely on gas turbines mainly for industrial cogeneration and remote microgrids.

Mexico remains driven by Comisión Federal de Electricidad procurement, especially combined-cycle plants in the northeast that benefit from new cross-border pipelines such as the Sur de Texas-Tuxpan system. Imports of U.S. pipeline gas, historically 20%-30% cheaper than domestic supply, anchor the North America gas turbine market growth in the region. Policy shifts have slowed private investment, but CFE’s 2024-2030 plan still includes roughly 3 GW of new gas-fired capacity to displace costlier fuel-oil units.

Regulatory Landscape

In the United States, stationary combustion turbines are governed under the U.S. Environmental Protection Agency (EPA) New Source Performance Standards (NSPS). The EPA finalized amendments to the NSPS for stationary combustion and stationary gas turbines on January 9, 2026 (published January 15, 2026), updating 40 CFR part 60, subpart KKKKa and creating new subcategories for new, modified, or reconstructed turbines based on size, utilization, design efficiency, and fuel type.

The revised NSPS applies to affected sources constructed, modified, or reconstructed after December 13, 2024, tightening alignment between permitting timelines and subcategory-specific NOx limits, along with documentation and testing requirements. For certain turbine subcategories, the rule identifies selective catalytic reduction (SCR) combined with combustion controls as the best system of emission reduction for NOx. It also introduces a dedicated subcategory for stationary temporary combustion turbines with a 25 ppm NOx standard when firing natural gas, shaping how fast-deployable and modular turbine packages are designed for compliance in reliability and behind-the-meter applications.

Competitive Landscape

Utility-scale segments of the North America gas turbine market display high concentration: GE Vernova, Siemens Energy, and Mitsubishi Power collectively capture well above 50% of heavy-duty frame orders, leveraging dense installed bases, bundled long-term service contracts, and readiness certifications for hydrogen blends. GE Vernova’s January 2025 multi-year agreement covering more than 40 HA-class turbines embeds its Digital Power Plant analytics, raising customer switching costs.

Distributed generation and oil-and-gas niches are more contestable. Solar Turbines excels with mid-range aeroderivatives, while Capstone Green Energy delivers sub-megawatt microturbines that can island critical loads. Wärtsilä Energy’s gas-engine plants, recently contracted for 400 MW across Texas, target ERCOT scarcity pricing events with flexible, modular blocks.

Technology differentiation intensifies. Siemens Energy’s Omnivise platform claims up to 30% downtime reduction, and Mitsubishi Power’s M501JAC arrives factory-certified for 30% hydrogen, giving it a first-mover edge in Section 45V projects. Patent filings in additive manufacturing of hot-gas-path components and advanced combustion controls suggest ongoing R&D investment aimed at mitigating supply-chain constraints and increasing fuel flexibility.

North America Gas Turbine Industry Leaders

GE Vernova

Siemens Energy

Mitsubishi Power Americas

Solar Turbines (Caterpillar)

Capstone Green Energy

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term whitespace is forming around fast-start, modular aeroderivative packages and turnkey expansions that can be permitted and installed faster than large heavy-duty frames, particularly where reserve margins tighten alongside renewable variability and data-center driven load additions. A concrete example is Lincoln Electric System selecting GE Vernova in February 2026 to supply two LM6000VELOX aeroderivative packages for Nebraska's Terry Bundy Generating Station expansion (100 MW), reinforcing demand for quick-start capacity additions that fit constrained interconnection timelines and local reliability needs.

Large combined-cycle project activity also continues to anchor procurement, while supply-chain tightness is pushing buyers to lock in EPC capacity and long-lead turbine slots earlier in project development. Basin Electric Power Cooperative's 1.5 GW Bison Generation Station in North Dakota (general contractor selection reported in February 2026) and the start of construction for the 600 MW Wolf Summit Energy facility in West Virginia in April 2026 highlight continued investment in dispatchable gas generation tied to system reliability and regional industrial and commercial demand growth. Alongside these builds, hydrogen-ready and emissions-compliant configurations create additional specification-driven opportunity, as buyers align turbine selections with finalized US emissions requirements and fuel-flexible pathways supported by federal incentives such as Section 45V.

Recent Industry Developments

- July 2026: Aecon won a CAD 1.2 billion EPC contract for the Greenlight Electricity Centre in Alberta, a combined-cycle project featuring two Siemens Energy SGT6-8000H gas turbines. The award points to continued investment in high-efficiency CCGT builds to supply dispatchable power, supporting OEM and EPC backlogs for large-frame turbines and related long-term service demand in Canada.

- May 2026: GE Vernova reported its HA gas turbine fleet surpassed 4 million commercial operating hours, spanning 128 units across 21 countries. The milestone supports buyer confidence in HA-class maturity for combined-cycle deployments and reinforces the service-led competitive dynamic in North America where installed-base performance and long-term agreements influence procurement.

- August 2024: Atura Power selected Mitsubishi Power Americas to supply an M501JAC hydrogen-ready combustion turbine for the Napanee Generating Station Expansion in Ontario, adding 430 MW in simple-cycle operation. The order reflects procurement preference for hydrogen-capable designs in provinces managing capacity needs during system transitions and provides a reference project for fuel-flexible turbine specifications in Canada.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated from gas turbine equipment supplied for power and industrial use across North America, including sales tied to new installations and planned replacement activity that is ordered as part of a project.

Scope exclusions: It does not count standalone long-term MRO service revenue, minor spare parts sold outside project scopes, or turbine use in aircraft applications.

Segmentation Overview

- By Capacity

- Up to 30 MW

- 31 to 120 MW

- Above 120 MW

- By Operating Cycle

- Combined Cycle

- Simple/Open Cycle

- Cogeneration/CHP

- By Fuel Type

- Natural Gas

- Liquid Fuels (Diesel/Kerosene/LPG)

- Other Fuel Types (Hydrogen, Biogas)

- By End-User Industry

- Power

- Oil and Gas

- Other End-user Industries (Industrial, Marine)

- By Geography

- United States

- Canada

- Mexico

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting map of demand centers and to pin down how turbine orders are typically reported in public sources. We relied on open, reputable references such as the US Energy Information Administration for generation and capacity context, the US International Trade Commission data for trade signals, Statistics Canada for industrial and energy indicators, and Mexico energy agencies and grid publications for project pipelines and policy context. For technology and operating-cycle context, we also used sources such as ASME publications and peer reviewed engineering journals that discuss performance and duty cycles.

In parallel, we reviewed annual reports, investor presentations, and public press releases to understand how revenue is recognized across equipment and project delivery timelines. We cross-checked delivery timelines using paid company financials data and, where relevant, a paid import export shipment level database for trade-aligned verification. The source list above is illustrative, and other public documents were also used to collect, validate, and clarify data points during the work.

Primary Interviews and Surveys

Primary interviews and surveys focused on confirming how demand is forming by application, and on stress-testing assumptions on pricing, delivery timing, and replacement cycles. We spoke with a mix of OEM-side experts, EPC and project engineering roles, power plant operators, and procurement stakeholders. The discussion was balanced across the United States, Canada, and Mexico, so local permitting timelines and grid needs were reflected in the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 21% | |

| Mid tier: 44% | Functional/Unit leaders: 28% | |

| Smaller Players: 22% | Managers: 51% |

Market-Sizing & Forecasting

Sizing started from a top-down build where power capacity additions, retirements, and announced project pipelines were reconstructed into likely turbine order volumes by capacity band and operating cycle, then translated into value using modeled average selling prices by class. To keep totals realistic, we added practical checks from the bottom-up side, including sampled project award values, typical turbine package pricing ranges discussed in interviews, and channel feedback on lead times, and then adjusted the overall run rate.

Key inputs that shaped the model included combined-cycle versus simple-cycle mix, the share of gas-fired additions versus other generation sources, typical unit capacity ranges used in utility and industrial sites, expected replacement timing for aging fleets, and fuel availability signals that influence dispatch and investment. For forecasting, scenario analysis was used because timing of large projects can shift due to permitting, financing, and grid reliability needs. Those timing risks were tested with expert views before the final curve was set. Where public data did not provide clear splits, such as smaller industrial installations, conservative allocation rules were applied and then revisited through follow-up calls.

Data Validation & Update Cycle

Outputs were checked against independent signals such as traded equipment patterns, announced build plans, and macro indicators that typically move with power investment. Any inconsistencies were reviewed before final numbers were signed off. When a segment showed an unusual jump, we rechecked the assumptions behind unit counts, pricing, and cycle mix, and if needed, re-contacted respondents to determine whether it reflected a real demand shift or a modeling artifact.

The work goes through multi-step internal review, so the same logic is applied across historical years and the forecast window. Reports are refreshed annually, and interim updates are made when material events occur, such as major policy changes, large project cancellations, or sudden shifts in fuel economics. Right before delivery, an analyst performs a fresh pass so clients receive the latest updated view.

Mordor Intelligence's North America Gas Turbine Market Size Compared With Other Published Estimates

Published numbers for this market can look far apart because firms often use different time windows, attach different price assumptions to similar project pipelines, or include adjacent revenue pools that buyers may not consider part of equipment demand. Even small choices, like how replacement units are timed versus new builds, can move the reported value noticeably.

Order pipeline checks, operating-cycle mix validation, and capacity-band splits are the evidence points that keep Mordor Intelligence aligned to equipment revenue in the United States, Canada, and Mexico, rather than blending in broader power-plant spend or long service streams. In other public estimates, the gap often comes from counting a wider set of industrial packages, applying more aggressive price escalation across large-frame units, or reporting a nearer-term year where a cluster of mega-project awards temporarily lifts the total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.06 B (2026) | |

| Global Consultancy A | USD 7.94 B (2024) | Uses an earlier base year that can capture a heavier project-award cycle and applies a broader application framing (including more industrial packages), which can lift the value versus an equipment-revenue view tied to the forecast start year. |

| Trade Journal B | USD 5.82 B (2024) | Likely aggregates wider turbine-related spend across the region and applies generalized growth assumptions, with less transparency on capacity band pricing and on how replacement timing is treated year to year. |

The table shows that the spread is mostly explained by year selection and what is counted as market revenue, not only by different growth rates. By keeping the scope tied to gas turbine equipment demand and by cross-checking project timing and cycle mix, our estimate stays traceable to inputs that can be re-tested when new builds or retirements are announced.

Key Questions Answered in the Report

How large is the north america gas turbine market today?

The market reached USD 3.06 billion in 2026 and is expected to climb to USD 3.66 billion by 2031.

What is driving new gas-turbine orders despite renewable growth?

Fast-ramping capability to stabilize grids with high wind and solar penetration, low natural-gas prices, and Section 45V hydrogen incentives all support new installations.

Which capacity class is expanding the fastest?

Turbines rated above 120 MW are growing at a 4.5% CAGR as utilities replace retiring coal units with large combined-cycle plants.

How are data-center loads shaping demand?

Hyperscale facilities increasingly procure on-site aeroderivative turbines to secure uninterrupted power and avoid interconnection delays.

Will batteries replace peaker turbines?

Four-hour lithium-ion systems are already displacing some simple-cycle projects, but longer-duration needs and grid-forming inertia keep opportunities open for gas turbines.

Which suppliers lead the regional market?

GE Vernova, Siemens Energy, and Mitsubishi Power dominate utility-scale orders, while Solar Turbines, Capstone Green Energy, and Wärtsilä compete in distributed segments.

Page last updated on: