Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 10.87 Billion |

| Market Size (2026) | USD 11.21 Billion |

| Market Size (2031) | USD 13.07 Billion |

| Growth Rate (2026 - 2031) | 3.12% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Telecom MNO Market Analysis by Mordor Intelligence

The South Africa Telecom MNO Market size in 2026 is estimated at USD 11.21 billion, growing from 2025 value of USD 10.87 billion with 2031 projections showing USD 13.07 billion, growing at 3.12% CAGR over 2026-2031.

Muted growth reflects a mature voice business, recurring load-shedding costs and tight pricing oversight, even as data-centric revenues, 5G launches and fintech services deepen digital engagement. Device subsidies, spectrum refarming and open-access infrastructure keep subscriber additions positive, while cloud-linked enterprise connectivity lifts average revenue per user. Regulatory support for a 2G/3G switch-off by December 2027, together with open-access tower and fiber models, helps operators pivot capex toward 4G and 5G densification. Persistent power instability, high data prices and occasional subsea-cable faults remain the most visible growth brakes.

Key Report Takeaways

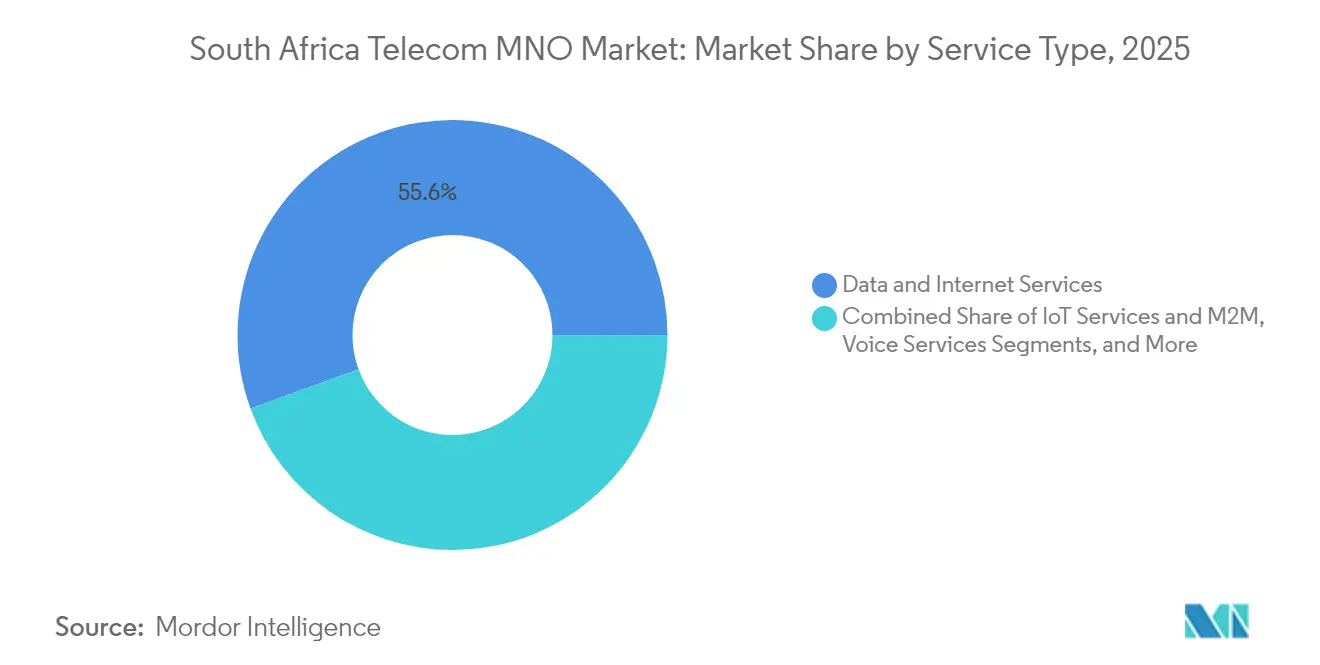

- By service type, Data and Internet Services led with 55.56% of South Africa telecom MNO market share in 2025, while IoT and M2M is advancing at a 3.22% CAGR through 2031.

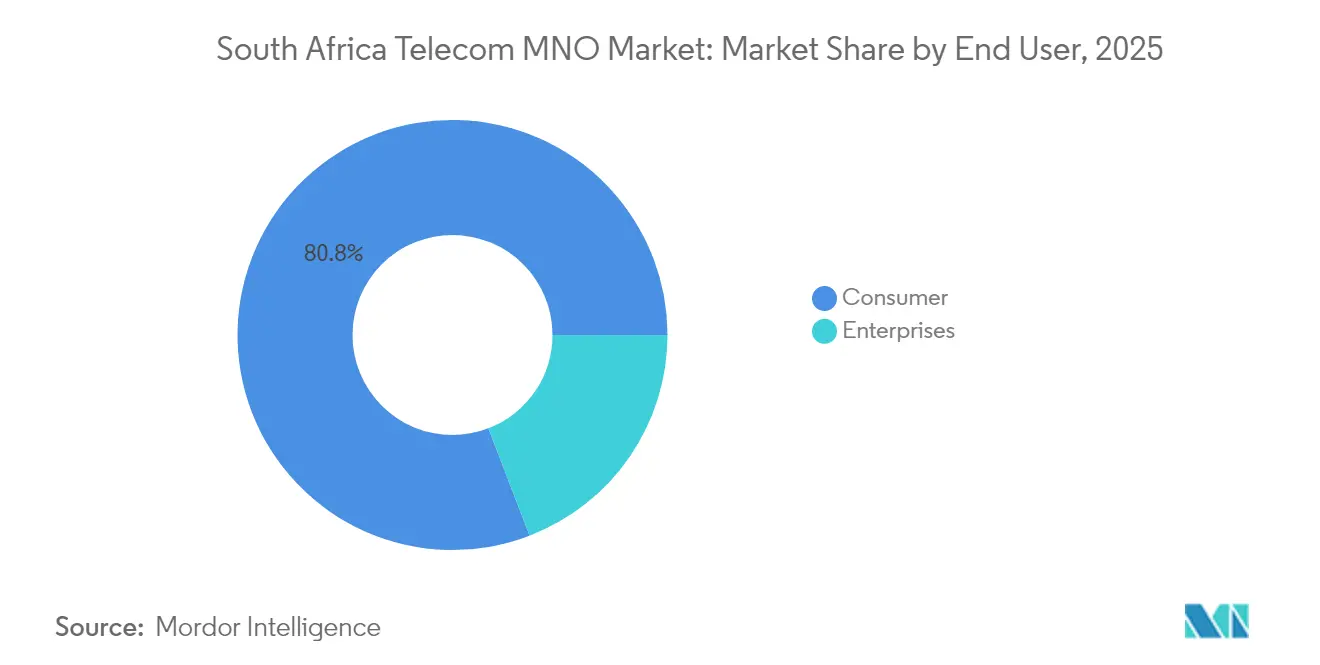

- By end-user, Consumer subscriptions accounted for 80.84% of the South Africa telecom MNO market size in 2025, while Enterprise services are forecast to record the fastest 3.67% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smartphone adoption | +0.8% | Urban Gauteng and Western Cape | Medium term (2-4 years) |

| Fibre-to-the-home expansion | +0.6% | Metros nationwide | Long term (≥4 years) |

| 5G spectrum auctions | +0.5% | Major cities nationwide | Medium term (2-4 years) |

| Enterprise cloud and IoT demand | +0.7% | Business districts nationwide | Long term (≥4 years) |

| Open-access fibre and neutral-host towers | +0.4% | Underserved rural areas | Long term (≥4 years) |

| Fintech–telco convergence | +0.5% | Urban centers nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Soaring Smartphone Adoption Drives Mobile Data Traffic

Rapid smartphone uptake multiplies data consumption, shifting revenues toward higher-margin bundles. MTN’s plan to seed 1.2 million low-cost 4G handsets in 2025 directly tackles affordability hurdles and accelerates migration off legacy networks.[1]Mobile World Live, “MTN to ship 1.2 million smartphones,” mobileworldlive.com The strategy aligns with the December 2027 2G/3G sunset, compelling operators to manage capacity upgrades while subsidizing devices. Network traffic across MTN South Africa climbed 35.7% to 9,054 PB in H1 2024, validating the revenue upside as adoption scales. [2]MTN Group, “FY 2024 Results,” group.mtn.com

Enterprise Cloud and IoT Connectivity Demand Surges

Hyperscalers’ local zones—from AWS Cape Town to Google Cloud Johannesburg—anchor South African firms’ digital-first roadmaps. [3]TechCrunch, “AWS and Google deepen African cloud play,” techcrunch.comVodacom Business earned AWS Direct Connect status, giving enterprises low-latency, secure links to cloud workloads. Large banks such as Standard Bank accelerated workload migration in 2024, driving demand for managed VPNs, SD-WAN and NB-IoT connections. Expanded IoT deployments—spanning agriculture sensors to municipal smart meters—support the segment’s 3.38% CAGR outlook.

5G Spectrum Auctions Unlock Premium-ARPU Services

The 2022 multiband auction assigned spectrum to six players, catalyzing differentiated 5G rollouts. Rain lit Africa’s first standalone 5G network, carving a data-only niche despite early execution headwinds. MTN’s ultra-range maritime 5G test off Mossel Bay illustrates the technology’s ability to tap previously unreachable revenue pools. Population coverage exceeded 50% by end-2024, supporting 10.8 million 5G users and R28.4 billion in service revenue.

Fintech–Telco Convergence Creates Sticky Revenue Streams

Integrating payments and lending into the mobile wallet cements loyalty and lifts ARPU. Mastercard’s USD 200 million minority stake valued MTN’s fintech arm at USD 5.2 billion, highlighting investor appetite for scaled digital-finance platforms. Vodacom processes R23 billion in daily mobile-money flows, showing the transaction volume achievable when telecom networks leverage financial inclusion. MTN’s fintech revenue jumped 59.1% year-on-year in H1 2024, demonstrating scalability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High data prices and affordability gap | -0.9% | Rural and low-income areas nationwide | Short term (≤2 years) |

| Market concentration and price regulation | -0.4% | National | Medium term (2-4 years) |

| Load-shedding raises opex and outages | -0.7% | National | Short term (≤2 years) |

| Subsea-cable outages risk bandwidth | -0.3% | National | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Data Prices and Affordability Gap Limit Usage

At USD 2.67 per GB, South Africa ranks 136th worldwide for mobile-data affordability, limiting uptake of premium plans. Inflation, load-shedding fuel costs and a weak rand pressure operator margins, prompting cautious discounting strategies. Regulator ICASA relaxed data-expiry rules in 2024, implicitly acknowledging the tight economics confronting networks. Affordability constraints hit rural and prepaid users hardest, slowing full market digital inclusion.

Load-Shedding Disrupts Network Availability and Opex

Rolling blackouts divert capital into generators and batteries instead of coverage expansion. MTN spent USD 100 million on backup power in 2025 alone, underscoring how energy scarcity reshapes balance-sheets. Vodacom’s R60 billion five-year plan allocates sizeable power-resilience budgets, while tower operators pivot to power-as-a-service models. Outages dent network-quality scores and heighten churn risk, keeping operating costs structurally high.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Anchor Revenue Transformation

Data and Internet Services held a 55.56% South Africa telecom MNO market share in 2025 and contributed 48.3% of MTN’s service revenue in Q1 2025. Voice and SMS volumes continue secular decline as over-the-top apps offload legacy traffic, yet dual-SIM penetration preserves a baseline of paid minutes. IoT and M2M, though only 1.96% of 2025 revenues, is the fastest-growing slice and underpins a projected 3.22% CAGR to 2031, aided by Vodacom’s nationwide NB-IoT network.

The South Africa telecom MNO market size attached to IoT and M2M is set to expand alongside provincial smart-city budgets and private-sector fleet-tracking contracts. OTT video drives Pay-TV partnerships such as Telkom-Netflix, while bundled value-added services—from cybersecurity to cloud backup—defend margins against pure-play data commoditization. Operators’ ability to package fintech wallets with data bundles adds retention levers absent from traditional service menus.

By End-User: Enterprise Demand Gains Momentum

Consumers still generated 80.84% of South Africa telecom MNO market revenue in 2025, yet enterprise lines are forecast to grow at a 3.67% CAGR on surging cloud and SD-WAN demand. Consumer ARPU pressures persist as aggressive bundle promotions offset high data-cost perceptions, but fintech services add incremental yield per user.

Enterprise connectivity contracts often bundle dedicated internet access, MPLS replacements and managed security, lifting contract sizes well above mass-market rates. The South Africa telecom MNO market size relevant to corporates will benefit from public-sector digitalization and multinationals’ cloud landing zones. Operators cultivating vertical-specific solutions—agri-IoT, retail analytics, industrial private-LTE—are positioned to defend margins amid slowing consumer growth.

Geography Analysis

Nationwide, 5G population coverage surpassed 50% by end-2024, with the Western Cape and Gauteng provinces capturing the bulk of early deployments. The South Africa telecom MNO market faces a rural connectivity shortfall as open-access fiber and neutral-host towers only gradually close coverage gaps. Nine subsea cables, including the new Equiano system, give the country bandwidth depth; nonetheless, a July 2025 WACS outage throttled international traffic, exposing reliance on coastal landing points.

Load-shedding impacts differ by province: Eastern Cape sites suffer longer outages due to sparse grid maintenance, whereas Gauteng operators deploy larger on-site batteries. Fibre-to-the-home adoption spikes in Cape Town, Johannesburg and Durban suburbs, stimulating fixed-mobile substitution and driving 5G fixed-wireless propositions. Government’s Digital Economy Master Plan targets a 15-20% GDP digital contribution by 2025, anchoring policy measures such as accelerated spectrum refarming and SA Connect rural-broadband tenders.

Competitive Landscape

MTN and Vodacom control a combined 70% South Africa telecom MNO market share, shaping a duopolistic tone that nevertheless faces regulatory pushback. The Competition Tribunal’s rejection of Vodacom’s Maziv purchase in November 2024 flagged concerns about vertical integration choking wholesale fiber access. MTN poured R10 billion into network modernization in 2024, achieving the country’s highest 82.48 Mbps average download speed. Vodacom leverages Vodafone’s scale for cloud alliances, while Rain’s standalone-5G bet aims at data-heavy cord-cutters.

Cell C’s migration to a virtual-operator model on MTN’s radio network slashes capex, yet brand positioning and service quality remain watch-points. Telkom monetized its Swiftnet tower unit for USD 371.5 million in March 2025, freeing cash for fiber expansion and mobile-ARPU uplift. Towercos such as American Tower and SBA Communications deploy power-as-a-service offers, turning energy crisis into an annuity opportunity. Fintech partnerships—MTN-Mastercard, Vodacom-Alipay—signal that future differentiation may rest more on platform ecosystems than on raw spectrum holdings.

South Africa Telecom MNO Industry Leaders

MTN Group Limited

Vodacom South Africa

Telkom SA SOC Limited

Cell C Limited

Rain (Pty) Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Vodacom Group posted USD 2.2 billion Q1 2025 revenue, buoyed by South Africa and Egypt operations.

- June 2025: A WACS cable fault slowed nationwide internet, highlighting the need for greater subsea redundancy.

- May 2025: MTN launched a 4G-device subsidy program targeting 1.2 million budget smartphones ahead of the 2G/3G sunset.

- March 2025: Actis completed Telkom Swiftnet tower acquisition for USD 371.5 million, emphasizing infrastructure monetization.

South Africa Telecom MNO Market Report Scope

Telecom or Telecommunication is the long-range transmission of information by electromagnetic means. Several factors, including an increasing demand for 5G, likely drive the adoption of telecom services in South Africa.

The South Africa telecom MNO market is segmented by services (voice services [wired and wireless], data and messaging services, and OTT and PayTV services) and telecom connectivity (fixed network [fixed broadband internet services, fixed voice services], mobile network). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Service Type

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

End-User

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-User | Enterprises |

| Consumer |

Key Questions Answered in the Report

How large is the South Africa telecom MNO market in 2026?

The South Africa telecom MNO market size stands at USD 11.21 billion in 2026 and is set to reach USD 13.07 billion by 2031.

What CAGR is forecast for mobile network operators through 2031?

Market revenue is projected to grow at a 3.12% CAGR between 2026 and 2031.

Which service type contributes the most revenue?

Data and Internet Services account for 55.56% of 2025 revenue and remain the dominant growth engine.

Why is IoT considered a high-growth segment?

Enterprise digitization and nationwide NB-IoT coverage underpin a 3.22% CAGR for IoT and M2M services through 2031.

How does load-shedding impact telecom operators?

Grid instability forces operators to invest heavily in generators and batteries, raising opex and diverting funds from network expansion.

Who are the leading players by market share?

MTN and Vodacom jointly command more than 70% of mobile service revenue, giving the market a high concentration score.

Page last updated on: