Algeria Telecom MNO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.68 Billion |

| Market Size (2026) | USD 2.73 Billion |

| Market Size (2031) | USD 2.97 Billion |

| Growth Rate (2026 - 2031) | 1.75% CAGR |

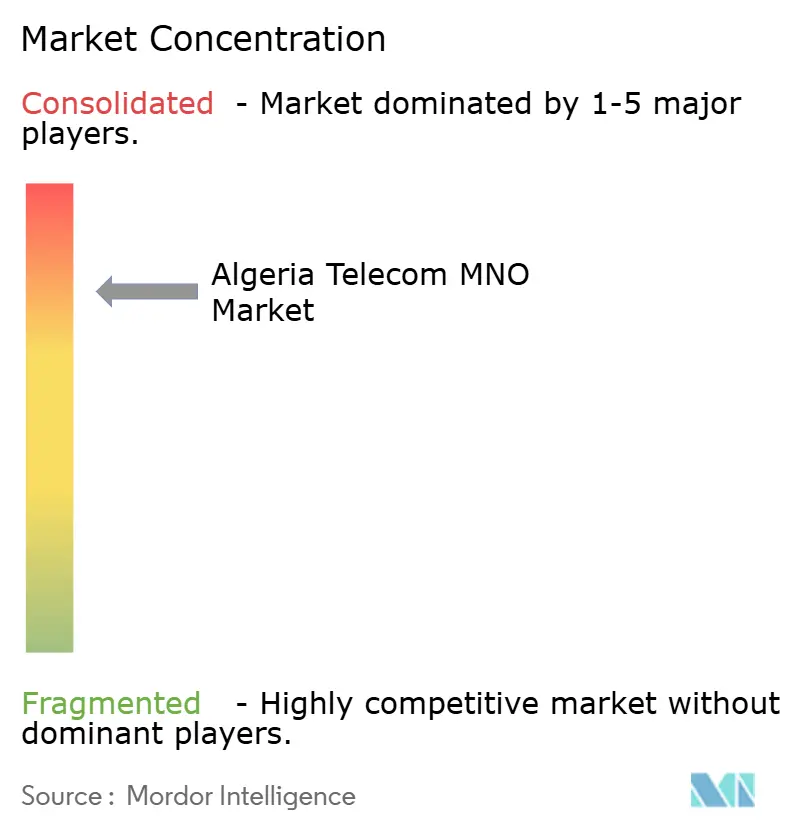

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Algeria Telecom MNO Market Analysis by Mordor Intelligence

The Algeria Telecom MNO Market size in 2026 is estimated at USD 2.73 billion, growing from 2025 value of USD 2.68 billion with 2031 projections showing USD 2.97 billion, growing at 1.75% CAGR over 2026-2031.

Much of this measured growth flows from a sharp pivot to data-heavy usage, as 36 million mobile internet users translate into a 77% penetration rate, while total mobile connections of 54.8 million reflect a 116% SIM-per-capita ratio. Revenue is migrating from legacy voice toward broadband because affordable 4G devices, larger data bundles, and government-subsidized fiber are stimulating bandwidth consumption in both urban and rural districts. Competitive positioning remains shaped by state influence more than pure market forces: Mobilis leads on coverage, Djezzy excels in dense metros, and Ooredoo focuses on operational efficiency. Strategic opportunities now revolve around wholesale fiber corridors, enterprise 5G fixed-wireless access, and oil-and-gas telemetry, even as currency-convertibility rules inflate equipment costs and temper private capital flows.

Key Report Takeaways

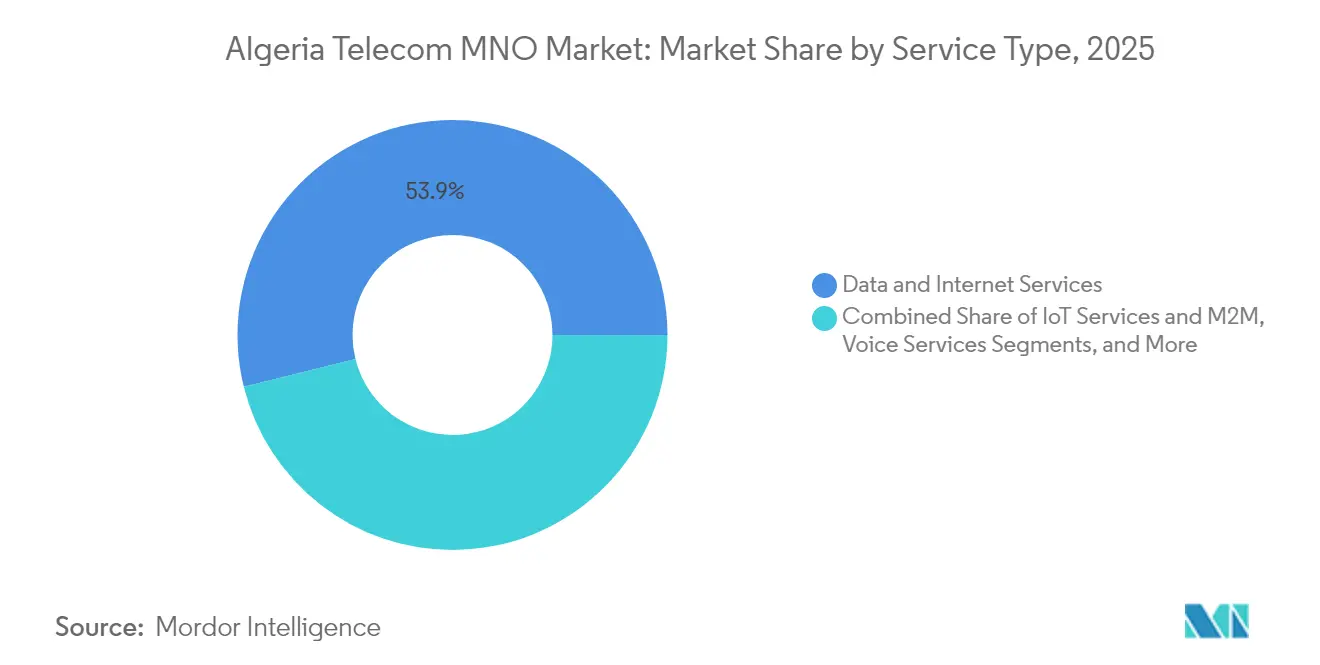

- By service type, data and internet captured 53.86% of Algeria telecom MNO market share in 2025, while IoT & M2M is advancing at a 1.86% CAGR through 2031.

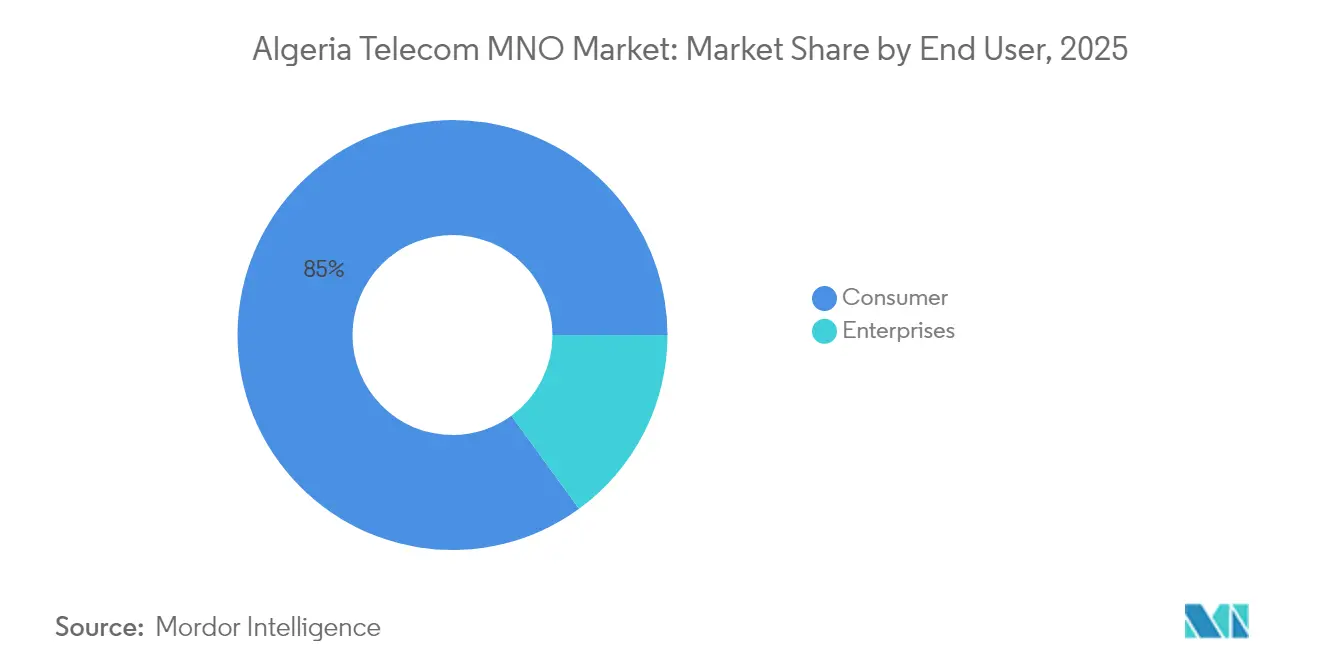

- By end user, the consumer segment commanded 85.02% of the Algeria telecom MNO market size in 2025; the enterprise segment is projected to grow at 2.46% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Algeria Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in mobile data usage driven by affordable 4G smartphones | +0.8% | National, early gains in Algiers, Oran, Constantine | Medium term (2-4 years) |

| Government-led FTTH rollout & wholesale fiber backbone projects | +0.4% | National, concentrated in urban centers | Long term (≥ 4 years) |

| Upcoming 5G spectrum auctions unlocking enterprise FWA potential | +0.3% | National, initial focus on major cities | Medium term (2-4 years) |

| Rapid digitization of public services and mobile-payment ecosystems | +0.2% | National, public administration and banking | Short term (≤ 2 years) |

| Cross-border fiber corridors opening new wholesale revenue streams | +0.1% | Border regions, international gateways | Long term (≥ 4 years) |

| Rising IoT demand from oil & gas telemetry in Sahara fields | +0.1% | Southern Algeria, oil & gas basins | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Mobile Data Usage Driven by Affordable 4G Smartphones

Mobile data traffic is eclipsing voice and SMS volumes because device prices have fallen and prepaid data bundles are aggressively promoted. Operators report network densification programs that prioritize 1,800 MHz and 2,100 MHz spectrum refarming to accommodate the surge. The 54.8 million mobile connections recorded in 2025 far exceed the population, indicating multi-SIM behavior shaped by promotions and network-quality variation. Monetization still lags usage because prepaid accounts dominate and average revenue per user (ARPU) remains under pressure. Even so, higher data consumption is nudging operators to accelerate content partnerships and introduce tiered quality-of-service plans to protect profitability. [1] Rami Ammari, “Algeria Mobile Network Experience Report,” Opensignal, OPENSIGNAL.COM

Government-Led FTTH Rollout and Wholesale Fiber Backbone Projects

With 1.8 million fiber subscribers, Algeria posts the largest FTTH base in North Africa and offers residential speeds up to 1.2 Gbps, the fastest in Africa. The wholesale backbone under Algeria Telecom links provincial capitals, supports metro rings, and reduces last-mile bottlenecks for private ISPs. Migrating copper lines to fiber is lowering churn and enabling upselling to higher speed tiers. However, the state’s control over backhaul preserves price-setting power that discourages neutral data-center growth, keeping domestic transit costs elevated and slowing the digital-services ecosystem.

Upcoming 5G Spectrum Auctions Unlocking Enterprise FWA Potential

ARPCE opened bidding in June 2025 for the 3.5 GHz and 26 GHz bands, structuring licenses to favor rapid service-launch commitments. [2]“Public Mobile Communications Licensing Notice,” Autorité de Régulation de la Poste et des Communications Électroniques, ARPCE.DZPilots by Djezzy and Ooredoo concentrate on campus-style deployments, industrial IoT, and business-park fixed-wireless access. Nevertheless, high spectrum fees and hard-currency shortages complicate radio-access network procurement, so mass-market consumer 5G is unlikely before 2027. Early uptake will hinge on enterprise demand for low-latency connectivity in manufacturing, logistics, and energy corridors.

Rapid Digitization of Public Services and Mobile-Payment Ecosystems

E-government portals, electronic utility payments, and payroll digitalization are lifting transaction volumes on mobile wallets. Algeria Telecom’s incentive that credits up to 30 days of free data for electronic payment of internet top-ups exemplifies how telcos align with policy targets to expand cashless adoption. Partnerships with fintechs and banks create bundled propositions combining connectivity, payments, and identity services, anchoring telecom networks as the backbone for national digitalization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High state control & regulatory uncertainty for private investors | -0.8% | National, especially capital-intensive segments | Long term (≥ 4 years) |

| Currency-convertibility limits inflating network-equipment CAPEX | -0.4% | National, network procurement | Medium term (2-4 years) |

| Diesel-based power-supply volatility impacting rural towers | -0.2% | Rural and remote regions | Short term (≤ 2 years) |

| Scarcity of neutral data centers inflating domestic backhaul costs | -0.2% | Urban enterprise districts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High State Control and Regulatory Uncertainty for Private Investors

Dominant ownership of backbone assets by Mobilis and Algeria Telecom, coupled with opaque licensing timelines, fuels investor caution. The 2022 nationalization of Djezzy crystallized perceptions that foreign equity can be diluted, prompting cost-of-capital premiums and reducing appetite for greenfield ventures. Delays in right-of-way approvals and fluctuating tax holiday terms further complicate business planning, resulting in slower rollouts and fewer innovative service launches. [3]Ben Roberts, “Algeria Telecom Market Attractiveness,” Capacity Media, CAPACITYMEDIA.COM

Currency-Convertibility Limits Inflating Network-Equipment CAPEX

Algeria’s managed-exchange regime requires central-bank approvals for hard-currency purchases, stretching procurement cycles for 4G and 5G radios. Suppliers demand euro- or U.S.-dollar terms, and conversion windows introduce timing risk that pushes overall CAPEX higher. The effect cascades across the supply chain, slowing nationwide coverage upgrades and prolonging dependence on diesel generators in rural sites. Postponed investments exacerbate congestion in high-traffic cells and widen the digital divide.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data and Internet Dominate Revenue Mix

Data and internet services generated 53.86% of total revenue in 2025, signaling their role as the primary value engine of the Algeria telecom MNO market. In monetary terms the segment captured an estimated USD 1.44 billion, reinforcing its status as the anchor for future growth. IoT and M2M contributes a small but expanding slice, supported by industrial telemetry in hydrocarbon fields and early smart-city proofs of concept. Voice and messaging revenues are declining because over-the-top applications cannibalize traditional usage. The Algeria telecom MNO market size for data services is poised to climb further as 5G fixed-wireless access emerges in enterprise parks and as fiber along the coast distributes IP traffic more efficiently. Price competition, however, may compress margins, compelling operators to bundle cloud storage, cybersecurity, and content streaming to lift average spend per account.

Historical momentum between 2019 and 2024 was anchored in 4G adoption, but saturation in the three largest metros moderates the forward curve. Operators therefore pursue adjacent revenue streams such as wholesale fiber leasing and edge-cloud hosting—services that tap existing backbone assets. Regulatory emphasis on spectrum efficiency forces continued investments in carrier-aggregation, small cells, and IP transport resilience. The Algeria telecom MNO market share associated with data services will likely exceed 60.00% by 2031, yet profitability will hinge on disciplined cost management and diversified service portfolios.

By End User: Consumer Segment Remains Core, Enterprise Gaining Momentum

Consumers delivered 85.02% of revenue in 2025, buoyed by prepaid data bundles and promo-led churn cycles. Blended consumer ARPU hovers in the low single-digit USD range, so volume, not pricing, sustains topline performance. The enterprise slice is smaller but expands at a 2.46% CAGR as SMEs, ministries, and oil-and-gas majors migrate to VPN, SD-WAN, and managed IoT solutions. The Algeria telecom MNO market size for enterprise connectivity is projected to add USD 73 million by 2031 as industrial sectors adopt private-LTE networks and as e-government demands resilient, secure links.

Operators differentiate through service-level agreements, local cloud hosting, and security certifications aligned with national data-sovereignty rules. Bundled fixed-mobile convergence is attractive to public-sector agencies, streamlining procurement under single invoices. The Algeria telecom MNO industry uses these enterprise contracts to stabilize cash flows and mitigate prepaid volatility, but execution requires continuous field support and integration skills that are still maturing within local workforces.

Geography Analysis

Regional dynamics reveal a north-south divide, with Algiers, Oran, and Constantine accounting for most fiber subscriptions and nearly two-thirds of LTE data traffic. These urban clusters enjoy dense cell-site grids and multiple fiber rings that underpin low latency and consistent throughput. Rural wilayas rely on macro sites powered by diesel, and weather-driven outages remain common. Satellite broadband supplements coverage, especially after the 2024 renewal of Djezzy’s Ku-band license, adding resilience for remote schools and clinics.

Coastal provinces will benefit first from the Medusa submarine cable, slated to activate in 2026, slashing wholesale transit costs and improving redundancy on Europe-bound routes. Inland trade corridors to Tunisia, Niger, and Mauritania are set to gain cross-border fiber that supports the government’s regional logistics hubs. As these backbones densify, the Algeria telecom MNO market will widen its wholesale addressable segment, opening paths for bandwidth resale, tower colocation, and cross-connection services.

The state’s regional-equity agenda mandates universal-service fund contributions that subsidize LTE rollouts in the high-plateau and Saharan communities. While coverage KPIs are met, throughput still trails urban benchmarks, keeping the digital divide in place. Addressing this gap remains central to long-run market sustainability and to unlocking latent demand for cloud-based education, healthcare, and agritech applications.

Competitive Landscape

The Algeria telecom MNO market is a tight three-player arena in which Mobilis, Djezzy, and Ooredoo collectively hold 100% of subscriptions. Mobilis leverages state affiliation to secure spectrum, backhaul, and universal-service subsidies, resulting in a 43.61% subscriber share. Djezzy holds 30.84%, benefiting from strong urban presence and early 4G leadership, despite constraints on foreign ownership. Ooredoo places third at 25.55%, yet posts a 40% EBITDA margin, indicating disciplined cost controls and efficient spectrum usage.

Price-based competition centers on prepaid data bundles, but differentiation increasingly rests on network quality and fiber footprints. Algeria Telecom’s 400G WDM backbone, deployed with Huawei in July 2025, provides nationwide capacity that supports Mobilis as well as wholesale clients. Djezzy’s eSIM rollout simplifies digital onboarding and aligns with its focus on youth and enterprise clients. Ooredoo’s adoption of an SMS firewall from Infobip curtails gray-route leakage and lifts application-to-person messaging revenue.

Barriers to entry remain prohibitive because license fees, spectrum costs, and a preference for state ownership deter new radio-access networks. Potential disruptors are expected to arise instead from fintech alliances, content platforms, and neutral-host tower companies that monetize infrastructure without full MNO status. The Algeria telecom MNO market therefore balances between consolidation-driven efficiencies and the innovation upside of opening select niches to specialized service providers.

Algeria Telecom MNO Industry Leaders

Mobilis

Djezzy Algeria

Ooredoo Algeria

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Algeria Telecom completed a 400G WDM national backbone in partnership with Huawei, bolstering nationwide capacity and supporting higher-speed broadband services.

- June 2025: ARPCE initiated 5G spectrum licensing, inviting bids for public mobile communications networks.

- March 2025: Ooredoo Algeria expanded its fiber network by 1,400 km and activated 740 new sites.

- January 2025: Djezzy renewed its satellite telecom license, sustaining rural connectivity services.

Algeria Telecom MNO Market Report Scope

Telecom or telecommunication is the long-range transmission of information by electromagnetic means.The Algeria Telecom MNO Market includes in-depth trend analysis based on connectivity like Fixed Networks, Mobile Networks, and Telecom Towers. The telecom services are divided into Voice Services (Wired and Wireless), Data and Messaging Services, and OTT and PayTV Services. Several factors, including an increasing demand for 5G, are likely to drive the adoption of telecom services.

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-User | Enterprises |

| Consumer |

Key Questions Answered in the Report

How large is the Algeria telecom MNO market in 2026?

The sector is valued at USD 2.73 billion in 2026 and is projected to grow to USD 2.97 billion by 2031.

Which service type drives the most revenue?

Data and internet services generate 53.86% of revenue, reflecting Algeria’s shift to broadband usage.

Who is the leading mobile operator?

Mobilis leads with a 43.61% subscriber share, leveraging extensive rural coverage and state backing.

What is the fastest-growing segment?

IoT and M2M services post the highest CAGR at 1.86%, fueled by oil-and-gas telemetry and emerging smart-city pilots.

When will 5G be commercially launched?

Spectrum licensing began in June 2025, with enterprise-focused fixed-wireless deployments expected to appear by 2027.

How does the Medusa cable impact the market?

Once operational in 2026, the cable will cut international transit costs and improve latency on Europe-bound routes, benefiting wholesale bandwidth services.

Page last updated on: