Burkina Faso Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

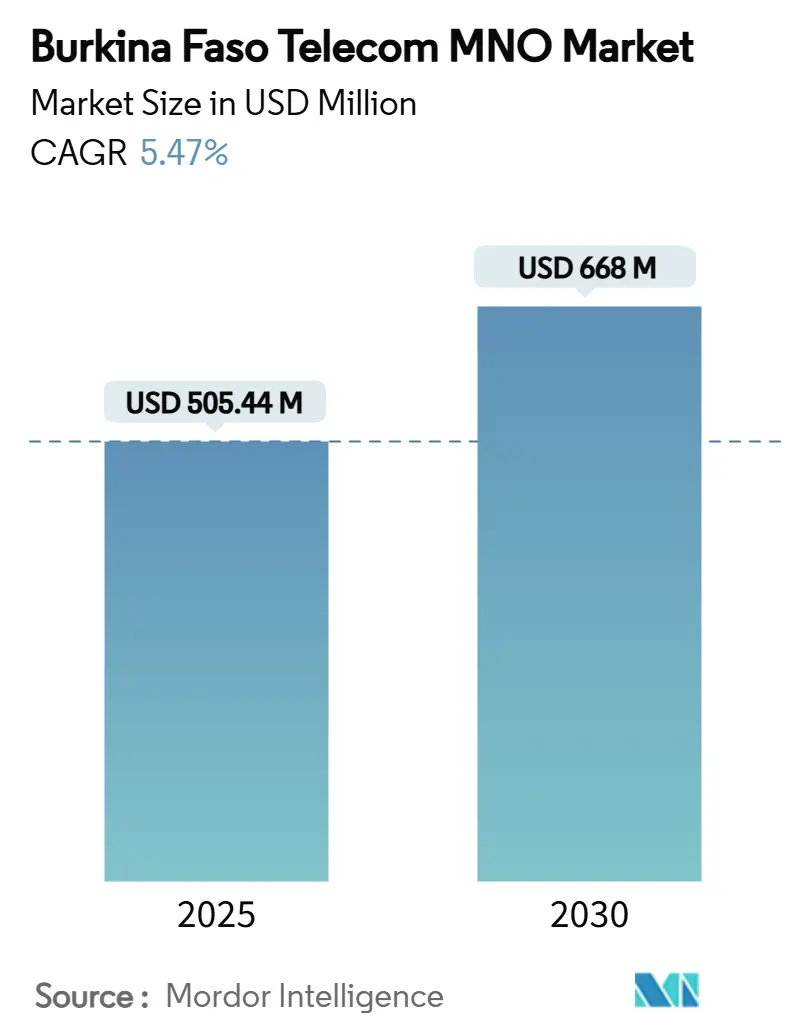

| Market Size (2025) | USD 505.44 Million |

| Market Size (2030) | USD 668 Million |

| Growth Rate (2025 - 2030) | 5.47% CAGR |

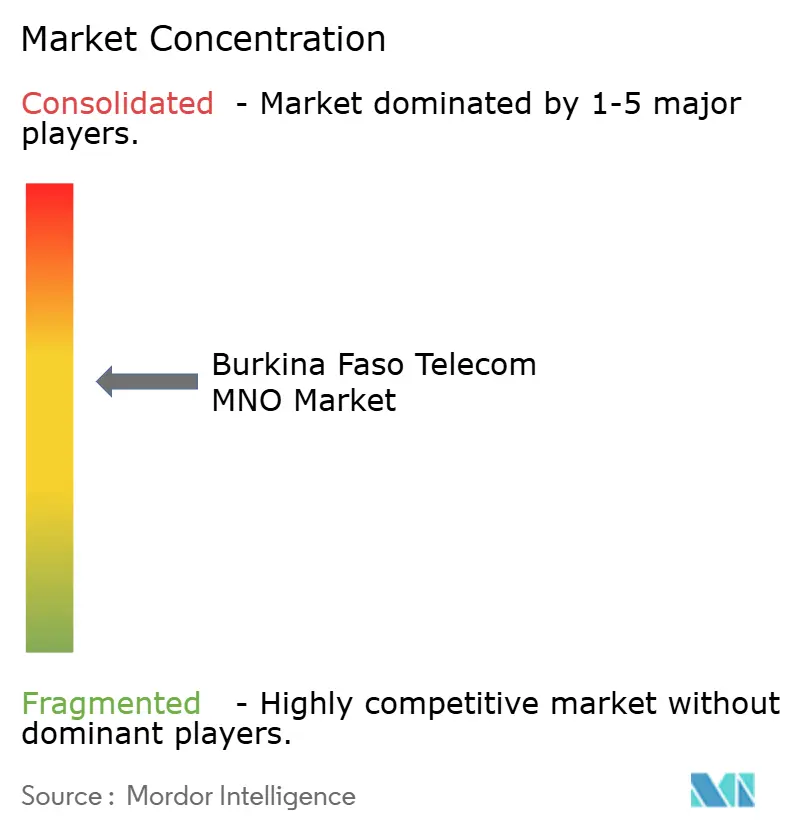

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Burkina Faso Telecom MNO Market Analysis by Mordor Intelligence

The Burkina Faso Telecom MNO Market size is estimated at USD 505.44 million in 2025, and is expected to reach USD 668 million by 2030, at a CAGR of 5.47% during the forecast period (2025-2030).

Robust universal-service funding, the surge in mobile money usage, and expanding enterprise digitization are the prime forces propelling this trajectory. The sector’s outsized contribution to national GDP keeps policy makers focused on connectivity as a socioeconomic priority, which in turn encourages operators to densify networks even in difficult security zones. Infrastructure sharing among the three mobile network operators (MNOs) lowers capital intensity, while wholesale fiber investments widen backhaul capacity and lift data quality. Yet currency shortages, site inaccessibility in conflict-affected regions, and low ARPU levels temper the pace at which emerging technologies such as 5G become commercially viable. The Burkina Faso telecom market continues to demonstrate resilience by aligning public-sector digital projects, mobile financial services, and regional fiber corridors into a mutually reinforcing growth loop.

Key Report Takeaways

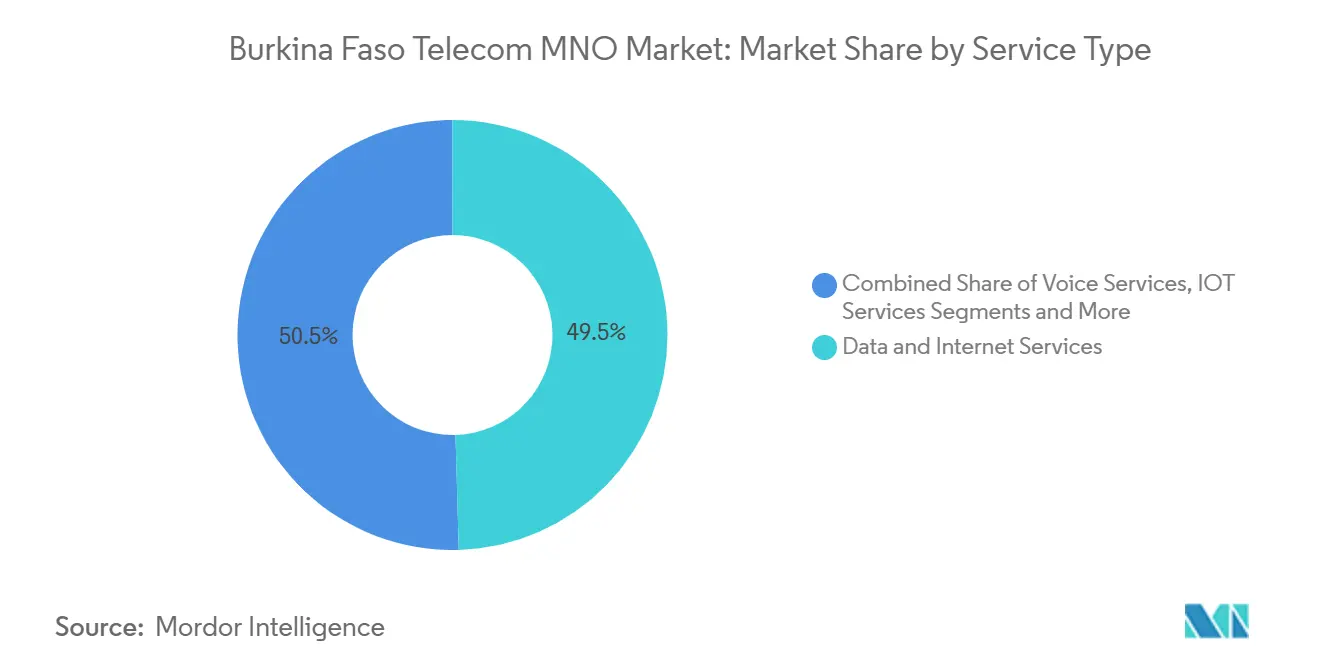

- By service type, voice services led with 40.04% of Burkina Faso telecom market share in 2024, while data services are advancing at a 5.80% CAGR through 2030.

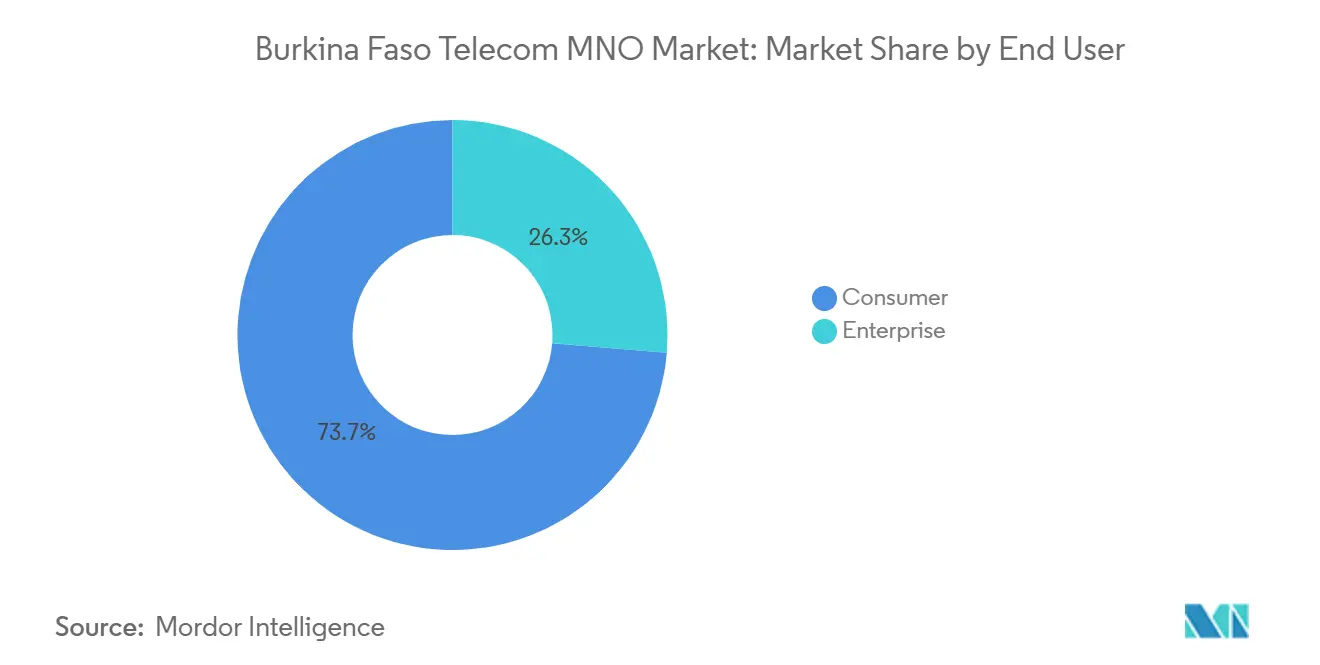

- By end-user, the consumer segment accounted for 73.69% share of the Burkina Faso telecom market size in 2024, whereas the enterprise segment is growing at a 6.13% CAGR to 2030.

Burkina Faso Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid mobile-data substitution for cash-based transactions | +1.2% | National, early gains in Ouagadougou and Bobo-Dioulasso | Short term (≤ 2 years) |

| Government USF program for 1,000 “white-zone” sites | +1.0% | Rural areas across 145 municipalities | Medium term (2-4 years) |

| Growing enterprise demand for managed IoT agriculture | +0.8% | Cotton and cereal belts in western and central provinces | Long term (≥ 4 years) |

| Wholesale fiber-backbone extension to 145 municipalities | +0.9% | National backbone connecting regional hubs | Medium term (2-4 years) |

| Orange/Moov tower-sharing initiatives | +0.6% | Nationwide | Short term (≤ 2 years) |

| Surge in regional content driving Pay-TV bundling | +0.4% | Urban centers expanding toward secondary towns | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid mobile-data substitution for cash-based transactions

Mobile money has evolved from simple person-to-person transfers into a full digital finance ecosystem that underpins everyday commerce. The launch of the government-backed FASO ARZEKA platform in 2025 bolsters national sovereignty over payments infrastructure and creates network effects that lift data ARPU for operators[1]Africa News Agency, “Burkina Faso: The Government Launched Digital Payment Platform FASO ARZEKA,” africa-news-agency.com . Orange Money’s 5.2 million active users and Moov Money’s 2 million reinforce how financial inclusion now hinges on stable mobile broadband. Transaction traffic generates continuous data sessions that displace legacy voice revenues yet enhances service stickiness, especially in markets with low banking penetration. World Bank–supported modernization of treasury payments funnels public-sector salaries and social benefits through mobile channels, anchoring institutional demand for reliable 4G coverage. Operators able to guarantee low-latency data links thus secure a competitive edge and open adjacent revenue lines in micro-lending and insurance.

Government USF program for 1,000 “white-zone” sites

The Universal Access and Service Fund earmarked CFA 6.2 billion (USD 10.47 million) to light up 1,000 underserved localities by 2027, the largest single telecom infrastructure push in Burkina Faso’s history. Public-private risk-sharing lowers roll-out barriers in villages where thin household incomes limit operator returns. Wholesale backbone fibers run alongside rural roads, enabling each MNO to plug in without duplicating trenches, while ARCEP enforces open-access rules that maintain competitive neutrality. Current 3G and 4G footprints—64% and 46% respectively—show ample headroom for cell-site densification. Because the program targets communes along agricultural corridors, improved connectivity concurrently advances e-agriculture and digital-health initiatives, compounding the driver’s positive weight on CAGR through mid-decade.

Growing enterprise demand for managed IoT agriculture solutions

Enterprises—especially agribusiness cooperatives and commercial farms—turn to sensor-driven irrigation, livestock tracking, and climate monitoring in response to erratic rainfall patterns. Field trials confirm that Bluetooth Low Energy and LoRa mesh architectures cut power needs and triple sensor range in Sahelian environments. This proof of concept helps elevate enterprise revenue, projected to rise at a 6.13% CAGR through 2030. The same connectivity enables seamless produce payments via mobile wallets, binding data and finance into a single service bundle. Operators emphasize turnkey platforms that include analytics dashboards and predictive crop modeling, allowing them to charge higher rates than plain bandwidth. Over time, embedded SIM modules in farm machinery create annuity-like subscription flows, stabilizing cash generation even when consumer growth plateaus

Wholesale fiber-backbone extension to 145 municipalities

Completion of cross-country fiber spines reduces dependency on high-OPEX microwave links and satellite backhaul. Orange’s Djoliba network layers 10,000 km of terrestrial fiber with coastal cable landings, providing Burkina Faso with diverse redundant paths to global internet hubs. The September 2020 launch of a local internet exchange point shortened routing distances, slashing latency for streaming and cloud applications. Rural broadband providers can now lease dark fiber on cost-based terms, a regulatory condition that prevents backbone bottlenecks. Government agencies under the eBurkina program tap this capacity to interlink data centers, boosting demand for carrier-grade services. In aggregate, the backbone lowers per-MB transport cost, enabling operators to widen 4G data allowances without eroding EBITDA margins.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Security-related site inaccessibility (≈ 15% BTS offline) | -1.8% | Northern and eastern conflict-affected provinces | Short term (≤ 2 years) |

| Foreign-exchange shortage inflating equipment imports | -1.1% | Nationwide | Medium term (2-4 years) |

| SIM-tax and two-SIM cap dampening multi-SIM uptake | -0.7% | National regulatory environment | Long term (≥ 4 years) |

| Low ARPU limiting 5G business-case viability | -0.9% | Rural districts with sparse population | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Security-related site inaccessibility affecting network operations

Heightened insurgent activity makes 15% of base-transceiver stations unreachable for maintenance or diesel refueling, directly curtailing available network capacity. Orange confirmed dozens of sites forced offline due to staff safety concerns, while Telecel and Moov report similar outages. Service blackouts erode consumer trust and prompt SIM churn toward operators perceived as more resilient, although all carriers suffer in absolute terms. Emergency public spending—about CFA 3 billion—earmarks tower reconstruction, yet new installations remain vulnerable until broader security improves. Operators deploy solar-powered small cells with remote monitoring to limit technician exposure, but such investments push up cost per covered user, squeezing margins during the forecast horizon.

Foreign-exchange shortages inflating equipment import costs

The CFA franc’s peg to the euro smooths daily volatility, but falling gold and cotton receipts shrink hard-currency reserves, making letters of credit harder to obtain for radio access network imports [2]International Monetary Fund African Dept., “Growth and Structural Transformation,” International Monetary Fund, imf.org . Vendors now demand down-payments in euros, pressuring operator liquidity and prolonging procurement cycles. Leased-equipment models and regional bulk purchasing mitigate the expense, yet they delay modern-cell activation dates, holding back capacity upgrades. Escalating costs spill into tariffs unless offset by efficiency gains from tower sharing. The restraint weighs more heavily on 5G roadmaps, whose economics already look challenging in low-ARPU rural districts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data services drive revenue transformation

The Burkina Faso telecom market size for data and internet services was USD 139 million in 2024 and is expanding at a 5.80% CAGR, eclipsing growth in legacy voice lines. Voice retained 40.04% Burkina Faso telecom market share in 2024 with USD 187.4 million in revenue, yet its plateau underscores the transition toward digital-first consumption. Operators monetize data through social-media bundles, video streaming, and zero-rated mobile-money access, strategies that raise effective price per gigabyte without deterring volumes. IoT services, though holding only 3.46% share, mark the first specialized revenue pillar outside consumer connectivity; crop-sensor connectivity plans command roughly five times the ARPU of standard prepaid lines. Over-the-top (OTT) and Pay-TV offerings, at 3.19% share, link linear television with catch-up content delivered over 4G, helping carriers upsell entertainment to urban subscribers. Messaging and other value-added services face substitution by third-party apps, propelling carriers to pivot toward application programming interfaces (APIs) for enterprise customers.

Sustained data demand benefits from wholesale capacity additions and local content caches introduced at the Ouagadougou internet exchange. Orange’s collaboration with OpenAI and Meta on multilingual AI models introduces voice-assistant services in indigenous languages, differentiating its broadband propositions [3]Ryan Browne, “Orange Partners with OpenAI, Meta to Develop Custom African-Language AI Models,” CNBC, cnbc.com . The approach positions data as the default medium for commerce, education, and public-service delivery, which in turn supports incremental growth in the Burkina Faso telecom market. Meanwhile, Moov’s affordable Night Pass plans capture price-sensitive youth segments, maintaining competitive balance even as market concentration stays moderate. Telecel leverages new international bandwidth secured in March 2024 to lower backhaul cost, translating into larger data allowances that help stem churn.

By End-User: Enterprise segment accelerates digital adoption

Enterprises generated USD 123.1 million in 2024 and will grow at 6.13% CAGR, outpacing the consumer base as corporate customers adopt managed security, cloud connectivity, and precision-agriculture platforms. Demand arises from diversified service sectors—public administration, financial services, and logistics—accounting for 43.6% of national GDP. Government digitization programs, such as eBurkina, require secure virtual private networks and high-availability links, pushing each operator to create dedicated business units. Bundled IoT and mobile-money packages let cooperatives automate produce payments, an offering that locks in both connectivity and transaction fees.

The consumer segment still commands 73.69% Burkina Faso telecom market share, equal to USD 344.9 million in 2024, but its CAGR is leveling off as SIM density approaches one per adult in metropolitan areas. Growth persists in underserved rural districts where the 1,000-site USF rollout will open fresh coverage pockets. Device affordability schemes, including operator-subsidized 4G handsets, accelerate first-time smartphone adoption, thereby sustaining data-traffic momentum. Yet price elasticity remains high, mandating careful calibration of bundle sizes to protect margins. Cross-selling of micro-insurance and pay-as-you-go solar kits via USSD channels offers incremental revenue opportunities without heavy capital outlays.

Geography Analysis

Burkina Faso’s telecom footprint covers 85% of the population, but network quality, speed, and resilience vary sharply among its thirteen administrative regions. Ouagadougou and Bobo-Dioulasso enjoy near-ubiquitous 4G, enabling fintech hubs and streaming start-ups to flourish. Secondary cities such as Koudougou and Banfora exhibit rising data uptake following backbone expansion, yet peak-hour congestion persists until additional spectrum refarming in 2026. Rural northern provinces confront the twin hurdles of sparse power infrastructure and security risks, factors that explain lower voice traffic and higher tower-downtime ratios.

International fiber paths interlocking with coastal cable landings in Côte d’Ivoire and Ghana mitigate landlocked-country penalties for transit pricing. Orange’s Djoliba ring gives Burkina Faso redundant south-west and south-east exits, cutting latency to key European internet exchanges and enabling cloud-based enterprise applications. Wholesale capacity trades on open-access terms under ARCEP oversight, allowing smaller ISPs to deliver competitively priced fixed-wireless broadband to schools and clinics.

Regional integration inside ECOWAS supports roaming-rate harmonization, which reduces bill shock for cross-border traders and seasonal farm workers. The policy complements Burkina Faso’s ambition to become a fiber transit corridor between Sahelian neighbors and Atlantic gateways. Simultaneously, security disruptions in Soum, Oudalan, and Yagha provinces downsize potential subscriber bases. ARCEP, in coordination with defense agencies, expedites temporary spectrum permits for rapid-deploy base stations in resettlement camps, sustaining basic connectivity during humanitarian operations. The interplay of opportunity and risk shapes a diversified growth map that rewards operators capable of agile capital deployment and nuanced pricing.

Competitive Landscape

The market hosts three principal licensees—Orange Burkina Faso, Moov Africa, and Telecel Faso—collectively serving more than 22 million SIMs. Orange leverages its pan-African scale to negotiate global transit deals and secure exclusive international gateway rights through its July 2024 agreement with VOX Solutions, lifting international call quality while compressing wholesale cost. Moov, a subsidiary of Maroc Telecom, positions itself as the price-value champion, pioneering tower-sharing to optimize capex and extending mobile-money rails to 2 million active wallets. Telecel aligns with regional fiber consortia to unlock fresh backhaul and aims to differentiate via enterprise-grade service-level agreements.

Moderate concentration allows each operator to carve distinct niches without resorting to ruinous price wars. Infrastructure sharing now covers roughly 40% of active towers, and joint-fiber trenching in peri-urban areas trims construction timelines. Product innovation takes center stage: Orange bundles video-streaming vouchers, Moov pairs voice-centred plans with zero-rated messaging, and Telecel promotes cloud storage for SMEs. Enterprise verticalization—agriculture, mining, public administration—creates specialized go-to-market squads offering connectivity plus sector-specific software.

Regulation remains predictably pro-competition. ARCEP renews spectrum licenses based on rollout obligations and enforces quality-of-service audits that publicize dropped-call and data-throughput scores. The watchdog’s transparency nudges carriers to invest defensively in network upgrades, underpinning customer satisfaction even where macroeconomic headwinds constrain discretionary spend. Against this backdrop, possible new entrants may exploit niche opportunities in wholesale satellite backhaul or neutral host indoor coverage, though no immediate fourth-license issuance is on the docket.

Burkina Faso Telecom MNO Industry Leaders

Orange Burkina Faso

Onatel (Telmob)

Telecel Faso

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Orange Africa and Eutelsat formed a satellite-internet partnership leveraging the KONNECT spacecraft to deliver up to 100 Mbps broadband in hard-to-reach Burkinabè localities.

- February 2025: The government, backed by the World Bank, detailed a USD 150 million PACT DIGITAL plan that will extend coverage to 500 localities and finalize a national data center.

- July 2024: Orange Burkina Faso appointed VOX Solutions as its exclusive international gateway, enhancing routing efficiency and voice clarity.

- March 2024: Telecel secured new international capacity, bolstering its consumer and enterprise offerings.

Burkina Faso Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumers |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumers |

Key Questions Answered in the Report

What is driving revenue growth for operators?

Universal-service funding, rapid mobile-money adoption, and managed IoT solutions in agriculture are the key contributors to top-line expansion.

Which service type is growing the fastest?

Data and internet services post the strongest 5.80% CAGR as consumer habits shift to digital communications and streaming.

Why is enterprise demand accelerating?

Public-sector digitization and agribusiness precision-farming projects require secure, high-bandwidth links, pushing enterprise revenue higher at 6.13% CAGR.

What challenges limit 5G roll-out?

Low ARPU and foreign-exchange constraints raise the payback threshold, while security-related site inaccessibility inflates deployment risk.

Page last updated on: