Wind Turbine Foundation Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

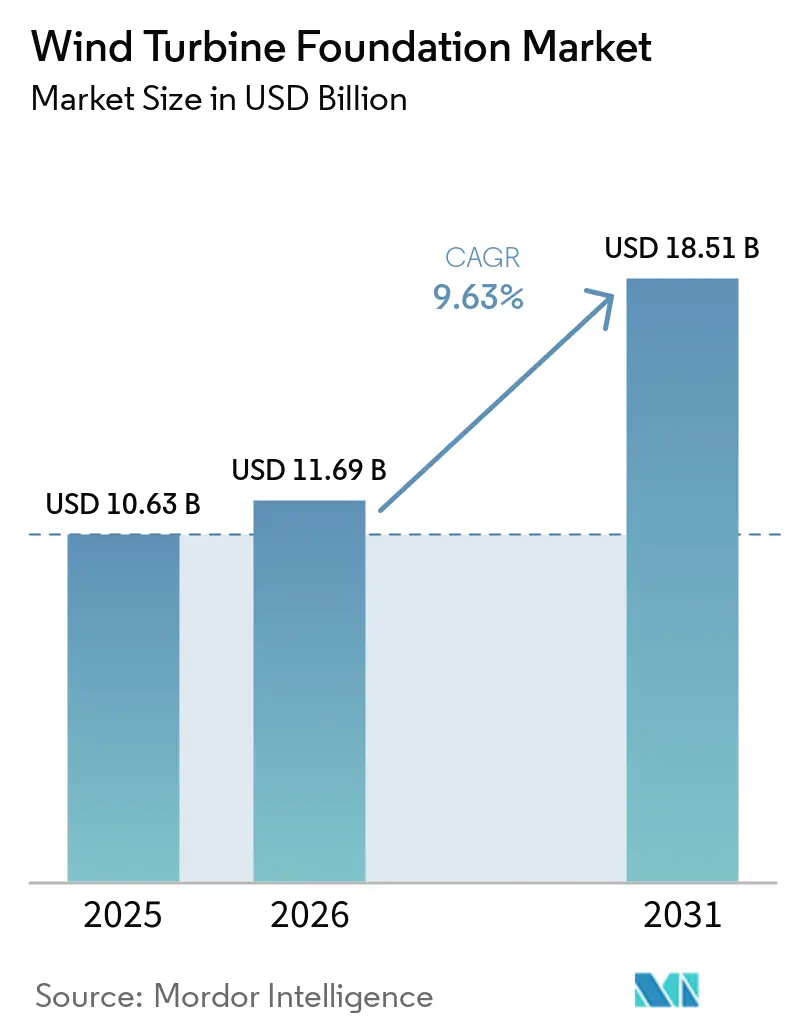

| Market Size (2026) | USD 11.69 Billion |

| Market Size (2031) | USD 18.51 Billion |

| Growth Rate (2026 - 2031) | 9.63% CAGR |

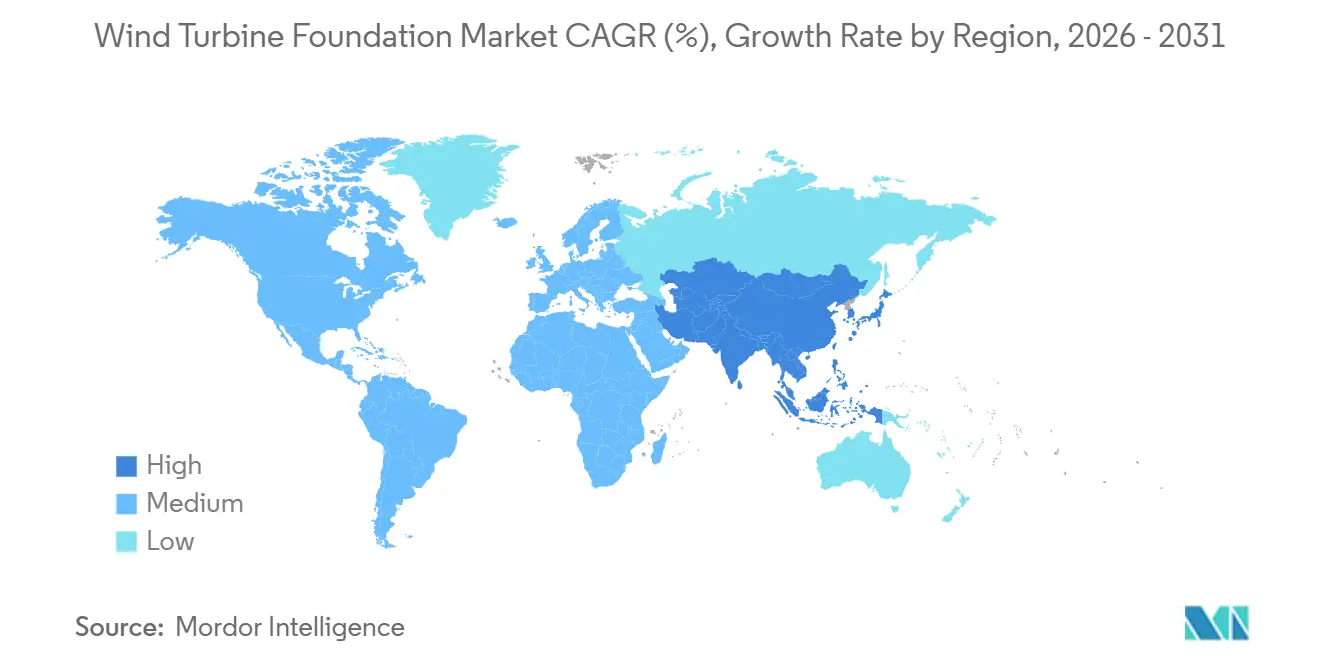

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

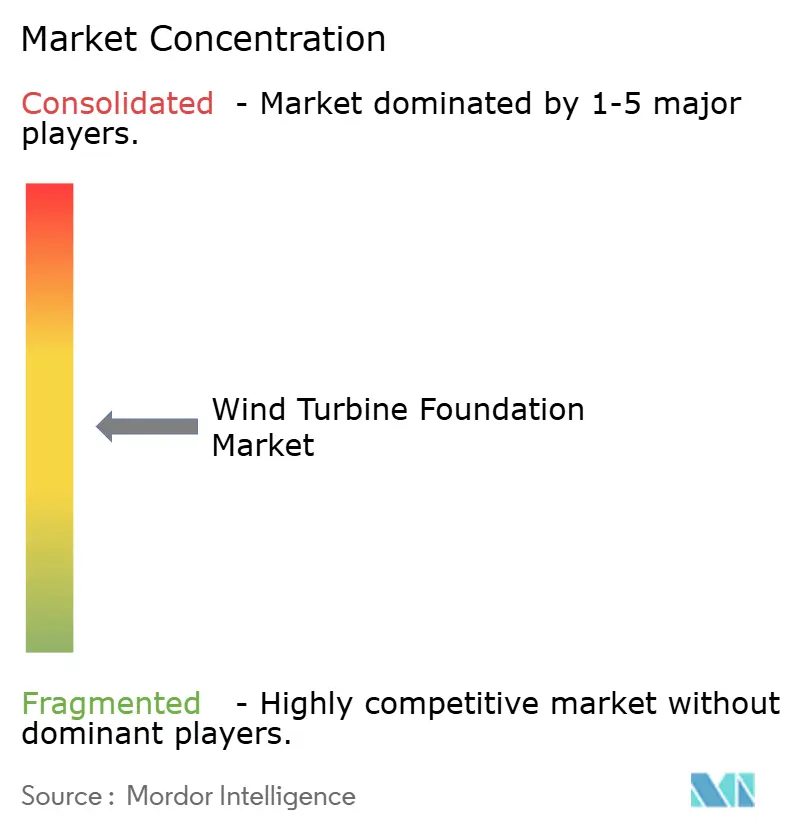

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wind Turbine Foundation Market Analysis by Mordor Intelligence

The Wind Turbine Foundation Market size was valued at USD 10.63 billion in 2025 and is estimated to grow from USD 11.69 billion in 2026 to reach USD 18.51 billion by 2031, at a CAGR of 9.63% during the forecast period (2026-2031). Rapid offshore wind licensing, turbine upsizing beyond 15 MW, and steel-plate supply tightness are restructuring procurement strategies. Developers are front-loading foundation orders to lock in scarce XXL monopile capacity, while floating concepts are opening deep-water sites in Japan, Scotland, and California. Port dredging in Esbjerg and Bremerhaven, digital-twin design workflows, and green-steel offtake agreements are compressing project timelines and curbing embodied carbon. At the same time, policy incentives such as the EU Net-Zero Industry Act and the U.S. Inflation Reduction Act are amplifying demand visibility and improving debt terms.

Key Report Takeaways

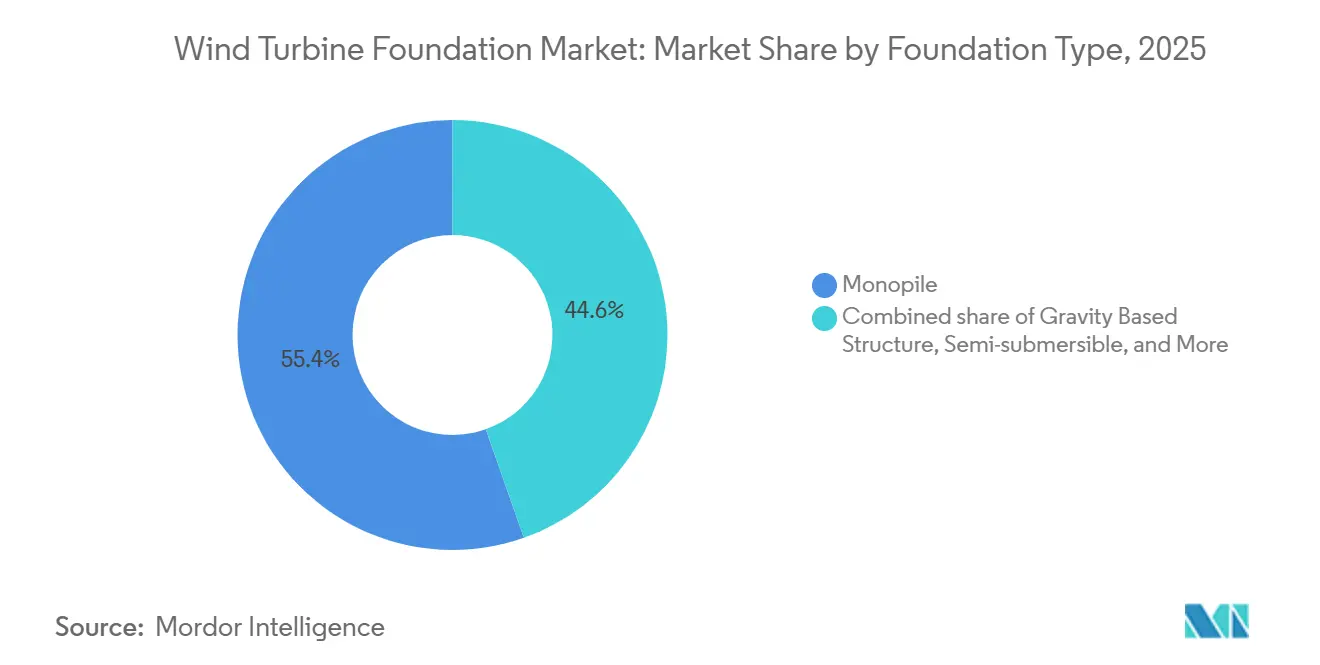

- By foundation type, monopiles led with 55.4% of wind turbine foundation market share in 2025, whereas semi-submersibles are projected to expand at a 27.8% CAGR through 2031.

- By material type, steel dominated with a 67.1% share in 2025, while composite/hybrid options are climbing at a 14.4% CAGR during 2026-2031.

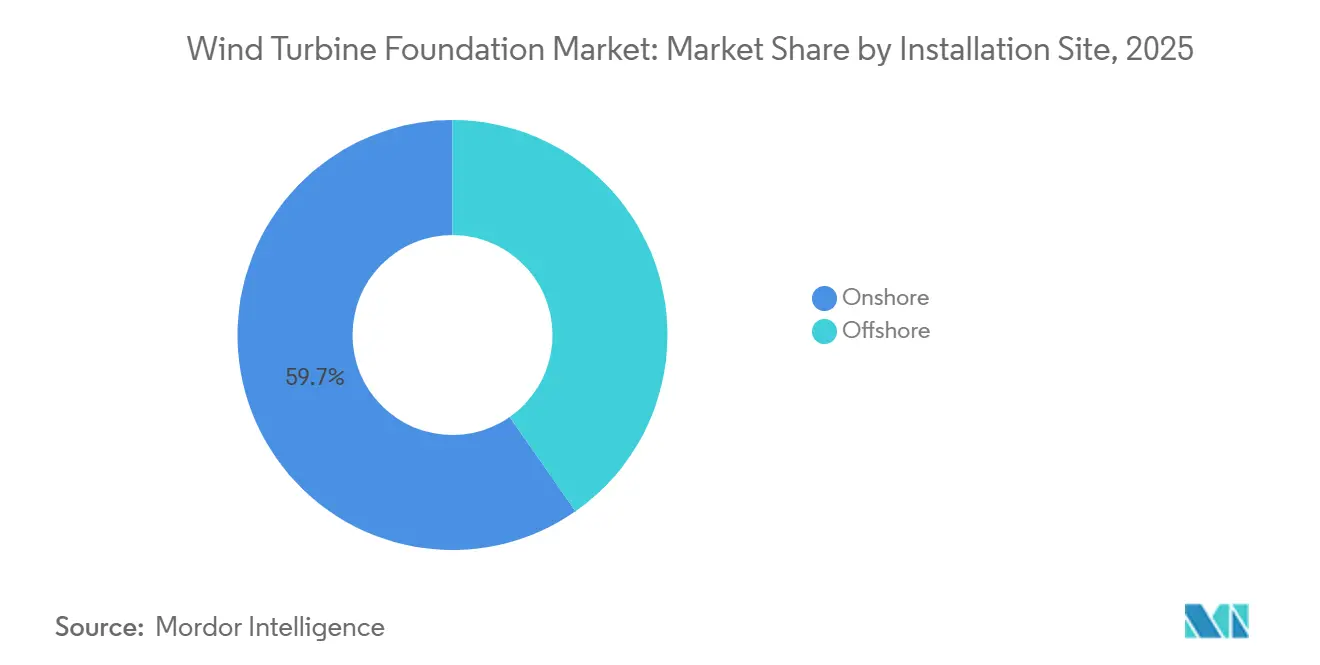

- By installation site, onshore retained 59.7% share in 2025, and floating offshore is accelerating at a 28.0% CAGR to 2031.

- By turbine rating, the above-5 MW class accounted for 49.8% of 2025 installations and is advancing at an 11.3% CAGR through 2031.

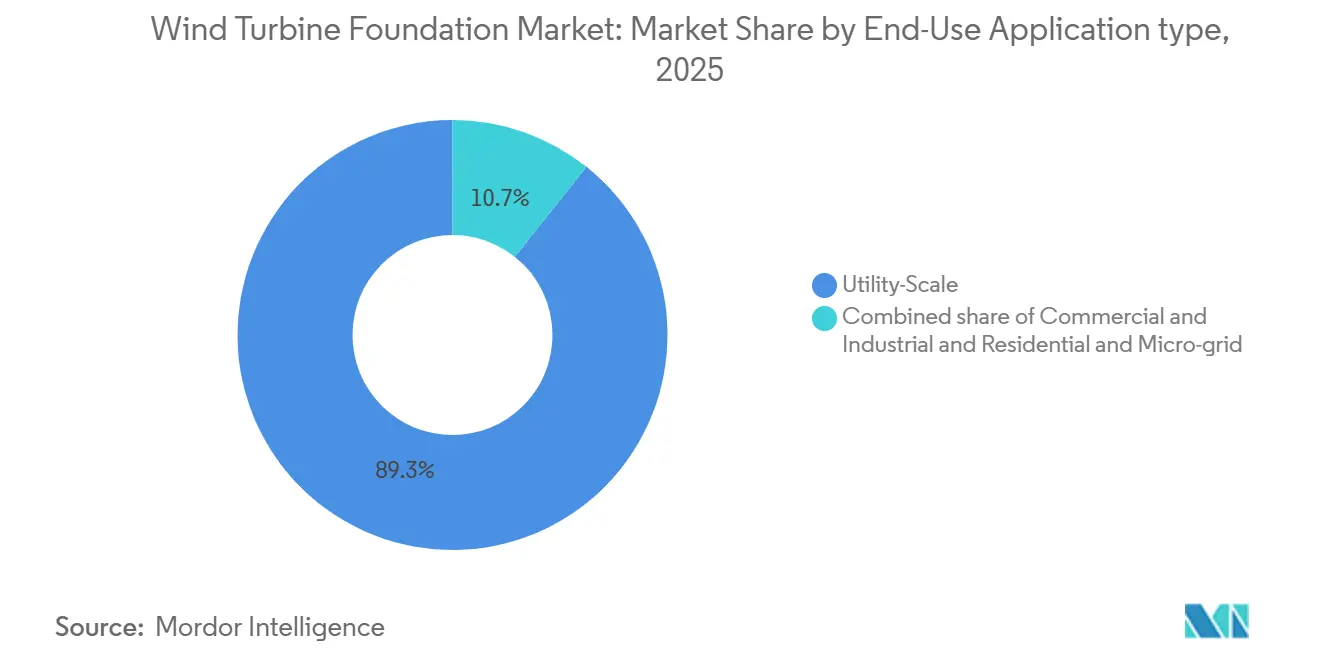

- By end-use application, utility-scale projects held 89.3% share in 2025, whereas residential / micro-grid schemes are gaining momentum at a 12.5% CAGR.

- By geography, Europe captured 37.2% revenue in 2025 and Asia-Pacific is the fastest-growing region with a 13.6% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Wind Turbine Foundation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid offshore wind-farm build-out under global net-zero targets | +3.2% | Europe, Asia-Pacific, U.S. East Coast | Medium term (2-4 years) |

| Turbine ratings ≥ 15 MW demanding XXL foundations | +2.8% | North Sea, Taiwan, China, U.S. East Coast | Short term (≤ 2 years) |

| Falling LCOE boosting developer ROI | +1.9% | Europe, Asia-Pacific | Long term (≥ 4 years) |

| Mass-produced modular concrete bases cutting port bottlenecks | +0.9% | Norway, Netherlands, China, South Korea | Medium term (2-4 years) |

| Digital-twin geotechnical modeling accelerating custom design | +0.6% | Europe, North America | Short term (≤ 2 years) |

| Demand for recyclable foundation materials | +0.5% | European Union, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Offshore Wind-Farm Build-Out Under Global Net-Zero Targets

Governments pursuing mid-century carbon neutrality auctioned roughly 100 GW of offshore wind capacity during 2025-2026 on top of the 83 GW already operating in 2024.[1]Global Wind Energy Council, “Global Offshore Wind Report 2024,” Global Wind Energy Council, gwec.net Europe’s REPowerEU blueprint alone eyes 300 GW by 2050, while the U.S. Inflation Reduction Act’s clean-energy incentives lift project IRRs by up to three percentage points. China’s 14th Five-Year Plan calls for 50 GW of offshore wind by 2030, fueling a domestic build programme that eclipses fabrication capacity.[2]Global Wind Energy Council, “Global Offshore Wind Report 2024,” Global Wind Energy Council, gwec.net In response, lead times for XXL monopiles have stretched to 24 months, pushing developers to reserve slots through 2029. Fabricators with automated lines and deep-water quays, such as Sif Group, whose FY 2026 EBITDA guidance jumped 181% year on year, are securing premium pricing.[3]Offshore Wind, “China Offshore Wind Capacity and Project Updates,” Offshore Wind, offshorewind.biz

Turbine Ratings ≥15 MW Demanding XXL Foundations

Next-generation turbines generate thrust loads 40% above 10 MW models, forcing monopiles to 10 m diameters, 120 m lengths, and 2,400 t weights.[4]Sif Group, “Annual Report 2025 and Net-Zero Industry Act Strategic Project Status,” Sif Group, sif-group.com Port depth is the chokepoint; only Esbjerg, Bremerhaven, Able Seaton, and Maasvlakte II currently handle >10 m monopiles. EEW and CS Wind delivered early Nordlicht 1 monopiles ahead of schedule, confirming that robotized welding keeps dimensional tolerances within 5 mm across 100 m lengths. The segment’s competitive edge now rests on mills able to roll >120 mm plate and fabricators that integrate real-time QC. RWE’s reservation of 320,000 t of plate through 2028 illustrates how large buyers are vacuuming up scarce capacity.

Falling LCOE Boosting Developer ROI

Offshore wind LCOE fell from roughly USD 125/MWh in 2023 to a USD 42–52/MWh range in 2026 as turbine scaling, serial production, and auction pressure took hold. Japan’s Noshiro/Mitane/Oga bid cleared 30% below the government reference price, signaling cost parity with gas in some Asia-Pacific markets. Lower LCOE improves financing spreads and attracts long-tenor institutional capital. Developers are transitioning to merchant exposure, which in turn raises demand for 30-year-life foundations with minimal O&M. Demonstrations such as Ørsted’s suction-bucket jackets in Taiwan shaved 20% off installation schedules while curbing underwater noise. Consequently, modular concrete and bucket jackets are gaining favor where environmental permitting is strict.

Mass-Produced Modular Concrete Bases Cutting Port Bottlenecks

BetongVIND’s serial gravity base cuts embodied carbon 80% versus steel monopiles by optimizing concrete mixes and using local cement. Peikko’s Cage Rock solution reduced excavation by 800 m³ per turbine at the Faroe Islands site and trimmed foundation diameter by over 10 m. Inland prefabrication of concrete segments allows barging to coastal assembly, bypassing deep-draft constraints that plague XXL monopile logistics. Carbon pricing above USD 93.6/t makes concrete alternatives cost-competitive, especially as EU rules require 70% material recovery by 2030. Market pull is reinforced by developers eager to derisk steel shortages and by banks that favor lower-carbon assets. As design standards evolve, modular concrete is set to claim a greater share in the wind turbine foundation market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX for deep-water floating solutions | –1.4% | Japan, Scotland, California, Mediterranean | Medium term (2-4 years) |

| Limited global supply of >120 mm steel plate | –0.8% | Europe, North America | Short term (≤ 2 years) |

| Shallow-draft ports delaying XXL monopile logistics | –0.5% | Baltic Sea, Vietnam, Gulf Coast | Short term (≤ 2 years) |

| Unclear salvage liability inflating finance costs | –0.3% | North Sea, U.S. East Coast, Taiwan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX for Deep-Water Floating Solutions

Floating foundations cost about EUR 3.4 million per megawatt, of which platform fabrication and transport represent up to USD 1.4 million, and installation plus mooring add as much as EUR 4.5 million. Vessel charters range from USD 234,000 to USD 351,000 per day and can last 10-15 days per unit, so installation expenses run 50-70% above fixed-bottom projects. Current floating levelized energy prices exceed USD 0.20 per kilowatt-hour, and DNV foresees only a gradual fall to USD 67 per megawatt-hour by 2050, keeping bankability challenging in the near term. Port upgrades intensify the bill; the U.S. West Coast alone needs at least USD 1.2 billion for new integration quays and crane capacity before large-scale assembly can start. Until total capital costs drop below USD 2.92 million per megawatt, most floating projects will remain limited to subsidized pilot zones in Japan, Scotland, and California.

Limited Global Supply of Greater than 120 mm Steel Plate

Monopiles for 15 MW turbines require a plate thicker than 120 millimeters, yet fewer than ten rolling mills worldwide can supply this grade, creating a structural bottleneck. U.S. domestic heavy plate prices climbed to USD 1,115 per short ton in March 2026, while lead times stretched beyond three months, forcing developers into long-term reservation contracts. RWE secured 320,000 tonnes of plate through 2028 from Steelwind, reducing spot availability for smaller buyers and tightening competition. European mills are raising green-steel premiums as carbon-border levies add USD 58.5-93.6 per tonne after 2027, further inflating costs. Until new capacity enters service at Dillinger in 2028, steel supply will remain the primary gating factor for XXL foundation schedules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Foundation Type: Semi-Submersibles Surge as Monopiles Dominate

The monopile segment accounted for 55.4% of the wind turbine foundation market size in 2025, underscoring its cost efficiency in depths to 60 m. Semi-submersibles, however, are poised to register a 27.8% CAGR as floating wind scales in >100 m waters.

Jacket foundations are gaining traction in Asia-Pacific, with Ørsted's Greater Changhua project achieving 20% faster schedules. Gravity-based structures are resurging in Norway, targeting an 80% carbon reduction. Floating foundations, driven by Japan's 11.7-gigawatt auction and Scotland's BW Ideol pipeline, represent 234 megawatts operationally, with a 244-gigawatt pipeline. Innovations like BW Ideol's Damping Pool and Principle Power's WindFloat enhance efficiency, reducing installation time by up to 60%, signaling a significant shift in foundation technologies.

By Material Type: Composite Hybrids Challenge Steel Hegemony

Steel owned 67.1% of the wind turbine foundation market share in 2025, reflecting mature supply chains and high strength-to-weight performance. Yet escalating steel-plate prices that hit USD 1,115 per short ton in March 2026 and carbon-border levies that will add USD 58-93/t by 2027 are nudging developers toward greener mixes. Composite and hybrid foundations, though smaller in absolute volume, are forecast to grow at a 14.4% CAGR to 2031, driven by EU circular-economy rules that demand 70% material recovery at decommissioning. Hybrid steel-concrete semi-submersibles such as BW Ideol’s Damping Pool offer 40% lower embodied emissions and simplified end-of-life dismantling. REFRESH trials showed recycled glass-fiber mats that match virgin properties and create a sink for the 25 Mt blade waste expected by 2050.

Concrete gravity bases are gaining a fresh lease because modular molds allow inland casting followed by barge tow-out, which bypasses draft limits that hamper XXL monopile logistics. Peikko’s Cage Rock rock-anchored system cut concrete volume 15% and reinforcement 17% at Flatnahagi, improving economics for small island grids. Dillinger’s PURE STEEL+ line, launching 2027–2028, targets 55–60% CO₂ reduction relative to conventional plate, signaling that even incumbent steel players are hedging with low-carbon supply. As carbon pricing tightens, developers will weigh upfront cost against future salvage credits, leading to a broader procurement palette. Consequently, while steel keeps its numeric lead, composite and hybrid solutions will carve the next leg of growth in the wind turbine foundation market.

By Installation Site: Floating Offshore Races Ahead of Onshore Maturity

Onshore foundations still accounted for 59.7% of the wind turbine foundation market size in 2025, thanks to lower CAPEX and shorter permit cycles. Peikko’s rock-anchored designs cut excavation by 800 m³ per turbine and help onshore sites with poor soil conditions, sustaining demand in mountainous and island regions. Fixed-bottom offshore retained the middle ground, propelled by Dogger Bank, Empire Wind, and Coastal Virginia projects that all rely on XXL monopiles. Yet floating offshore installations are projected to surge at a 28.0% CAGR and transform the geographic spread of orders.

Floating wind unlocks waters deeper than 60 m, where 80% of global offshore wind resources reside. Japan’s 16.8 MW Goto pilot reached COD in 2024 and reinforced confidence for the nation’s 11.7 GW auction held in 2025. Scotland and California together line up over 5.5 GW of floating leases that require semi-sub or tension-leg platforms with CAPEX premiums near USD 3.97 million per MW, but support schemes and rising wholesale prices narrow the gap. As dredging projects finish at Esbjerg and Bremerhaven, Europe will still dominate fixed-bottom, while Asia-Pacific captures the lion’s share of new floating activity. The interplay means that although onshore volumes stay large, incremental value growth tilts offshore, particularly toward floating solutions that expand the total addressable wind turbine foundation market.

By Turbine Rating: Megawatt-Class Upscaling Shapes Foundation Demand

Turbines above 5 MW comprised 49.8% of the 2025 installation count and are advancing at an 11.3% CAGR, effectively steering the wind turbine foundation market toward heavier, larger-diameter substructures. Vestas’ V236-15 MW and Siemens Gamesa’s SG 14-236 DD require monopiles up to 120 m long and 2,400 t in weight, doubling the steel needed versus older 8 MW units. China is leapfrogging straight to 18 MW models from Mingyang and CSSC Haizhuang, so foundation specs must now withstand 60% higher thrust loads.

Foundations for the 2-5 MW class remain vital for onshore repowering and nearshore projects, but face moderate growth as grids favor higher output per tower. Sub-2 MW turbines find niches in micro-grids, islands, and remote industrial loads, yet their small foundations seldom move the global needle. The wind turbine foundation market share advantage, therefore,e consolidates in the ≥15 MW bracket as fabrication lines worldwide shift to automated welding cells that keep dimensional tolerance under 5 mm over 100 m lengths. Port capacity limits for parts exceeding 10 m in diameter restrict competitive entry to four European hubs, highlighting infrastructure as a gating factor. As OEM prototypes march toward 20 MW, plate thickness beyond 140 mm may be required, pressuring mills and raising the strategic value of low-carbon steel supply.

By Application: Utility-Scale Dominance With Micro-Grid Upside

Utility-scale projects held 89.3% wind turbine foundation market share in 2025 because only gigawatt-scale clusters can amortize installation vessels and heavy-lift cranes. Empire Wind, Dogger Bank, and Jiangsu Dafeng exemplify the segment’s appetite for multi-hundred monopile orders that keep fabrication lines humming through 2029. Developers lock multi-year capacity with Sif, EEW, and Bladt, protecting schedules but narrowing price flexibility.

Residential and micro-grid applications are growing at a 12.5% CAGR as islands and off-grid mines value energy security and avoid costly submarine cables. These projects lean on modular gravity bases or rock-anchored pads that install with conventional equipment and cut CAPEX by up to 40% compared with utility-scale norms. Commercial and industrial buyers, including data centers, use behind-the-meter contracts to hedge electricity cost inflation, creating room for 2-3 MW turbines on bespoke foundations. Although smaller in absolute value, the segment yields better margins for regional fabricators that tailor designs and integrate balance-of-plant scope. As policy strings tighten around local content and recyclability, micro-grid foundations may become test beds for composite hybrids before mainstream adoption. In sum, utility-scale orders underpin volume, but diversified demand broadens the customer base and fortifies resilience across the wind turbine foundation market.

Geography Analysis

Europe commanded 37.2% of the global wind turbine foundation market share in 2025, underpinned by the North Sea build-out and upgraded ports in Esbjerg and Bremerhaven. Esbjerg deepened its fairway to 12.8 m and expanded the Combi-Terminal, enabling load-out of monopiles larger than 10 m in diameter. Germany’s Gennaker and Windanker projects together need more than 80 XXL foundations, while the United Kingdom’s Dogger Bank and Hornsea 3 require over 250 units. Sif Group’s Maasvlakte II plant produces 200 monopiles a year, giving Europe ample fabrication headroom through 2030. Suction-bucket jackets deployed at Ørsted’s Greater Changhua site are now being evaluated for noise-sensitive North Sea zones.

Asia-Pacific is the fastest-growing region, advancing at a 13.6% CAGR to 2031 and steadily lifting the wind turbine foundation market size. China already operates 23.5 GW in Guangdong and 11.3 GW in Jiangsu, both shifting to 15 MW and larger turbines that need plates thicker than 120 mm. Taiwan completed 66 suction-bucket jackets at Greater Changhua 2b & 4 in January 2026, proving that local yards can handle complex lattice work. Japan awarded 11.7 GW of capacity across four zones in 2025 and is counting on semi-submersibles for depths beyond 100 m. South Korea’s GS Entec is doubling monopile capacity by early 2026 to serve export orders to Vietnam and the Philippines.

North America trails in installations yet holds a robust 5.8 GW pipeline along the U.S. East Coast, giving the region a growing share of the wind turbine foundation market size. Empire Wind and Coastal Virginia Offshore Wind together installed 230 XXL monopiles in 2025, but federal stop-work orders briefly halted construction and raised financing spreads. California’s 4.6 GW of floating leases will pivot demand toward semi-submersible platforms that cost about USD 3.97 million per megawatt. Canada plans 5 GW of offshore capacity by 2030, while Brazil and Morocco have each cleared over 1 GW in environmental permits. These emerging pipelines suggest that North America and selected frontier markets will steadily close the gap with established European and Asian hubs.

Competitive Landscape

The wind turbine foundation market is moderately concentrated, with Sif Group, EEW, Bladt Industries, Steelwind Nordenham, and Navantia-Windar together controlling about half of global offshore capacity. Sif Group obtained “Strategic Project” status under the EU Net-Zero Industry Act in March 2026, giving the company faster permitting and state-aid access for its Maasvlakte II plant that can roll 200 monopiles annually up to 11 m in diameter. EEW and CS Wind delivered the first Nordlicht 1 monopiles ahead of schedule in February 2026, underscoring the execution benefits of robotized welding lines. Dillinger and Sif signed a green-steel addendum that targets a 55–60% cut in embodied carbon and locks in low-emission plate supply from 2027, allowing both firms to capture premium pricing as carbon-border adjustments rise.

Installation contractors are moving upstream to secure margins and schedule control. DEME bought additional turbine-installation and cable-laying vessels, enabling project timelines to compress by 10–15% and supporting a 30.7% EBITDA margin on USD 2.45 billion in 2025 turnover. Van Oord’s new Calypso vessel completed its first cable work at the 1.4 GW Sofia farm in September 2025, illustrating vertical integration benefits. Jan De Nul used the Les Alizés heavy-lift ship to install monopiles up to 1,500 t at Denmark’s Thor site, proving the capacity to handle 100 m components on a single lift. Seaway 7 secured Gennaker’s foundation transport contract, expanding its portfolio beyond cables into full engineering, procurement, construction, and installation scope.

White-space growth centers on floating and low-carbon solutions. BW Ideol’s Damping Pool semi-submersible won DNV certification for 15 MW turbines in May 2025 and attracted USD 147.42 million in public funding for the Fos3F factory, opening an early lead in deep-water applications. Principle Power’s WindFloat tension-leg design secured a fabrication slot in France to serve Scotland’s pipeline, while Peikko and BetongVIND are scaling modular concrete bases that cut embodied CO₂ by up to 80%. Steel-plate scarcity is squeezing smaller yards without long-term offtake deals, accelerating consolidation as developers demand multi-year slot reservations. Overall, the wind turbine foundation market favors players that combine automated XXL fabrication, secured green-steel supply, and in-house installation fleets, positioning the current top tier to defend share even as floating platforms expand addressable demand.

Wind Turbine Foundation Industry Leaders

Sif Group

EEW Group

Bladt Industries

Steelwind Nordenham

Ramboll (engineering design share)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: The status gives priority in permitting and financing to support faster deployment of offshore wind and strengthen the European industrial base.

- February 2026: EEW and CS Wind delivered the first Nordlicht 1 monopiles ahead of schedule.

- January 2026: Ørsted finished installing 66 suction-bucket jackets at Greater Changhua 2b & 4.

- May 2025: U.S. plate prices hit USD 1,115/short t on tight supply, while imports landed at USD 970–990/short t despite tariffs.

Global Wind Turbine Foundation Market Report Scope

A wind turbine foundation is an engineered structural base designed to support a turbine tower by anchoring it securely into the ground (onshore) or seabed (offshore). It ensures stability by transferring vertical and horizontal loads, including gravity, wind pressure, and dynamic forces, safely into the earth, thereby preventing tilting, settlement, or overturning.

The Wind Turbine Foundation Market is segmented into foundation type, material type, installation site, turbine rating, end-use application, and geography. By foundation type, the market is segmented into gravity-based structures, monopile foundations, and other foundation types. By material type, the market is segmented into concrete, steel, and composite/hybrid materials. By installation site, the market is segmented into onshore, offshore fixed-bottom, and offshore floating installations. By turbine rating, the market is segmented into below 2 MW, 2 to 5 MW, and above 5 MW turbines. By end-use application, the market is segmented into utility-scale and other applications. The report also covers the market size and forecasts for the wind turbine foundation market across major regions, including North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Gravity-Based Structure |

| Monopile |

| Jacket |

| Tripod |

| Semi-submersible |

| Others |

| Concrete |

| Steel |

| Composite/Hybrid |

| Onshore | |

| Offshore | Fixed-Bottom Offshore |

| Floating Offshore |

| Below 2 MW |

| 2 to 5 MW |

| Above 5 MW |

| Utility-Scale |

| Commercial and Industrial |

| Residential and Micro-grid |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Russia | |

| Finland | |

| Sweden | |

| Tukey | |

| Netherlands | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Vietnam | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Egypt | |

| Morocco | |

| Rest of Middle East and Africa |

| By Foundation Type | Gravity-Based Structure | |

| Monopile | ||

| Jacket | ||

| Tripod | ||

| Semi-submersible | ||

| Others | ||

| By Material Type | Concrete | |

| Steel | ||

| Composite/Hybrid | ||

| By Installation Site | Onshore | |

| Offshore | Fixed-Bottom Offshore | |

| Floating Offshore | ||

| By Turbine Rating (Capacity) | Below 2 MW | |

| 2 to 5 MW | ||

| Above 5 MW | ||

| By End-Use Application | Utility-Scale | |

| Commercial and Industrial | ||

| Residential and Micro-grid | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Russia | ||

| Finland | ||

| Sweden | ||

| Tukey | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Vietnam | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Egypt | ||

| Morocco | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the market size of wind turbine foundation market?

The capacitor bank market size is forecast to reach USD 18.51 billion by 2031, up from USD 11.69 billion in 2026 with CAGR of 9.63%.

Which foundation type currently holds the largest share?

Monopiles led with 55.4% of 2025 installations.

Which region is expected to grow the fastest through 2031?

Asia-Pacific is projected to advance at a 13.6% CAGR.

How are steel-plate shortages affecting project timelines?

Limited >120 mm plate supply has extended monopile lead times to 24 months and driven multi-year reservation deals.

Why are semi-submersible foundations gaining traction?

They enable floating wind farms in >100 m depths, expanding viable sites in Japan, Scotland, and California.

What role do digital twins play in foundation design?

They cut design cycles in half and optimize material use, lowering costs and extending asset life.

Page last updated on: