Industrial Gas Turbine Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

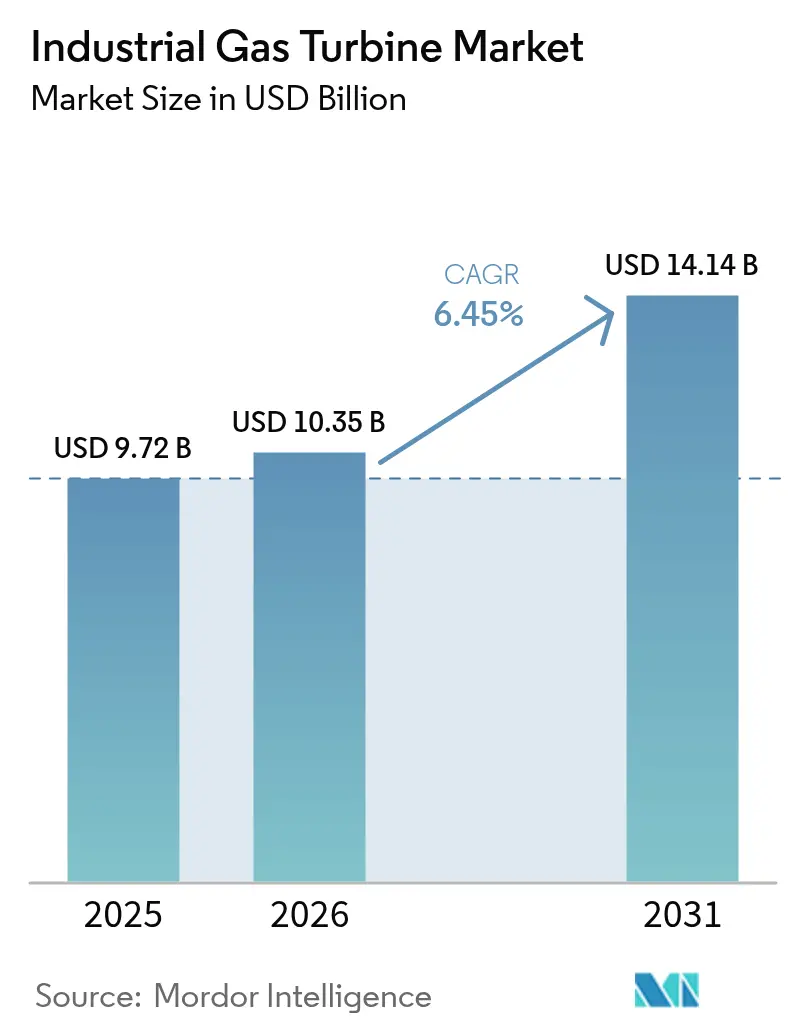

| Market Size (2026) | USD 10.35 Billion |

| Market Size (2031) | USD 14.14 Billion |

| Growth Rate (2026 - 2031) | 6.45% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Gas Turbine Market Analysis by Mordor Intelligence

Industrial Gas Turbine Market size in 2026 is estimated at USD 10.35 billion, growing from 2025 value of USD 9.72 billion with 2031 projections showing USD 14.14 billion, growing at 6.45% CAGR over 2026-2031.

Rapid growth in electricity demand from digital infrastructure, the adoption of hydrogen-ready technology, and utilities’ push for lower-carbon baseload capacity continue to keep the industrial gas turbine market on an upward trajectory. Large-scale capacity additions, particularly in the Asia-Pacific region, align with surging demand for flexible backup generation that complements the rapid growth of renewables. Data-center combined heat and power (CHP) projects, above-300 MW turbines’ efficiency leadership, and mobile modular units for climate-resilient grids collectively reinforce market momentum. Meanwhile, OEMs are racing to mitigate forging and super-alloy constraints, expand their regional production footprints, and validate 100% hydrogen capability to secure long-term relevance.

Key Report Takeaways

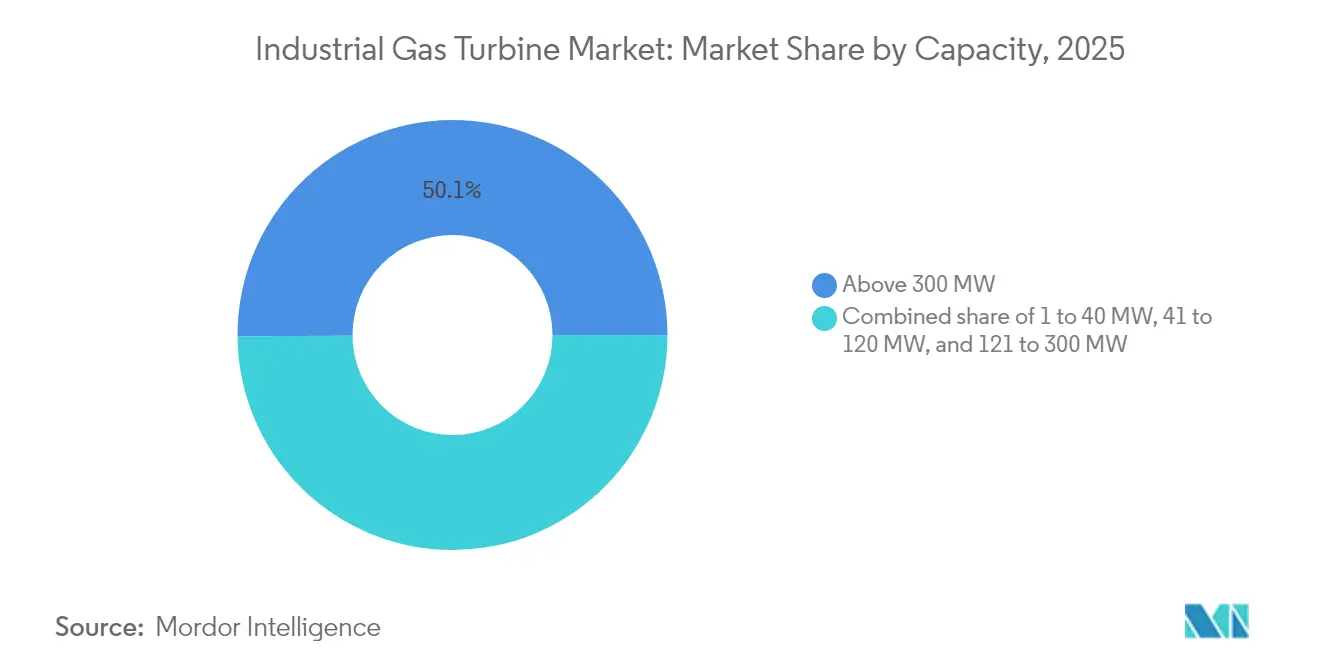

- By capacity, above-300 MW units led the industrial gas turbine market with 50.10% of the market share in 2025, while the 120–300 MW segment is projected to grow at a 9.42% CAGR through 2031.

- By frame type, heavy-duty machines accounted for 69.20% of 2025 revenue; aero-derivative units are projected to exhibit the highest CAGR of 8.2% through 2031.

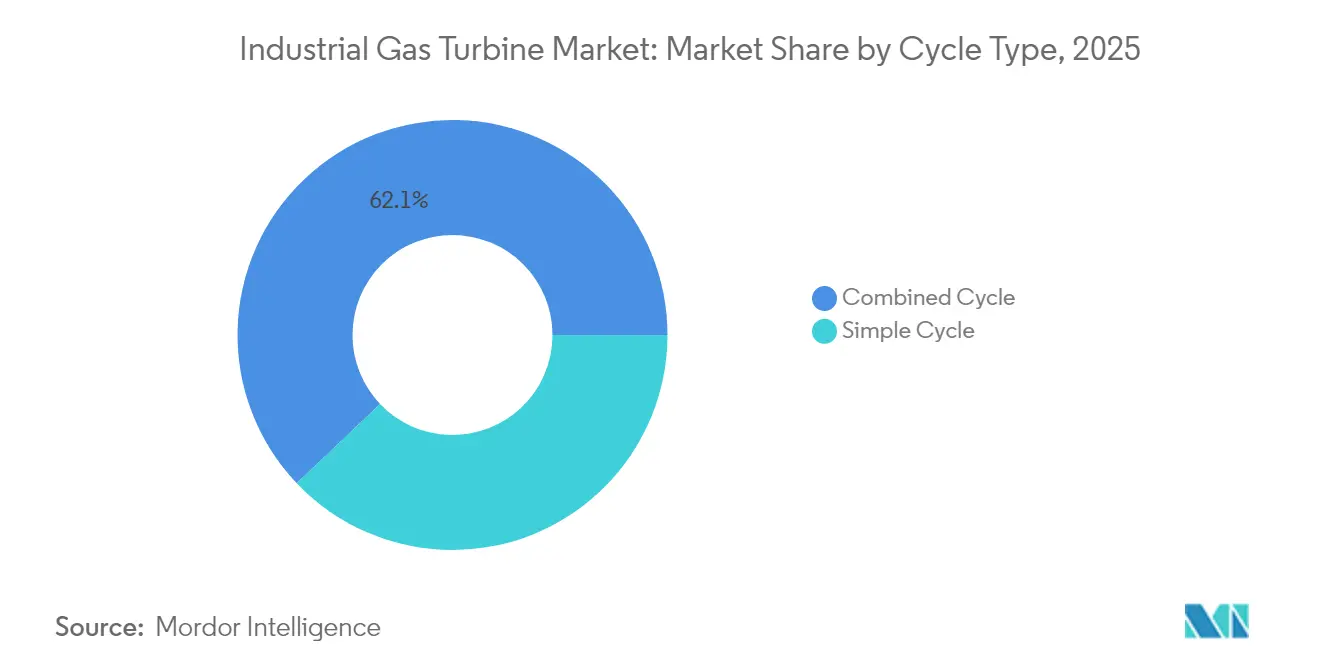

- By cycle, combined-cycle systems captured 62.10% of the industrial gas turbine market size in 2025 and are forecast to grow at a 7.25% CAGR between 2026 and 2031.

- By application, power utilities commanded 70.20% of the 2025 revenue, whereas industrial CHP is projected to advance at a 8.95% CAGR to 2031.

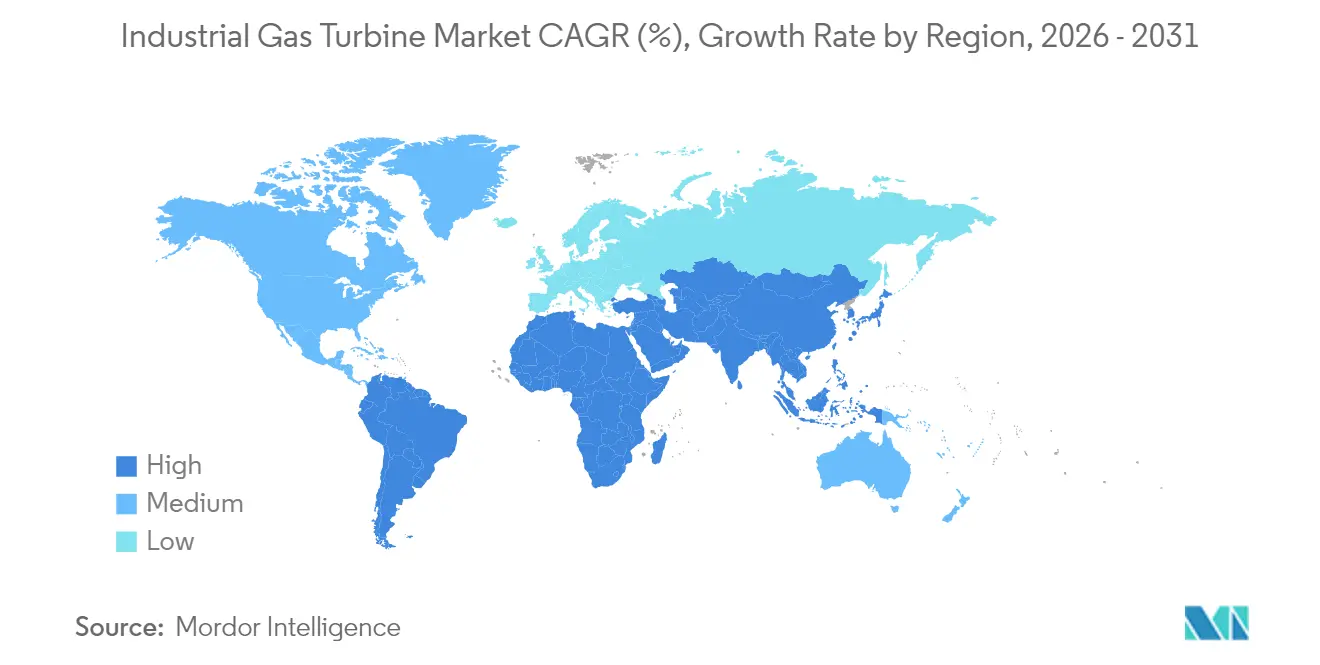

- By geography, Asia-Pacific accounted for 45.60% of global revenue in 2025 and is set to expand at a 6.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Industrial Gas Turbine Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising power demand in emerging economies | +1.80% | Asia-Pacific, Middle East, Africa | Medium term (2–4 years) |

| Coal-to-gas shift in utility generation mix | +1.50% | Global, concentration in Asia-Pacific and Eastern Europe | Long term (≥ 4 years) |

| Renewable-balancing flexibility needs | +1.20% | Global, especially Europe and North America | Short term (≤ 2 years) |

| Data-center CHP build-out surge | +1.00% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Hydrogen-ready industrial retrofits | +0.80% | Europe, North America, Australia | Long term (≥ 4 years) |

| Mobile modular turbines for climate-resilient grids | +0.40% | Global, disaster-prone regions | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Power Demand in Emerging Economies

Nigeria’s 1,350 MW plant, Vietnam’s plan for 84 GW of LNG-based capacity by 2035, and Tanzania’s first combined-cycle facility illustrate how developing nations leapfrog to cleaner gas technology to meet industrialization-driven consumption spikes. Export-credit agencies and multilateral lenders, such as the U.S. International Development Finance Corporation, underpin project bankability, accelerating turbine orders across sub-Saharan Africa. Given their fast-ramp capability and lower particulate emissions compared to coal, regional policymakers view gas turbines as pragmatic complements to renewables.(1)Sumitomo Corporation, “Tanzania Kinyerezi II Combined Cycle Power Plant,” sumitomocorp.com

Coal-to-Gas Shift in Utility Generation Mix

Utilities replacing coal with high-efficiency combined-cycle plants report up to 70% CO₂ reductions and capital cost savings of 30% versus greenfield builds by reusing existing infrastructure. Asian projects such as Guangdong Huizhou deploy 9HA-class turbines capable of 10% hydrogen blends today, with roadmaps to 100%, aligning national decarbonization policies with grid reliability. Cumulative coal-to-gas conversions have already averted 500 million t of CO₂ since 2010, underscoring the transition’s climate significance.

Renewable-Balancing Flexibility Needs

Gas turbines’ sub-5-minute start-up windows provide critical ancillary services as wind and solar penetration climb. A 48 MW UK peaking plant achieves full output in 2.5 minutes, balancing intermittent renewables for 20,000 homes. New designs emphasize fast cycling and part-load efficiency, while hybrid configurations pair aeroderivative turbines with battery systems for multi-hour resilience.

Data-Center CHP Build-Out Surge

AI-driven data centers could require 1,000 TWh by 2030, comparable to Japan’s total electricity demand, and investors are turning to gas turbine-based CHP for reliable, efficient on-site power.(2)International Energy Agency, “Data Centers and Digitalization Outlook 2024,” iea.org LM2500XPRESS packages replace fleets of diesel gensets, cut energy costs by up to 60%, and already operate on hydrogen blends. A USD 10 billion Pennsylvania campus will pair seven 7HA.02 turbines with carbon capture to supply hyperscale compute loads.

Restraints Impact Analysis of Industrial Gas Turbine Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renewables’ LCOE under-cutting gas | -1.40% | Global, notably Europe and North America | Short term (≤ 2 years) |

| Natural-gas price volatility | -0.90% | Global, highest in import-dependent regions | Medium term (2–4 years) |

| Carbon-border tariffs on gas-based exports | -0.60% | Europe with global spillover | Long term (≥ 4 years) |

| Forging & super-alloy supply-chain bottlenecks | -0.80% | Global, tech-manufacturing hubs | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Renewables’ LCOE Under-Cutting Gas

Solar PV costs have plummeted by 90% since 2010 to USD 0.044/kWh, and 81% of new renewables outperform fossil alternatives in price in 2023. Dispatchable value keeps combined-cycle plants competitive where grid services command a premium. Gas turbines, therefore, pivot from baseload to flexible peakers, demanding design upgrades for rapid cycling.

Natural-Gas Price Volatility

LNG spot prices swung 21% up then 29% down within Q4 2023, underscoring geopolitical risk. Forward curves indicate 2025 Asian LNG at USD 13/mmBtu, which is double India’s regulated price, prompting buyers to opt for long-term contracts and diversified fuels.(3)Institute for Energy Economics and Financial Analysis, “LNG Market Tracker Q4 2024,” ieefa.org OEMs answer the uncertainty with dual-fuel capability and higher hydrogen blend limits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Industrial Gas Turbine Market Segment Analysis

By Capacity:

Utility-Scale Units Dominate While Mid-Range Turbines SurgeAbove-300 MW machines accounted for 50.10% of the industrial gas turbine market share in 2025, favored for their capital efficiency and readiness for carbon capture. A flagship 5,300 MW Thai complex using eight M701JAC units illustrates the scale benefits of these giants. In parallel, the 120-300 MW class, the fastest-growing segment at a 9.42% CAGR, caters to modular power schemes, microgrids, and distributed generation. Such projects align perfectly with climate-resilient grid strategies and staged investment models. Supply chain limitations constrain ultralarge frame production slots until 2031, driving customers toward the mid-range, where lead times are shorter and shipment logistics simpler.

OEMs continuously refine combustion systems for both classes, initially targeting 50% hydrogen blends and pathways to 100% by upgrading burners and control software. The mid-range units' industrial gas turbine market size is projected to expand significantly as governments incentivize the rapid deployment of low-carbon capacity.

By Frame Type:

Heavy-Duty Reliability Outweighs Aero-Derivative Agility—Yet Growth Favors the LatterHeavy-duty configurations secured 69.20% of 2025 revenue, a testament to their multidecade lifecycle in baseload service. Efficiency now exceeds 64% in combined-cycle mode with the latest HL platforms. Aero-derivative packages, which account for just 30.80% of revenue, are expected to expand at an 8.2% CAGR through 2031, driven by demand for 10-50 MW blocks that can cold-start in minutes. LM2500XPRESS units, for instance, shave construction schedules by 40% and accept 35% green hydrogen from day one. Heavy-duty vendors address this by modularizing auxiliary skids and shortening outage windows, thereby narrowing the total-cost-of-ownership gaps with the aero-fleet.

By Cycle:

Combined Cycle Efficiency Drives Market PreferenceCombined cycle units accounted for 62.10% of the industrial gas turbine market share in 2025 and are projected to record a 7.25% CAGR during 2026–2031, underscoring their clear cost-to-performance edge over simple-cycle alternatives. Their ability to push facility efficiencies beyond 60% by harvesting exhaust heat for steam generation cements their role in baseload and intermediate duty, especially where carbon regulations favor high thermal performance. Projects such as Saudi Arabia’s Taiba and Qassim complexes demonstrate how utilities can fast-track multi-gigawatt expansions while reducing CO₂ emissions by 60% compared to oil-fired plants. Simple-cycle packages remain relevant for peaking service, emergency backup, and markets that prize rapid dispatch at lower upfront cost.

Continuous upgrades to heat-recovery steam generators and tighter steam-turbine integration shrink installation windows and boost operating flexibility. China’s Zhoushan plant illustrates the trajectory: its 9HA.02 turbines began service on a 10% hydrogen blend with scope to reach 50%, proving combined-cycle assets can migrate toward cleaner fuels without sacrificing efficiency. Modular balance-of-plant skids and factory-finished HRSG sections compress construction schedules, a decisive benefit as grid operators rush to pair high-renewable penetration with firm capacity. As a result, the combined-cycle slice of the industrial gas turbine market size is expected to expand in absolute terms, even as simple-cycle orders remain steady in niche applications.

By Application:

Power Utilities Lead While Industrial CHP AcceleratesPower utilities dominated the sector, accounting for 70.20% of the industrial gas turbine market size in 2025, reflecting the continual expansion of the grid and the replacement of aging coal assets. Large integrated utilities value turbine durability, high efficiency, and compatibility with emerging carbon capture systems as they modernize their baseload fleets. In contrast, industrial combined heat and power (CHP) is the fastest riser, with a 8.95% CAGR through 2031, driven by energy-intensive manufacturers seeking efficiency gains and lower Scope 1 emissions. The switch from coal boilers to gas-turbine CHP at Tate & Lyle’s plant lifted overall efficiency above 80% while sharply reducing pollutants, showcasing the segment’s economic rationale.

Industrial CHP economics remain compelling: facilities capture 20–60% in energy-cost savings and trim demand charges by more than 40% compared to separate heat-and-power configurations. Data centers now form a high-growth subsegment, repurposing turbine exhaust for absorption chillers that support rack cooling. U.S. Environmental Protection Agency studies confirm that gas-turbine CHP can achieve an overall efficiency of 80% or higher, a metric prized by regulators and investors. In marine propulsion, Baker Hughes and Hanwha’s small ammonia-fueled turbine under development mirrors the wider market pivot toward cleaner fuels. Collectively, these trends position CHP and specialized industrial uses to claim a larger share of the industrial gas turbine market, even as the utility segment retains its volume leadership.

Geography Analysis

APAC Industrial Gas Turbine Market

The Asia-Pacific region accounted for 45.60% of global revenue in 2025, driven by coal-to-gas transitions, relentless urbanization, and state-backed investment. China's hydrogen-ready Zhoushan project and Vietnam's 84 GW LNG roadmap exemplify policy commitment to swift decarbonization without compromising energy security. India's upgrading of gas pipeline infrastructure and Australia's peaking-plant mandates further reinforce regional appetite. The Asia-Pacific's industrial gas turbine market is the world's largest and is projected to grow at a 6.75% CAGR in the region.

The Americas and EMEA Industrial Gas Turbine Market

North America's mature fleet continues to expand through data center CHP and renewable projects. Duke Energy's booking of up to 11 American-made 7HA turbines speaks to robust domestic demand, heavy states. Europe's focus has shifted to hydrogen readiness and carbon-capture-enabled technologies, as seen in EnBW's Stuttgart-Münster installation. In the Middle East, Vision 2030 initiatives translate into multigigawatt tenders in Saudi Arabia and the UAE, where natural gas remains a strategic bridge fuel. Africa showcases several projects, such as Nigeria's 1,350 MW plant, which will supply 11% of the nation's demand. South America selectively adds high-efficiency combined-cycle stations, with Brazil emphasizing dispatchable capacity to firm its hydro-dominant grid.

Competitive Landscape

GE Vernova, Siemens Energy, and Mitsubishi Power collectively hold about 70% of the global industrial gas turbine market share, producing frames from 5 to 575 MW. Supply chain stress hiked new-build lead times to as much as five years, prompting GE Vernova’s USD 600 million Greenville expansion and Siemens Energy’s tooling reshoring for hot-gas-path components.(4)RBN Energy, “Gas Turbine Supply Chain Bottlenecks Report 2025,” rbnenergy.com Strategic alliances are proliferating: Baker Hughes teams with Hanwha on small ammonia turbines, while IHI partners with GE Vernova on ammonia combustors, accelerating alternative-fuel roadmaps.

Aftermarket service, worth a cumulative USD 302 billion this decade, drives consolidation. One Equity Partners’ acquisition of EthosEnergy broadens turbine-overhaul capacity to meet swelling demand from fleets commissioned in the 2000s. Mobile solutions and data-center CHP represent white-space arenas where niche aero-derivative specialists compete fiercely with traditional utility-scale OEMs. Competitive differentiation is sharpening around validated 100% hydrogen firing, integrated digital twins, and carbon-capture-ready islanded blocks.

Industrial Gas Turbine Industry Leaders

Siemens AG

Mitsubishi Heavy Industries Ltd

Harbin Electric International Company Limited

Kawasaki Heavy Industries Ltd

General Electric Company

- *Disclaimer: Major Players sorted in no particular order

Industrial Gas Turbine Market Companies Covered in this Report

- GE Vernova (General Electric)

- Siemens Energy

- Mitsubishi Power

- Ansaldo Energia

- Harbin Electric

- Bharat Heavy Electricals

- Kawasaki Heavy Industries

- Solar Turbines (Caterpillar)

- MAN Energy Solutions

- MTU Aero / Vericor

- Baker Hughes

- Rolls-Royce Power Systems

- Doosan Enerbility

- Shanghai Electric

- Capstone Green Energy

- OPRA Turbines

- Triveni Turbines

- Alstom (GE Gas Power heritage)

- Elliott Group

- Centrax Industries

Recent Industry Developments in Industrial Gas Turbine Market

- May 2025: GE Vernova secured a significant deal in Saudi Arabia, valued at up to USD 14.2 billion, to supply heavy-duty gas turbines manufactured in Greenville, SC, for projects supporting Saudi Vision 2030.

- April 2025: Duke Energy will purchase up to 11 GE Vernova 7HA gas turbines as part of a new partnership aimed at meeting growing energy demands. This deal is underpinned by GE Vernova's USD 600 million investment to expand its Greenville, South Carolina, manufacturing facility, which will add 1,500 jobs.

- March 2025: Honeywell agreed to buy Air Products’ LNG process technology business for USD 1.81 billion, strengthening end-to-end natural-gas solutions.

- February 2025: Baker Hughes and Hanwha have partnered to develop and commercialize 16 MW ammonia-fueled marine turbines by 2027. This collaboration leverages Baker Hughes' small-sized gas turbine technology and Hanwha's expertise in ammonia combustion systems.

- January 2025: Chevron, Engine No. 1, and GE Vernova are collaborating to develop 4 GW of data center power capacity using GE Vernova's 7HA gas turbines, which feature carbon capture technology capable of capturing over 90% of CO2 emissions.

Global Industrial Gas Turbine Market Report Scope

A gas turbine is a type of combustion engine that can transform liquid fuels, such as natural gas, into mechanical energy. This power then propels a generator, which creates the electrical energy that transmits along power lines to residences and commercial buildings.

The industrial gas turbine market is segmented by capacity, technology type, application, and geography. By capacity, the market is segmented into 1 to 40 MW, 41 to 120 MW, 121 to 300 MW, and above 300 MW. By technology type, the market is segmented into the combined cycle and simple cycle. By application, the market is segmented into power, oil and gas, and other applications. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. For each segment, the market sizes and forecasts are based on revenue (USD).

Segmentation Overview

| 1 to 40 MW |

| 41 to 120 MW |

| 121 to 300 MW |

| Above 300 MW |

| Aero-derivative |

| Heavy-duty |

| Simple Cycle |

| Combined Cycle |

| Power Utilities |

| Oil and Gas |

| Industrial CHP |

| Marine and Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia | |

| Rest of Asia Pacific | |

| South America | Argentina |

| Brazil | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Capacity | 1 to 40 MW | |

| 41 to 120 MW | ||

| 121 to 300 MW | ||

| Above 300 MW | ||

| By Frame Type | Aero-derivative | |

| Heavy-duty | ||

| By Cycle | Simple Cycle | |

| Combined Cycle | ||

| By Application | Power Utilities | |

| Oil and Gas | ||

| Industrial CHP | ||

| Marine and Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia | ||

| Rest of Asia Pacific | ||

| South America | Argentina | |

| Brazil | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Industrial Gas Turbine Market?

The Industrial Gas Turbine Market size is expected to reach USD 10.35 billion in 2026 and grow at a CAGR of 6.45% to reach USD 14.14 billion by 2031.

What is the current size of the industrial gas turbine market?

The industrial gas turbine market size stood at USD 10.35 billion in 2026 and is on track to hit USD 14.14 billion by 2031.

Which region leads the industrial gas turbine market?

Asia-Pacific dominates with 45.60% revenue share in 2025, propelled by coal-to-gas transitions and robust infrastructure investments.

Why are data centers adopting gas turbine CHP systems?

Gas turbine CHP delivers up to 60% energy cost savings and high reliability, meeting stringent uptime needs while enabling future hydrogen fuel use.

How fast can mobile gas turbines be deployed?

TM2500 units can be installed in as few as 11 days, supplying 20–35 MW blocks for emergency or temporary grid support.

What share do combined-cycle turbines hold?

Combined-cycle configurations accounted for 62.10% of industrial gas turbine market share in 2025 thanks to efficiencies above 60%.

Page last updated on: