Trusted Platform Module (TPM) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

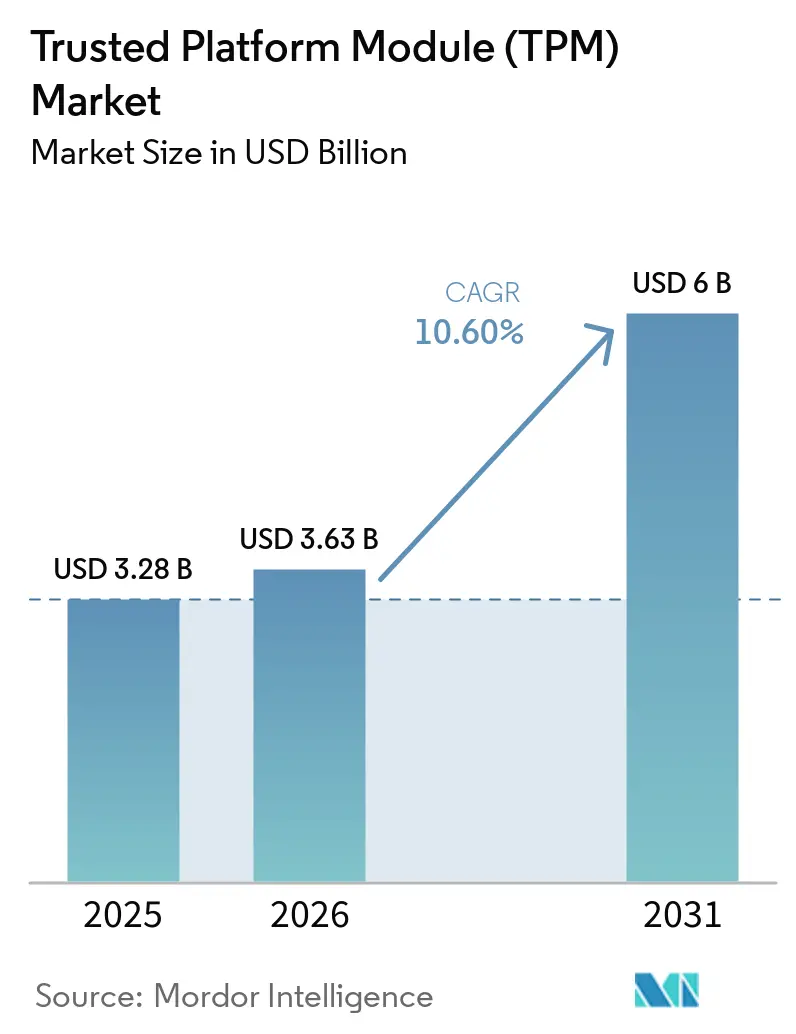

| Market Size (2026) | USD 3.63 Billion |

| Market Size (2031) | USD 6 Billion |

| Growth Rate (2026 - 2031) | 10.60% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Trusted Platform Module (TPM) Market Analysis by Mordor Intelligence

The Trusted Platform Module (TPM) market size was valued at USD 3.28 billion in 2025 and estimated to grow from USD 3.63 billion in 2026 to reach USD 6.00 billion by 2031, at a CAGR of 10.60% during the forecast period (2026-2031). Hardware-based trust has become part of the baseline security stack as operating system vendors, insurers, and regulators increasingly expect verifiable device identity at the hardware level. The Windows 10 end-of-life milestone in October 2025 made the Windows 11 TPM 2.0 requirement a direct hardware-refresh trigger across enterprise fleets and commercial devices. Confidential computing and zero-trust security models are also pushing trust verification closer to silicon, broadening demand beyond client PCs to servers, edge AI gateways, and automotive electronic control units. The post-quantum transition is creating an additional refresh path for both discrete and firmware-led security architectures as vendors prepare for new cryptographic requirements. At the same time, the market is being reshaped by processor-embedded security, which lowers bill-of-material costs in some deployments while reinforcing the position of large platform vendors.

Key Report Takeaways

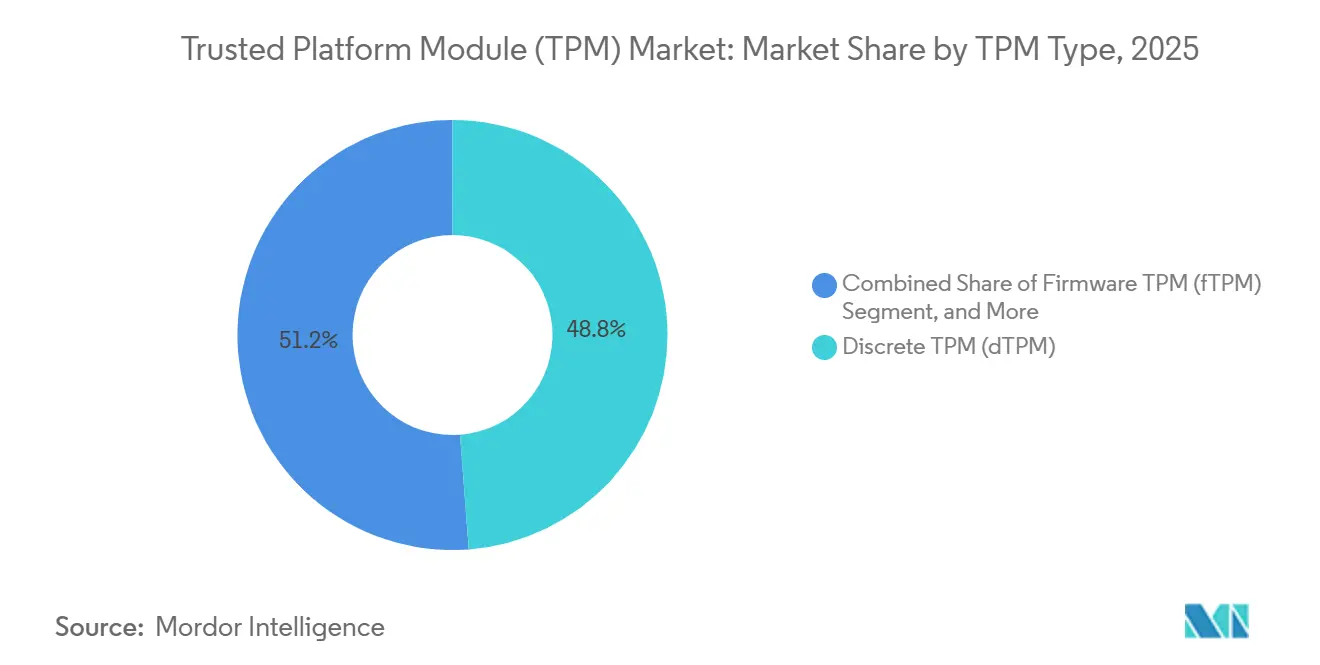

- By TPM type, discrete TPM led with 48.8% share in 2025 in the trusted platform module (TPM) market, while virtual TPM is forecast to expand at a 12.8% CAGR through 2031.

- By host interface, SPI/eSPI held a 46.7% share in 2025, while PCIe/USB is projected to record the highest CAGR of 13.7% through 2031.

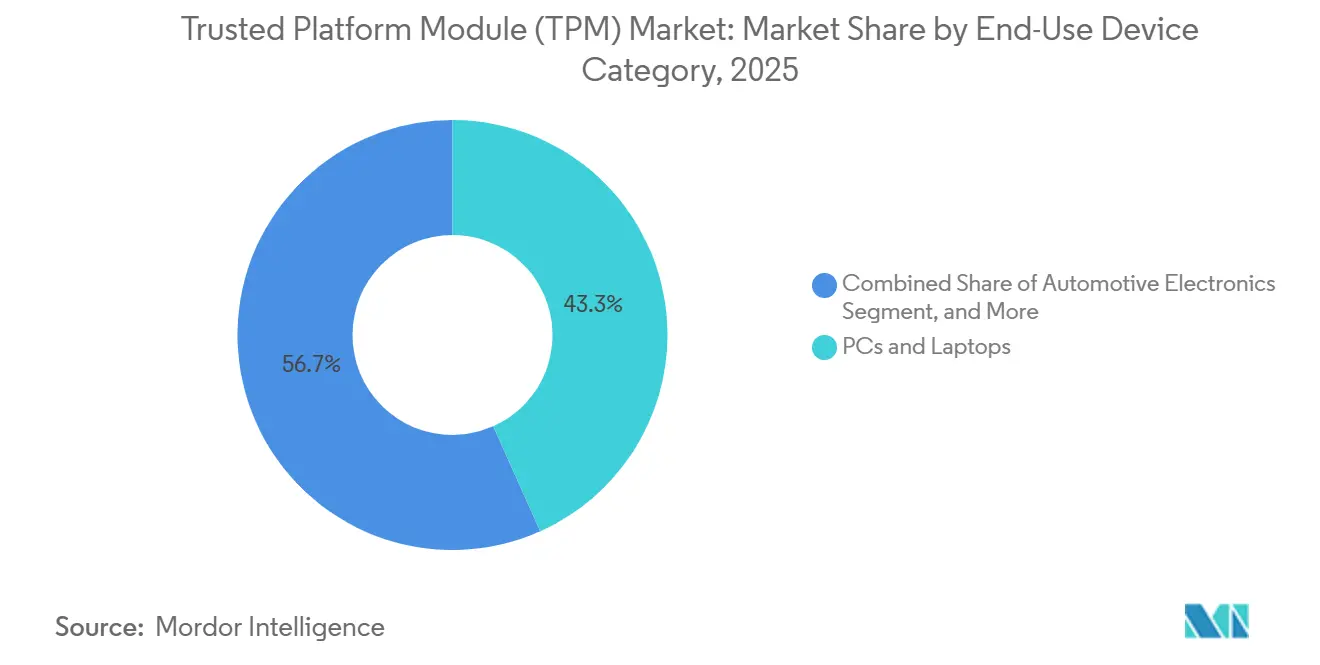

- By end-use device category, PCs and laptops accounted for 43.3% of the market in 2025, while automotive electronics is expected to grow at a 13.03% CAGR through 2031.

- By industry vertical, IT and Telecom held 30.4% share in 2025, while Healthcare and Life Sciences are projected to expand at a 12.5% CAGR through 2031.

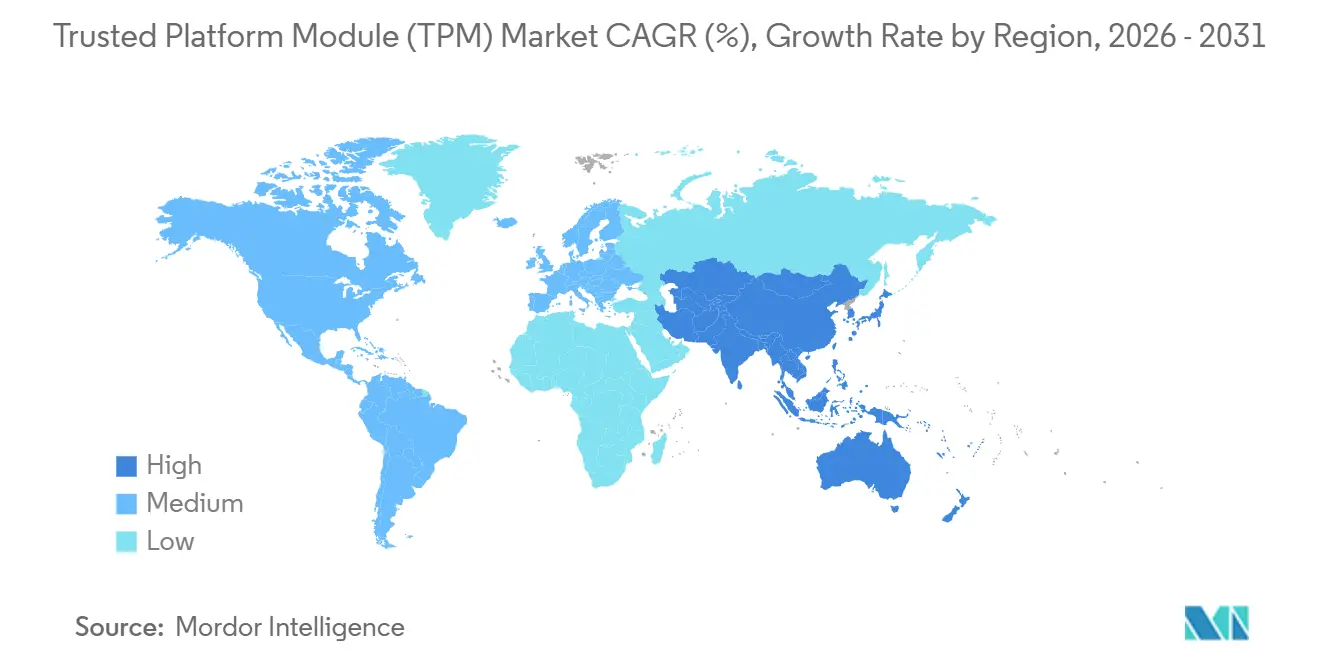

- By geography, North America retained 38.2% share in 2025 in the TPM market, while Asia-Pacific is forecast to grow at a 12.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Trusted Platform Module (TPM) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Hardware-Based Root of Trust in PCs and Servers | +2.5% | Global, with concentrated impact in North America and Europe | Short term (≤ 2 years) |

| Mandatory TPM 2.0 Requirement for Windows 11 Upgrade Cycle | +2.0% | Global, particularly strong in North America, Europe, and Asia-Pacific | Short term (≤ 2 years) |

| Rising Cyber-Insurance Premiums Driving Demand for Certified Secure Elements | +1.3% | North America and Europe | Medium term (2-4 years) |

| Automotive UNECE R155/R156 Compliance Accelerating Secure ECU Rollouts | +1.1% | Europe, Japan, South Korea, Australia, and China | Medium term (2-4 years) |

| Edge AI Inference Platforms Requiring Hardware Security for Model IP Protection | +0.7% | Global, with Asia-Pacific spillover to North America and Europe | Medium term (2-4 years) |

| Quantum-Resistant Firmware Initiatives Boosting Next-Gen TPM Refresh | +0.5% | Global, with the earliest adoption in defense and critical infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Hardware-Based Root of Trust in PCs and Servers

Demand in the Trusted Platform Module (TPM) market has strengthened as the hardware root of trust has shifted from an optional upgrade to a required security layer. Microsoft places TPM 2.0 at the center of Windows 11's protections, including BitLocker, Windows Hello for Business, and virtualization-based security.[1]Microsoft, “Windows 11 Security Book - Hardware Root-of-Trust,” Microsoft Learn, learn.microsoft.comThat same trust anchor now extends to newer client platforms that integrate Microsoft Pluton into modern processor families, moving hardware-backed identity deeper into standard device architecture. Network infrastructure is also adopting this pattern, as IETF RFC 9683 formalized remote integrity verification workflows for routers, switches, and firewalls that contain TPMs.[2]Guy C. Fedorkow, Eric Voit, and Jessica Fitzgerald-McKay, “Remote Integrity Verification of Network Devices Containing Trusted Platform Modules,” Internet Engineering Task Force, datatracker.ietf.orgThis expands the market's serviceable base beyond traditional PCs into servers, networking equipment, and cloud infrastructure.

Mandatory TPM 2.0 Requirement for Windows 11 Upgrade Cycle

The Windows 10 support deadline turned the TPM market into a direct beneficiary of operating system migration. Microsoft continues to treat TPM 2.0 as a non-negotiable security requirement in Windows 11. That baseline forces enterprises to assess their installed fleets earlier than planned, because devices that cannot meet the requirement become harder to keep in place over long service cycles. The same expectation reinforces a broader endpoint security stack that links TPM 2.0 with secure boot, UEFI, device identity, and measured startup processes. The result is that a software transition now behaves like a hardware procurement event across the market.

Rising Cyber-Insurance Premiums Driving Demand for Certified Secure Elements

Cyber underwriting is making device integrity a purchasing issue in the Trusted Platform Module (TPM) market. Hardware-backed encryption and attestation provide a clearer way for enterprises to demonstrate protected key storage and measured device state when they negotiate coverage terms and internal control standards. This changes TPM from a technical preference into a procurement requirement for laptops, servers, and connected operational assets in security-sensitive environments. The Trusted Computing Group has also linked hardware-based cyber resilience, remote update control, and anti-theft capabilities with lower exposure to field failures and recovery costs across automotive and industrial deployments.[3]Trusted Computing Group, “Ensuring Cyber Resilience from the Hardware Up,” Trusted Computing Group, trustedcomputinggroup.orgThat widens the addressable market beyond its historic reliance on enterprise PCs.

Automotive UNECE R155/R156 Compliance Accelerating Secure ECU Rollouts

Automotive compliance is becoming a structural growth engine for the Trusted Platform Module (TPM) market. UNECE R155 and R156 have raised the bar for cybersecurity management and software update integrity across vehicle electronic control units. That shift makes hardware roots of trust more valuable for credential storage, firmware protection, and secure over-the-air validation in software-defined vehicles. Infineon's March 2026 TEGRION SLI22 launch showed that suppliers are now pairing automotive-grade security controllers with post-quantum readiness and deep vehicle platform certification for platforms that must operate over long product lifecycles. The compliance burden also extends to the supplier network, making certified secure silicon harder for Tier 1 vendors to treat as optional.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Chain Volatility for 45 nm and Older Trusted Foundry Nodes | -1.2% | Global, most acute in North America and Europe where trusted foundry mandates limit sourcing options | Short term (≤ 2 years) |

| Cost-Sensitive IoT Nodes Opting for Lightweight Crypto Alternatives | -0.9% | Asia-Pacific core, with spillover to emerging IoT markets in the Middle East and Africa | Medium term (2-4 years) |

| Fragmented Attestation Standards Across Cloud, Edge, and Automotive Domains | -0.7% | Global | Medium term (2-4 years) |

| Emerging Zero-Trust Architectures Reducing Reliance on Local TPMs | -0.5% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Volatility for 45 Nm and Older Trusted Foundry Nodes

Supply tightness at mature nodes remains a direct brake on the TPM market. Discrete TPM designs depend on 40-90nm processes where tamper resistance, shielding, and side-channel protection matter more than density gains. Product families in this category are often designed for long life and harsh operating conditions, which limits how quickly vendors can move to new manufacturing paths without affecting qualification and lifecycle commitments. Security certification and platform-level validation also slow down sourcing changes, which favors incumbents with deep manufacturing and compliance experience. As a result, supply disruptions at qualified nodes can limit near-term market expansion even when demand remains firm.

Cost-Sensitive IoT Nodes Opting for Lightweight Crypto Alternatives

Cost pressure in small devices keeps part of the Trusted Platform Module (TPM) market from reaching the broad IoT base. NIST's lightweight cryptography standard provides constrained devices with a credible way to implement authenticated encryption and hashing without the full overhead of a TPM stack. DICE-based designs also provide hardware-rooted identity and layered attestation with very low boot overhead in embedded systems. These approaches are well-suited to consumer IoT products and industrial sensor nodes where board space, power draw, and unit economics are tightly controlled. Unless firmware and integrated security options narrow the economics gap, discrete adoption in this part of the market will remain capped.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By TPM Type: Virtual Deployments Challenge Discrete Silicon Dominance

Discrete TPM held 48.8% of the trusted platform module (TPM) market share in 2025, which shows that enterprise and government buyers still place a premium on physical separation for key storage and trust validation. Its position remains strongest in systems where tamper-resistant packaging, independent power domains, and certification depth directly shape procurement decisions. Integrated TPM and firmware TPM solutions continue to gain presence in PCs and mobile platforms because they add security functions without requiring a separate component. This is pushing discrete suppliers to compete less on basic availability and more on certification history, supply-chain provenance, and long-term lifecycle support.

Virtual TPM is projected to grow at a 12.8% CAGR from 2026 to 2031, making it the fastest-growing format in the TPM market. The industry is also seeing vTPM and fTPM gain traction in cloud environments and edge AI systems, where software-managed trust can scale faster than new discrete hardware. Research on ARM-based embedded architectures already points to post-quantum attestation paths that can be implemented within firmware-led trust models. wolfSSL's May 2026 firmware TPM release with ML-DSA and ML-KEM support shows how vendors are responding to that need before native PQC silicon becomes widely available.

By Host-Interface: PCIe/USB Growth Signals Platform Architecture Shift

SPI/eSPI retained 46.7% of the market in 2025, reflecting its broad installed base across commercial PCs and embedded industrial systems. That footprint keeps the interface relevant even as newer platform designs favor higher-throughput connections. LPC still supports a meaningful legacy base, but its role is narrowing as server and data-center architectures move away from older bus designs. In the Trusted Platform Module (TPM) market, host-interface selection now affects supplier choice, qualification work, and upgrade timing as much as raw security capability.

PCIe/USB is forecast to grow at a 13.7% CAGR from 2026 to 2031, indicating a broader platform shift in modern server and infrastructure designs. This change matters because interface migration often requires system-level requalification and opens procurement windows for vendors aligned with the new architecture. I2C and I3C are also gaining share in automotive and IoT use cases where lower pin counts matter, and I3C offers higher throughput for next-generation control and attestation workloads. STMicroelectronics addresses these needs through its ST33KTPM family with SPI or I2C options, FIPS 140-3 and Common Criteria EAL4+ certification, and industrial variants rated from -40°C to 105°C with a 20-year product lifetime.

By End-Use Device Category: Automotive Electronics Lead The Next Growth Wave

PCs and laptops accounted for 43.3% of the trusted platform module (TPM) market in 2025, keeping endpoint computing at the center of revenue generation. That position still reflects the direct link between commercial PC refresh cycles and TPM socket demand. Servers and data-center platforms form the next major layer because confidential computing and secured-core requirements are moving hardware attestation deeper into infrastructure. IoT and embedded systems remain important to overall deployment volumes, but low per-device budgets continue to limit discrete penetration.

Automotive electronics are projected to expand at a 13.03% CAGR from 2026 to 2031, making it the fastest-growing end-use category in the market. Software-defined vehicle platforms are increasing the need for authenticated over-the-air updates, protected credentials, and trusted execution across large numbers of ECUs. Infineon's OPTIGA TPM portfolio and its 2025 demonstration with Fraunhofer SIT demonstrated how TPM 2.0 can protect user data, OEM data, and the integrity of remote firmware updates in automotive environments. Industrial control and automation systems are also gaining relevance as operators align hardware trust anchors with critical infrastructure protection programs.

By Industry Vertical: Healthcare Growth Accelerates Amid Security Mandates

IT and Telecom accounted for 30.4% of the market in 2025, supported by broader adoption of attestation across network equipment and hyperscale infrastructure. Remote integrity verification standards are expanding the role of TPMs in routers, switches, and firewalls rather than limiting them to client endpoints. BFSI remains a major adopter because secure identity, payment infrastructure, and regulated workloads all benefit from hardware-backed trust. ENISA's wallet security work also points to durable demand for secure cryptographic devices in digital identity ecosystems, which supports continued adoption across financial and public-service environments.

Healthcare and Life Sciences is expected to grow at a 12.5% CAGR from 2026 to 2031, making it the fastest-growing vertical in the Trusted Platform Module (TPM) market. Hospitals, connected medical devices, and supporting vendors face a greater need to demonstrate device identity and software integrity as ransomware pressure and product security expectations rise. The EU Cyber Resilience Act reinforces that shift by classifying secure cryptoprocessors as critical products subject to conformity assessment and stronger cybersecurity obligations. Retail and commerce should continue to drive demand through point-of-sale upgrades and payment security requirements, though growth there remains slower than in healthcare.

Geography Analysis

North America held 38.2% of the trusted platform module (TPM) market share in 2025, which made it the largest regional contributor. The United States remains the anchor because federal procurement expectations, cloud assurance needs, and enterprise security baselines keep certified silicon in steady demand. A dense concentration of hyperscale data centers also supports stronger server-side deployment across the Trusted Platform Module (TPM) market. Canada adds a smaller but meaningful layer through digital government programs and financial-sector security requirements. North America's preference for trusted sourcing helps preserve pricing power for qualified discrete TPM suppliers.

Asia-Pacific is projected to grow at a 12.4% CAGR from 2026 to 2031, making it the fastest-growing regional segment of the trusted platform module (TPM) market. Japan, South Korea, China, and India are all contributing to this acceleration through stronger automotive, semiconductor, and connected-device activity. China's GB 44495 rollout is widening the compliance pull for secure vehicle electronics across the region. South Korea shows the depth of this movement, with Rambus security IP integrated into BOS Semiconductors' Eagle-N automotive AI accelerator on Samsung's 5nm process for authenticated startup and protected over-the-air updates. The Trusted Computing Group's Japan Regional Forum also shows that standards engagement in Asia-Pacific is mature enough to support broader deployment across the ecosystem.

Europe is the second-largest regional market, with Germany, the United Kingdom, and France as principal demand centers. Windows 11 migration requirements and the EU Cyber Resilience Act are reinforcing the case for certified hardware roots of trust across enterprise and product-security use cases. South America, the Middle East, and Africa remain earlier-stage regions where adoption is concentrated in government, defense, and telecom projects rather than mass enterprise refresh cycles. These regions are still smaller today, but infrastructure digitization and sovereign cybersecurity investment should support a broader role for the Trusted Platform Module (TPM) market over time.

Competitive Landscape

The Trusted Platform Module (TPM) market remains moderately concentrated in discrete silicon, with Infineon Technologies AG holding structural leadership and STMicroelectronics, Nuvoton Technology, and Microchip Technology forming the main secondary group. That hierarchy is supported by certification experience, long product lifecycles, and the ability to serve enterprise, industrial, and automotive requirements with dependable supply. Infineon's 2025 annual report showed the scale of that advantage, with 1,900 patent filings in 2025 and a total portfolio of 29,700 patents and applications. This level of R&D depth matters because post-quantum readiness and certification renewal are becoming more central to supplier selection. The Trusted Platform Module (TPM) market, therefore, continues to reward incumbents that combine secure design with long validation records.

Infineon's March 2026 launch of the TEGRION SLI22 illustrates how leading vendors are defending share through certification depth and automotive specialization. The controller combined automotive-grade protection with post-quantum security, strengthening Infineon's position in software-defined vehicle programs. wolfSSL followed a different path in May 2026 by releasing a firmware TPM with ML-DSA and ML-KEM support for platforms where discrete PQC-capable silicon is not yet commercially available. That move puts pressure on hardware-only suppliers in segments where customers value upgrade flexibility more than physical isolation. In the Trusted Platform Module (TPM) market, this is creating a clearer divide between high-assurance discrete demand and fast-scaling firmware-led deployments.

Mid-tier and emerging suppliers are also repositioning around manufacturing efficiency and ecosystem access. Nuvoton's March 2026 agreement with Tower Semiconductor to restructure TPSCo shows that footprint optimization is now part of the competitive playbook. SecEdge's onboarding to the NVIDIA Halos AI Systems Inspection Lab in March 2026 also shows how firmware-based trust vendors are targeting robotics, industrial automation, automotive, and medical systems through ecosystem partnerships. These moves keep the Trusted Platform Module (TPM) market competitive enough to avoid high concentration, even though leadership remains concentrated among a relatively small group of established security silicon suppliers.

Trusted Platform Module (TPM) Industry Leaders

Infineon Technologies AG

STMicroelectronics N.V.

Nuvoton Technology Corporation

Microchip Technology Inc.

Samsung Electronics Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: wolfSSL released a standalone wolfTPM firmware TPM (fwTPM) implementation with full post-quantum cryptography support, including ML-DSA-44/65/87 and ML-KEM-512/768/1024 per TCG TPM 2.0 Library Specification v1.85, targeting embedded MCUs, automotive ECUs, Linux platforms, and RTOS environments where discrete TPM silicon with native PQC support is not yet commercially available. The release introduced TPM2_Encapsulate and TPM2_Decapsulate commands for ML-KEM and a full signing and verification sequence for ML-DSA, with PQC key persistence across TPM restarts.

- March 2026: Infineon Technologies AG launched the TEGRION SLI22, a 28nm automotive security controller that received Common Criteria EAL6+ certification from the German Federal Office for Information Security (BSI) and integrates post-quantum cryptography. The controller is the world's first automotive-grade security controller to achieve this certification level, supports hybrid classical and PQC cryptography, and targets eSIM, V2X, and automotive access applications requiring 17-year data retention.

- March 2026: SecEdge's SEC-TPM firmware was onboarded to the NVIDIA Halos AI Systems Inspection Lab, the first ANAB-accredited inspection lab for AI-driven physical systems. The integration provides a silicon-anchored root of trust, measured boot, device identity, and hardware-anchored AI model protection for robotics, industrial automation, automotive, and medical deployments, supporting alignment with IEC 62443 and the EU Cyber Resilience Act.

- March 2026: Nuvoton Technology Corporation, Japan, and Tower Semiconductor announced a framework agreement to restructure TPSCo, under which Tower is expected to assume full ownership and control of TPSCo's 12-inch Uozu fab business, while the 8-inch Tonami fab business will become a wholly owned Nuvoton subsidiary. Nuvoton Japan is to pay Tower USD 25 million at closing, with the transaction expected to close on April 1, 2027, subject to regulatory approvals.

Global Trusted Platform Module (TPM) Market Report Scope

The Trusted Platform Module (TPM) market refers to the global industry focused on the development, manufacturing, integration, and commercialization of hardware- and software-based security modules that provide cryptographic functions, secure key storage, device authentication, platform integrity verification, and trusted computing capabilities across connected digital systems. TPM solutions are deployed to enhance endpoint, network, and infrastructure security by enabling encryption, secure boot, attestation, identity management, and protection against unauthorized access and cyber threats in enterprise, industrial, automotive, and consumer environments.

The Trusted Platform Module (TPM) Market is Segmented by TPM Type (Discrete TPM (dTPM), Integrated TPM (iTPM/Platform Trust Tech), Firmware TPM (fTPM), and Virtual TPM (vTPM/Software)), Host-Interface (SPI/eSPI, I2C/I3C, LPC, and PCIe/USB), End-Use Device (PCs and Laptops, Servers and Data-Center Platforms, IoT and Embedded Systems, Automotive Electronics, Industrial Control and Automation, Mobile and Consumer Devices, and Others End-Use Devices), Industry Vertical (IT and Telecom, BFSI, Healthcare and Life Sciences, Government and Defense, Retail and Commerce, and Other Industry Verticals ), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Discrete TPM (dTPM) |

| Integrated TPM (iTPM/Platform Trust Tech) |

| Firmware TPM (fTPM) |

| Virtual TPM (vTPM/Software) |

| SPI/eSPI |

| I2C/I3C |

| LPC |

| PCIe/USB |

| PCs and Laptops |

| Servers and Data-Center Platforms |

| IoT and Embedded Systems |

| Automotive Electronics |

| Industrial Control and Automation |

| Mobile and Consumer Devices |

| Other End-Use Device Categories |

| IT and Telecom |

| BFSI |

| Healthcare and Life Sciences |

| Government and Defense |

| Retail and Commerce |

| Other Industry Verticals |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By TPM Type | Discrete TPM (dTPM) | |

| Integrated TPM (iTPM/Platform Trust Tech) | ||

| Firmware TPM (fTPM) | ||

| Virtual TPM (vTPM/Software) | ||

| By Host-Interface | SPI/eSPI | |

| I2C/I3C | ||

| LPC | ||

| PCIe/USB | ||

| By End-Use Device Category | PCs and Laptops | |

| Servers and Data-Center Platforms | ||

| IoT and Embedded Systems | ||

| Automotive Electronics | ||

| Industrial Control and Automation | ||

| Mobile and Consumer Devices | ||

| Other End-Use Device Categories | ||

| By Industry Vertical | IT and Telecom | |

| BFSI | ||

| Healthcare and Life Sciences | ||

| Government and Defense | ||

| Retail and Commerce | ||

| Other Industry Verticals | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the Trusted Platform Module (TPM) market?

The Trusted Platform Module (TPM) market is valued at USD 3.63 billion in 2026 and is projected to reach USD 6.00 billion by 2031 at a CAGR of 10.60%.

Which TPM format is growing the fastest?

Virtual TPM is the fastest-growing TPM type, with a projected CAGR of 12.8% from 2026 to 2031, supported by cloud, virtualization, and edge AI deployments.

Why is Windows 11 important for TPM demand?

Windows 11 keeps TPM 2.0 as a core security requirement, which turns operating system migration into a hardware review and refresh cycle for many enterprises.

Which end-use segment is driving the next growth phase?

Automotive electronics is the fastest-growing end-use segment, expanding at a 12.3% CAGR through 2031 as secure ECUs and authenticated software updates become more important.

Which region leads global adoption?

North America led with 38.2% share in 2025, while Asia-Pacific is the fastest-growing region with a forecast CAGR of 12.4% through 2031.

Page last updated on: