Steam Turbine MRO Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 23.65 Billion |

| Market Size (2031) | USD 29.21 Billion |

| Growth Rate (2026 - 2031) | 4.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Steam Turbine MRO Market Analysis by Mordor Intelligence

The Steam Turbine MRO Market size is expected to grow from USD 22.56 billion in 2025 to USD 23.65 billion in 2026 and is forecast to reach USD 29.21 billion by 2031 at 4.31% CAGR over 2026-2031.

Regional demand is pivoting toward Asia-Pacific, nuclear life-extension programs in the United States and France, and advanced combined-cycle builds in the Middle East, all of which reshape the service mix and lift long-term contract values. Coal retirements across OECD nations are reducing the transactional repair pool, yet life-cycle extensions for subcritical and nuclear units continue to generate high-value overhauls. OEMs now bundle predictive analytics and spare-parts guarantees inside long-term service agreements (LTSAs), converting episodic spending into annuity streams and fortifying switching barriers. Independent service providers, however, are winning legacy fleets by promising 20–30% lower cost and faster turnaround while exploiting parts scarcity through additive manufacturing.

Key Report Takeaways

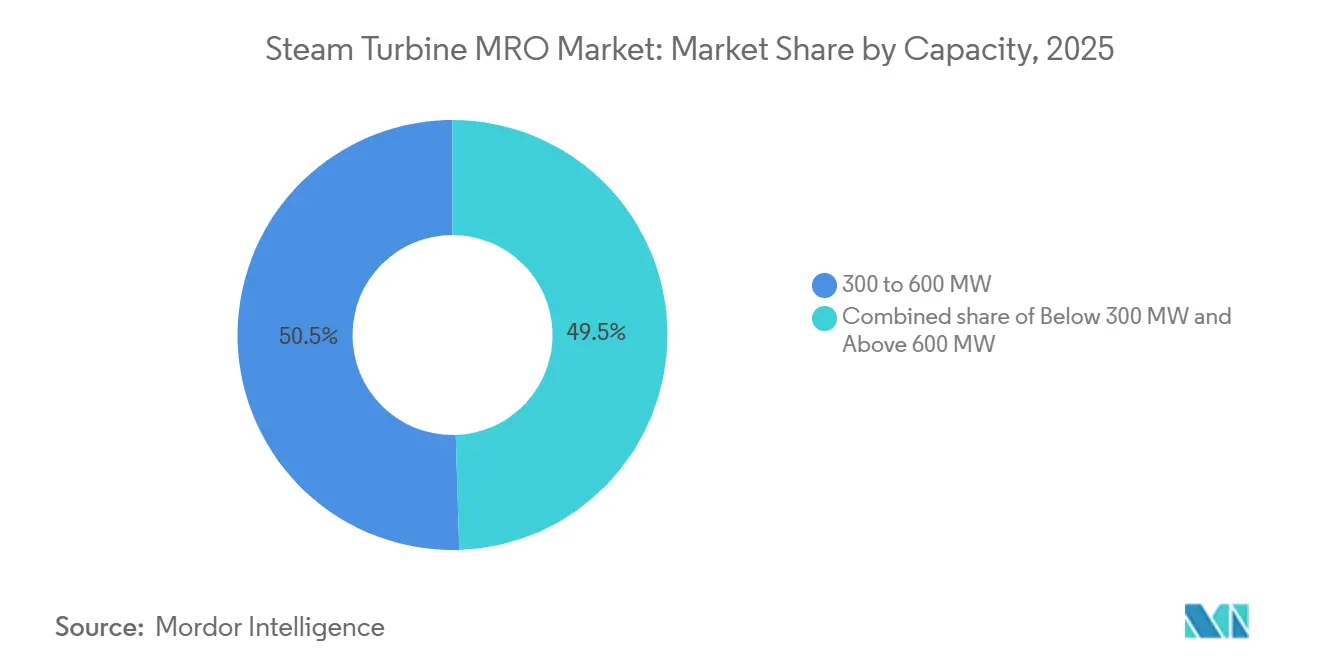

- By capacity, the 300–600 MW bracket held 50.5% of the steam turbine MRO market share in 2025. Turbines above 600 MW are forecast to expand at a 5.1% CAGR through 2031.

- By plant fuel, coal captured 60.1% of expenditure in 2025. Nuclear services are advancing at a 5.5% CAGR to 2031.

- By service, maintenance dominated with 53.9% revenue share in 2025. Repair work is rising at a 5.0% CAGR through 2031.

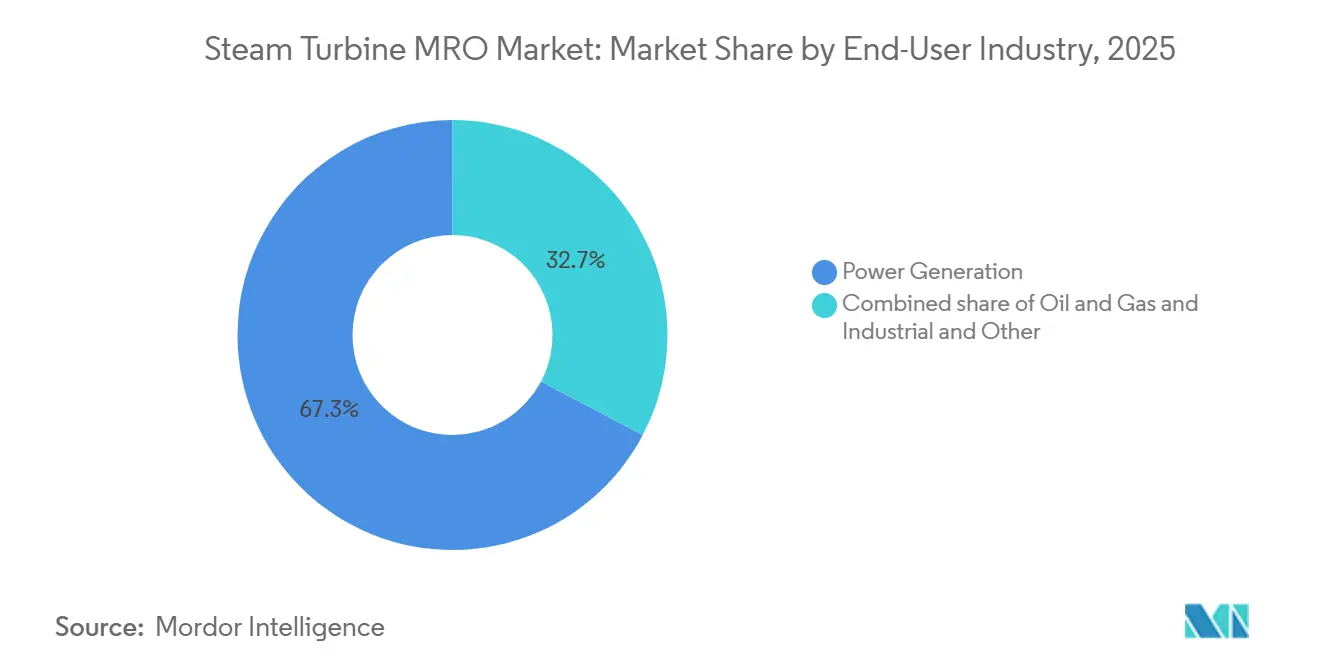

- By end user, power generation commanded 67.3% spending in 2025 and will grow at a 4.7% CAGR through 2031.

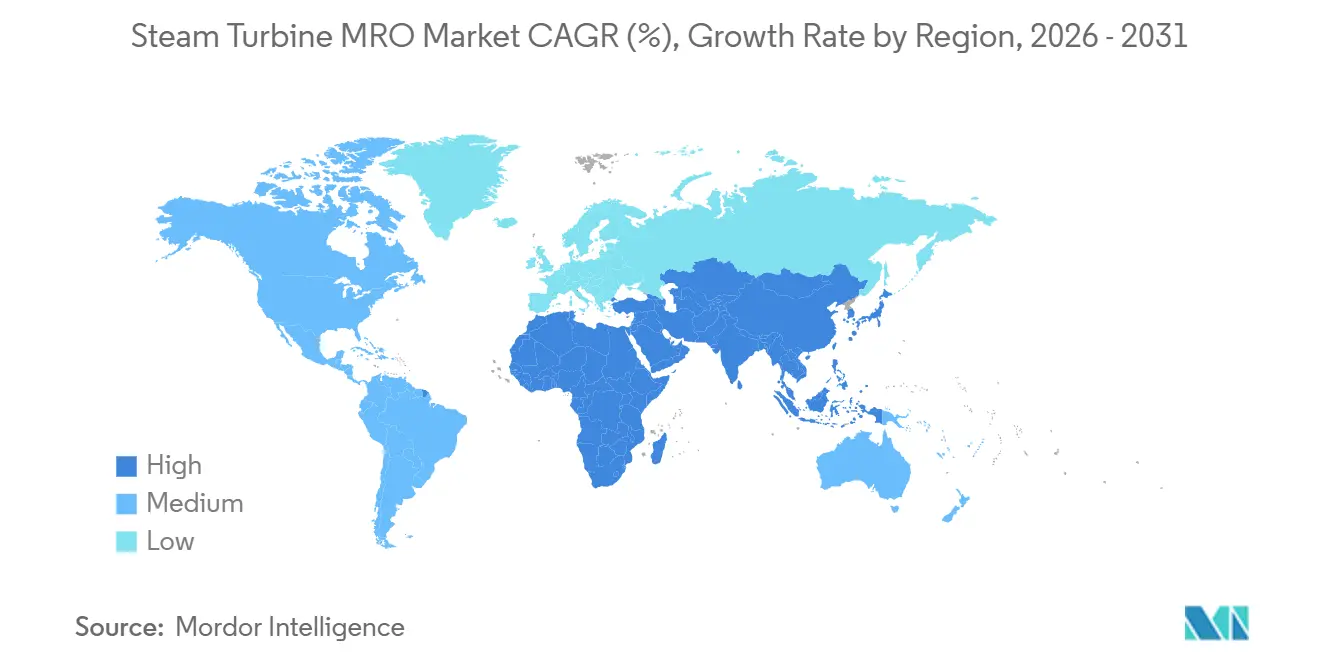

- By geography, Asia-Pacific led with 49.6% regional share in 2025, and is also the fastest-growing geography at 5.8% CAGR.

- GE Vernova, Siemens Energy, and Mitsubishi Power collectively held 45% of the aftermarket in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Steam Turbine MRO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging global thermal-power fleet lifecycle extension | +1.2% | Global, concentrated in North America, Europe, China, India | Long term (≥ 4 years) |

| Expansion of combined-cycle & advanced ultra-supercritical plants | +0.9% | Asia-Pacific core (China, India, Japan), Middle East, spill-over to Southeast Asia | Medium term (2-4 years) |

| OEM long-term service agreement boom | +0.8% | Global, early adoption in Middle East (Saudi Arabia, UAE), North America | Medium term (2-4 years) |

| Predictive-maintenance digital twins adoption | +0.6% | North America & Europe lead, Asia-Pacific following | Short term (≤ 2 years) |

| Decarbonization retrofits including H₂/NH₃ co-firing | +0.5% | Europe, Japan, pilot projects in Middle East and Australia | Long term (≥ 4 years) |

| Rise of industrial micro-CHP in emerging markets | +0.3% | Southeast Asia, Latin America, Sub-Saharan Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Global Thermal-Power Fleet Lifecycle Extension

The median U.S. coal unit age reached 44 years in 2024, and owners are choosing 50–60 year life extensions that call for rotor re-boring, creep assessments, and 3D aerodynamic blade retrofits, typically restoring 80–90% original efficiency at one-third of new-build capital.[1]National Energy Technology Laboratory, “Steam Turbine Life Extension Techniques,” netl.doe.gov NTPC extended fifteen Indian units totaling 3.8 GW in 2025 under a Bharat Heavy Electricals contract covering metallurgy upgrades and advanced seals. China mirrors the pattern, retrofitting pre-2010 subcritical plants with upgraded seals and low-pressure stage replacements to meet 2030 carbon-intensity targets while deferring decommissioning.

Expansion of Combined-Cycle & Advanced Ultra-Supercritical Plants

Steam temperatures above 600 °C in these units accelerate creep, doubling inspection frequency versus legacy subcritical fleets. Japan’s J-POWER introduced nickel-based 650 °C blades in 2024, requiring specialist weld repair unserved by most independents. China added 28 GW of ultra-supercritical capacity in 2025, and mandated 12,000-hour inspections, raising overhaul incidence. Siemens Energy’s 15-year Qurayyah LTSA in Saudi Arabia demonstrates how high-efficiency assets lock in long-duration MRO cash flows immediately after commissioning.[2]Siemens Energy, “Omnivise Suite Digital Reliability Results,” siemens-energy.com

OEM Long-Term Service Agreement Boom

LTSAs now guarantee availability, efficiency, and emissions compliance. GE Vernova’s 20-year Kuwait LTSA covers 4.8 GW and taps its Asset Performance Management platform for failure prediction 6–12 months out. Mitsubishi Power secured a 25-year New Capital deal in Egypt with a 95% availability guarantee that pushes proactive blade replacement and rotor balancing. Siemens Energy disclosed that LTSAs generated 38% of Gas Services revenue in fiscal 2025 at margins 15–20% above transactional work.

Predictive-Maintenance Digital Twins Adoption

Siemens Energy’s Omnivise cut forced outages 22% across 12 GW of European capacity in 2025 by flagging rotor eccentricity and blade erosion ahead of control-room alarms. GE Vernova’s Turbine Life Assessment software lets operators defer major inspections by up to 12 months when calculated creep life remains adequate. Hybrid models that blend finite-element stress analysis with machine-learning anomaly detection achieve 94% crack-identification accuracy, curbing false positives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated retirement of coal assets in OECD | -0.7% | North America, Europe (Germany, UK, Netherlands), Japan | Short term (≤ 2 years) |

| High outage CAPEX & downtime for major overhauls | -0.4% | Global, acute in liberalized power markets (US, EU, Australia) | Medium term (2-4 years) |

| OEM software lock-in limiting independents | -0.3% | Global, most pronounced in North America and Europe | Medium term (2-4 years) |

| Scarcity of legacy spare parts for <300 MW units | -0.2% | North America, Europe, parts of Asia with aging subcritical fleets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Retirement of Coal Assets in OECD

EIA data show 23 GW of U.S. coal shut in 2024, with another 14 GW slated by 2029, eliminating large swaths of addressable MRO volume.[3] U.S. Energy Information Administration, “International Energy Outlook 2025,” eia.gov The U.K. closed its last coal station in 2024, and Germany debates pulling its 2038 exit forward to 2030, squeezing European service demand. IEA forecasts a 40% decline in OECD coal capacity by 2035, a contraction that disproportionately hurts independents unable to pivot to gas or nuclear.

High Outage CAPEX & Downtime for Major Overhauls

An overhaul on a ≥300 MW unit costs USD 5–15 million and idles the plant 30–90 days, creating up to USD 2 million daily opportunity cost when spot power prices soar, pushing some merchant operators into run-to-failure mode.[4]Electric Power Research Institute, “Steam Turbine Overhaul Cost Study 2025,” epri.com OEM modular rotor-exchange programs trim downtime to 15–25 days but demand 20–30% price premiums that only high-capacity-factor plants can justify.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Capacity: Mid-Range Dominance, Large-Unit Growth Accelerates

In 2025, 300–600 MW units accounted for 50.5% of the steam turbine MRO market share thanks to the vast 1990s subcritical coal fleet. Above-600 MW turbines will post a 5.1% CAGR to 2031, lifting the steam turbine MRO market size for this bracket as China, India, and Japan deploy ultra-supercritical designs that demand nickel-alloy repairs and phased-array ultrasonic inspections.

Mid-range units are far from obsolete; J-POWER lifted four 600 MW subcritical units’ efficiency 2.3 points by swapping low-pressure stages for 3D blades in 2025, underscoring retrofit economics over retirement. Below-300 MW machines face parts shortages and early retirement, producing only 14% of MRO revenue on 22% of capacity in the United States.

By Plant Fuel: Coal Dominates, Nuclear Surges on Life Extensions

Coal plants generated 60.1% of global spend in 2025 and underpin the steam turbine MRO market despite OECD retirements, because Asia runs 1,900 GW of coal capacity. Nuclear work will outpace all fuels at 5.5% CAGR after NRC and ASN approvals push U.S. and French reactors to 80-year lives, swelling steam-generator swaps and rotor re-boring scopes that expand the steam turbine MRO market size for nuclear sites.

Natural-gas combined-cycle fleets carry 25% of spending and will grow 4.8% CAGR, buoyed by Middle-East megaproject LTSAs. Biomass and WtE plants remain niche yet require corrosion-resistant coatings, a specialized repair opportunity.

By Service Type – Maintenance Leads, Repair Gains on Aging Fleets

Maintenance activities, which include routine inspections, vibration monitoring, lube-oil sampling, and minor component swaps, accounted for 53.9% of 2025 revenue and represented the largest steam turbine MRO market share. The dominance stems from a broad installed base still within its first three decades of operation, when preventive work keeps forced-outage risk low and satisfies ISO 55000 asset-management requirements. OEMs monetize this layer through digital-twin subscriptions that trigger just-in-time part shipments and shorten outage windows, converting what was episodic spending into predictable annuity streams. Independents respond with mobile condition-monitoring trailers that can be deployed within twenty-four hours, a model favored by industrial plants lacking dense instrumentation. As combined-cycle and ultra-supercritical fleets mature, owners are bundling hot-gas-path inspections with standard maintenance visits to limit downtime overlap, raising average contract value and expanding the steam turbine MRO market size for service packages that promise 96% or better fleet availability.

Repair work, blade refurbishment, rotor re-machining, seal replacement, and bearing overhaul will rise at a 5.0% CAGR through 2031 as thermal fleets age and fatigue-induced failures accelerate. GE Vernova’s laser powder-bed fusion process rebuilds eroded nickel-based blades within six weeks, cutting lead times by 70% and protecting operators against legacy-spare scarcity. Mitsubishi Power’s 2025 introduction of laser-clad blade leading-edge restoration extends component life 50,000-80,000 operating hours, deferring USD 2–4 million full-stage replacements. Cold-spray additive services from Sulzer reduce repair costs by 35% versus weld-and-machine methods, broadening access for sub-300 MW units pressed to operate beyond design life. High-energy cogeneration turbines in refineries and petrochemical complexes now specify service agreements that blend predictive analytics with rotor-exchange modules, halving downtime to fifteen days and reinforcing long-term demand for advanced repair capabilities.

By End-User Industry – Power Generation Anchors, Industrial CHP Diversifies

Utility-scale power producers commanded 67.3% of 2025 spending, benefiting from an installed base that spans coal, gas, and nuclear assets and delivers multi-decade steam turbine MRO market size stability. Nuclear life-extension programs in the United States and France alone will lock in USD 400–600 million turbine and balance-of-plant overhauls per reactor. Gas-fired combined-cycle plants in Saudi Arabia and the United Arab Emirates rely on LTSAs that guarantee 95% availability, embedding OEMs for twenty years and ensuring recurring overhaul revenue streams. Coal plants in Asia remain the largest single source of transactional repair, but creeping retirements in OECD countries are shrinking this pool and pushing service firms toward diversified customer mixes.

The industrial and oil-and-gas segment is driven by 5–50 MW micro-CHP turbines that run at 85–95% load factors and require more frequent hot-section inspections than grid-connected peers. India commissioned 4.2 GW of industrial cogeneration capacity in 2024–2025, with Triveni Turbine capturing 38% of sub-30 MW installs and supplying regional hubs that guarantee a forty-eight-hour response, a service advantage over global OEMs. Vietnam’s twenty-year PPA regime for factory CHP projects created a 1.8 GW pipeline that demands localized MRO networks and mobile diagnostic rigs for plants where online sensors are sparse. Saudi Aramco’s ten-year, USD 680 million agreement with Baker Hughes covering 12 GW of refinery cogeneration shows the scale of future refinery-sector opportunity and highlights the premium placed on remote condition monitoring in hazardous locations. As industrial users adopt ISO 45001 safety frameworks, they increasingly favor service partners that can integrate emissions testing and regulatory documentation into overhaul scopes, shortening permitting cycles and elevating value-added engineering content.

Geography Analysis

Asia-Pacific controlled 49.6% of 2025 revenue and is projected to deliver a 5.8% CAGR to 2031 as China, India, and Southeast Asia expand ultra-supercritical and combined-cycle fleets. State Grid contracts for 78 GW of Chinese ultra-supercritical capacity already rely on domestic repair houses that possess nickel-alloy weld and phased-array UT capabilities, compressing foreign OEM share. India’s 3.8 GW NTPC refurbishment award to Bharat Heavy Electricals showcases the large-scale lifecycle-extension pipeline through the next decade.

North America’s growth is slowing down as coal closures offset nuclear life-extension gains; however, 250 GW of combined-cycle capacity anchors a robust LTSA base. Europe’s market is propelled by French nuclear upgrades and German CCGT build-outs to firm renewables. The Middle East and Africa market growth is fueled by Qurayyah, Al Dhafra, and New Capital mega-contracts linking LTSAs with digital-twin analytics. South America’s 6% slice benefits from Brazilian hydro-thermal hybrid upgrades and Argentine cogeneration tied to Vaca Muerta shale gas.

Competitive Landscape

The market is moderately concentrated. GE Vernova, Siemens Energy, and Mitsubishi Power jointly hold a 45% share, reinforced by installed-base data, proprietary controls, and LTSAs that limit third-party entry. GE Vernova operates 180 service centers and prints nickel-based blades in-house via additive manufacturing, cutting lead time to six weeks. Siemens Energy leverages Omnivise predictive analytics across 12 GW to foresee blade-crack propagation. Mitsubishi Power leads alternative-fuel retrofits after its 50% hydrogen and 20% ammonia references.

Regional OEMs dominate home markets: Shanghai Electric, Harbin Electric, and Dongfang Turbine command 65% of China’s aftermarket, while Bharat Heavy Electricals controls 55% in India, leveraging preferential procurement and cost advantages. Independents such as EthosEnergy and Sulzer push into non-OEM fleets by promising 30% savings and cold-spray blade repairs that shorten outages, though software lock-in still blocks their advanced analytics offerings. Additive manufacturing disrupts component supply chains and may erode OEM spare-parts mark-ups over the forecast horizon.

Steam Turbine MRO Industry Leaders

-

GE Vernova

-

Siemens Energy

-

Mitsubishi Power

-

Shanghai Electric

-

EthosEnergy (incl. Wood Group JV)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Bechtel and Westinghouse Electric Company have chosen Arabelle Solutions to provide three half-speed Arabelle steam turbines and generator sets for the AP1000, marking Poland's inaugural venture into nuclear power.

- December 2025: Rotating Machinery Services, Inc. has acquired the steam turbine and centrifugal compressor business from EthosEnergy, rooted in the TurboCare brand.

- January 2025: Mitsubishi Heavy Industries Compressor International Corporation (MCO-I) has revolutionized steam turbine maintenance by integrating Phased Array Ultrasonic Testing (PAUT).

- January 2024: Mechanical Dynamics and Analysis (MD&A) installed new buckets and covers on a steam turbine in Saudi Arabia and completed diaphragm repairs at its facility. During an inspection, the company identified damage and repaired the 1st and 17th stages of the rotor. The rotor consists of 19 stages: 12 high-pressure and 7 reheat stages.

Global Steam Turbine MRO Market Report Scope

A steam turbine is a machine that uses compressed steam to collect heat energy and turn a rotating shaft to do mechanical work. Steam turbines are spread all over the world and are also used to drive generators and generate electricity. On the steam turbine MRO market, maintenance, repair, and overhaul services are offered by the original equipment manufacturers, independent service providers (ISP), and internal maintenance departments.

The global steam turbine MRO market is segmented by capacity, plant fuel, service type, end-user industry, and geography. By capacity, the market is segment into below 300 MW, 300 to 600 MW, and above 600 MW. By plant fuel, the market is segmented into coal, natural gas, nuclear, and biomass/waste-to-energy. By service type, the market is segmented into maintenance, repair, and overhaul. By end-user industry, the market is segmented into power generation, oil and gas, and industrial and other. The report also covers the market size and forecasts for the steam turbine MRO market across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Below 300 MW |

| 300 to 600 MW |

| Above 600 MW |

| Coal |

| Natural Gas |

| Nuclear |

| Biomass/Waste-to-Energy |

| Maintenance |

| Repair |

| Overhaul |

| Power Generation |

| Oil and Gas (Up-/Mid-/Down-stream) |

| Industrial and Other |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Capacity | Below 300 MW | |

| 300 to 600 MW | ||

| Above 600 MW | ||

| By Plant Fuel | Coal | |

| Natural Gas | ||

| Nuclear | ||

| Biomass/Waste-to-Energy | ||

| By Service Type | Maintenance | |

| Repair | ||

| Overhaul | ||

| By End-user Industry | Power Generation | |

| Oil and Gas (Up-/Mid-/Down-stream) | ||

| Industrial and Other | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of steam turbine MRO market?

The market size stood at USD 22.56 billion in 2026.

What percentage of service revenue came from routine maintenance in 2025?

Maintenance activities accounted for 53.9% of global spending, reflecting the largest steam turbine MRO market share among all service categories.

Which end-user group drives the majority of aftermarket demand?

Utility-scale power generators represented 67.3% of 2025 spending and remain the anchor segment thanks to large coal, gas, and nuclear fleets.

How are industrial cogeneration projects influencing the aftermarket?

Rapid build-out of 5-50 MW micro-CHP turbines in emerging markets is raising demand for localized MRO hubs that can respond within forty-eight hours.

What role do long-term service agreements play in end-user decisions?

LTSAs bundle predictive analytics, spare parts, and availability guarantees, turning unpredictable repair costs into planned expenditures and lowering refinancing risk for asset owners.

Why is repair work expected to outpace maintenance growth?

Aging coal and gas fleets are encountering more fatigue-related blade and rotor issues, pushing repair expenditures to a projected 5.0% CAGR through 2031.

Page last updated on: