Over The Top (OTT) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

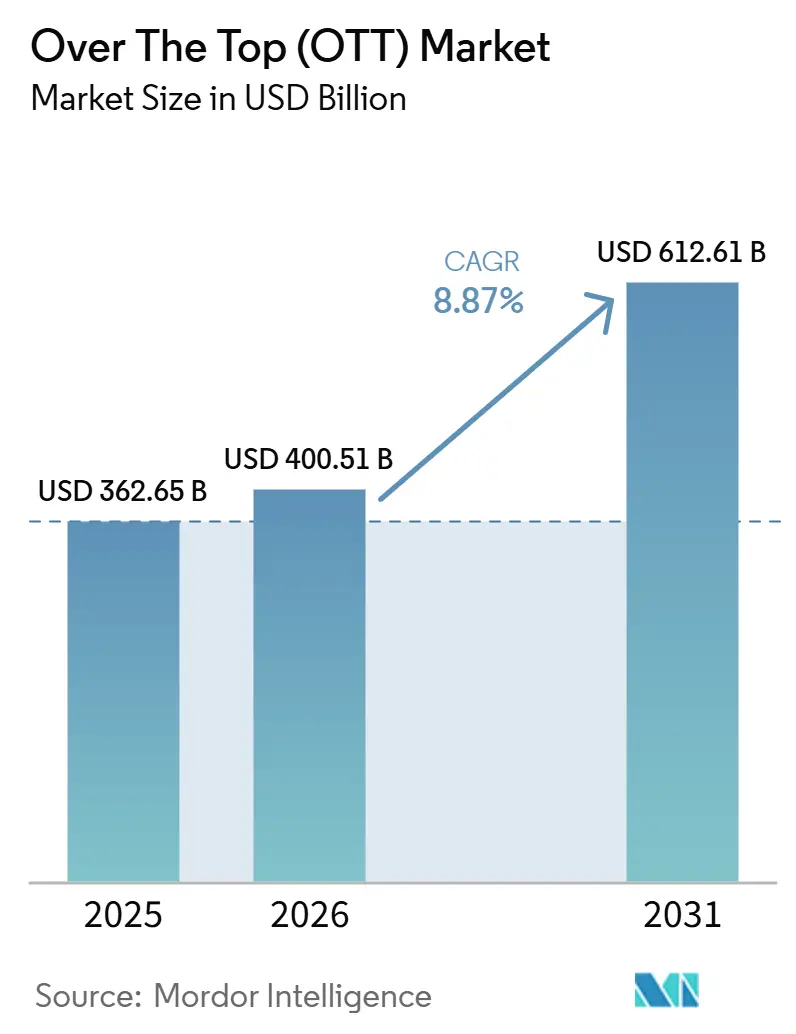

| Market Size (2026) | USD 400.51 Billion |

| Market Size (2031) | USD 612.61 Billion |

| Growth Rate (2026 - 2031) | 8.87% CAGR |

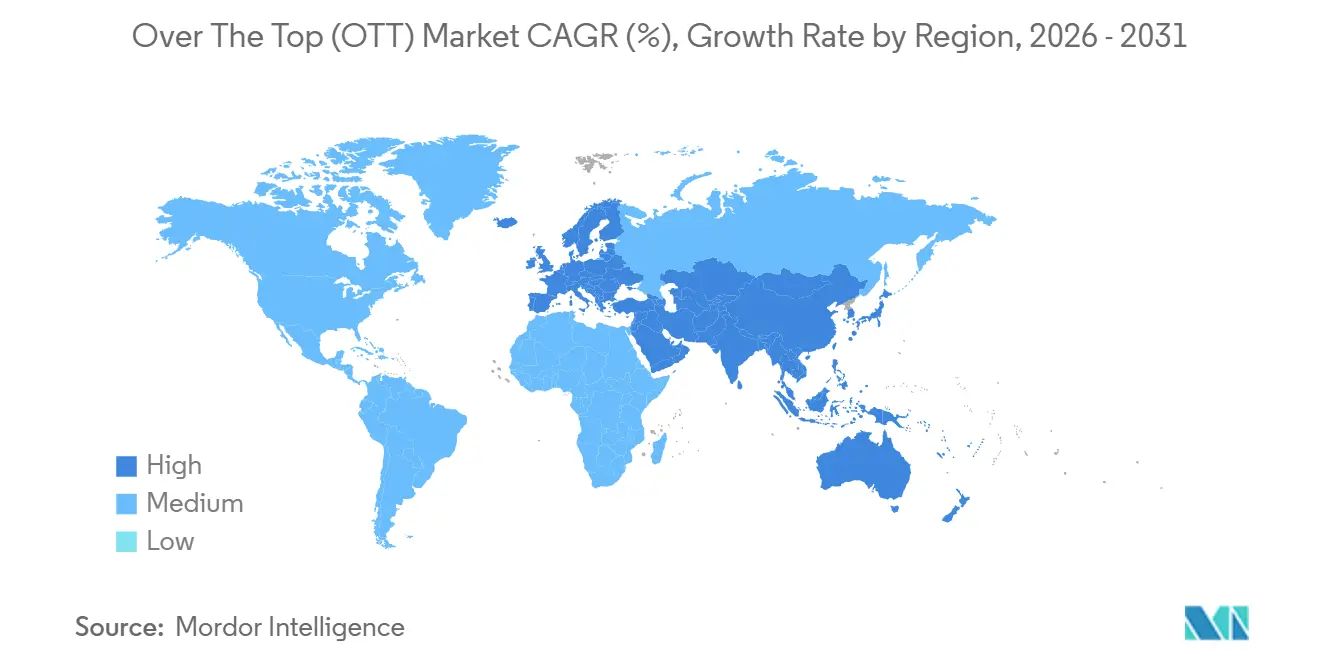

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Over The Top (OTT) Market Analysis by Mordor Intelligence

The over the top (OTT) market size is projected to expand from USD 362.65 billion in 2025 and USD 400.51 billion in 2026 to USD 612.61 billion by 2031, registering a CAGR of 8.87% between 2026 to 2031. The over the top (OTT) market is being shaped by wider telecom bundles, connected TV advertising, and a larger supply of local-language programming. Streaming had reached 47.5% of U.S. television viewing in December 2025, while cable accounted for 20.2%, which indicated an ongoing shift in viewing time toward on-demand services. Advertising is becoming a more important revenue source as platforms combine lower-priced subscriptions with paid advertising. Local content rules are also directing commissioning budgets toward domestic production in several countries. The over the top (OTT) market therefore offers room for growth, but platforms need to balance distribution reach, content spending, and revenue per subscriber.

Key Report Takeaways

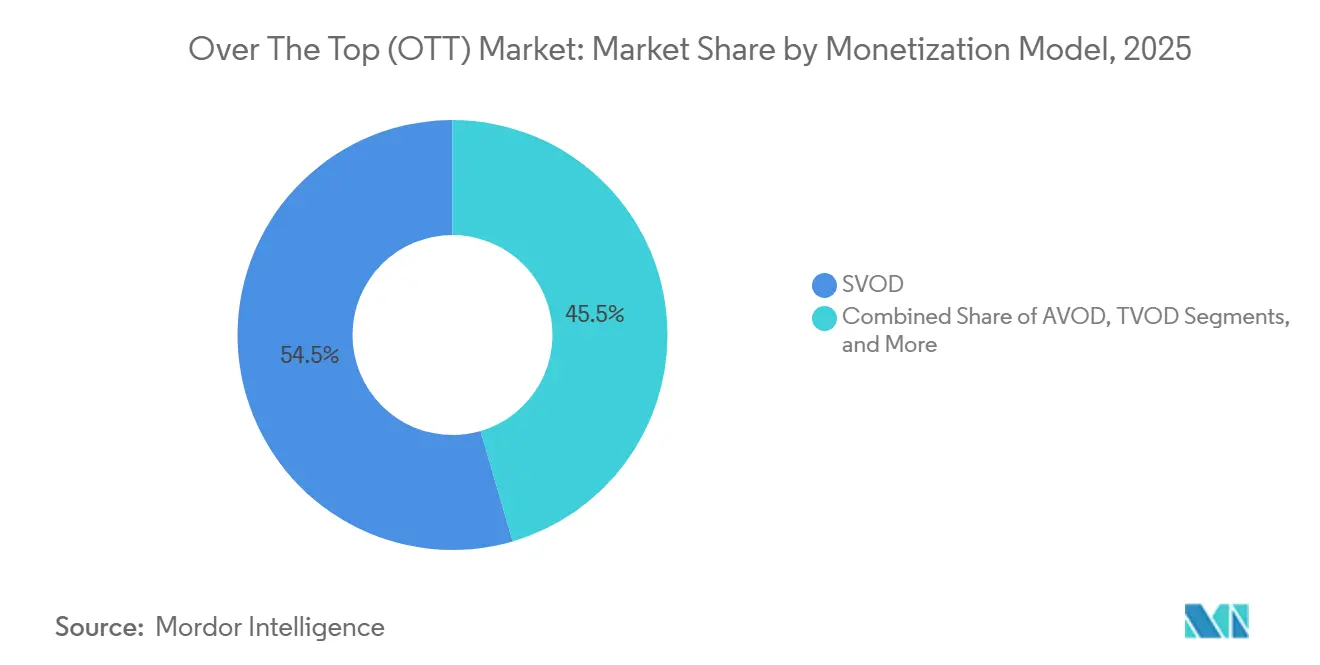

- By monetization model, SVOD held 54.52% of the over the top (OTT) market share in 2025, while hybrid tiers are projected to expand at a 10.54% CAGR through 2031.

- By device type, smart TVs accounted for 51.69% of the over the top (OTT) market share in 2025 and are expected to expand at a 10.21% CAGR through 2031.

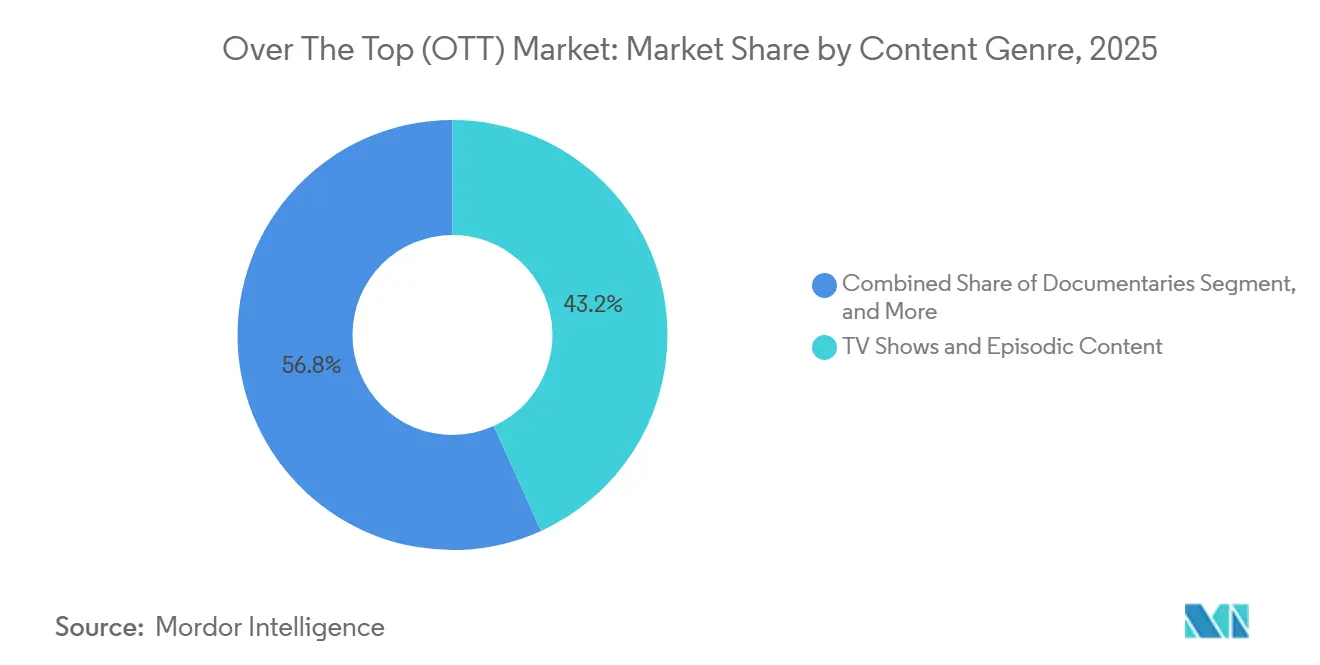

- By content genre, TV shows and episodic content held 43.24% of the over the top (OTT) market in 2025, while documentaries are projected to expand at an 11.24% CAGR through 2031.

- By geography, North America held 48.22% of the over the top (OTT) market in 2025, while Asia-Pacific is expected to expand at an 11.17% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Over The Top (OTT) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bundled Telco and OTT Partnerships | +1.8% | Global, with concentrated gains in Asia-Pacific, South America, and Middle East | Short term (≤ 2 years) |

| Live Sports Rights Inflation | +1.6% | North America and Europe, spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Connected TV Advertising Shift | +1.5% | North America and Europe, early gains in core Asia-Pacific markets | Short term (≤ 2 years) |

| Government Domestic Content Quotas | +1.2% | European Union, Australia, Canada, with global spill-over | Medium term (2–4 years) |

| Cloud-Based Content Delivery and AI Personalization | +1.0% | Global, strongest in North America, Europe, and core Asia-Pacific | Short term (≤ 2 years) |

| Hybrid Monetization and Ad Tier Expansion | +0.8% | Global, with early gains in North America and South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Bundled Telco and OTT Partnerships

Telecom bundles have become an important distribution route for the over the top (OTT) market, especially where customers are price sensitive. The arrangement can reduce cancellation rates for operators and lower subscriber acquisition costs for streaming platforms. Reliance Jio introduced an INR 200 (USD 2.10) OTT Pass in May 2026 that bundled 15 platforms, 1,000 live TV channels, and unlimited 5G access for 28 days. This package placed streaming services within a broader mobile offer rather than treating them as separate purchases. The model can broaden reach in high-volume markets, but it also places pressure on platforms to accept lower revenue per user. It has encouraged providers to use advertising and hybrid plans to recover revenue that a standalone subscription may not deliver.

Live Sports Rights Inflation

Streaming platforms are expected to spend USD 14.2 billion on sports rights in 2026, compared with USD 13.2 billion in 2025. Amazon Prime Video was expected to spend USD 3.8 billion, supported by the first full season of its NBA agreement. Live sports can attract viewers at a fixed time and create valuable advertising inventory for the over the top (OTT) market. The same rights can also support subscriber acquisition in mature markets where general entertainment subscriptions have slowed. However, rising rights fees create a difficult cost position for platforms that lack other large revenue streams. The OTT market is therefore likely to reward services that can use sports programming across subscriptions, advertising, and wider commercial ecosystems.

Connected TV Advertising Shift

U.S. digital video advertising is projected to reach USD 81.9 billion in 2026, up from USD 73.6 billion in 2025. Connected TV, social video, and online video are included in this category. The Interactive Advertising Bureau reported that 61% of U.S. ad buyers considered CTV and OTT inventory a must-buy format in 2026.[1]Interactive Advertising Bureau, “2026 IAB Digital Video Ad Spend and Strategy Report Part One,” Interactive Advertising Bureau, iab.com Platforms with authenticated users can use first-party viewing data to support more targeted advertising. This capability strengthens the position of scaled services that can offer advertisers both reach and measurement. The over the top (OTT) market is also moving toward shoppable formats and attribution tools that can make streaming inventory more useful to performance-focused advertisers.

Government Domestic Content Quotas

Domestic content rules are directing more commissioning money toward local production markets. Australia introduced a requirement that applies to large subscription video services with at least 1 million Australian subscribers from January 2026.[2] Australian Office for the Arts, “New Australian Content Laws for Streaming Services,” Australian Government, arts.gov.au Eligible platforms must invest 10% of total program expenditure or 7.5% of Australian revenue in new local content. These requirements cover drama, documentary, children’s, and arts programming. Canada also formalized a 15% domestic-programming contribution requirement for online streaming services in 2026. The over the top (OTT) market may gain deeper local content libraries through these policies, although compliance costs can weigh more heavily on smaller entrants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Content Acquisition and Production Costs | -1.4% | Global, with pronounced pressure in North America | Medium term (2–4 years) |

| High Churn and Subscription Stacking | -1.1% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Bandwidth Constraints and Playback Quality Gaps | -0.7% | Emerging markets in Asia-Pacific, Africa, and South America | Medium term (2–4 years) |

| Regulatory, Privacy, and Content Compliance Complexity | -0.5% | Global, with concentrated compliance cost in European Union and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Content Acquisition and Production Costs

Content spending remains the largest cost pressure in the over the top (OTT) market. Netflix added USD 17.1 billion in content assets in fiscal 2025 and reported USD 24.0 billion in content obligations.[3]Netflix, Inc., “Annual Report on Form 10-K for the Fiscal Year Ended December 31, 2025,” U.S. Securities and Exchange Commission, sec.gov Its 2025 revenue was USD 45.18 billion, which shows the scale of content investment needed to maintain a global service. Sports rights add a further cost burden because premium competitions require large multiyear commitments. In India, OTT content spending fell to INR 21.8 billion (USD 228 million) in 2025 from INR 26.7 billion (USD 279 million) in 2024 as platforms became more selective with mid-budget commissions. The over the top (OTT) market is consequently encouraging licensing, co-productions, and shared production arrangements where providers can limit risk without losing access to relevant content.

High Churn and Subscription Stacking

High churn remains a restraint because households can move between services when a desired program becomes available. Monthly churn ranged from 2-3% for premium platforms with large libraries to 5-10% or more for mid-tier and single-genre services in early 2025. Higher ad-free plan prices have made price a leading reason for cancellation. U.S. households maintained an average of 5.8 streaming subscriptions, which supports rotational viewing and raises retention costs for every provider. Ad-supported plans can bring in new customers, but they also establish lower price expectations. The over the top (OTT) market is responding through telecom bundles and weekly release schedules, although both approaches involve trade-offs in revenue sharing or content planning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Monetization Model: Hybrid Tiers Reshape Subscription Economics

SVOD held 54.52% of the over the top (OTT) market by monetization model in 2025. Subscription revenue still anchors the largest platforms because it provides recurring income and a direct customer relationship. Hybrid services are projected to record the fastest growth at a 10.54% CAGR from 2026 to 2031. These plans combine a subscription charge with advertising revenue from the same viewer. AVOD is the second-largest monetization model and has particular relevance in price-sensitive markets across Asia-Pacific and South America.

TVOD and freemium services remain smaller parts of the OTT market, but they retain a clear role in selected use cases. TVOD is relevant for sports and live events where viewers may accept a transaction fee for time-sensitive access. Freemium services can introduce consumers to a platform before a paid conversion. The shift away from entirely ad-free subscriptions reflects the need to diversify revenue as mature services face slower subscriber additions. Netflix reported that advertising revenue exceeded USD 1.5 billion in 2025 and forecast that it would approach USD 3 billion in 2026. The OTT industry is therefore using hybrid plans as an enduring commercial model rather than a temporary promotional option.

By Device Types: Smart TVs Anchor Long-Form Viewing

Smart TVs accounted for 51.69% of the over the top (OTT) market by device type in 2025 and are projected to expand at a 10.21% CAGR through 2031. Their leadership reflects a growing installed base of internet-connected televisions and a return to larger screens for long-form viewing. Connected television also supports shared viewing in the household. Smartphones and tablets are the second-largest device group. They remain especially important in Asia-Pacific, where mobile-first access and younger audiences support high streaming engagement.

Laptops and desktops have a declining role as viewing patterns normalize after the earlier increase in home and workplace viewing. They remain relevant in locations with lower smart TV ownership. Other device types, including streaming sticks, gaming consoles, and set-top boxes, serve important distribution roles in Japan and South Korea. Smart TV viewing improves advertising value because a large screen and household co-viewing can support stronger engagement. In 2026, 61% of U.S. ad buyers considered CTV and OTT inventory essential, according to the Interactive Advertising Bureau. Canal+ also entered a multiyear arrangement with Google Cloud in June 2026 to improve content discovery and personalization across its app in European and African markets.

By Content Genre: Documentaries Support Ad-Supported Libraries

TV shows and episodic content held 43.24% of the OTT market by genre in 2025. Serial programs can support repeat viewing and sustained engagement through their release cadence and continuing storylines. Documentaries are projected to record the highest genre growth at an 11.24% CAGR from 2026 to 2031. Their lower production cost per hour and replay value support large content libraries. These attributes also make documentaries useful for hybrid and AVOD services that need programming at varied price points.

Movies and films form the second-largest genre category and can support acquisition campaigns and platform visibility. Their value to the OTT market depends increasingly on the period between theatrical release and streaming availability. In India’s Hindi-language film segment, the window for mid-budget films had fallen to 35-45 days in 2025. Documentary programming has gained formal investment support as providers seek multiple revenue windows from the same catalog. Ionic Studios made an equity investment in Documentary+ in June 2026 and became the publisher of record for its ad-supported operations. The OTT industry can use documentary catalogs across SVOD, AVOD, and free ad-supported streaming television services, which gives factual programming a broader commercial role.

Geography Analysis

North America held 48.22% of the over the top market in 2025. High household broadband availability, established subscription video use, and mature advertising systems supported this position. Netflix, Disney, and Amazon collectively accounted for 65% of U.S. subscription VOD viewership in December 2025. The region faces a saturation challenge because new subscribers often come from competitors or from reactivated former subscribers. Canada’s 15% domestic-programming contribution requirement, formalized in 2026, is changing the commissioning choices of global platforms.

Asia-Pacific is projected to be the fastest-growing OTT geography at an 11.17% CAGR from 2026 to 2031. China accounted for 46% of the region’s online video revenue in 2025, followed by Japan at 17% and Australia at 10%. India is expected to become the world’s largest SVOD subscription market by 2030 with 358 million individual subscriptions. Local platforms held 84% of SVOD subscriptions across Asia-Pacific, which limits the revenue share available to international services even as the over the top (OTT) expands.

Europe is the second-largest geographic segment in the over the top market and is centered on Germany, the United Kingdom, and France. European services operate under a 30% European content availability requirement. Germany is expected to apply an 8% local-revenue investment requirement from January 2027. South America is an emerging region where Brazil anchors adoption and telecom bundles are extending access beyond major cities. The Middle East has premium revenue centers in Saudi Arabia and the United Arab Emirates, while Africa remains centered on mobile access in South Africa, Egypt, and Nigeria.

Regulatory Landscape

In the European Union, the Digital Services Act (DSA) continues to shape compliance requirements for designated Very Large Online Platforms, with the European Commission moving toward recurring audit cycles and mandatory systemic-risk assessments through 2025-2026. These rules deepen accountability around transparency, data access, and user safety by design for ad-supported and recommendation-driven services.

Value Chain Analysis

The OTT value chain begins with content origination (studios, leagues, creators, and rights holders), then moves through financing and production, post-production and localization, packaging and rights management, and finally distribution and monetization across apps and connected-TV platforms. Distribution is increasingly cloud-mediated, relying on hyperscale compute and storage, encoding and transcoding stacks, DRM and entitlement systems, and multi-CDN delivery to handle peak demand, latency, and ISP congestion.

Competitive Landscape

The over the top market has a consolidated top tier and a more fragmented group of regional and specialist providers. Netflix held 32.5% of U.S. subscription VOD viewership in December 2025, while Disney held 16.7% and Amazon held 15.3%. The three services together accounted for 65% of U.S. subscription VOD viewers. Their scale provides broad viewing reach and large advertising inventory. Netflix generated USD 45.18 billion in revenue in fiscal 2025 and reported a 29.5% operating margin.

Competition in the over the top market is increasingly based on aggregation, licensing, and advertising capability rather than exclusive originals alone. Amazon Channels, YouTube Primetime Channels, and Comcast Xfinity StreamSaver illustrate how distributors can combine several subscription services in one customer relationship. These arrangements can make distribution access as important as ownership of a single catalog. DAZN’s acquisition of Foxtel showed how a sports-oriented provider can pursue added scale and a wider content base. Platforms with authenticated subscriber data can use their own measurement tools to offer advertisers more precise attribution than linear television.

Several strategic moves illustrate this shift. Paramount agreed in February 2026 to acquire Warner Bros. Discovery in a transaction valued at USD 81 billion in equity value and USD 110 billion in enterprise value, with plans for more than USD 6 billion in synergies. In July 2026, NBCUniversal and YouTube announced a streaming bundle that paired Peacock with YouTube Premium. STARZ and Crunchyroll also introduced a U.S. bundle on Prime Video in July 2026. These actions show that the over the top market is rewarding broader distribution, shared customer access, and advertising technology alongside original programming.

Over The Top (OTT) Industry Leaders

Netflix Inc.

Google LLC

The Walt Disney Company

Tencent Holdings Limited

Prime Video (Amazon.com, Inc.)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Connected-TV advertising and FAST channel expansion create specific opportunities as advertiser budgets shift toward CTV. US CTV ad spend reached USD 30 billion in 2024, and Roku reported 18 percent year-over-year platform revenue growth in Q3 2025. Telcos and pay-TV operators are also packaging FAST offerings, including Vodafone Germany's GigaTV FAST initiative with Amagi in August 2025.

Recent Industry Developments

- July 2026: Netflix announced a strategic multi-year collaboration with Mythical Entertainment to co-produce and co-distribute a slate of creator-led IP across Netflix, YouTube, and partner platforms. The collaboration expands creator-led programming within a major SVOD app while preserving creator primary distribution rights.

- December 2025: Amazon Prime Video introduced an ad-supported default tier across the United States, United Kingdom, Germany, and Canada, and offered a USD 2.99 add-on to remove ads. The update broadens reach and adds more monetization options for both advertisers and subscribers.

- September 2024: Apple TV+ expanded its live-sports footprint through a long-term Major League Soccer agreement, extending streaming windows and adding exclusive match content. The deal illustrates how OTT platforms use sports rights to attract and retain subscribers in mature SVOD markets.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the over the top (OTT) market is counted as consumer revenue earned from internet-delivered video, audio, and consumer VoIP services that bypass traditional broadcast or telecom delivery, across subscription, advertising, transactional, and hybrid models.

Scope exclusions: Hardware sales for streaming devices, traditional pay-TV subscriptions, and enterprise communication suites are excluded from the market totals.

Segmentation Overview

- By Monetization Model

- SVOD

- AVOD

- TVOD

- Hybrid

- Freemium

- By Device Types

- Smartphones and Tablets

- Smart TVs

- Laptops and Desktops

- Other Device Types

- By Content Genre

- Movies and Films

- TV Shows and Episodic Content

- Documentaries

- Other Content Genres

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Qatar

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the market boundary and to build the starting demand and pricing picture that later gets tested with interviews. We mostly lean on public datasets and official publications that can be checked by readers, such as ITU connectivity indicators, World Bank macro series, OECD telecom and digital economy releases, national telecom regulators, and UNESCO or WIPO references for media and IP context.

We also review company filings and investor decks, industry association pages, and reported pricing or plan changes in reputable press to understand monetization shifts like ad-supported tiers and bundled offers. For specific company financials, patent activity, and news and financial context, we selectively use paid database subscriptions that help validate timelines and reduce the risk of missing large revenue moves. These examples are not exhaustive, and many other public sources were also used for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with OTT ecosystem participants, including platform operators, telecom and broadband stakeholders, content owners, ad buyers, and enabling technology and service providers. Because this is a global market, feedback was gathered across APAC, EMEA, and the Americas, so adoption patterns, pricing, and ad load assumptions could be validated and then applied consistently across regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 13% | APAC: 38% |

| Mid tier: 49% | Functional/Unit leaders: 40% | EMEA: 35% |

| Smaller Players: 15% | Managers: 47% | Americas: 27% |

Market-Sizing & Forecasting

Market sizing starts with a top-down build where population online, broadband and 4G-5G coverage, and device readiness are used to reconstruct the addressable streaming and communication user pool by region, which is then converted to revenue through paid penetration and ad-supported monetization. To keep the totals realistic, we corroborate outputs with selective bottom-up approximations, such as sampled subscription price points by country, ad-supported ARPU checks, and roll-ups of disclosed digital media and OTT-related revenue where it is reported clearly.

A few inputs that materially shape the model include internet and smartphone penetration, paid subscriber trends, average monthly subscription pricing, ad load and CPM direction for AVOD and FAST, and currency timing for large markets where USD translation can swing year-to-year comparability. When data gaps show up, smaller markets are grouped using proxy indicators like GDP per capita and connectivity, and then later adjusted using interview feedback on local pricing and payment behavior. Forecasts are produced using multivariate regression, with drivers like connectivity growth, ARPU progression, and ad market outlook being stress-tested through scenario analysis for aggressive and conservative cases.

Data Validation & Update Cycle

Outputs are checked against independent signals, such as regional broadband additions, major plan price moves, and reported digital advertising growth, so the market does not drift away from observable demand. Any sharp variances are re-opened, assumptions are re-tested, and follow-up calls are triggered when a key geography or business model shows a break in trend.

Before sign-off, the model goes through multi-step analyst review so definitions, currency treatment, and year alignment remain consistent across regions. The report is refreshed annually, and interim updates are made when material events occur, after which a final pre-delivery pass is completed to reflect the latest available information.

Mordor Intelligence's Over the Top Market Size Measured Against Other Published Estimates

Published OTT market values rarely match because firms do not count the same revenue streams, and they often mix different years, currency timing, and add-on categories. Differences also show up when one estimate is built from user and ARPU logic, while another leans more on broad digital media totals.

The table shows a wide spread mainly because some external figures pull in adjacent categories like streaming hardware, enterprise communications, or very broad definitions that can inflate the end number. Another common driver is the forecast stance, where aggressive ad growth and rapid ARPU expansion are assumed without enough checks against price points and paid penetration by region.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 347.57 B (2025) | |

| Industry Research Publisher A | USD 707.60 B (2025) | Uses a wider OTT definition that includes many solution and service buckets across industries and content types, which can blend consumer OTT revenue with broader platform and service spending. |

| Global Research Firm B | USD 364.57 B (2025) | Covers OTT devices and services together, so hardware and device-linked revenues can be included alongside streaming services, which lifts totals versus a services-only view. |

The table points to scope as the biggest gap, and in Mordor Intelligence's model the number is restricted to consumer OTT service revenue across video, audio, and consumer VoIP, with streaming device hardware and pay-TV excluded. With that cleaner boundary, the result stays traceable to practical drivers like paid penetration, price points, and ad monetization, which makes the sizing steps easier to repeat and validate year after year.

Key Questions Answered in the Report

What is the size of the global OTT market?

The global OTT market is projected at USD 400.51 billion in 2026 and USD 612.61 billion by 2031, registering a CAGR of 8.87% during 2026-2031. Growth is driven by bundle distribution, advertising adoption, local content availability, and the ongoing shift from traditional linear TV to streaming. Subscription services, ad-supported models, connected TV consumption, and telecom partnerships continue to strengthen the OTT ecosystem.

Which monetization model leads OTT services?

SVOD (Subscription Video on Demand) led the market with a 54.52% share in 2025. However, hybrid monetization models are expected to grow the fastest, at a 10.54% CAGR through 2031. Hybrid plans combine subscription and advertising revenues, while AVOD caters to cost-conscious viewers and TVOD remains relevant for live events and sports.

Why are hybrid streaming plans expanding?

Hybrid streaming plans are expanding because they combine subscription fees and advertising revenue, enabling platforms to diversify income streams while appealing to budget-conscious consumers. These plans also offer lower-cost entry options and support broader telecom bundling strategies.

Which device is most important for OTT viewing?

Smart TVs were the leading device category, accounting for 51.69% of OTT revenue in 2025. The segment is expected to grow at a 10.21% CAGR through 2031, supported by larger-screen viewing experiences, shared household consumption, increased connected TV advertising, and demand for long-form content.

Which region is growing fastest for OTT services?

Asia-Pacific is projected to be the fastest-growing region, with an 11.17% CAGR from 2026 to 2031. Growth is fueled by major markets such as India and China. Local platforms account for 84% of regional SVOD subscriptions, highlighting the importance of localized content and distribution partnerships.

What is the main cost challenge for streaming platforms?

Content production and rights acquisition remain the primary cost challenges. For example, Netflix reported USD 17.1 billion in content asset additions in fiscal 2025. Costs related to sports broadcasting rights and original content creation can be especially burdensome for smaller streaming providers with limited revenue diversification.

Page last updated on: