Roadm WSS Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

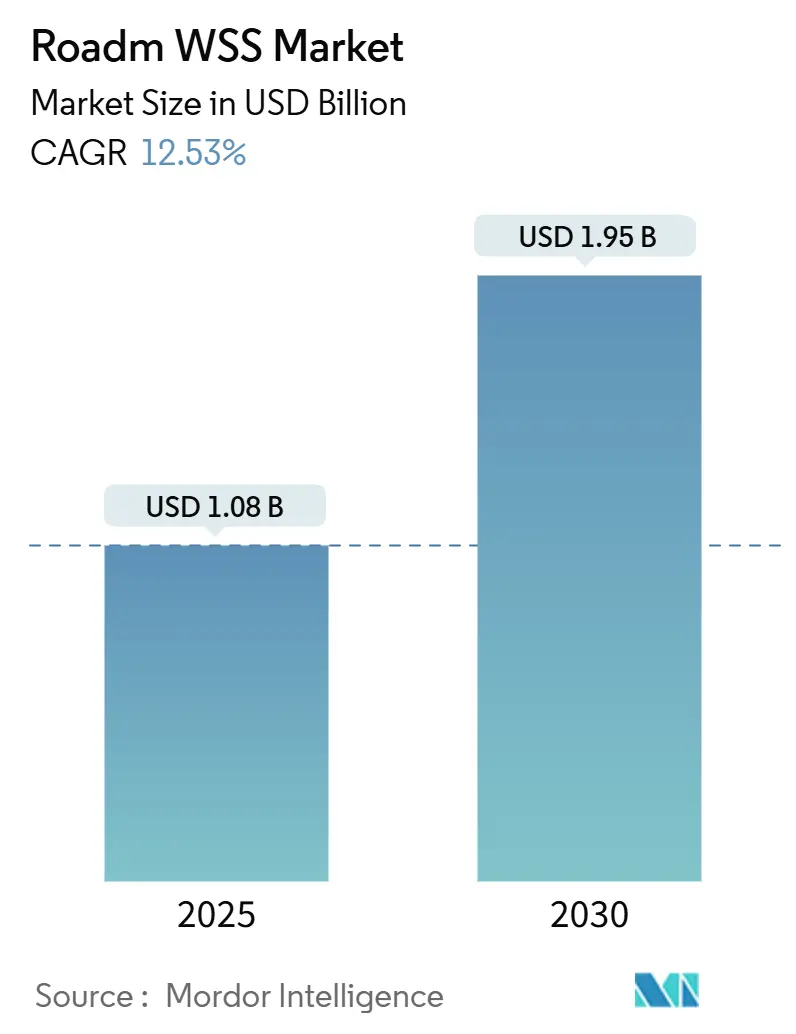

| Market Size (2025) | USD 1.08 Billion |

| Market Size (2030) | USD 1.95 Billion |

| Growth Rate (2025 - 2030) | 12.53% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Roadm WSS Market Analysis by Mordor Intelligence

The Roadm WSS market size stands at USD 1.08 billion in 2025 and is forecast to touch USD 1.95 billion by 2030, reflecting a 12.53% CAGR that outpaces wider optical component growth trends. Ongoing 400 G/800 G coherent upgrades, densifying 5 G mid-haul routes, and the rise of edge-cloud AI workloads are steering carriers toward programmable wavelength-routing architectures that maximize existing fiber assets. Liquid-crystal-on-silicon (LCOS) switching holds pole position thanks to low insertion loss and superior beam-steering accuracy, while flex-grid designs gain momentum as operators pursue granular spectrum control for mixed-rate traffic. Asia-Pacific dominates shipments owing to vertically integrated supply chains and strong domestic demand, whereas North America and Europe accelerate deployments in disaggregated, open optical networks. Although higher upfront capex challenges small operators, falling LCOS costs and automation-driven opex savings continue to strengthen the investment rationale.

Key Report Takeaways

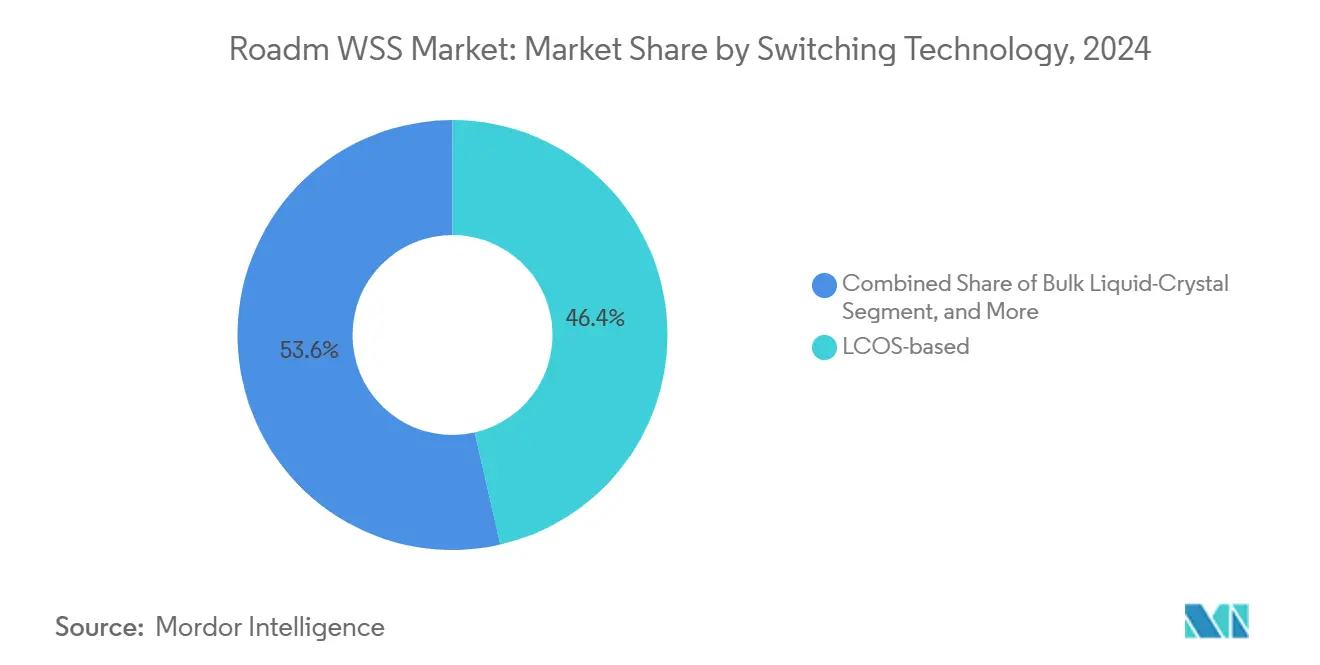

- By switching technology, LCOS captured 46.43% share of the Roadm WSS market in 2024 while hybrid LCOS-MEMS solutions are advancing at an 18.9% CAGR through 2030.

- By channel flexibility, fixed-grid systems held 64.21% share in 2024; flex-grid variants are projected to expand at a 14.23% CAGR to 2030.

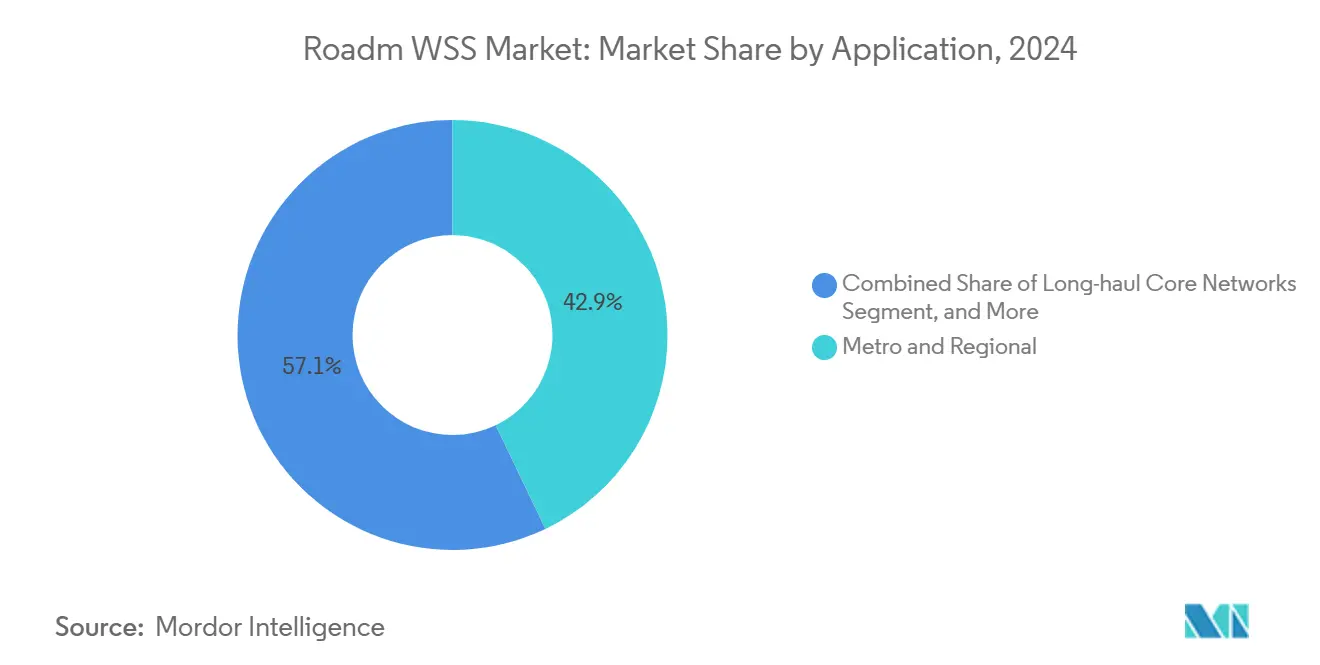

- By application, metro and regional networks led with 42.89% share in 2024, whereas data-center interconnect is forecast to post the fastest 15.6% CAGR during the outlook period.

- By end-user, telecom service providers accounted for 55.93% of the Roadm WSS market share in 2024; cloud and hyperscale operators register the highest 12.97% CAGR through 2030.

- By geography, Asia-Pacific commanded 38.72% revenue in 2024 and is advancing at a 12.81% CAGR to 2030 on the back of China’s 5 G roll-outs and Japan’s photonics research leadership.

Global Roadm WSS Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in 400G/800G coherent upgrades | +3.2% | Global, with North America and Asia-Pacific leading | Medium term (2-4 years) |

| 5G mid-haul and backhaul densification | +2.8% | Asia-Pacific core, spill-over to Europe and North America | Short term (≤ 2 years) |

| Cloud-scale DCI build-outs | +2.1% | Global, concentrated in hyperscale regions | Medium term (2-4 years) |

| Open optical networking initiatives | +1.7% | North America and Europe early adoption | Long term (≥ 4 years) |

| Edge-cloud AI traffic localization | +1.9% | Global, with emphasis on developed markets | Medium term (2-4 years) |

| Sub-sea cable disaggregation trend | +0.8% | Global submarine routes, Asia-Pacific and transatlantic focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in 400 G/800 G Coherent Upgrades

Global carriers are shifting from 100 G to 400 G and 800 G line rates, creating a pronounced up-cycle for LCOS-based WSS modules that maintain signal integrity across wider channel bandwidths. NTT recently exceeded 100 Tbit/s over 800 km using ultra-long-wavelength band conversion, a milestone that demands multi-degree wavelength switching to exploit C + L bands efficiently. [1]NTT Corporation, “World’s First Long-Haul Optical Inline-Amplified Transmission,” group.ntt Australian operator Telstra partnered with Ciena to deploy 400 G across its backbone, illustrating how software-defined WSS units replace manual patching and accelerate service turn-up. Price convergence between next-gen coherent optics and legacy 100 G transceivers further strengthens the business case. As a result, the Roadm WSS market gains a virtuous loop: higher traffic density drives WSS upgrades, which in turn unlock additional capacity without fresh fiber builds.

5 G Mid-haul and Backhaul Densification

Distributed RAN topologies introduce bandwidth bursts between centralized and distributed units that static mux-demux pairs cannot satisfy. Ericsson’s transport solutions show live bandwidth re-allocation across cell sites through colorless-directionless WSS shelves, removing truck rolls and enabling elastic RAN slices. [2]Ericsson, “Optical Fronthaul Solutions,” ericsson.com Densification also fuels mesh-based metro architectures where multi-degree ROADMs improve path diversity for mission-critical services. Operators in Asia-Pacific, particularly China Mobile and NTT DOCOMO, deploy flex-grid WSS to squeeze diverse 5 G, FTTH, and enterprise services onto shared fiber. Short-term growth is accelerated by aggressive spectrum fees that force operators to extract more value per fiber pair.

Cloud-scale DCI Build-outs

Hyperscalers are linking distributed compute clusters with terabit-class pipes to feed AI model training. Nvidia’s 1.6 T port switch roadmap pairs co-packaged optics with programmable WSS nodes that steer wavelengths based on workload demand. [3]SPIE Europe, “Nvidia Reveals Plan to Scale AI Factories,” optics.org Alibaba and Meta embrace open line systems where best-of-breed WSS blades interoperate through OpenConfig APIs to automate provisioning. Demand for 75 GHz and 150 GHz super-channels fuels flex-grid adoption, while software hooks allow network planners to repurpose spectrum during nightly troughs for replication traffic. Consequently, the Roadm WSS market benefits from continuous hyperscale capex even when broader telco spending cycles soften.

Open Optical Networking Initiatives

Operators are unbundling line systems from terminals to diversify suppliers and compress costs. AT&T’s open ROADM program and NTT’s Open APN proof-of-concept confirm that LCOS-based WSS modules from multiple vendors can occupy the same shelf with uniform management semantics. This policy encourages niche suppliers to innovate on insertion loss, port count, and response time while leveraging common control planes. Over the long term the movement reduces vendor lock-in, widens addressable demand, and intensifies competition, thereby lowering average selling prices and stimulating uptake among cost-sensitive operators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial capex vs. fixed mux/demux | -1.8% | Global, particularly affecting smaller operators | Short term (≤ 2 years) |

| Complexity in multi-vendor interoperability | -1.2% | North America and Europe early adoption markets | Medium term (2-4 years) |

| Polarisation-related performance drift | -0.9% | Global, affecting high-capacity deployments | Long term (≥ 4 years) |

| Supply-chain concentration risk in LCOS die | -1.1% | Global, with Asia-Pacific manufacturing concentration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Capex vs Fixed Mux/Demux

A fully configured multi-degree ROADM node with twin WSS blades can cost three to five times more than a passive mux-demux chassis of similar port count. The premium deters budget-constrained regional carriers even when life-cycle opex models favor automation. Vendors counter the hurdle with pay-as-you-grow slot cards and subscription-style software licensing. Developed markets, where field labor rates exceed USD 100 per hour, realize quicker payback than regions with low labor costs. As LCOS fabrication volumes rise and port densities climb above 1×32, hardware cost curves are starting to intersect those of legacy passive gear, moderating the restraint’s drag on the Roadm WSS market.

Complexity in Multi-vendor Interoperability

Disaggregated optical stacks replace turnkey systems with components from several suppliers, multiplying integration touchpoints. Field trials reveal compatibility gaps between WSS embedded firmware and third-party optical line systems that prolong acceptance tests. Early adopters such as Deutsche Telekom mitigate risk through exhaustive lab certification and open-source YANG models, but smaller operators lack comparable bench resources. Industry forums continue to refine interoperability specs, yet practical deployments often depend on bilateral collaboration between vendor engineering teams. While the learning curve flattens over time, integration complexity remains a headwind for widespread adoption in the next two to three years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Switching Technology: LCOS precision sustains leadership

LCOS-based designs led the Roadm WSS market size with a 46.43% share in 2024 and are projected to retain dominance through the forecast, underpinned by sub-1 dB insertion loss and <10 ms switching speeds that meet metro latency budgets. MEMS variants trail in high-port-count builds yet maintain relevance for cost-sensitive links. Hybrid LCOS-MEMS architectures emerge as compromise platforms that pair LCOS beam control with MEMS reliability, expanding addressable applications in compact access nodes.

Substitution risk remains contained because silicon photonics-based planar-lightwave circuits still struggle to match LCOS performance on polarization insensitivity and spectrum tilt control. Component specialists such as Santec and Coherent scale port counts beyond 1×48 while maintaining 25 GHz guard-band flatness, further locking in LCOS advantages. Consequently, the Roadm WSS market share of LCOS solutions consolidates among vendors with in-house liquid-crystal alignment and proprietary driver ICs.

By Channel Flexibility: flex-grid captures momentum

Fixed-grid gear accounted for 64.21% of the Roadm WSS market size in 2024 due to its established footprint in legacy DWDM backbones. Nevertheless, flex-grid nodes are expanding at a 14.23% CAGR because they support alien wavelengths and 75 GHz super-channels favored by cloud operators. Operators report 35% spectrum utilization gains after switching from fixed 100 GHz spacing to 37.5 GHz flex channels, validating the economic upside.

NeoPhotonics showcased 400 ZR over 75 GHz channels, proving that flex-grid solutions maintain performance parity with wider fixed channels while doubling fiber throughput. As more 1.6 T transceivers enter volume production, demand for flexible spectrum slices will accelerate, lifting flex-grid’s incremental Roadm WSS market share during the out-years.

By Application: metro networks remain the workhorse

Metro and regional rings consumed 42.89% of the Roadm WSS market size in 2024, reflecting dense urban footprints and frequent service churn. Multi-service operators exploit colorless-directionless-contentionless switching to migrate T-DM, enterprise, and mobile traffic without disruptive re-cabling.

Data-center interconnect, while smaller today, is the fastest-growing slice thanks to AI cluster traffic that requires predictable low latency and dynamic bandwidth pooling. Coherent’s 800 G QSFP-DD line card specifically targets leaf-spine fabrics where WSS modules optimize redundant paths. Submarine upgrades incorporate tri-degree ROADMs that minimize in-line amplifier counts, further extending use cases.

By End-User: telcos hold majority yet hyperscalers surge

Traditional telecom service providers commanded 55.93% of the Roadm WSS market share in 2024 because they operate nationwide fiber estates that need automated spectrum engineering. Cable MSOs and government networks absorb modest volumes centered on secure, hardened equipment.

Hyperscale operators, however, register the swiftest 12.97% CAGR as they interconnect regional campuses at terabit rates. Molex anticipates double-digit unit growth of high-speed optics inside cloud data centers, implying parallel lifts for disaggregated WSS nodes that sit at peering edges. The shift toward AI-ready fabrics and open control APIs further tilts new investment toward hyperscaler-friendly WSS designs.

Geography Analysis

Asia-Pacific generated 38.72% of 2024 revenue for the Roadm WSS market and posts a 12.81% CAGR through 2030. Regional incumbents China Mobile and NTT DOCOMO expanded backbone capacity with LCOS-equipped ROADMs that deliver colorless add-drop at provincial hubs. Vertically integrated suppliers such as Fujitsu Optical Components and O-Net scale production, shrinking lead times and lowering landed costs. Regional governments promote domestic silicon photonics fabs, shielding supply chains from export controls and ensuring long-term resiliency.

North America is the second-largest contributor, propelled by hyperscaler roll-outs and investment in open line systems. Lumentum’s acquisition of NeoPhotonics for USD 918 million gives the region a consolidated champion with end-to-end LCOS design, driver ASICs, and transceiver portfolios. Multiple ISPs adopt open ROADM standards orchestrated through streaming telemetry, fostering rapid software upgrades. The U.S. CHIPS Act underwrites new photonic fabs that diversify LCOS supply away from a single geography.

Europe favors interoperable frameworks and sustainability benchmarks that promote energy-efficient ROADM nodes. Operators like Orange and Deutsche Telekom pilot lithium-niobate-on-insulator WSS prototypes showing 30% lower insertion loss than equivalent LCOS blades. Policy incentives for multi-vendor ecosystems open doors for medium-size suppliers who tailor products to green-data-center objectives.

Competitive Landscape

The Roadm WSS market is moderately consolidated: the top five suppliers control an estimated 66% of 2024 revenue, yet specialized challengers continue to erode share with niche differentiation. Lumentum scaled LCOS output by 40% post-NeoPhotonics buyout, giving it bargaining heft with hyperscalers. Coherent leverages vertically integrated epi-growth and transceiver assembly to capitalize on AI datacenter optics, landing multi-year agreements with U.S. cloud providers.

Asian vendors Santec, Accelink, and O-Net focus on aggressive pricing and rapid custom variants, supported by domestically sourced driver ICs. European players such as HUBER+SUHNER Cube Optics stand out in ultra-compact passive multiplexing that complements disaggregated WSS deployments. Patent filings shift toward software-defined wavelength orchestration, AI-based impairment prediction, and co-packaged integration rather than legacy mechanical innovations. Industry observers predict incremental consolidation as suppliers seek broader portfolios to serve end-to-end open optical strategies.

Emerging start-ups like NewPhotonics and Eoptolink chase white-space around AI transport fabrics, showcasing 1.6 T pluggable modules and multicore fiber transceivers that couple tightly with next-gen WSS roadmaps. Supply risk around LCOS drive controllers encourages exploration of alternate switch mechanisms such as thin-film lithium niobate and tunable wavelength-selective couplers. Competitive intensity thus remains high despite headline consolidation.

Roadm WSS Industry Leaders

Lumentum Holdings Inc.

Coherent Corp. (incl. II-VI Inc.)

Santec Corporation

Molex LLC

Accelink Technologies Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Mouser began stocking Molex Quasar OptiX field-mount connectors for rapid outdoor fiber termination.

- March 2025: Eoptolink Technology unveiled the first 800 G optical transceiver for multicore fiber at OFC 2025, cutting fiber counts in AI clusters.

- March 2025: Furukawa Electric introduced an S-band concentrated Raman amplifier delivering >30 dB gain over 70 nm to extend spectrum reach.

- February 2025: Molex forecasted accelerating adoption of high-speed optics to improve port density in hyperscale data centers.

Global Roadm WSS Market Report Scope

| MEMS-based |

| LCOS-based |

| Bulk Liquid-Crystal |

| Planar Lightwave Circuit (PLC) |

| Fixed-grid WSS (50/100 GHz) |

| Flex-grid WSS (≤ 12.5 GHz) |

| Long-haul Core Networks |

| Metro and Regional Networks |

| Data-Center Interconnect (DCI) |

| Sub-marine Cable Systems |

| Telecom Service Providers |

| Cloud and Hyperscale Operators |

| Cable MSOs |

| Government and Defense |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Switching Technology | MEMS-based | ||

| LCOS-based | |||

| Bulk Liquid-Crystal | |||

| Planar Lightwave Circuit (PLC) | |||

| By Channel Flexibility | Fixed-grid WSS (50/100 GHz) | ||

| Flex-grid WSS (≤ 12.5 GHz) | |||

| By Application | Long-haul Core Networks | ||

| Metro and Regional Networks | |||

| Data-Center Interconnect (DCI) | |||

| Sub-marine Cable Systems | |||

| By End-User | Telecom Service Providers | ||

| Cloud and Hyperscale Operators | |||

| Cable MSOs | |||

| Government and Defense | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the Roadm WSS component market?

The market is valued at USD 1.08 billion in 2025.

How fast is the Roadm WSS market expected to grow?

It is forecast to expand at a 12.53% CAGR between 2025 and 2030.

Which switching technology leads global shipments?

LCOS-based WSS modules held 46.43% share in 2024 due to low insertion loss and high beam-steering accuracy.

Why are flex-grid Roadm's gaining traction?

Flex-grid designs let operators squeeze varied-rate services into narrower spectrum slices, boosting fiber utilization and supporting 400 G/800 G coherent links.

Which region dominates revenue?

Asia-Pacific leads with 38.72% share, propelled by 5 G builds and vertically integrated photonics supply chains.

Who are the key players shaping the competitive landscape?

Lumentum, Coherent, Santec, Accelink, and O-Net headline the market, with start-ups like NewPhotonics and Eoptolink introducing disruptive components.

Page last updated on: